Price History

Premium Content

Premium Content

Premium Content

Source: Slide 3 from GNG's March 3rd HY26 Investor Presentation - green stuff added by me.

From Vault Minerals (VAU) Today (Thursday 26th March 2026): KoTH-stage-1-plant-upgrade-commissioning-commenced.pdf

Excerpt: "Stage 1 of the plant upgrade project, to increase plant throughput capacity to ~6.0mtpa, has progressed on time and budget and is now in the final stages of commissioning."

Another on-time-and-on-budget build by GNG, with Stage 2 of the KoTH plant upgrade to follow.

Disclosure: GNG is currently one of my two largest real money holdings (along with LYL) and the same applies here on SM as well. I do not currently hold any VAU shares.

Despite a recent drop in the gold price, gold producers like Vault (VAU) are printing cash at current spot prices and they all want their plants expanded or new plants (mills) built ASAP, and GNG's expertise in that area remains in high demand.

They (GNG) recently announced that they had been names preferred contractors for projects by Brightstar (BTR: their Laverton Mill build) and Genesis (GMD: their Tower Hill Mill build) so we can expect confirmation of those contract awards shortly.

As they say in that slide above, they are also expected to be awarded the EPC contract for the Bellevue Paste Plant (by BGL).

Also, @BkrDzn and I both expect GNG to be awarded the Black Swan mill conversion contract shortly (from Nickel to Gold) by Horizon Minerals (HRZ) now that they (HRZ) have their financing all sorted and have a positive PFS for Black Swan (done by GNG) which is all they (HRZ) said they said they needed for a FID. This announcement from HRZ on March 16th (10 days ago) backs up that assumption that they're super keen to start that mill conversion ASAP: HRZ-Key-Project-Team-Appointment.pdf

Additionally GR Engineering Services (GRES, ASX: GNG) are working on other studies that should lead to other work, such as the Forrestania Nickel-to-gold mill conversion for Medallion Metals (MM8).

There's PLENTY of work for GNG over the next few years, even if gold drops another A$1,000/ounce, and I personally think it's more likely to rally from here than fall much further.

They've been sold off recently to below $4 - looks to me like a good buying area and I'm trying to accumulate more here on SM, but I'm being hampered by the 20% limit here on individual positions at the time of purchase or top-up. I've got over $150K worth of them already in my (real money) income portfolio, but I'm considering topping that position up further also.

GNG is my 2026 stock pick as well as a large personal holding of mine, so I'm certainly talking up my own book here, but it's hard to work out how they could run out of work over the next couple of years, and they are a profitable company with zero debt and high insider ownership that is run conservatively and pay higher-than-average fully franked dividends, so I reckon it's worth pointing out when things are shaping up well for them.

4th March 2026: I was asked today about my opinion on how tethered companies like SXE, GNG & LYL are to the overall commodities cycle. I thought my answer was worth sharing with the rest of the community so here it is (just my own opinions, for whatever they're worth):

SXE is not too dependent on commodity cycles as most of their revenue and earnings are derived from commercial, infrastructure etc now and only a minor percentage from miners, which is a big change from a few years ago when they were almost 100% mining services.

I reckon that's a great question to ask their CFO tomorrow. I might add something along those lines to slido in a minute. [I've done that now]

XRF and C79 are going to be fine because sample testing continues as long as production continues - i.e. grade reconcilliation testing, mine planning-related testing and deposit extension testing, etc., however those testing machine and consumables companies do get an extra tailwind from further exploration activity when the prices of the commodities they are assaying for are elevated and incentiving explorers to spend more.

Something to note is that when the gold price is high, as it is now, junior explorers are able to raise money much more easily, compared to when we are the bottom of a cycle and it gets much, much harder, so there is more cash available to spend on drilling and testing when commodity prices are high. But that's just the junior explorers.

GNG and LYL are probably 80% gold - somewhere between 70% and 80% I would say in terms of revenue and earnings contributions, however they also do copper, rare earths, lithium, and other metals. LYL has some other divisions but they are almost all commodity-(metals)-facing, other than their rail (infrastructure) servicing division which is a small part of their business. GNG have GRPS which is their energy sector services division which services oil and gas infrastructure - as in multi-year operations and maintenance contracts with large energy players for kit like drill rigs, barges, on-land oil pumping stations, etc., but again, it's a smaller part of their overall revenue mix compared to their larger EPC business which is squarely facing the mining sector.

So in that respect GNG and LYL are certainly impacted by cycles, however because their studies often take years - and they both do those studies, like Scoping (SS), Pre-Feasibility (PFS), and Definitive/Bankable FS (DFS/BFS), also sometimes just called FS - Feasibility Studies - and then the E&C contracts (EPC/EPCM/EP&PM/etc.) contracts usually also take between 1 and 2 years, sometimes longer for really big projects - NST's Hemi in the north of WA (the De Grey Mining assets that NST acquired) is going to probably take longer than 2 years to build when NST get around to that - and Barrick's massive Reko Diq in western Pakistan that LYL did the studies for and then declined to participate in the final stages of the EPCM contract tender process (so walked away from - for risk management reasons) would have taken somewhere between 3 and 5 years to build - from what I've read - the studies tend to be commissioned when sentiment around the commodity is more positive but the actual builds (the E&C) can stretch through various stages of a cycle.

There is always a risk that a company pulls the plug on a project half way through a build because one of more metal prices have tanked, if they are in a position to do so, and that actually happened two years ago (in mid-2024) to GNG with BHP's West Musgrave nickel-copper project in WA. GNG had previously (when nickel prices were higher) completed the project studies for the then-owners, OZ Minerals (were OZL) and were awarded the $312 million EPC contract (see here) in April 2023 by OZL who were then acquired by BHP the following month (in May 2023). BHP were initially happy for GNG to proceed with West Musgrave, however a year later, in July 2024, due to the nickel price having dropped so low that BHP's nickel production was no longer economic (they were losing money on nickel production), BHP decided to put all of their nickel assets on C&M, and shelve (postpone/defer) West Musgrave, so GNG were paid for what they'd done up until that point, and also paid some compensation for the inconvenience of having that project put on ice, but the project just stopped and has not proceeded since then. I expect GNG will get the call-back from BHP if nickel prices rise enough and they'd be back on the job there, but BHP can be a bit of a dinosaur with their decision making, so I wouldn't bet the farm on that happening any time soon.

So, there is certainly risk around commodity prices relating to those two (GNG & LYL) but not SXE very much, however consider this:

- Wars don't last forever and one of the side effects of war is supply constraints as we are seeing with oil and gas not being able to be exported out of certain middle east countries right now because their ships have to pass by Iran which is blowing up any ships they see off their coast if they are able to. If this war expands, metal prices could actually get a tailwind rather than a headwind. Weaponry and ammunition takes metal to manufacture and countries like the USA are not totally self-sufficient with a significant percentage of those metals. Wars tend to increase production in some areas of the economy while inflation due to supply-side issues can stifle production in others, or make it more expensive.

- Gold companies tend to get sold down initially along with all other liquid assets in times of panic but then the gold price rises in times of uncertainty and hightened volatility and that then drags up the prices of gold companies and also those companies that service the gold industry, as both GNG and LYL do. Overall, wars that matter to most people tend to result in a higher gold price than a lower one. Wars that don't matter to most people can have almost no effect on the gold price. This one DOES matter to most people so my expectation is that the gold price goes higher.

- There are a number of companies, like VAU, HRZ, MM8, BTR etc. who have either now fully funded or are very close to fully funding their new gold mill builds, gold mill conversions (nickel to gold), or gold mill expansions, where GNG have done all of their studies and are going to build/convert/upgrade those mills. These companies are committed to going ahead with that expenditure over the next 6 to 18 months. Brightstar (BTR) announced today that they have just issued US$120 million worth of Bonds, which together with their recently completed placement and SPP which raised a combined A$193 means that the last piece in the funding jigsaw for their Goldfields Project (in WA) is now in place and GNG have already commenced work on that project with FEED work and orderering long-lead-time items. As part of that announcement BTR have also stated today that they have enough funding now to not only cover that new mill build but to also advance a second project, their Sandstone project (also in WA). To quote them: "The combination of the Bond issue and the previously announced A$193 million equity raising means Brightstar has secured all required funding to construct and deliver the Goldfields Project, while maintaining a substantial budget to advance the Sandstone Project through to Final Investment Decision." And that's today, in the middle of this war in the middle east. So I would suggest that this war isn't going to slow down any gold project developments, if anything it may increase the urgency for these companies to get these mills built even more quickly to take advantage of the higher gold price sooner. Many companies are just too far into the process to bail now, especially smaller companies that have limited alternative options. It's much easier for a company like BHP to shelve their nickel assets (as they did in July 2024) when they are one of the world's largest iron ore producers, and they have copper, manganese, met coal, potash uranium, zinc and silver assets all over the world (I reckon they're still the largest mining company in the world at this point in time). Much harder for companies where the mill build they're working on will be their first producing asset.

