Consensus community valuation

I have been doing a bit of work on KME, just because they have started reporting a bunch of metrics they previously did not. While I think reporting contribution margin is important, there's two issues: Firstly, KME is a far more complex business than it was pre-covid when it was just a high margin franchisor and secondly they have an issue with expense escalation. I think the new metrics are probably designed to try and give a better understanding of thinking about the business, although I think management still does quite a poor job of explaining what's going on under the hood.

So my way of thinking about KME is to push some of the opex into the COGS line and then get a "gross profit" that is franchise revenue + the GP of the corporate centres and TF (there are some assumption here around what % KME keeps). It at least gives me some basis to compare to 2019. As you can see the issue is that while revenue has grown strongly, the change in the nature of that incremental revenue – high margin franchise to low margin student lessons – has not been able to support the opex cost escalation. Granted, part of that is they have had to invest through front ended expenses in the p&l. But I think most investors (and the SP) would agree the main issue here has been quite undisciplined expense control.

So my interest here is that with a bit of cost discipline, like from say a new chairman, there is potentially a lot of latent operating leverage that could flex over the next 12-18 months. The AGM trading update was positive but more interesting to me was the outlook of focussing on ROC, expectations of reducing capex spend and potentially some margin expansion.

I'm still not convinced about TF, it seems like a massive distraction for a business that brings in ~$500k or so, but maybe they take a view that it is part of the expansion into the US. The franchise business seems to have a lot of potential, it is low capex and high ROIC given they already have a presence in AU/UK, I would see it as a positive if they decided to try and juice that a bit more rather than try and crack the US. But down here, I think the odds are in my favour and they really only have to not do stupid things and the SP should do quite well. The test will be watching what happens to the gross profit, opex cost jaws.

KME provided an update for the first 4 months of trading of 1H FY25 - Looks Good

There were certain red flags as well

I could count the number of AI mentions. I hope Storm doesn't invest in some crazy AI idea now.

The migration of Silver Franchises to Gold Franchises is accelerating. Very soon, all Silvers will go, and then hopefully, KME can increase gold franchises or keep the existing ones and grow them.

I should have a look at this. I sold my shares a few months ago.

Kip McGrath reported 1st half 2024 result today.

Main issue as i see it is ongoing investment in the business. It increased revenue by $2.5m but increased employee expense by $2.6m.

This increase in employee expense increase probably coming from corporate centers ( management flagged recent corporate center acquisitions incurred additional cost of $250,000.

It seems like it lost the Abu Dhabi schools' contract after AGM i.e lost $510,000 profit and it is the probably the reason why it subtly downgraded the full year outlook

From "Expect FY24 full year NPAT to exceed prior year" at the time of AGM in November to now " FY24 full-year profit is expected to align with the prior year result"

The market has lost patience and I am not sure how long current shareholders can keep faith in management.

Bag holder.

Here is an interesting chart.

KME is increasing its Revenue/Share but in the last 5 years, it has also invested heavily in corporate rollout / online shift / US expansion. Hence, increased Revenue/Share hasn't been contributing to an increase in earnings/share in the last 5 years. Hopefully, We are at the end of this investment cycle.

Kip McGrath released its FY23 report and the following are the graphs,

Revenue:

Customer Receipts:

Expense:

Operating Cash

No. of Shares

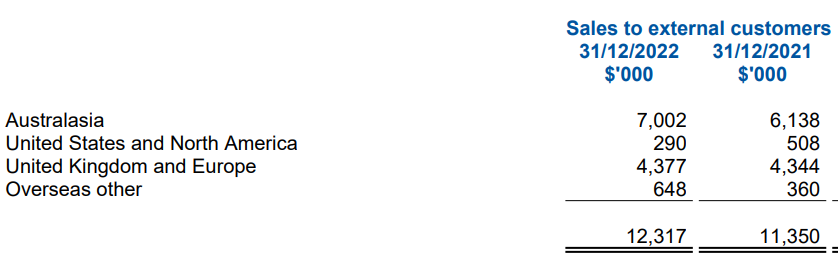

Geographic info ( USA is dragging the performance)

