Price History

Premium Content

Premium Content

Premium Content

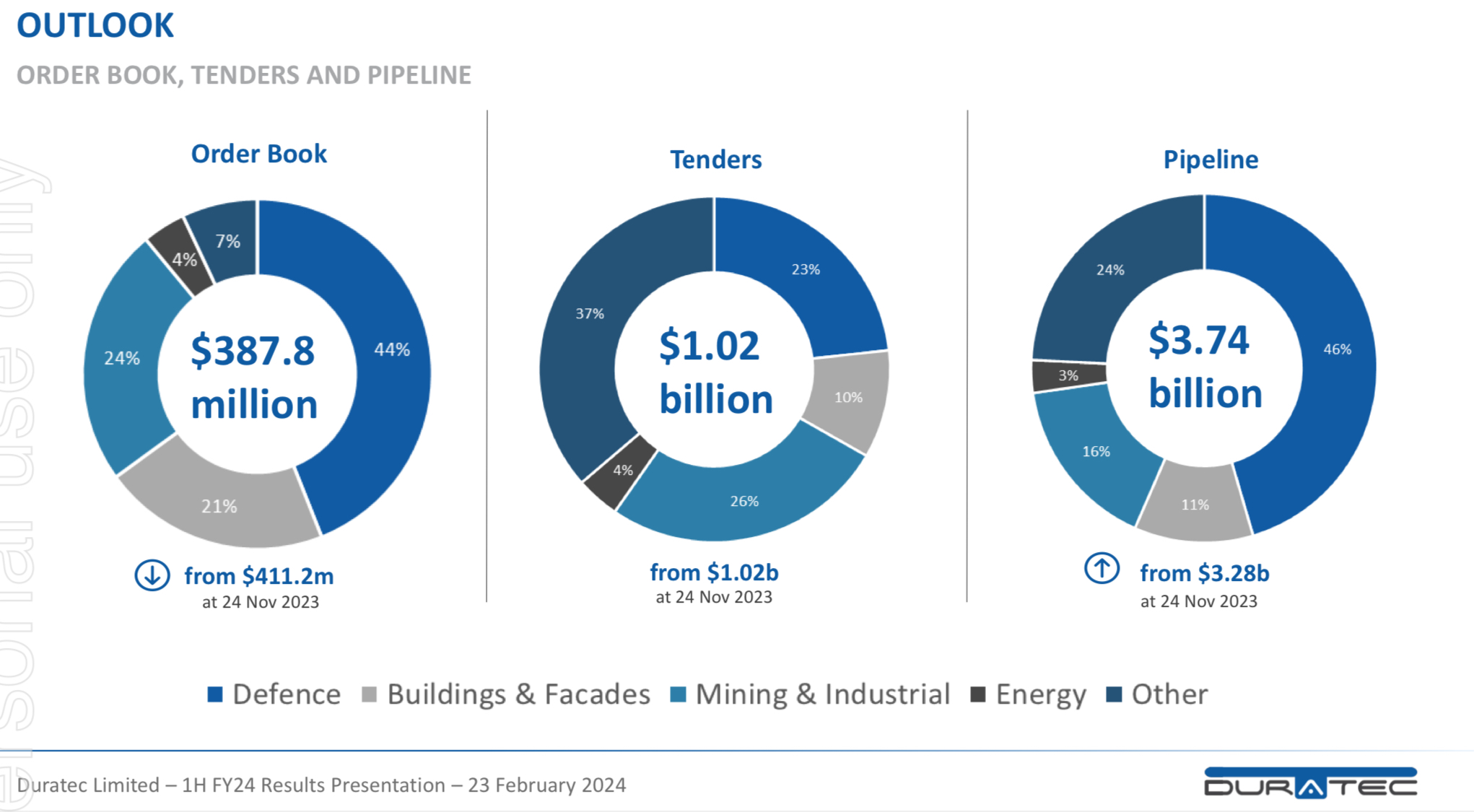

In February this year 44% of Duratec’s order book consisted of Defence projects, and management believes this represents only 1.3% of the total addressable market (TAM) of $17 billion. This was before the Labour government announced additional defence spending over the next decade.

On the 24 November 2023 Duratec’s order book was down 6% pcp. The weaker order book appears to be the main reason for the share price weakness since Duratec announced a record 1H24 result on the 23rd February 2024.

The defence budget is about to receive an additional $5.7 billion per year from this year, and $50 billion more over the next decade, compared with the funding trajectory of the previous Coalition government.

By 2034, annual defence spending will be about $100 billion, hitting 2.4 per cent as a share of the economy. This year’s defence budget is about $53 billion, just over 2 per cent of GDP.

As part of the Defence budget review an additional $1.4 billion will be directed towards upgrading northern bases instead of defence buildings in Canberra.

