Consensus community valuation

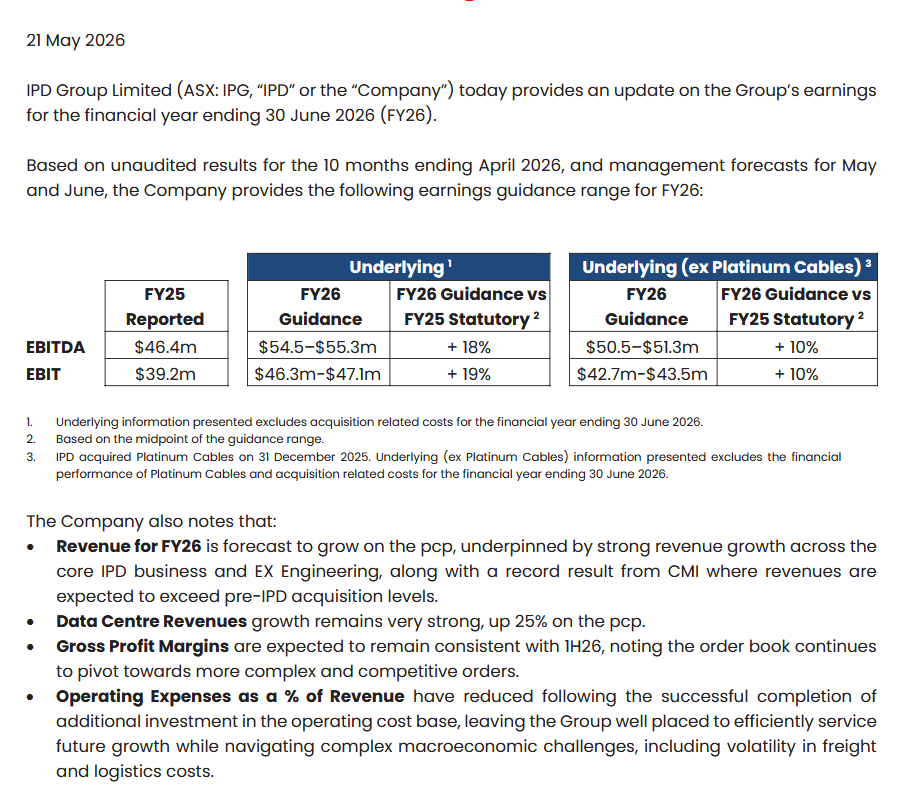

IPD Group put out what looks like solid guidance

But the news sent the shares down 12% from around $6 to $560.

I'll leave the others to decide whether this fall was justified.. Results below.

[held]

Electrical Infrastructure Group IPD published a solid FY26 1H print yesterday beating guidance and the market liked it, up 1.5% on quite a red ASX day.

Highlights and details of interest were as follows:

- Underlying EBIT was up 7.4% on the PCP and beat their own $21.1m-$21.6m guidance coming in at $21.7m. (Underlying results excluded $440k-ish of purchase expenses for new bolt-on business Platinum cables)

- Gross Revenues continue to surge (+8.9% pcp), however this is slightly offset by declining gross margins, as they win bigger data centre jobs that are becoming more cost competitive. Gross Margins were down -1.9% on the pcp, but up 0.2% on the previous half.

- Data Centre income continues to surge up 16% on the PCP, with one late project delivery the only thing stopping them from delivering +25% for the half

- Nice to see operating expenses as a % of revenue falling from 22.1% to 20.2%, although this still wasn't enough to deliver a positive operating leverage movement at the EBIT level given the bigger fall in gross margins.

- Addelec the EV charging installation arm doesn't appear to be going particularly well, with revenues unchanged on the PCP and continued delays on the Kingsgrove bus depot project, but it's hard to see the full picture as they don't break out results by business unfortunately.

