Consensus community valuation

Pulmonary Embolism: (PE)

(PE) is a major acute cardiovascular condition. Epidemiological studies and public-health reporting in the United States indicate that PE results in approximately 600,000 – 650,000 diagnosed clinical episodes per annum, with the true burden likely higher due to under-diagnosis, and in a meaningful proportion of cases sudden death is the first presentation.

No Revenue here yet - so speculating on profits.

See how the Tuesday trading goes..

4DX Performance

Extending CT:VQ ™ into one of the largest outpatient imaging networks in the U.S.

SimonMed, headquartered in Scottsdale, Arizona, is one of the most influential, physician-led radiology Groups in the United States. Founded in 2003, it operates over 170 imaging centres across 10 states,

supported by a team of over 300 radiologists, and has built its national network around high-access, community-based imaging. SimonMed is recognised for its methodical approach to technology adoption, thoroughly validating new capabilities before deploying them at scale. This disciplined approach safeguards quality of care while maximising clinical impact across one of the largest outpatient imaging networks in the US.

4dx/announcements/ctvq-enters-us-outpatient-market-

The Performance looks okay here... These percentages look better than my 'emotional' meter %..

Something to 'crow' about up 18.86%

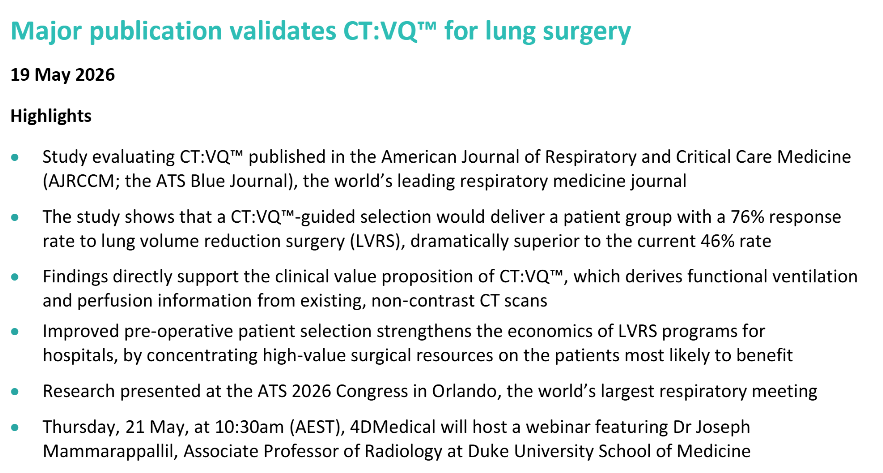

lung volume reduction surgery (LVRS).

The study included patients with severe emphysema undergoing bilateral LVRS and analysed pre ‑ operative

Non ‑ contrast inspiratory and expiratory CT scans using quantitative imaging techniques, including CT ‑ derived perfusion (CT:VQ™).

The authors conclude that integrating functional data from CT:VQ™ perfusion and anatomical (emphysema)

information from routine CT imaging can enhance and streamline patient selection for LVRS, increasing

successful outcomes from 48% to 76%, with potential to reduce reliance on additional perfusion imaging studies and improve clinical outcomes.

But the 4DX share price trades below $4 today

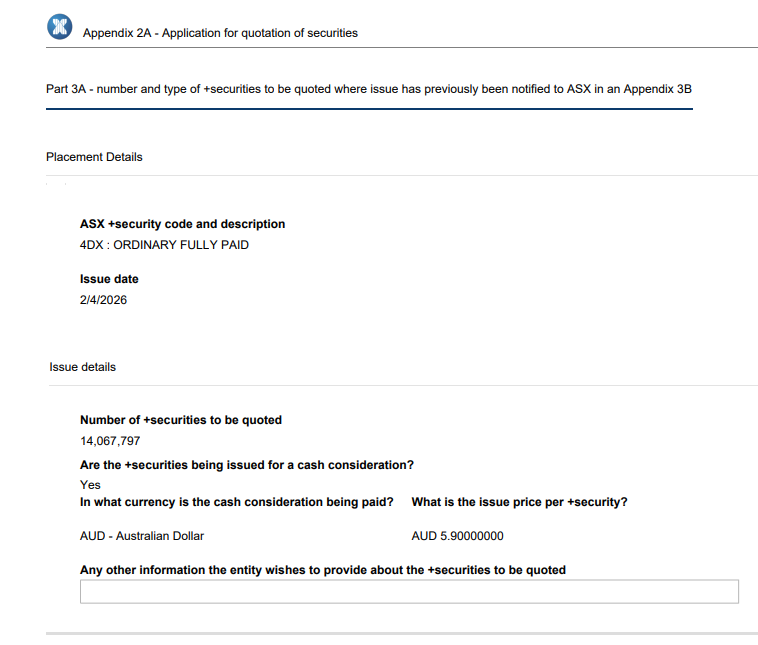

Just in this afternnoon:

application-for-quotation-of-securities

Added extra approx' 4% securities = Total will be 617mill issued

$4DX published its 4C earlier this week, and we've seen a bit of a pullback from recent highs, even before it was published.