- Where we are in the cycle - this one is a big one - have a read about what Hedley Widdup reckons about where we are right now in the commodities cycle - he is famous for his cycle clock and we're between 6 and 7 right now (cue the 6/7 hands weighing air action here that all the cool kids are apparently doing) according to Hedley, so at the start of a new mining boom - you can find that material under LSX here on SM. Below is a sample slide from his most recent LSX presentation. LSX (Lion Selection Group) is a junior-mining focused LIC that Hedley runs (and his father Robin Widdup founded) that invests only in early stage miners who have plenty of upside potential - he is mostly invested in gold companies at this point, and his portfolio and my own SPF (speccy portfolio) share a few names - like BTR, MM8, AZY & GBR - but he's not Robinson Crusoe on that mining cycle call - plenty of other analysts that I respect and follow are also calling the same thing.

He backs this up with plenty of data - have a flick through his latest presso here to see what I mean.

So I wouldn't be worried about cycles right now, I'd be thinking of where we most likely are in this cycle, plus this middle east conflict, as tailwinds rather than headwinds.

Share prices will be volatile, but I'm talking about what this means for the earnings potential of these companies rather than what might happen shorter term with their share prices. In the short term, we will likely get to buy good companies at lower prices. I don't know how low they'll go, but the lower the better if you're a buyer. And if you hold them already and have a 3 to 5 year investment time horizon or longer, then short term price volatility doesn't matter even if you already have your full allocation of a company.

20-Feb-2026: HY26-Financial-Results---Media-Release-(GNG).PDF

No Presentation from GNG yet to accompany these H1 results. In Feb 2024 they released their presso on the same day as the results, however last year (Feb 2025) they released the results in Feb and the Presso in March, as shown below:

I have just emailed their CFO to enquire when they expect to be releasing their FY2026 H1 Results Presentation. I'll share that here as an added comment once I receive a reply.

Interesting market reaction to GNG's results today - they were sold down -11% but still finished above their Monday (16th Feb) close of $4.57/share, so in terms of "value" being "wiped off", it's merely 4 days worth.

Perspective. Also, if you compare that market reaction today (as shown above) to the market reaction to Lycopodium's (LYL's) results on Wednesday, they both started off as very similar, with LYL also being sold off -11% (low point of $13.18 at the start of the trading day, being -11.19% below their previous day's $14.84 close), however what happened then was that the LYL SP bounced back up during the day (Wednesday) as people digested LYL's presentation rather than that just rely on their initial reaction to those headline numbers vs their PCP, and their minor full year revenue and profit guidance downgrade, as shown below:

GNG did not downgrade their full year guidance, they just had a weaker H1 this year than their H1 of last year (FY2025), however with an expected stronger H2, they are still on track to meet their full year guidance given at their November AGM of FY26 Group revenue of between $500 million to $520 million (FY25: $479.0 million). This guidance was repeated in today's results announcement.

So assuming they don't have significant margin reduction, we're looking at higher revenue and higher profits for the full year when they report in August (compared to FY2025).

The difference is that without any results presentation yet from GNG that fleshes out how busy they are and why they are confident of a stronger H2, the market stuck with that negative sentiment from the headline numbers for the half being lower than GNG's previous corresponding half (H1 of FY2025), and there was therefore no share price rebound during today for GNG, as happened on Wednesday with LYL.

It will be interesting to see how the market reacts when GNG do release that H1 Results Pressoentation.

Some highlights from today's report from GRES (GNG):

- They've increased their interim fully franked dividend by +20% to 12.0 cps (HY25: 10.0 cps, fully franked).

- They have $86.5 million cash in the bank vs $71.0 million 12 months earlier, and no debt.

- Their MD, Tony Patrizi, said: "The HY26 period was characterised by solid operational performance across the Group. Engineering, design and construction works are continuing on key projects including the King of the Hills Operations Stage 1 and Stage 2 Upgrade Projects, Eloise Copper Expansion Project, Lake Way Upgrade Project and Dalgaranga Paste Plant Project. Early works have commenced on the Laverton Processing Plant and Bellevue Paste Plant Projects. During HY26, the Kainantu Gold Project successfully achieved practical completion. GR Engineering is currently working on multiple minor projects, ongoing FEED and early contractor involvement engagements and is involved in a high volume of studies across a broad range of commodities and geographies." They are very busy!

- Their smaller energy industry services division, GR Production Services (GRPS), achieved revenue contributions primarily through the provision of longer term (multi-year contracted) operations and maintenance services to the energy sector and during HY26, GRPS has been able to increase its earnings visibility through additional work from clients including Santos, Chevron, QGC and Mitsui E&P Australia. Tendering activity remains high.

- Mipac and Paradigm are leading providers of control systems, operational technology and engineering services in the mineral processing, iron ore and energy sectors. The process controls business continued to deliver control systems, automation and digital solutions for key repeat clients. During HY26, Mipac and Paradigm were awarded new contracts from clients including BHP, Rio Tinto, First Quantum, Ok Tedi and HudBay, so some big names in there.

- The Group’s contracted and near term pipeline across the business is solid and is continuing to grow.

- They have today reaffirmed their previous revenue guidance (provided at their AGM in November) for FY26 Group revenue to be in the range of $500 million to $520 million (FY25: $479.0 million) - which at the guidance mid-point of $510 million, would be a +6.47% increase on FY25, with of course potential to exceed that guidance if they convert more of their tender pipeline into signed contracts and receive some initial revenue from those new contracts before June 30th.

Most of that is quoted directly from today's H1 results announcement (HY26-Financial-Results---Media-Release-(GNG).PDF), so yeah, nothing scary in there for mine, and they are my largest real money position now.

Still a happy holder, and looking forward to reading their H1 Results Presentation when they release it.

17-Feb-2026: Preferred-Contractor---Laverton-Processing-Plant.PDF

Nice!

Still relatively low volume with less than $2 million worth of shares traded all day, so that +7.22% rise today was partly due to the low liquidity which is shown on the sellers side above (the bids and the gaps between them).

There's 5x the number of shares bid for on the buy side than there is shares offered on the sell side after the close, as shown above (280,675 vs 55,428), and almost 10x the number of buyers than sellers (only 8 parcels for sale on the sell side, but 76 parcels on the buy side).

That all changes during every trading day obviously, otherwise there couldn't have been 1,507 trades today for 418,060 GNG shares, but the lack of liquidity does tend to accentuate / exaggerate the moves, both up and down, in this case up.

The BTR contract for the design, procurement, construction, installation and commissioning of Brightstar's 1.5 Mtpa Laverton gold mill is still subject to the achievement of FID (Final Investment Decision) and finalisation of project funding, but that's really a formality after BTR's recent CR, and as GNG said in their announcement today, FID and financing are anticipated to be completed by late March 2026, so within 6 weeks of today.

The estimated contract value is $115 million. An early works agreement has been executed and ordering of long lead items and engineering works by GNG have commenced.

This is one of a number of both new mill build contracts and mill conversions that GNG are likely to announce they've won over the course of this calendar year.

That statement of mine is based on the number of studies that GNG are involved in, and we can assume the majority of those that are related to gold are going to result in favourable project economics in the current gold price environment, so will proceed (most of those projects will get built).

The company that does the studies (scoping, pre-feasibility then feasibility studies) is usually the company that gets awarded the EPC contract if they also have that capability and capacity - not all studies firms do E&C [engineering & construction such as EPC/EPCM contracts], but LYL and GNG both absolutely do. The company that did the studies is intimately involved in the project already and knows it back to front so that's why they have the inside running for the E&C work.

