Consensus community valuation

Works in Progress

The latest press release from Anteris confirms they have now received regulatory approval for the PARADIGM trial in France. With public confirmation of the same approval in Denmark and the USA, I imagine the regulatory delays in any remaining participant countries are going to get smaller.

[Link to Anteris press release]

The clinical trials website now has 5 areas recruiting (with additional centers being added in San Francisco and a further Danish one having been added in recent weeks).

https://clinicaltrials.gov/study/NCT07194265

Final patient implantation by December 2026 and trial completion by December 2027 is still plausible.

Skin in the Game

I imagine that her financial advisor may not be too impressed, her concentrating her human and financial capital so closely. However, it has made a great first impression on me — and perhaps on the rest of the market. Newly appointed director Susan Knight has bought 11,000 shares (coincidentally the same as Pablo E. Bruh’s Strawman holding) on market and at a near 52 week high.

Welcome aboard Susan. Take the wheel and steer this bad boy north!

Upgrading the Phone Plan

Cast your mind back to 2001. In Australia you could get yourself a Nokia 3310 that was pretty much guaranteed to be an upgrade of your previous mobile and had the added benefit of having Snake II. I’m sure Motorola had something equally popular at the time, at least in the more mature US mobile market. Nokia and Motorola were the market leaders for mobile phones back then. Nobody was sitting in boardroom at either of those companies thinking about new technology posing an existential threat to their businesses – they were the new technology. They weren’t to know that just ten years later in 2011 Apple would be selling more phones than Nokia.

Edwards Lifesciences’ Sapien and Medtronic’s Evolut, in 2025 these companies were your Nokia and Motorola. They worked, they dominated, and there was nothing else on the horizon. Combined, they own roughly 90% of a global TAVR market nudging $10 billion.

Into this almost cosy duopoly, two new entrants are now running pivotal randomised trials. Both use identical primary endpoints — the VARC-3 composite of all-cause mortality, all stroke, and cardiovascular rehospitalisation at one year. Both enrol approximately 1,000 patients in a 1:1 randomised design. Both have FDA IDE approval and CMS coverage. Both have started enrolling patients. From the outside, these products may look like twins, but they are not.

The first is Anteris, which brings to its PARADIGM pivotal trial its biomimetic edge – with its single-piece DurAVR valve whose shape may be responsible for delivering laminar flow, measurable left ventricle mass regression, and haemodynamics in the patient comparable to their pre-disease states. If this is confirmed, then it is a game-changing product – not just incremental improvement, but something akin to the iPhone.

The second is MiRus, which brings to its STAR pivotal trial for its (and now effectively Boston Scientific’s, following their acquisition of a third of the company for approximately $1.5 billion USD) Siegel valve a different focus. Its literal strength is enabled by its nickel-free rhenium alloys, a strength with allows a smaller sheath and a smaller 8-French catheter (compared to Anteris’ 14Fr).

This is an engineering story which promises less vascular trauma, potentially lower pacemaker rates, and the possibility of smaller and more frail patients. That’s the delivery system and stent, the valve is still a fairly conventional three leaflet design. To finally overstretch this phone analogy, it’s like an early Samsung Galaxy – beautifully engineered, but more of an improvement to the existing product category rather than paradigm-shifting innovation.

However, MiRus has perhaps one more edge, that of Dr Martin B Leon. Leon joined Anteris' Global Medical Advisory Board in July 2022. More recently (in June 2025) he co-presented a three-part sponsored webinar series making the affirmative scientific case that laminar flow restoration and LV mass regression are exactly the clinical endpoints the TAVR field should care about. The link to the videos remains on Anteris’ website (https://anteristech.com/news/studying-the-clinical-impact-of-restoring-native-flow-with-biomimetic-DurAVR-THV.html).

That he has turned up in April 2026 as co-chair of the STAR trial gave me some momentary pause. Does that mean that he is necessarily no longer on team DurAVR at all? But I don’t think it works like that with these guys. Their loyalty is to their patient outcomes, the progress of technology, and to the science – and less to whoever may have sent some consulting fees their way the previous financial year.

Probably, he’s just like the rest of us when we are upgrading our phone – we will just go with whatever makes sense to us at the time. It’s always going to be with something new and improved, and often whether you like iPhones or not just comes down to preference.

Capital on Tap

This is probably the best (and most orderly) way I’ve seen Anteris raise capital yet:

$250 million USD agreement with investment bank TD Cowen. There’s no immediate need for capital (following the recent raise), but there are a number of good points to this that I can see:

- It goes some way to future-proof Anteris upon completion of the pivotal trial when negotiating scaling up.

- Makes us less dependant on Medtronic at that time. Any move in that direction helps keep the path open for a proper bidding war.

- Minimises dilution at low prices. On current prices I see a maximum dilution of 25% (my valuation accounts for a 50% dilution over next 6 years).

- May smooth out volatility — Anteris is currently on a tear, up 68% the past month on volumes of over double the average on many days. Over 2 million shares exchanging hands on NASDAQ last night. Not that I’m complaining about the price going up. It’s just that I know the inevitable retracing can happen just as fast (or faster) and that scares away good institutions and creates opportunities for dodgier ones.

- There is a 3% commission which I don’t know enough about to know if that’s a good deal or not — but I imagine it’s just the cost of doing business.

Boston TAVI Party — BSX’s Shot in the Dark Heard Around the World

There is nothing like the spectre of an unforeseen event suddenly looming over your highly concentrated investment to chill the blood. I confess for a few moments this news stopped me cold and had me asking myself “What have I missed here?” like I was some miscalculating British general at Concord in 1775. In that second it was my own ticker skipping a beat.

Boston Scientific it seems — which by all rights should still be licking its wounds from its multi-hundred million dollar failed Acurate gamble — is back on the punt. This time it has staked some $1.5 billion USD on MiRus LLC. Thankfully, I reckon they have backed the wrong pony again.

I should just give up guessing whether the market will agree with me in the short-term. The market might in fact put itself though a prolonged bout of the Anteris cold sweats the likes of which I had briefly this morning. Fair enough too, because if my understanding is correct it’s a little bit counterintuitive.

Assuming I’m not just a highly incentivised Pollyanna Anteris optimist here (a big ‘if’ perhaps), then this is my take. Boston Scientific and Anteris might have taken to the same field on this occasion — but they are running completely different races. The one thing they have in common but is they are both chasing some of the $10 billion USD TAM of TAVR. BSX doesn’t really care how it gets it. It just needs its own product that it can get FDA approved — it will happily be an also-ran, it doesn’t care if it’s not the best.

