Consensus community valuation

Update 26/08/2025

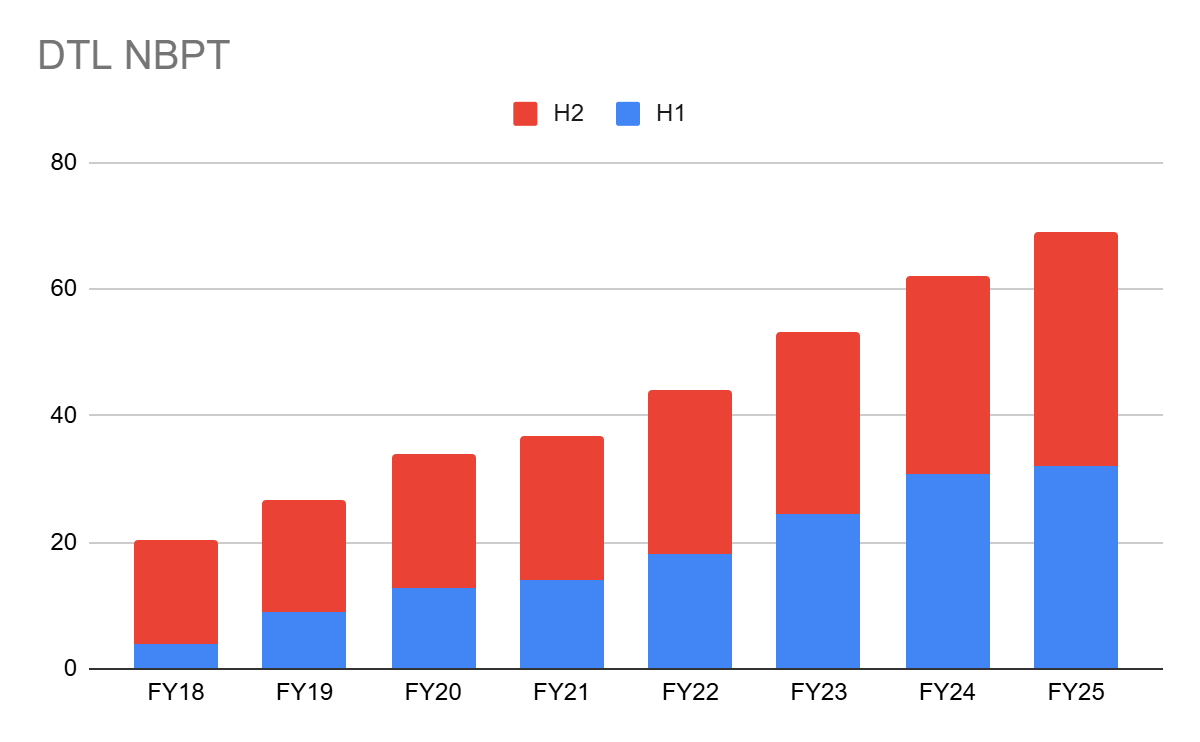

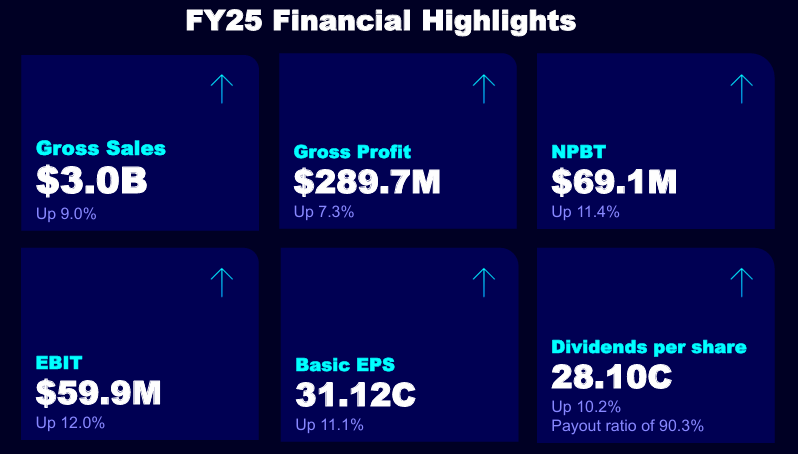

Updating based on FY25 results.

