Consensus community valuation

Scroll down - latest updates are at the end of this.

09-Feb-2024: I reckon they're close to fair value at current levels (closed today at $1.56 today, and at $1.61 yesterday). People say there is a management premium built in already - as there should be - because it's been earned. However, give this company about three years and they should be a top 7 Australian gold producer in terms of ounces produced p.a. (at over 300 koz per annum) and I have no doubt that unless things really turned pear-shaped for Raleigh, GMD will STILL be one of the top 5 Aussie gold producers in terms of market capitalisation. And my price target at that point would be a minimum of $2.35/share, so that's what I'm going with today, with a three year time frame, so by February 2027.

They could easily overshoot that target, but that's a reasonable target I think.

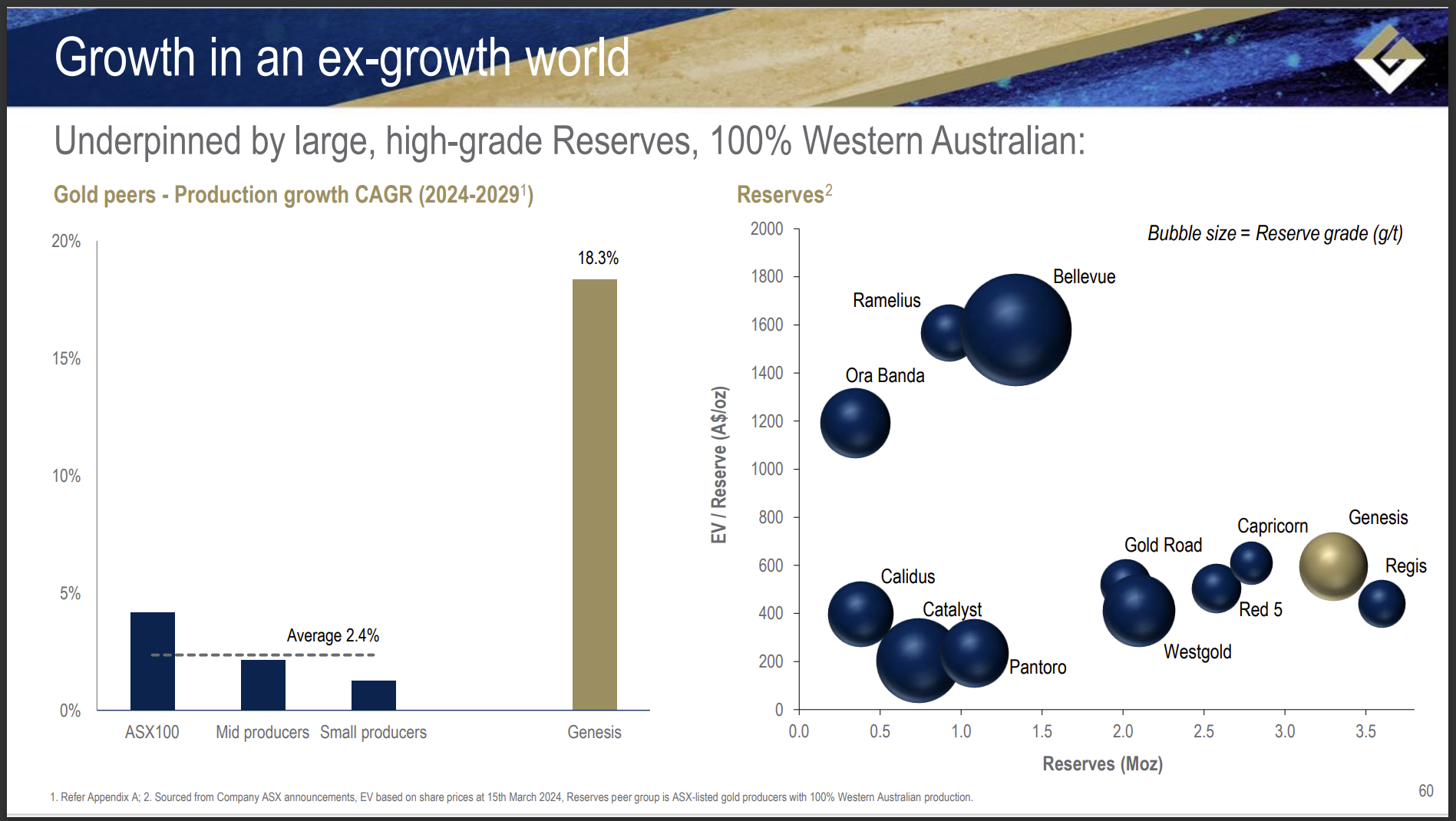

The following three slides are all taken from the recent joint presentation by Red 5 (RED) and Silver Lake Resources (SLR) [Presentation - Red 5 and Silver Lake Resources to Merge 05-Feb-2024] highlighting the benefits of merging the two companies together. I am using slides 7, 10 & 15 from that Presso because they show where all of the main ASX-listed (and Aussie HQ'd) gold producers sit in relation to each other on various metrics.

I have highlighted Genesis Minerals (GMD) in green. In the first slide that shows Gold Production for FY2024), I have shown where they expect to be within the next 3 years (at the left end of that green line) - at over 300 koz Au p.a. (300,000 ounces of gold per annum) [Source: Corporate-Presentation---Ready-set-grow---Assets-and-people-in-place-for-+300koz-p-a-27Nov2023.PDF]

Since they put that presentation together in November, Genesis have bought more gold: GMD-to-acquire-the-Bruno-Lewis-and-Raeside-gold-projects-14-Dec-2023.PDF plus Kin-Completes-Sale-of-WA-Gold-Deposits-for-Cash-and-Shares-09-Feb-2024.PDF

And here is slide 15 (below) from GMD's November 2023 Corporate Presentation that I talked about above.

So what Raleigh Finlayson did with Saracen Minerals was he acquired a number of quality gold projects, got them all or at least most of them into production, which dragged Saracen up to #4 in terms of Aussie Gold producers, with only Newcrest (now owned by US-based Newmont), Northern Star (NST) and Evolution Mining (EVN) producing more gold per year than Saracen did (in terms of Aussie-based and ASX-listed gold producers), and then Raleigh and NST's Bill Beament orchestrated a merger of the two companies which was achieved via NST acquiring Saracen.

So Saracen is now part of NST, and with Newcrest having been taken out by NYSE-listed Newmont Corp last year, NST is now Australia's largest ASX-listed and Australian-based gold producer.

Not long after the merger, Raleigh left NST on agreeable terms, and set up Genesis Minerals with plenty of financial backing - he is highly respected and has an excellent track record of value creation so he has plenty of people, particularly insto's and HNWI's, with money who are happy to back his latest venture. Then Bill Beament left NST himself and went to run Venturex, now known as Develop Global (which I also hold shares in).

So, back to Genesis. Can Raleigh do it again? Well, so far, so good.

Only two Aussie goldies (NST & EVN) have a greater Mineral Resource than Genesis' 15 Moz (15 million ounces); That's a LOT of gold. Genesis are only currently producing from one mill (Gwalia at Leonora) which is not being fully utilised (running well below capacity), however they have a second, larger mill at Laverton that they are going to fire up soon (the gold mill/plant formerly known as Dacian Gold's Mt Morgans Mill) and they have a lot of gold in various projects that is still in the ground or in ore stockpiles awaiting processing. And they have plans to fill both mills to capacity (see their presentation - link above - between the last two slides).

In terms of Gold Ore Reserves, the GMD Presso (first slide up from here, put together in November) suggests that they are in 5th position behind NST, EVN, PRU (Perseus Mining) and RSG (Resolute Mining), but the more recent RED/SLR slide suggests that GMD are one spot higher than that with only NST, EVN and WAF (West African Resources) ahead of them with greater Reserves, because the latest Reserve numbers from PRU and RSG are lower, probably due to either depletion through mining, or asset sales, or a combination of both.

GMD's table doesn't have WAF in it for some reason. Possibly because their latest numbers weren't available at the time? WAF first produced gold at Sanbrado, in Burkina Faso (West Africa) in March 2020, so they've been producing for a few years now, so it's not as though they've just started producing.

That's something worth pointing out, I tend to avoid West African gold miners, even when they are Australian managed, Australian headquartered, and ASX-listed, because I think the risks associated with mining in West Africa do not justify the potential upside - for me. Those West African miners include WAF, PRU and RSG - so if you take those three out of it, there's just NST and EVN ahead of GMD in terms of Reserves and Resources, and if the RED/SLR merger goes through then RED might move up to challenge GMD for third best gold ore Reserves.

I already hold NST, and I've recently sold out of EVN due to their increased reliance on copper production out of both Ernest Henry and Northparkes which they use to make their gold AISC look reasonable. Without those copper byproduct credits they are NOT low cost gold producers, which is what they market themselves as, and I don't like that, and I think they're due for a big downward re-rate, so I'm out of EVN.

So Genesis (GMD) is the next logical goldie for me to own, and I do.

If you look at the fourth chart on the second last slide above, the one titled, "EV / Resource (A$/oz Au Eq)", you'll see Genesis is 4th from the bottom, with their current share price and market cap valuing their Gold Resource at just A$112/ounce, while the current spot price is over A$3,100/ounce. And Genesis have Zero Hedging; yep, they're completely unhedged and totally exposed to a rising spot price.

So, what does that mean? I would suggest that means that they are actually still quite cheap - there are only three goldies that are even lower than $112/oz, and one of those is Westgold (WGX) who look cheap across most metrics actually - and I am looking to get some exposure to Westgold in my SMSF shortly as it happens - plus there's also two of those three West African goldies (WAF and RSG) who trade with a risk-discount in their share price which always makes them look cheaper than many of their peers - but they are also riskier than most of their peers because of where their mines are located.

In summary, while GMD can look expensive based on their current production, they are about to ramp up production significantly, like more than double it, and they do NOT look expensive based on the gold that they own that is still in the ground.

And it's not low grade stuff either - have a look at this:

Tower Hill is just one of GMD's development projects and it's got higher grades than the world-class Tropicana open pit gold mine (30% owned by Regis, 70% owned and operated by AngloGold Ashanti) - and Tropicana is very profitable. Note - those mines in that chart are single open pit deposits only, so no underground mines or projects. And open pit gold is a lot easier and cheaper to truck out than gold is from underground mines.