This is why knowing which studies GNG and LYL are involved in really helps with predicting how much work they are likely to be awarded in the next couple of years. GNG tend to release more details about study wins than LYL do, but both will release announcements relating to these sort of major EPC/EPCM contract wins.

LYL has been quiet on that front since their Nyanzaga-Gold-EPCM-Contract-Award.PDF announcement on July 30th last year, but then, to be fair, so have GNG until today. I just know that GNG are involved in studies for DVP, MM8, HRZ, BGD, VAU and EVN, and there are a heap of other gold projects out there that they could also be working on, or could be contracted to do studies on that may well lead to future EPC work.

GR Engineering Services (GRES) (ASX:GNG) is a good company to have exposure to, and they happen to be my largest real money holding now, as well as my stock pick for the 2026 SM stock picking comp.

GNG are also one of my top 3 positions here on SM, probably my second largest now after today's price rise.

Disc: Held (absolutely!)

P.S. LYL will report tomorrow (Wednesday 18th Feb) and GNG will report a week later on Wednesday 25th Feb.

25th August 2025: GNG-FY25-Financial-Results---Media-Release.PDF

GNG typically release a results presentation later in the day or during the following week rather than when they release their results, and this appears to be the case once again with no presentation being lodged yet, just the media release announcement (link above).

They have released their Full Year Statutory Accounts.

Here's how the did in FY25 compared to FY24:

As usual, they did not provide any percentages or arrows - that green stuff has been added by me. A small decrease in cash from $74.6 mill to $71 mill is nothing to worry about - the cash moves around a lot with these E&C contractors due to the timing of milestone and project completion payments, etc. They have negligible debt, basically they are debt free with a nice pile of cash relative to their market cap (which is currently $738 million).

Here is an excerpt from their announcement today:

They did disclose more info on their Energy division (GRPS) however they derive the bulk of their income from their Mineral Processing (MP) division, so that's the one that interests me most. Please read the whole announcement (link at the top of this straw) for full details, including their Energy Division performance during the year.

I personally think that what's exciting investors the most about GNG is the sheer number of studies (30) that they are undertaking for clients and we know that some of their clients (like DVP, HRZ and MM8) have already indicated that they expect GNG to be awarded the EPC contracts for those projects when those projects get greenlighted to proceed, which in many cases is going to be in the current financial year or calendar 2026, so we can expect some more contract win announcements from GNG over the next 12 to 18 months. E&C companies like GNG and LYL who do the scoping and then the PFS and FS studies for their clients' projects tend to win the EPC contracts to design and build those projects most of the time, when those projects receive positive FID decisions - not all projects ultimately get built - so study numbers are a leading indicator of future work.

That final dividend was 10 cps last year, so it's 20% higher this year. Fully Franked again.

The market continues to drive GNG's SP higher:

They made a new all-time high this morning of $4.62/share.

Lots to like here - very high insider ownership, zero debt, plenty of cash, profitable, growing, busy, tailwinds (elevated gold price), excellent management with a track record of superb capital allocation - they rarely make acquisitions and they are usually small and paid for using their own cash, superb industry position here in Australia, wonderful reputation that sees them winning more and more work, including from existing/previous clients, some baseline ARR from Energy (GRPS) division; the only negatives are that their MP division can have lumpy revenue and profits, their margins do move around a bit, and they can go through lean times because they're exposed to cyclical sectors like precious metals and base metals mining, but they have tailwinds right now rather than any headwinds.

Disclosure: Holding both here and IRL.

GNG is slated to report in a week's time, on Tuesday 26th August, and they've had a good run-up leading into these results:

And while I have been thinking they looked overbought, and have been lightening (trimming) my positions up here - although I still hold GNG - today's results and associated market reactions from SRG and MND, two other engineering and construction companies who have some similarities to GNG - have been encouraging:

SRG FY25 Full Year Results Announcement

2025 Full Year Results Briefing

2025 Full Year Results Presentation

Monadelphous-Reports-2025-Full-Year-Results.PDF

2025 Full Year Results Presentation

So, both SRG and MND have had a good run up into today's results and then been bid-up on their results on top of that. It's seems like there's some bullish positive sentiment returning to the sector on the back of positive results and increased work and profitability.

Looking forward to GNG reporting next Tuesday (26th) and LYL reporting tomorrow (Wednesday 20th August), particularly LYL (Lycopodium) as they are my largest position in real life by a decent margin.

18th June 2025: Firstly, I hold GNG, and remain bullish on the company, so that's the context of this post. However, their share price has run ahead of where I expected them to be right now, and I'm wondering if there's either a takeover brewing or else a fundie is building or increasing a position ahead of what they expect to be a better than anticipated full year report from GNG in August (for FY2025).

That 52 week high of $3.22 was hit yesterday, as shown below, and that's also an all-time high share price for GNG. Below is the recent daily trading data for GNG and I note that the last 6 trading days (prior to today) have been above-average volumes for GNG, and they've broken out to the top side of a pennant formation (as shown above).

Here's the past 3 months so you can see that breakout more clearly:

The share price ticked up to $3.16 (from $3.15) when I was screenshotting that, but it dropped back to $3.15 a minute later.

Below is a graph of GNG's share price since IPO and shows that they've been in a long term uptrend for 12 years now - since June 2013:

And they've broken up above that rising channel now, which I do not think is sustainable, however I do reckon it is likely signalling that somebody or some entity (fund or company) is building a decent stake, which is impossible to do in a low liquidity company like GNG without moving the share price.

In my largest real money portfolio (the one outside of my SMSF), GNG is the second largest position (behind LYL), but I haven't added to that position since early June (2nd) when I added more at $2.80, after also topping up in May at prices varying between $2.76 and $2.84 (I made 4 top up buys in May).

It's interesting because LYL (Lycopodium) is a very similar company, and their share price has been trading sideways between $10 and $11 for 3 months and they've been in a short term downtrend during the past 3 weeks, so this rise in the GNG share price on higher volumes does not appear to be an industry sentiment driven thing, it's specific to GNG.

I don't fully understand it yet, but I'll take it.

For further context, GNG have only released two new contract win announcements during the past 3 months (i.e. since their H1 results were released in Feb):

King-of-the-Hills-Operations-Stage-2-Upgrade-(GNG-05-June-2025).PDF

GR-Engineering-Awarded-Black-Swan-Plant-Engineering-Study-(HRZ-08-April-2025).PDF

They did release their HY25 Investor Presentation in mid-March, being just over 3 weeks after their H1 results were released, which included the following slide:

Typically understated confidence. They rarely make any acquisitions and when they have, those have been both strategically smart as well as earnings accretive. They might be about to announce another acquisition, but I also wouldn't be surprised to see another company try to acquire GR Engineering (GNG).

Of course it might just be that one of the three brokers that cover them (see below) have recently released an update and upgraded their call and/or their target price for GNG, and that the subsequent retail buying has caused the share price to break out simply due to the lack of sellers (low liquidity).

Source: https://www.gres.com.au/investors/analyst-reports.aspx

I'm not a client of Argonaut, EH or TC, so I don't have access to those reports. I do subscribe to FNArena, however FNArena don't cover those three brokers within their closely monitored "Expert Views" a.k.a. "Broker Calls", and only have TC on their "Extra Coverage" list (a.k.a. "B.C. Extra"), and they say (about that), "Please note: unlike Broker Call Report, BC Extra is not updated daily. The info you see might not be the latest. FNArena does its best to update ASAP."

FWIW, FNArena have summarised TC's latest three updates like this (below, latest one at the top):

Source: https://fnarena.com/index.php/analysis-data/consensus-forecasts/stock-analysis/?code=GNG

Could also be that news has leaked of an impending major new contract award to GNG. We shall see...

Disc: Holding. GNG is one of my largest positions at this point in time in my real money portfolios. And a smaller position here on Strawman.com.

24-Feb-2025: GNG-HY25-Financial-Results---Media-Release.PDF

Source: GNG-HY25-Financial-Results---Media-Release.PDF [24-Feb-2025]

See also: Half Year Financial Report and Appendix 4D.PDF

Disc: I hold GNG and bought more in my largest real money portfolio today.