- NPBT = $69.1m

- NPAT = $48.2m

Updated chart below:

2H coming through similar to the trend in previous years of being the stronger half.

Will keep the valuation at 25x PE which gives a valuation of $7.78. Although Management did mention some potential headwinds going into 1H FY26 which if the result shows it being flat could show some risk to the share price

Disc: Held IRL and on Strawman.

Update 22/08/2024

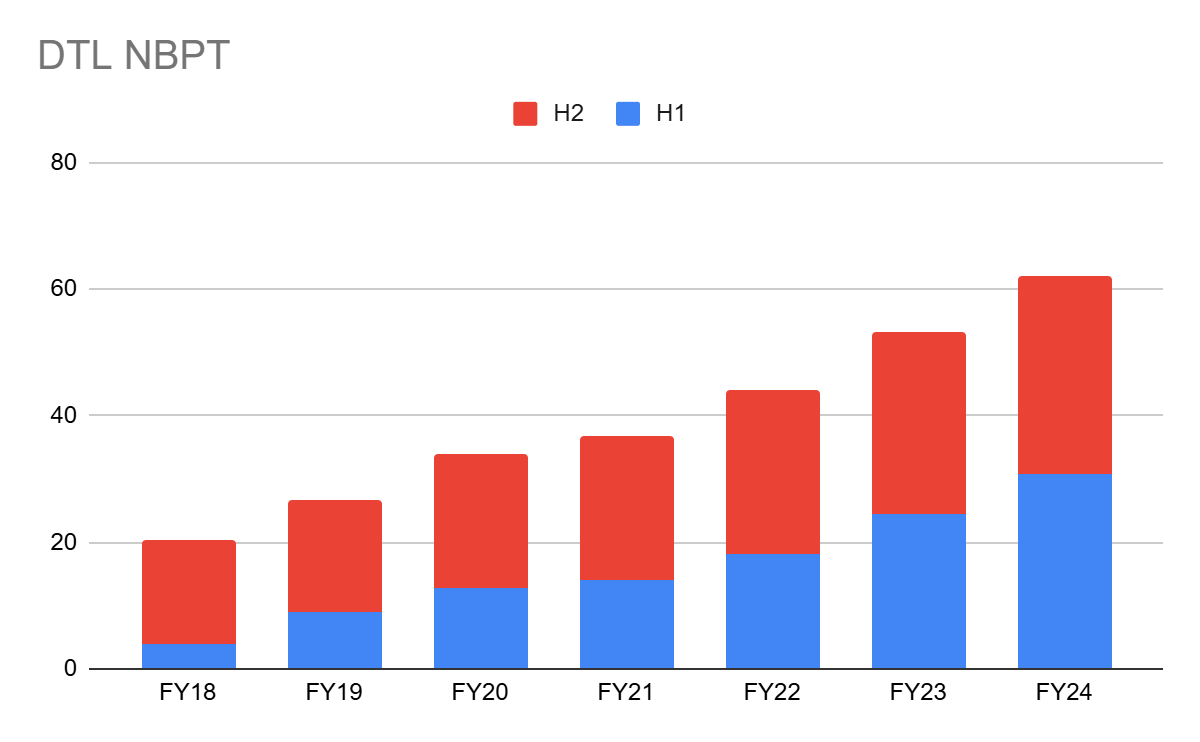

Updating based on FY24 results.

- NPBT = $62.1m

- NPAT = $43.3m

Updated chart below:

Must say that I was quite surprised by the market's reaction yesterday. I agree that the performance was ok given tough economic conditions but potentially shows the cyclicality involved in this industry.

The 2H FY24 was quite weak given that management have mentioned that their sales cycle usually peaks in May and June however NPAT was basically flat compared to 1H FY24.

