Consensus community valuation

13-April-2024: Update: I don't think McPhillamys is going to progress much in the next little while because of significantly increased costs - probably best explained by the MoM lads here:

Regis disappoints with McPhillamy's numbers [03-April-2024]

McPhillamys-Gold-Project-Definitive-Feasibility-Study-Update.PDF [03-April-2024]

So yeah, nah... Sold my Regis shares out of my SMSF after I digested all of that and I now have zero direct exposure to RRL either here or there (or anywhere).

My current opinion is that there are better gold companies to be invested in at this time than Regis.

My previous thoughts (when I held them) are below:

12-June-2023: My $2.78 price target (PT) is probably a LOW price for this company once they start producing gold from McPhillamys, which has now received the necessary development approvals to go ahead. McPhillamys is still farmland at this stage, so production is a couple of years away, and they are still working through the final FID alongside further issues that they still need to resolve. The recent approval, which I did discuss here at the time, did come with a raft of conditions, as expected, which are designed to protect the nearby Belubula River, and the rest of the surrounding environment.

The headwaters of the Belubula River - which runs into the Lachlan River near Cowra, then the Lachlan River runs into the Murrumbidgee River (near Balranald) which runs into the Murray River (at Boundary Bend, just east of Robinvale) which runs all the way to the sea at Goolwa (south east of Adelaide, S.A.) - are in and around the McPhillamys area.

The Belubula River actually starts about 10km north east of Blayney, but it's just a stagnant creek until it gets down to Blayney.

Below is what the Belubula looks like where the NSW Mid Western Highway (A41) crosses it about 2km northeast of Blayney:

Note the "Save the River" sign on the right.

The photo above is looking east, away from Blayney. The following photo is from the middle of that bridge looking south, i.e. downriver.

Not much of a river at this point, but the start of the river.

And McPhillamys is North of this point, above the start of the Belubula River, but considered to be in an area that forms part of the Headwaters (or source water catchment area) for the Belubula River.

Here's an example of the type of protest group that is against McPhillamys and against mining in the area altogether.

https://www.facebook.com/BelubulaHeadwatersPG/

So, while RRL HAVE received approval to develop McPhillamys as long as they comply with a heap of conditions and rules, there is still opposition to the mine, as there often is. So it's not a done deal until they get the thing into actual gold production, and that's not going to happen before CY 2025 or 2026 I would imagine.

Meanwhile, Regis have one of the most disastrous hedge books of all of the mid-cap Aussie gold miners, as explained here:

Regis Resources takes $27 million hit on hedging book in December quarter | The West Australian

Regis Resources takes $27 million hit on hedging book in December quarter

Danielle Le Messurier, The West Australian, Wed, 25 January 2023 10:26AM.

Haul trucks at the Tropicana gold mine. Photo Credit: Marc Esser.

Regis Resources took a loss of $27 million on its hedging book in the three months to December, delivering 25,000 ounces of gold at approximately $1571 an ounce.

That was well below the spot gold price of $2675 at the end of December. The Subiaco-based gold producer and explorer sold 121,3000/oz of gold in the quarter at an average price of $2412, which included the hedge impact.

The company’s quarterly report on Wednesday showed it generated operating cash flow of $93m from the Tropicana project east of Kalgoorlie— which it shares with AngoGold Ashanti — and Duketon project, north of Laverton.

Gold produced over the quarter totalled 117,3000oz all at average all-in-sustaining cost of $1760/oz.

Gold has been rallying since early November on signs the Federal Reserve was turning less hawkish. Spot gold was trading around around $US1937/oz on Wednesday.

The impact of Regis’ hedge book could grow, with Regis set to deliver a further 50,000oz into the hedging program over the remainder of fiscal 2023 — at 25,000oz a quarter and all at $1571/oz, below its current all-in-sustaining costs.

Another 120,000oz will be delivered in equal instalments of 30,000oz per quarter in fiscal 2024.