- Something @Shapeshifter picked up on 6 months ago is that the services division remains a problem. Revenue was down 9% on the pcp and it's gone from $424k of EBITDA to -$566k! Although I suppose this is better than the -$1.8m last half, but overall, what is this division doing?

For their market outlook IPD again refused to include an order book size, going instead with the following statement - "The Company enters the second half with a healthy order book and a well qualified opportunity pipeline, both of which provide confidence in the sustainability of revenue and earnings growth."

One thing I did like from the call yesterday was that new purchase Platinum Cables (acquisition was finalised on 31 December) is seeing a strong start to 2026 and they are confident that it will be immediately accretive at the margins level to the group.

Overall summary is that IPD seems relatively well placed to keep riding the twin waves of increased data centre and mining demand, despite continued mild concerns about gross margins and management. Australian PCI construction index measures continue to point in the right direction which would hopefully imply that IPD can grow top line revenue at a strong rate.

26-Nov-2025

Valuation $4.20 ($3.20 - $$5.20)

Assumptions

Quick update following the AGM presentation and 1H FY26 guidance, just adjusting P/E scenarios to 12/14/16, and nudging down Revenue CAGR scenarios and narrowing the range to 6.0%/6.75%/7.50%.

See straw for discussion.

26-Aug-2025

Valuation $4.75 ($3.60 - $6.00)

Assumptions

Results of my first independent valuation of $IPG, given (mostly) clean FY25 results.

Method: Projection of EPS to FY30 and discounted back at 10% p.a.

Range of scenarios covering the following input variables:

- Revenue growth: 6%, 7%, 8% p.a.

- %GM starting at 34.5% improving progressively to up to 37.5% in FY30

- Expenses growth 5%, 5.5% and 6% p.a.

Other Parameters (Fixed)

- Other Income and Finance Cost, fixed as % of revenue

- Growth of SOI at 0.3% p.a.

- Tax Rate = 30%

Assumed P/Es in FY30

Although $IPG's PEs since IPO have ranged from 12 to 22, the period of elevated PE's was, in my view, unsustainable exuberance with the market failing to value M&A-driven growth correctly. Upper PE's are therefore ignored. PE's for a decent distribution business are assumed to be 14 to 18. Management are yet to earn the right for a higher premium, and this will be reconsidered at each update.

An upside risk is that $IPG PE's and earnings growth could accelerate if it increases exposure to fast growing industry segements (datacentres, EV charging if this accelerates!, electrification).

Other Assumptions

I have assumed no further M&A, which is both an opportunity and a risk, so I've treated it as net neutral. Clearly, this is NOT going to happen.

Graphical Output

25-Nov-24

$5.00 ($4.00 - $6.00) based on today's soft guidance for 1H FY25.

Thesis fully intact, as I consider this to be purely cycical.

16-Jul-24

See my related straw:

I don't yet have any unique insights on $IPG. I think the three covering analysts are generous / bullish with an average TP of $5.58 and a very narrow range ($5.50 - $5.65) versus today's close of $4.81. I'll therefore be a tad more conservative and post an inital Strawman valuation of $5.40.

I'll have a go at my own model, once I get to see a clean 6-months for the combination of IPG+CMI in Feb 2025.

AGM today for IPD group and they have an earnings guidance for 1H26:

This looks to be a small beat over the Taylor Collison broker forecast of $24.5m EBITDA from August.

Further commentary from the chairman below:

"IPD enters FY26 from a position of strength. Demand for integrated electrical solutions continues to grow, driven by infrastructure upgrades, data centre expansion and decarbonisation objectives across the economy. We are positive the Group’s strategic direction is sound and remain focused on innovation, disciplined execution and shareholder returns. As CEO Michael Sainsbury will shortly detail in his presentation, year to date trading is showing positive momentum across all Group businesses and we are pleased to announce guidance for the first half of FY26 in the range of 5.1%-7.2% for EBITDA growth over the FY25 pcp."