Using a 25x PE on EPS of 28cps, gives a valuation of $7.

Disc: Held IRL and on Strawman.

Update 15/02/2024

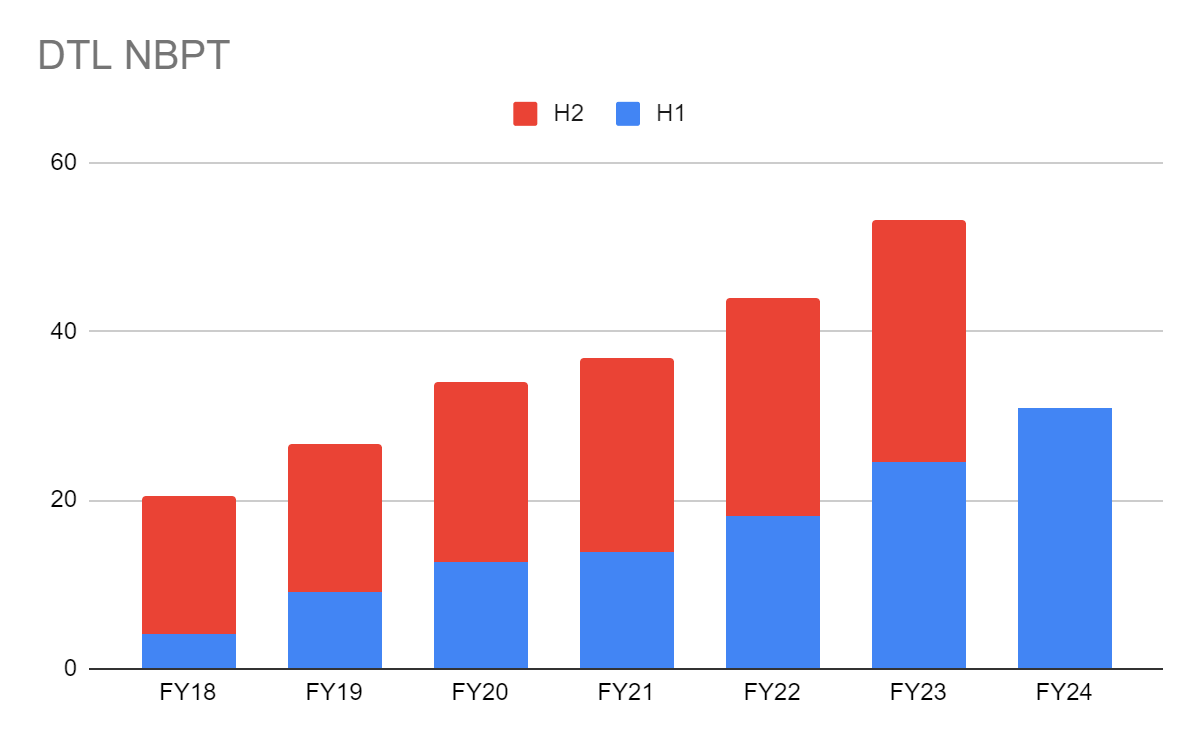

Updating based on 1H FY24 results.

- NPBT = $30.8m

- NPAT = $21.4m

Updated chart below:

Based on historic seasonal strength in 2H, I'll assume around $45m NPAT for the full year.

25x fwd PE would give a valuation of around $7.27.

Disc: Held IRL and on Strawman.