Guidance for the 2023 financial year remains unchanged with Regis forecasting 350,000-500,000kz at an all-in-sustaining cost of $1525-$1625/oz.

“The significant inflationary environment experienced in the September quarter continued in the December quarter, but we have seen some recent easing of pressure through reduction in the cost of diesel,” Regis Resources managing director Jim Beyer said.

“Despite this background of cost pressures, the planned increased production in the second half means we are anticipating our AISC unit costs to lower albeit to the top end of full year guidance, with efforts to contain costs continuing to be an important focus.”

--- end of excerpt --- [from that January article in the West Australian newspaper]

In short, the management at Regis (RRL), led by their MD Jim Beyer, entered into a fair amount of gold hedging (which is forward selling of future gold production at set prices) when gold prices were substantially lower, to guarantee future profitability, and those hedges were agreed to at prices that were well below the current gold price levels (which have risen substantially). Meanwhile, Regis' costs have increased, and in some cases their costs are now above the prices of some of that hedged production, so they will be selling a portion of their production at prices that are lower than their actual costs of production, so at a loss. Until they close out all of those low-priced hedges, they are only getting limited exposure to the current high gold price.

For context, the spot gold price is currently A$2,900/ounce, and has recently (in the past month) spent time over A$3,000/ounce. All of Regis' remaining hedges - which are scheduled to expire in June NEXT year (2024) are set at A$1,571/ounce. That's a LONG way below the spot price, and below most gold miners' costs these days.

Source: RRL-Change-To-Hedging-Structure-28May2021.pdf

Further Reading: ASX RRL: Gold miner Regis sinks on operational hiccups, wet weather (afr.com) [17 April 2023]

The original management that built Regis up from nothing, by successfully developing their Duketon assets, have all departed the company, and most of them turned up at either Capricorn Metals (CMM) or Emerald Resources (EMR) who both have better share price charts that Regis do, by a LONG shot.

The Senior Management and Board at Regis are therefore relatively new, and they haven't covered themselves with glory thus far, with the hedging debacle being their worst mistake, but there have been others.

So, a LOT rides on McPhillamys, because without McPhillamys, unless RRL get a decent takeover offer, I can't see the market getting super excited about this company. If they extinguished those hedges early, or if we just wait until the hedges have all been filled - which they will be by 28-June-2024, then they might get a positive re-rating, as long as the Aussie gold price was still nice and high at that time, but McPhillamys is the big one.

I think McPhillamys has the potential to be as positive for Regis as nearby Cadia has been for Newcrest (NCM), but it's a waiting game until they get McPhillamys into production, and many market participants don't have the patience to wait for these catalysts to play out. I expect Regis to get cheaper as we get closer to the end of June. However, I won't be adding to my positions, because I have enough exposure already. There is still risk there. Significant risk. And there are plenty of safer options within the sector, however I can justify maintaining an allocation within my gold sector funds to Regis because IF they get McPhillamys into production in a timely manner, and don't enter into more stupid hedges in the meantime, there is significant upside - in my opinion - that does justify that risk - for me.

But because of the risk, which is real, I wouldn't bet the farm on them.

12-Dec-2023: Update: Marked as stale. I was going to reduce my price target, but they've just closed out their hedgebook - see here: Closure-of-Hedge-Book.PDF [11-Dec-2023] so that is a real positive. They are now 100% unhedged and fully exposed to the high spot gold price.

The investment thesis still heavily relies on McPhillamys getting up and running, and that's still a few years away, with progress remaining very slow on that, despite the conditional approvals they've received - but I'm thinking that this closing out of their terribly priced hedgebook is a huge step in the right direction in terms of getting some positive market interest again.

Not sure if the market will respond straight away though. It might take a few more positive announcements - particularly concerning McPhillamys - for the market to turn positive on Regis again. However, WITH McPhillamys, Regis should hit $2.78/share at some point, so no change to that share price target today from me.

