As I’m a bit over getting bullied by spec resources investors (*cough* @BkrDzn), I thought it might be worthwhile to filter out the gold price for a while and focus on an interesting microcap idea.

Like most microcaps that that have been listed for a while, Nova Eye Medical (EYE) comes with a rocky history. I won’t go too deeply into it given our friendly LLM junior analysts can do a pretty good job of summarising. But long story short EYE is the old Ellex Medical Lasers, who after selling their laser business to a French company in 2020, used the proceeds to fund the development and commercialisation of iTrack, a microcatheter used in canaloplasties of the eye to treat glaucoma. Messy history aside, EYE now appears to be a one product company and a much cleaner investment story.

The treatment of glaucoma is a big industry but is dominated by eye drops which make up 85-90% of the market. That said, minimally invasive glaucoma surgeries (MIGS) are growing, largely because a lot of patients are non-compliant with eye drops and glaucoma is a progressive disease where they eventually require surgical intervention. Improvements in MIGS technologies is also leading to many ophthalmologists to prefer surgical intervention sooner.

Within the smaller but growing MIGS segment the dominant solution is bypass stents to reduce the build-up of pressure in the eye. Stents have historically been 60-70% of the MIGS market, but with improvements in products and a preference for ophthalmologists to not leave hardware behind in the eye, canaloplasties are taking market share.