Update 22/08/2023

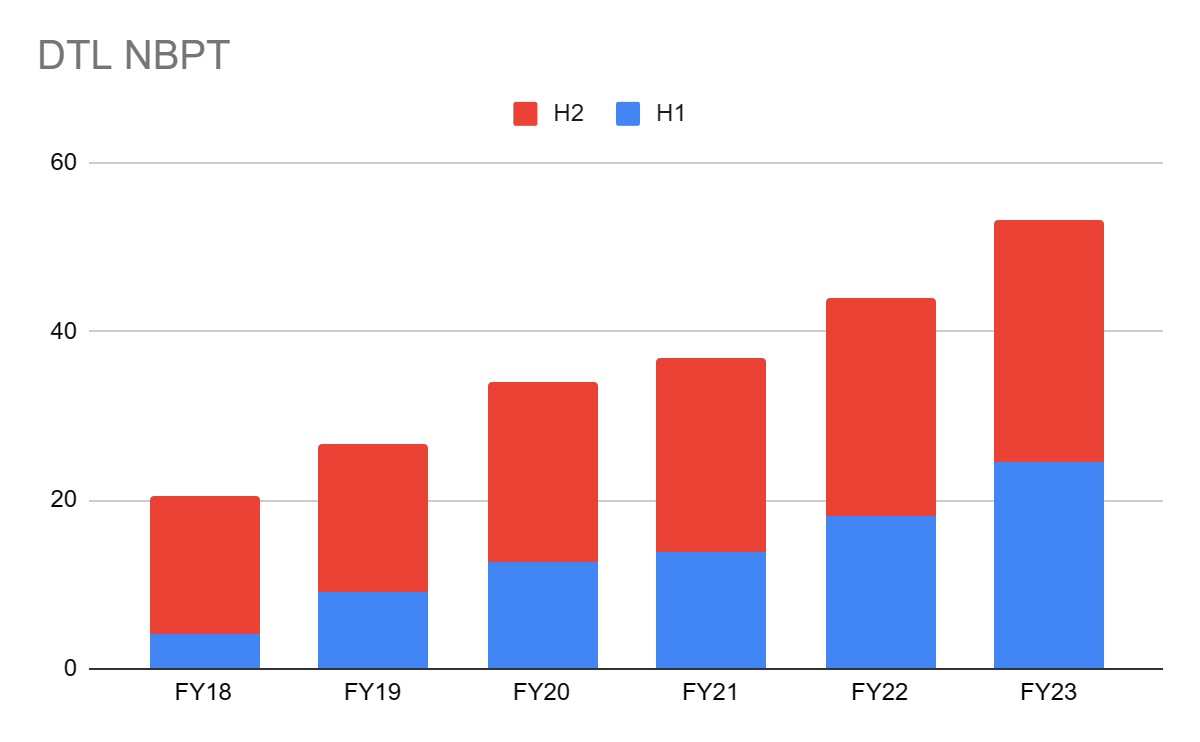

Updating based on FY23 results. Below is the graph of their NPBT results.

Maintaining a 25x PE on the current set of numbers, gives me a valuation of $5.98.

I think I will likely top up at around $6.

Disc: Held IRL and on Strawman.

Update 20/01/2023

More of a target buy price to top up my current holdings. A 25x PE would equate to a share price around $6.20.

$6.20 is also the valuation for DTL assuming 15x EPS growth for 5 years and discounting back 10%pa.

Disc: Held IRL and on Strawman

Update 14/07/2022

DTL are reporting NPBT of $44m for FY22. NPAT ~$30.36m

$5.75 valuation would give a fwd PE of ~30x

For a company that has grown NPAT YOY by 19% this isn't too demanding IMO

Disc: Held IRL and on Strawman

Original Report

Assuming NPAT of $29.5m for FY22 (See my Straw)

PE of 30x = 885m MC

SOI = 154.3m

Valuation = $5.75

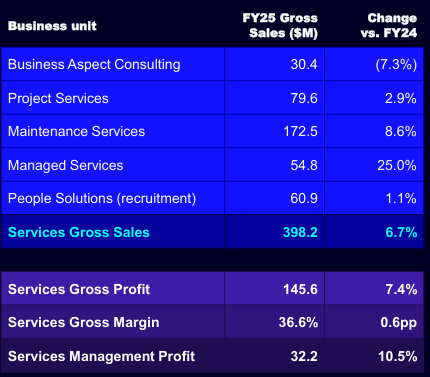

Data #3 reported earnings yesterday. From their presentation:

Overall a solid result given some small sector headwinds which they have mentioned at previous reports. Continued EPS and DPS growth proving that their business is maybe more resilient rather than cyclical.