The other important detail I'm seeing is that founding director and ex-CFO Mohamed Yoosuff will step down from his executive role and assume a non-executive director role from 31 December. He currently owns ~11% of the company. I've included the chairman's comments about his transition below. Notably, he states that Mohamed has no current plans to reduce his holdings, but we've all heard that one before.

"To close, I would like to thank my fellow Directors for their considerable input and guidance across the financial year. I’m particularly pleased that Founding Director and major shareholder Mohamed Yoosuff will continue his long standing connection with IPD Group as a Non-Executive Director following his retirement from his current executive role at the end of December. As disclosed in October, Mohamed has made an indelible mark on IPD Group over the past two decades, a period of significant growth, multiple acquisitions, and a successful ASX listing. I also note his commentary at the time that he will remain actively engaged as a Non-Executive Director and long-term shareholder, with no current intention of reducing his shareholding. Thank you to all our shareholders, staff and supply chain partners for your continued support and belief in IPD’s future."

Overall, IPD is probably the shareholding I have weakest confidence in, as I don't necessarily trust their governance based on past behaviours. But this is a solid print and they are still a key supplier to a sector growing strongly, right as the construction industry starts to rebound as well. Please no one remind me of this when Mohamed Yoosuff sells off 50% of his holdings in January.

Disc - Held

Electrical distribution and automation supplier $IPG announced their 1H Results this morning.

I've provided a full summary of the investor call this morning later in this straw. However, it is important to recognise that in this 1H result we have the first full inclusion of the major CMI acquisition, which had been absent from the PCP. And so, I want to focus on just one slide - probably the least flattering of the entire presentation. The pro forma comparison, which lets us see how the actual operating businesses performed.

Figure 1

So essentially, revenue and gross margin just inched ahead. And profit fell back, with management explanation that this is due to 1) CMI’s lower-margin impact, 2) shift to larger, lower-margin projects, 3) higher operating costs to support future growth, and 4) commercial construction weakness. Reading my summary below, you get a very different view of the business, which is why when M&A is at play, it is vital to look at the pro forma picture.

The commercial environment is tough, and CEO Michael Sainsbury reportdc that the result shows that $IPG is gaining market share.

He said:

" ... there are a number of our competitors that are reporting 8% and 10% and 15% revenue degradation as well because of the market conditions. So I think we've done better than the market. I certainly feel as though we've taken some share in these tough conditions, which will hold us in really good stead when the market does pick up again that you've secured that business and you move into more buoyant market with more share."

(I need to dig into some of this.)

Overall, the market responded positively to the result on the day with SP +4% on the day, but yet to claw back all the losses when it issued the underwhelming guidance at the AGM. Today's result just beat 1H guidance for EBITDA and EBIT.

Increasing the dividend by +40%, with the payout at 50% is a good result. The balance sheet is strong and operating cashflow was good. I think these helped encourage the market response.

My Overall Takeaway

Overall, I think the result is OK. It represents a starting point for the enlarged group and, over the next year, we should start to see business efficiencies come through, as well as revenue synergies between the individual business units.

Management have said a lot about each of the business units over the last year, and so I am happy to see how much of this pans out over the year ahead. I am still getting to know the business, management, and the sector. For today, I am content to stick with my valuation of $5.00 ($4.00 - $6.00) from the AGM.

----------------------------------------------------------------------------------------------

Full Summary of the Investor Call and Presentation

Overall

IPD Group delivered record revenue and profit growth in 1H FY25, exceeding guidance. Strong cash generation, debt reduction, and a record order backlog provide confidence for sustained performance in 2H FY25. While commercial construction remains weak, IPD is gaining market share, expanding into data centers, renewables, and EV infrastructure. Management remains optimistic about continued growth, supported by price increases, acquisitions, and product diversification.

1) Key Results Headlines (Comparison to 1H FY24)

- Revenue: A$176.9 million, up 46.6% from A$120.7 million.

- EBITDA: A$23.6 million, up 46.6%.

