Consensus community valuation

Following the discontinuation of TACTI 004, a payment obligation has arisen under the Companys licence agreement with Dr. Reddys. Under the licence agreement terms, the Company must pay US$10 million to Dr. Reddys by June 2026 in these circumstances. No payment has been made to Dr. Reddys at the date of this announcement. The expected payment will result in a cash outflow of US$10 million in the June 2026 quarter and corresponding reduction in unearned revenue.

The remaining balance of US$7.3 million in unearned revenue is expected to be recognised as revenue for the half-year ending 30 June 2026.

/immutep-quarterly-activities-report-

Appendix 4C cash flow and estimated Cash:

Thursday Close:

receives-fda-odd-for-efti-in-soft-tissue

CEO of Immutep, Marc Voigt said: “We are pleased that the FDA has recognised the potential of efti for patients with soft tissue sarcoma, a rare and difficult to treat cancer

Return (inc div) 1yr: -77.96% 3yr: -39.09% pa 5yr: -34.38% pa

on todays announcement

Trades at 0.055cps

up 0.016cps

Up today 41%

The company's CEO, Marc Voigt, said: "We are very disappointed and surprised with the outcome of the futility analysis, in light of efti's performance in every other clinical trial. […] We are currently conducting a comprehensive review of the available data to better understand the results and determine the appropriate next steps for the program."

Immutep Limited (ASX: IMM) – Trading Halt Trading in the securities of Immutep Limited (‘IMM’) will be halted at the request of IMM, pending the release of an announcement by IMM. Unless ASX decides otherwise, the securities will remain in trading halt until the earlier of: • the commencement of normal trading on Wednesday, 11 March 2026; or • the release of the announcement to the market. IMM’s request for a trading halt is attached below for the information of the market. Issued by ASX Compliance

https://www.marketindex.com.au/asx/imm?src=search-all

IMM - Holders had 7 days 6th till 13th Mar then Bang the shares slide down the 'elevator'.. So speculators lost their shirts there.

Return (inc div) 1yr: -84.21% 3yr: -44.16% pa 5yr: -32.73% pa

Microcap $66Mill

No profit organisation!

please visit www.immutep.com.

IMM still has a pipeline of trials..

threads/ann-immutep-quarterly-act

- Release Date: 29/01/26 11:36

- Summary: Immutep Quarterly Activities Report and Appendix 4C

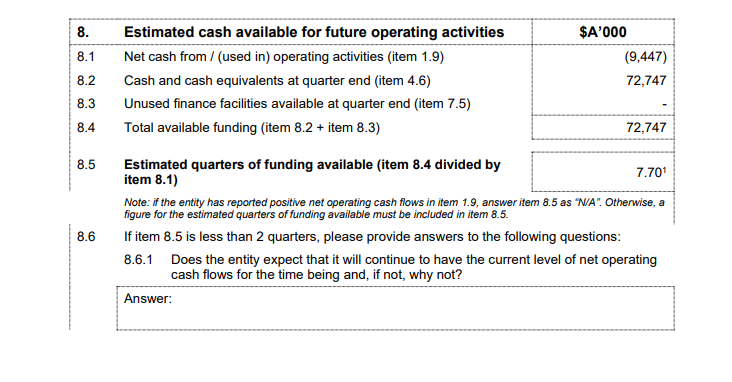

- IMM Estimate 7.7 quarters of funding. here:

Did the market misunderstand the recent results, Im no expert in clinical trials but I do think it has been misunderstood...

The first question is what is a phase 2 trial.... simply to assess if there is a dosing efficacy to the compound (EFTI) + pembrolizumab (Keytruda) (in the TACTI-002) study. The answer is yes. They now have the data (and are approved) to progress to a phase 3 trial.

The data.

(TACTI-002) Assessing 2nd line non squamous head and neck cancer (2nd line is refractory to PD-1/PD-L1 treatment. which is a super important part to understand)

- Cancer patients (refractory to treatment) who had minimal physical disadvantage (could walk/ mobilise and had limited physical limitation). 37/39 participants evaluated with 30% of participants tumour progression free at 6 months.... That is a huge result given this was cancer non responding to other treatments.

AIPAC (Active immunotherapy PAClitaxel + IMM's EFTI) is the largest and most progressed clinical trial, looking at hormone receptor positive metastatic breast cancers. It is important to understand how breast cancer treatment works. Essentially therapeutics target hormone receptors to slow/ destroy the tumour. Less hormone receptors = less treatable.... AKA Triple negative breast cancer is the most aggressive and least treatable breast CA.

- 114/227 participants (114 in the active group, the rest in usual care + placebo)

- In the overall study population EFTI + paclixatel showed a benefit of +2.9 months which doesn't seem that positive, however if the study population is further divided the results are much better.

- Patients who are younger (<65 had better results).. +7.5months survivability

- Patients with low monocytes had +19.6 months survivability (thats pretty huge)

- Patients with more aggressive 'luminal B' had a survival benefit of +4.2months.

A few points....

Clinical trials take time and there is still a phase 3 to go but overall I thought these were pretty good results, a phase 2 study is not designed to shoot the lights out, or in IMM's goal to cure cancer that is just simply not going to happen in this study but the definitely built a pretty impressive foundation for furthering this line of enquiry particularly in metastatic breast cancer. In terms of financials metastatic breast cancer is such a huge market with a huge burden of illness.

What didn't they report... lots of things. And my main question was what was the quality of life adjustment for these patients. For example the low monocyte group.... Did they 'live longer with really poor quality of life' or did this improve their ability to live and spend precious time with family.

Disclosure watching IRL and holding on strawman.

Mainly because I am a poor uni student who would back it given more appropriate circumstances.

Would really love feedback from some of the more medically educated people in here.