Good growth in the managed services division which is their higher margin segment offset some difficulties in the consulting segment impacted by QLD state election.

No specific guidance was given which is normal at FY results, there is usually a small guidance given at the AGM. They did mention that some headwinds in 1H will be offset in the 2H which may indicate that FY26 could be more of a flat result YOY? Will have to watch how the year plays out.

Overall still happy to hold.

Disc: Held IRL and on Strawman.

Base case Valuation

1/ starting eps: $0.30 grows at 8%pa computed below:

Best case 'bullish' Valuation by Macquarie article via Motley fool -

Data3# posted gross sales of $2.8 billion for FY24, up 7.6% on the previous year.

That saw the company report a gross profit of $270.1 million for the financial year, an increase of 7.8% on FY23's result.

Where to next?

Macquarie has a price target of $9 on Data#3 shares.

That represents a potential total shareholder return of 24% over the next 12 months.

The broker is expecting Data#3 to steadily increase profits over the coming years.

The IT company's gross profit is forecast to grow to over $350 million for FY27.

In the near term, Macquarie expects Data#3's business to benefit as cloud migration and AI adoption continues.

Demand for Data#3's services will further increase as customers require support when Windows 10 reaches its end-of-life date in October, according to the broker.

*so Macquarie are targeting an eps growth of 24%pa ..which is very attainable.

Data #3 Limited (DTL) Reported 1H FY25 results this morning.

From their presentation:

A solid result despite some headwinds that have been previously disclosed. Continued strong growth in higher margin Services sector of the business.

No specific guidance given for the remainder of FY25 although as seasonal, sales peak in May/June which usually leads to a stronger 2H result.

Overall I thought this was a solid result albeit maybe showing growth may be slowing although overall sector tailwinds should be strong with continued IT spend. Will watch to see if services can continue to grow allowing for a more stable revenue base which should alleviate any fears of this being too cyclical.

Disc: Held IRL and on Strawman.

Fundamentals ROE 57.8 great profitability, EPS 28c up17%

% Outlook Optimistic for 2025

See how the 'market' reads / reacts to this report.

Outlook no Quantitative # projections here. But DTL are Optimistic :

We are expecting to see continued momentum in As-aService and recurring revenue solutions through FY25, ensuring customers have access to different consumption approaches. Demand for end user devices will be driven by the need to support Windows 11, and AI-enabled edge, in addition to postcovid refresh cycles.

Our Device as a Service offerings gained momentum in FY24, and we see this continuing into FY25.

Our Security practice will only strengthen as customers are challenged by ongoing cyber threats, in addition to security related challenges presented by their gradual adoption of AI.

Cloud and data centre will likely see growth in response to security and data concerns, and in determining how AI is best utilised in the right location for workloads and use cases.

Sustainability will be a focus as customers navigate the increase in AI-enabled infrastructure, which can potentially be high in its environmental footprint. Vendors such as Microsoft and HP who are leading the way in sustainability practices will be an important influence on customer decision making

There is some optimism that the challenging trading conditions caused by a highly inflationary and high-interestrate economic environment will ease early in calendar year 2025, resulting in improved consumer sentiment and a return to more normal levels of sales growth. Investments by the Public Sector in new infrastructure projects should also help to grow our pipeline across all lines of business.

The foreseeable risks (and any available mitigants) to achieving our short to medium-term financial growth aspirations, specific to Data # 3 and in addition to the general macro-economic risks that would impact most organisations, include the following:

• Major changes to customer and reseller sales strategies and vendor incentive programs that would negatively impact future profitability. Mitigant: Data # 3 works closely with vendors to stay abreast of any potential changes and adapts sales strategies and vendor management processes accordingly.

• Access to skilled technology labour to enable us to deliver contracted work and achieve growth in areas of strategic focus. Mitigant: Our talent attraction and retention policies, including staff benefits and people development initiatives.

