Consensus community valuation

Update 25/0282026

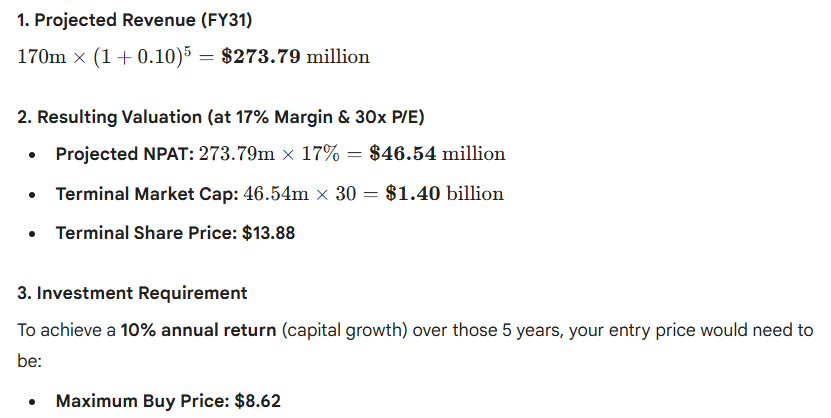

Been using Gemini AI to look into the valuation. This is what it comes up with the following assumptions:

- FY26 total revenue of $170m

- CAGR of 10% pa

- Increase in NPAT margins back to FY24 levels (17%)

- Terminal PE of 30x in 5 years time

Will leave this as the valuation for now.

Update 22/08/2024

Updating with FY24 results added:

FY24 result came in a bit below expectations given that H1 was very strong.

Management have flagged that the next year will likely be an investment year as they build out their capability to facilitate further growth.

I'm going to give them the benefit of the doubt that a CAGR of 15% is still achievable in the long run. Discounting it back 10% pa with a terminal PE of 30x gives a valuation of $7.75.

I think I see some value if the price got to below $8 given the potential upside of their Aerospace and Defence segment (100% yoy growth) but this is still only 15% of total revenue.

Disc: Held IRL and on Strawman.

Update 22/02/2024

Updating my charts with 1H FY24 results added:

Revising some assumptions with NPAT growth of 25% for FY24 before returning to 15% growth for the next 4 years.

Discounting back 10% pa with a terminal PE of 30x gives a valuation of $8.14.

Disc: Held IRL and on Strawman.

Update 19/08/2023

Basing my valuation on a return to growth of 15% pa for the next 5 years and a terminal PE of 30x. This gives me a valuation of $6.80 in order to achieve a return of 10% pa.

Disc: Held IRL and on Strawman.

Update 18/03/2023

H1 FY23 results were quite disappointing for a company that was trading on a high PE although I do think the underlying business will benefit from the near term increase in investment to scale out their business.

I still regard this as one of the highest quality companies on the ASX and am willing to maintain my valuation of $6.51. I think if the share price decreased below $7 this starts to look interesting again. Capital allocation from management has always been first class and there are plenty of projects in the pipeline to continue on their growth trajectory.

The skew to 2H has always been strong so I wouldn't be surprised if they had a killer 2H FY23.

Definitely one to watch if there is further share price weakness.

Disc: Held IRL and on Strawman. Did sell some shares above $11 but will likely look to top up again if the SP fell below $7.

Update 18/08/2022

FY22 NPAT came in at around $20.4m representing a 24% increase YOY.

I am usually hesitant to assume that NPAT will continue to grow by such a large amount every year and so if I maintain my assumption of 15% CAGR for the next 5 years, and a terminal PE of 30x. This gives an updated valuation of $6.51.

Disc: Held IRL and on Strawman.

Update 08/06/2022

Just adjusting my valuation slightly as I think there will be further compression of PE ratios.

Same assumptions as above but assuming a terminal 30x PE would give a valuation of $5.77.

A terminal 25x PE would give a valuation of $4.81.

Disc: Held IRL and on Strawman

Original Valuation

PWR is an interesting company focusing on building cooling systems mostly in automobiles but are pivoting into other opportunities such as aerospace and defence.