Anteris is trying to prove it’s superiority with a next generation heart valve (think what the electric toothbrush is to the normal toothbrush).

BSX will be more than happy with the most minor of differentiated of products (think what the first rubber tongue scrapers in the back of the toothbrush is to the normal toothbrush). They need anything they can lawfully sell in the US, and then marketing can worry about the rest.

Long-term I think the upshot of this news is that Boston Scientific has just massively upped the ante on TAVR M&A for the next couple of years. On this deal they have paid $1.5 billion USD for 34%. On that valuation it takes a full $4.4 billion USD to get the whole thing — or about $6.5 billion AUD.

Anteris — arguably further ahead of the development curve than MiRus (which btw is running its own, but less ambitious than Anteris, Pivotal trial atm) — has a market cap of about $1 billion AUD. You might notice a sixfold increase in that would be in the Fenway ballpark of my Strawman valuation for Anteris.

For all we know Boston Scientific’s might have been one of Wayne Paterson’s low-ball offers that left the door open for Medtronic’s later 20% stake in Anteris. If that is the case then they have certainly paid for their mistake, and will pay further yet. But even better, I think they’ve inadvertently made sure that Medtronic — or whoever else is interested — is going to have to pay also. Couple of billion USD is now table stakes.

It may not be all rainbows ahead. I’ll concede that too much competition will eventually start to eat into the fat TAVR margins that reside in the $30,000 price tag of a spanking new aortic valve. However, that’s a problem for a distant future and this industry is far from being commoditised. Even if that does happen, I don’t think it will be DurAVR adopting the Jetstar business model — we’ll leave that to the others. We’ll be more like the Qantas Lounge, but like it was say 10 years ago, when it was still special.

Some decent momentum overnight on Anteris’ NASDAQ ticker (which is about 90% of the company’s valuation these days) on nothing specific that I can see. Also about twice the average volume. I expect ASX will follow on open which may see a 52 week high today here as well.

There is probably also some revised US price targets to come in the coming weeks as medtech analysts crunch their numbers.

Too Much Think + Maths = Make Brain Hurt

Trying to work out how many humans currently have a DuAVR is hard. It’s a bit like doing an escape room or scavenger hunt whilst simultaneously lodging your own tax return inclusive of applying post July 2027 CGT rules — and probably equally as pointless. The whole thing is almost certainly not good for you either.

I’ve just listened to a podcast published yesterday (but the interview appears to have been recorded last week), where CEO Wayne Paterson talks about the number being more than 200. He also said that just prior to the pivotal commencing that number was just north of 150.

The bulk of DurAVR implantation in between has been during the Paradigm trial. So approximately 50 patients, with the other 50 being randomised to standard of care. Which means that’s close to 10% of the 1200 patients done already and the US is only just getting started due to the CMS approval. Paterson went on to say that the study will be fully enrolled (read all patients implanted) by end of March 2027. Which means, the answer is…that by this time next year at least 750 people on this earth have a DurAVR in their heart.

The prospect of interim readouts has come up before in these discussions @mikebrisy, and it looks like we might now have an answer to that also:

Host: Is there an interim analysis on the pivotal study?

Paterson: No, it's such a quick study. Well, firstly, I think we've got so much data already that in a device, that doesn't change. It's not like the variability you get in the phase three or even a binary outcome.

When you've got this much data that we have on a device, you're within 1% of what the clinical trial is going to look like. And we've already been in clinical trials, including FDA studies, so controlled studies, of course. So interim analysis on a 12-month study is actually going to slow you down.

Interesting that he is thinking in terms of 12 months for what is a nearly 3 year pivotal trial — I think it shows that Paterson is saying the cat is out of the bag from the moment the last patient is off the table (and likely even before). I tend to agree. To industry insiders the skinny on this will be known long before the 12 month endpoints for each patient, and the share price re-rated accordingly.

Putting the Hard Miles in Milestones — Finally the First US Patients Treated in PARADIGM Trial

It’s more than just the Metric System that Europe has in its favour in the efficiency stakes these days. Some six months ago we had the announcement that the Paradigm trial was underway in Europe. Finally, the US has done the same:

So off to a slower start, although I will concede that the speed in which this happened from the date of CMS approval (less than a week) is impressive.

Hopefully these 5 patients implanted by the Montefiore Center in New York are just the start of some pent up demand.

It’s also heralded another Proactive Investor interview with Anteris CEO Wayne Paterson. As always I remain very sceptical about his very bullish (bluesky) estimates of the future TAM of TAVR (and I don’t use those in my valuations). But I have paid much more attention to how happy he seems about the post-operative patient data. That he was also happy with the randomised standard of care option here is, I think, indicative that it was one of the Edwards Sapien range. I wonder if this is going to be a common theme as the surgeons using Edwards are already demonstrating bias towards balloon expandable delivery — which DurAVR also has. Potentially good news as Medtronic Evolut is clinically superior to Sapien. Both, however, are considered standard of care.

Still no share price inflection/re-rate. I expect it this year. Upon information that enrolments are a quarter or halfway through perhaps. I can’t see the lid staying on this thing longer than that.

Never tell me the odds…

When a company makes a price sensitive announcement after the end of trading it’s an odds on chance that it is going to shift the price one way or another upon next opening. This one happens to be good news. However, there have been times I’ve held on too tight to Anteris in the past — and I’m kind of just enjoying taking a hands-off approach to the equity markets for the first time in a long time this year. It has shone through in the diminished quality of my research though, an example of which is as follows:

Pablo E. Bruh: In less than 50 words tell me how much of a big deal is Anteris securing CMS reimbursement for the Paradigm trial.

R2D2: It’s a very big deal. CMS reimbursement de-risks the PARADIGM trial Anteris, validates clinical credibility, lowers cost barriers, and signals a clearer path to U.S. adoption—materially boosting Anteris Technologies’ commercial prospects and investor confidence.

Pablo E. Bruh: On a scale of 1 to 10. 10 being highest. To nearest two decimal points.

R2D2: 9.20

Pablo E. Bruh: Explain your work…in less than 35 words.

R2D2: CMS backing for the PARADIGM trial Anteris reduces funding risk, validates evidence quality, and accelerates U.S. adoption pathways—major catalysts for Anteris Technologies, though not full approval (hence <10).

The NASDAQ tonight will show whether Wall St analysts feel the need to move on this quickly, or if they will just wait to see if it actually does cause the US trial centres to move faster. It can be hard to tell sometimes what is actual news and what is something these experts have already factored in.