I was concerned that this result might have been weaker than what had been expected, particularly with the very strong run-up that the GNG share price has had into this result, but I needn't have worried - they knocked it out of the park.

At today's close of $3/share (GNG's highest closing share price ever), paying 20 cps p.a. in dividends (10c interim + 10c full = 20cps per year), they're paying a 6.7% dividend yield, and that is fully franked, so a grossed up yield of 9.5% including the full value of those franking credits.

Again, income plus growth, gotta love it!

27-Nov-2024: FY24 Annual General Meeting Presentation.pdf

Also: GRES (GNG) 2024 Annual Report.pdf

I've been reducing my exposure to GNG leading up to today's AGM, despite the company being one of my favourites and having been a very positive performer for me over recent years, with a good percentage of those TSRs coming from their generous dividends.

At below $2/share they still looked like a buy, despite their current and near-term headwinds, and I was buying, but at around $2.20 and over, they looked like there was significant near-term downside if they couldn't pull a rabbit out of the hat and outperform again this FY.

The AGM presentation and commentary is usually a decent indicator of how they are travelling, particularly as it comes out towards the end of H1.

But to understand my concerns over recent months, we need to look at GNG's FY23 vs FY24, and their 2024 Annual Report:

The three projects I have highlighted there (above) all have issues. Kathleen Valley is Liontown's (LTR's) flagship lithium project, and lithium, as everyone knows, has been smashed - and Kathleen Valley won't be profitable at these lithium prices. I don't want to dwell on LTR much, but if you look at their 12-month share price graph, their SP has more than halved this past year from over $1.60/share to now under 80 cents/share (cps). GNG are constructing just two paste plants for Kathleen Valley in FY25 (this FY) and the total value of that work is just $71 million, so GNG's Kathleen Valley (lithium) exposure is not major, but exposure to lithium doesn't look as positive in FY25 as it did a few years ago.

The next one I've highlighted there, West Musgrave, is predominantly a nickel project, which was awarded to GNG by OZ Minerals before OZ Minerals were acquired by BHP. It formed the bulk of GNG's order book (dwarfing other projects) up until July this year when BHP announced a "temporary suspension" of both the West Musgrave project and also BHP's entire Nickel West operations, due to the persistently low nickel price with nickel having undergone a structural change due to low-cost Indonesian nickel now dominating the market.

I had expected West Musgrave to be shelved at some point, and I talked about that here earlier in this calendar year, and that did indeed come to pass in July, and GNG announced the expected financial impact for them from BHP's decision here: Market-Update---West-Musgrave-Project.PDF on July 12th - saying that FY25 revenue would now be $80m lower. My larger concern was that the bulk of that West Musgrave revenue would have flowed through to GNG in FY26 and that FY26 revenue from West Musgrave is now likely to be $0.

The market ran the numbers over the next few days, well - the very tiny percentage of the market that even know that GNG exists and are also interested in them as an investment opp did, and the share price was sold down -21.7% from $2.12 to as low as $1.66 on September 9th. I was buying at those levels (below $2 and especially below $1.80). This was, after all, something I fully expected to happen, so I figured if the market overreacted, which it did, it was a buying opp, so I was buying.

The third project I've highlighted there is Hastings Tech Metals' Yangibana REO project. I won't go into that in too much detail except to say that this was a significant project, worth $210 million to GNG, and Hastings have headwinds right now:

Cash-strapped Hastings yet to draw on taxpayer-funded loan [AFR]

Peter Ker, AFR Resources reporter, Nov 11, 2024 – 7.31pm

Cash-strapped rare earths developer Hastings Technology Metals has not been allowed to draw down the $220 million of taxpayers’ funds pledged towards its Yangibana project more than 33 months after the first tranche of the proposed loan was announced.

The federal government’s Northern Australia Infrastructure Fund confirmed that Hastings had still not met the conditions required to access the money, and the agency would need to review Hastings’ strategic pivot towards China before deciding whether to proceed with the loan.

Hastings is developing the Yangibana rare earths project in West Australia’s Gascoyne region.

The comments from NAIF add to the uncertainty over pre-revenue Hastings’ ability to fund the completion of the Yangibana mine at a time when billionaire businessman Andrew Forrest’s company, Wyloo Metals, is mulling whether to call in a $150 million loan over a debt dispute.

Hastings had just $9.9 million of cash on hand on September 30 and needs to raise close to $300 million to complete the construction of Yangibana, near Carnarvon in Western Australia.

The $220 million pledge from NAIF and a further $100 million pledged by the federal government’s Export Finance Australia agency were supposed to provide a large portion of the money needed for the construction of Yangibana.

The government agencies loaned the money on the condition that Hastings would build a rare earths separation plant for Yangibana.

That plan appealed to government agencies in an era when they were trying to break China’s stranglehold on the processing of the rare earth elements needed for defence applications and clean energy infrastructure.

But Hastings pivoted towards a cheaper strategy in May last year, with plans to produce an intermediate rare earths product. The company has since struck agreements to have that intermediate product processed in China and recently welcomed a Chinese investor to buy 9.8 per cent of its shares.

Asked whether the strategic pivot towards China had soured NAIF’s willingness to pump taxpayer funds into Yangibana, a spokesman said all ownership changes were monitored by NAIF.

“Any material changes to the product sales strategy would require detailed review by NAIF prior to funds being available,” said the spokesman.

“NAIF’s facility has not reached contractual close.”

A company linked to Hastings chairman, Charles Lew, loaned $5 million to Hastings last week, a move that has angered Wyloo, which believes it was a breach of the conditions attached to the $150 million loan it made in 2022.

If Hastings was deemed to be in default of the conditions attached to Wyloo’s loan, the lender would be able to demand repayment.

But Hastings tried to assure investors on Monday that Mr Lew’s loan did not amount to default on the Wyloo loan.

“Both facilities were established for separate purposes and are not in contravention of each other,” said Hastings in an ASX statement.

--- ends ---

Short version is that Wyloo, a large private company owned by Andrew ("Twiggy") Forrest (founder and major shareholder of FMG) is Hastings' major lender and there is a lending covenant that stipulates that Hastings must not seek aditional funding from anyone other than Wyloo, or else Wyloo can call in their loan to Hastings immediately, and Wyloo have now done that, and Hastings are not in any position to be able to either (a) repay Wyloo at this early stage, or (b) refinance at even vaguely reasonable terms so as to pay out Wyloo. The two companies are currently in dispute over this.

It pays to understand that as one of Australia's richest people Twiggy tends to take longer term views and make investments based on longer time horizons than most people, and Wyloo is bullish nickel over a longer term, like 10 to 20 years, and is willing to hoover up distressed nickel assets and then sit on them until the cycle finally turns. Hastings' Yangibana project is rare earths, NOT nickel, but clearly Wyloo also has the capacity and intention to also hoover up REO projects as well.

Nickel and rare earths all play into Twiggy's push for decarbonisation and his belief that demand for battery metals and rare earth magnets are only going to increase over time. Wyloo will likely end up with 100% ownership of Yangibana, which it has security over due to being Hastings' largest lender, and there are no guarantees that the project will continue to be built at this point in time. Once in full control of the asset, Wyloo could easily decide to defer construction, so Yangibana may also get shelved, like West Musgrave was been.

Hastings (HAS.asx) has a share price that has declined even more than LTR's SP; HAS had an SP that was over 70 cps at the start of calendar 2024 - and is now 28 cps, so that's around a -60% SP decline. In January 2022 HAS was trading at $5.70 (closing SP on 31-Jan-2022). They are now -95% below that level, in just under three years.

So perhaps you can see why I had some concerns about GNG's order book as at June 30, 2024, as described in their FY24 results and 2024 Annual Report.

Not all bad news though - here's the next page from their 2024 Annual Report:

Mipac seems to be firing, and the bolt-on acquisition of Paradigm Engineers in Feb adds additional capability in terms of electrical engineering and control systems, automation and technology.

And the level of Studies that GNG are engaged in sounds healthy.

Those who follow GNG & LYL know that a good number of these studies do lead to the award of EPC / EPCM (or in LYL's case also EPM or EP & PM) contracts if and when those studies flow through to positive FIDs (final/financial investment decisions) by the project's owners.