Let's think about why that might be.

First up, as I write, this business has a market cap of $2.3bn.

In the 9 months YTD, it's operating revenue has been $5.0m, up 12% to pcp. That's an annual run rate of $6.7m. So that means today, the business is trading on a current revenue multiple of 343x.

And in the 4C while there lots of newsflow, including trials with several leading AMC, other agreements and sales, a EU/UK approval, and a deal with Glaxo, the detailed 4C report is conspicuous by the absence of one important factor for this type of business: Contracts with disclosed minimum values.

So at this point, you might say that it is early days - and you'd be right. You might also say that the revenue is coming because the CMS reimbursement was granted soon after FDA approval of CT:VQ. And a lot of commentators are pointing to that.

But there is where it is important to understand how the US healthcare system works.

Without getting into the details, the current US CMS reimbursement code is for a trial technology. It means AMCs and other facilities can use the product and get reimbursed for a limited period. Trial reimbursement also doesn't fit into the standing imaging workflow. And that's a big commercial barrier. Often, in order to process the claim, specific evidence/reports have to be attached to the submission.

Providers (specifically, the VACs that are gatekeepers within providers) will be reluctant to grant approvals for routine use given the temporary validity of the reimbursement and the non-routine workflow required.

And that's why I believe $4DX cannot disclose $-value contracts, ... because they don't yet exist.

We might be entering a phase now where $4DX is trialled by the leading AMCs, and these trials might run for 6 months, a year, maybe more.

Why do I know this --- well if you track back to the early days of $PME in the US, that was a similar journey they followed.

So what about the impressive numbers scans in the report: 477 site, +32% yoy, a quarter of 86,200 scans, up 79% in the Q and 240,000 scans YTD?

Well, at $5.0m revenue, that represents $21 per scan, not the US$1,150 opportunity touted for CT:VQ scans. Which means, the lion's share is coming from the legacy products, not the high value CT:VQ.

So, what's my point?

I think the market had turned $4DX into something of a meme stock. Some time ago I predicted that as the revenues fail to materialise at the rate implied by the valuation, there was a high likelihood it would come back down to earth.

Don't get me wrong, I think the tech is great, and in time, this might offer a great investment opportunity. (And of course, I am salty because I offloaded it at $1.90, when I felt it was already grossly over-valued, and wanted to bank my 10+-bagger.)

However, as each quarter unfolds, there is a risk that the revenue will fall short of the promise, and the stock continues to re-rate....downwards.

Fortunately for Andreas, he was smart and raised a ton of capital. (I can imagine Sam whispering in his ear: "Dude, there is a Valley of Death you now have to cross, cash up while you can.") And to Andreas' credit, he did. And so the board and management can ignore the share price, hopefully for long enough for the revenues to materialise. So, I remain poised for the "shoe to drop" ...

And I think Sam is on top of this too - he was super clear at the last $PME results to make sure everyone was focused on the PME "underlying" result, as the $4DX holding promises to bring a little volatility to the bottom line of that business.

Disc: Not Held (I hold $PME)

Today the application for quotation of securities finalised..

Trades at $6 up 7.7%

Financial position As at 31 December 2025, 4DMedical’s cash balance was $56.8 million. Considering the net proceeds of the January 2026 Placement and accompanying exercise of listed and unlisted options, the Company’s proforma cash position as at 31 December 2025 was $206.2 million.

I note: Just a Review - No forward looking projections here> cash in the bank ..always good...

Pro Medicus investment: leading global healthcare company invests $10m into 4DMedical to drive commercialisation of its product portfolio

$150 million institutional placement: welcoming several high-quality global institutional investors, whilst limiting dilution to existing shareholders limited to only 3.86% • Pro Medicus investment: leading global healthcare company invests $10m into 4DMedical to drive commercialisation of its product portfolio

Receipts from customers 2,917,023 2,564,271

Salary?

4DX $3.93. Opened at $4 now up 10%

Good vibes here..

After the COB today Cyclopharm (ASX:CYC) lodged the following with the ASX:

Cyclopharm with their Technigas product are in a fight to the death with 4DX with its recently FDA approved and US reimbursable CT:VQ™ technology.