So where is Tower Hill? Somewhere remote? A long way from Infrastructure? Yeah, Nah! It's just 2 km north of Gwalia:

Here's another look at a peer comparison based on gold reserves and resources from a September 2023 North American Investor Presentation by GMD:

In that slide the two ASX100 goldies (NST & EVN) have been removed and so have all of the West African and other goldies that do not have gold mines here in Australia - so they (GMD) are saying their "peer group" is small to mid-tier ASX-listed gold producers who have mines here in Australia.

Have a look at who is backing Genesis:

Below is that "Ownership Geographic" blown up so it's easier to read:

Insto ownership accounts for 70% of their shares on issue, split as follows: 52% owned by Australian Institutions, 10% North American insto's, 7% UK insto's, and 1% owned by European insto's (ex-UK). 29% Free Float (Retail) but it looks like the 2.4% owned by the Genesis Board and Management may be included in that 29%, so that leaves 26.6%. Not too bad, but it underlines how much institutional backing this company has because of what Raleigh Finlayson (GMD's founder and MD) managed to achieve with Saracen Minerals previously.

And it looks like he's on his way to doing something similar with Genesis.

Slides sourced from: INTRODUCING GENESIS - A growing Australian gold house - CORPORATE PRESENTATION - NORTH AMERICA - September 2023 and Corporate-Presentation---Ready-set-grow---Assets-and-people-in-place-for-+300koz-p-a-27Nov2023.PDF

See also: GMD-Quarterly-Activities-Report---December-2023.PDF

So, I see GMD as a no-brainer in terms of me choosing to have exposure to them at this point. There's plenty of upside from here.

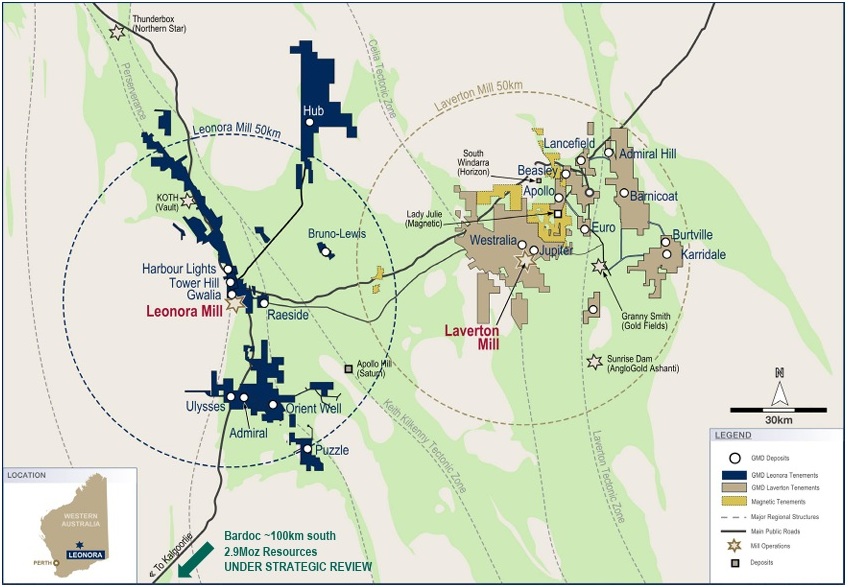

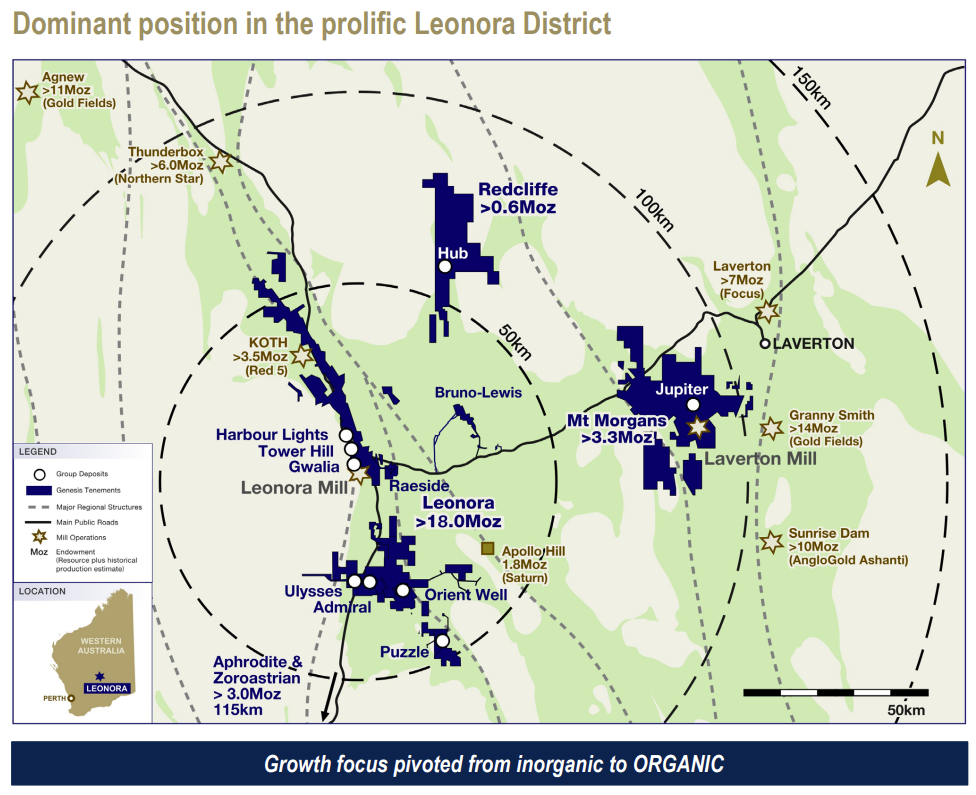

And for those people with a higher risk tolerance, have a gander at the three projects within that 50km radius of GMD's Gwalia mill at Leonora (within the smallest circle) there that are named in Brown instead of Blue - meaning they are NOT already owned by Genesis - there's KIN's Cardinia project, Saturn Metals (STN's) Apollo Hill project, and Red 5's (RED's) KOTH (King of the Hills) mine and mill.

KOTH is already in play with the proposed SLR/RED merger, so I hope Raleigh doesn't come over the top with an even higher offer for RED than what SLR have proposed with their reverse takeover (RED acquiring SLR). Raleigh just doesn't need KOTH that badly - he wants it, but he doesn't need it, and if he clearly overpays for that asset, it could shake the market's confidence in both him and his company. It might not, but it might. But he doesn't need to do it - it would cost over $1 billion and it's really not a good acquisition at the price in my view.

And since that map was put together in September, GMD have bought part of KIN's Cardinia project, the Bruno-Lewis gold project and the Raeside high-grade gold project - see here: GMD-to-acquire-the-Bruno-Lewis-and-Raeside-gold-projects-14-Dec-2023.PDF

Here's the updated map (below) that GMD included in that mid-December announcement:

Now there's just RED's KOTH and STN's Apollo Hill left inside that 50km radius circle - that isn't already owned by GMD. If I was a betting man, I might take a small bite of STN - whose shares are trading at around 16 to 17 cents/share and whose market cap is only $30 million. RED's market cap is $1.14 Billion. GMD's is $1.76 Billion.

Of course RED has a working gold mine and working gold mill and STN just have a gold project that they are trying to develop, so it's like comparing an apple to a truckload of oranges. But I'd have thought that taking over STN or just buying Apollo Hill from STN would make a lot more sense than trying to trump SLR once again to attempt to takeover RED.

Acquiring Apollo Hill would also mean that Genesis would own every decent gold deposit between Leonora and Laverton, as that last map (above) shows.

There would still be Focus Minerals's (FML's) Laverton mill just north of Laverton, but Focus is now a 63% owned subsidiary of Shanghai-listed Shandong Gold International Mining Corporation, and I doubt they would sell to an Australian company unless it was at a very high price, and I doubt Raleigh would be interested in any of FML's assets anyway. He already has plenty of mill capacity at Laverton.

And his focus is really on Leonora - as the maps clearly show. Anyway, time to catch some Zzzz's. That'll do Donkey. That'll do.

Bill and Raleigh when the NST-Saracen merger was announced in early October 2020.

Raleigh Finlayson in March 2020 in the Saracen office (before the merger).

Same again below.

Shortly after the merger with NST.

Raleigh last year. Now running Genesis.

At the Genesis Minerals Office.

Raleigh and sister Marnie Finlayson, who is an executive at Rio Tinto and is also on the NST Board.

Marnie and Raleigh Finlayson: Rio’s lithium star and her Genesis CEO brother (afr.com)

(24) Raleigh Finlayson | LinkedIn

Genesis Minerals Limited | Perth WA | Facebook

https://genesisminerals.com.au/

11-Aug-2024: Update: This one was marked as stale, and the company is no worse now than they were when I last updated this - in fact they're looking better - and remain disciplined in terms of M&A, with a lot of opportunities around them for smaller bolt-ons, which they have so far resisted, and I'm also happy that Ral did NOT get involved in the SLR/RED merger where SLR have effectively taken over control of Red 5 without paying a management premium by way of a reverse takeover (so officially RED acquired SLR but the SLR management team are now running RED) - because the way that was structured, GMD buying into RED (who owned KOTH, the mine and mill near Leonora that would fit nicely into Ral's empire at GMD) wouldn't have made any difference because he would have needed a blocking stake in SLR to have scuttled that deal, and there's no way GMD want to own any SLR shares with all of their assets (prior to the SLR/RED merger) a fair way north west of Leonora.

So no movement from Ral to try to slow down or stop that one going through, unlike SLR/RED's Luke Tonkin's behaviour when he made multiple attempts to either halt or delay the GMD acquisition of Gwalia and the other Leonora assets from St Barbara in the first half of last year. There's no love lost between Raleigh Finlayson and Luke Tonkin, but Ral remains the superior human being, with the better business, and better business sense.

So Genesis (GMD) continues to deliver to plan, and they are the big growth story in the Aussie Gold sector and should remain so as they bring more projects online and fill up their Leonora (Gwalia) and Laverton (Mt Morgans) mills. There is a management and growth premium in the SP now, but it is well deserved. However, I can understand why Ord Minnett (OM) recently moved GMD from "Accumulate" to "Hold" based on their share price appreciation rather than any change in the outlook for the company.