So, now we get to see where GNG see themselves now, as at today's AGM, and their outlook statement for FY25:

Considering that both GNG & LYL like to set realistic and easily achievable targets and then overdeliver (exceed those targets), GNG providing an FY25 revenue guidance range today (above) that starts just above their FY24 revenue (of $424.1 million) and their FY25 revenue guidance midpoint (of $437.5 million) that is 3% above FY24 revenue, is actually a good result when you consider those individual project and commodity headwinds I mentioned above.

And it's hard to say that GNG are going backwards or even going through a period of weaker demand based on their results and guidance:

Source: GNG AGM Presentation (today)

Source: Commsec

Source: GNG 2024 Annual Report

Source: GNG AGM Presentation (today) (above and below).

By the way, there are just two brokers covering GNG - see below - and they don't make their reports available to the public too often. So the company is not very well known.

The small part of the market that is interested in GNG wasn't underwhelmed at all with today's report; in fact it appears that the market got what they hoped for, it's "steady-as-she-goes" with no surprises in today's new info.

Source: Commsec at around mid-day today.

Here is how they describe their two main divisions in terms of order books (today):

Their "Energy" division (GR Production Services, previously known as Upstream Production Solutions) provides some decent ARR, however GNG's "Mineral Processing" division (GR Engineering) is where the big dollars are made, and it's more lumpy, and we see that West Musgrave and Yangibana have dropped off the June 30th list (see top of this straw) but that Evolution Mining's (EVN's) Mungari expansion (future growth project), Liontown's Kathleen Valley, and TSX-(Canadian)-Listed K92 Mining's Kainantu Gold Mine project are all still there (2nd slide up, above), and that Develop's (DVP's) Woodlawn restart has been added.

So, no need to panic. Onwards and upwards. I reckon I'll be accumulating more on any further share price weakness.

I note that their FY25 guidance at the AGM today suggests that revenue will likely be weighted towards the first half of FY25 and that their forecast FY25 revenue is largely underpinned by the contracted orderbook across the Group - so their forecast / guidance is NOT reliant on further contract wins, and that, to me, suggests that there is scope for a guidance upgrade IF some of their healthy tender pipeline does convert to orders that do start in H2 of FY25.

It is certainly refreshing to have some guidance that is NOT relying on a stronger second half. Relying on a stronger second half to meet guidance is a trend I've seen a fair bit across other companies this AR/AGM season. But not with GNG. Nice!

[held]

Further reading/viewing: https://www.gres.com.au/projects/default.aspx

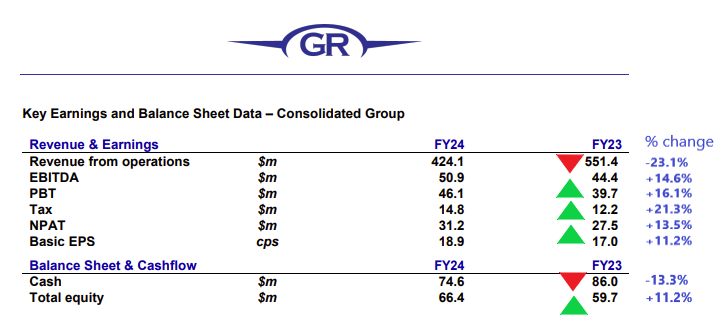

Today, another very similar company to LYL reported, GR Engineering Services (GNG), and despite having had BHP shelve the West Musgrave project (see here: Market-Update---West-Musgrave-Project.PDF) in July, GNG maintained their very high final dividend at 10 cents per share (cps) which means their full year dividends for FY24 (interim + final divs) adds up to 19 cps, same as FY23, and that means that at yesterday's closing share price of $1.855, GNG are paying a dividend yield of 10.2% and that's fully franked, so if you add in the full value of those franking credits (which I can use), the "grossed up" dividend yield is 14.3%. Again, this is another company (like LYL) who specialise in gold mills (so, tailwinds), have zero net debt, have high insider ownership (17% of the company owned by Directors and company founders and their families) and are conservatively run, but run well. They aren't growing as fast as LYL are though - they are smaller and have lumpier revenue and earnings.

GNG reported $74.6 million net cash, -13.3% lower than the $86 million they had at 30 June 2023, and their ROE is also very high at 47% (based on today's results), and it's been over 45% for the previous 3 financial years also according to Commsec, but the main difference in the eyes of the market appears to be that the market had lower expectations of GNG and GNG did maintain their very high dividend, so GNG is up today, currently trading just over $1.90 and they've traded this morning up to $1.95. I was buying GNG two days ago at $1.81 (average), so that's one thing I did get right this week (selling down Codan yesterday here on SM, not so much...)...

Like LYL, GNG is a highly illiquid stock where large volume trades can significantly move the share price, but unlike LYL who had a detailed and positive outlook statement yesterday, GNG's outlook statement was more, "We'll let you know in a couple of months.":

"FY25 Update and Outlook: GR Engineering has a solid contracted pipeline and has been building its orderbook for FY25 and future periods. GR Engineering intends to provide FY25 guidance at its 2024 Annual General Meeting, to be held on 27 November 2024, when it is likely to have more certainty in relation to the timing of key projects."

'Nuff said. Oh, except their EPS, earnings and margins were all higher, on lower revenue:

Source: GNG-FY24-Financial-Results---Media-Release.PDF

I hold GNG (third largest real life position, plus here also).

30-May-2024: FY24-Guidance-Update.PDF

I saw this sell-down as an opportunity and topped up GNG today both in my largest real money portfolio (@ $2.09) and also here on Strawman.com (at the $2.10/share closing price).

This is an engineering and construction company predominantly, although they do have recurring revenue through their Energy division (was called Upstream Process Solutions / Upstream PS, now called GR Production Services), so I view this downgrade in much the same way that I viewed the recent Duratec (DUR) guidance update.

Here's what GNG reported at the half (for the 6 months ending 31-Dec-2023):

And here's what they reported for FY23 and FY22 (full year results):

FY24 (full year) EBITDA now expected to be $50 to $51m ($50.5m midpoint), so lower than FY22, but +13.7% higher than the $44.4m EBITDA they reported in FY23, so they'll earn more than they did last year.

The market is reacting negatively to the revenue guidance downgrade - previously a midpoint of $515m, now $422.5m (midpoint), which is huge - if you take the lower end of the new guidance, which is $415m of revenue, that's $100m less now, or -19.4%. Using the midpoints ($515m to $422.5m), it's an -18% reduction in revenue.

And it would be significantly lower than FY22, when the reported $651.7m in revenue.

However, as I said with Duratec, that's revenue, let's look at earnings: The second paragraph of the announcement states that GNG continues to achieve solid operational performance across its core business (GRES - GR Engineering Services, a.k.a. their "Minerals Processing" division) and from its two key subsidiaries, GR Production Services (a.k.a. their "Energy" division) and Mipac (which now includes their recent Paradigm Engineers acquisition), and that all divisions are forecast to achieve EBITDA growth - by margin and percentage - in FY24 compared to the prior year.

So their EBITDA margins are improving. That is borne out by their new guidance of $50.5m EBITDA from 422.5m in revenue - giving them an 11.95% EBITDA margin, compared with FY23 where their EBITDA margin was 8% ($44.4m EBITDA from $551.4m in revenue) and their EBITDA margin of 8.6% in FY22 ($55.8m EBITDA from $651.7m in revenue) - as shown above.

Their Net Assets moves around that $60m mark, give or take about $2m, and their cash balance is very up and down because it depends on a lot of factors and the timing of various milestone and completion payments for both ongoing work and completed work, as well as outgoing expenditure when gearing up for new projects at various times. Importantly, GNG rarely carry debt - they almost always maintain a net cash position, which is very wise for a company of their small size and the industries that they operate in, in addition to the types of clients they work for, often it's GNG who get the contracts to construct the initial mills for gold miners who are transitioning from explorers to developers to producers.