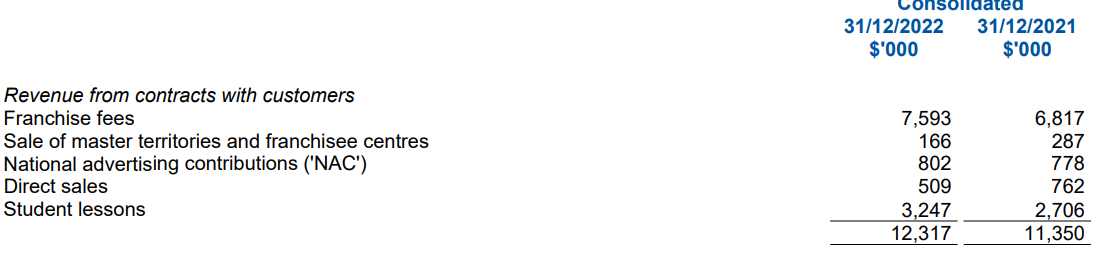

Revenue breakdown

Franchise fees are increasing because the Silver franchise is getting converted to Gold. Overall Student lessons are bringing higher revenue. ( at the end of the day that's the most important matric to see )

Some encouraging traction for Tutorfly

Corporate Center

Yes, Tutorfly is a drag but its a relatively small part of the business. The Franchise Network and Corporate Center are going in right direction. Hopefully based on the comments from the Annual Report, Tutorfly will come good in FY24. Overall happy with the result.

Monthly Newsletter_July_2023_Digital_230712_093419.pdf

Page 13 : Australasian Emerging Companies Fund comments

Not bad. 200k, 50k, and 100k worth of shares purchased yesterday, which is a total value of ~$150-175k.

Curious that the directors chose to coordinate buying, not sure how to interpret that.

Tutorfly's performance was a major drag on Kip McGrath's performance in 1H FY23. with promising words about 2nd half in report.

Seems like the new revenue stream: drop-in tutoring" is working (https://www.dropintutor.com/)

https://gmcs.org/2023/01/free-on-line-tutoring/

KME Reported its FY23 report and the share price has gone downhill ( i.e no change after the result as it was going downhill before the result as well)

It seems that the market didn't like that NPAT has gone 29% down or it didn't like that revenue only increased by 9.2%.

Yes, the result wasn't great but to my eyes, It wasn't bad at all compared to what I was expecting or fearing that inflation will seriously hamper its tuition numbers.

Some of the bright spots in the results for me

- The corporate business continues to scale and has achieved profitability for the first time

- May be market didn't like the cashflow shown but the underlying net cash flow from operations was $3.1M

- Cash flow from operations this half was affected by $2.3M in outflows to franchisees

- Revenue from Franchise fees and Student lessons are trending in the right direction

- Revenue performance was hampered by UK/Europe and the USA. Now I have noticed the trend that most of the reported companies had issues gaining growth momentum in UK/Europe in this period and for USA, KME is saying that there were some delays with Tutorfly Director comments as below:

- " We have contracts in place for the second half to see revenue return to last year’s levels for the full year and are now working with 4 school districts up from 1. We have also developed a new revenue stream for ‘drop-in tutoring.’ Currently, in use at one school district, a click button provides an instant help feature. We believe this new service for drop-in tutoring provides an exciting new business opportunity more widely throughout all operations"

So in nutshell, Yes company didn't had a great half but I think it has been punished way more than it should ( in my opinion - anyway) probably illiquid nature has to do with it. Hopefully, the same illiquidity will at some point act in shareholder's favor - I shall wait for such time.

Looks to be a fair amount of consistent volume (compared to history - still illiquid) going through KME over the last few weeks. Wonder who is buying and who is selling.

Nice to see Tutorfly already profitable.

With all the pieces falling into place FY23 looks like the year for KME.

KME has provided guidance so the following is what I am expecting

Things I want to know in FY22 reports

- How Corporate centers are performing? What level of margin can be expected and when we will see effect on bottom line?

- How blended tutoring is working? Online tutoring percentage? further technology investment required?

- Tutorfly progress? What's the plan for the near and medium term for tutorfly?

One of the online learning platforms Cluey released its half-yearly result today.

Revenue has increased significantly from the previous period but I am not sure if the model is going to survive longer.

The way I read it, They had to spend 4.5m in marketing to get 15.7m revenue.

15.7m revenue required 7.2m cost to generate 8.5m gross profit

To increase gross profit, they increased their marketing 15 times, Admin roughly 10 times, and employee expense 10 times.

Most of the employee expense is also the cost of sales for this business as without tutors there is no classes. [ so in fact gross margin would be very less if you factor that also in]