I'd like to see Ral buy MAU (Magnetic Resources) for GMD (Genesis), because it makes strategic sense for their Laverton mill, but there's no rush as MAU already has a significant market cap for a gold project developer, so they wouldn't be buying them super-cheap here. There is a good chance he won't do that however, because Ral has made it very clear that consolidation of gold assets around Leonora remains his number one priority, and right now his main focus is developing what GMD already own.

Other companies on his radar would include Kin Mining (KIN, soon to be known as Patronus, it's a Harry Potter reference apparently, to do with magical transformation or the conjuring up or personification of a strong positive emotion - and comes after the acquisition of PNX Metals (PNX) so PNX will probably become KIN's new ticker after they officially become known as Patronus), and to a lesser extent Mt Malcolm Mines (M2M) - which is worth almost pocket change to Ral at this point and may well go into VA and become available for even less, and Saturn Metals (STN) whose Apollo Hill project is likely going to become a large scale heap leach project rather than a traditional gold mill.

I think Saturn (STN) is the LEAST likely to be an M&A target for GMD because Apollo Hill would not provide feed for Gwalia (GMD's Leonora mill) and while it's within the 100 km radius of Leonora that Ral is targeting, it's down to the south east of that circle and further away from Gwalia/Leonora than the other projects are - so it makes far less strategic sense than all of his other options (MAU, KIN/PNX, M2M).

But, as I said, I don't think M&A is still a high priority for Ral at this point - I think he has plenty to keep him busy for now - the only reason he would do further acquisitions in the near term would be (a) because he sees a good strategic opportunity that he does not want falling into somebody else's hands, and/or (b) he sees a cheap opportunity that is likely to become significantly more expensive if he waits and buys it later. I think under either or both of those scenarios he has the firepower and the will to make a move, but I don't think he needs to now - he's got plenty of projects to develop and two good mills already - one at each end of that area that Genesis own most of (Leonora across to Laverton) - or most of the gold deposits in that area (rather than most of the land in the area) - but, plenty to be going on with for now.

For context, Ral would have liked to have bought RED to get KOTH (King Of The Hills), but that chance has passed now, and he can only get KOTH now by buying the "new" RED which post-SLR-merger is now worth $2.3 Billion. On 21-May-24 RED closed at 49 cents/share (cps), they are now 35.5 cps with a sh!tload more shares on issue post the merger with SLR, but on 20-Feb-23 (18 months ago) they closed at 13 cps with far less shares on issue.

At 13 to 16 cps earlier last year - maybe even up to 20 cps - RED, with all of their assets relatively close to Leonora, made plenty of sense, but Ral had his hands full with trying to first merge with SBM and spin out their non-Leonora assets into a newco (which was going to be called Phoenician Metals) and then instead Plan B (after Ral realised just how dire SBM's own situation had become which allowed him to re-jig the deal in a major way to Genesis' benefit and St Barbara's detriment) was to buy the Leonora assets from SBM and leave SBM with everything else - which is what eventuated after a number of delays caused by Luke Tonkin's SLR lobbing in inferior bids. Then in September last year Luke Tonkin's Silver Lake Resources (SLR) bought 11% of RED as a "strategic" (blocking) stake and then moved to acquire the remainder of RED this year via the reverse acquisition I mentioned a few paragraphs up.

It should be noted however that while both SLR and GMD had no net debt and a big pile of cash, so both seemed to be well run gold producers, GMD have a history of only buying assets at good prices where the acquisitions made strategic sense, and SLR have a history of overpaying for assets that they could have bought much cheaper earlier (i.e. RED) and where analysts struggle to understand any strategic sense or how any synergies might be realised. So Luke Tonkin is an empire builder with not a lot of strategy - or at least his strategy is hard to fathom, whereas Ral has done this all before with Saracen Minerals (which merged with Northern Star Resources - NST - a few years ago) and is able to communicate his strategy clearly and get plenty of backers onboard and more than happy to throw money at him and anything he turns his hand to because he has such a great history of producing superior TSRs for his shareholders.

That's why I hold GMD shares (and currently also MAU, KIN/PNX and some STN for further drilling result upside - I intend to sell out of STN on their next decent spike up) but not RED (and I wasn't an SLR shareholder either).

In terms of gold producers, my current exposures, in weighting order are NST, RMS, GMD, EMR and PRU. My project developer exposure is significantly smaller because of the elevated risk of owning pre-revenue companies - so MAU, KIN and STN are smaller positions held for shorter-term gains.

I have raised my GMD valuation a little today based on the higher gold price and my outlook for an even higher gold price being reasonably bullish, and GMD being so well positioned within Australia's larger gold producers - and with multiple growth projects.

16-Nov-2024: Update:

I'm raising my price target for GMD to $2.77 based on their latest presentation (their 2024 AGM Presso, released this past week) and their outstanding growth profile over the next few years. They are very well positioned.

The larger the bubble size above middle and above right, the higher the Reserve/Resource Grades are.

However, the higher up the chart the bubbles are, the more expensive they are, so you're paying more for each ounce of (underground) gold that they own. Ideally, you want to hold companies towards the bottom right corner of those two bubble graphs, being cheaper (lower down) and with a higher gold Reserve (middle graph) or higher gold Resource (right graph), meaning towards the right side of each graph above.

On that basis, both Westgold and Genesis look really good right now. I've topped up my Genesis (GMD) shares (in my SMSF and here) and added a Westgold (WGX) position to my SMSF during the past week, after selling all of my Perseus (PRU) and all of the IOO ETF out of my SMSF. I rate PRU's management a lot more highly than WGX's management, as I've mentioned here before, but I think WGX probably offers a better risk/reward trade-off from current levels than Perseus does, at least for the next little while.

But Genesis is the goods. They've got it all. Top quality management who think and act like owners rather than managers, always making strategically sensible decisions with a goal of long term value (TSR) creation. No debt. Cashed up. Backed by everybody who matters, because Raleigh is so highly respected in the industry. Huge access to growth capital whenever they want to pull the trigger. Focused on what matters, increasing grades, decreasing costs, so creating a gold company that will outperform in all sorts of different gold price scenarios. Heaps of growth. Realistic goals and timeframes. A history of underpromising and overdelivering, both with Genesis Minerals and formerly with Saracen Minerals (which merged with Northern Star in early 2021).

Some more deets:

Skin in the game:

That map a bit larger:

Value creation being reflected by the share price rising within a nice channel:

That was a snapshot during Thursday this past week (14-Nov-2024).

And still finding more gold: Updated - Strong drill results support growth [12-Nov-2024]

The Aussie gold price is going to be volatile I think over the next little while, so opportunities to pick up quality gold miners at lower prices might well present themselves.

We've got a falling US dollar due to our commodities-based econcomy struggling as China faces a few headwinds, and the surging US dollar isn't helping Aussie gold miners who mine all of their gold here in Australia and sell it all in A$'s, like GMD do.

However, Trump's rediculous appointment choices in the USA for his upcoming 4 year Administration starting on January 20th, some of which won't go through, like Matt Gaetz as Attorney General, and Kristi Noem (the one who tried to appeal to gun owners by admitting in her autobiography to shooting her pet dog and her goat) for Secretary of Homeland Security, and "Fox & Friends" (a show on the US' Fox News network) weekend presenter Pete Hegseth as Secretary of Defence - a guy who admitted on-air at the start of Covid (in 2020) - much to the amusement of his co-hosts - that he hadn't washed his hands in 2 years because germs aren't real because he can't see them, and some Trump choices which just might get up, like RFK Jnr as head of Health and Human Services and Marco Rubio for Secretary of State... are just another factor that points to a significantly increased level of volatility in 2025 that we probably haven't seen before, and in that scenario, gold certainly has the potential to rebound strongly and go substantially higher.

Many of the people who voted for Trump, and the millions who would have voted Democrat but instead stayed home because they weren't overly enthused with Karmala Harris' message and positioning, are now saying, "What the f@ck have we done?!?"

Not good for the US - like Trumps proposed 60% tariffs on Chinese imports and 10% to 20% tariffs on most other imports - which will be worn by US consumers and will only increase their inflation - and likely see the previously expected interest rate cuts being less likely now.

And not good for the world, with Marco Rubio - Trump's pick for Secretary of State - being anti-United-Nations and an isolationist, as is Trump himself. Trump and his appointees are not interested in the rest of the world, or how the US is viewed by the rest of the world; their motivations are to do what is in their own interests.

Trump has significantly changed the political landscape over the past 9 years. Trust in the government and the media and traditional institutions and organisations is at an all-time low in the US, and he can say whatever the hell he wants with zero consequences.

People actually don't expect him to be honest and to do exactly what he says - even those people who voted for him. They understand that everything is a negotiation with Trump. He states a position but that is often not his final position on that particular subject. It's a starting position.

There is only one thing we can assume - and that is that Trump will do whatever he views as being in his own best interests, and to a lesser extent in the best interests of those who have supported him recently, but in terms of where that leads us, all bets are off.

If he establishes a Bitcoin reserve, or whatever you want to call it, because he's pro-Bitcoin, and his son is heavily into it, that could drive Bitcoin to even more rediculous levels, and have a negative effect on gold, but outside of that, next year should be another positive year for gold in my view, particularly as more and more large players exit or reduce their US Bonds and other US dollar investments and look for alternative stores of value that can't be erroded in the way that traditional currencies can.

It won't be up in a straight line, and we might see a decent pullback over the next couple of months first, but gold is not something I try to time, because nobody can accurately predict what gold will do, so it could tear higher at any time, for any reason; you just have to be in it before that happens.

Watching Friday's MoM podcast earlier today, I was reminded that you can't predict the gold price based on supply and demand expectations, because:

- The vast majority of gold producers will sell every ounce of gold they produce, regardless of the price they receive, unlike in some other commodities where stockpiling during periods of lower prices is more common, so in that sense supply is fairly predictable with gold; but

- Gold demand is entirely unpredictable because nobody NEEDS to buy gold every week, it's hugely sentiment driven, and sentiment can turn on a dime, multiple times in a single day in fact, let alone weekly and monthly.

- Because such a tiny percentage of gold is used in ongoing industrial applications, i.e. used to make something else such as gold plated electrical components for example, and the VAST MAJORITY of gold is bought for investment purposes, the gold price behaves like no other metal on earth.

So, NO predictions, at least none with any sense of certainty or even a sense of comfort, but on the whole I feel it in my bones that gold goes higher over time from here.

And my preferred exposure to gold is via quality gold producing companies with excellent TSRs.

