Price History

Premium Content

Premium Content

Premium Content

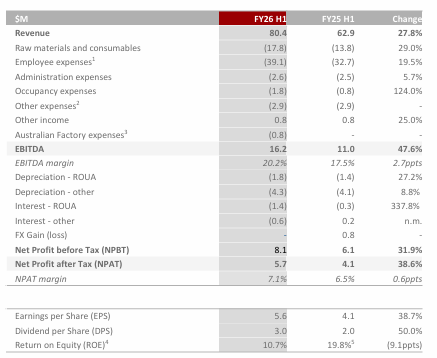

PWR Holdings (PWH.ASX) reported their 1H FY26 results last week. From their presentation:

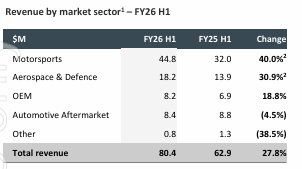

A record half result driven by good growth in the Motorsports and Aerospace & Defence (A&D) segments.

Motorsports was driven by the new F1 regulations requiring all teams to redesign their cars as well as the introduction of an 11th team (Cadillac) on the grid. Testing for the new cars was also brought forward from February to January which brought forward some revenue usually banked in H2 to H1. Management said on the call that the seasonality usually experienced with a stronger 2H won't be as evident due to this.

A&D continues to be the big growth driver of the business with the recognition of the 1st US government project and production of this project in the 1H. There is an expectation that this will bring further projects to the business given they are now an approved supplier and have achieved accreditation after their factory relocation.

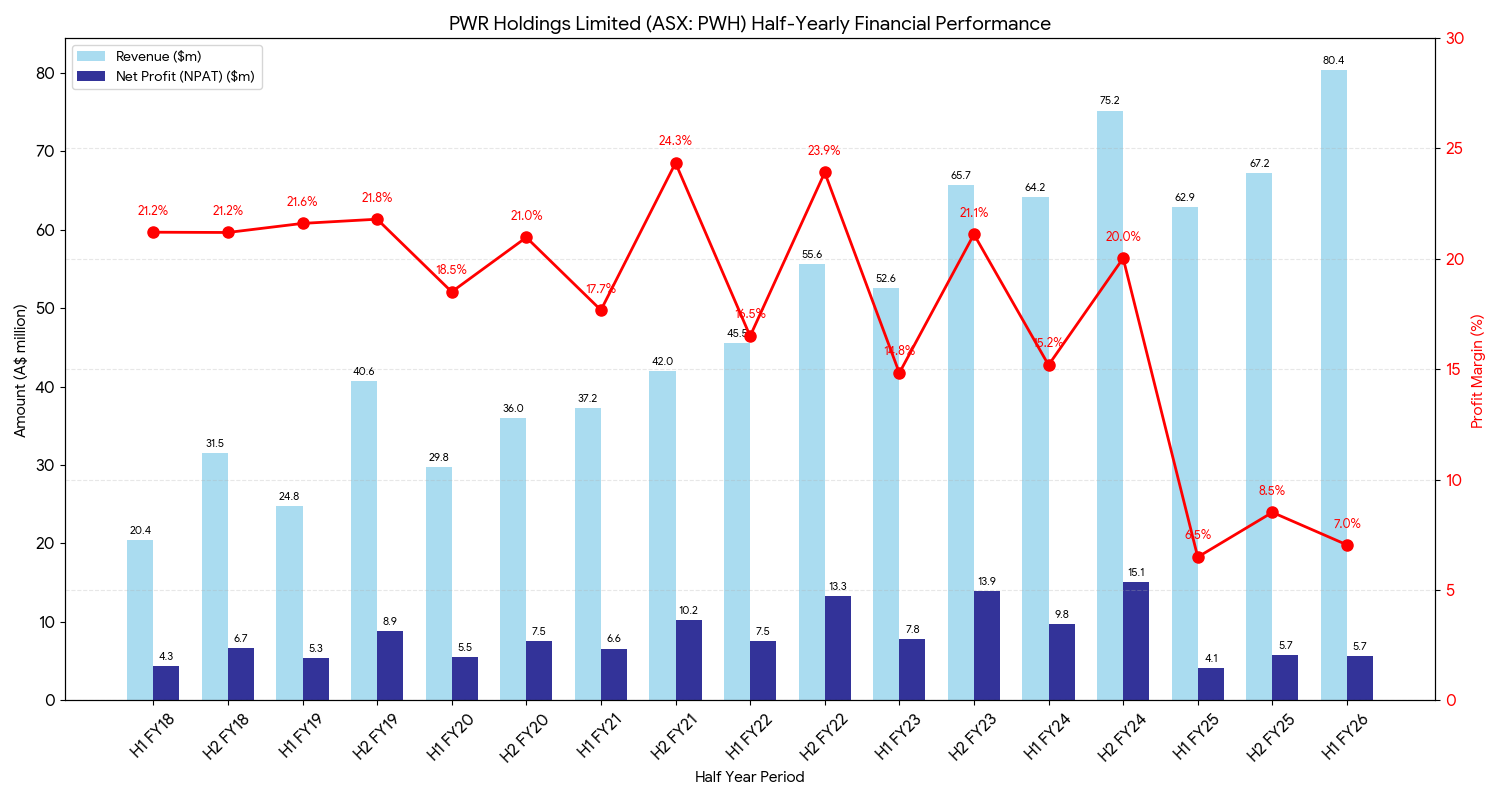

On margins, I've plotted the graph below showing Revenue, NPAT and NPAT margins for the last few years. As we can see, NPAT margins have deteriorated mostly due to increased costs involved with the build out of the new factory as well as costs involved with relocation. Management said on the call that they expect the profit margin to improve back to FY24 levels in the next 3-5 years as the investment phase has mostly completed following the move to the new facility.