As for me, I’ve already placed my bets a long, long time ago. I still think I’m on a winner, and this sort of news is always positive and thesis-affirming. It is just taking much longer to play out than I anticipated.

Office Space

Can this guy be serious? Did he really just say US $152,708.63 per month for office space? Maybe they put the decimal in the wrong space.

Oh well, a Minnesota commercial property expert I ain’t. This all seems in order, you do you Anteris and just make sure you call me if we get rich or go broke.

Done Deal

Price sensitive ASX announcements for Anteris are coming at me thick and fast this morning — faster than I can run all the PDFs through ChatGPT almost.

The gist of them is that the: public offering has closed; Medtronic is now confirmed as a cornerstone investor and will be the preferred partner for any later acquisition; and Anteris has raised $320 million USD for dilution of about just over 50%.

It still boggles my mind just how much can be done — and just how quickly it gets done — in the United States. The Paradigm trial is now fully funded. And the world’s second biggest TAVR player have been outed as DurAVR fanboys.

Links to ASX announcements for those interested:

CEO Paterson on Medtronic Deal

Concise interview with CEO Wayne Paterson discussing the most recent cap raise and Anteris’ future trajectory:

Struck Oil

A cheeky $200 million USD placement by massive competitor Medtronic wasn’t on my bingo card this morning — but I’ll take it.

Sit back and watch time.

Possible Omen of News

Something is brewing in the Nasdaq Anteris price tonight. At least a 20% jump on over 4X the average volume — all on no news.

Could be news leakage of first US Paradigm implantation? Who knows.

There might be an ASX spending ticket if we follow suit in trading today and no updates to the market.

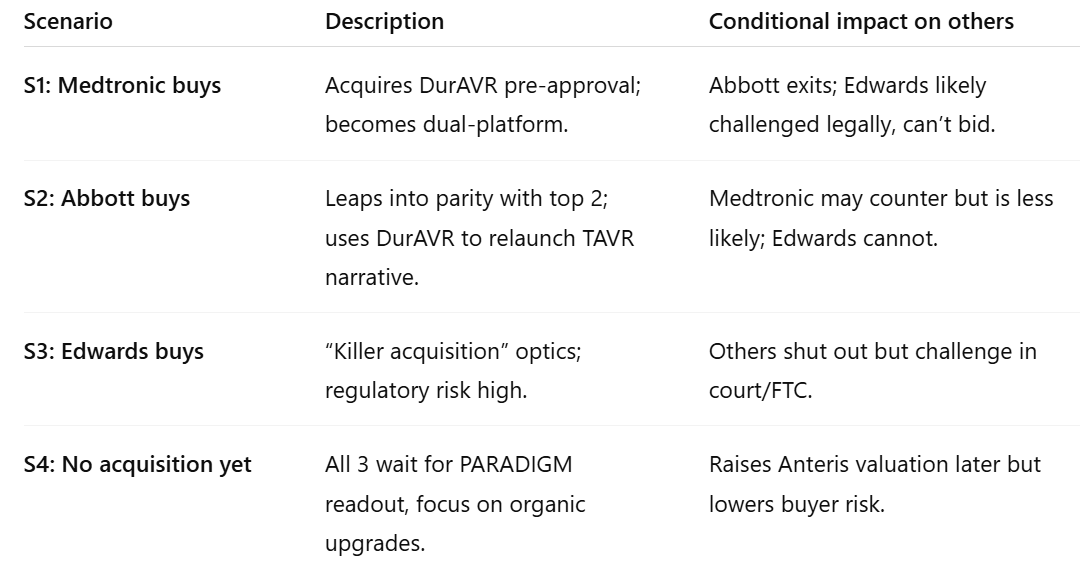

In an earlier exchange with @PabloEskyBruh I wrote that I considered the likelihood that $AVR get's taken out before the PARADIGM trial concludes as 30% to 50%.

Candidates are either the two market leaders, Edwards and Medtronic, or category "attacker" Abbott. Each have established products in the category. The first two stand to lose $ billions of value, if $AVR's DurAVR proves to be a superior product (so, M&A would be defensive), and for Abbott the acquisition would make sense as part of an "attacker" strategy. There are likely other acquirers in the next tier down, but I have ignored these for simplicity.

So, I framed the following question for my BA (ChatGPT5.0):

"Assess the probability that either Edwards, Medtronic or Abbott acquires Anteris in the next 12-18 months in order to get their hands on the DurAVR product?"

TLDR: My BA "thinks" there is a higher 45-60% likelihood than my original hunch of 30-50%.

Probabilites of acquition by actor are:

Edwards: 10-15% (anti-trust concerns)

Medtronic: 40-45%

Abbott: 30-35%

I've included the full response below - I've not summarised because it has some interesting insights and obvious limitations! I've removed all the references for ease of formatting.

Based on the patterns of M&A in medical devices, the likelihood of acquisition is highest before PARADIGM reports or FDA decides on approval, simply because the value of $AVR in that case would pop to a multi-billion dollar realm.

Now, in the first analysis, my BA has assumed the chances of $AVR remaining independent until FDA approval, as only 10-20%, assessed (erroneously) as the residual of the sum of the above three probabilities. This is flawed reasoning, because the events are not independent probabilities.

On challenging my BA, they've come back with a residual probability of $AVR remaining independent until FDA approval of 40-55%, or a 45-60% chance of $AVR being taken out. (I'm not entirely convinced by that analysis either, but directionally, it takes into account the co-dependencies.)

While still a bit higher than my 30-50% hunch, it seems that my BA and I are in strong agreement that there is a pretty good chance that $AVR gets taken out before FDA decision.

So What?

Obviously, each of the potential acquirers is very well plugged in to the cardiac market. So, my key next question is whether industry insiders can access privileged insights on the 1-year comparative performance stats. before the formal data is released to the market? I guess a surgeon will know first hand how their own patients are performing, but any one surgeon will only have a very small percentage of the 1000 candidates, and unless the relative advantages are large, you'd think they'd be unlikely to form a view with any confidence. But I guess that's just the point. If DurAVR is significantly better on key endpoints (like with the PPM metric reported yesterday) then, conceivably, the highest volume surgeons could get early insight.

But of course, there are communities and networks of specialists in every medical specialty, Cardiac surgeons are not different. So, is there any chance that a "consensus" view could emerge, informally, across a small group of leading cardiac surgeons who are sharing experiences?

I think the answer is quite possibly.

And of course the potential acquirers will have close relationships with their KOLs, and I have no doubt they will be obsessively seeking to glean any insights possible via these relationships.