Northern Star (NST) has been the poster child for that in prior years, and with the Fimiston mill expansion (the Super Pit expansion) due for completion in the next couple of years, NST still have growth, and I hold NST both here and in my SMSF, but Genesis (GMD) is the pick of the crop for quality growth over the next 3 to 5 years, in my opinion, so I have a larger exposure to Genesis than to NST at this particular point in time.

19th April 2025: Update:

Raising my price target to $4.82 as Genesis shot straight through my old one. See here for my commentary around their latest (March 2025) quarterly report: https://strawman.com/reports/GMD/Bear77?view-straw=28349 - that will likely take you back to this GMD "valuation" of mine - which is more of a price target and investment thesis - and the straw will appear below it if you scroll down far enough - you can access the comments thread here (click on the word "here") which also includes that straw linked to above.

Still holding this and Ral (GMD's CEO and MD) is executing on his vision and guidance for Genesis, so they have further to run, IMO, despite a fair bit of future growth already being priced in up here, as long as Ral keeps delivering.

I also expect further positive M&A from Genesis, so we'll likely get organic and inorganic growth, to keep raising the bar / expectations in terms of future production (ounces of gold produced per annum). I think that while Vault's KOTH mill (surrounded on three sides by Genesis' tenements and located a little north of Leonora) is always at the forefront of commentators and analysts minds when it comes to Ral's future acquisition targets, it is far more likely (IMO) that Ral will first move on smaller players and assets around Laverton to fill up their Laverton Mill that they recently brought back online.

I've had a look at those possible Laverton targets, companies like Focus Minerals (FML) whose Laverton assets are for sale, Magnetic Resources (MAU) who are clearly for sale (many of us remember how MAU's MD, George Sakalidis blurted out during D&D last year that Magnetic already had at least two companies in their data room preparing offers, a level of disclosure which apparently scared those companies away at that time), and Brightstar Resources (BTR) who already have an Ore Purchase Agreement (OPA) with Genesis, which allows Brightstar to deliver, sell, and process up to 500,000 tonnes of ore at Genesis's Laverton Mill.

FML is majority Chinese owned - 63.19% of FML is owned by Shandong Gold International Mining Corporation Limited - so my best guess is that FML as a company is not for sale, despite their Laverton gold assets being for sale, however a full acquisition of BTR or MAU is always a possibility. However, I'm not positioned in those possible acquisition targets (i.e. I do NOT hold FML, BTR or MAU shares) because I've been caught out previously trying to anticipate M&A moves, and we don't have all the facts; we don't know how that pans out. Ral could make a move on one or more of those three, or not, or make a different move on an entirely different company or asset. My play is to just hold Genesis, and enjoy the ride.

And the gold price is certainly not doing Genesis any harm:

Source: https://goldprice.org/gold-price-australia.html [accessed at 11:50am Sydney Time, 19th April 2025, prices were current as at 5:15pm New York time on 18th April 2025]

That's a solid uptrend, and Genesis are one of the Aussie gold sector's best growth stories, so it's little wonder their share price chart is also in a similar uptrend.

GMD has outperformed the other 4 gold miners that together with GMD make up Australia's largest 5 gold miners by market capitalisation, and they've all thrashed the ASX200 TR Index (XJO):

Disclosure: I'm holding GMD, NST & EVN. NST are in the process of acquiring DEG.

7th May 2026: Update:

Raising PT to $9.75. They're bigger and better now - as expected - since my last update, and the gold price is higher too.

After acquiring FML's Laverton assets, GMD is now acquiring all of MAU (Magnetic Resources), so will also own the Lady Julie gold project providing even more high grade ore for their Laverton mill.

Here's how those MAU tenements fit in to GMD's Laverton Tenements - very nicely:

The yellow tenements are the MAU tenements.

I've just written a decent length straw about why I still like this company so much - so I won't repeat it all here, but yeah, I reckon their SP is heading further north and $9.75 within the next 2 years looks very achievable once they resume their previous uptrend:

So, yeah, I'm calling $9.75/share or higher for GMD by May 2028. [not advice].

7th May 2026: Presentation - Growth AND Cash Flow

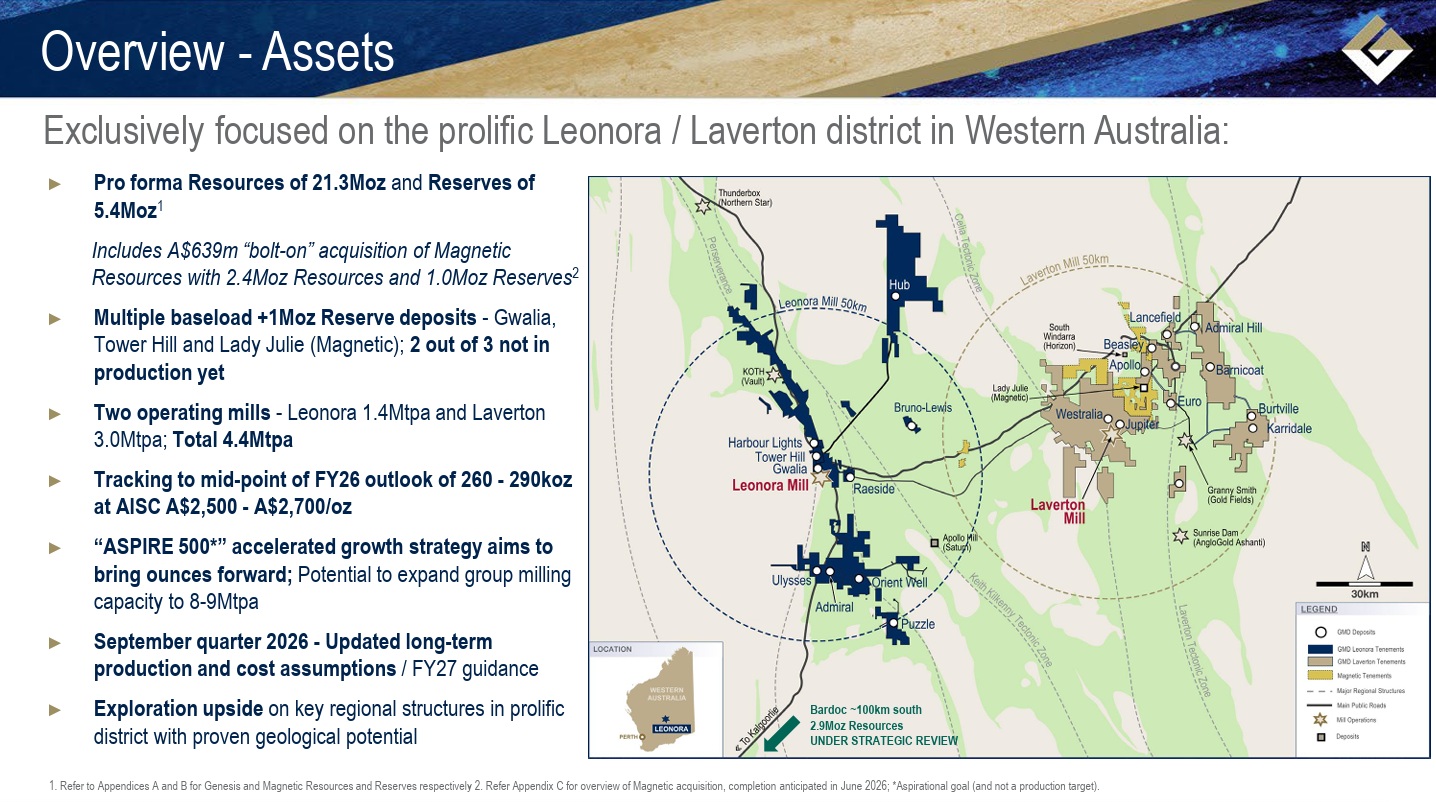

In this latest presso from GMD today, we see just how well the new MAU (Magnetic Resources) tenements that Genesis are acquiring (via the takeover of MAU) fit into their Laverton tenement package:

The MAU tenements are yellow; and GMD's tenements around Laverton are brown. GMD's tenements around Leonora on the left side are dark blue and you can see they surround VAU's KOTH mill on three sides (north, east and south) which is why many people thought VAU would be swallowed up by GMD eventually, and that is less likely now that RRL and VAU have agreed to merge, although that merged entity, if that deal does go through, could then sell off KOTH and the surrounding tenements to GMD at some point. Importantly, Luke Tonkin (who Ral Finlayson at GMD does NOT get along with) will no longer be running the show there, he is retiring, and the Regis (RRL) MD Jim Beyer is going to run the new group, again IF that merger goes through. For clarity, while they're calling it an agreed merger, it is subject to no superior offer being received for either company and if it does go through, VAU shareholders get RRL scrip (shares) - not cash, so they become RRL shareholders if the decide to keep those shares. The market doesn't seem to be too keen on that proposed merger based on the share prices of the two companies since the announcement, although they are both up today. Almost all of the Aussie gold sector is up today.

Anyhoo, back to Genesis Minerals (GMD) - that map above is taken from the slide below, which was part of today's investor presentation by GMD.

I did mention here last year that GMD became the natural owners of MAU as soon as they bought FML's Laverton assets which included a tenement that bordered the northern edge of the planned Lady Julie open pit that was MAU's flagship gold project, and not only that, MAU had hit good gold grades right up to that boundary so they knew the gold extended north into Focus Minerals' (FML's) tenement, which was acquired by GMD last year. My reasoning was that nobody was going to touch MAU after that except for GMD because GMD owned the tenements all around Lady Julie including the one to the north that would allow the open pit to be extended significantly north, and that's how it has panned out.

Now I don't currently own any GMD at this moment, but that's just a timing thing as my SMSF - where I have held them previously and hold all my positions large enough to be in the ASX300 - is 100% cash now (including my sold CBUS managed infrastructure fund units, now sold as well) awaiting the opening of my Income Stream Account (ISA), which will allow me to trade without any CGT payable on gains, and CBUS assured me by phone yesterday that the ISA would be up and running by the end of next week. There will then be a 2 to 3 day delay while I move 80% of the balance across into the "self managed" option - it takes a couple of days to go through after I place the instruction, so realistically I'm probably looking at around a fortnight before I can begin buying back all of my favourite ASX300 companies, like GMD, NST, etc.

Being in cash since late Feb has been a blessing, but only if those companies' share prices stay below the price that I sold them for back in Feb - for the next 2 weeks. Either way, I'll be buying GMD back some time this month because they have oodles of gold production growth over the next few years. Likewise NST, but this straw isn't about NST.