As with Lycopodium (LYL), GNG get a lot of initial study work, so the Pre-Feasibility Studies (PFSs) which often lead to Bankable/Definitive Feasibility Studies (BFSs/DFSs). Both companies are involved in the scoping, initial testwork in most cases, the engineering and design of the plant in consultation with the client, and then if they are awarded the EPC (engineering, procurement & construction) contract or the EPCM contract (which includes overall project Management), they are then responsible for the final designs, the tendering and ordering of long-lead-time items (such as ball mills and large drive motors), and the actual plant/mill construction. Because LYL often design gold mills to be built in some of the most dangerous places in the world, such as some of the more risky West African countries, you'll often see them (LYL) announce EPM or EP & PM contracts, which is where they do everything EXCEPT the actual in-country construction; that work is usually subcontracted to a locally owned builder already operating in-country, so those contracts are either called Engineering, Procurement and Management (EPM) contracts or more recently the trend has been to call them Engineering, Procurement, and Project Management. GNG, on the other hand, work mostly within Australia, and they almost always do the "C" (construction) themselves.

Some of these contracts take months, such a mill refurbishment or an expansion or upgrade of an existing mill, however some will take years, such as the West Musgrave Mineral Processing Plant (nickel and copper) for OZ Minerals (now owned by BHP) - see here: GNG-Contract-Award---West-Musgrave-Project.PDF [14/04/2023] - which is worth over $300m (in revenue) and was expected to last around 2 years (so until around April/May 2025).

I did mention here a few months back that with the Nickel price tanking and BHP threatening to lay off hundreds of workers across their nickel operations in WA if they did not receive significant government support to carry them through until nickel prices bounced back, that the West Musgrave project could either be shelved or suspended, and that could definitely affect GNG because it was GNG's largest project at the time - here is an overview of their current Minerals Processing (GRES) contracted projects (as reported in Feb with their H1 results):

Source: HY24-Investor-Presentation.PDF [22-Feb-2024]

And here is the recurring revenue from their Energy (GRPS, formerly Upstream PS) division, along with the various contract lengths, which vary from 2 to 5 years, and are often rolled over (extended) at the end of those periods.

As you can see from those two slides, they are a small company that relies on a relatively small number of contracts to keep them busy at any given time, so their revenue can be lumpy for sure. Last night, GNG was a $364m company (bit smaller after today's SP drop), LYL was a $480m company, and Duratec's market cap was around $255m, so these are microcaps and none of them are in the ASX300 yet.

Since those slides were prepared in Feb, GNG have announced the following:

05-April-2024: Market-Update---Abra-Paste-Plant.PDF [Galena Mining Limited (G1A) reported that voluntary administrators had been appointed to Galena’s 60% owned subsidiary, Abra Mining Pty Ltd. GR Engineering was engaged in September 2021 to undertake the engineering, procurement and construction to relocate, refurbish and commission the Abra Mining owned Higginsville paste plant, which was successfully delivered and commissioned in accordance with the Contract, which included deferred payment terms. Prior to the appointment of the Administrators, Abra Mining has made monthly payments to GR Engineering in accordance with the applicable payment schedule in the Contract. GR Engineering notes the intention of the Administrators to operate the Abra mine and processing plant on a business as usual basis. The Administrators have confirmed that they will continue to pay the contracted monthly payments to GR Engineering. GR Engineering’s current exposure for remaining payments to be made by Abra Mining under the Contract is $8.5m representing unpaid deferred receivables. Given the deferred nature of the progress claims under the Contract, at the time of entering the Contract, GR Engineering sought and obtained first ranking security over the paste plant equipment and design documentation. This security relates to the paste plant only and does not extend to any other assets of Abra Mining. Based on GR Engineering's secured position, its preliminary assessment of the value of the secured assets, the intention of the Administrators to operate the mine and processing plant on a business as usual basis and the Administrators’ intention to continue to pay the contracted monthly payments to GR Engineering, GR Engineering expects that any adverse impact on GR Engineering's financial results for the financial year ending 30 June 2024 will be immaterial.]

18-April-2024: Appointment-of-Non-Executive-Director---Debbie-Morrow.PDF [Deb Morrow has over 25 years’ experience leading large-scale projects and has had a range of senior corporate and sustainability roles across the energy and mining sectors which includes a 20 year career with Woodside Energy Ltd and being a senior executive at OZ Minerals Ltd, prior to its acquisition by BHP in 2023. Ms Morrow is currently the MD & CEO of ASX listed Agrimin Ltd, who are focused on the development of its 100% owned potash projects in WA. Ms Morrow is a NED of Miner’s Promise and Holyoak.]

10-May-2024: GNG-EPC-Contract---Kathleen-Valley-Lithium-Backfill-Project.PDF

plus: LTR-Liontown-executes-Paste-Plant-EPC-contract.PDF

So not just gold. Lithium, copper, nickel, plus their energy division. Happy to be a shareholder of GNG, and thought today's drop was a good buying opportunity.

GNG-1H24-Results.pdf (taylorcollison.com.au) [04-March-2024]

Plain Text: https://www.taylorcollison.com.au/wp-content/uploads/2024/03/GNG-1H24-Results.pdf

Below are screenshots of pages 1 and 2 - please click on the link above for the full report which contains disclaimers and disclosures on pages 3 and 4.

Disclosure: I hold GNG shares both here on Strawman.com and in a real money portfolio as well.

01-Feb-2024: GNG-Acquisition-of-WA-Based-Process-Controls-Business-(Paradigm-Engineers).PDF

GR Engineering Services Limited (ASX:GNG) announced this morning that its wholly owned subsidiary, Mipac Holdings Pty Ltd (Mipac) has entered into an agreement to acquire Paradigm Engineers Pty Ltd (Paradigm), a provider of control systems and electrical engineering, automation and technology services based in Western Australia.

Transaction Highlights

- This transaction enhances Mipac’s control system and electrical design capabilities and expands its existing footprint in Western Australia. Paradigm has significant expertise working across a range of commodities, including iron ore, gold and battery minerals.

- Paradigm is forecasting FY24 revenue of $16 million and an EBITDA margin % consistent with Mipac. Similar revenue is anticipated for FY25, supported by Paradigm’s current order book and pipeline. The combined Mipac and Paradigm business is expected to generate revenue of approximately $50 million on a proforma basis.

- Paradigm’s current management team have agreed to continue in their roles post-completion.

- The purchase price is $9 million, with 50% payable in cash and 50% payable in GR Engineering scrip, subject to voluntary escrow. It is anticipated that the transaction will be immediately earnings per share (EPS) accretive.

This is a small bolt-on acquisition that does NOT require a CR, and is immediately EPS accretive. All good! GNG don't do M&A very often, but when they do make an acquisition, it tends to be a good strategic fit, for a good price.

Paradigm Engineers | Control systems and electrical engineering company

GR Engineering - Global Mineral Processing Solutions (gres.com.au)

GR Engineering Services Limited - Mipac - Engineering Consultants and Contractors (gres.com.au)

Disc: I hold GNG shares (both here and in a real money portfolio).

27-August-2023: I'd like to highlight the income and growth track record and future potential of a couple of smaller lower-liquidity microcaps that don't get talked about here much:

Firstly, GR Engineering Services (GRES, GNG.asx):

GR Engineering - Global Mineral Processing Solutions (gres.com.au)

GR Engineering: Providing Global Mineral Processing Solutions - YouTube [video]

GNG-FY23-Financial-Results-23-August-2023.pdf

GNG-FY23-Results-Presentation-23-August-2023.pdf

That presso (from last Wednesday) isn't overly long, however I'll shorten it even more by providing the 10 most important slides for current and prospective shareholders:

FY22 was a great year, and FY23 didn't quite hit those same highs, however FY23 was still a solid year and with negligible debt plus $86m cash in the bank (at June 30th), GRES (GNG) have matched FY22's high 19 cps dividend (for the full twelve months, so adding the interim and final dividends together). In terms of FY24, I'm more than comfortable that the good times are going to keep rolling on with GNG, based on their order book and track record (more on that order book in a minute).

Now, this company has three divisions, as shown above with some examples of their respective current clients. Those 3 divisions are:

- Mineral Processing ("GR Engineering", their main business which provides the majority of revenue and earnings, but the revenue is lumpy due to the one-off nature of the contracts);

- Energy ("Upstream PS", or "Upstream Production Solutions", provides recurring revenue from multi-year maintenance/operations contracts in the Oil/Gas sector); and

- Process Control Systems (Mipac, their most recent division, formed via the acquisition of Mipac in 2021 for just $21.4m max - being only $14.5m upfront - in cash and GNG shares - plus the other $6.9m being deferred subject to meeting EBITDA targets - which shows both how frugal and how smart GNG management are).

