If the 'intent' follows through all good.. Prefer to see the cash transaction

This offtake agreement follows the mutual decision to modify the original agreement between Lynas and the DoW based on significant uncertainty as to whether the construction of the Heavy Rare Earth processing facility at Seadrift, Texas would proceed.

Lynas and the DoW continue to discuss further supply arrangements including for Heavy Rare Earth oxides.

Commenting on the signing, Amanda Lacaze, CEO and Managing Director of Lynas Rare Earths said: “Lynas is pleased to sign this binding Letter of Intent with the U.S. Department of War.

Through this agreement, the U.S. Defense Industrial Base will continue to have access to Light and Heavy Rare Earth oxides that are essential for modern manufacturing.

“We thank the U.S. Government for working with Lynas to reach this mutually beneficial arrangement and look forward to finalising the definitive agreement in due course and continuing our productive engagement with the U.S. Government.”

Authorised by: Sarah Leonard, Company Secretary Media Relations: Jennifer Parker E: [email protected] T: +61 8 6241 3800 Investor Relations: Daniel Havas VP Strategy & Investor Relations E: [email protected]

Amanda ends up with a good report card CV here,,,

announces that Chief Executive Officer and Managing Director Amanda Lacaze has advised the Board of her intention to retire after 12 years in the role. The Board has initiated a search process to select a new CEO to lead the company through its next stage of growth. This process will consider both internal and external candidates. Ms Lacaze intends to remain with the company until the end of the current financial year to enable a smooth transition.

Amanda Lacaze said: “I’ve loved every day of my 12 years at Lynas. It has been a great privilege to lead the company from a troubled startup to an ASX50 company. I am extremely proud of our achievements over this time. I am leaving the company in good hands with a fabulous team with unique skills and know-how, and a balance sheet to support future growth plans.

Having successfully concluded the Lynas 2025 capital investment program and launched the Towards 2030 growth strategy, it is the right time to make this transition.” Board Chair John Humphrey said: “Amanda has made an outstanding contribution to Lynas and the rare earths industry over the past 12 years. On behalf of the Board and the whole Lynas team, I thank Amanda for her leadership and dedication to our people and our company.

This company was in a very difficult position when Amanda took on the role of CEO. It is thanks to Amanda’s hard work, drive and tenacity that Lynas is today a leading rare earths producer and critical supplier to global manufacturing supply chains.

Under Amanda’s leadership, the company’s production and operating footprint has grown and our market value has increased from around $400 million in 2014 to close to $15 billion. This provides an excellent foundation for the company’s continued growth and development.”

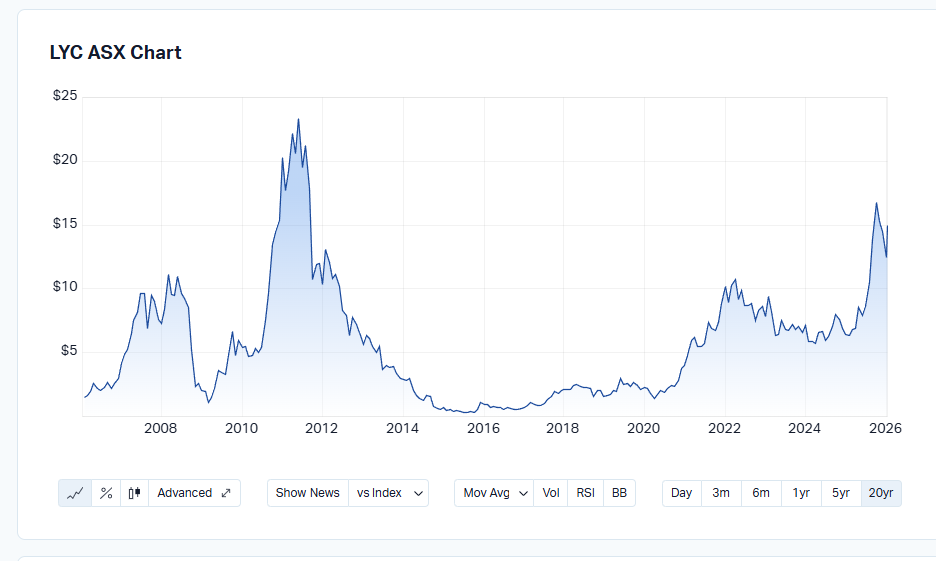

2014 chart shows price below $2

Now circa $15 share price.

