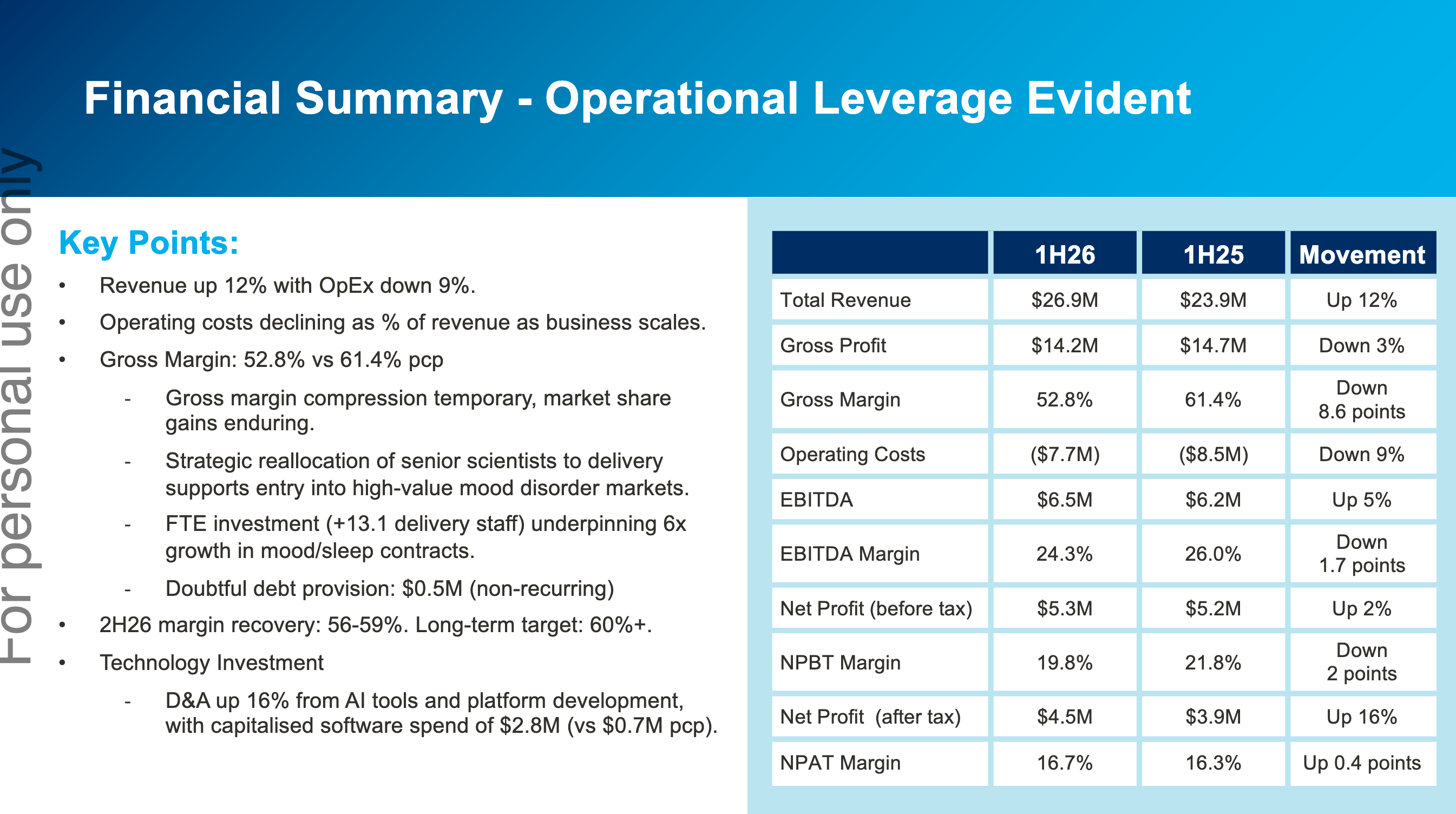

It was a solid, though unspectacular half. There’s been a bit of margin pressure due to increased investments which have been flagged 6 months earlier. They’ve flagged for a stronger second half based on significantly higher contracted revenue on hand verses this time last year.

