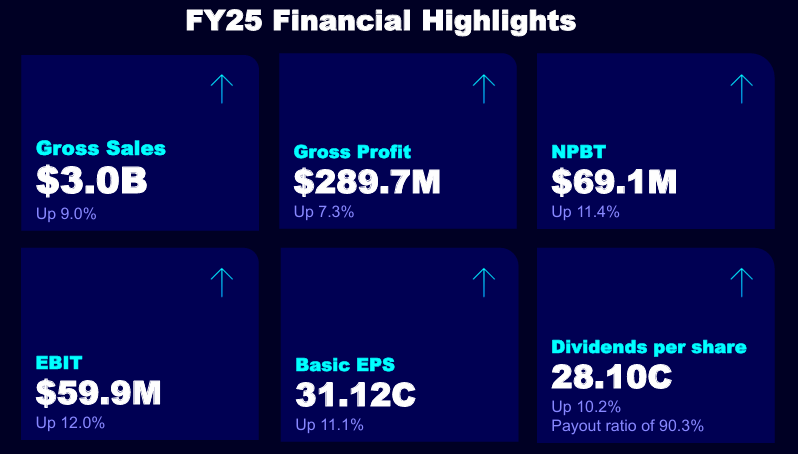

Data #3 reported earnings yesterday. From their presentation:

Overall a solid result given some small sector headwinds which they have mentioned at previous reports. Continued EPS and DPS growth proving that their business is maybe more resilient rather than cyclical.

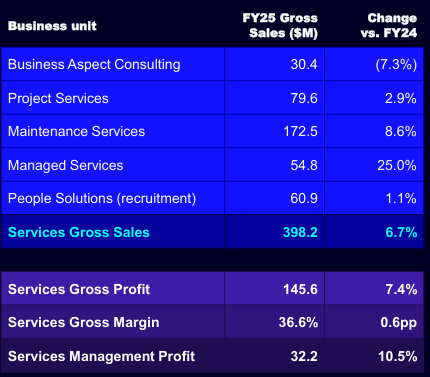

Good growth in the managed services division which is their higher margin segment offset some difficulties in the consulting segment impacted by QLD state election.

No specific guidance was given which is normal at FY results, there is usually a small guidance given at the AGM. They did mention that some headwinds in 1H will be offset in the 2H which may indicate that FY26 could be more of a flat result YOY? Will have to watch how the year plays out.

Overall still happy to hold.

Disc: Held IRL and on Strawman.

Data #3 Limited (DTL) Reported 1H FY25 results this morning.

From their presentation:

A solid result despite some headwinds that have been previously disclosed. Continued strong growth in higher margin Services sector of the business.

No specific guidance given for the remainder of FY25 although as seasonal, sales peak in May/June which usually leads to a stronger 2H result.

Overall I thought this was a solid result albeit maybe showing growth may be slowing although overall sector tailwinds should be strong with continued IT spend. Will watch to see if services can continue to grow allowing for a more stable revenue base which should alleviate any fears of this being too cyclical.

Disc: Held IRL and on Strawman.

This was announced at the AGM a few days ago, long time CEO and MD Laurence Baynham is stepping down from his position and will be replaced by Brad Colledge who is the current Executive General Manager of Software Solutions, Infrastructure Solutions and Services.

The transition will occur over a 4 month period with Brad formally stepping into the role on March 1 2024.

Guidance for 1H FY24 was also given at the AM with expected NPBT to come in between $27m-29m:

I've updated my chart below showing the earnings growth over the last 5 years:

If they meet midrange of guidance then this represents growth of around 13% to pcp.

As expected, H2 will be the stronger half and management did state that they expect to have overall earnings growth, although the level of growth may not be as large as previous years. Nonetheless this remains a solid company with good growth prospects.

AGM meeting address here

Disc: Held IRL and on Strawman.

Data #3 (DTL) released their results. From their presentation:

The market has not liked their results giving them a 15%+ sell off.

By my estimates, 2H profit which has often been very strong compared to 1H missed by around 5% (I had them growing NPAT by around 15% compared to 2H FY22, they grew by only 10%). I suspect this is the reason for the sell off today. Overall NPAT was still up by 22.4% which was on the back of strong growth in the 1H of the year.

The breakdown of revenue by sector was interesting. The increase in higher gross margin sectors had an overall increase in the gross profit and net profit margins for the business. As this increases further we may see less seasonality in the overall profit timing for the business. The increase in gross profit margins is also pleasing given the relatively low overall margins that DTL runs on.

Cash flow seasonality was as usual with a high cash balance at June 30 reflecting the increased receipts prior to the end of the FY. The next half will be the one to watch in terms of working capital concerns as stated in my straw from 1H FY23. As long as they can receive cash from their customers quickly enough to pay off their payables I don't think there should be any concerns. Management of their cash flows has always been solid so I'll give them the benefit of doubt for now.

Overall I think this result was solid even though profit was a slight miss in the 2H. Will likely adjust my valuation down slightly but don't see any reason to sell as yet. May even look to add with the current share price weakness.

Disc: Held IRL and on Strawman.

