Price History

Premium Content

Premium Content

Premium Content

I’m No Longer Sweating Over This One

Pharmaceutical company $BOT reported their 4C today, having now had their sole anti-Auxiliary Hyper-Hidrosis product on the US market for 11 months.

While I exited $BOT last year after their last 4C at $0.165, my exits are as often poor decisions as my buys, so I attended this morning’s call, and have also poured over the results. I thought it worthwhile writing up, as I observe that there are several long-suffering StrawPeople still holding on, who might therefore presumably be interested in the result and what I think about it.

First to their summary.

Their Highlights

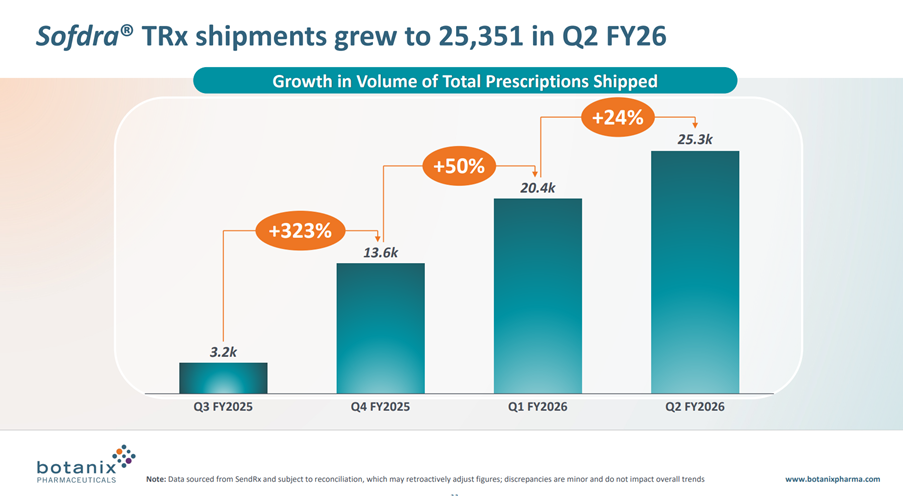

• Total prescriptions shipped grew 24% for the quarter from 20,418 in Q1 FY26 to 25,351 in Q2 FY26

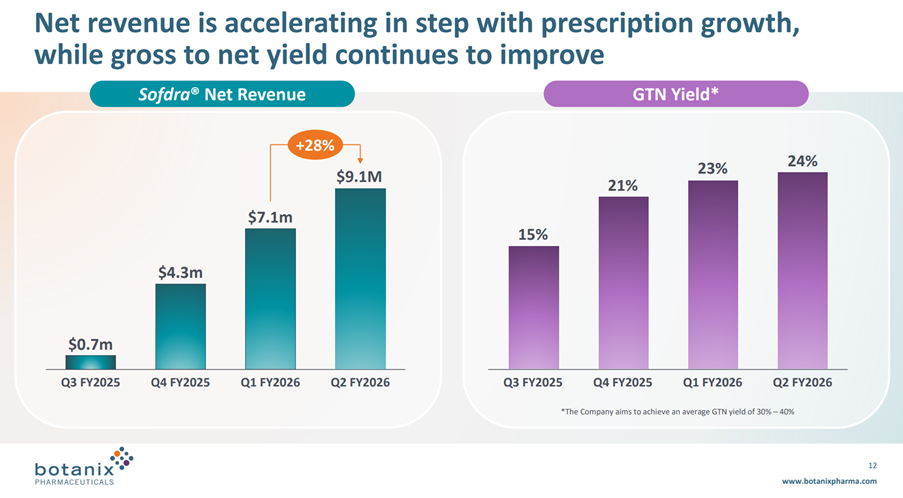

• Sofdra net revenue (unaudited) increased from $7.1 million in Q1 FY26 to $9.1 million in Q2 FY26, representing an increase of 28%

• Operating cash outflow increased from $13.1 million in Q1 FY26 to $17.2 million in Q2 FY26, primarily due to the addition of 23 sales professionals and associated one-time start-up costs

• Cash position of $31.5 million on 31 December 2025 and undrawn debt facility of $14.9 million

• New market research showed strong acceptance for Sofdra and SendRx by healthcare professionals, with 90% expecting to increase Sofdra prescribing volume in the next six months

• 50 sales professionals are currently active; new hires and existing sales professionals are highly productive and performing as expected

My Assessment

In a word … underwhelming.