So, I believe there is a credible mechanism for information to "diffuse" through the KOL community during PARADIGM, and for these insights to become available to potential acquirers.

This raises for me to an even greater importance the question, what is CEO Wayne's strategy for disclosing information to the market as the trial progresses? (Particularly because this isn't a blind trial!)

While this is all very interesting indeed, it sheds no light on whether DurAVR is a superior product! But it does indicate to me that if early signs show that PARADIGM is progressing well, that could up the likelihood of an M&A deal.

Of course, the market knows this too. And so therefore I expect that any positive newsflow from PARADIGM will potentially be a very poweful SP catalyst, because it will drive the speculative M&A valuations.

----------------------------------------------------------------------------------

The Full Assessment Follows

Let’s treat this like an M&A screen you’d build for a cardiology fund: (1) strategic fit, (2) timing/risk, (3) ability to pay, (4) antitrust. Then I’ll give you indicative probabilities.

Context we need in our head first:

- Anteris’ DurAVR THV is a balloon-expandable, single-piece, biomimetic transcatheter aortic valve that aims to behave like a native human aortic valve (large effective orifice area, very low gradients, laminar flow, minimal prosthesis–patient mismatch, low pacemaker rate). Early human data out to ~1 year show single-digit mean gradients (~8–9 mmHg), large EOA (~2.1 cm²), no valve-related CV mortality, and essentially no clinically relevant paravalvular leak in small annuli patients.

- PARADIGM, the global pivotal trial, has just begun enrolling and will compare DurAVR head-to-head with currently approved TAVR systems. First patients were recently treated and EU regulatory green light for trial sites has been granted in October 2025.

- TAVR is a ~US$6–7B global device market today and growing faster than surgical valves. Edwards has ~60–70% US share with SAPIEN. Medtronic is #2 globally with Evolut. Abbott is the would-be disruptor (Navitor / Portico heritage, ENVISION pivotal, etc.).

So DurAVR is showing best-in-class hemodynamics in anatomies (small annuli, low gradients) where current valves sometimes struggle, and Anteris is still pre-approval, i.e. pre-revenue, i.e. theoretically “buyable.”

We’ll do each buyer:

1. Edwards Lifesciences

Strategic fit

- Edwards is the incumbent leader in balloon-expandable TAVR (SAPIEN line).

- DurAVR is also balloon-expandable. From a portfolio lens, this can cut two ways:

- Pro: it could be a next-gen platform that resets durability/hemodynamics (laminar flow, native leaflet geometry) and protects the SAPIEN cash cow (~US$4B+ TAVR revenue in 2024).

- Con: it could also obsolete SAPIEN, forcing Edwards to swallow something that says publicly “your #1 franchise is inferior in small annuli, LV recovery, etc.” That’s not fatal (big strategics buy ‘cannibals’ all the time), but it raises integration/positioning questions.

Timing / regulatory posture

- Edwards is already in the US antitrust crosshairs. The FTC has challenged or scrutinised its efforts to acquire JenaValve (for pure aortic regurgitation) and JC Medical-style assets to dominate more anatomies.

- Buying Anteris now would look like the global #1 in TAVR buying an emerging competitor before US approval, i.e. classic “killer acquisition” optics. That is exactly the pattern US and EU regulators are now trying to block in medtech (esp. in high-concentration, high-ACV markets like TAVR). That creates serious deal friction.

Ability to pay / appetite

- Edwards absolutely has the balance sheet and strategic will to buy differentiated leaflet/tissue tech. They’ve historically paid up for pipeline (e.g. JenaValve).

- The prize here is “durability + low gradient = push TAVR down into younger, lower-risk patients.” That is the multibillion-dollar long-term TAM unlock. Edwards cares deeply about this.

Internal alternative?

- Edwards is already iterating SAPIEN (SAPIEN X4 etc.) with lower-profile delivery, coronary access, tissue enhancements, plus separate platforms for aortic regurgitation. They may believe they can close DurAVR’s hemodynamic gap in-house, or through JenaValve-style leaflet geometries.

Antitrust

- This is honestly the killer. Edwards + Anteris would be framed as the dominant incumbent removing a future challenger that has just entered its pivotal randomized head-to-head vs incumbent TAVR valves.

- Realistically, that’s the single hardest path to regulatory approval.

Edwards takeout probability (next ~12-18 months): Low (~10–15%)

- Rationale: Enormous strategic logic, but politically toxic. I would only put a real chance on this if Anteris data in PARADIGM suddenly show a step-change survival / LV remodelling benefit that makes DurAVR “existential,” forcing Edwards to fight the FTC in court anyway. Otherwise, Edwards is more likely to watch, copy, and litigate, not buy.

2. Medtronic

Strategic fit

- Medtronic’s Evolut line is self-expanding nitinol. That’s their identity and their clinical moat (large effective orifice area, good gradients in small annuli, low profile, supra-annular leaflet position). They pitch this as superior for many anatomies vs balloon-expandables.

- DurAVR is balloon-expandable and anatomically biomimetic. Two angles:

- It could give Medtronic immediate “we now have both platforms” credibility (self-expanding + balloon-expandable) so they can match Edwards SKU-for-SKU and attack niche anatomies where Evolut is less ideal (coronary access post-implant, certain leaflet calcification patterns, redo-TAVR).

- It also gives them a biomimetic leaflet story that neither SAPIEN nor Evolut can currently claim.

This is attractive. Medtronic does not currently have a best-in-class balloon-expandable valve. Buying Anteris would solve that overnight.

Timing / regulatory posture

- Medtronic is #2, not #1. Regulators are generally less aggressive about #2 buying a pre-revenue challenger to #1 than #1 buying that challenger. The acquisition could be framed as increasing competition with Edwards (Medtronic broadens its arsenal to challenge SAPIEN head-to-head in every anatomical class). That’s a friendlier antitrust story.

Ability to pay

- Medtronic’s Structural Heart & Aortic franchise is already a multi-billion-dollar platform and a strategic growth area.

- They have the scale, manufacturing, clinical, and reimbursement muscle to finish PARADIGM, run the FDA PMA process, and sell globally.

Cultural / integration factors

- Medtronic is comfortable buying pipeline-stage structural heart assets and incubating them through pivotal trials. This is part of their playbook historically.

- DurAVR’s messaging (laminar flow, LV reverse remodelling, zero/moderate PPM in small annuli, low gradients) mirrors Medtronic’s long-running “hemodynamics first” pitch for Evolut.

- In other words, Medtronic can credibly market DurAVR as “our next-gen balloon-expandable that keeps all our hemodynamic advantages and fixes the last remaining complaints.”