Disclosure: I no longer hold Regis here on SM or in my largest real money portfolio - they are only a smaller position in my SMSF now. That could however change at any time, without notice.

---

13-Apr-2024: As disclosed at top of this lot, I have now sold that small RRL position out of my SMSF, as I no longer think McPhillamys is likely to get built within the next 3 to 5 years, and there are far better places to invest in the Aussie gold sector at this point in time than in RRL. I no longer have any direct exposure to RRL.

11-Dec-2023: Regis Resources (RRL) had a diabolical hedgebook that would have seen them continuing to sell a good portion of their gold at around half the current spot price through until the middle of 2024. However they've just closed that hedgebook out - see here: Closure-of-Hedge-Book.PDF

That's a very positive move by a management team that has made their fair share of mistakes. It's not the same management team who were there during the Duketon build-out when Regis were fast growing and also one of the best dividend paying gold companies in Australia - no, those people all ended up at either Capricorn (CMM) or Emerald (EMR) - see screenshots from their websites below - and that former management team would NOT have signed up for such low priced gold hedges that didn't even gurantee profitability in the recent inflationary cost environment. But this lot - that are in charge now - have finally bitten the bullet and closed out all of their hedges - and are now fully exposed to the high spot price.

Not before time!

Their (RRL's) share price didn't rise, but it also didn't fall today, which was actually a good result, because there was a sea of red across the Aussie Gold Sector.

Here's where the early Regis management (prior to 2020) ended up. Some of them were together at Equigold before Regis:

I've highlighted some of the Regis experience in orange and Equigold in blue.

And here is a link to the list of current Regis Board and Management: Our Leadership - Regis Resources

DYOR if you are interested enough. Disc: I hold Regis (RRL) in my SMSF as part of a group of gold miners, but nowhere else currently. I hold CMM shares here on SM, and have held both CMM and EMR in real money portfolios previously, but do not currently hold any shares in either of them.

I am bullish on Regis IF they can get McPhillamys (in central NSW) up and running, but they're a few years away from that at this point. This news today about them now being unhedged is a definite positive. Imagine how much better off they'd be now if they'd done this last year!

The four logos at the top of that 14th June "Media Release" letter are the main 4 protest groups that RRL have to deal with in relation to developing their McPhillamys Gold Project.

- The Belubula Headwaters Protection Group (BHPG): The Belubula Headwaters Protection Group | Kings Plains NSW | Facebook - this group is the one most focused on McPhillamys. They were trying to stop it, but now that McPhillamys has been given development approval by the NSW Government, the BHPG is probably going to switch their efforts to trying to ensure that all environmental conditions stipulated in the approval documents are adhered to in full by RRL. They are also reportedly considering whether to spend the money required to appeal the approval decision. No appeal has been lodged to date.

- The Mudgee Region Action Group (MRAG): Mudgee Region Action Group (lueactiongroup.org) and Mudgee Region Action Group | Facebook MRAG is more concerned with stopping the Bowdens zinc/lead/silver project near the small village of Lue, 28 km east of Mudgee, but all of these groups are against mining and metals processing plants (including gold mills) in the NSW Central West region.

- The Cadia Community Sustainability Network (CCSN): Cadia Community Sustainability Network | Orange NSW | Facebook The CCSN is mostly concerned with the nearby Cadia mine, owned and operated by Newcrest Mining (NCM), and its environmental impacts, and holding NCM to account for environmental damage they might cause, but they also don't want a second open-pit gold mine in the area, which is what McPhillamys will be.

- The Central West Environmental Council (CWEC): About CWEC | Cwecouncil The CWEC is an umbrella network of district environment groups in the Central West of NSW. Member groups are based in Orange, Bathurst, Dubbo, Lithgow, Mudgee, Rylstone and other parts of the region. The CWEC provides resources to their member groups, helps to coordinate protests and meetings, submissions, etc, and organises Media Releases like the one at the top of this post on behalf of various member groups.

