Price History

Premium Content

Premium Content

Premium Content

Another solid report from GNP.

Thesis still very much intact.

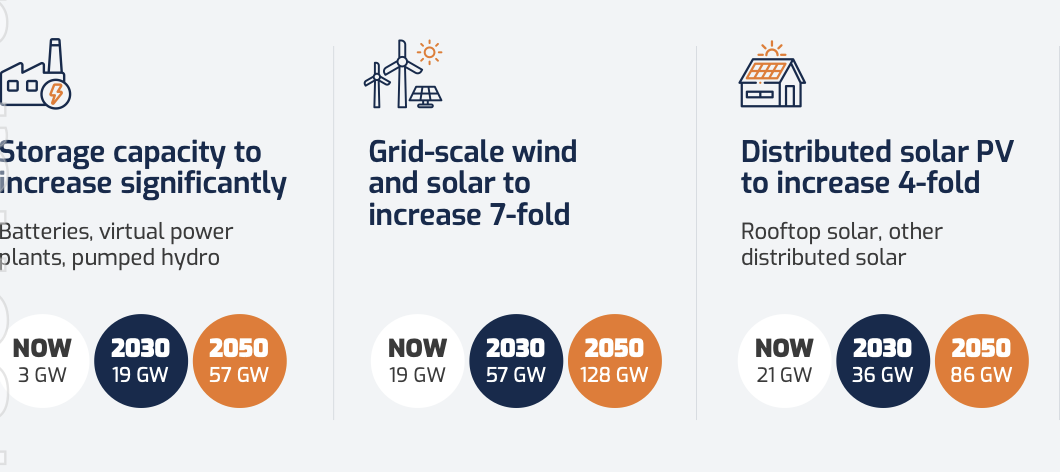

It's important to realise just how far the tailwinds for this industry still have to run. We are just at the beginning of the energy transition and grid upgrade. This slide illustrates it well

GNP is in the box seat, and continues to execute well.

Happy holder, largest position in non-super portfolio.

• Genus, as part of the ACCIONA Genus JV (AGJV) has been awarded a contract by AusNet to

construct the Western Renewables Link (WRL) Project in Victoria subject to project approvals

• AGJV Contract for the construction of WRL is worth approximately AUD$1.6 billion

• A further strategic move into the VIC Renewables market for Genus

GNP are 25% of the partnership, so a $400m increase revenue

However, it’s not unalloyed good news given the grumpy farmers blocking access to Vicgrid like these two:

Its difficult to know if resistance to the work will incur extra costs for GNP or not