Total Scripts

While total TRx shipped in the quarter was up 24% (that’s a CAGR of +136%), as you can calculate from the graph below, the absolute increase in scripts shipped was +4.9k compared with +6.8k in the prior quarter. This, despite the quarter seeing benefit of the salesforce expansion from the initial 27 Reps, now up to 50 Reps. In fact, this final quarter had the benefit of the expanded workforce for the entire period – albeit, it takes some time for new Reps to get traction with their accounts.

What does this mean? Well, it means that in the 4th quarter in the market we are not in an accelerating growth phase, but at best a linear growth phase, and potentially a declining rate of growth phase. So I am at complete odds with management who use the language “Net Revenue is Accelerating”. I’ll come back to that later.

To give a flavour of how far TRx are falling below the model I updated after Q425, the actual TRx delivered have been 20.4k (Q1) and 25.3k(Q2), whereas my model has 26.6k(Q1) and 42.3k(Q3), so you can see a big gap opening up.

But why, I hear you say, should anyone care what my model says? Well, the reason I care is that it reflects a typical s-curve for a product that reaches peak sales in 3-4 years, shows some of the expected properties of penetrating the prescriber base, and scripts per prescriber and importantly, is the trajectory needed for $BOT to become reasonably profitable in FY27 and not to run out of cash! More on this last point later.

Management said lots of encouraging things on the call in terms of sales force performance, and prescriber intentions. However, prior information about the number of prescribers (from which we can calculated scripts per prescriber per month) have been removed from this report, which is a loss of transparency from my perspective.

(Now, I have to say that it is completely normal for management to not give the level of detail we were provided in the first few reports on an ongoing basis. But they were being given then so that they would establish trends of strong growth, and I believe we’ve now seen the removal of that level of detail because the positive signs have gone. That’s just my hunch, and I have no other reason to base it on.)

Bottom line: last Q I was open to the possibility that we could still be on an accelerating growth trajectory, and that I might have hit the "ejector seat" prematurely. Today’s result confirms my bearish perspective.

Revenue

Net Revenue grew 28% from the last Q, driven both by the increasing TRx and a modest increase in GTN from 23% to 24%. See graph below.

As I mentioned before, I don’t like the language of “Net revenue is accelerating”, because the increase in Net Revenue each quarter has followed the sequence: +$3.6m, +$2.8m, +$2.0m despite i) early prescribers gaining experience, ii) coverage of prescribers increasing and iii) the sales force almost doubling over the year.

I fear we will see the revenue growth curve starting to flatten long before the cost base is covered. I think this is the key risk that anyone holding onto this stock needs to assess and satisfy themselves about.

On GTN, management continue to aim to develop GTN to a range of 30-40%. Again, the GTN progression looks to be flattening off, and so I wonder if it can ever make 30%.