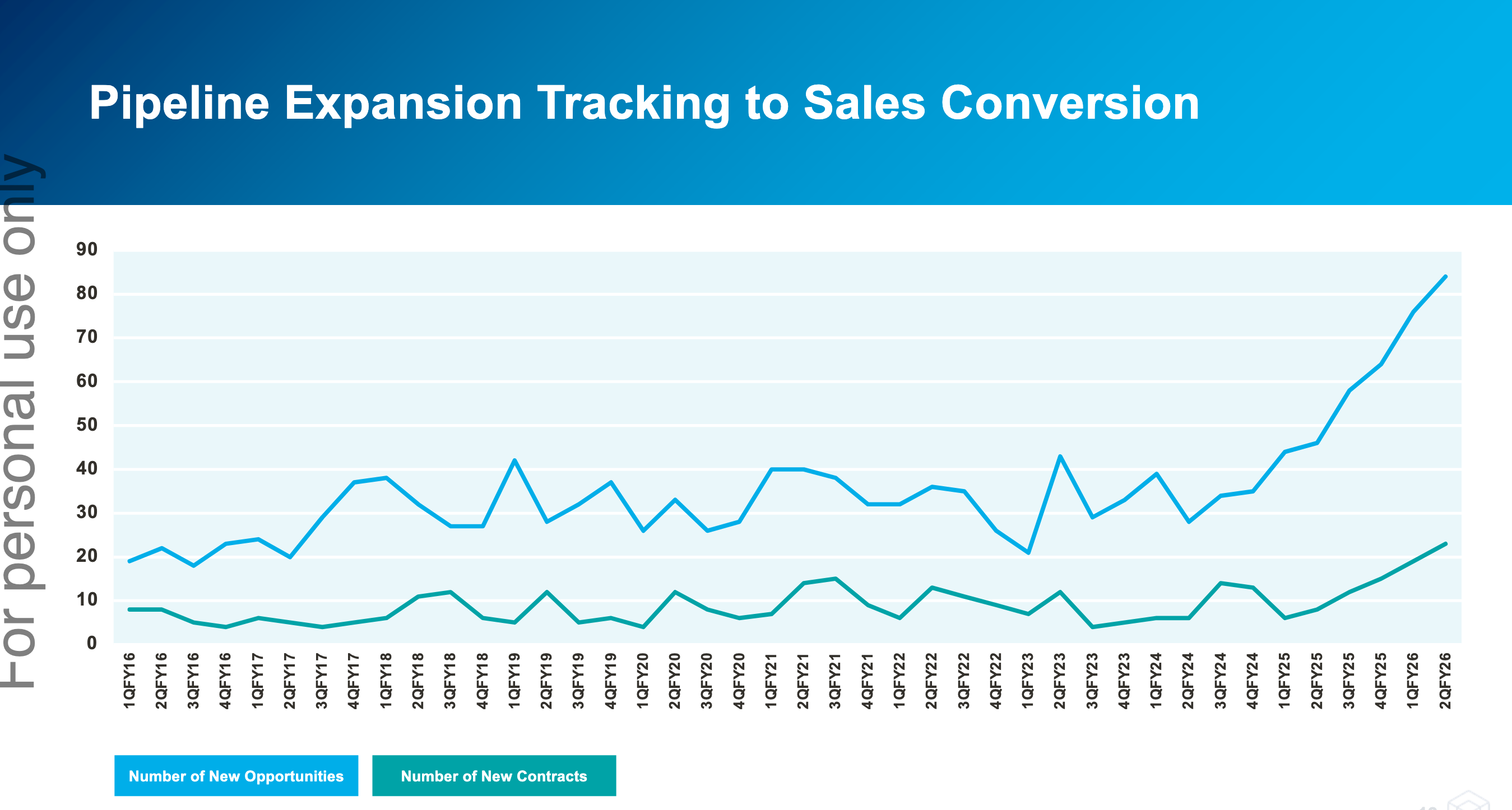

While the current results are subdued, the outlook has never been brighter. The number of new opportunities and new contracts is breaking out. Management has previously stated that contract wins lag opportunities by ~9 months, but there’s evidence that contract wins are now also starting to tick up.

A lot of this is due to expansion into new indications outside of Alzheimer’s Disease (AD) and work from the partner channels, specifically Medidata. Partner channels were 62% of new contracts in Q2 - I estimate it was less than 30% in Q1 and even lower previously. These new contracts are smaller in size, but are faster to execute, are more predictable and less prone to unexpected delays.

Reading through some of the old straws, it’s evident that a lot of investors were put off by how dependent the company was in winning large Phase 3 AD contracts. These contracts are large, concentrated, incredibly lumpy and prone to unexpected delays.

However Cogstate’s last large Phase 3 AD win was in FY22, and they’ve proven they can grow without these. And as new contract wins have shown, non-AD contracts are forming the “cake” of the growth story while AD contracts have been relegated to the cream and cherry on top.