Regal Funds Management has 11% of CYC. Looking like another Opthea moment for Phil.

Update: 5 September 2025

I have withdrawn my SM $4DX valuation. I am keeping the illustration here, below, unchanged for transparency and my own learning.

The reason is that in seeking to independently verify management's $1.1bn market sizing claim for NUC:VQ in the US, I am finding several observations that cause me to lose confidence:

- The market is likely significantly smaller, if I exclude sources that trace back to $4DX or the reference they've cited.

- Primary source analysis of US CMS databases confirms @Chagsy's observation that the procedure count decline in NUC:VQ and which can be confirmed as a US-market wide trend as reported over the period 2004-16 in the JAMA article I cited earlier, can be observed to continue over the period 2020-24. The decline is material and appears to be ongoing.

- An initial market size analysis driven by publicly-reimbursed procedure counts and reimbursement rates, and scaled for likely public-private splits and rates, leads to a conservative estimate of US$230m (AUD354) and a more balanced estimate of US$365m (AUD561m).

Again, the above numbers might also contain errors, but at least I have transparency of them to primary source data of procedures actually report. I am not reliant on some consultant's TAM report.

Thus, there is a potentially material error in my illustration of the potential value of $4DX that is attributable exclusively to CT:VQ displacing NUC:VQ.

As I have not completed my market deep dive, nor assessed the other value drivers for $4DX, I do not at this time have a valuation update to replace those posted yesterday. However, from the above notes, you can see the numbers will be very different.

Again, I want to emphasise that my analysis was solely focused on the NUC:VQ opportunity. There is a lot more to $4DX than that. It's just that I don't have a number for that yet!

Meanwhile, the SP soars upwards relentlessly, +25% today at the time of writing. (HC rules!)

And, as ever, this is not advice and you must do your own research.

Disc: Held, but I will be taking some profits in RL today (I'll let it run on SM for fun!)

---------------------------------------

Original Straw: 4 September 2025

Having realised I didn't allocate nearly enough capital to $4DX 5 weeks ago, even though I had a reasonable idea it was about to hit a transformational milestone, the question obviously arises "when should I be prepared to allocate more"?

It is of course important to not get caught up in the market reaction and hype and I find no better antidote than diving into ... yes, you guessed it ... a spreadsheet.

There's massive uncertainty around this business, but equally, there are some pretty solid facts to ground the valuation on. So, in this Straw, I'll layout how I've made some estimates of valuation.

In this case, I've reverted to a DCF, because the economics of the business are really quite simple, and I will go with that.

1. The Market

Quite simply, CT:VQ will over time replace NUC:VQ. It is as effective, much cheaper and more accessible. (I haven't assessed second order effects such as, the potential to increase the demand for CT facilities, which seems logically to folllow. @Scoonie already having flagged the negative impact on demand for nuclear medicine facilties.)

$4DX have estimated their TAM as 1.1bn in the US and 1.5 bn in RoW.

So, I will run three adoption scenarios, Slow, Moderate, Fast, where in the US 80% of the NUQ:VQ market is displaced, and in Row only 50% is replaced, as a lagging rate.

Rather than describe each scenario, here's what they look like in terms of market penetration.

Obviously, there are scenarios where the maximum penetration achieved is significantly lower. However, based on the data presented, this is really looking like a true technology replacement modality. Nonetheless the residual 20% in the US and 50% in RoW present some conservatism in the long run numers that drive the NPV.

2. Revenue

Calculating revenue is then simply the TAM x % market market penetration x Gross to Net.

I've assumed a GTN of 20%.

How reasonable is this?

Well in medical devices there are several possible supply chains:

$4DX - Hospital - Patient

$4DX - HMO - Hospital - Patient

$4DX - PACS Vendor HMO - Hospital - Patient

$4DX - Equipment Vendor - HMO - Hospital - Patient

Depending on the model the manufacturer ($4DX) can end up with anything from 10% to 40% of the revenue, skewed to the lower end.

However, $4DX is a breathrough technology, there is no alternative using CT methodology, and the modality offers significant advantages over the standard of care.

Therefore, in the direct sales model, $4DX should be able to keep 30+% of the $650 per scan, and even in the distributed chains, it should be able to negotiate better than the market norms.

So, I think 20% GTN is a reasonable assumption.

The resulting revenues are shown below:

3. Costs

I'm essentially assuming COGS are $0 (actually $4 per $650 scan). No a biggie for this guesstimate.

3.1 Opex

Opex is currently running at about $48m p.a. - that's a lot - although they have recently implemented some cost savings, to significantly reduce the burn rate.