These groups held a public meeting yesterday (Saturday) in Orange:

If I see any newspaper coverage online (usually in the local rags like the Blayney Chronical or the Central Western Daily in Orange) of this or any other relevant meeting - I'll add a comment to this straw.

The last meeting they held was attended by around 100 people.

It is par for the course to encounter opposition to new mines being developed, however it is up to the mining company and the relevant government departments to ensure that the community and the environment are protected to the fullest possible extent and that all opposition concerns are heard and addressed. It is the mining industry's woeful prior track record that results in such opposition to new mine development, which is entirely understandable.

The industry needs to do a LOT better, and the relevant Government departments responsible for new mines being developed around the world are, for the most part, acting to enforce much greater environmental protections during the development and production phases throughout the mine-life of new mines that are approved for development. This means that companies wanting to develop new mines have to be prepared to spend a LOT more money these days than they would have had to spend 50, 40 or 30 years ago to develop a similar mine in a similar location.

The consultation and approvals processes are longer and more costly, they need to spend more on the design and construction to protect the environment (and their neighbours, including from excessive noise), they need to spend more during production to monitor environmental impacts (did somebody say Envirosuite? No? Just me then...) and there are much stronger compliance and reporting programs in place which also result in greater costs during the production years.

There are also usually higher costs included in a gold miner's ongoing AISC (all-in sustaining costs) during production, which relate to complying with environmental regulations and conditions. For instance, while mines can often still use Arsenic in the extraction process, that very toxic Arsenic has to removed from the tailings (a.k.a. waste slurry, which is all of the ore and processing chemicals and water used in the gold extraction process that remains after the gold has been extracted). And not just Arsenic. There are a lot of potentially harmful substances which can't be pumped out into TSFs (tailing dams) these days, especially in the better regulated countries like Australia and Canada.

Companies don't always get these responsibilities 100% right all of the time, but it can be very costly for them when they stuff up and do cause environmental damage, especially in countries like Australia and Canada.

To be clear, I am pro-mining, but only when the mining is done in an environmentally responsible manner, so I fully support these changes that have resulted in increased costs that miners have to endure. It means that the hurdles that new mines need to overcome are higher - the bar has been raised - so you need a project to be VERY good before you get serious about developing it into a mine, and that's a GOOD thing. And proper environmental protection during construction, commissioning and production, plus proper site rehabilitation after the mine has reached the end of its life, are essential.

It's just a pity that these much stronger approval processes and compliance monitoring/enforcement - plus environmental bonds that cover the rehab cost up front - were not introduced decades ago.

Disclosure: I am a RRL (Regis Resources) shareholder. I do not own NCM shares (NCM own the Cadia gold mine and mill). My IT (investment thesis) with RRL is fairly dependent on them getting McPhillamys into production in the next few years, as they aren't nearly so good without McPhillamys gold.

I expect most punters won't have the patience, or won't want to hold RRL shares during the next couple of years while McPhillamys gets built and commissioned. Meanwhile RRL have another year of low-priced gold hedges to close out, which limits their exposure to the higher gold price (much higher than their hedges which are all priced at AU$1,571/ounce and are due to last through to June 2024). So, RRL have gone from a low-cost, high-dividend-paying mid-tier Aussie gold miner to a middle-of-the-road-AISC, low-dividend-paying mid-tier Aussie goldie who are selling some of their gold at a loss over the next 12 months due to diabolical hedging mistakes by their overly conservative and short-sighted management team. Not much going for them, except for McPhillamys, which could be as good for RRL as nearby Cadia was for Newcrest. Cadia is not only Newcrest's best mine, it's their ONLY good gold mine - the other two (Telfer and Lihir) are rubbish IMO.