SP up 10% on the news

Here’s the link to the announcement

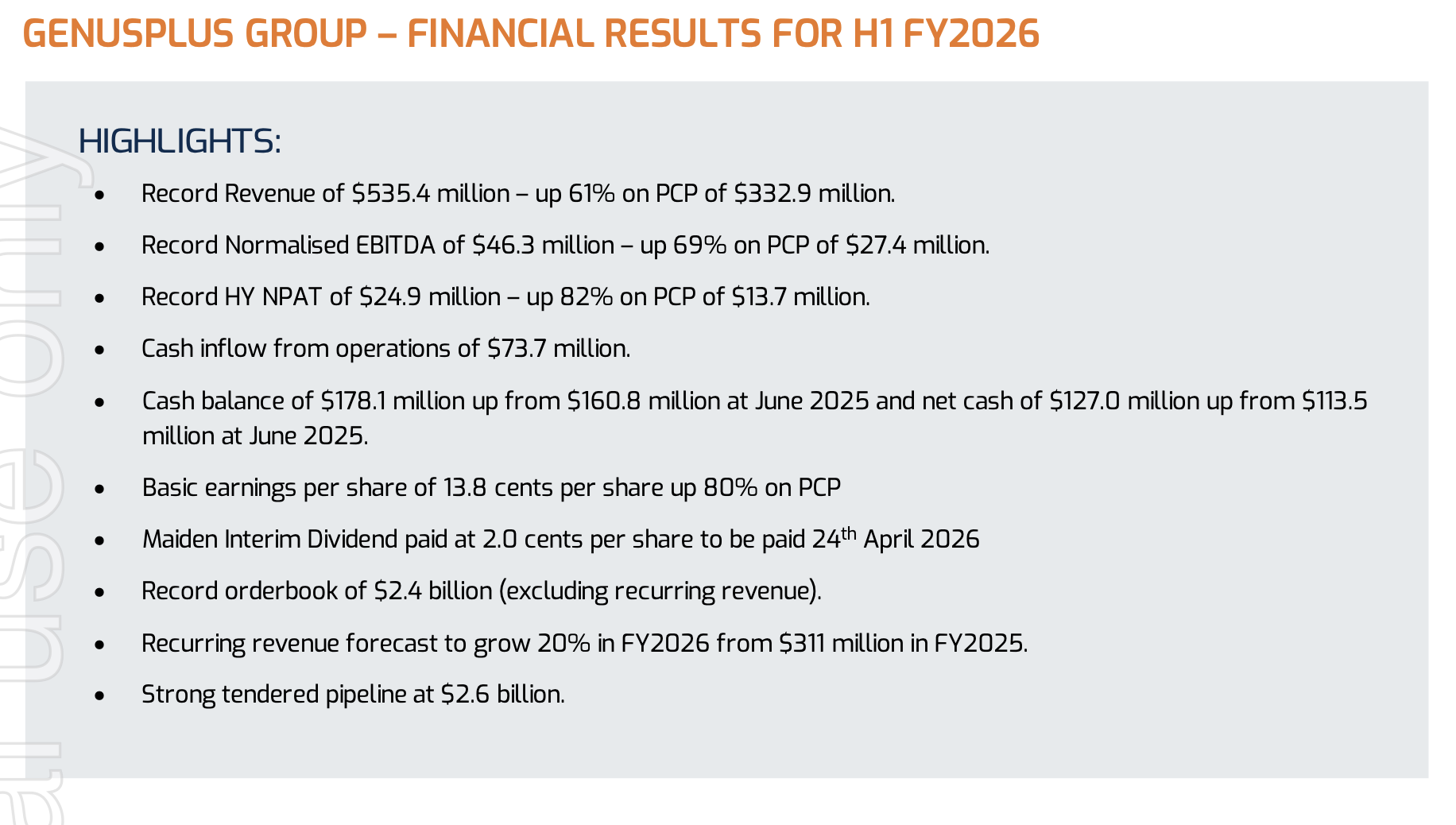

GNP posted there results for FY 2025 and it was another good one:

Selected highlights

All 3 divisions of the business saw huge improvements and with the Energy transition still in the early stages and GNP able to bid for an execute profitably on multiple projects, plus have an increasing fraction of revenue coming from maintenance as evidenced by the above graph, the future continues to look good.