That "Mineral Processing" Order Book (confirmed orders) that totals over $650 million is enough by itself to beat both FY22's and FY23's revenue in FY24 (the current financial year), without ANY contribution from their other two divisions, or any further work added to the order book, including those near-term opportunities they mentioned, however it's likely that some of that (order book) work will extend into FY25, especially West Musgrave (for BHP), so part of that revenue will fall into FY25. Regardless, FY24 is going to be another strong year, and I believe they will continue to pay above-market dividends, both because they have the balance sheet (no debt and over $80m in cash) to do so, and also because they have perfect shareholder alignment. Check this out:

Yes, that's right folks, 56% of the company is owned by the company's directors and the company's founders (or their families as some of the founders have sadly pased away) and it's been like that for years, so there hasn't been much selling down of these insider positions at all. I find that when the majority of a company is owned by insiders, they tend to be rather focussed on total shareholder returns, particularly on paying out decent dividends when they can.

And they use debt much more wisely than other companies where management are just managers rather than part-owners of the business. With small companies, I prefer them to have no debt at all, and GNG Management agree, because they have what they refer to as "negligible debt" and over $80m of cash in the bank.

The free float (all shares on issue less those owned by insiders and instos) is notionally 27%, however most of that retail shareholder base isn't selling either, so it could become a lobster pot stock; easy to get into, much harder to get out of in a mad rush. So great for patient money, but perhaps not as good for money you might need to pull out quickly.

That's the last image that I've copied across from that Investor Presentation from last week (link above, near the top of this straw). This is a company with a market cap of around $372m (based on a $2.30 share price, where they closed at on Friday), with $86m cash (at June 30th), that's paying out some really nice dividends, and doing it consistently.

See below:

Source: Commsec

OK, nice dividends, all fully franked since March 2021, and a trailing yield of 8.3% plus the value of franking credits, so a grossed up trailing yield of 11.8% (including the full value of the franking credits) based on a share price of $2.30 (where they closed on Friday). I paid a fair bit less than $2.30/share for most of mine, but I think they still represent value at current levels.

But what about growth? Well...

Source: Commsec.

If you want to compare that to the index - here it is - and I've thrown in another similar company that is probably even better - Lycopodium (LYL):

Source: Commsec.

I've used the XAO there for a benchmark, the All Ords accumulation index, which includes all dividends and distributions reinvested back into the underlying companies, whereas the LYL and GNG lines ONLY represent the share price, without any dividends. You could also use the XJO - the S&P/ASX 200 TR (total return) index, however that is almost identical to the All Ords (the XAO) with the XJO returning +38.56% over 10 years (total, not p.a.) vs. the +43.07% return of the XAO. LYL has returned triple that, with +128.89% and GNG has returned +286.55% over 10 years, and that's of course without factoring in any dividends with GNG or LYL. Dividends substantially increase the total shareholder return - way beyond what that chart could show, except for the green line - the XAO - the All Ords Accumulation (or Total Return) Index - because with the XAO the dividends are already factored in.

So there you have it - great INCOME PLUS GROWTH. And LYL is even better, but that's another straw.

Disclosure: I hold GNG & LYL both here on SM and in my real life portfolios.

P.S. While they DO specialise in the design and construction of gold processing plants (gold mills), they also do other stuff, like Mineral Sands for instance:

03-May-2023: This announcement from GNG (who I hold both here and IRL) caught my eye this evening: Binding-Term-Sheet---Yangibana-Rare-Earths-Project.PDF

That's another contract win to add to their order book. Details: GR Engineering (GNG) have entered into a binding term sheet with Yangibana Pty Ltd, a wholly owned subsidiary of Hastings Technology Metals Limited (ASX: HAS) (Hastings), for the engineering, procurement and construction (EPC) of the beneficiation plant and associated infrastructure for the Yangibana Rare Earths Project (the Project) in Western Australia.

The Project is located approximately 250km north east of Carnarvon, in Western Australia.

GR Engineering and Hastings have agreed the material terms of the EPC contract in the binding term sheet. The EPC contract for the works will be finalised shortly and GR Engineering will commence early works. If the EPC contract is entered into, it is expected that the contract sum, including provisional sum, will be $210 million.

Commenting on the award, Mr Tony Patrizi, Managing Director said: “GR Engineering is pleased to have received the binding term sheet for this world class rare earths project in the Gascoyne region of Western Australia. It will be exciting to work on this project as it is focused on globally critical minerals that are used as key components for electric vehicles and wind turbines. We look forward to engaging closely with the Hastings team to deliver safe and successful outcomes for this project."

--- ends ---

Here's a link to the Hastings Technology Metals (HAS) announcement today: HAS-Reduces-Yangibana-Delivery-Risk---Awards-EPC-Contract.PDF

In their H1 results Presentation in February (see here: HY23-Investor-Presentation.PDF) GNG gave us an overview of the major projects in their EPC (Engineer, Procure & Construct) Order Book (on slide 5):

By the way, that West Musgrave Project ccontract (with OZ Minerals) has now been finalised - see here: GNG-Contract-Award---West-Musgrave-Project.PDF [14-April-2023 - Estimated revenue: $312 million over a two year period - I did mention here a little while ago that I thought that West Musgrave would be a Big contract for GNG when it was finalised.]

GNG are a bit like Lycopodium (LYL) in a number of ways - not just in what they do, but also in how they go about things, and they are both very modest - tending to underpromise and overdeliver most of the time. While LYL have been positively re-rated by the market in recent months, GNG have not: Here are GNG's 1 and 3 year charts:

Over 3 years they've done alright, but over the past 7 or 8 months... not so much... in share price terms. However there can often be a disconnect between the business value and the business share price with these microcap companies that aren't followed by the majority of market participants. As we have seen with LYL in recent months, when the market decides to positively re-rate them, they can put on quite a bit in a very short space of time...

I hold both companies (GNG & LYL) both here and in real life. Here is GNG's "Outlook" slide from their Feb Presso (H1 FY23 Results presentation, link above):

See what I mean - very understated. For context, here's their FY22 vs FY21 results:

With current guidance for FY23 Revenue in the $500m to $530m range, that's better than FY21 ($392.4m), but not as good as FY22 ($651.7m), however that "return to historical levels" for their EBITDA margin in the second half (current half) of FY23 suggests that the EBITDA margin will be more like FY21's 9.5% than FY22's 8.6%, and their margins have been higher than that in prior years.

They're tracking along nicely. Great dividend yield too. And their share price will recover at some point, sooner or later. Good income stock, with capital growth when it comes, just like LYL.

21-Nov-2022: I've just been looking through some recent announcements from GR Engineering Services (GNG) which is one of my favourite companies, and one that continues to pay me market leading dividends. Their trailing dividend yield is 8.68% based on their closing share price today of $2.19 and the 19c worth of dividends they've paid during the past 12 months, higher if you gross it up to include franking - their dividends are also fully franked). So income and some capital gains as well.

Here's some of their recent announcements, starting with their presentation on August 24th:

24-Aug-2022: FY22-Investor-Presentation.PDF

23-Sep-2022: West-Musgrave-Project---FID-Achieved.PDF

Also: OZL: Green-Light-for-West-Musgrave-Project.PDF

07-Oct-2022: GNGThunderbird-Mineral-Sands-Project-Full-Notice-to-Proceed.PDF

26-Oct-2022: Managing-Director-Transition.PDF

31-Oct-2022: Cosmos-Nickel-Concentrator-Facility-Upgrade---Scope-Change.PDF

21-Nov-2022: GNG-Preferred-Tenderer---Sorby-Hills-Lead-Silver-Project.PDF

Also: BML: BML-GRES-Selected-for-Sorby-Hills-Process-Plant.PDF

Yeah, they're keeping busy!

GNG are involved in dozens of studies for various projects. The specialise in gold mills, but as well as precious metals, they also design and build processing plants for base metals and battery metals, just like Lycopodium (LYL) do. While both LYL and GNG are based here in Australia, and are both listed on the ASX, LYL do most of their work overseas, and they specialise in West Africa, where many others fear to tread, whereas GNG do most of their work here in Australia. I imagine the two companies might merge one day. I hold shares in both, and they have very complimentary businesses, but I guess the other factor is that they both also have very high insider ownership, so perhaps they will always be separate because neither management team wants to give up control. No matter. They both keep performing admirably.