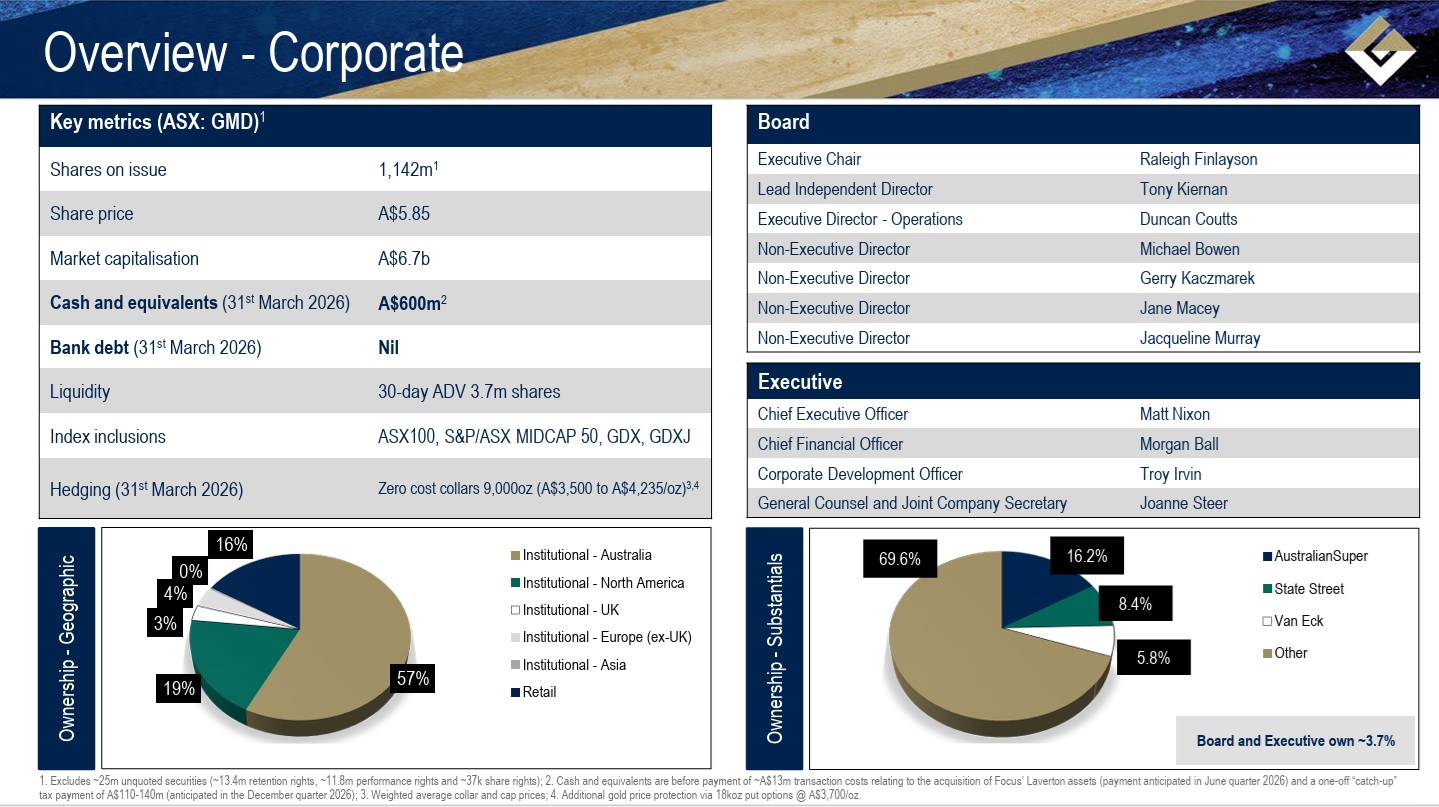

So, GMD. Have a look at this:

Market cap now over $7 billion (they were up +4.41% today). Zero debt and $600 million in cash and cash equivalents, very liquid, an ASX100 company, with AustralianSuper owning 16.2%, another 14.2% owned by two of the world's largest ETF providers, State Street and Van Eck, 3.7% owned by the Genesis Board and Executives, only 16% of the register is retail shareholders, and the company is run by Raleigh Finlayson who built Saracen Minerals (was SAR.asx) up from nothing to become Australia's 4th largest gold miner, then co-orchestrated (with Bill Beament) a merger between NST and SAR which consolidated NST as the #2 gold producer in Australia, which soon became #1 when US-based Newmont acquired Newcrest Mining (which was previously Australia's largest gold producer) leaving NST at #1 and EVN at #2, with a fair bit of daylight back to #3.

There's a lot to like, and they do have a small but smart hedging strategy that is costing them nothing, and has no downside beyond capping some potential upside. Specifically, GMD have zero-cost collars over a small quantity of gold, as detailed above.

A zero-cost collar in gold hedging is a strategy used to protect against falling gold prices without paying upfront option premiums. It involves simultaneously purchasing an out-of-the-money put option (floor) and selling an out-of-the-money call option (cap) on gold. The premium earned from selling the call covers the cost of buying the put, making the strategy cost-neutral.

Key Aspects of Gold Zero-Cost Collars:

- Downside Protection (Put): A gold holder buys a put option to set a minimum price they will receive if gold prices fall, limiting losses.

- Upside Limitation (Call): To pay for the put, they sell a call option, which caps the maximum price they can receive, sacrificing potential gains if gold prices spike.

- Cost-Neutral Structure: The premium from the call offsets the cost of the put, resulting in zero or near-zero initial cost.

Example in Gold Hedging: An investor holds gold and wants to hedge against a price drop when the gold price is $4,200. They might:

- Buy a Put with a strike price 5% below the current spot price (e.g., floor at $4,000).

- Sell a Call with a strike price 10% above the current spot price (e.g., cap at $4620).

If gold prices fall below $4,000, the put option protects the investor. If gold prices rise above $4,620, the investor must sell at $4,620, missing out on higher profits, but the net cost of setting up the strategy was zero.

In GMD's case, it looks like they have a legacy position that involves just 9,000 ounces of gold, a paltry amount for them, and their average weighted collar and cap prices are A$3,500 and A$4,235/oz respectively with additional gold price protection via 18koz put options @ A$3,700/oz.

Importantly, Genesis is tracking to achieve the mid-point of their FY26 guidance of 260 - 290koz at an AISC of bertween A$2,500 and A$2,700/oz, so they are going to produce around 275 koz of gold this FY and are planning to be producing 325 koz p.a. by FY29 and have recently updated their aspirational longer term target from 400 koz p.a. to 500 koz p.a. by FY34, so within the next 8 years, and I reckon they'll get there - Ral tends to underpromise and over-deliver.

But right now they're a 270 to 280 koz p.a. gold producer so having those collars and put options over up to 27 koz of gold represents 10% or less of their current annual production, so they are essentially unhedged.

As I said, I don't want the GMD share price to rise too much in the next fortnight, as I need to get back onboard before they resume that strong uptrend again:

There's a LOT to like about this company!

Letter to Shareholders > Genesis Minerals produced a record 214,311oz of gold in the year, up 59% from 134,451oz in the previous 12 months. This stemmed from a strong performance at our Leonora operations and the start of production at our Laverton plant. The Gwalia team has done an exceptional job, not only in terms of what has been produced at the mine but also in the way it has managed the asset to ensure it continues to deliver for many years.

Generating strong production results at Gwalia has only been part of their task, with considerable emphasis also placed on mine development, grade control and near-mine exploration to ensure a long-term sustainable future for this mine. Just 30km along the highway from Gwalia, the new Ulysses underground mine is ramping up and the Admiral and Hub open pit mines made strong contributions for the year.

At Laverton, our team did an outstanding job by bringing forward the commencement of milling at the 3 million-tonne-a-year mill to October 2024. The ramp-up has been very successful, contributing to our overall production for the year and paving the way for Laverton to play a vital role in our ”ASPIRE 400” accelerated growth strategy.

https://hotcopper.com.au/threads/ann-fy2025-annual-report.8722483/

Return (inc div) 1yr: 101.38% 3yr: 50.03% pa 5yr: 46.20% pa

USA Good for Gold price support

FED = Market expectations currently price in an 85% chance of a September rate cut, further supporting bullish sentiment in the metal.

Hey ... Chat GPT:

How much does it cost to mine gold? (i.e. cost per ounce)

The most up-to-date metric available is the All-in Sustaining Cost (AISC), which represents the comprehensive cost—including mining, processing, sustaining capital, and overhead—per ounce of gold produced.

- For the full fiscal year, Genesis achieved a AISC of A$2,499 per ounce. This figure corresponds to their record production of 214,311 oz for the year The Capital Club.

- In quarterly terms, especially during the June quarter, Genesis also reported an AISC of A$2,499/oz The Capital Club.

- In earlier quarterly periods, such as a December half-year report, Genesis recorded AISC closer to US$2,202 per ounce—due to exchange rate differences—but the most recent and consistent figure remains A$2,499/oz IGAustralian Securities ExchangeThe Capital Club.

Summary: The current cost to mine (AISC) is approximately A$2,499 per ounce.

10th June 2025: Corporate Presentation - Focused

Raleigh likes the odd pun. They've just bought all of the Laverton assets from Focus Minerals (FML). And GMD are "Focused".

Yeah, I see what he did there.

So this presso is all about how the Focus Minerals Laverton assets feed into the Genesis Minerals growth narrative, and before I get into the most interesting slides, I want to point out something that this presentation does NOT touch on, which is that one of the tenements that came with these Focus assets is the one directly to the North of Magnetic Resources' (MAU's) Lady Julie North gold project, the one that contains most of their gold, which is planned to be an open pit operation.

The following image is a snapshot from a virtual project flyover video on the Magnetic Resources' website (link below image) which shows how the pit should look eventually:

Source: https://youtu.be/5cd4FW7P-Lc

From: https://magres.com.au/

Time Stamp Link: https://youtu.be/5cd4FW7P-Lc?t=33

That image is looking basically east with the yellow line on the left side being MAU's northern boundary. The Lady Julie North gold deposit is open to the north but MAU have been unable to buy that adjoining tenement (left side of the yellow line) because FML wouldn't sell it by itself. Focus Minerals did however just sell it to Raleigh Finlayson's Genesis Minerals as part of their entire Laverton tenement package, so, as the MoM lads pointed out last week, this is also a strategic move by Ral at GMD to lock up MAU if and when he wants to move on them, as the reality is that whoever buys Magnetic to get Lady Julie Central and Lady Julie North (and Magnetic is definitely for sale!) can NOT mine all of that Lady Julie North gold deposit without encroaching on that tenement to the north that is now owned by Genesis (GMD).