Strategic urgency

- There is some urgency. Edwards is trying to defend its balloon-expandable beachhead and is moving into new indications (e.g. pure AR, younger patients).

- If DurAVR can show superiority in PARADIGM, that would become a sales weapon against both SAPIEN and Evolut, especially in small annulus females and Asian anatomies (historically tricky).

- Medtronic cannot afford to let a third branded TAVR player with “biomimetic native-like leaflet” positioning carve out a new premium segment and start poaching high-value younger patients.

Antitrust

- Much cleaner than an Edwards bid. Regulators can be told: “We’re increasing competition by letting Medtronic go toe-to-toe with Edwards across all valve archetypes, rather than leaving Anteris capital-constrained.”

Medtronic takeout probability (next ~12-18 months): Moderate-to-High (~40–45%)

- Rationale: Best strategic fit, acceptable antitrust optics, obvious synergy (global sales channel, manufacturing scale, regulatory machine). Medtronic gains a differentiated balloon-expandable platform that could go after younger/lower-risk patients — the future profit pool.

3. Abbott

Strategic fit

- Abbott is trying to grow its Structural Heart business fast (MitraClip/repair, tricuspid repair, PFO closure, etc.), and is actively pushing into TAVR with Navitor (successor to Portico) and ongoing pivotal work to close the gap with Edwards and Medtronic.

- Abbott’s pitch to cardiologists is increasingly: “We are the broad structural heart partner across valves (mitral, tricuspid, aortic) and closure.”

- DurAVR would instantly upgrade Abbott’s aortic offering from “credible follower” to “arguably best hemodynamics in class,” with data already showing excellent gradients, EOA, and early LV mass regression.

- That is huge for Abbott. Instead of fighting for scraps in TAVR, they could leapfrog into a differentiated story.

Timing / regulatory posture

- Abbott is currently the #3 / aspiring entrant, not the incumbent. Regulators are generally welcoming of a stronger #3 because that should increase competition in a very concentrated duopoly.

- Buying Anteris would be framed as pro-competitive (“we’re challenging Edwards/Medtronic sooner, with higher-performance tech, rather than waiting 5+ years to build our own”). That’s attractive politically.

Ability to pay / execution risk

- Abbott can absolutely write the cheque. Structural Heart is already a multibillion-dollar growth engine for them.

- Where Abbott is arguably weaker vs Edwards/Medtronic is in super-high-volume aortic valve implant support infrastructure (proctors, training, field force for TAVR in every high-volume cath lab). They are building this, but it’s not yet at Edwards/Medtronic scale in TAVR specifically. So integration is non-trivial: Abbott would need to absorb Anteris’ program and also harmonise it with Navitor / their own in-flight trials.

Internal pipeline conflict

- Abbott already has Navitor in trials.

- Acquiring DurAVR risks signalling: “Our homegrown valve is not the future.” They could keep both — position Navitor as mid-risk workhorse, DurAVR as premium/young/low-gradient platform — but that’s complexity and potential write-down of sunk R&D.

Strategic urgency

- Very high. Abbott needs a wedge to prise open the Edwards/Medtronic duopoly. DurAVR is exactly the sort of clinical wedge (native-like leaflet geometry, laminar flow, potential LV mass regression, etc.)

- If Medtronic buys Anteris first, Abbott is locked out and condemned to be a distant #3 in a market that will define structural heart for the next decade.

Antitrust

- Easiest path of the three. Abbott + Anteris = more competition, not less.

Abbott takeout probability (next ~12-18 months): Moderate (~30–35%)

- Rationale: Immensely attractive strategically and far cleaner from a regulator point of view than Edwards. Slightly lower than Medtronic only because Abbott would have to reconcile DurAVR with its own active TAVR program and scale up TAVR commercial infrastructure fast, which is heavy lift (but doable).

4. Overall view / base case

- The “sale window” for Anteris is classically before pivotal data mature and before FDA approval, i.e. now to mid-pivotal. After DurAVR clears PARADIGM and files, Anteris’ standalone valuation balloons and becomes much more expensive. But buying too early means you (the acquirer) take pivotal / regulatory risk.

- PARADIGM has started and is designed as a head-to-head vs approved TAVR valves.Market Index+1 That is exactly the sort of pivotal data an acquirer wants to own and control, because a clean superiority or “no prosthesis–patient mismatch in small annuli” label claim would be commercial gold in women/small anatomy/Asian markets — a massive, durable niche.

Ranking the probability of an Anteris takeout in the next ~12–18 months:

Medtronic (~40–45%)

- Strategic bull case: adds a best-in-class balloon-expandable / biomimetic platform to pair with Evolut, strengthens Medtronic’s low-gradient / small annulus narrative, defends share against Edwards in younger/low-risk patients, and is antitrust-manageable.

Abbott (~30–35%)

- Strategic bull case: leapfrogs Abbott from follower to genuine contender with differentiated performance data, and regulators will view this as increasing competition. Execution risk is higher because Abbott’s current TAVR presence is smaller and they already have Navitor in the works.

Edwards (~10–15%)

- They absolutely appreciate the tech (this is their backyard), and they have shown willingness to buy pipeline valves.

- But right now the FTC/EU lens on Edwards buying emerging TAVR challengers is intense, and DurAVR directly threatens SAPIEN’s narrative, which complicates internal politics and public messaging.

Residual (~10–20%)

- That leftover probability is basically “no deal in that window,” i.e. Anteris stays independent through pivotal, raises more capital (including possibly via US listing/IPO process which they’ve already been exploring to fund trials), and then comes to market post–PMA with a far higher sticker price

Bottom line:

If you’re handicapping M&A, Medtronic is the most natural buyer, Abbott is the spoiler, and Edwards is the least likely in the near term mainly because of antitrust optics, not lack of technical interest.

But we are not finished yet!

This is a classic case of my BA applying flawed first order thinking. So, I have challenged in on the analysis as follows:

Challenge: "Your residual of 10-20% seems remarkably low. Can you critically assess that? For example, are the 3 probabilities truly indepedent. i.e., the probabilities will likely change if there is a first-mover attempt. Can you please reconsider the residual assessment?"

Excellent point — and you’re right: my earlier “residual 10–20%” implicitly assumed the three probabilities were independent (which they’re not) and that one of them must move in the next 12–18 months. In reality, the market and regulatory game theory make that much less certain. Let’s unpack this more rigorously.