- EBIT: A$20.2 million, up 47.4%.

- Net Profit After Tax (NPAT): A$13.3 million, up 40.0%.

- Earnings per Share (EPS): A$0.129, up 19.4%.

- Operating Free Cash Flow: A$25.3 million, up from A$10.1 million, reflecting strong cash conversion (107.6%).

- Net Debt: A$2.2 million, a substantial reduction from A$8.8 million at June 30, 2024.

- Order Backlog: A$92.7 million, up 49%, ensuring strong revenue visibility.

- Interim Dividend: A$0.064 per share, up 39.1%, with a 50% payout ratio.

(Yeah - so, now you understand why I wanted to highlight the pro forma page!)

2) Operational Highlights by Sector

- Data Centers:

- Revenue from data centers grew 25% YoY, now representing 15% of total revenue.

- Strong order book with Amazon and NEXTDC data center projects.

- EV Charging & Public Transport Electrification:

- Continued expansion in EV infrastructure projects via Addelec Power Services.

- Notable wins include Perth Transit Authority ($10.9 million project pipeline) and NRMA (A$3.5 million opportunities).

- NSW Kingsgrove Bus Depot project officially commenced, with revenue expected in 2H FY25.

- Commercial Construction & Infrastructure:

- Remains largest revenue contributor, though facing headwinds in broader market.

- Successfully expanding into water & wastewater, contributing 13% of total revenue.

- Industrial & Mining:

- Hazardous area electrical equipment sales grew significantly via EX Engineering.

- Secured major contracts in oil & gas.

- Wholesale & Trade Sales:

- Outperformed market trends, gaining share from competitors despite construction slowdown.

- CMI Operations showed weakness in New South Wales and Victoria due to commercial construction softness but gained traction in WA and export markets.

3) Cash Flow Highlights

- Net Operating Cash Flow: A$25.3 million, up over 100%, reflecting strong conversion.

- Net Investing Cash Flow: -A$4.5 million, primarily due to capital expenditure and acquisitions.

- Net Financing Cash Flow: -A$2.2 million, driven by debt repayments.

- Cash Balance (End of Period): A$28.9 million.

- Debt Reduction: A$10 million in borrowings repaid post-half-year, reducing core debt by ~33%.

4) Balance Sheet

- Total Net Assets: A$158.1 million, strengthening the group's financial position.

- Net Debt: A$2.2 million, down from A$8.8 million.

- Inventory: Increased slightly by A$1.2 million, reflecting demand growth.

- Dividend: A$0.064 per share, fully franked (payout ratio: 50%). Increased by 40,

5) Industry Outlook & Competitive Landscape

- Market Conditions:

- Commercial construction remains challenging, but IPD is outperforming competitors.

- Interest rate cuts may boost sector activity in the next 6-12 months.

- Growing demand for data centers, renewable energy, and EV infrastructure supports future growth.

- Competitive Positioning:

- Taking market share in high-margin trade business, outperforming ASX-listed peers.

- Expanding ABB product range but not exclusively reliant on ABB.

- IPD currently only captures ~20% of the electrical contractor market, indicating significant growth potential.

6) Summary of Q&A with Analysts

- Order Backlog Conversion:

- Current backlog (~A$93M) represents 3-4 months of work, supporting 2H FY25 revenue.

- Some Amazon orders were pulled forward into 1H FY25, but pipeline remains strong.

- Market Share & Expansion Strategy:

- ABB partnership still has growth runway, but IPD is not limited to ABB products.

- Opportunity to expand into other electrical contractor product categories (beyond current 20% penetration).

- Daily Trade Business & Market Conditions:

- IPD has outperformed competitors, gaining share in a weak construction market.

- CEO expects the market has bottomed out, with gradual recovery over the next 6-12 months.

- Price Increases & Margins:

- No supplier price increases for 12 months, but IPD to implement a 3-4% price rise in March 2025.