In the 1H24 presentation Duratec said they were well positioned to capitalise on accelerated defence spend in key regions such as NT and WA. While we haven’t heard any news of project wins from Duratec yet, the stars are starting to align for more defence projects in the NT.

Held IRL (2.6%)

We now have a RL holding in Duratec (2.4%). I probably rushed into this a bit too early given the $388 million order book at 1H24. However, I’m here now, so it’s in my best interests to keep an eye on the pipeline of work. I am hoping to get some insight into what lies ahead to help with decisions for our holding. To help with this I’ve developed a Pipeline to Profit Model (another spreadsheet of course!).

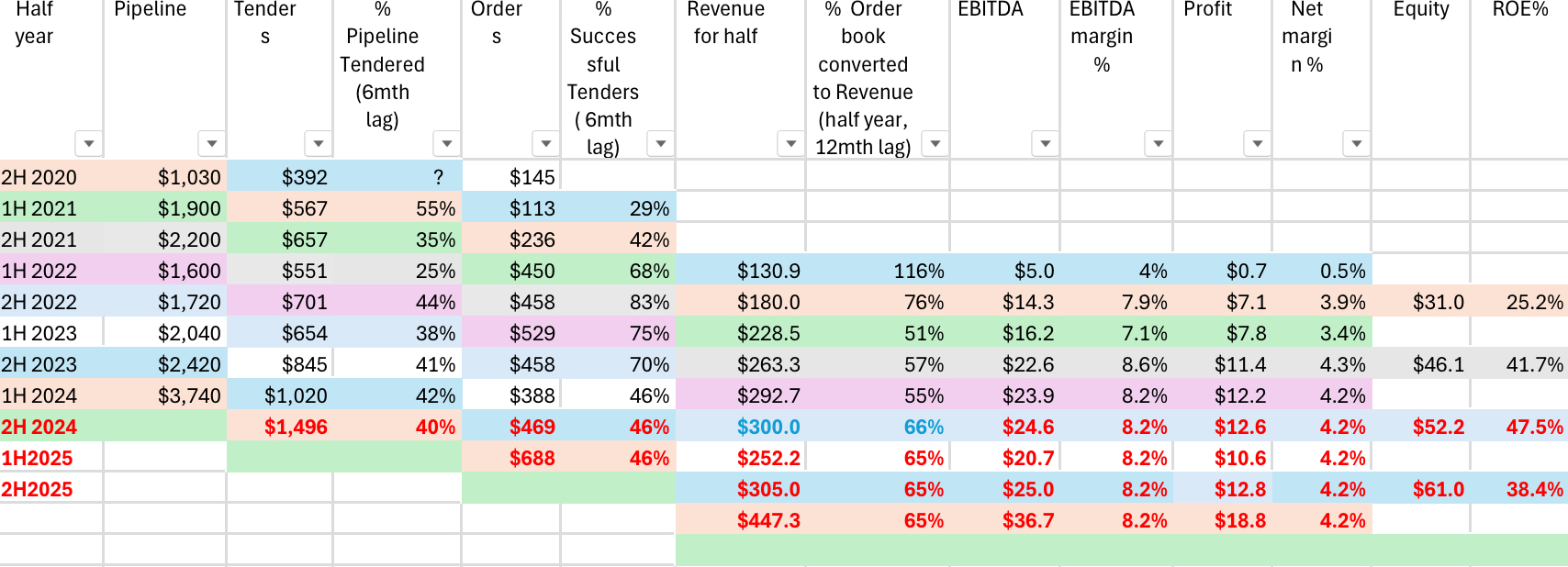

Since listing, Duratec has consistently reported the dollar values for the pipeline of work, tenders and the order book for each half year. They have also reported EBITDA, NPAT and the margins for each. This comprehensive data makes it possible to model the historical dollar flows from pipeline to profit, and to see if there are any relationships that might be useful in forecasting profits. If they were to stop providing this data I think that could be an orange flag.

In the spreadsheet below I’ve modelled the dollars flowing from pipeline to profit assuming average lag times between each stage, noted in the column headers. I’ve assumed lag times of 6 months from pipeline to tenders, 6 months from tenders to order book, and 12 months from order book to revenue. This assumes an average lag time of 2 years from pipeline to profit, which sounds too short, but it will serve to test the model. I think the model could be very rubbery at this stage, but it’s somewhere to start and the aim is to update and improve the assumptions over time.

I’ve colour coded the dollar flows across different stages of the pipeline, and used black text for actual data, blue text for guidance, and red text for forecasts.

Analysing the conversion percentage for each stage in the pipeline, there appears to be some relationships that might be useful in forecasting profit. The conversion from pipeline to tenders ranged from 25% to 55%, narrowing from 38% to 44% over the last 2 years. For forecasting purposes I’ve assumed 40% of the 1H24 pipeline could result in tenders, ie c. $1.5 billion in tenders for 2H2024. Of course the lag times might be out of whack, and that won’t be very useful. Time will tell!