Further Reading:

McPhillamys gold mine, near Bathurst, approved to operate open-cut pit for 11 years - ABC News

McPhillamys Gold Project determination - NSW Mining

McPhillamys Gold Project | Mining, Exploration and Geoscience (nsw.gov.au) [McPhillamys Approval details from the Gov. Dept.]

Independent Planning Commission gives the go-ahead for McPhillamys Gold Project - McPhillamys

Green light for McPhillamys Gold Project - Mining Magazine

5_MGP_Community-Consultative-Committee-CCC-updated-310523.pdf (mcphillamysgold.com)

Community Consultative Committee (CCC) - McPhillamys (mcphillamysgold.com)

30-April-2023: I have recently written about this over in the "Gold as an Investment" forum, however I think it also deserves a straw under "Regis Resources", as McPhillamy's is their largest growth project, and this permission to go ahead from the IPC of NSW (in late March) has been a long time coming.

RRL have been in a nasty downtrend that is evident on their 3-year chart below, however they had a decent March and the first couple of weeks of April weren't bad either - the last two weeks have been fairly ordinary however...

Regis Resources (RRL) had a share price that rose +19.5% in March and another +2.4% in April, and while a lot of the recent rise can be attributed to the gold price which is making regular new all-time highs of late, they've also had a big win in late March with their McPhillamys gold project in rural NSW (not far from Newcrest’s flagship Cadia/Ridgeway mining complex) receiving approval from the NSW Independent Planning Commission (IPC) for an initial 11 year mine life – see here:

McPhillamys gold mine, near Bathurst, approved to operate open-cut pit for 11 years - ABC News [30-March-2023]

ABC Central West / By Xanthe Gregory and Hugh Hogan - Posted Thu 30 Mar 2023 at 1:35pm

The company has received conditional approval to extract gold for up to 11 years. (ABC Central West: Micaela Hambrett)

Regis Resources has received approval, with conditions, for its McPhillamy's Gold Mine at Blayney, near Bathurst, which includes an open-cut pit and tailings storage at the head of the Belubula River, as well as a pipeline to transfer water from Lithgow's Mount Piper Power Station.

The company intends to extract up to 60 million tonnes of ore, and, produce up to 2 million ounces of gold, during the mine's estimated 11-year life span.

The plans also include the construction of a 90-kilometre pipeline to supply excess water to the site from a coal mine near Lithgow.

The Department of Planning and Environment recommended the mine for approval, but, it was up to the NSW Independent Planning Commission (IPC) to make the final determination due to the number of submissions opposing the plan.

Key points:

- The mine has created significant debate in the community

- About 80 locals spoke about it at a meeting in February

- Strict conditions will be put on the mine's operator, Regis Resources

There was significant community debate about the mine.(ABC Central West: Xanthe Gregory)

The three-member panel found "on balance" the project was in the public interest.

The benefits, the IPC said, included "producing a significant mineral resource to meet the growing demand for raw materials".

It also said the mine would create employment, training and investment opportunities for the community, which would "outweigh the negative impacts".

Regis Resources wants to build the open-cut mine in the rural area.(ABC Central West: Tim Fookes )

In February, community members fronted IPC commissioners at a meeting.

About 80 people spoke, with most opposing the mine due to environmental concerns, particularly about water contamination, and, dust.

At least 85 people live within 2 kilometres of the proposed mine.

The IPC today acknowledged the various concerns about the mine, including its impact on Aboriginal cultural heritage, but said they could be "effectively avoided, minimised or offset through strict conditions".

In a statement to the Australian Stock Exchange, Regis Resources said it was "pleased" with the result.

"McPhillamys is one of Australia's largest undeveloped open-pittable gold resources and underpins significant value potential for Regis," said managing director Jim Beyer.

"We look forward to working with local communities, stakeholders and companies to mitigate the risks and concerns surrounding the project," he said.

Local environmental organisation The Belubula Headwaters Protection Group said it was disappointed with the decision but not surprised.

"We're working in a system that's skewed to approve projects like this, so unfortunately it's not surprising," said President Daniel Sutton.

