Consensus community valuation

Update below appears positive considering the number of times "substantially up" is used but the stock has had a roller coaster ride with the stock up as much as around $9.00 early in trading to being down 53c not long after. Not sure why the extreme volatility.

Held since 2009 and can't bear to sell and donate to the ATO.

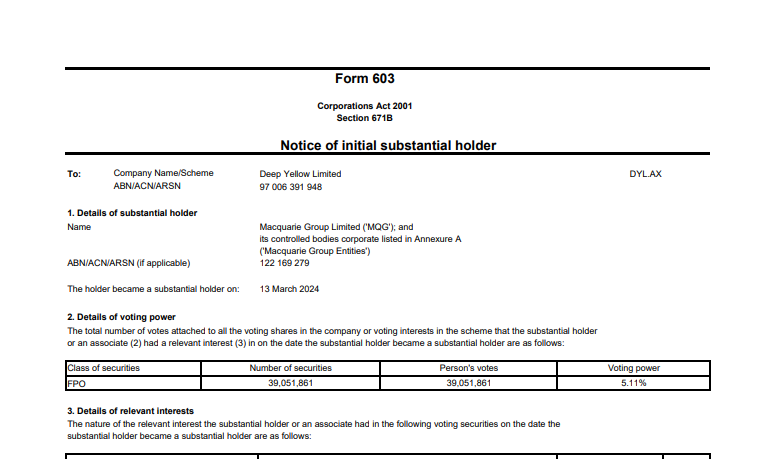

Macquarie Group Limited ('MQG')

What is Macquarie doing buying into DYL Uranium? - Are they shorting this DYL?

Some people might be surprised to find out that Australia's highest paid boss (CEO/MD) of all listed Aussie companies is actually a Woman, the CEO & MD of MQG, Shemara Wikramanayake.

That's the Good news. The Bad news is that the other 9 on that list above are all men, and that she wasn't even the highest paid executive at Macquarie last year, just the highest paid MD/CEO, as explained below.

Her large payout is in part in thanks to the Macquarie Group’s profit share arrangement, which richly rewards executives when the company does well.

And the listed financial group did do well in 2022, securing net profit of A$4,706 million, 56% up on the year before.

Founded in 1969, Macquarie provides clients with asset management, banking, leasing, advisory and risk and capital solutions. The Sydney-headquartered firm employs more than 18,000 people and has offices in 33 markets globally and A$871 billion assets under management.

Driving the financial group’s success since 2018, Shemara has a three-decade-long career at Macquarie Group, most recently serving as Head of Macquarie Asset Management before taking the CEO role in 2018.

Since joining Macquarie Capital in Sydney in 1987, aged 25, she has worked in six countries and across various business lines, establishing and leading Macquarie’s corporate advisory offices in New Zealand, Hong Kong and Malaysia, and pushing the emerging asset management division of the business to become the bank’s most profitable venture.

Shemara, who is UK-born and of Sri Lankan descent, is the first Asian-Australian woman to head an ASX 200 company and has been instrumental in driving diversity at Macquarie, where at least half of female employees identify as coming from a culturally diverse background, while globally, more than a third of Macquarie female directors identified as ethnically diverse.

Despite this, the firm remains male-dominated, with less than 30% of the senior management ranks female.

--- ends ---

Source: https://businesschief.asia/corporate-finance/these-six-ceos-are-australias-highest-earning-heres-why [27-July-2023]

That top 10 list (of highest paid CEOs/MDs from 2022) above is based on the ASX100 Index, so Australia's largest 100 companies, generally speaking. If you expand that out to the full ASX300 Index, and look at the top 50, Shemara is still at #1, but the Bad news is she is still the only woman on the following list. Well there are two others, Liz Gaines (FMG) who quit that role late last year, and Jeanne Johns from Incitec Pivot (IPL) who left in June this year.

Jeanne Johns was replaced by Paul Victor as an interim CEO at IPL (and he's still in that role today), while the changes at FMG were a little more complicated. Liz was offered a new role as an executive director and global ambassador for Fortescue, and is paid around $1.3 million p.a. for that, and her old CEO job was split into two - Metals and FFI - with the CEO of Fortescue Metals job going to Fiona Hick who left after only 6 months and was replaced by Dino Otranto who had been their head of operations. The other CEO role at FMG was called CEO of FFI (Fortescue Future Industries) and is now called CEO of Fortescue Energy - which includes:

- Fortescue Future Industries (FFI) - Green energy technology and production;

- Fortescue WAE (Williams Advanced Engineering) - Battery and fleet technology development and manufacturing; and

- Fortescue Hydrogen Systems - Electrolyser and hydrogen production systems development and manufacturing.