For those who are interested, you can check out Lycopodium's recent announcements here: ASX Announcements | Lycopodium and their presentations here: Presentations | Lycopodium

The studies (PFS, BFS, DFS, etc) often/usually lead to them being the front-runners for the relevant EPC (or in LYL's case, EPCM, or EPM - or EP & PM) contracts for those projects if and when those projects get the green light (positive FID) from the owners (and those owners get their finance sorted out). GNG and LYL don't usually announce the studies (Pre-feasibility, Bankable Feasibility and Definitive Feasibility Studies) when they are awarded them - because they're not usually material, but when those studies lead to the award of Engineering, Procurement and Construction (EPC) contracts or EPC + Management (EPCM) contracts, or Engineering and Procurement plus Project Management (EP + PM) contracts, they do announce them, because they are material. Both companies are quite busy this year, and have been regularly announcing additional contract awards.

In addition to that work, which can be quite lumpy, due to it's one-off nature, GNG also have recurring revenue from their Upstream PS division - which stands for Upstream Production Solutions. It's one of the only acquisitions they've ever made; they prefer organic growth. Upstream PS is the quiet achiever within GNG that keeps churning out profits from recurring revenue from multi-year contracts from some of the largest names in the Australian oil and gas industry - as well as from some of the smaller players.

Here's their main website: Upstream Production Solutions (upstreamps.com)

And here's the section within the main GNG website that discusses Upstream PS: https://www.gres.com.au/our-companies/upstream-production-solutions.aspx

So, yeah, for a company that not many people have heard of, and that even fewer people follow, they are keeping busy, and rewarding their shareholders.

Disclosure: I hold shares in GNG and LYL both here on SM and in real life.

23-Sep-2022: GNG: West-Musgrave-Project---FID-Achieved.PDF

OZL: Green-Light-for-West-Musgrave-Project.PDF

The following is Page 3 of OZ Minerals' (OZL's) announcement (full announcement link above):

I reckon this is a big one - for GNG, in terms of the sort of contracts they have been winning over recent years. The work that GNG did for IGO at their Nova Nickel project back in 2015 was worth $114m plus another $12m for the non-process infrastructure ($126m all up):

Nova Nickel Project (gres.com.au)

GR Engineering wins more work at Nova (businessnews.com.au) (2015)

And that was a smaller project I reckon, and it was nine years ago. GNG (GR Engineering) also have a history of doing a lot of builds and upgrades of nickel concentrators for Western Areas at Forrestania and then Cosmos that dates back to 2008/2009, so while gold processing plants is GNG's game, they are also pretty good at designing and building nickel plants. Western Areas (WSA) was taken over by IGO earlier this year - see here: IGO gets Forrest backing in Western Areas takeover (australianresourcesandinvestment.com.au)

GNG closed down 3c today (or -1.32%) at $2.25, which was also their day-high, so they closed on their highs, having traded as low as $2.16 earlier in the day (which was -5.26% down from Thursday's $2.28/share close).

The market may have been disappointed that there were no estimates of revenue (no $ value) in today's announcement by GNG, however they have yet to finalise the contract details. It is important that OZ Minerals (OZL) did say in their announcement today that GNG (GR Engineering Services) would be building their (OZ Minerals') nickel processing plant at West Musgrave, despite not all of the details (such as the price) being finalised yet.

Interesting that rival engineering firm Lycopodium (LYL) who also specialise in gold processing plants, but do their best work overseas, mostly in Africa these days, rose +12c (or +1.77%) to close at $6.90/share today, on the back of this announcement: LYL-Award-of-Sabodala-Massawa-Project.PDF which is interesting in that it is a EP and PM contract (Engineering & Procurement plus Project Management) but there's no Construction aspect to it, so another company is doing the actual construction of the Sabodala-Massawa Expansion Project in Senegal for Endeavour Gold Corporation (a.k.a. Endeavour Mining, who are listed on the London Stock Exchange with a secondary listing in Canada on the TSX). As I mentioned in my Gold Forum post earlier tonight, Senegal shares a border with Mali and there's plenty going on in Mali that would tend to encourage most sensible people to stay well clear of the area, so it's possible that this is a risk management or risk mitigation strategy by LYL - i.e. to do the majority of the work from here in Australia and let another company do the in-country construction in Senegal. Of course that means that this contract is worth a fair bit less than previous EPC and EPCM contracts that LYL have been previously awarded in West Africa. This contract is "valued at over A$26 million, with first gold pour from the BIOX® plant expected in early 2024."

They would normally get 5 to 10 times that for an EPC or EPCM contract for the delivery of a gold processing plant in West Africa, but when you remove the "C", the price is a lot lower, but then, in this case, I imagine the risks (for LYL) are also a lot lower. Interesting times...

And interesting that the contract that the market learned today that GNG had secured in WA (sure, West Musgrave is in the middle of the desert, just to the west of the bottom left corner of NT and the top left corner of SA, so at the convergence of the three states, but importantly still right here in Australia) is worth at least 10 times what this new LYL contract is worth, in my opinion, and yet GNG were sold down, and LYL were bid up. Doesn't matter, I hold both of them.

Here's an excerpt from the OZL announcement today:

"Our project execution strategy will enable us to mitigate industry-wide cost inflation being experienced globally. An increase in direct Project capital to approximately $1.7 billion* is offset by a substantial increase in Project value and results in stronger cash flow generation of circa $1.9 billion [nominal value from commencement of production] during the first five years of production."

* Nominal value. Assumes a third-party power purchase agreement, a mining fleet lease agreement, and a lease of the Living Hub.

Now that $1.7 billion in direct project capital committed by OZL isn't all going to go to GNG of course, GNG will only get a slice of that pie, but it should be a generous enough slice considering they are going to engineer, procure, construct and deliver the processing plant, which tends to be one of the most expensive elements of new mines. It will be in terms of hundreds of millions in my estimation, not tens of millions. But time will tell.

Suffice to say I'm glad that GNG is one of the largest positions in one of my real life portfolios, and if GNG or LYL were in the ASX300 index, they would both also be in my SMSF (which is in an industry super fund, so I am limited to ASX300 companies unforunately). GNG is in the All Ords, LYL isn't even in that index, too small, and too many shares held by management, so insufficient free float for index inclusion. GNG also have a lot of insider ownership, heaps! But they have a larger market cap than LYL. Both great companies with superb management, and both paying very decent dividend yields this year. They've been showing me the money - by putting it in my bank account.

20-July-2022: GNG-EPC-Contract---Bellevue-Gold-Project.PDF

From BGL: BGL-Bellevue-awards-EPC-Contract-to-GR-Engineering.PDF

That's today. Back on May 24th, both companies announced that GNG were undertaking preliminary works, so had won the contract, but that it had not been officially awarded and signed off.

GNG-Preliminary-Works-Agreement---Bellevue-Gold-Project.PDF

BGL-Preliminary-works-agreement-signed-with-GR-Engineering.PDF

In that announcement, Bellevue said, " GR Engineering knew the project well from its work during the study phase".

That's important to understand, GNG is the main player in doing studies (PFS, BFS and DFS studies) for Australian gold companies, and much of that work does lead to GNG being awarded the EPC (engineer, procure, construct) contracts when those projects do get a positive FID (financial investment decision, i.e. the green light to proceed by the board of the company that owns the project) and funding is secured.

In terms of GNG taking part payment for their services in shares @PortfolioPlus - they have a positive track record of doing this, as does another mining services contractor (who mostly do the actual mining) in the gold sector, MACA (MLD). Both of them have regularly bought shares in their clients, or accepted shares as part-payment for their services, and have for the most part made additional profits by later selling those shares at a higher value that what they were issued at. Not always, but usually. The shares are not generally subject to any escrow agreements, so GNG and MLD are free to sell them any time they wish to.

In GNG's case, they usually only accept a smallish proportion of their total revenue as shares. In this case it's up to $7.5m of the $87.8m fixed price contract value, so around 8.5%. While there are obviously risks associated with taking part-payment in shares, GNG are in a very good position to know exactly what those risks are, especially as they have prepared the DFS (definitive feasibility study) for the project, and they are engineering and building the processing plant themselves.