Lynas Rare Earths announces the signing of a Memorandum of Understanding (MoU) with Korean permanent magnet manufacturer JS Link to develop a sustainable rare earth permanent magnet value chain in Malaysia.

Under the terms of the MoU, Lynas will collaborate with JS Link on the development of a 3,000 tonne capacity NdFeB permanent sintered magnet manufacturing facility near the Lynas Malaysia advanced materials plant in Kuantan, Malaysia. Lynas and JS Link will also collaborate in respect of the supply by Lynas of Light and Heavy Rare Earth materials to JS Link to support production of NdFeB permanent sintered magnets. The MoU is non-binding and subject to a definitive agreement.

( my opinion generally these MOU just hot air! no quantitative use for shareholders )

Lynas is delighted to report a number of ‘firsts’ in the quarter to 30th June 2025.

- At 2,080 tonnes, quarterly production of NdPr exceeded 2,000 tonnes for the first time

- Dysprosium Oxide (Dy) and Terbium Oxide (Tb) were produced on the new production line at Lynas Malaysia in May and June respectively, the first commercial production of separated Heavy Rare Earths (HRE) for Lynas and the first commercial production outside China in decades

- The installation of the first wind turbine at Mt Weld and the completion of the solar farm as we transition to largely renewable energy sources at Mt Weld

- A first MOU has been signed with the Kelantan Menteri Besar (MB) Inc for the collaborative development of rare earth deposits and the future supply of mixed rare earth carbonate (MREC) to the Lynas Malaysia plan

Idea is that the free cash flow to improve from today

Return (inc div) 1yr: 68.44% 3yr: 6.90% pa 5yr: 37.00% pa

Return (inc div) 1yr: 14.91% 3yr: 3.72% pa 5yr: 27.23% pa

5yr chart:

LYC has charted $10 back in 2022

During the March 2024 quarter Lynas expects maximum production rates of approximately 300tpm growing to 750tpm in the June 2024 quarter.

24/10/23, Share Price Reaction: $6.82 up 12.4%

Return (inc div) 1yr: -13.23% 3yr: 33.60% pa 5yr: 34.26% pa

05-Sep-2023: I've been trawling through some recent MoM (Money of Mine) podcast episodes today while doing other things, and I came across a very interesting discussion on Lynas, and why they are not well liked by the locals in Kalgoorlie. It suggests that they don't rate a Social Licence to operate as being particularly important, and may give some insight into why things went so pear-shaped for them in Malaysia - apart from the court challenges and protesting from Chinese-sponsored protest groups that may have been mostly "rent-a-crowd" participants, or so I was previously led to believe.

If you're interested in Lynas as a prospective investment, or are already invested in the company, or even if you're just interested in how a company like Lynas can piss off the local community in a big way and how that might affect their future prospects, this is worth a listen:

Lynas Confirms Kalgoorlie Cost Blowout and Red 5 cash? | Daily Mining Show - YouTube

Plain Text: https://www.youtube.com/watch?v=iW78Zhs8tyo

August 29th, 2023: Their Show Notes: "More annual results with intriguing company commentary for us to pull apart today. We get the ball rolling with a snippet from Monday’s Fortescue (FMG) investor call, honing in on why Fiona Hick departed after just 6-months in the job. We have an in-depth discussion on Lynas (LYC), looking into their Kalgoorlie plant build, the social licence to operate and their current rare earth strategy. Then, Red 5’s (RED) annual result caught our eye, with a close look at trade payables. Ramelius (RMS) get a mention with majority ownership at Musgrave (MGV), while Hillgrove Resources (HGO) is our final talking point of the day, with the aspiring copper producer releasing some copper intercepts from depth."