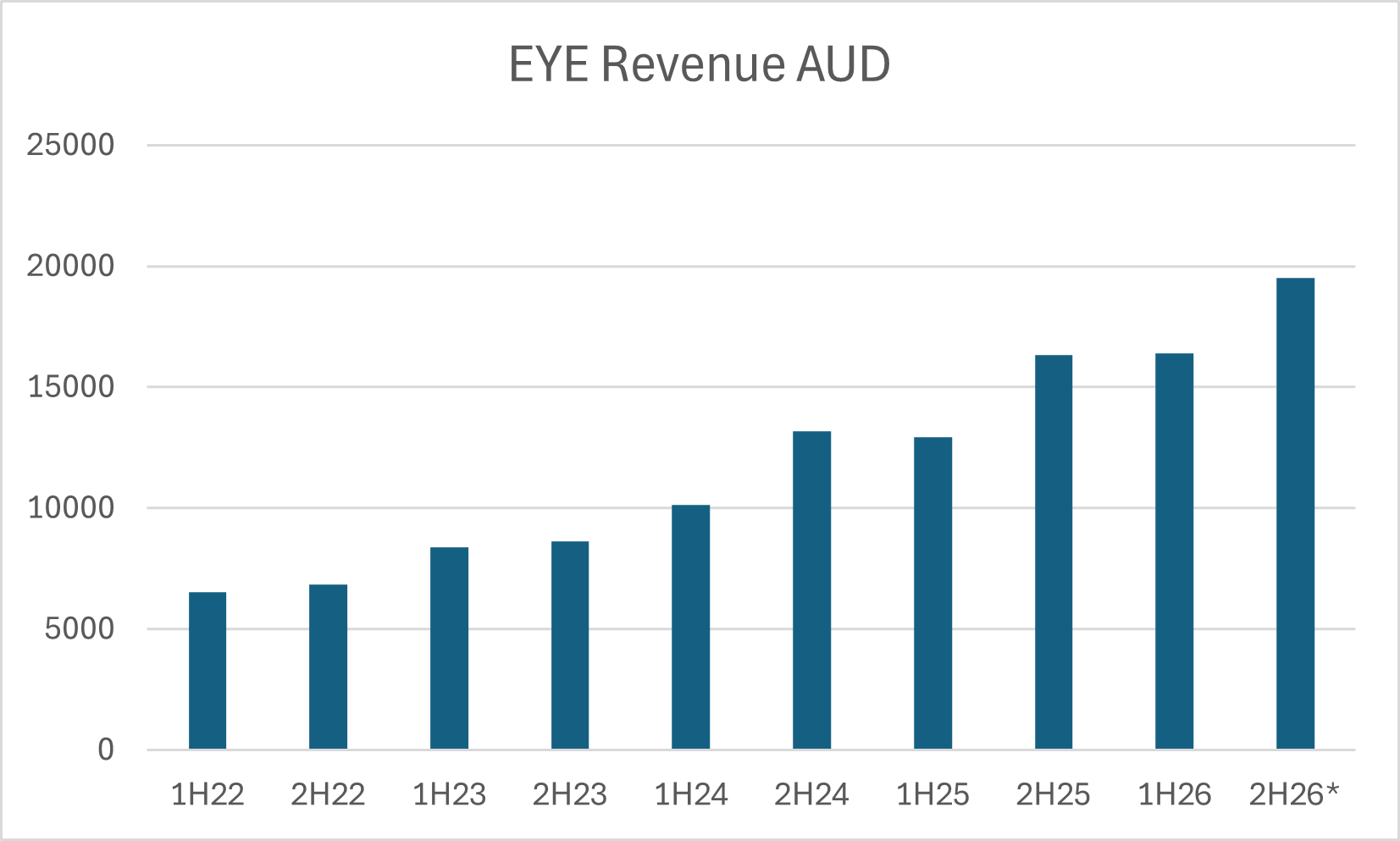

EYE’s original iTrack device had FDA approvals since 2008, but it wasn’t until the approval and commercialisation of the second generation iTrack Advance in 2023 where we started to see good sales traction, particularly in the US:

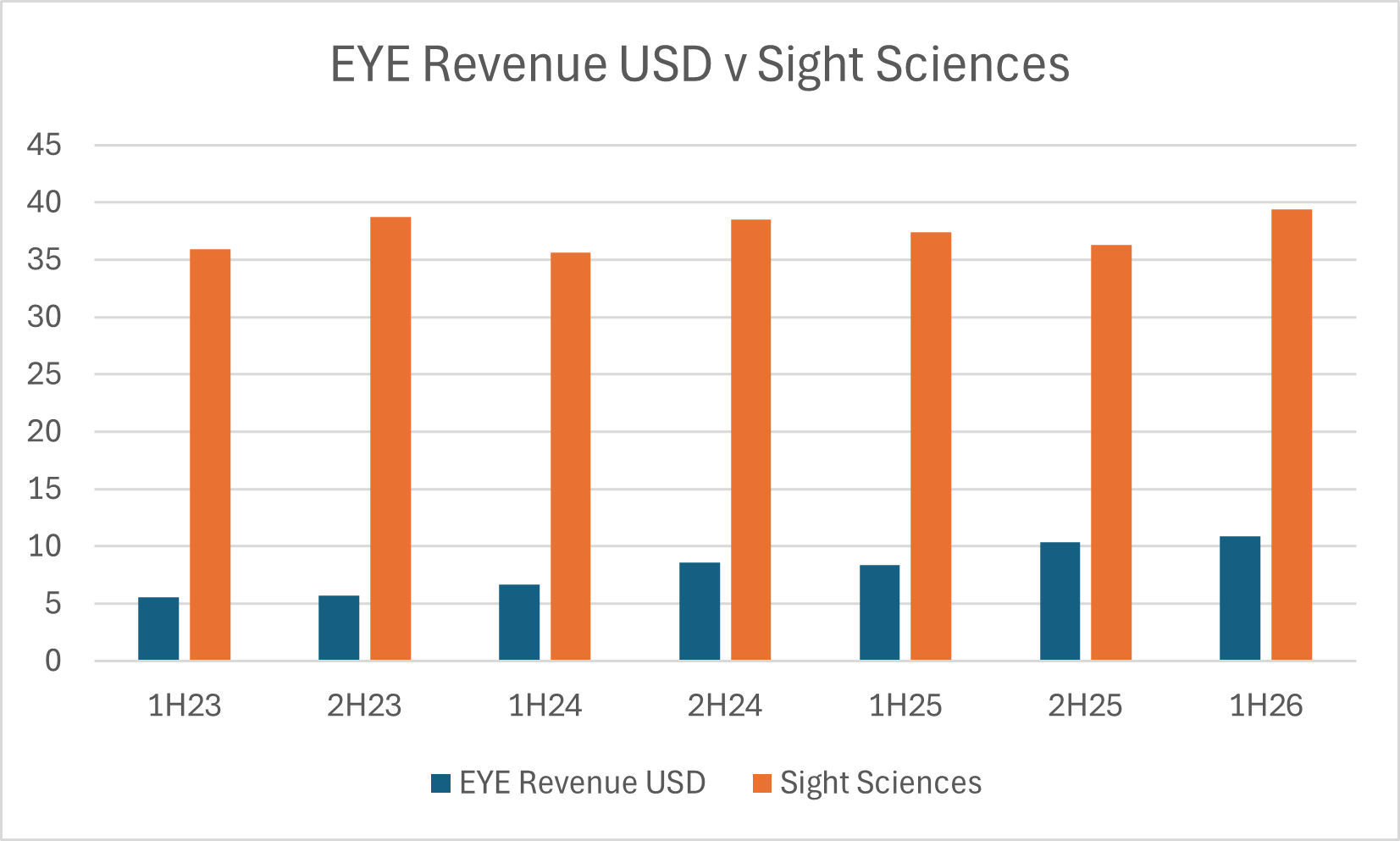

In the canaloplasty niche EYE effectively has just one competitor which is the Omni system produced by US based Sight Sciences. Fortunately, Sight Sciences is a listed business and we can track their glaucoma treatment segment over time and see how it compares to EYE:

Yes, it’s off a low base, but nonetheless it’s impressive to see EYE ~2x its revenue while Sight Sciences has largely been flat at the same time. It also supports EYE’s claim to be growing 3x faster than the broader glaucoma market.