...and that role was given to Mark Hutchinson.

So while there are three women on the following list of the 50 highest paid CEOs from Australia's largest 300 listed companies (i.e. from the ASX300 Index), only one of those three, Shamara Wikramanayake, is still a CEO or MD today (Shamara is both).

Source: https://www.afr.com/work-and-careers/workplace/revealed-australia-s-50-highest-paid-ceos-in-2022-20221205-p5c3o6 [9-Dec-2022]

Well done to Shemara obviously - she has done very well - however - while it's great that she tops these lists, it's not too great that all the other CEOs and MDs are men. At least the well paid ones seem to be dominating these lists, and despite a fair amount of progress getting better representation on company Boards, women are not getting anywhere near equal representation in very senior roles within Australian listed companies. I'm am seeing more women CFOs these days and heaps of women are in senior HR, "People" and "Safety" roles, but we do need to see more women CEOs and MDs. I find that many women tend to have superior multi-tasking skills, they are more willing to listen and take other ideas on board and work collaboratively (maybe that's a testosterone and/or ego issue with many men), they tend to have less anger management issues, and from my limited experience with middle-management, they tend to deal with stress more appropriately and effectively. And the good ones also know bullsh!t when they hear or see it and don't accept it. Being a strong, decisive and effective leader doesn't mean you automatically have to be a dick - or have one.

Macquarie chief Shemara Wikramanayake topped the ranks of CEO pay again in 2022. Bloomberg

Further Reading: https://www.smh.com.au/business/small-business/it-s-despicable-kim-jackson-calls-out-lack-of-funding-for-women-led-companies-20190701-p52333.html

Venture capitalist Kim Jackson wins business award (afr.com)

How I made it podcast: Carolyn Creswell and Carman’s, from checkout chick to $170m empire (afr.com)

Manning Cartell co-founder Gabrielle Manning on how to create a successful fashion brand (afr.com)

Topic | Female Founders | Australian Financial Review (afr.com)

- A look back at 27/07/23:

*Difficult for the 'Millionaires Factory " the increasing high interests is the wrong environment for MQG the strategy.

Return (inc div) 1yr: 2.99% 3yr: 16.67% pa 5yr: 11.59% pa

Return (inc div) 1yr: 2.99% 3yr: 16.67% pa 5yr: 11.59% pa

Glenny's report a bit here:

Mr Stevens said “The Group delivered a record profit of $A5.2 billion, for a return on shareholders’ equity of 16.9 per cent. This was an exceptional outcome, achieved by a high-performing management team who deliver for shareholders by delivering for clients.

Macquarie’s diversification was again evident – even as some business lines faced difficult trading conditions, others were able to expand profitably by servicing a growing client base

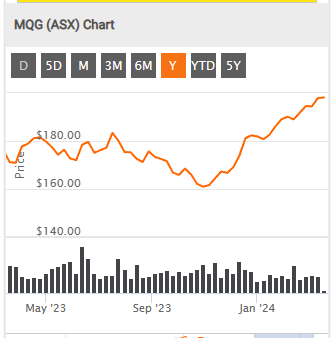

MQG below:

Return (inc div) 1yr: -1.24% 3yr: 19.43% pa 5yr: 13.19% pa

Return (inc div) 1yr: -1.24% 3yr: 19.43% pa 5yr: 13.19% pa

MQG Return peak to trough is 100% 1- 2 = $200/$100

Compare Growth performance:

While here - A look at CBA over the last 5 years.

Conclusion: MQG vs CBA ends up at the same destination in recent times..........x Return( inc Div ) Compared..

MQG - i guess, can have certain assets that generate returns. CBA and the big 4 have more banking rules around how they can grow their assets., to grow profitability.

CBA chart Below:

CBA Calculate from the chart here:

Peak to trough is 66% 1- 1.666 1.666'=100/60

( so CBA less growth 66% vs MQG 100% ..not including dividends ...)