CHAPTERS

0:00 Preview

1:11 Intro (with Brodes)

7:07 Fortescue investor call

10:16 Lynas Kal update, Community standing & Rare-earth strategy

24:16 Red 5 post up annual numbers

37:11 Ramelius get majority ownership at Musgrave

37:35 Hillgrove approaching first production

-------------------------------

DISCLAIMER

All Money of Mine episodes are for informational purposes only and may contain forward-looking statements that may not eventuate. The co-hosts are not financial advisers and any views expressed are their opinion only. Please do your own research before making any investment decision or alternatively seek advice from a registered financial professional.

-------------------------------

Disclosure: I do not hold Lynas (LYC) shares, but I have done in prior years, and it was far from a smooth ride. I would be worried about a company that is prepared to drain Kalgoorlie's parks and reserves irrigation water reservoir - because they (LYC) have the right to - a very stupid decision by the Kalgoorlie-Boulder City Council to be sure - and then spend so little supporting the local community. The locals already hate them and Lynas are doing very little to try to improve their standing in the community in which they wish to operate.

Noted the slide no percentage comparison: - 43%=310 / 540 Sales: -20% ( Return not Good )

Phew, not easy to read LYC financials.

mmm. Cannot see ant Out Look statement,

- FIN FY23 Financial Results Announcement

Revenue of $739.3m remained strong. EBITDA, at $377.7m was 51% of revenue with NPAT at 42% of revenue. Whilst strong, these results were lower than those in FY22 when market prices were at record highs. “During the year, we invested $595m in capital projects and completed the year with a cash balance of $1 billion, providing funding certainty for completion of our key growth projects.

Heres more a better view of position

Appendix 4E and FY23 Financial Report

EPS -43%= 34/59

...will announce its quarterly results for the period ending 31 March 2023 on the morning of Friday 21 April 2023

As intimated by the string of recent broker upgrades, the Lynas sell-off has been getting folks' attention (including mine). Whatever Lord Elon or his minions say apparently strikes fear and panic (or joy) into the hearts of the herd and would appear to have turbocharged Lynas' descent.

As part of my Lynas homework, I came across references to research and commentary from Adamas Intelligence who seem to be a (the?) go-to rare earths research house. They've provided some quite useful commentary regarding the Tesla announcement and authored the pay-to-read "Rare Earth Magnet Market Outlook to 2035" report (though posted some useful excerpts/findings here). They also authored + released for free the "State of Charge: EVs, Batteries and Battery Materials" report covering 2022 H2 global passenger xEV (i.e., HEV, PHEV and BEV) market performance which is tangentially relevant to Lynas.

In a nutshell, Adamas are forecasting a structural supply deficit for rare earths through 2035. Combined with concerns over China's supply dominance and the comparative environmental "dirtyness" of their supply operations vs other non-China minor players, there seems to be a pretty solid outlook for Lynas who are proven, profitable, and growing their production capacity (their Malaysian licencing woes notwithstanding).

Forward estimates look up and to the right if you ignore last year's result as a PCP anomaly, and extrapolating out 2-3 years using some low to mid range PEs suggests there are better than average odds of easily achieving 10-15%p.a. growth at the current ~$6 SP.

I took a ~1% starter position today @ $6.05 and will probably average down if it keeps tanking.

As an ethical and environmentally responsible rare earth producer, with capability and customer relationships built over the past decade, Lynas was well positioned to benefit from the robust rare earths market during the year.

All ethical here.

So looks ok, What we can mine and cannot mine is all ok. The choices we make could be governed by a few......

LYC under the ASX query microscope

- Release Date: 05/10/22 10:18

- Summary: Response to Appendix 3Y Query

- Price Sensitive: No

note, generally these reports are called Quarterly Report Appendix 4C

The bears are in the market so skittish holders all over the markets at present 2022.

The 2Q22 production update revealed a 33% lift in total Rare Earths Oxide production on 1Q22. Strong demand translated to favourable commodity pricing, which resulted in a record sales revenue of $202.7m over the quarter (vs $121.6m in 1Q22).

And for Comparison 30th September 2021

so the trend is still up going on these #s eg Sept Q Sales R': $121.6m vs Dec 2021 $202.7m up $81Mill at 67%

Discl: RL,