- FY21 NPAT = $16.797m

- EPS = $0.1677

If they can grow NPAT at 15% per annum for the next 5 years (ambitious but some analysts have forecasts of greater than this) this gives:

- FY26 NPAT = $33.78m

- FY26 EPS (assuming around 120m shares on issue) = $0.28

- FY26 target price (assuming 35x PE) = $9.85

Discounting this back 10% per annum gives us an FY22 price of $6.73.

A PE of 40x would have FY22 price of $7.65.

Currently do hold some shares purchased around current prices but wouldn't likely add unless the price started with a $7.xx.

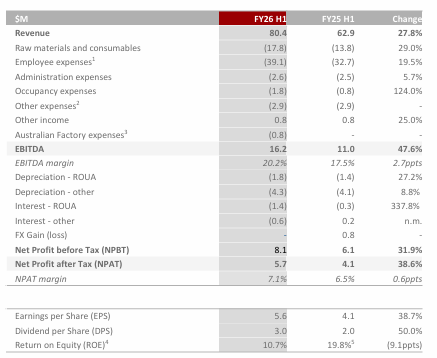

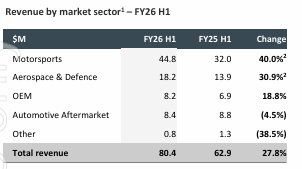

PWR Holdings (PWH.ASX) reported their 1H FY26 results last week. From their presentation:

A record half result driven by good growth in the Motorsports and Aerospace & Defence (A&D) segments.

Motorsports was driven by the new F1 regulations requiring all teams to redesign their cars as well as the introduction of an 11th team (Cadillac) on the grid. Testing for the new cars was also brought forward from February to January which brought forward some revenue usually banked in H2 to H1. Management said on the call that the seasonality usually experienced with a stronger 2H won't be as evident due to this.

A&D continues to be the big growth driver of the business with the recognition of the 1st US government project and production of this project in the 1H. There is an expectation that this will bring further projects to the business given they are now an approved supplier and have achieved accreditation after their factory relocation.