- Due to contract structures, only ~50% of this price increase will flow through in 2H FY25.

Disc: Held in RL and SM

The biggest takeaway from the AGM was this slide from the CEO, Michael Sainsbury’s, Presentation:

Michael said the business model is changing from day to day projects to larger projects with longer time frames. He said the order backlog has grown from $62 million to $92 million in the 12 months from October 2023, up 50%, and the average monthly orders are up 39% compared to 1H24. These orders will be eventually invoiced and come through in the revenue. He expects 2H24 to be much stronger than 1H25.

His said construction has slowed but will come back (sort of contradicts the order book story) but will come back. He did have a little slip of the tongue when talking about the cost base relative to sales revenue, saying “we have controlled the bleed”. He quickly covered up by saying that was a poor choice of words. Did the truth slip out? I guess we’ll find out in about 10 months time.

Interesting that Data Centre revenue is growing at 25% per year and currently makes up 12% of the revenue.

i come away thinking the business seems to have enormous potential. I’ve come away with a bit more confidence the business is on the right track. If the order book backlog does converts to invoices and revenue we should see good growth return. However, we need to trust management on this and take a big leap of faith. I’d like to see the order book included in each trading update going forward if this is the “new” business model. If we don’t hear about the order book backlog going forward, that won’t be a good sign.

Held IRL (tiny)

25/11/2024

I’m new to IPD Group (ASX: IPG) after taking a nibble today. The business was listed on the ASX in December 2021, so there’s only 3 years of historical data to go on, and we’re still getting to know management. Specialising in supplying products and services for Australia’s growing electrical infrastructure, the businesses should have tailwinds as Australia moves forward with renewable energy and data centres.

Until FY24 the business has performed well, growing revenue at 26.2% per year, and NPAT at 35.8% per year. ROE has averaged 18% (FY22 17.5%, FY23 22.1% and FY24 15.4%).

Source: Commsec

Following the updated guidance for 1HFY25, I’m expecting FY25 NPAT to be c.$25 million, up 10% on FY24 (similar to @mikebrisy’s assumptions). Shareholder equity at 30 June 2024 was $151 million, so I expect FY25 ROE to be c. 16.5%. This would bring the average 4 year ROE to c. 18%. For valuation purposes I’m going to assume IPG goes forward with ROE of 17% and hope that I’m being too conservative.

Using McNiven’s Formula and assuming ROE of 17%, shareholder equity of $1.46 per share, 54% of earnings reinvested, 46% of earnings paid as fully franked dividends, and requiring a minimum annual return of 10%, I get a valuation of $3.90. At the current share price ($3.69) I think the shares are reasonable value, but they’re not exceptionally cheap. I’d be happy to add more on further share price weakness.

Held IRL (starter position)

The market has reacted very negatively to IPD Group’s Earnings guidance today, down over 11%. Is this an overreaction, or is it warranted?

1H25 EBIT guidance is $19.2 million to $19.8 million, mid-point $19.5 million. Assuming a 30% tax rate, that’s $13.6 million net profit before interest. Assuming 2H is similar that’s about $25 million before interest for FY25 which is a miss on analyst expectations of c. $30 million.

CEO, Michael Sainsbury, said margins will be impacted in 1HFY25.

What do others think?

Not held.

Based on unaudited results for the 4 months ending October 2024, and management forecasts for November and December, the Company provides the following earnings guidance range for 1H25:

The Company also notes that:

• Revenue for 1H25 is forecast to exceed the pcp (Pro Forma);

• Average monthly orders received has grown 39% in Jul-Oct 2024 Vs 1H24 (Pro Forma); and

• Order Backlog (as at end October 2024) has grown to $93.1m, a 50% increase on the pcp (Pro Forma).