1. Dependency and conditional probability structure

The three probabilities (Edwards, Medtronic, Abbott) are not independent:

- If one moves first, it changes the base rate for the others — not just because of scarcity (Anteris can only be bought once) but because the market response, regulatory posture, and competitive imperatives all shift.

- Conversely, if none move in the next 12–18 months, that outcome actually becomes self-reinforcing: Anteris continues de-risking via PARADIGM and the acquirers wait for more data, which raises the price later but reduces execution and antitrust risk. So a “no-deal-yet” scenario is not just possible — it’s rational.

Let’s reframe the space as mutually exclusive and collectively exhaustive outcomes for the next ~18 months:

These four scenarios must sum to 100%. The first three are mutually exclusive; S4 is the residual.

2. Corrected probability reasoning

If we model conditional dependencies:

- The prior probability that any of the three makes an acquisition attempt within 18 months (before pivotal data) is not additive; it’s limited by strategic window, deal readiness, and antitrust drag.

- The true aggregate probability of acquisition might sit more around 35–50%, not the 80–85% implied earlier.

So, re-estimating with conditional overlap and realistic timing:

3. Drivers that push the residual up or down

Pushes residual up (→ no deal yet):

- Regulatory uncertainty and FTC sensitivity to TAVR consolidation.

- Anteris raising equity on strong interim data (reducing need to sell early).

- Large strategics preferring to watch PARADIGM mature to mid-point (~2026) before paying a premium.

- Complexity integrating a small, early-stage team into a large regulatory machine mid-trial.

Pushes residual down (→ earlier takeout):

- Anteris publishes unambiguous superiority (lower gradient, larger EOA, better LV remodelling).

- Early FDA or EU Breakthrough designation accelerates competitive pressure.

- One strategic initiates due diligence, prompting others to move defensively (first-mover game).

- Private equity or sovereign funds push a pre-IPO valuation that tempts Anteris shareholders to exit.

4. Updated expected range

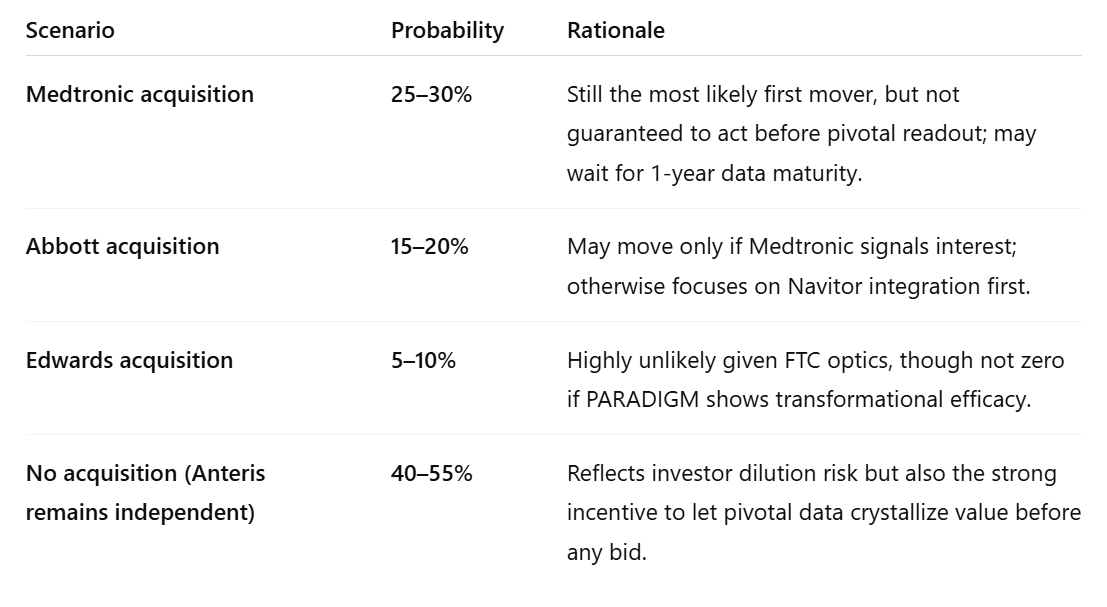

So, after incorporating dependency and timing effects, the residual (no-deal-yet) probability should be raised to roughly 40–55%, not 10–20%.

That implies a composite acquisition probability of roughly 45–60%, dominated by Medtronic (most logical fit) and Abbott (credible spoiler).

✅ Final calibrated view (12–18-month horizon):

- Medtronic: 25–30%

- Abbott: 15–20%

- Edwards: 5–10%

- No deal (Anteris continues solo through PARADIGM): ≈45–55%

In other words, it’s now slightly more probable than not that Anteris stays independent through pivotal completion — but if there is a deal, the conditional probability that Medtronic is the buyer jumps to well over 50% among the acquiring cohort.

Pablo E. Bruh’s Top 5 Reasons to Buy AVR

I’ll admit it. As I wallow in this lonely unventilated barn of stale, rotting, self-indulgent straws, I’ll concede that this ageing bull does tend to go on a bit about Anteris. For anyone new to it (or just morbidly curious) I’ve compiled this summary of my 5 main themes to spare you the unpleasantness of foraging in this bilge. For those patient (perhaps slightly concerned) more familiar readers, these are also the reasons I think Anteris is a less risky proposition now than when you first heard about it.

In any event I can feel this beast stamping in its stall and I think it will be busting out of here soon, so here goes:

- 1) The Pivotal Trial Catalyst — The PARADIGM pivotal trial has now commenced in Denmark. There will be a steady news flow of commencement in further European countries, as well as the USA and Canada to come. This is a necessary step to commerciality and fundamentally changes the value proposition of Anteris. The company’s confidence in its product (DurAVR) means the trial is a head-to-head study against industry juggernauts (and current TAVR leaders) Edwards Lifesciences and Medtronic.

- 2) A Differentiated Device — DurAVR isn’t a generic brand device trying to steal a piece of that market from those players — it’s a new class/generation. DurAVR is a balloon-expandable, biomimetic aortic valve designed to replicate native valve geometry and flow. Its superior haemodynamic performance and durability claims position it as a potential next-generation leader in the TAVR market. It’s IP protected and crucial steps ahead of any other contender.

- 3) Strengthened Operational Positioning — Recent board and executive appointments with U.S. med-tech expertise, along with new supplier agreements, media coverage, job advertisements, and regulatory progress, indicate that Anteris is building the commercial and reputational infrastructure needed for US and European market entry at scale. Read point 5, but know that — if it needs to — there is a strategy for Anteris to do this alone.