Data #3 Limited released their 1H FY23 result today. Results were basically as expected as they had pre-released unaudited results about a month ago.

From their presentation:

NPBT came in just under their top end of guidance as expected with another record half.

Once again management stated that profit would likely be skewed again towards the 2nd half of FY23. I don't expect 2H FY23 to have another 38.1% increase on PCP like 1H but if they increased on the previous half by 20% then 2H FY23 NPBT would come in at around $31m giving full year NPBT of around $55.6m. EPS for the full year would be around $0.25 giving DTL a fwd PE of around 29x.

Probably the only thing I'm keeping an eye on is the cash position of the business. DTL typically operate on a short of negative working capital basis and so the timing of cash receipts is usually elevated around the FY year end (May, June). Operating cash flow is very often negative for the 1H as a result of this as evidenced in the current report (operating cash outflow of $88m). However in the last few years, full year operating cash flow has also been negative and the cash balance has decreased down to a level not seen since Dec 2019. With increasing supply chain issues, the company has stated that cash flow collection has slowed to around 33 days (up from around 27 days) and inventory is inflated but will be allocated to non-cancellable orders. The below chart from the presentation shows the slow increase in the working capital requirements of the business. If working capital goes above cash, will DTL be able to fund its operation? Something to look out for in the next half. I expect management to be able to work through this issue as shown in the past.

I will maintain my valuation at $6.20 as a potential top-up price.

Disc: Held IRL and on Strawman.

Sorry been on holidays and just catching up on announcements now.

DTL gave an update last week that they would achieve NPBT on the top end of their guidance for 1HFY23. This would be around $25m NPBT for the half representing a 37% increase compared to 1HFY22.

Part of this increase was due to the backlog at the start of the half from supply chain constraints although they did mention that the backlog would be ongoing going into the next half due to increase volume of business.

I have updated my chart to reflect this announcement.

Assuming 2HFY23 will be similarly strong (20% increase on pcp) we can expect NPBT of around $55m for the full year. This would equate to around $38.5m of NPAT for the full year. At the current share price the PE is around 28.5x.

It will be interesting to see if this trend of EPS growth continues. As was discussed on the Baby Giants Podcast, IT consulting is usually quite a low margin business and highly acquisitive. DTL seem to have bucked the trend and have grown organically quite well in the last few years. If we end up going into a recession will IT spending be slowed? Difficult to tell however being the dominant player in Australia bodes well for DTL.

Will update my valuation shortly to reflect this announcement.

Disc: Held IRL and on Strawman.

Data 3 limited (DTL) held their AGM today and released an outlook for the 1st half of FY23:

Taking the midrange of guidance would equivalate to around 24% growth to NPBT. This does include a backlog of $6m which could not be invoiced in FY22 due to supply constraints (normal backlog is around $3m). Management did mention that they would once again be heavily skewed towards 2H of the FY as is seasonal so to achieve good growth in the 1H is a good result.

Updated chart below of trending NPBT. Note the FY23 figures are estimates.

Disc: Held IRL and on Strawman

Data #3 Limited (DTL) release their FY22 results today. From their release:

- Revenue = 2.19b (up 12% YOY)

- NPAT = $30.26m (up 19.1% YOY)

- Final Dividend of 10.65c bringing the final dividend to 17.9c for the year (up from 15c in FY21)

Not much news considering they released a market update around a month ago. They have continued to avoid giving guidance for FY23 given supply chain issues and other covid related disruptions however they did mention that there was a backlog of $6m of NPBT that will be realised in 1H23.

Some charts given from their results presentation.

I also found it interesting that they are changing their revenue mix with increasing high gross margin revenue.

This may help with profitability in the long term and already shows with increasing profit compared to increase in revenue.

Disc: Held on Strawman and IRL

Thought I'd take a look at this company following their announcement yesterday regarding 1H22 result.

DTL expect a 30% increase in NPBT compared to 1H21 which would be approximately $18.1m. This just above their top end of guidance. Management did mention that 1H22 would be a good half due to the backlog at the end of FY21.

Reading back through their past results, DTL usually have markedly more activity in the backend of the year as shown in the below graph so the large increase in profit for the 1H is definitely encouraging.

I have assumed only slight growth for 2H22 which would bring their total NPBT for FY22 to around $42m. NPAT would therefore come in at around $29.5m.

At the current share price this represents a forward PE of around 32x.

In the past 4 years DTL have averaged NPAT growth of 20% PA although there has been a slow down in FY21 (may be related to COVID). FY19 and 20 NPAT growth was 28% and 32% respectively. At my calculated NPAT for FY22, growth was around 16%.

Obviously if DTL can recover their NPAT growth back to FY19 and 20 rates then the current share price is very attractive however I find it very hard to determine if this is possible. DTL, whilst are profitable, operate a very low margin business with net margins around 2%. Therefore they would need to increase revenue markedly in order to be able to increase their NPAT at rates above 20%.

I will look at this company again following their full year 22 results to see if their second half of the year can continue the momentum of the first half.

Disc: Not held IRL or on Strawman.