The short version is that the most likely buyer of MAU at some point in the future is now GMD because GMD now own the tenement directly North of Lady Julie North that MAU need to fully mine that Lady Julie North gold.

This is one of the reasons why George Sakalidis at MAU keeps telling everybody that he has heaps of people interested in buying his company (7 different companies were currently showing interest he said two weeks ago) - something he was doing back at D&D (Diggers and Dealers) in Kalgoorlie last year - BUT nobody has lobbed in an offer yet. Nobody wants to buy MAU without that adjoining tenement that has now just been acquired from FML by GMD.

Which probably means that Ral at GMD can bide his time now and wait for MAU's share price to go back down to more sensible levels - MAU's SP has an M&A premium in it, which is a direct result of George talking up the M&A interest at every opportunity, but it won't stay elevated if nobody makes a bid, and now that GMD own that adjoining tenement, it's quite possible (not 100% locked in, but still quite possible) that nobody will make a bid, until Genesis Minerals make one when they're good and ready, which could be a year or two away. It could also be tomorrow, but I would imagine Ral can afford to wait for a better price level. Genesis is now the natural owner of those Lady Julie gold deposits that MAU own, IMO, but there is no rush.

Similarly, Genesis is also the natural owner of Vault Minerals' (VAU's) KOTH (King Of The Hills) gold mill and mine, but, again, Ral has shown plenty of patience with that asset also, having not made a move yet, or not one that has been disclosed by either VAU or GMD anyway.

But back to today's presso, which is all about why Ral has bought those Focus tenements:

Here is a selection of the most interesting slides (IMO) from the 28 slides in the deck:

Wow - that came out small - here's that map again, hopefully larger:

That map a little larger:

You can see Magnetic's (MAU's) "Laverton" project (which includes Lady Julie Central and Lady Julie North) as the black dot with the gold centre immediately below the FML Tenement containing the Apollo and Beasley gold deposits/prospects in the "Chatterbox" tenements which are marked with a red "3" on the map above.

That last one is super interesting to me because it is highlighting all of the Refrac ore in the area (both refractory and semi-refractory) ore that GMD now own, which requires more than a basic CIL mill to extract the gold; They also mention that the Hemi deposit that came with De Grey (which NST just paid $5 Billion worth of NST shares for) includes refrac mineralisation.

NST's largest existing mine, the Kalgoorlie Super pit, also known as KCGM (Kalgoorlie Consolidated Gold Mines) and/or the Fimiston Mill, already processes refrac ore, so NST are no strangers to it and that's why they weren't afraid to shell out the big bucks for De Grey to get Hemi.

Here's that map a little larger:

Always big on the investor relations and explaining what they are doing, their targets, their timelines, and their progress to date, Raleigh Finlayson, GMD's MD, is doing exactly what I expect him to do, and I'm very happy to be along for the ride once again (I rode his Saracen Minerals up also through to the merger with NST).

There is a reason why this company is so loved by insto's and brokers, and can borrow any amount of money they want, if and when they want money. Or raise fresh capital through placements of additional shares.

It's as close to the perfect Aussie gold growth story as you can get on our market - it's pretty damn close to perfect actually. There's a management and growth premium in the SP, but you get that with a company like this, and if you wait for a big pullback before jumping on, you may never get to enjoy the ride at all.

Disclosure: I hold GMD shares both here and in my SMSF.

26th May 2025: Acquisition of Laverton Gold Project.PDF [GMD]

plus Sale-of-the-Laverton-Gold-Project.PDF [FML]

Makes sense !

We knew that GMD were going to buy something around Laverton to fill up their existing 3Mtpa Laverton Mill (the mill that came with the Dacian Gold acquisition a couple of years ago) which is just 30km away from this gold deposit they have just acquired, and we knew they couldn't buy all of Focus (FML) because Focus are 63.19% owned by Shandong Gold International Mining Corporation of China ("Shandong"), so are considered to be a wholly controlled subsidiary of Shandong, despite FML being ASX-listed, and Shandong are China's second largest gold mining company (after Zijin) and also one of the largest gold mining companies in the world, and they rarely sell off their prospective land tenement packages, and they aren't doing that on this occasion either - as the FML announcement (link above) makes clear:

Focus’ Executive Chairman, Mr Wanghong Yang said: “We are extremely pleased with the outcome achieved in the sale of Laverton and believe the consideration payable represents compelling value to our shareholders. Proceeds from the sale of Laverton will strengthen the financial position of the Company as it continues with development at the Bonnie Vale Underground Mine and open pit mining operations at the Coolgardie Gold Project.”

Importantly, FML retains a good percentage of their over 1,650 square kilometers of land tenements in Western Australia across multiple regions including the Coolgardie and Laverton areas within the eastern goldfields. My understanding is that the Laverton tenements are included in this sale to GMD, but none of the other tenements.

So Focus retain plenty of optionality while monetising one asset.

From Genesis' POV, through paying just $250 million (cash), they are buying relatively cheap ounces of gold that they need for their own Laverton mill. The Laverton Gold Project (LGP) that they are acquiring has a global Mineral Resource of ~4Moz at 1.7g/t so their $250m purchase price equates to ~A$63 per Resource ounce. The LGP Reserves stand at 546koz at 1.3g/t.

The GMD announcement (link above) also says that in Raleigh Finlayson's opinion there is substantial scope for Resource growth from this acquisition through the large tenement package comprising highly prospective gold tenure.

Makes sense !

GMD is up today on this announcement, so it makes sense to the market also.

And on good volume too (over $11m worth of GMD shares have changed hands already today).

And FML's SP has doubled. In fact, it was up as much as +166.67% this morning - @ 60 cps, but is back at 45 cps now (or was one minute ago when I took that screenshot below). Not bad, considering they closed at 22.5 cps on Friday.

Mind you, FML is not widely held because of the controlling interest by Shandong (63.19%), so you can get some mighty big moves in lightly traded companies like FML when something significant actually happens, like this. I haven't held FML since before Shandong became their controlling shareholder, so not for a few years now.

While this is good news for GMD shareholders (like me) and great news for anybody lucky enough to be holding FML (not me), it's not AS great for some of those other names around Laverton who were also possibly on GMD's radar, such as Brightstar (BTR) and Magnetic Resources (MAU), because it seems less likely now that GMD need to acquire those companies in addition to today's acquisition of FML's LGP.

However MAU still made a new 12 month high of $1.705 this morning, and is currently trading just 1.5 cps higher (or +0.9% higher @ $1.675) than Friday's $1.66 close.

My personal thoughts are that MAU's colourful MD George Sakalidis cooked the company's chances of being taken over any time soon when he blurted out at last year's D&D in Kal that they had several companies in their data room and actually named some of them. He then doubled down on that mistake by telling the West Australian newspaper this month (May 2025) that Magnetic had SEVEN gold producing companies showing interest: https://thewest.com.au/business/mining/seven-gold-producers-attracted-to-magnetic-resources-lady-julie-project-near-laverton-c-18635991 [Fri, 9 May 2025].

Potential acquirers generally do NOT like being outed by the MD of their prospective target company while they are still at the DD stage, and while Sakalidis' behaviour is likely designed to both elevate the MAU share price and increase competitive tension for Lady Julie (MAU's flagship and most advanced gold project), it backfired on him last year, and it could backfire again now.

I am fairly certain that Raleigh Finlayson at Genesis prefers to surprise the market with his acquisition announcements, like he has today, rather than have his intentions broadcast in advance by whoever is running the company he is looking at possibly acquiring.

So while GMD may still acquire MAU at some stage, I doubt it's going to happen while MAU's George Sakalidis keeps running his mouth off and driving up the MAU SP.

Just my opinion, FWIW.

For the record, I like today's announcement, as a GMD shareholder.

07/05/2025: 3:26 pm AEST: May Corporate Presentation - Long Ore

A couple of slides from today's presentation that sum up why I hold Genesis (GMD):

That Map a little larger (hopefully):

Source: https://gmd.live.irmau.com/showdownloaddoc.aspx?AnnounceGuid=3599bce9-f168-46c5-9f17-a798b207e01c

The market likes them - this opportunity is NOT a secret:

Yes, there's some growth priced in already, but all of it? Not likely. If the gold price stays up around current levels or goes higher, there's no reason to expect GMD to be trading at lower levels if Ral keeps delivering on his promises as he has so far.

Disclosure: I do hold this one both here and in my SMSF. One of the best growth stories in the Australian Gold Sector and also one of the best management teams. People that made money out of Saracen (was SAR.asx until they were acquired by NST) have followed Ral into GMD hoping for more of the same, and he's certainly been delivering so far. I was one of those people - I made money out of Saracen, and I've made even more from GMD so far, with more to come (IMO). Not advice. Just my thoughts based on my experience.

16th April 2025: Genesis Minerals (GMD) Quarterly Activities Report - March 2025

Another cracking quarterly from Genesis, who are, IMO, the best growth story in the Australian Gold Sector in terms of decent sized multi-mine producers, and all of their assets are concentrated around Leonora and Laverton in the WA Goldfields.

Excerpts from the first three pages:

Importantly, they are still finding more gold across their tenements:

Which will also be added shortly here: https://genesisminerals.com.au/investor-centre/company-reports/quarterly-reports/

See also: https://genesisminerals.com.au/about-us/

The market clearly liked this latest quarterly report from GMD:

GMD made another new all-time high share price this morning - this time it was $4.31/share. Their 12 month low, almost a year ago, was $1.67. It's a good looking chart! They're not Robinson Crusoe - they DO have company - but Genesis (GMD) are certainly one of the better performers in the past year!

And they weren't even the best performing Aussie gold company this morning, although they are certainly in the mix.

[Only the top performers - with over +3% SP gains today so far - are shown above - that snapshot was taken at 10:52am today]

The gold price is providing a continuing strong tailwind to the sector:

Note: It's interesting that A$ gold has now outperformed US$ gold in terms of percentage returns for every time frame from 30 days up to 20 years, as shown in the side-by-side comparison tables above.