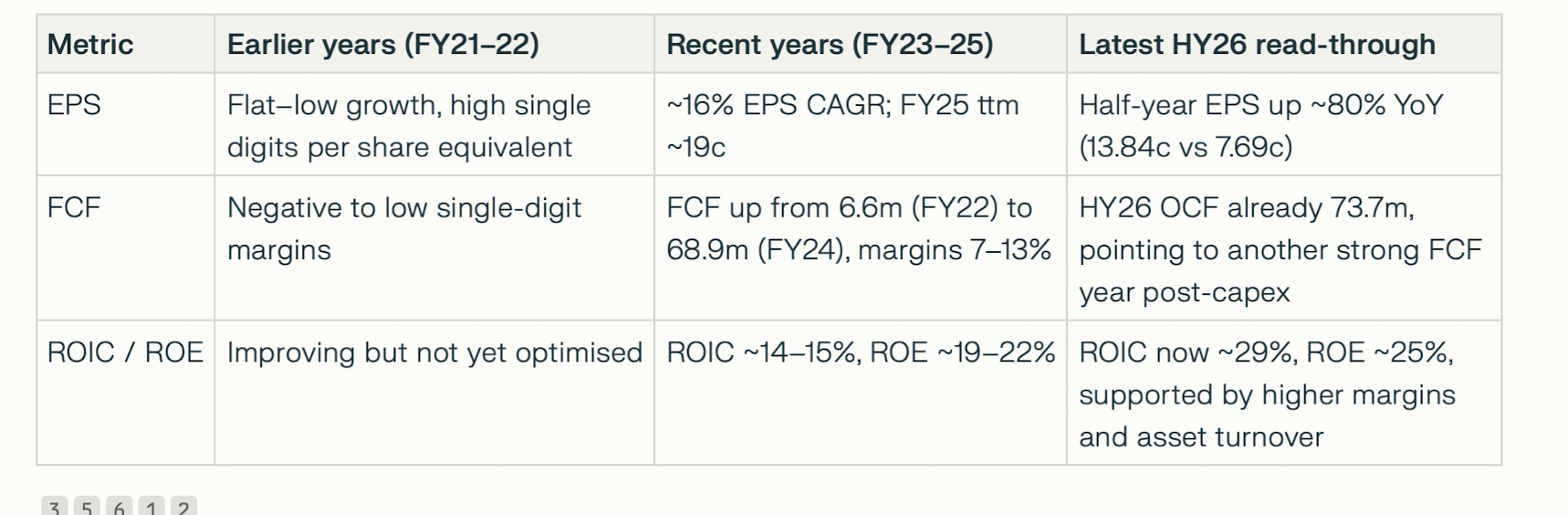

I calculate

Net profit margin is 4.7% - about standard for the industry they operate in

ROE of 25.2%

The SP is up ~15% in early trade producing a PE ratio of ~25 with isn't too onerous given how full the order book is.

GNP is my largest holding outside of super and is now an outsized 25% of that portfolio. I am happy to keep it that size as my confidence in their future is high.

You can access full results here https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02984836-6A1280466&v=4a466cc3f899e00730cfbfcd5ab8940c41f474b6

HELD IRL AND SM

GNP has just managed to breach the $4 mark today, on the back of a recent slew of contract wins

Individually, none are particularly huge but would seem to validate the thesis that they are gaining significant momentum.

This slide gives a summary of the 3 arms of the business all continuing to perform well:

GNP is my largest holding in my "beer money portfolio" (ie not Super)

Slowly catching up with companies I follow/own but not many others do, as this is of more interest than the already excellent coverage others have provided on more common holdings.

I cannot prove the same depth or quality of assessment as others, particularly in breaking down in questioning financial statements as more esteemed members, but hope there are some points that are worthwhile.

For context (and for new members), GNP is one of my largest holdings in my portfolio outside of Super. I have been happy with their progress since I have owned and so far the thesis is holding and panning out pretty much as well as I could have hoped. This is not a company with fantastic near term re-rate potentials, but I hope to be one of those steady 15-20% compounders. Rare gems.

In summary, it was another great half with headline numbers all impressively up (with exception of their debt - due to an acquisition)

They split their business into three segments, infrastructure, industrial and telecommunications

To me, the first two are an ever increasingly overlapping set of circles in a Venn diagram.

They infrastructure and industrial segments are mostly exposed to the "green revolution" of the renewable energy grid build out. Predominantly this means pylons, batteries and smart grid upgrades to existing networks. But an increasing part of their contracts have a repair and maintenance contract build in which gives a recurring revenue:

This is increasing quickly and gives a small degree of downside protection to the investment thesis. These segments contribute the majority of the earnings. Interestingly, the "telecoms" servicing business which I had always thought to be a lemon and an irrelevance to the rest of the company, has had a spectacular turn around:

It is also good to see the revenue by geography slowly become less concentrated in WA. This remains a significant risk.

EPS has increased 50% vs pcp

Overall a great result and......

The outlook is rosy:

The only issue was the suspension of the dividend, which caused an intra-day drop in the SP of ~6% from memory. It is now up 7% from the pre-announcement SP.

I am happy with this decision as I believe this reflects a conviction that the company can achieve a higher ROIC with that money than returning as dividends, to the benefit of all shareholders.

David Riches, the Director, is a 50% shareholder.

HELD IRL & SM

Not the largest contract in the world, but another proof of concept win.

Ausgrid supply 1.8 million homes in NSW. This is one of their first smart grid upgrades, and GNP are in the box seat. Importantly, this is an east coast contract, validating their take over activity of the last few years.

There has been a fair bit of discussion of engineering services companies on Strawman, I remain non-plussed why this company hasn't received more love. It's kicking goal after goal and rewarding shareholders handsomely. The energy transition and grid re-build is only just starting with an expected $16-20 billion price tag over the next 10 years.