By the way, the opportunities for large Phase 3 AD wins have not disappeared. The CEO has been hinted that he expects to see new Phase 3 pre-clinical AD contracts (which CGS has a very high win rate) to be rewarded in CY 2026. My bet is Roche’s upcoming PrevenTRON trial, or a brand new trial from Eli Lilly.

Looks like they "beat" the downgraded forecast for 1H FY26 that was given just a month ago

A couple of things to note.

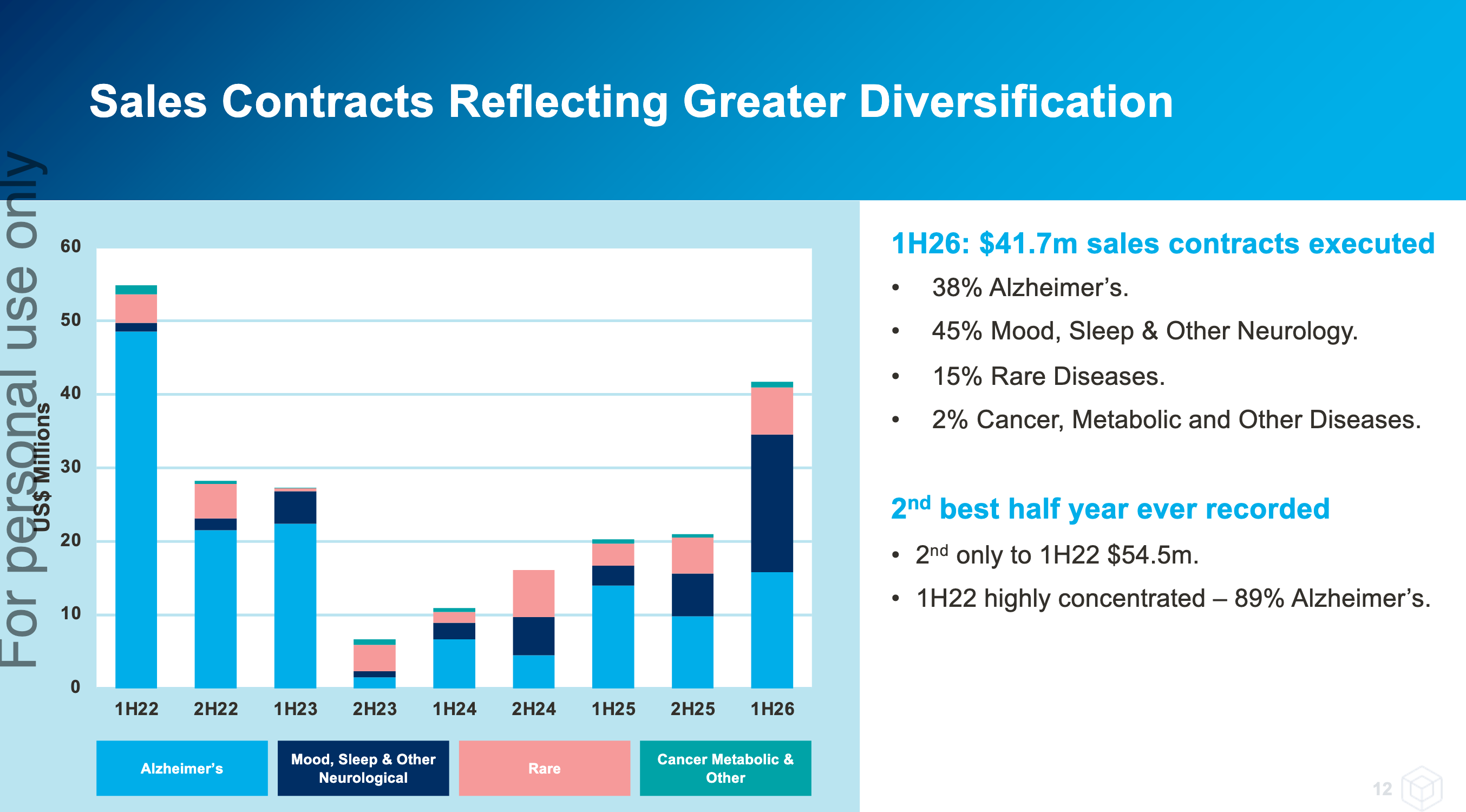

1) They're diversifying into other non-AD indications. These are also small and faster to execute trials, which make the business more predictable. From conversations with management, they're still hinting at a large AD win not too far in the horizon - so there's no visible deterioration in competitiveness there, it's just big and lumpy.

2) They've always recognised license revenue upfront. But now they're starting to do it across the length of the trials. I believe this is only for the new endpoints they've developed. Will smooth out revenues are bit more, and probably made 1H FY26 look a little worse, particularly on the margin side of things (license is 90%+ GM vs ~50% GM for services).