• Any negative geopolitical influence on the region or supply chains. Mitigant: We work with vendors to expedite deliveries (where possible), utilise distributors with available stock, and provide customers with ongoing updates, as evidenced with the pandemic-related supply chain challenges.

• Delayed decision making due to state government elections. Mitigant: We work with Agencies in the lead up to the election to ensure customer requirements have been addressed prior to lock down periods and again after an election to ensure any technology requirements for Machinery of Government Changes are addressed.

• Government change in policy with regards to the use of contractors. Mitigant: We provide both contract resources and outcome-based project offerings. While some governments may prefer to reduce contractors in preference of employing full time staff, the limited access to skilled resources means outcome-based projects are still a solution for public sector customers

Return (inc div) 1yr: 12.95% 3yr: 16.75% pa 5yr: 25.67% pa

JP Morgan Research note from February 2024

Been a volatile period for holders and the below explains the factors quite well.

Tempting to add at the lows but I always get distracted by some other shiny new thing now and then.

[held]

52 Week high today

Checking the investor day presentation , apart from having the MD for Microsoft Australia as guest speaker, the word "AI" was mentioned several times on the 15 November call from the new CEO

The CFO Cherie O'Riordan also mentioned focusing less on margins and more on improving profitability. They believe by not growing gross margins, Data#3 will be more competitive in winning new business and hence increase profitability.

Data#3 also mentions they are able to still pass price and wage inflation into their customer contracts. Several measures mentioned include:

- Reseller agreements that allow the company to pass price increases to the customer

- Professional services contracts being more time and materials based while managing fixed price contracts

- Periodic price reviews of managed services contracts

Finally for Working capital, they have no issues with drawing down this component as it is mostly current and there is a low default rate from customers

Lots to unpack from the call transcript so above is just a summary of the main points..

There was also a special call today which I do not have access to the transcript so not sure who was invited here.

Note: I've been cashing on the dividend reinvestments in SRL only. If only I bought more during that mini crash months back.

[held]

This was announced at the AGM a few days ago, long time CEO and MD Laurence Baynham is stepping down from his position and will be replaced by Brad Colledge who is the current Executive General Manager of Software Solutions, Infrastructure Solutions and Services.

The transition will occur over a 4 month period with Brad formally stepping into the role on March 1 2024.

Guidance for 1H FY24 was also given at the AM with expected NPBT to come in between $27m-29m:

I've updated my chart below showing the earnings growth over the last 5 years:

If they meet midrange of guidance then this represents growth of around 13% to pcp.

As expected, H2 will be the stronger half and management did state that they expect to have overall earnings growth, although the level of growth may not be as large as previous years. Nonetheless this remains a solid company with good growth prospects.

AGM meeting address here

Disc: Held IRL and on Strawman.

Data #3 (DTL) released their results. From their presentation:

The market has not liked their results giving them a 15%+ sell off.

By my estimates, 2H profit which has often been very strong compared to 1H missed by around 5% (I had them growing NPAT by around 15% compared to 2H FY22, they grew by only 10%). I suspect this is the reason for the sell off today. Overall NPAT was still up by 22.4% which was on the back of strong growth in the 1H of the year.

The breakdown of revenue by sector was interesting. The increase in higher gross margin sectors had an overall increase in the gross profit and net profit margins for the business. As this increases further we may see less seasonality in the overall profit timing for the business. The increase in gross profit margins is also pleasing given the relatively low overall margins that DTL runs on.

Cash flow seasonality was as usual with a high cash balance at June 30 reflecting the increased receipts prior to the end of the FY. The next half will be the one to watch in terms of working capital concerns as stated in my straw from 1H FY23. As long as they can receive cash from their customers quickly enough to pay off their payables I don't think there should be any concerns. Management of their cash flows has always been solid so I'll give them the benefit of doubt for now.

Overall I think this result was solid even though profit was a slight miss in the 2H. Will likely adjust my valuation down slightly but don't see any reason to sell as yet. May even look to add with the current share price weakness.

Disc: Held IRL and on Strawman.