One interesting question that was asked of management was whether they have had any interest in terms of developing cooling solutions for the AI and Data Centre use cases. Management said that whilst they have had some interest come to them they don't believe that they will pivot into this space at this stage. Stating that the cooling solutions needed for AI and Data Centres are more mass produced, high volume products where as they prefer to stick to their expertise and niche which is highly specialised and custom solutions for their customers.

Disc: Held IRL and on Strawman.

PWR Holdings (PWH) released results after market close last night. From their presentation:

On paper an ugly result but was well flagged in their trading update from Nov 24. Decrease in revenue mostly due to delays and cancellations is its automotive OEM segment but this was offset by a large increase in A&D revenue.

FY25 is an investment year for PWH as they look to upgrade their Australian factory as well as increase capacity in Europe and North America. This coupled with the loss of revenue in some segments of the business means that this result along with the FY25 result will look ugly.

Outlook was given with the company expecting FY25 revenue to be around 5-10% less than FY24. Although on the call Kees did mention that this was mainly due to some "timing issues" with regards to them moving to the new factory along with them being a bit more conservative with guidance in the hope of "under promising and over delivering".

At the current share price it definitely looks expensive looking backwards and you'd hope that this current investment period will bear fruit in the medium-long term future. I'm willing to give management the benefit of doubt that they will pay off in the future so will likely top up on expected share price weakness.

Disc: Held IRL and on Strawman.

PWR holdings reported their H1 FY24 results after hours last night. From their presentation:

A much better half compared to this time last year. Their increase in investments over the past year are starting to show through now. Seasonally 1H is always the weaker half with lower revenue and lower margins. Although net margins have improved back above 15% for the half. Overall net margins are usually around 20%.

Customer mix is improving with less than 50% of revenue coming from the motorsports segment showing their increasing footprint into aerospace and defence.

Overall I thought this was a very solid result given the increased investment of the past year and look forward to seeing the growth come through in future periods.

Disc: Held IRL and on Strawman.

PWH released their FY23 results a few days ago, from their presentation:

I thought the result was pretty solid after a fairly disappointing 1H FY23. This year has been a year of investment in the business with the acquisition of several businesses to increase their footprint into Europe. The increase in net assets and lease liabilities reflects this.

Whilst 1H FY23 saw net margins fall below 15% as a result of this increase in spending and also the increased cost of raw materials. 2H FY23 saw a return to increased profitability with net margins improving to back above 20% again.

Management themselves have mentioned that with the increased investment, they will be able to support further growth with current capacity at their new site in Rugby (UK) only being 50% utilised at present.

Once again there was strong growth in emerging technologies with Aerospace and Defence now making up 9% of total revenue. This table below shows their Revenue by Customer Market.

Still lots of projects in the pipeline and interestingly as an F1 fan, I saw that they had secured the contracts for multiple teams for FY26. This is interesting as this is around the time that several major teams will be entering/re-entering the F1 scene. I believe given the growth of F1 in North America, there will likely be more than 10 teams on the grid, thus providing more teams for PWH to work with.

Will update my valuation shortly. Whilst the business seems to be back on track, shares are still quite expensive, and growth would need to continue into the future to support the current price.

Disc: Held IRL and on Strawman.

PWR Holdings (PWH) released their 1H FY23 results after market yesterday. From their presentation:

Probably not the best result considering before the results release they were trading on a PE of around 60x. Management stated that increase labour costs and raw material costs impacted the bottom line. They also spent money to expand into Europe in the last half.

I think in the long term PWH should benefit from the current investment period. Their business is relatively capital intensive, needing to purchase assets in order to scale up their business, and so it remains to be seen whether this level of investment will pay off in years to come.

Shares are still too expensive (even after today's pullback) for mine. I did sell around half of my shares at above $11 around a month ago as I thought the valuation was looking stretched then. At under $7 I think I will likely top up my holdings but they remain a solid hold at the moment. Still lots of projects in the pipeline.

Disc: Held IRL and on Strawman.

PWR Holdings (PWH) released their FY22 Results ahead of their conference call tomorrow morning. From their release:

A bumper H2FY22 saw a record result for the company as they ticked over $100m in revenue for the first time. NPAT was also a record. Cash flow was a little lower due to increase in spending due to supply chain constraints although management have said that this will ease as supply chains revert back to normal.

I have updated my chart from the previous straw to reflect the full year results.

If you ignore FY20 which was covid impacted, NPAT has compounded at 15% for the last 5 years and shows the quality of this company to execute their goals.

I will update my valuation accordingly.

Full presentation here

Disc: Held IRL and on Strawman.

PWR Holdings (ASX:PWH) released their results for H1 FY22 after hours yesterday. From their release:

Overall a decent result given current covid headwinds driven mostly by a return in motorsports to a more normalised race program. I have graphed out their revenue growth and NPAT growth for the last few years below.

H2 is seasonally the stronger half so it will be interesting to see if they can maintain the growth. I still see a very long run way for this company as their cooling systems can be used in a multitude of applications and we are only just starting to see this playing out (emerging technologies grew by 36% but is only 14% of overall revenue).

I will maintain my valuation (see my valuation straw) as I still think currently shares are a bit overvalued but am a happy holder at current levels.

Disc: Held IRL and on Strawman