Disc: I hold GMD shares. In the Aussie Gold Sector I also currently hold NST, RMS, EVN, CMM, SPR, BGL, BC8, NMG, PLC, MEK and CYL. Some of those are held for shorter-term trades, others as longer term investments.

30-Jan-2024: One of my largest real life positions - my second largest across my largest two real money portfolios, Genesis Minerals (GMD) - which is held in both of them - made another 12-month (52 Week) high (share price) today. It could be considered an all-time high also, as while the share price chart does show a spike up above these levels briefly back in 2011 and again even further back in 2008, they were a very different company back then with different management and those spikes were immediately followed by drops to below $1/share in both 2008 and 2011. Now, with Raleigh Finlayson running the company, we don't see that sort of volatility in the share price, just a nice uptrend:

And what an uptrend it's been. I trimmed another 2,000 GMD shares this morning from my largest portfolio - to free up another $6 K - but still hold 10,000 GMD in that one and another 20,000 GMD in my super (SMSF) which is limited to ASX300 companies and is currently heavily skewed to Aussie gold producers.

Here's a snapshot of the shares portion of my SMSF portfolio as of last night:

My ex-300 companies plus more GMD and RMS and AEL are held within my other larger portfolio outside of super.

The market certainly views Genesis (GMD) as a growth company now - here is their latest quarterly report:

16/01/2025 8:17 am AEDT : Quarterly Activities Report - December 2024

Some highlights:

- December quarter production of 57,055oz at an all-in sustaining cost (AISC) of A$2,202/oz. With costs reducing over the next 4 years to closer to A$1,600/oz. The A$ gold price is now over $4,400/oz (see chart below).

- Cash generation was robust. Gold sales of 49,643oz underpinned revenues of A$200.9 million, allowing Genesis to grow its cash and equivalents to A$237.5 million at quarter-end. This was up $59.9 million from last quarter (A$177.6 million).

- During the quarter, Genesis brought forward the re-start of the Laverton mill to October 2024, six months earlier than flagged in the March 2024 Five-year Plan. This resulted in an increase in the FY25 production outlook to 190 - 210,000oz (from 162 - 188,000oz) at an AISC of A$2,200 - 2,400/oz (from A$2,250 - 2,450/oz).

- With the Laverton mill already running at 3.0Mtpa nameplate, Genesis has 4.4Mtpa processing capacity from two mills at the one production centre. With record December half production of 93,075oz at an AISC of A$2,383/oz Genesis is on track to meet upgraded guidance.

- As planned, Gwalia stoping progresses through a selective, lower grade portion of the mine schedule in the current March quarter, before the next lower cost bulk stope comes online in the June quarter. So we can expect grades to drop in the current quarter after rising in the December quarter, but Gwalia will return to higher gold grades in the June quarter this year. Gold mined at Gwalia underground for the December quarter was 35.3koz at 6.0g/t vs. the September quarter which produced 29.9koz at 5.0g/t. Remember that Gwalia underground is now 2km deep (vertical depth), so one of the deepest producing gold mines in the world, and by far the deepest in Australia, so it takes some time to get that ore to surface for milling, however Gwalia underground is not where Genesis' main growth is going to come from.

- At Ulysses underground, stoping successfully commenced late in the December quarter following the completion of escapeway installations, ahead of schedule. Ore production totalled 3.5koz mined at 3.4g/t (September quarter 2.7koz at 3.2g/t). Ulysses is ramping up, and will be significant for them in the future.

- The Leonora mill processed 349kt at 4.1g/t (September quarter 345kt at 3.5g/t) with a metallurgical recovery of 93.8% (September quarter 93.1%). Building on the processing rates accomplished in August and September 2024, the Leonora mill achieved a full half year of delivery at nameplate capacity of 1.4Mtpa being the first time since 2015 that the mill has been fully utilised. Importantly, grades increased and recoveries did also (vs the previous quarter).

I won't go on - it's all in their quarterly report. Point is, Raleigh is delivering on his promises, as he did with Saracen previously.

And they have a nice tailwind with the Aussie gold price STILL being on a tear:

Aussie gold prices on the left, US$ gold prices on the right.

Source: https://goldprice.org/

Yep, investment thesis is still on track.

Disc: Holding.

Further Info: Excerpts from quarterly report:

Ulysses Underground:

Leonora Mill (formerly known as the Gwalia Mill when it was owned by St Barbara - SBM):

The following is just one example of future growth with Genesis:

And their current Hedging situation:

Plenty of flexibility through the use of collars and put options, with minimal forward sales of just 13,500 ounces of gold in total.

Lots to like about GMD!

14-Nov-2024: Genesis Minerals (GMD) held their AGM today, and I've attached links to their Chairman's Address and AGM Presentation below:

Highlights and interesting stuff:

Skin in the game: They have 7 people on their Board, of which 5 hold GMD shares, and those shares represent 3.1% of the SOI (shares on issue). The vast majority of those shares (the 3.1%) are held by their Managing Director, Raleigh Finlayson, who holds 26,213,858 GMD shares plus another 12,250,000 options.

Data in that table above was sourced from Commsec.

We have an updated map that also includes Aphrodite and Zoroastrian between Menzies and Kalgoorlie, which are future growth options, however the focus is still clearly on that area between Leonora and Laverton in WA, and Raleigh loves Leonora as a town, and supports the local community through GMD:

Here's that map again, by itself, hopefully larger:

They've come a long way in a couple of years since the Saracen merger with Northern Star and Raleigh subsequently leaving Northern Star to build up Genesis from bugger-all to now a $2.6 Billion company.

While gold stocks have been sold down since Trump won the US election, which includes the Aussie gold sector being the worst performing sector both Tuesday (12th Nov) and today (14th Nov), on the back of a moderating (falling) gold price, GMD remains within their uptrend channel:

Right in the middle of it actually, at $2.25.

The company is well positioned for continued growth also:

Source of Slides: GMD AGM Presentation [14-Nov-2024]

They also released this on Tuesday: Updated - Strong drill results support growth [12-Nov-2024]

And this on Monday: Presentation - Accelerate, UBS Australasia Conference [11-Nov-2024]

All good. Holding. Smaller position here. Larger position in my SMSF.

05-Aug-2024: GMD D&D Presso: https://gmd.live.irmau.com/pdf/8f1e27d6-e139-474d-ae74-3aecd578eec1/Corporate-Presentation-Accelerate-Diggers-and-Dealers.pdf

Also, back on 19th July: Gold explorer Ordell Minerals debuts on ASX after raising $6m.PDF

GMD own 8% of ORD (Ordell Minerals) with another 8% of ORD owned by ORD's CEO and Managing Director, Michael Fowler, who was also the CEO and MD of Genesis Minerals (GMD) up until 23-Feb-2022, the day that Raleigh Finlayson took over those positions at GMD. So Genesis and Mick Fowler are the two equal largest shareholders in ORD.

ORD might be another one to keep an eye on - I don't think Genesis will want to take them over, because ORD's main asset - their Barimaia JV Project - is up near Mt Magnet, not down near Leonora or Laverton, but what about Ramelius Resources (RMS) - who are already all over that Mt Magnet area.

Ramelius have already taken a 17.94% strategic stake in Spartan (SPR) who own the Dalgaranga Mill there - to the NW of RMS' Mt Magnet mill. Barimaia is right next to RMS' Mt Magnet Mill (immediately SE of it).

About the Barimaia JV:

- Strategic location in the Murchison Gold District of WA

- Immediately SE of Ramelius’ Mt Magnet Gold Mine

- Opportunity to assess a drill ready ground package in close proximity to several producing gold mines

- Extensive gold system defined with limited drill testing

- Ordell has acquired Genesis Minerals Limited’s (ASX: GMD) 80.2% interest in the Barimaia Project by acquisition of 100% of Metallo Minerals Pty Ltd

- Genesis commenced the JV in 2017 following the acquisition of Metallo

- Exploration by Genesis during time of Barimaia JV was limited as a result of the focus on the Ulysses Project near Leonora

- Ordell’s objective is to define significant shallow (<100m) gold resources

- Extensive gold system defined associated with felsic intrusion host rocks within mafic-ultramafic stratigraphy

- East-west orientation of the stratigraphy confirmed by Genesis drilling and interpretation in 2018

- No modern exploration until post 2010

- The McNabs Prospects are under up to 10m of transported cover

- 2021 AC drilling extended the ENE trending Au anomalous corridor a further ~900m to the east

- 2024 drill testing over 3.5km of strike

Source: https://www.ordellminerals.com.au/barimaia

So, this is a non-core asset of GMD that they have spun out effectively, but retain an 8% stake in, and the natural owners are definitely Ramelius (RMS).

And RMS have half a billion in cash and liquid shares (in other goldies), plus are producing gold from multiple locations at low costs and high margins.

Further Reading: Maiden drill program underway at the Barimaia Gold Project, WA 2,600m: Phase 1 RC drill program to target Eridanus-style discoveries.PDF (31-July-2024)

Disc: I hold GMD and RMS shares, but not any ORD directly. ORD's entire market cap is only about $13m according to the ASX website, so they would be a small bolt-on acquisition for RMS, however RMS may elect to wait and see if ORD find anything decent with their drilling before having a sniff. RMS' and GMD's m/caps are both over $2 Billion.

21-Mar-2024: Five-year Strategic Plan plus Growth strategy underpinned by robust Reserves

Below are a selection of slides from that 68 page/slide presso [the "Reserves" one was 370 pages long - links above] which was released after the market had already closed this arvo, so we'll see the market's reaction tomorrow morning.

Some of the areas covered:

And here are some of the maps that they included:

Below is how they anticipate those assets feeding their Leonora Mill (shown in Blue) and their Laverton Mill (shown in grey):

Below is a wider view that shows where their Aphrodite and Zoroastrian projects sit in relation to that lot above:

And here's that map a little larger:

That map is of their main exploration targets where they hope or expect to find more gold, below is the Bardoc Gold Project back when Bardoc Gold was a listed company in March 2020. It was from their PFS:

Aphrodite is at the top, and would be just below the Chameleon Trend target in the Genesis map. St Barbara acquired Bardoc Gold in April 2022 after announcing the acquisition back in December 2021, and Genesis acquired all of St Barbara's WA Goldfields (Leonora) assets (including the Bardoc Gold assets) in the middle of calendar 2023. There are over 3 million ounces of gold there already that they know about - mostly in Aphrodite and Zoroastrian - however Genesis don't even talk about that, as they much more focused on their assets between Leonora and Laverton, those assets within that 100km radius of Leonora, but we shouldn't forget about the Bardoc Gold assets, which are around 150km south of Leonora. They are also significant!