However, I think they need to step up US sales and marketing, so I am going to step them back up to $50m in FY26 and inflate at 5% p.a.

3.2 Capex

Most of the develop costs appear to be expensed, however, I am going to put in $5m capex p.a., escalating at 5% p.a..

Other Assumptions

I have ascribed not value to $4DX's other products, other than the base $5m revenue from 2025, which is assumed to contine.

SOI - I assume capital will be raised soon to bring FY26 SOI to 500m, and thereafter to grow at 1% p.a.

WACC - 10% (sensitivity run at 15% discount rate)

Tax - 30%

DCF model run to 2040, with continuing value growth of 3% p.a.

4. Valuation Outputs

(in parenthesis I've added a sensitivity with a 15% discount rate)

Scenario1: Slow = $1.26 ($0.44)

Scenario 2: Moderate = $1.64 ($0.69)

Scenario 3: Fast = $1.92 ($0.91)

Conclusions

These are just one set of illustrations for what this business might do in the success case.

However, the potential is exciting enough that when the current froth blows off, I'll consider adding more around $0.70.

In terms of my SM valuation, I will put in the "Slow" senario of $1.26, and for the range around this I will put $0.50 - $2.00, as guesstimates.

Disc: Held in SM and RL

Lung imaging software firm $4DX has announced its FY25 results.

Their highlights

• Operating revenue for FY2025 was $5.9m, up 56% vs FY2024, with gross margins >90%

• Underlying SaaS revenue for FY2025 up 95% vs FY2024

• Cost reduction program initiated in Q3 FY2025 has delivered $6.5m in annualised savings and focused resources on revenue generation

Secured $10m strategic investment from Pro Medicus (ASX:PME), a leading global medical imaging software company

• CT:VQ™ FDA 510(k) submission filed in May 2025 and progressing towards clearance within anticipated timelines

• Announced the signing of a Reseller Agreement with Philips under which 4DMedical’s combined product suite was added to Philips’ product catalogue in Q3 FY2025

• Accelerating commercial progress in the U.S. with new contracts signed at key reference sites (UChicago Medicine and UCSD Health) and renewals at Cleveland Clinic, Stanford University and University of Michigan

• Contract wins in Australia included Integral Diagnostics (ASX:IDX), QScan and Perth Radiological Clinic (PRC)

• 4DMedical is now delivering SaaS products at 388 sites globally, up 60% YoY, and produced over 74,000 structural and functional scans in Q4 FY2025, up 35% QoQ and 105% YoY

My Assessment

Quick high level thoughts only: I'm expecting that FY25 and early FY26 will prove to be a pivotal period for $4DX. Should the 501K for CT:VQ be granted in a few week's time, then that will be a significant catalyst.

Of course it is very early days and $4DX is seriously burning cash, hence the timely assistance from $PME was important, and no doubt allowed $PME to extract a good deal.

In the 4 weeks since I took an initial speculative 0.5% RL position, it has grown to a 1.0% position. Part of me thinks I should be bold and increase ahead of the 501k decision, given their track record on 501s over the last few years has been pretty good.

That said, it is not cheap, and it will clearly be giving a lot of value away in its deals with Phillips, $PME. and others. However, good distribution deals accelerate the GTM and we have seen elsewhere, that these imaging companies can burn a lot of cash over many years as they try to grow via a direct strategy (e.g., $M7T and $VHT).

Patience required here, and I will take a risk averse approach initially, but increase with continued progress. The good news is that the SP is quite volatile, so picking your days to buy can make quite a difference.

Disc: Held in RL and SM

11 June 2025 Highlights • Olympus Corporation, one of the world’s largest medical device companies, launches a new campaign for SeleCT™ Screening across the United States

• SeleCT™ Screening uses 4DMedical’s lung density analysis technology on existing CT scans to identify candidates for the Olympus Spiration™ Valve System

• Full market release by Olympus creates large-scale U.S. deployment of 4DMedical’s AI-based lung imaging for therapeutic screening

The share price is not reflecting the CEOs cheerie confidence! ...normal ..hehe

see how this opens..

30.0¢

Change

0.000(0.00%)

Mkt cap !