- 4) Improved Capital Structure and Funding Runway — This one I can’t stress enough. Anteris just raised $38 million AUD in a matter of days. That wasn’t happening a few years ago. And if there is one thing I have lived experience of it is Anteris and capital raises. There will be more just FYI. But if you are looking at just the cash burn on this, and it is scaring you away, I submit (respectfully) that you are looking at this the wrong way. Or that at least you should look at it in a holistic fashion by also looking at the TAVR TAM. Thats is where the asymmetry of this investment lies. Even just googling what one of these devices sells for will, I guarantee, surprise many. The corporate restructuring (ie NASDAQ re-domiciling and IPO) and recent capital raise have seriously reduced excessive dilution risk and provided a clearer financial runway for Anteris to execute the pivotal trial and beyond.

- 5.) Large Market and Strategic Optionality — The global TAVR and redo/valve-in-valve market is expanding rapidly, offering both high organic growth potential and the possibility of strategic acquisition (or partnership) by major med-tech companies seeking next-generation valve technologies. The TAM we are talking about is approaching $10 billion USD by the end of this trial.

Thanks for reading, and perhaps giving it a second thought. Feel free to tell me why I’m crazy in the comments, or to even add your own alternative valuation.

Investor Deck

There was a link to this investor deck in an SEC filing overnight which Anteris appears to have used in its latest capital raise.

No further details that I could see regarding interim readouts @mikebrisy. However, to the extent your question may have been about early share market realisation of value I have included the above slide. I’m still learning about ‘continued access revenue’ but my understanding so far is that certain (or all US centres) in the trial will be able to continue with implantation beyond the 1000 patients before the PMA. Anteris can still charge US $25,000 a device. My estimates of the margin of this is that it is still more than 50%, meaning Anteris has the potential to approach near commercial levels of sales before the PMA in the US.

The deck also does give a couple of anticipated milestones. Also a couple of diagrams for where the aortic stenosis and valve-in-valve components diverge, as well as differences between and FDA vs Europe CE mark.

Coming soon…

I couldn’t see Meg Ryan this time, but it is still promising lots of stars in the TAVR space. This holidays’ hottest accessory:

https://x.com/anteristech/status/1981058039240069315?s=46&t=9gCnoC2XgU49IFy4DjUAFg

Risky Disruptions

I was broadly aware of the issue, but although this article is a couple of months old it’s the first time I’ve waded into this level of detail:

https://www.medpagetoday.com/opinion/faustfiles/115367

I’m now prepared to consider the current FDA approval process as being it’s own independent risk.

No government agency is ever perfect. Realists understand that there are often going to be: tolerable and workable biases; occasional instances of regulatory capture; and manageable interferences of an ideological or political nature at the fringes. In the free and developed world those dynamics are general knowable and predictable. Where ultimately it’s the science that is still king.

Anteris’ strategy has been optimised to compete on that playing field with the goal posts set where they have been for the past couple of decades. I’m hopeful that they haven’t yet moved — or have moved negligibly. However, it would be naive to look at the current landscape of the executive branch of the US government and assume nothing has changed.

For example, Anteris’ use of US facilities and US labour helps from a tariff perspective — but within that ‘pro’ is the tacit acknowledgment of the ‘con’ of the volatility of commercial realities in the US. So too, that familiar notion that separate departments, and agencies in those departments, operate with autonomy within clearly defined boundaries, needs re-examination. Just a brief look at the news with respect the very separate areas of crypto regulation and the (albeit never uncontroversial) area of presidential pardons is enough to at least raise questions and for one to be guarded about the blurring of lines and beware of a potential lack of transparency in incentives.

In a similar vein — I’m taking little comfort that for the moment the changes are largely focused on Pharma and not Medtech. Because of that phrase ‘for the moment’.

So it’s a risk that that’s now on my radar as its own distinct ‘bogey’. Not a particularly actionable one at this point. In some respects it’s already baked into the margins of safety of my valuation by way of: expected dilution due to the length of the approval process; discount rate; conservative revenue projections; and low market sentiment metric (ie P/E). Still, it will be a factor in any updates to my valuation going forward.

In fact, I take some comfort in reading this in light of the apparent delays in Anteris obtaining IDE approval for an application lodged as early as February 2025. Since that time there have been other IDE approvals granted for other companies including those in the structural heart space (even some TAVR products). However, without knowing when those applications were submitted it’s impossible to draw any inference about any delay being specific to Anteris. But again — and perhaps this is the optimist in me — I’m encouraged to see that while the FDA may be slower, it certainly hasn’t ground to a halt.

Slow News Days…

I’ve been finding myself more impatient than usual for actual Anteris news and have been pondering why that is the case. Even allowing for the notion that the scheduled commencement of the pivotal trial is a critical milestone for Anteris, I’ve had more of a sense there there is a decision that I have to make somehow. The last meaningful announcement for Anteris was for its quarterly results published last month [ASX announcement 14/05/2025]. Even with their positive spin it’s hard not to read into it that both timeframes and costs are running beyond the best, or most optimistic, expectations of management. This — coupled with some helpful and poignant prompting from the Strawman community — has forced me to consider just what are the full implications of this news.

I’ve concluded that it’s not a thesis breaker, or at least not yet. But, I do have to concede that every delay — and every dilutive raising of capital — is a problem for my valuation. Too many of either could eventually damage my multi-bagger investment thesis. And without this being a multi-bagger then I’m just not interested. If I wanted smaller returns for my money I’d stick to the NASDAQ 100 rather than deal with the risk of a TAVR start-up.

I’ve been operating on the basis that the US IPO is a net-positive, in that it presents the optimal forum for future capital injection / partnerships / acquisition. However, I am not yet prepared for the opposite side of that coin: the confronting thought that I may, in fact, be dealing with an efficient market — that Anteris is actually priced correctly.

However, I’m also conscious that I’m straying into ‘over-thinking’ territory here. I do find it hard to accept that Anteris is actually only worth a couple of hundred mil more than its current cash position. For that reason I’ve decided it might be time for me to take some advice from Charlie Munger and that perhaps I’m at the the ‘sit-on-my-ass’ stage of this particular investment. The news will come and the chips will fall where they may, hopefully without taking my net worth with them.

I’ll revisit my valuation at the end of Q3 and see where I am at.

Potential longer-term TAVR disruptor

I find this type of thing spooky frankly:

https://www.medtechdive.com/news/bivacor-fda-breakthrough-titanium-total-artificial-heart/749506/

Obviously this particular device is being implanted during open-chest surgery and only in the sickest of patients — so not an immediate threat to TAVR. But it’s just another unique example that time in this industry does not stand still. Even best case scenario Anteris may only have a few years at the top of the heap whilst ongoing innovation whittles away its edge.