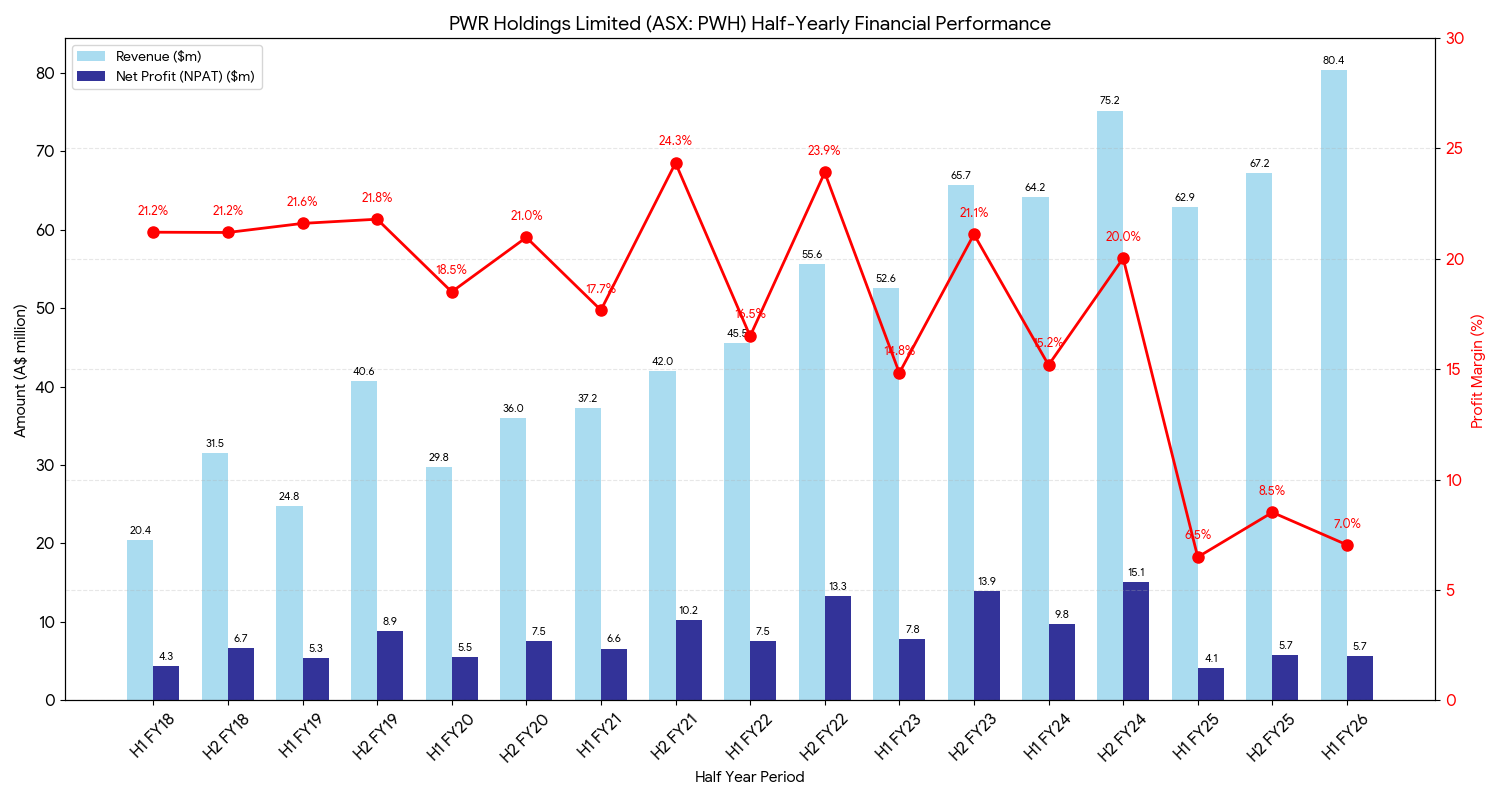

On margins, I've plotted the graph below showing Revenue, NPAT and NPAT margins for the last few years. As we can see, NPAT margins have deteriorated mostly due to increased costs involved with the build out of the new factory as well as costs involved with relocation. Management said on the call that they expect the profit margin to improve back to FY24 levels in the next 3-5 years as the investment phase has mostly completed following the move to the new facility.

One interesting question that was asked of management was whether they have had any interest in terms of developing cooling solutions for the AI and Data Centre use cases. Management said that whilst they have had some interest come to them they don't believe that they will pivot into this space at this stage. Stating that the cooling solutions needed for AI and Data Centres are more mass produced, high volume products where as they prefer to stick to their expertise and niche which is highly specialised and custom solutions for their customers.

Disc: Held IRL and on Strawman.

The good news is they have an 8am call tomorrow to present their case. The bad news is prima facie this is their case.

I think a FY26 10% increase in revenue and 20% increase in costs are heroic assumptions, which I've fully adopted because otherwise...

SP to get smashed tomorrow.

PWR Holdings (PWH) released results after market close last night. From their presentation:

On paper an ugly result but was well flagged in their trading update from Nov 24. Decrease in revenue mostly due to delays and cancellations is its automotive OEM segment but this was offset by a large increase in A&D revenue.

FY25 is an investment year for PWH as they look to upgrade their Australian factory as well as increase capacity in Europe and North America. This coupled with the loss of revenue in some segments of the business means that this result along with the FY25 result will look ugly.

Outlook was given with the company expecting FY25 revenue to be around 5-10% less than FY24. Although on the call Kees did mention that this was mainly due to some "timing issues" with regards to them moving to the new factory along with them being a bit more conservative with guidance in the hope of "under promising and over delivering".

At the current share price it definitely looks expensive looking backwards and you'd hope that this current investment period will bear fruit in the medium-long term future. I'm willing to give management the benefit of doubt that they will pay off in the future so will likely top up on expected share price weakness.

Disc: Held IRL and on Strawman.

BAE systems has made the first STRIX VTOL test flight PWR Holdings involvement in this project is for the cooling system.

Reference of PWR Holdings initial involvement can also be found on the BAE systems website - https://www.baesystems.com/en-aus/blog/how-pwr-went-from-f1-to-drone-technologies

I think this project with BAE systems has been the only thing supporting the share price lately although the price appears to pump in the morning before getting dumped late in the day. Interesting this bit of news was not announced recently to the market.

Hard to say where the market demand for this drone will be in the future.