Data #3 Limited released their 1H FY23 result today. Results were basically as expected as they had pre-released unaudited results about a month ago.

From their presentation:

NPBT came in just under their top end of guidance as expected with another record half.

Once again management stated that profit would likely be skewed again towards the 2nd half of FY23. I don't expect 2H FY23 to have another 38.1% increase on PCP like 1H but if they increased on the previous half by 20% then 2H FY23 NPBT would come in at around $31m giving full year NPBT of around $55.6m. EPS for the full year would be around $0.25 giving DTL a fwd PE of around 29x.

Probably the only thing I'm keeping an eye on is the cash position of the business. DTL typically operate on a short of negative working capital basis and so the timing of cash receipts is usually elevated around the FY year end (May, June). Operating cash flow is very often negative for the 1H as a result of this as evidenced in the current report (operating cash outflow of $88m). However in the last few years, full year operating cash flow has also been negative and the cash balance has decreased down to a level not seen since Dec 2019. With increasing supply chain issues, the company has stated that cash flow collection has slowed to around 33 days (up from around 27 days) and inventory is inflated but will be allocated to non-cancellable orders. The below chart from the presentation shows the slow increase in the working capital requirements of the business. If working capital goes above cash, will DTL be able to fund its operation? Something to look out for in the next half. I expect management to be able to work through this issue as shown in the past.

I will maintain my valuation at $6.20 as a potential top-up price.

Disc: Held IRL and on Strawman.

Data 3 limited (DTL) held their AGM today and released an outlook for the 1st half of FY23:

Taking the midrange of guidance would equivalate to around 24% growth to NPBT. This does include a backlog of $6m which could not be invoiced in FY22 due to supply constraints (normal backlog is around $3m). Management did mention that they would once again be heavily skewed towards 2H of the FY as is seasonal so to achieve good growth in the 1H is a good result.

Updated chart below of trending NPBT. Note the FY23 figures are estimates.

Disc: Held IRL and on Strawman

Data #3 Limited (DTL) release their FY22 results today. From their release:

- Revenue = 2.19b (up 12% YOY)

- NPAT = $30.26m (up 19.1% YOY)

- Final Dividend of 10.65c bringing the final dividend to 17.9c for the year (up from 15c in FY21)

Not much news considering they released a market update around a month ago. They have continued to avoid giving guidance for FY23 given supply chain issues and other covid related disruptions however they did mention that there was a backlog of $6m of NPBT that will be realised in 1H23.

Some charts given from their results presentation.

I also found it interesting that they are changing their revenue mix with increasing high gross margin revenue.

This may help with profitability in the long term and already shows with increasing profit compared to increase in revenue.

Disc: Held on Strawman and IRL

Thought I'd take a look at this company following their announcement yesterday regarding 1H22 result.

DTL expect a 30% increase in NPBT compared to 1H21 which would be approximately $18.1m. This just above their top end of guidance. Management did mention that 1H22 would be a good half due to the backlog at the end of FY21.

Reading back through their past results, DTL usually have markedly more activity in the backend of the year as shown in the below graph so the large increase in profit for the 1H is definitely encouraging.

I have assumed only slight growth for 2H22 which would bring their total NPBT for FY22 to around $42m. NPAT would therefore come in at around $29.5m.

At the current share price this represents a forward PE of around 32x.

In the past 4 years DTL have averaged NPAT growth of 20% PA although there has been a slow down in FY21 (may be related to COVID). FY19 and 20 NPAT growth was 28% and 32% respectively. At my calculated NPAT for FY22, growth was around 16%.

Obviously if DTL can recover their NPAT growth back to FY19 and 20 rates then the current share price is very attractive however I find it very hard to determine if this is possible. DTL, whilst are profitable, operate a very low margin business with net margins around 2%. Therefore they would need to increase revenue markedly in order to be able to increase their NPAT at rates above 20%.

I will look at this company again following their full year 22 results to see if their second half of the year can continue the momentum of the first half.

Disc: Not held IRL or on Strawman.