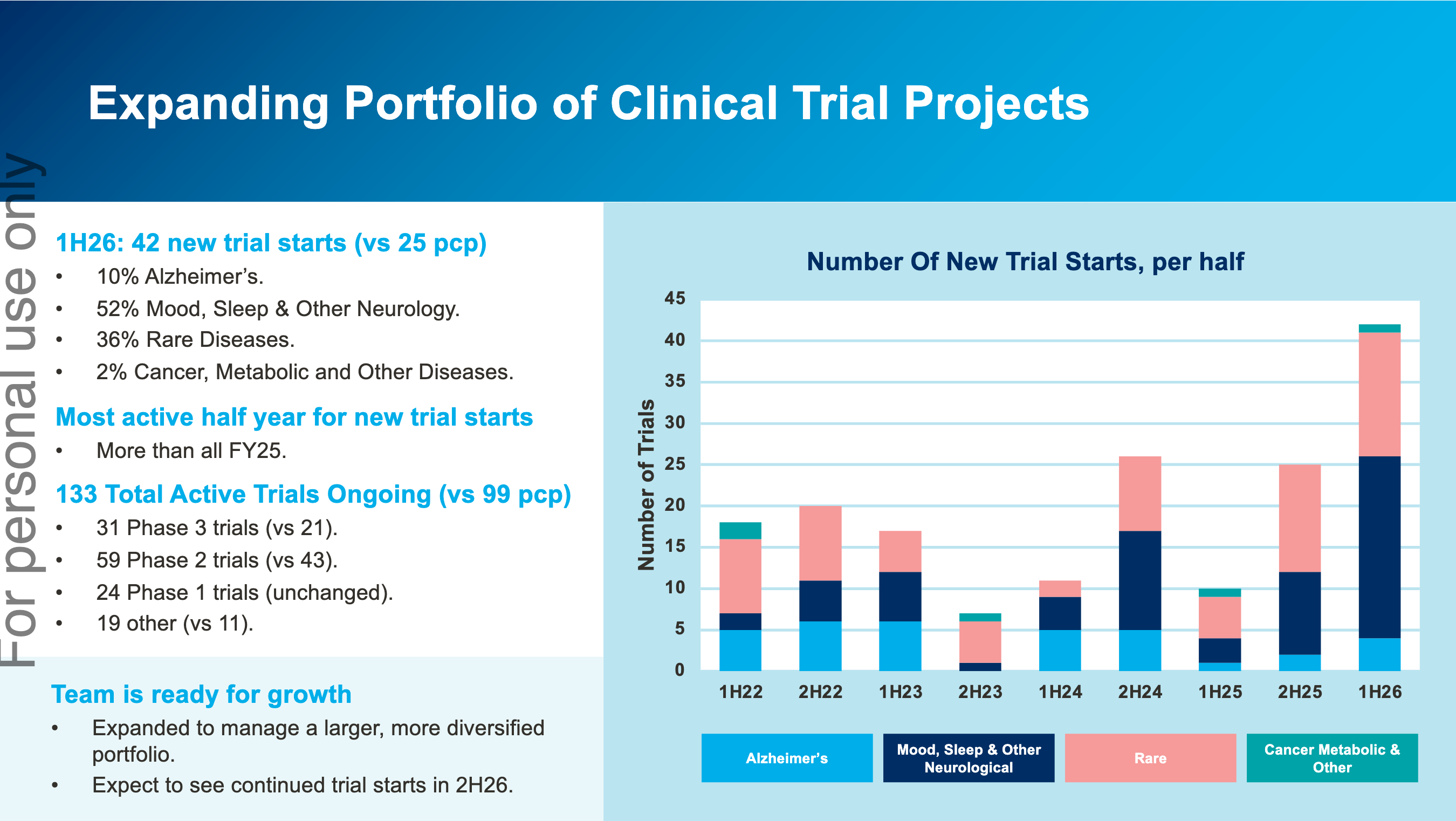

It was a great set of results for FY25. Though much of it was pre-announced in an earlier trading update, so there were no surprises. 2H was significantly stronger with $27.9m revenue and $8.1m EBIT. A notable shift from prior years is the growing share of smaller clinical trial wins, which provide faster turnarounds and earlier revenue recognition.