Michael Sainsbury, IPD Group Limited CEO, said: “We are pleased to remain on track to deliver another half of revenue growth in a challenging environment. Amidst the wider macroeconomic challenges in the commercial construction sector, we have seen our order book transition from daily trade to larger and more complex orders, which typically have longer lead times and less certainty around delivery timing. This has resulted in a proportion of orders that would previously have already become invoiced Revenue now sitting in our Order Backlog. We have made additional investments into our operating cost base to generate and deliver these additional orders, which will impact margins for 1HFY25. Our operating cost base however is well placed to service future growth. We remain excited by IPD’s ongoing evolution and the continued improvements to our overall value proposition and look forward to providing more details around today’s update at the Company’s AGM on Tuesday, 26 November 2024.”

Bell special if you need to find the source of the recent price declines

[held]

From investor presentation 30/8/24

Growth for the year was great by acquisition, but not pro forma which was +3% NPAT. Also EPS growth was 30% because of share issue.

Reported growth.

Pro

Based on unaudited results for the 10 months ending April 2024, and management forecasts for May and June, the Company provides the following earnings guidance range for the FY24 full year:

EBIDA FY23 v Fy24 range: up 44%

Return (inc div) 1yr: 20.03% 3yr: N/A 5yr: N/A

Net Profit Margin: 7.5% (Thats good for this industry)

Electrical products distributor and service provider $IPG announced their 1H results last week.

The company which was listed in late-2021 has seen its SP on a tear, heading into the results up 5x since listing. (Max kudos to the early StrawPeople who got onboard!)

$IPG has been on my watch list for 6-9 months, and I took a starting position in it on the pullback following results, which saw SP fall from a peak of $5.43 to close on Friday at $4.75, a handy correction of 14%.

I'll write next week in further detail as to why I am investing in $IPG, and will here just discuss the results. For those wanting more detail, there are broker reports by Bell Potter (TP $5.95) and Taylor Collison (TP $5.00 - free on the ASX broker report service.)

Now, as a word of caution on analyst views, my understanding is that Bell Potter was the lead Manager and Underwriter of the November capital raising. Their very high TP should be considered in that context.

Their 1H FY24 Highlights

- Record half-year revenues and earnings at the top end of the guidance range

- Revenue of $120.7 million representing 8.8% growth on pcp

- EBIT of $14.0 million representing 21.7% growth on pcp

- NPAT of $9.8 million representing 22.5% growth on pcp

- Fully franked interim dividend of 4.6 cents per share declared

- Strong balance sheet, with $142.7 million of net assets at period-end (net debt of $23.7 million as at 31 January 2024)

- Successful completion of the acquisition of EX Engineering Pty Ltd (“EX Engineering”)

- Announced acquisition of 100% of CMI Operations Limited (“CMI Operations”), a leading distributor of electrical cables and manufacturer & distributor of plug brands in Australia, from ASX-listed Excelsior Capital Limited (ASX:ECL)

- Raised $65.0 million of new equity capital in December 2023

- Post financial year-end: Entered into new $40 million debt facility to partially fund acquisition of CMI Operations and Completed acquisition of CMI Operations on 31 January 2024

My Analysis

I was unable to attend the call and haven't looked at the transcript. So my analysis is a simple desktop exercise.

Expectations for $IPG were high. SP has been on a tear.

The 1H FY24 doesn't include the material CMI acquisition, although the EPS is lowered temporarily because the new shares were issued in late December, but the deal only closed in early 2H24. I'll pick through this in my preliminary valuation, which I'll post next week.

The table above shows why the market has reacted negatively and also why I think the results are not that bad.

Revenue growth at 8.8% is a softer result, compared to the trajectory over recent years (pre- and Post IPO). I think it is this softer result that perhaps triggered the SP correction. In the lead-up to results, the SP had run up hard, close to a stretching consensus, driven by Bell Potter's bullish view. However, despite low revenue growth (and short term revenue growth is not central to my investment thesis!), as we progress down the P&L, the results look pretty healthy.

%Gross Margin is a healthy 40%, up 2.4% from pcp.