Many locals are concerned about potential impacts on the Belubula River.(ABC Central West: Xanthe Gregory)

The group said it was good to see conditions placed on the mine to minimise impacts such as noise, dust and water but the focus should now be on enforcement.

"It's one thing for something to get approved and have conditions on it, but it's entirely different to actually enforce them," Mr Sutton said.

The group is now considering whether to appeal the decision to the Land and Environment Court.

--- ends ---

Related Stories

'It makes the village unliveable': Dust from gold mine will leave residents unable to open windows, panel hears

Critics claim proposed gold mine would risk food security, planning panel told

Mental health decline, fears for river dominate hearing into community's struggle with gold mine plan

So there is an option for the Belubula Headwaters Protection Group to appeal the decision, but I can't imagine an appeal would be succesful unless they are able to introduce new evidence or data that they have not already provided to the NSW DPE (Department of Planning and Environment) and/or the IPC (NSW Independent Planning Commission). Both sides have now had a number of years to present their case and I would expect that all sides of the argument have been carefully considered and, in the words of the IPC, "on balance" the project was deemed to be in the public interest.

In handing down their decision the IPC said that the benefits of the proposed mine (McPhillamys) included "producing a significant mineral resource to meet the growing demand for raw materials".

It also said the mine would create employment, training and investment opportunities for the community, which would "outweigh the negative impacts".

So, as I said, I'm not counting my chickens yet, but it's looking positive, and I just need to give Regis time to progress this through. They have allowed for a substantial amount of spending in relation to progressing the McPhillamys gold project in the current and the next financial year, so I'll continue to watch and wait. In the meantime, they continue to benefit from their 30% stake in Tropicana and their 100%-owned Duketon assets (producing gold mines in WA).

They are saying that McPhillamys has at least 2.5 million ounces of gold there and that they expect to extract at least 2 million of that during the initial 11 year open-pit period (that they have been approved for at this stage). Anybody who knows anything about Newcrest's (NCM's) nearby Cadia mine, without which NCM would be a total basket case in my view, as Cadia is the only really good gold mine they have (Telfer is rubbish, and Lihir has been a huge disappointment), may have an inkling about just how good McPhillamys may well end up being. Cadia is the mine that just keeps on giving for Newcrest.

Newcrest's flagship Cadia/Ridgeway gold mine and processing plant is shown there (in the map above) to the left (west) of McPhillamys, which itself is west of Bathurst and NE of Cowra (and very close to Blayney). Cadia is the open pit and the processing plant, while Ridgeway is the underground extension of Cadia. Together they are known as Cadia/Ridgeway and they are by far the best asset that Newcrest Mining (Australia's largest gold mining company, currently under a takeover offer from the World's largest gold company Newmont Corporation) have. Their other producing mines, Telfer and Lihir are very inferior to Cadia/Ridgeway.

Anyway, McPhillamys is NOT in production yet, and they're probably still a couple of years off being in production, but I definitely want to still be holding my RRL shares when they start producing gold at McPhillamys (in addition to Duketon and Tropicana).

While the approval can be challenged (appealed), I would doubt that any appeal would be successful given the lengthy consultation process that has already occurred in the lead up to this decision by the NSW IPC. So this is an important milestone for Regis.

I should also note that I expect the initial 11 year mine life to be extended at some point, just as the mine life at Cadia has been. It is, after all, a heck of a lot easier to get permission to extend the life of an existing operating mine than it is to get permission to build a new one from scratch. The more gold they find (at good mineable grades) the greater the chances of a mine life extension down the track.

Disclosure: I hold RRL shares (both here and IRL).

27-Sep-2021: https://www.ausbiz.com.au/media/the-call-monday-27-september?videoId=15169

That link will take you to "The Call" on Ausbiz at midday on Monday 27th September 2021 where Gaurav Sodhi from Intelligent Investor and Mathan Somasundaram from Deep Data Analytics both have a positive view on Regis Resources (RRL). The commentary on Regis starts from the 35 minute mark.