Costs

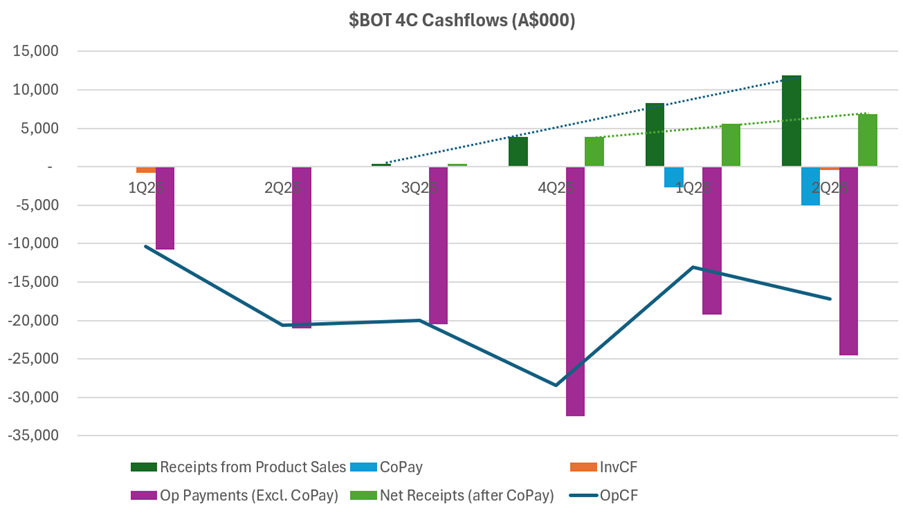

Turning now to costs, I want to examine these in the context of operating cash flows. The chart below, which I’ve pulled from today’s and historical 4C’s needs some explaining.

What I like about this picture is that it puts the revenue progression into the context of the relatively large cost base this business has. Any positive trend in OpCF in the last 4 quarters is weak, and there is a significant gap to close.

So with $31m cash remaining, management were asked in the Q&A if they have enough cash to get to cashflow breakeven. The CFO took on the question, and didn’t really answer it. The best I could pull from the rambling response, is that there is enough cash “for the short term”.

To be clear, with a cash burn in the Q of $18m, I’m pretty sure these guys are going to have to raise capital before the end of CY 2026. Why do I say that?

On cash receipts, you can see in the chart the trend (dark dotted line) in what I call “Receipts from Product Sales.” Looks pretty decent, doesn’t.

The problem, is you have to net off the light blue bars, which are essentially the CoPay made to customers (part of the why the GTN is so low).

This means that net receipts from product sales is shown by the light green bar, and the trend over the last 3 Q is shown by the light green dotted line. So, in the context of the operating cost base – the purple bars – this is pretty anaemic operating levage.

If – and it’s a big if – SOFDRA can maintain linear revenue growth for two more years, it is plausible that receipts might cover operating costs. I'm not sure they've got the cash to get there.

I was also bothered about the CFOs remarks about product manufacturing costs. Over the last two quarters, $BOT has had sufficiently inventory in place – not only of finished good, but importantly of the costly API (Active Pharmaceutical Ingredient), so that manufacturing costs have been artificially low. Management made clear that in the Q3 they will have to buy more API, so that will be a increase in cash outflows. But what bothered me was that the CFO then said that in following quarters these costs would return to more normal levels. Wow! As if buying API isn’t a core and ongoing part of manufacturing operations. (I nearly fell off my chair.)

I know I am sounding very negative here. It is possible that with good cost control and continuing increasing sales, that the picture above will evolve and improve significantly with each successive quarter, such that in 12 months’ time we could be looking at a much healthier picture. However, from where we stand today, given that the rate of sales growth may decline into Year 2, and with a relatively high operating cost base locked in, I believe there is a high likelihood that:

1) Capital will need to be raised in late calendar 2026 or early 2027 and

2) Profitability will not be achieved until FY27 at earliest, and could be significantly later.

Management Commentary

I’m not going to comment further on what management said, partly because the narrative isn’t really the story that I think the data tells. And frankly, I don’t have any more time to spend on this.

Overall, Vince and Howie seem to be putting a brave face on things, and telling as positive a story as they can without saying anything that is factually misleading. (That is my subjective opinion and impression, rather than something I can factually defend.)

Valuation

According to tradingview.com, analysts have valuations of $BOT with an average TP of $0.775 ($0.24, $2.00, n=4).

I fundamentally disagree. So, what’s my view?

That’s harder to call, and I can't put a number of this one.

As the need for dilution becomes clear, the SP can be expect to fall further. So there is a risk of an unknown level of dilution in the next 1-2 years, and a lot of uncertainty (in my view) as to when a profit might be achieved, if ever. And that’s because, despite impressive q-o-q growth, from my perspective, I can’t see the path to profitability with any confidence.