EBITDA Margin is 13.7%, up 1.6%, drive by falling freight and distribution costs. (The marginal %EBITDA is actually 33% on a PCP comparison, which is not to be anchored on because the freight and distribution cost improvements cannot be sustained. I should also do the marginal analysis on the prior period.)

EBIT Margin was 12.0% up from 10.6%, and NPAT Margin was 7.9% up from 7.2%,

Note: My analysis is on the Statutory numbers and differs from the table above. I'm not prepared to consider the Underlying because M&A is an ongoing part of the business model, and core to my thesis, so I will not correct for the costs that arise from it.

These are pretty healthy numbers.

If we ignore the CMI acquisition, and assuming 2H and 1H are similar (there appears to be a slight historical weighting to 2H), then that would put $IPG on a annualised NPAT of $19,09. Backing out the new shares (because the result is not affected by the CMI acquistion), then by my calculation that puts $IPG on a p/e of 21.5 at its Friday close of $4.75.

This is a high p/e for a distributor. However, when I set out my investment thesis I explain why I am happy with this entry point.

I've had a quick look at cashflows, which were underwhelming, however movements in payables, receivables and inventories needs a deeper dive to make sense of it all, and therefore I am assuming the financials are a better guide. Cashflow and debt are not a concern based on a longer term historical view, so I'll leave this for another day.

My Key Takeways

In summary, there is no escaping that organic revenue growth was soft in the half, however the business was able to achieve good margin expansion, achieving what are pretty decent metrics for a 91% distributor / 9% services business.

Drivers of margin expansion have been moving more of the support activities of the individual businesses onto a share service model, consolidating their regional distribution networks, and favourable distribution costs in the PCP comparison.

From my selfish perspective, the down-trend in SP might continue for a while (gotta love technical traders), as I would like to increase my position here recognising I have paid more than I wanted to get started. More on that next week when I set out my investment thesis and valuation.

Disc: Held in RL and SM

Full text from behind the paywall of the Weekend Australian.

Interesting article that highlights the valuation gap of the CMI sale vs the book value of CMI from Excelsior but not getting any answers why this has happened.

Excelsior’s valuation perplexity - 16dec23

[held]

Tuesday Trades at $4.47 will this price give way to the Offer Price of $3.93 (price normally will fall to the Offer price)

All New Shares offered under the Equity Raising will be issued at a price of $3.93 (“Offer Price”)

A decent rally today closed at $4.77 up 13.57%

IPG way above the Cap raising of $3.93 ( 1 for 13.65 shares held )

Return (inc div) 1yr: 55.96% 3yr: N/A 5yr: N/A

IPD Group is undergoing a capital raising.

Funds raised: $65m

Extra shares: 16.5m

Synergies: Expected but not included

Because I don't have time, hopefully someone can do an exact valuation. If you are inclined go to fightfinance for the methodology after clicking the answers.

Roughly we should expect a market cap from 364m to 429m and SOI of 103m shares.

Some important slides that will help

But I'm sure the market will try and drag this below $4.

As I already topped up at the recent lows, I think I have enough shares already - not sure if I take up the rights issue.

[held]

Revenue of $226.9million, up 28.3% on pcp – Strong organic growth has been delivered predominantly by the existing product portfolio and growing market share – Strong statutory growth displayed by a 37.4% CAGR

EBITDA of $27.7 million, up 37.1% on pcp – There have been ongoing strategic investments made during the year, some of which include: • Expansion of the Gemtek team

• Recruitment of specification focused business development managers across the country

• Operational expansion with a new 4,000sqm warehouse – While the Group has invested into these strategic initiatives during the financial year, the Group continued to deliver strengthening EBITDA margins, and a 44.9% EBITDA CAGR over the past four financial years

So Check out IPG a steady pathway to growth. could add some units today with the expected bearish market..

Return (inc div) 1yr: 132.35% 3yr: N/A 5yr: N/A