Gaurav says at one stage that Regis could be the cheapest gold stock on the market (at this point in time obviously, they have all fallen but Regis has clearly fallen more than most, this bit in brackets is my own commentary, not from Gaurav) and that the valuation looks extremely attractive. He also says that while Regis clearly overpaid for the 40% of Tropicana that they bought from IGO, that should not hurt them longer term because Tropicana is a wonderful asset, and one of the best three gold mines found in Australia over the past 20 years; it will be producing gold for decades to come, and with low costs as well.

While they both said that RRL is a Buy, the boys did not mention the ace up Regis' sleeve, being the McPhillamys gold project (in NSW), but I can tell you that if Regis get the approvals through for McPhillamys, it's going to cause a significant positive re-rating of Regis by the market, regardless of what the gold price is doing at that time, because McPhillamys is going to be a major gold mine with very attractive economics, and the fact that it is so close to (28 km from) Newcrest Mining's (NCM's) flagship Cadia/Ridgeway gold mining operations which processes approximately 27 to 30 million tonnes of ore per annum; Cadia produced 76,000 ounces of gold and 106,000 tonnes of copper in FY21.

Disclosure: I hold RRL shares.

19 Oct 2018: Regis (RRL) have released a presentation to the ASX announcements platform titled, "SEPTEMBER 2018 QUARTERLY REPORT & EXPLORATION UPDATE" - see here

Highlights:

- Q1 gold production 90,879 ounces at AISC of A$923/oz

- Another very strong operational quarter at the Duketon project

- Production above mid-point of FY19 guidance & AISC below bottom of guidance

- Continued strong cash-flow from operations $77.9m for Q1 (Q4: $85.3m)

- Cash and bullion holdings were $190m (Q4: $209m)

- $15.3m growth capex spent on satellite prestrips & TSF lifts (FY19f: $40m significantly weighted to H1)

- Board approved development of Rosemont UG operation

- Portal to be developed in Q3, development ore Sept19Q and production ore Dec19Q

- Exploration results indicating expansion opportunities beyond current stoping/resources

- Exploration efforts continue to deliver:

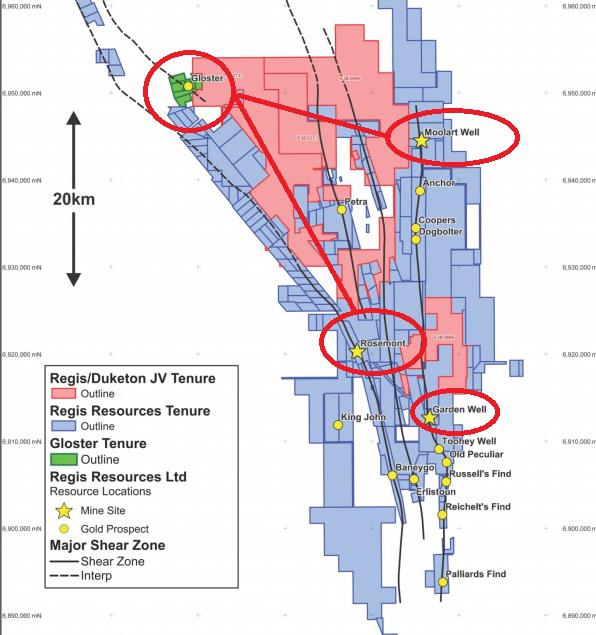

- Early stage drilling of Garden Well high grade underground targets very positive and suggest GW to follow same path as RMT

- Very strong extensional results at Discovery Ridge in NSW – exciting addition to MGP

- McPhillamys EIS and DFS work continuing

- PEA submitted and EARs issued, facilitating completion of EIS and DFS in Q3

- Investment decision expected Q3

Disclosure: I hold RRL shares.