There's a lot going on at Genesis Minerals.

Yep, I hold GMD shares.

05-Feb-2024:

Red5 Dangles the Carrot for Genesis in $2.2Bn Merger with Silver Lake | Daily Mining Show - YouTube [Money of Mine podcast, 05-Feb-2024]

Chapters:

0:00:00 Preview

0:00:00 Introduction

0:01:08 Silver Lake's alternative marketing strategies

0:07:02 Red 5 MERGING with Silver Lake Resources

0:43:00 Potential Lynas and MP Materials merger

0:44:29 Centaurus get Environmental approvals

0:45:09 Silvercorp/Orecorp update

0:45:36 New Copper producer on the ASX

The short version:

The best thing about SLR is their large cash balance. The worst thing about RED is their debt and lack of cash, and to a lesser extent their out-of-the-money hedgebook. Putting the two companies together certainly makes sense for RED, as they need SLR's cash, and SLR will have better prospects to spend their cash on than they appear to have currently - in terms of exploration spending in highly prospective areas. And it will frustrate the hell out of Raleigh Finlayson at Genesis (GMD) who wants Leonora all to himself (or within his company, Genesis Minerals). Luke Tonkin might not have stopped the Gwalia sale from going through (from SBM to GMD), but he might just end up with RED, unless this deal gets trumped by Raleigh/GMD with a better deal.

The best thing about RED is their KOTH gold mill which is close to one of GMD's big gold deposits that they intend to develop. But does Raleigh Finlayson think Genesis Minerals (GMD) needs KOTH yet, or ever? The MoM boys have a long and detailed discussion about these and many other questions in today's poddy - links above - and for my thoughts see here.

14-Dec-2023: Genesis (GMD.asx) has just agreed to buy a couple more gold projects, this time from Kin Mining (KIN.asx).

GMD-to-acquire-the-Bruno-Lewis-and-Raeside-gold-projects.PDF

GMD-Reporting-on-select-Kin-Mining-gold-projects.PDF

Kin-Receives-$535m-from-Sale-of-Gold-Deposits-to-Genesis.PDF

That's $53.5m, not $535m as the KIN announcement file name suggests - can't have dots in the middle of file names - I wish companies would stop doing that, as it can give an entirely wrong impression until people open the announcement and read it properly.

Below is the first Page of GMD's first announcement, with some notes from me on the right:

Map from page 2 of that same announcement:

As I write this, GMD's SP is up +8% at $1.80 (closed at $1.665 yesterday), however they spiked up to as high as $1.90 this morning which was +14.1% above yesterday's close. They got down to below $1/share in mid March, so they're up over +80% from there.

KIN is up +10%, but were up +16.7% earlier at 7 cps (closed at 6 cps yesterday, currently trading at 6.6 cps).

The rise in the GMD share price today might seem a bit overdone for such a small acquisition, but it's more about the fact that the market may be coming around to my way of thinking in terms of Raleigh being less likely to be bidding for RED (Red 5) now. My argument is that RED has now become too expensive, and their mill is no longer needed by GMD now or in the near term, AND that SLR have a blocking stake in RED that they would almost certainly use to frustrate any takeover of RED that GMD might attempt. It would be a negative if Raleigh tried to go after RED at current levels because he would almost certainly be overpaying, however with every small acquisition like this the likelihood of GMD making a near-term bid for RED reduces in the eyes of the market.

In short - the roll-up (growth via acquisition) model remains intact without Genesis clearly overpaying for any assets that they are acquiring - so all good, thesis remains on track. The market is liking the progress to date.

Sidenote: Saturn Metals' (STN's) Apollo Hill gold project is absolutely in the firing line for Genesis Minerals. Apollo Hill is around 40km south east of the Gwalia (Leonora) Mill. RED's KOTH (King of the Hills) mine and mill are around the same distance north west of Gwalia/Leonora (see map above). RED's market cap is $1.17 Billion. STN's m/cap is less than $40 million - currently $33.46m according to the ASX website. Genesis could buy all of Saturn (STN) for less than $100m, or just Apollo Hill, although the price difference wouldn't be much considering Apollo Hill is STN's main asset. They bought it off Peel Mining (PEX) in mid-2017.

That's from the Saturn Metals website: https://saturnmetals.com.au/projects/apollo-hill/

...which needs to be updated - as it shows Gwalia as still being owned by SBM and Mt Morgans still being owned by Dacian (which is now 100% owned by Genesis) - plus it shows Apollo Hill as having 1.47 Moz (million ounces of gold) in the ground (see below) but the up-to-date map from today's GMD announcement (scroll up for that - towards the top of this straw) shows Apollo Hill as having 1.8Moz. Not particularly high grade, but close to Leonora. Raleigh would have an eye on that one for sure.

Disclosure: I hold GMD shares, and I have STN on a watchlist now.

That's a better buy than RED is at current levels - for sure. The major differences are that RED are in production, have WAY more gold, at higher grades, and a very decent mill as well, but they're priced for all that at over $1 billion. So STN is high risk for sure, and RED is expensive but de-risked. If I was to invest in STN, it would be an appropriately small punt rather than an investment, because they don't make any money, and they could go broke if they're not taken over by somebody like Genesis. High risk means I would put way less money at risk, but I'm not pulling the trigger on them yet - just on a watchlist for now.

07-Dec-2023: Genesis-now-owns-100-per-cent-of-Dacian.PDF

Dacian Gold (DCN) has now been removed from the ASX list. As I have said elsewhere (here), with full control of the Mt Morgans Mill (that DCN owned), as well as full control of the Gwalia Mill (that Genesis bought from SBM at the end of June), Genesis now have sufficient ore processing capacity in the Leonora (WA) area to satisfy their immediate and near-term requirements, so there is no pressing need for Raleigh Finlayson to go after Red 5 (RED) and their KOTH (King of the Hills) Mill, which has been widely expected by the market, and is one of the reasons why the RED share price has been on a tear over recent months.

I'm fairly certain that Raleigh won't make any moves on RED in the next few months, certainly not while their share price is so high, and with SLR (Silver Lake Resources) owning 11.08% of RED (a blocking stake) and SLR's Luke Tonkin having form for going out of his way to frustrate Raleigh when he was purchasing SBM's Leonora assets for Genesis (GMD) earlier this year. I hold GMD shares by the way, and I'm very happy with their progress so far.

And I'm also very happy to be OUT of SBM.

27-Nov-2023: Just noting (1) that GMD hit a new 12 month high closing price of $1.76 today and also reached an intra-day high of $1.785, another record, and (2) that despite holding them both here and IRL, I haven't posted any straws on the company.

That ends now!

Firstly, the company is in a sector with some tailwinds - gold was one of only two sectors in the green today (see below) and secondly, it's a growth story via both organic and acquisitive growth - in fact Raleigh Finlayson has been very upfront about his intentions to roll up all of the good gold around Leonora into Genesis Minerals (GMD), and he's already bought all of SBM's Leonora gold and gold producing assets, including Gwalia, Australia's deepest operating gold mine, the 1.4 Mtpa Gwalia Mill, and some advanced gold projects around the same area (Tower Hill open pit, Zoroastrian high grade underground mine, and others) to add to the ones GMD already had, plus Dacian Gold is also now 100% owned by GMD, which comes with their Mt Morgans 2.9 Mtpa Mill, with more than twice the current annual ore processing capacity of the Gwalia Mill.

If a picture is worth 1,000 words, the following should be worth around 20,000 words...

Above: Gwalia Gold Mine, circa 1921. Below: Gwalia today (or recently).

And Below - the Mt Morgans Gold Mill:

d

Zenith Energy's BOO (Build-Own-Operate) Power Plant at Mt Morgans (above) and Mt Morgans Mill by night (below) during commissioning by GR Engineering (GNG).

They are also the 4th most shorted company on the ASX according to Shortman.com today. They were the third most shorted company last week:

But Core Lithium have leapfrogged them since I took that screenshot, so GMD are now the 4th most shorted.

The GMD shorting may have peaked however, and we may have seen a little short squeeze today (GMD +6.5 cps or +3.83% to $1.76).

The screenshot below is from this evening:

Source: https://www.shortman.com.au/stock?q=GMD

That data does not include today as there is 4 day lag, as explained above.

In terms of WHY people are shorting Genesis, the prevailing theory seems to be all about Red 5 (RED) and that either (a) that Raleigh's Leonora Consolidation Plan is going to turn pear-shaped now that Silver Lake Resources (SLR) own 11.08% of RED (bought as a "strategic investment" according to SLR's MD, Luke Tonkin) and have proven to be adversarial towards Raleigh and Genesis by putting in multiple rival bids to try to prevent Genesis from acquiring St Barbara's Leonora assets earlier this year despite SLR having zero assets in the Leonora area themselves (so zero obvious synergies for SLR), or (b) that Raleigh is going to end up overpaying for all of RED - based on Genesis paying over-the-odds to mop up the final 20-odd-per-cent of DCN - and that will cause a negative re-rate of Genesis by the market at that time.

In reality, Genesis don't actually need RED and their KOTH (King of the Hills) gold mill now that they (Genesis) have full control of both the 1.4 Mtpa Gwalia mill and the 2.9 Mtpa Mt Morgans mill. I'm sure Raleigh is still interested in acquiring RED, purely as part of his Leonora gold asset consolidation plan, but he doesn't have any pressing need to do it soon now that he has all the milling capacity he wants for the time being. He can afford to bide his time - so the ball is now in Red 5's court - and their management - to prove that they deserve the positive market re-rating that they've received - RED's market cap has grown to $1.12 Billion now (yes, with a "B", not an "M") and they really don't look THAT good to be honest. They were trading at 13 cps in February and they closed at 33.5 cps today. The market is now valuing RED ($1.12B) as being worth more than SLR ($963m) and SLR have a much stronger balance sheet, a pile of cash, more mines, more mills, better quality assets, and they're producing a lot more gold at much lower costs than RED are. And I don't want to own SLR, due to their management, so I definitely am not buying RED at current levels!! My best guess is that the Red 5 (RED) share price comes down from here as the M&A premium comes out of it. Either way, Raleigh is probably going to ignore RED for a while. He's got plenty to be going on with currently. I'm sure RED will remain on his longer-term radar, but there's certainly no reason for him to move on them while their share price is this high.