Goodspeed Anteris, my little wealth generation engine that could and still can. Go forth and make some bank. Some American Bank. Bring on the green days. I guess this is why Peter Lynch said to never fall in love with a stock…it just hurts so much when they leave :(

Patent Pended

This was never unregistered garage chiropractory, but it’s still good to see Anteris continuing to de-risk with the ASX announcement today that DurAVR has been granted a 20 year patent.

Less important than FDA approval, but dispels any doubt that mere imitation is still an option for the bigger players.

Hedge Dimensions

So Hedge Funds have now joined the growing list of things that I have realised — as I age — that I simultaneously: know too little about to understand properly; and, accept that life is just far too short to dedicate much time to rectifying this.

L1 Capital is a Hedge Fund. They are sometimes Long. They are sometimes Short. Anteris has just published an announcement on some data that gives insight into L1 Capital’s AVR Volume [ASX announcement]. Now I think that means — while I rack my brain for some year 8 algebra and trigonometry — if I can just go about rooting this whole thing cubicly I could then work out the Height and Depth. Then, whatever else I had, I would have some more numbers. One thing I do know is that getting rich involves numbers, Mamma didn’t raise no fools.

Now, some parts of Investopedia have just informed me that Long/Short Funds may actually be different to Hedge Funds. Too late of course. I’ve already found a picture I like for this post and we won’t be changing that I’m afraid. All knowing that information would achieve is that it would make me feel slightly less clever. Which, let’s face it, is what always happens when we are out here Dunning-Krugering ourselves silly.

L1 Capital first arrived on the Anteris scene in October 2021 when we were still getting over some of our more desperate days, finance-wise. We were still a bit crazy back then. Personally, I think the fact they are still hanging around is kinda sweet. Many others didn’t. Sure, they might get some pretty sick unlisted options occasionally but at least part of their strategy appears to be one of long-term accumulation. They currently comprise about 10% of Anteris’ share register.

Both that August to October 2021 capital raise I’ve referred to above — and last week’s placement (February 2023) — were brokered by Evolution Capital. I expect there may be another analyst report soon, but here is the link to Evolution Capital’s latest research on Anteris (November 2022).

There’s never harm in just that little bit more research …

** Edit 26/11/2021: Partly for balance, perspective, and a little bit just for fun, I am rebooting this Bear Case from circa February 2019.

But more importantly because it both explains some of the genesis of the tightness of Anteris’ share registry (a Phoenix rising from the burned ruins of the dreams of some ASX baggies like yours truly scooped up by sophisticated investors on the cheap) AND it demonstrates just how uncertain the new investment case was nearly 3 years ago, and, by extension, how much it has been de-risked already. Both those factors are relevant to understanding how the negative legacy of a company can lead to a present opportunity being undervalued. **

Dubious Track Record

Albert Einstein utilized a famous thought experiment to explain his theory of general relativity. It involves the different perspectives of a person travelling on a train versus that of another person (more accurately, another man, women not winning the right to watch trains from platforms until the late 1970s – in fact train-spotting remains a very gender-imbalanced past-time to this day) watching that same train from the platform [1]. I understand about 15% of this little allegory, and about a nanoparticle of a percent of the broader theory it seeks to explain. It is often said that if you can’t explain something simply then you don’t understand it. I don’t know what is said of those who don’t understand the simple explanations, other than that a deep gulf exists between the minds of the likes of Einstein and yours truly.

The reason I mention such an abstract topic is twofold. Firstly, the task of watching Admedus these days is like watching a slow-moving train wreck, unfortunately from inside one of the carriages…the third class one getting struck by the lightning…in the early days of steam engines when disastrous train crashes still happened with relative frequency and first aid was in its infancy. Admedus’s 4C quarterly released on 21/01/2019 and their response to the ASX query re the same [20/02/2019] are just the latest examples of this. Money is being spent like it’s the last days of Rome, for little result, and further capital raises are on the way to keep this thing afloat for reasons I can only chalk up to tradition.

Secondly, I do not understand the perspective of the two sophisticated investors who – from the safety of the platform – have seen what was unfolding on the tracks and hopped on the 5:00pm insolvency express anyway. What were they told to make this happen? Now representing close to 50% of the share registry I am morbidly curious as to why this was a good idea for them.

Probabilistically, it is just an example of wealthy people being capable of the same sort of mistakes your average mug ASX punter is prone to. Ideally, I am faintly hopeful that their unique perspective and access to boardrooms – which must be decked out with the most beautiful of mahogany supporting porcelain plates wielding danishes and other pastries of the topmost of notches – has informed their decisions to jump aboard. Time will tell which.

** Edit 11/02/2021: I first shared this in July 2018 however much of it is still relevant. I have now added more recent straws to Anteris and I think they should be read in the context of caution and scepticism I first described here. **

The very colour of the sky itself has been called into question in recent years by historians, linguists and psychologists [1] [2]. It turns out that our ancient forbears may not have been able see the colour blue and this could be the reason behind the Greek poet Homer’s description of the sea as being “wine-dark”, rather than blue. The theory suggests that only the ancient Egyptians, whose environment contained the correct pigments to make blue dye, could see the colour blue.

The sky has been blue since at least the 1900s however. This was when legislation was first enacted in some areas of the United States to curb the pitches some shady stock promotors made to struggling and gullible farmers [3]. The term ‘blue sky’ is now a part of the investment vernacular, used to describe risky investments that promise sky-high returns.

Admedus has had a complicated relationship with the concept of blue skies in this latter sense. Since first listing publicly in 2004 both the promotions of its many capital raisings and its organic following of retail investors have touted the idea that its immunotherapies division would take the company to these heights.

With this pipe-dream now firmly dispatched the temptation might be to see such potential elsewhere. In some ways TAVR presents a more natural fit for the company. Admedus’ foray into this field is based on its valve being created with its patented ADAPT tissue, and in some other ways any developments in this field may be more in Admedus’ wheelhouse than bringing a successful vaccine to market. However, much more work is required – or unpredictable events, such as partnerships, need to occur – before these developments begin to shift the fundamentals of this company and by extension justify a shift in the share price.

In the meantime I have created the separate straw (# TAVR Milestones) to track updates in this area, which Admedus refers to as a multi-billion dollar addressable market [4]. However, some healthy scepticism rarely goes astray and we may be better off taking a page from Homer’s book (or more accurately, that of his unknown scribe some centuries later) and turn a blind eye to blue skies.