Why is this? From everything I can tell, $BOT are doing a good job on sales and marketing execution. It's just I am not sure the product is that great, given its cost which is significant. It is also unclear to me what the changes in the Afforable Care Act are going to have on persistency as well as new scripts. Some of the increases in insurance premiums being faced by middle income Americans are pretty scarey, and there are anedoctal reports in the press of people going uninsured. To the uninsured, middle income American, is Sofdra a treatment there are going to pay up for? Interestingly, this was not discussed on the call. Only one question on "impact of tarriffs" ... go figure.

Maybe all of this will change in the next couple of reports. Heaven knows I've been badly wrong on $BOT in that past. But for me, the sidelines is the place to be.

Disc: Not held

While several of us in the community are still traumatised by the June "Nightmare on ..." it is worth bracing ourselves for what I expect to be a $BOT Trading Update next week, ahead of the 4C towards the end of the month.

@jcmleng covered the August Canaccord Genuity Conference, and I thought as part of my own preparation, I'd share some extracts from the Canaccord Genuity Analyst Report following that conference (published 1 September 2025, but I've only read it today).

While the presentation gave no new disclosures, which was also the case at the more recent Wainwright Investment Conference (in early September), there was a "fireside chat" format, and so some insights were gleaned from that, which I've highlighted in bold below.

TLDR: I am reasonably aligned with CG. Their valuation of $0.27 compares with mine of $0.35, and I believe the depressed SP at the moment reflects a loss of trust, so that void left by shareholders who fled with their "night terrors" was not been replaced with new believers. If the next update is half decent on scripts, GTN, and revenue, that could be a significant step towards rehabilitation.

Extracts from Canaccord Genity Report (1/9/25)

Summary

"We maintain our BUY rating and $0.27 PT on Botanix Pharmaceuticals. BOT remains in a holding pattern as investors wait to re-establish trust with the expectations around Sofdra traction, particularly as it relates to script volume and gross-to-net yield improvements. We would caution investors not to place too much focus on single data points, however. Our fireside chat with management at Canaccord Genuity's 45th Annual Boston Growth Conference suggested to us that the 30 sales reps now in field are continuing to convert patients at the expected rate. We have therefore maintained our script volume growth and assess the ability for Botanix to meet these numbers as reasonable. There are calculable reasons as to why the gross-to-net yield can sit at ~25-30% within a ~18-month time frame; we have moderated this over FY26e and FY27e to 26-32% (from 29-33%) to reflect this. We view revenue expectations being met through either volume growth or gross-to-net improvement as alternate commercial strategies, rather than preferring either one - with the caveat that we expect profitability to rema intact for 2Q27e. We, and the market, keenly await a trading update in October."

"FY25 summary. Revenue: Total revenue of A$5.8m was largely pre-reported, noting ~A $5.0m directly relates to sales of Sofdra in the US (the remaining attributed to royalties from Ecclock sales in Japan). Sofdra sales reflected ~16,689 total prescriptions (TRx) sold since Jan-25. At a gross price of ~A$1,500 per script (per month), gross revenue sits at A$25.2m, reflecting ~20% average gross-to-net yield across the period. OpEx and earnings: Total OpEx of A$94.1m was 10% ahead of forecasts (CGe: A$85.6m), noting cash OpEx (excl. SBPs) of A$73.5m was only ~4.9% ahead of forecasts (CGe: A$70.8m). Loss from operations therefore sat at A$86.4m (CGe: A$83.4m, -3.5%). Cashflow: operating cash outflow of A$78.6m was driven by a large WC outflow for inventory build (~A$27m) as well as inflows related to R&D tax incentive (A$1.5m) and interest income (A$1.9m) sitting ~$4m ahead of forecasts (CGe: A$82.6m outflow). As reported in the 4C, Botanix closed FY25 with $65.0m in cash, having raised $40m in equity in April-25 and established a US$30m (A$48m) debt facility with Kreos Capital, of which A$31m was drawn down."