Being a test flight it is still early days so we shouldn't expect what is on the latest AGM presentation below

What happens to a growth company with a high PE when it announces it won't be growing the coming 12 month period, then subsequently announce to market that it's revenue will reverse?

Well the share price will fall, substantially. We are down ~23% at time of writing, and down close to 50% in the space of about 3 months. Why?

Well, PWR Holdings (PWH), has provided this update to the market this morning.

Key points to the above table are as follows:

- Lower revenue in two markets:

- OEM – three niche OEM EV programs are not proceeding in FY25 despite PWR receiving purchase orders in FY24 for the FY25 work program. Whilst several new programs are in various stages of discussion, the volatility of the EV market is creating unpredictability; and

- Aftermarket – revenue globally has been impacted by broader economic pressures.

- Semi-Fixed Production Costs – production costs are higher than pcp as they cannot be immediately reduced to match lower than expected volumes and, accordingly, are expected to disproportionately impact forecast earnings for H1 FY25.

This has come as a bit of a sucker punch after their full year release back on the 15th of August that FY25 will be a "transitional year" for them as they look to position themselves for "future growth" which will impact margins. What the market didn't expect is that revenue will go backwards, so this is a bit of a surprise and hence likely to take some time to digest.

I'm still mulling this one over, as PWH is a long term compounder for me, however this will cause for some reflection. Concerned about management not guiding for this a couple of months ago, and also the added pressure this will place on management which, if they depart or lighten holdings may be a deal/thesis breaker for me.

At this stage I am keen to see how this transitional year progresses but FY26 will definitely want to see them shift back to some growth and see some runs put on the board after the "transition" settles. Always risky to take a bet on how long this takes.

HELD here and IRL.

Seems like a logical Trump trade

Seems like institutions don't agree

BlackRock still has 900K left to sell. Van Eck has completely gone

[held]

A rare special from Bell Potter

Been quite hard to find any broker report

I did top up here but not in real life since I think maybe price is not right yet and appears a few index funds aren't done selling since it is now below the magical $1bn

[held]

Would be truly gobsmacked if someone or a group was selling purely because they knew the CFO was about to retire and there was nervousness about transition process. Selling on the basis of inside information?

If so, then this is pretty unfair that someone has taken pure advantage of this information that the rest of the market was unaware of.

Seems to have done a recovery but will have to see...

I guess next time if I see this happen to something I hold, I know where to look...

Probably fully priced

[held]

Reported Results after hrs with revenues and profits coming in softer versus consensus forecasts.

PWH: have spent some cash on the business expansion this generally dints the Revenue, Profit trend.

PWH is this a Buy?

The investments in headcount, factory space, equipment and systems are necessary to prepare PWR to deliver on our medium- and long-term growth objective, specifically growth in aerospace and defence, and is consistent with our approach to “invest now and collect later”

Opened down this morning

After hours announcement of FY24 results.

Prepare for some cheap shares since it was after hours.

[held]

PWR holdings reported their H1 FY24 results after hours last night. From their presentation:

A much better half compared to this time last year. Their increase in investments over the past year are starting to show through now. Seasonally 1H is always the weaker half with lower revenue and lower margins. Although net margins have improved back above 15% for the half. Overall net margins are usually around 20%.

Customer mix is improving with less than 50% of revenue coming from the motorsports segment showing their increasing footprint into aerospace and defence.

Overall I thought this was a very solid result given the increased investment of the past year and look forward to seeing the growth come through in future periods.

Disc: Held IRL and on Strawman.

PWH released their FY23 results a few days ago, from their presentation:

I thought the result was pretty solid after a fairly disappointing 1H FY23. This year has been a year of investment in the business with the acquisition of several businesses to increase their footprint into Europe. The increase in net assets and lease liabilities reflects this.

Whilst 1H FY23 saw net margins fall below 15% as a result of this increase in spending and also the increased cost of raw materials. 2H FY23 saw a return to increased profitability with net margins improving to back above 20% again.

Management themselves have mentioned that with the increased investment, they will be able to support further growth with current capacity at their new site in Rugby (UK) only being 50% utilised at present.

Once again there was strong growth in emerging technologies with Aerospace and Defence now making up 9% of total revenue. This table below shows their Revenue by Customer Market.