There seems to be more variability in the conversion of tenders to order book (contract wins). The conversion rate increased from 29% to 83% between 1H2021 and 2H2022, and then fell each half to 46% for 1H24. That means less than half of the projects tendered for resulted in a contract. It would appear that Duratec has become more focused on maintaining margins than in winning additional contracts, which is a good thing. Assuming 46% of the tenders would result in contracts, the 2H2024 order book could be c. $470 million.

Conversion of the order book to revenue has ranged from 51% to 66% for each half year. This makes sense as you might expect more than half of the order book would be converted to revenue each half year in the year/s of delivery due to the order book growing (not shrinking?). I’ve assumed 65% of the $388 million 1H2024 order book would be converted to revenue in 1H2025, resulting in 1H2025 revenue falling to c. $250 million. NPAT might be c. $10.6 million using a net margin of 4.2%. Based on this model NPAT could fall from c. $24.8 million in FY2024 to $23.4 million in FY2025 (5.6% lower).

The next update to look out for will be Duratec’s guidance for FY24. Last year this was released on 24 April 2023. We should have an update on the order book within a month, and hopefully it’s up on the $388 million at the 24 November 2023, or that could spell trouble!

Last year the FY23 results all came in at the top end of the upgraded guidance provided in April 23. I like to see this with guidance. I think Duratec is in for a record profit this year, but it’s the order book, the pipeline of profits, the margins and the ROE that we need to be watching.

Click on the photo to view the Duratec 3D model of a Main Roads Timber Bridge. Drag and expand with two fingers. The detail is incredible!

@mikebrisy, I’ve been exploring the Duratec website trying to better understand the services they provide. The whole-of-life asset management service is really interesting.

On the Duratec website I found some interesting information about one of Duratec’s unique services. I can see how these services would be sought after by government and big industry to manage and maintain infrastructure to avoid costly and unnecessary premature deterioration of assets. The following is from their sustainably page on the Duratec website. The detail in the 3D models developed by their engineers is incredible (I wonder if they are client of Pointerra?) Here’s an example of a 3D Model of a Main Roads Timber Bridge. Click on the link and explore the structure. There are other examples in the 3D models link below.

Duratec is a solutions-driven contractor, providing whole-of-life engineering, construction and remediation services.

We work to extend the life of existing assets and infrastructure. In doing so, we help to reduce reliance on the development of new infrastructure. In partnership with our clients, we work to provide long-term, sustainable and intergenerational outcomes whilst considering harsh environmental factors.

With an in-house technical team, one of our unique offerings is our ability to provide condition assessments to determine the level of deterioration and decline, and then develop 3D models of these assets to assess and monitor changes over time.

As a national contractor working across a range of industries, we understand the potential environmental impacts of our work are varied. With this in mind, we work in strict accordance with our Environmental Management System, certified to ISO 14001.

Claude held Duratec until its peak in February 2023, then sold. Perfect timing Claude! What a master!

The reason Claude sold is behind the paywall, so I’m none the wiser. This is one opinion I would hold in very high regard. I’ve joined the waiting list to be a subscriber to “A Rich Life”. I guess I’ll just have to wait until Claude lets me in!

After Claude sold (well I assume he sold) another article appeared in May 2023 regarding upgraded guidance. That’s behind the paywall also. :(

The market has turned bearish on Duratec (DUR) recently. I’ve had it in my watchlist for a while and today I’ve finally added IRL (0.8%). I hope to add more on further weakness. I’m a little late to the party on this one, missing some incredible growth since it listed. However, I still see a lot of potential going forward.

Again, I agree with @Karmast’s reasons for holding Duratec and valuation of $2.20. At the current price of $1.23 I am hoping for an annual return of approx 16% (McNiven’s Formula).

There’s a lot to like about this business, much of which @Karmast has already covered, +40% ROE, low 27% debt on equity, and $58.5 million in cash. Management has provided guidance for record revenue in FY24 (between $570 million to $610 million). I am expecting earnings to be approx 10.4 cps (midpoint of revenue guidance $590 million, 4.37% NPAT margin, NPAT of $25.8 million) which would put Duratec on a FY24 multiple of 11.8x.

If the business can continue double digit earnings growth from here, +40% ROE, while reinvesting 70% of its earnings back into growth, that would make this quality business sound reasonably cheap. While past performance is not an indicator of future performance, the historical revenue growth for Duratec has been very impressive since it was established in 2010. In fact, revenue growth has accelerated since listing in November 2020 at an offer price of $0.50 per share.

More cash than debt (Source: Simply Wall Street)

More cash than debt (Source: Simply Wall Street)

ROE increased to 41.7% in FY23, Expecting +45% in FY24, and circa 40% over the next few years (Chart from Commsec)

Held IRL (0.8%)