"Forecasts and outlook. Our main model adjustments include: a) moderating GTN yield in FY26e from 29% to 26% (A$6m topline), b) adjusting expenses, accounting for a larger SBP expense, c) inventory (noting no inventory build is expected in 1H26e), d) removal of additional debt drawdown. We see the next two quarters as paramount to Botanix reestablishing trust with the market. We expect Botanix to provide a 1Q trading update in Oct-25. For context, we forecast 1H26e net revenue of A$23.2m. The A$23.2m is predicated on two factors: 1) on the basis that June-July growth is the same as May-June growth (~21%); we forecast ~14% MoM growth in script volumes is required to reach our 1H26e number which needs to be coupled with... 2) an improvement in gross-to-net yield. As a reminder, as of June, GTN yield sat at 23%; we need to see GTN head ≥26% (remember 2H of a CY is a stronger GTN period). "

"Valuation. Our diluted 12-month price target of $0.27 is informed by our DCF model (WACC: 10.3%, Tg: 2.5%) and cross-checked against ASX-listed and global comps (median FY+1 EV/Rev: 3.2x), as well as dermatology deal values (median EV/Rev multiple: 3.4x), which sits broadly in line (4.0x) based on FY27e CGe net revenue: A$140m. More importantly, across the forecast period (FY26-FY28e), we believe Botanix has the capacity to build into a peer comparable EV/EBITDA multiple of 8.0-11.0x, with our PT in line with FY28e EV/EBITDA at 7.5x."

My Assessment

Who knows what 1Q revenue will look like, as multiple factors are at play:

1) seasonality (+ or -)

2) evolution of GTN (+)

3) maturing market penetration (-) and

4) expanding sales force and territories (+)

5) increasing prescriber experience in prescribing ... initial cohort entering their second 6-month period. (likely + but could be -)

Revenue is the key unknown, because costs are controllable and management have demonstrated that they know they have to show an improved control of expenses.

I think the CG numbers above are a good reference to check 1Q against. They could be a little bullish, because of the delay in getting new reps up to speed, but as I've shown above that is only one of several factors.

In my assessment, there is a significant margin of safety between today's SP and any reasonable valuation on fundamentals. The discount is really a management credibility one, and as CG state, $BOT will need two solid quarters of execution to start to repair that.

When we get the next management briefing, I will be very interested to hear about the prescribing behaviour in the more established accounts. How that trends will be an important indicator of where we end up in terms of revenue plateau.

At the start of the year, I followed the Chairman by selling 25% of my RL holding at $0.465 (and sold some in SM too). At the time, I feared I was being a wally, given my valuation at the time. But I was unnerved by Vince's sale. It turns out that was a good decision (for Vince and me!)

But in recent weeks, when the SP hit $0.125, I bought those shares back in RL (and also added again in SM) because things would have to go really badly for the business to have that value. Unfortunately, in that case I was on my own with the Directors and Insiders not sharing my enthusiasm.

Management have been very tight-lipped during the last Q. Maybe they were rightly beaten up for all the loose talk early in the year about revenue expectations for FY26, and perhaps the Board resolved "Shut the f*** up and let the results do the talking."

Well, not long until we see what the revenue trajectory is looking like.

(I have to remind myself that I'm sweating more not because I need the product, but because its just warming up in QLD as we head towards the Summer.)

Disc: Held in RL and SM

In this Straw I set out details of the valuation I posted last night. I know Monday's webinar may well quickly date what I write here. However, it is a line in the sand because it sets out the basis for why I continue to HOLD $BOT. And that was a decision I needed to take today. If Monday brings new information, so be it.

SUMMARY

This Straw presents a valuation analysis of Botanix Pharmaceuticals ($BOT) based on the first six months of SOFDRA sales. Using updated data from the 8th July 2025 company webinar (The “Nightmare on Hyperhidrosis Street”), I built a scenario-based revenue model projecting to FY28 and applied forward P/E multiples to derive a valuation discounted to FY25.