$139.6M

4DX on the move!

https://hotcopper.com.au/threads/ann-4dmedical-files-fda-submission-for-ctvq.8597580/

4DMedical files FDA 510(k) submission for CT:VQ™, a non-contrast CT-based lung imaging software product for assessing both ventilation (V) and perfusion (Q) in the lungs

• CT:VQ™ represents a revolution in ventilation perfusion imaging, solving key clinical and logistical limitations across all forms of nuclear ventilation perfusion imaging

• Compelling clinical validation package, demonstrating equivalence (or superiority) to SPECT ventilation perfusion across multiple lung conditions

• 4DMedical expects to capture 100% of the one million nuclear ventilation perfusion scans performed annually

• CT:VQ™ is expected to align with the Company’s existing CT LVAS™ CPT code (USD $650), supporting rapid clinical adoption

• Provides the potential to grow the current ventilation perfusion market into new applications in disease monitoring and screening, due to the wide availability of CT infrastructure

• When including days spent with the applicant, the average time for FDA 510(k) decision is approximately 120 days

• 4DMedical will hold an investor webinar tomorrow, Tuesday 27 May 2025 at 11am AEST

Investor Webinar 4DMedical will hold an investor webinar tomorrow, Tuesday 27 May 2025 at 11am AEST, where Dr Andreas Fouras will provide further information, and host a Q&A session, in relation to CT:VQ™. Please register in advance using the following links: Phone registration: https://s1.c-conf.com/diamondpass/10047546-qpjld5.html Webcast: https://ccmediaframe.com/?id=a2ozxVzA After registering, you will receive a confirmation email containing information about joining the webinar or dial-in details for those who would prefer to join by telephone.

Last

30.5¢

Change

0.045(17.3%)

Mkt cap !

$137.4M

Life support for of $1.1M - 4DX will have to grow profitability eventually though.....

We are extremely excited to have been awarded the $1.1 million CTCM funding announced today. Combining both functional components of airflow and blood flow into a single analytical process represents a dramatic advancement in respiratory healthcare, providing the ideal test for phenotyping, early detection and evaluation of specific treatment responses for high-impact lung diseases such as Chronic Obstructive Pulmonary Disease (COPD), Cystic Fibrosis, pulmonary hypertension and pulmonary embolism.

A total of 28,044,096 fully paid ordinary shares New Shares will be issued to SPP applicants at an issue price of $0.89 per New Share. The New Shares issued will represent 8.1% of 4DMedical’s issued capital and will rank equally with existing shares on issue from their date of issue.

The New Shares issued under the SPP are expected to be allotted on Wednesday, 31 May 2023 and are

expected to commence trading on ASX on Thursday, 1 June 2023. The total funds raised, comprising the Placement ($20m) and SPP ($25m), amount to $45m (before costs).

Proceeds raised under the Placement and SPP will be used primarily to accelerate commercialisation of 4DMedical's respiratory imaging software and significantly strengthen the Company's balance sheet. Funds raised leave the Company with a cash balance of approximately $79.6m after costs as at 31 March 2023 on a proforma basis

Fouras - CEO (2012) circa 23% voting power.

1 Month ago 4DMedical (ASX:4DX) signs first US hospital SaaS contract https://youtu.be/ef8j0lr2JUI

Dr Andreas Fouras

Chief Executive Officer,Managing Director (Since 2012)

Bio

Dr Fouras is the founder, Managing Director and Chief Executive Officer (CEO) of the Group. He is also the Groups Chief Technology Officer being the inventor of its core XV Technology, maintaining a direct role in its evolution and development. Andreas career in academic research has a foundation gained within the Department of Mechanical and Aerospace Engineering at Monash University in Melbourne, Australia. This research into wind tunnel quantification garnered recognition as a young leader in the scientific discipline of fluid dynamics, developing a number of new approaches to the imaging of gas and liquid flow. Following completion of a Masters degree by research and a Doctorate (PhD), Andreas rapidly rose to the position of Professor of Mechanical and Aerospace Engineering and Director of the Laboratory for Dynamic Imaging.

He received accolades from a wide range of premier research bodies including the National Health and Medical Research Council (NHMRC) and the American Asthma Foundation. Andreas applied a novel concept to clinical use through the development of XV Technology, uniquely measuring airflow within the breathing lungs at every stage of the breath, providing both high spatial and temporal resolution at very low dose.

This research has been documented in over 100 peer reviewed publications and resulted in 72 patent applications with 40 granted. In December 2012, Andreas founded 4DMedical resulting from a deeply held personal and professional desire for his work to reach and positively influence as many people afflicted by respiratory compromise as possible, through global clinical translation.

Andreas leadership is evidenced as a commissioned officer in the Australian Army (Infantry) and through the prestigious Australian Davos Connections Australian Leadership Award for 2013. The focus of Andreas substantial intellect and energy is now concentrated upon applying business acumen, drive and innovation to the successful commercialisation of 4DMedicals technologies. Andreas is a member of the Medical Advisory Committee.