21-Mar-2021: Most of the companies that are popular here on Strawman.com do not have a lot of major broker coverage, so I don't look at this too often, but I was having a look at Macquarie today and I was surprised by how varied the broker opinions and targets are. Obviously MQG is a leveraged play on the stockmarket, in that they tend to outperform in a bull market and are absolutely smashed in a bear market, i.e. they tend to overshoot the general market in both directions when the markets are moving. Broker views on MQG are therefore based on their outlooks for markets globally, as well as whether or not they think MQG has already run too hard. Here's what they most recently had to say, as summarised by Rudi Filapek-Vandyck at FNArena.com:

Morgans - 23/02/2021 - Add - Target: $162.30 - Gain to target $13.93

Macquarie Group has upgraded recent guidance for profit (NPAT) to be “up around 5%-10%” on pcp from "slightly down on FY20”. This was driven by increased demand for gas and power as a result of severe weather conditions across North America, explains Morgans.

After upgrading forecasts, the analyst notes the diversification of the Macquarie business has come to the fore and will help deliver an impressive profit growth outcome. It's considered the group remains well positioned to seize opportunities on the other side of covid-19.

The Add rating is unchanged and the target price increased to $162.3 from $147.

Target price : $162.30 Price : $148.37 (23/02/2021) Gain to target $13.93 9.39%

Credit Suisse - 23/02/2021 - Neutral - Target: $145.00 - Loss to target $-3.37

Macquarie Group has upgraded guidance for FY21 earnings to be up around 5-10%, having previously guided to "slightly down" on FY20. Accordingly, Credit Suisse upgrades estimates, anticipating an improved performance from the commodity markets.

Macquarie Group has indicated extreme winter conditions in North America have increased demand from clients for its services in relation to gas and power. Neutral rating retained. Target rises to $145 from $141.

Target price : $145.00 Price : $148.37 (23/02/2021) Loss to target $-3.37 -2.27%

Morgan Stanley - 23/02/2021 - Overweight - Target: $160.00 - Gain to target $11.63

Macquarie Group now expects FY21 profit to be up 5-10% compared with the prior guidance of "slightly down". Morgan Stanley expects a mildly positive reaction in the share price.

Winter weather in North America has driven stronger commodity trading conditions and the broker calculates new guidance implies an extra $500-600m in revenue in the commodity market segment.

This will be a one-off trading gain, with no flow to FY22. Overweight rating, $160 target and In-Line industry view maintained.

Target price : $160.00 Price : $148.37 (23/02/2021) Gain to target $11.63 7.84%

Ord Minnett - 23/02/2021 - Accumulate - Target: $158.00 - Gain to target $9.63

Macquarie Group has upgraded first half guidance, now expecting net profit to rise 5-10%. Extreme weather in North America has increased demand for the company's capabilities in the gas and power business.

Ord Minnett increases assumptions regarding multiples, to better reflect the value of the long volatility position that pays off sometimes when conditions are supportive. This leads to an increase in the target to $158 from $155. Accumulate retained.

Target price : $158.00 Price : $148.37 (23/02/2021) Gain to target $9.63 6.49%

Citi - 23/02/2021 - Sell - Target: $125.00 - Loss to target $-23.37

Macquarie Group has upgraded its FY21 net profit guidance by 5-10% implying a profit of $2.85-$3bn. – The upgrade was led by severe cold weather in Texas that has caused prices in the pipeline to spike.

Citi believes the upgrade suggests the group's commodities and global markets' division earned $600m in revenue in just 2 weeks. The broker upgrades its FY21 profit to $2,934m or 7.5% higher than FY20 while leaving the outer years unchanged.

Sell rating is maintained with a target of $125.

Target price : $125.00 Price : $148.37 (23/02/2021) Loss to target $-23.37 -15.75%

UBS - 10/02/2021 - Neutral - Target: $145.00 - Loss to target $-2.37

UBS observes Macquarie Group's update on December quarter shows a strong cyclical recovery in revenue with market conditions improving significantly. Even so, the group expects FY21 earnings to be slightly down on FY20.

The broker has a positive medium-term view on Macquarie Group as hard asset deal-flow improves and asset recycling accelerates.

Looking at the recovery in trading and markets revenue and the significant operating leverage, UBS upgrades the group's FY21 earnings forecast by 15%.

Neutral rating with the target price rising to $145 from $135.

Target price : $145.00 Price : $147.37 (10/02/2021) Loss to target $-2.37 -1.61%

Note: Excludes dividends, fees and charges - and negative figures indicate an expected loss.

MQG closed at $148.80 on Friday (19-Mar-2021). [I do not currently hold MQG shares.]