In the past, Cogstate has hinted that channel partnerships (with groups like ERT or Clario) could help drive sales. It now looks like they’ve found the real deal in Medidata - a major electronic data capture company with 4,000+ staff and roughly 800 salespeople. The partnership is still in its infancy: the sales team only began ramping up in February 2025, yet proposals involving Medidata already represent around 20% of Cogstate’s pipeline. With Medidata’s far deeper reach into clinical trials, Cogstate is accessing a broader range of opportunities than it could on its own. Management has made it clear this is only the beginning, with expectations of further pipeline growth and contract wins as the joint approach matures.

We’re also beginning to see the benefits of the April 2024 licensing amendment with Japanese pharma giant Eisai, which returned global rights to Cogstate’s assessment technology. That technology is now being used to help pharma companies pre-screen patients for clinical trials - an application that generated $1.2m in FY25 revenue, with more opportunities of this kind already in the pipeline.

It’s been a tough stock to hold over the years, largely because Cogstate has been so reliant on a small number of large phase 3 Alzheimer’s trials. The scarcity of these large deals, combined with their inherent lumpiness and the impact of patient recruitment delays, has led to significant year-to-year swings in the company’s performance.

All of a sudden, the outlook looks much brighter. The business is diversifying beyond Alzheimer’s into areas like rare disease, sleep disorders, and Parkinson’s - smaller trials that are quicker to secure and faster to recognise revenue from, smoothing out the historic lumpiness. Medidata is now driving meaningful RFP flow and opening doors into new indications. Cogstate has also began monetising its consumer-facing technologies for patient recruitment, with scope to expand into further use cases. Importantly, the upside from large phase 3 Alzheimer’s trials remains intact, with a number of big pharma companies currently progressing phase 2 programs.

Management have suggested revenue growth is once again expected in FY26, but with the shortened sales cycles and revenue recognition, no specific numbers have been given. Also expect a modest margin decline (~0-3 percentage points on EBITDA/EBIT) due to increase investments. They’re off to a strong start with $14.1m of contract revenue banked since June 30. A maiden $0.02/share fully franked dividend was also declared.

One could make the case that it’s a very reasonably priced company with an EV/E of 15x (annualise 2H performance), that’s more self-reliant than it has previously been (broader beyond AD, stronger channel-partner leverage, and a faster cadence of smaller contracts), with some tremendous tailwinds (pursuit of AD treatments, pharma chasing earlier stages of AD that require more sensitive endpoints, etc). Ultimately, this is only for investors that have belief in the long-term tailwinds and willing to ride the bumps and grinds - this is not your grandad’s SaaS company adding incremental ARR every year.

Not a huge surprise, but good news nevertheless.

Hopefully in the eyes of pharma companies and biotechs this helps de-risk the development of future Alzheimer’s treatments, and in turn increase the demand for Cogstate’s clinical trial products and services. This is the main bull case of the FDA approval for CGS.

Apart from the financial strain to the US government (US$26.5k per year for the treatment), other key concerns involve the strain of the demand to the medical system. PET scans, genetic tests, neurologists, the laborious administration by intravenous infusion every 2 weeks, and so forth.

Cogstate may stand to benefit in a couple of ways. One is the likely follow up clinical trials for Leqembi, and other likely FDA approval candidates, to use less laborious administration of the drug. Perhaps longer intervals or subcutaneous injections instead of infusion.

Two, in order to qualify for Leqembi, prospective patients will need to have cognitive tests completed and submitted to centralised registries. A low-touch digital test would help ease the load on the medical system by opening up the pool of healthcare professionals that can administer them. No doubt Eisai and Cogstate are hoping their upcoming digital apps will play a large role in this.

I've put together this graph to better visualise the contracted clinical revenue (which is 90% of the business) over time. As you can see, FY23 and FY24 contracted revenues are tracking well ahead at similar stages to prior years

The CEO mentioned on the conference call that he believes the tailwinds from the Aduhelm approval have yet to kick in.

So hopefully when it does...

There's been talk on Cogstate's valuation - how it's high and has a lot of the direct to consumer/doctor upside priced in.

I actually think the opposite is true - the valuation is very reasonable on the clinical trials business alone.

Right as of this moment, the company has more clincial trial contracted revenue in FY22 (USD$30.5m) and FY23 (USD$29.5m) than recorded in FY21. Through the last set of presentations, management is pretty much guiding $47-$55m group revenue (+48-74% growth) with no upside from the Healthcare segment. It's growing very quickly, and there's more visibile than ever.

I've included a "cohort" chart of contracted clinical trial revenues, and how it grows over the years. FY22 and FY23 numbers are of course my own forecasts. The assumptions in my opinion are quite balanced. All numbers are in USD.

On these numbers the company is currently trading at FY23 4.2x sales and 13x EV/EBIT. Again zero upside on the direct to consumer/doctor healthcare segment is built in.