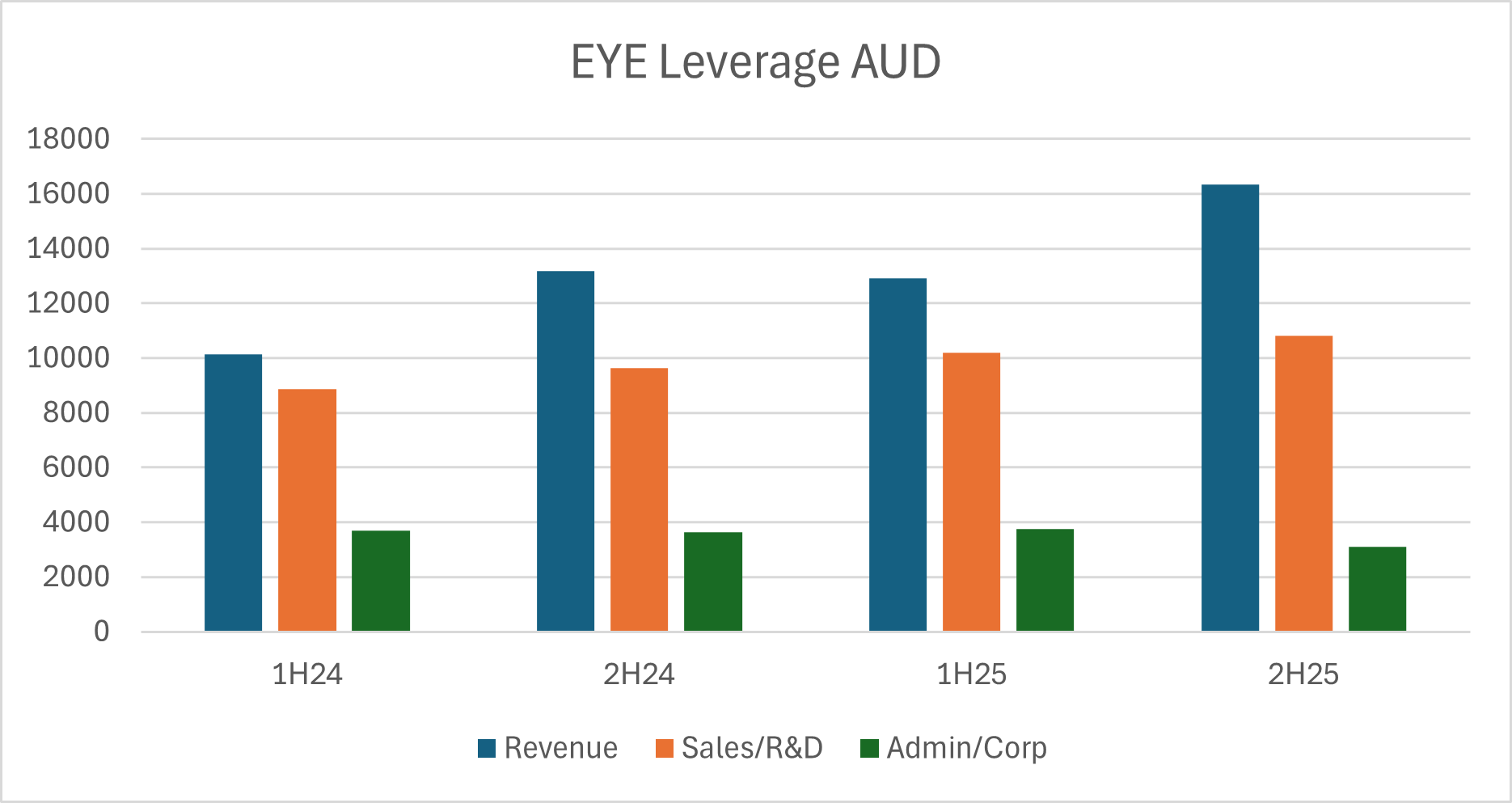

But we know what the market has wanted from microcaps for quite some time and that is profitability (or a clear path towards it). On that front EYE management has guided to EBITDA breakeven in 2H26, though it is worth noting that in the past this is a business/management that has missed targets and ultimately disappointed investors. That said, they have done a decent job in recent years of maintaining cost control while revenue has grown. It’s noteworthy that administration/corporate costs have been steady/falling with modest increases coming from sales/R&D:

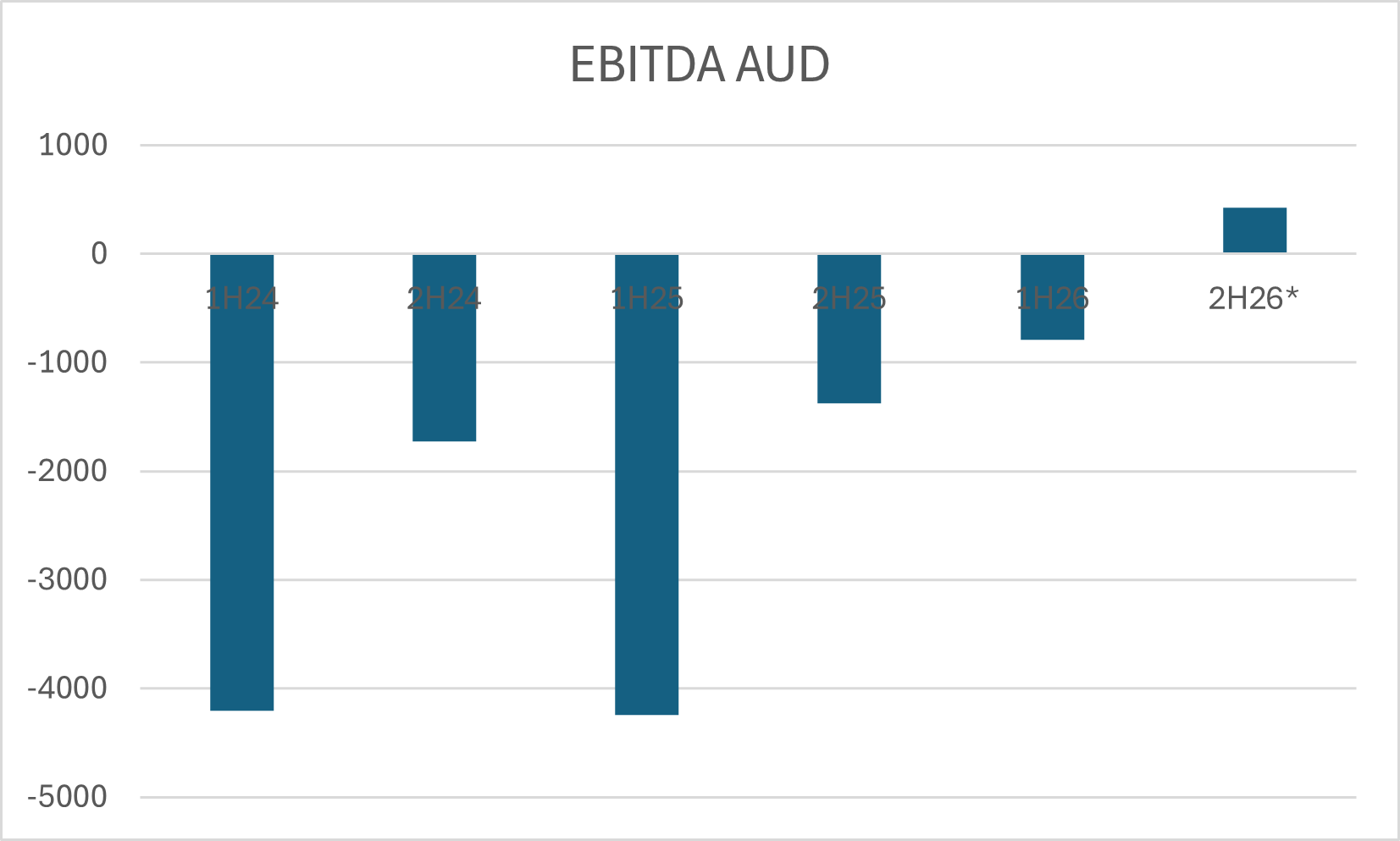

Assuming these cost trends continue and management land in the upper end of their guidance range, I think the target of EBITDA breakeven is achievable and would be a huge turnaround from the heavy operating losses of a couple of years ago:

Of course, despite being an interesting idea EYE is not short of risks. While they have shown consistently strong execution in their US sales since the launch of iTrack Advance, they need to continually invest in sales and R&D to maintain an advantage over larger peers with more resources. Changes to reimbursement is also a risk, right now reimbursement is $542 for surgeons and $2,231 for facilities which is supportive for MIGS growth, but reimbursement rates can change.

Finally, liquidity risk is real. EYE is tracking toward EBITDA profitability, but there is ~$1m in cash costs below that line in capitalised R&D and leases. At September EYE had $4m cash in the bank and a $2m working capital facility. The line between current cash liquidity and sustainable free cashflow breakeven is a tightrope, not impossible but it will require continued sales execution towards the top end of current guidance.

Ultimately, I think EYE is at an interesting point from an investment lens. A product gaining traction in the lucrative US market with high gross margins that can lead to genuine operating profit leverage as revenue scales over modest sales/R&D cost growth. The risk as we approach this key inflection is if US sales can't maintain its >20% revenue growth rate given the balance sheet may not be able to support any hiccups.

Would also love to get a view from the doyens of bio/medtech @mikebrisy and @Scoonieon this one!