It's still reasonably priced and one of my biggest holdings IRL.

C

Pretty good result from GNP as largely flagged in previous updates.

All metrics improved significantly and they confidently predict increased contracts wins and higher recurring revenue through service contracts. It is largely due to the rapid increase in the Industrial segment, see below, which builds electrification solutions (Poles, wires and BESS stations)

EPS have leapt to 10.8 cent, up 43.4%, this makes the current ~PE 20. They predict strong growth of the medium term and "at least 20% increase in EBITDA", so not expensive for company with good medium term growth prospects. Maybe a forward PE of 15?

The other aspect that is gratifying to see is the ROE start to trend beck up towards where it has been historically 15-25%. This fills me with a bit more confidence that the recent big acquisitions have been successful and it is becoming a quality company.

I'll do a valuation a bit later today if I get the chance

EDIT: PE should have been 20 not 9.2. Ive rounded it up to 20 for simplicity. A few more comments included

GNP has rallied significantly over the last 6 months and is now sitting at ~$1.90.

They updated the market yesterday with increased guidance:

So, the bull case is very much coming to pass: they are winning more and larger contracts and managing to maintain reasonable margins on contracted work (a big worry for me previously).

There are huge tailwinds in this sector as outlined in previous straws, and it is great to see them executing well.

@Strawman would it be possible to get David Riches in for a meeting to see what he has to say?

Thanks

Held: 11% IRL (beer money portfolio)

GNP published their 1/2yr today. The headline numbers are positive and the SP has edged higher after appreciating significantly over the last few months:

They have been expanding eastward from their home state of WA and are staking a claim to be part of the $20 billion "re-wiring the nation" program. This "new grid" has been talked about a lot over the past few years but the Government is actually starting to throw some real money at it now, and this can be seen by how large the potential order book is now. GNP have a healthy pipeline of works and have been winning contracts fairly regularly in all states. There are three arms to the business but I am predominantly interested in the New Energy Infrastructure section.

Before they expanded eastward, they had a very healthy ROE in excess of 25% (at one point in excess of 40%), but given the investment and re-structuring required to compete in the Eastern states this has dropped to the low - mid teens.

Of note, I was pleased they elected to not pay a dividend but instead re-invest the cash into growing the business.

My thesis for this company is as follows:

- there are healthy tailwinds creating a sh*t-ton of work that needs to be done over the next 10 years and beyond

- GNP have demonstrated they can win large contracts and deliver them

- As efficiency returns to the business, they will return to their above average ROE and hence become a highly attractive business

The risks are the that they cannot return to that higher ROE because:

- they are competing in a new market, with new operating costs and I am comparing apples to oranges

- they bid for a big contract and find they are on the hook for a blow out in costs

- the cost of labour continues to escalate and their margin gets eroded away by the time arbitrage thingy working in reverse

it is therefore concerning that contract and labour hire costs are increasing proportionately faster than revenue:

I currently hold - please see valuation straw for updated numbers

There was nothing particularly wrong with this report, but I was hoping for more.

As a recap - GNP have been executing on a strategy to expand their core WA based business to the East coast by acquisition.

They have made a number of purchases over the last few years and have been successful at bidding for a lot of contracts. Consequently revenue has increased significantly, but EBIT and NPAT, not so much. In many ways this is to be expected when bedding down acquisitions, dealing with both pandemic induced labour market disruptions, supply chain disruptions and an inflationary environment - so perhaps I am being unrealistic.

I am not able to give any insight into the accounting differences between the normalised and non-adjusted figures.

Due to the increased share count from the takeover of FPA, the EPS has actually decreased:

They make much of the forward order book and pipeline being enormous. And this is great but only if its possible to make a bigger profit off all this increased work.

Management have flagged that FY23 will be a year of consolidation. It remains to be seen whether they can cope with all the pressures of assimilating new acquisitions in new geographical areas, plus all the labour market, supply chain and cost increases whilst increasing profitability.

From my reading, and David Riches repeated and sizeable on market share purchases, I have a degree of confidence that GNP can fix this. Will have to watch for drift in my thesis over next 12 months, but happy to hold for now.