Still lots of projects in the pipeline and interestingly as an F1 fan, I saw that they had secured the contracts for multiple teams for FY26. This is interesting as this is around the time that several major teams will be entering/re-entering the F1 scene. I believe given the growth of F1 in North America, there will likely be more than 10 teams on the grid, thus providing more teams for PWH to work with.

Will update my valuation shortly. Whilst the business seems to be back on track, shares are still quite expensive, and growth would need to continue into the future to support the current price.

Disc: Held IRL and on Strawman.

PWR Preliminary Final Report and 2023 Annual Report

Your new Chairman, Roland Dane, who has unanimous support of the Board, has substantial Board, leadership, operational and financial experience and has been a Board member since March 2017. Roland will take over as Chairman at the conclusion of the 2023 Annual General Meeting

Return (inc div) 1yr: 4.38% 3yr: 27.35% pa 5yr: 27.90% pa

PWH: returns are like the leaky radiator at the moment. Engine light is amber!!! not red yet...

PWR Holdings (PWH) released their 1H FY23 results after market yesterday. From their presentation:

Probably not the best result considering before the results release they were trading on a PE of around 60x. Management stated that increase labour costs and raw material costs impacted the bottom line. They also spent money to expand into Europe in the last half.

I think in the long term PWH should benefit from the current investment period. Their business is relatively capital intensive, needing to purchase assets in order to scale up their business, and so it remains to be seen whether this level of investment will pay off in years to come.

Shares are still too expensive (even after today's pullback) for mine. I did sell around half of my shares at above $11 around a month ago as I thought the valuation was looking stretched then. At under $7 I think I will likely top up my holdings but they remain a solid hold at the moment. Still lots of projects in the pipeline.

Disc: Held IRL and on Strawman.

PWR Holdings (PWH) released their FY22 Results ahead of their conference call tomorrow morning. From their release:

A bumper H2FY22 saw a record result for the company as they ticked over $100m in revenue for the first time. NPAT was also a record. Cash flow was a little lower due to increase in spending due to supply chain constraints although management have said that this will ease as supply chains revert back to normal.

I have updated my chart from the previous straw to reflect the full year results.

If you ignore FY20 which was covid impacted, NPAT has compounded at 15% for the last 5 years and shows the quality of this company to execute their goals.

I will update my valuation accordingly.

Full presentation here

Disc: Held IRL and on Strawman.

PWR Holdings (ASX:PWH) released their results for H1 FY22 after hours yesterday. From their release:

Overall a decent result given current covid headwinds driven mostly by a return in motorsports to a more normalised race program. I have graphed out their revenue growth and NPAT growth for the last few years below.

H2 is seasonally the stronger half so it will be interesting to see if they can maintain the growth. I still see a very long run way for this company as their cooling systems can be used in a multitude of applications and we are only just starting to see this playing out (emerging technologies grew by 36% but is only 14% of overall revenue).

I will maintain my valuation (see my valuation straw) as I still think currently shares are a bit overvalued but am a happy holder at current levels.

Disc: Held IRL and on Strawman

PWR Holdings (ASX:PWH)

PWR produces advanced cooling systems to the motorsports, aerospace/defence sector. Also derives part of its revenue from OEM and automotive aftermarket segments. Basically - super niche, high tech/IP company run by founder/MD Kees Wheel.

Financials

- 77% gross margin, >25% operating margin and 21% net margin

- $19.8m in cash, no debt

- Consistent share count since listing

- ROA >15%, ROIC > 20% and ROE > 20% over last 5 years

Insider Holdings

- Kees Wheel Founder/MD 20.3m shares (20% of company)

- Matthew Bryson CTO 3.3m shares

Summary

- Valuation seems a little stretched at the moment - Sitting on TTM PE of 52x, and P/FCF of 94x

- However - if we take a closer look at the business, wow. Ticks many boxes for me:

- Founder led with huge amount of skin in the game. So far management have been very transparent and fair to shareholders

- 20%+ net margins, rock solid balance sheet

- Optionality - Some mentions in the AGM to branch into the aerospace/space segment.

- Their clients are largely those with deep pockets, willing to pay a premium to get the best product for their cars etc. Largely unaffected by Covid.

- Been a happy shareholder for the last 18 months, will be very happy if the market gives me a discount to pick up more shares in the future.