Key components of the model include:

- Market Penetration: Three uptake scenarios (70%, 85%, 100%) based on prescribing dermatologist adoption over 24 months, with consideration of potential GP involvement and expansion of the specialist base over time.

- Refill Dynamics: Volume driven by average new scripts per prescriber and monthly patient churn. Churn is conservatively set at 18.5%, with sensitivities at 16% and 20%.

- Gross-to-Net Revenue: Gross sales per refill is AUD 1,500. A gross-to-net (GTN) ratio of 32% is assumed on average, reflecting early-year deductible effects and expected improvements in reimbursement management.

- Cost Structure:

- Sales & Marketing: Based on sales force headcount and dermatology industry benchmarks (AUD 462k per rep), with sensitivities up to AUD 20 million additional spend.

- COGS: Assumed at 7% of gross refill revenue.

- Other Expenses: Adjusted from the FY25 interim results, net of sales and marketing.

Twelve scenarios are modelled, combining varying assumptions for prescriber activity, churn, GTN, and S&M cost. The base case (P/E = 25) yields a valuation range of $0.22–$0.90, with a central (p50) estimate of $0.35. Even in worst-case scenarios, valuations remain above the current share price of $0.16- $0.18.

Using an alternative methd of applying an M&A revenue multiple of 5x FY28 revenues and discounting back yields valuations of $0.24 to $0.42. (Average is $0.33)

I conclude that despite recent market pessimism, SOFDRA retains strong risk-reward potential, and management has a reasonable timeframe to demonstrate longer-term value generation through platform exploitation and licensing.

INTRODUCTION

My basic approach is to model scenarios for revenue to the end of FY28, estimate the NPAT at that stage and apply a range of P/E ratios at that point, discounting back to end of FY25.

Revenues are driven off modelling total refills per month, using the detailed monthly history provided in the “The Webinar” (aka “Nightmare on Hyperhidrosis Street”, 8th July).

The structure of the analysis is as follows:

1. The Revenue Model

1.1 Market Penetration

1.2 Refill Volumes

1.3 Average Number of Scripts Per Subscriber Per Month

1.4 Patient Churn

1.5 Gross to Net

1.6 So What Revenue Do I Expect

2. The Rest of the Financials – A “Ball Park” Estimate

2.1 Sales & Marketing Expense

2.2 COGS

2.3 Expenses

2.4 Getting to NPAT and EPS

3. Valuation

4. Model Outputs Discussion

4.1 Discussion

4.2 M&A Valuation

5. “A Nightmare on Hyperhidrosis Street 2 – The Revenge of the Applicator”

6. So, What About My Thesis?

------------------------------------------------------------------------------------------------------------

1. The Revenue Model

1.1 Market Penetration

The market is large with some 3.7m seeking treatment in a Dermatologists office out of an estimated market potential of 10m.

The key volume drivers are therefore:

· How many dermatologists (Derms.) are prescribing Sofdra

· Number of new scripts written per month

· How many refills each patient gets

We know there are around 4,000-5,000 Derms. who see patients with PAHh and will therefore assume 4,500 as 100% of the prescribing base.

The market penetration scenario assumptions are:

· Maximum penetration achieved over 24 months

· Penetrations of 70%, 85% and 100% modelled.

This is justified because very rapid penetration (51%) was achieved inless than 6 months. However, ultimate penetrations of 70%, 85% and 100% might at first glance appear unreasonably high. However, there are three further factors to consider:

First, the actual Derm base is 10,000-12,000, so if the product gains market acceptance, there is the possibility that the specialist prescribing base expands.

Second, the experience for the other anticholinergic in the market (Qbrexa) is that over time, some GPs will prescribe refills, or potentially write a script for a patient who has tried the drug but them come off it (for example, at first they couldn’t get the health fund to pay). Apparently, this has been written as acceptable by some health funds (Note: verification of this is required.)

Finally, the upside case (100% of 4,500) also allows for the potential that there are actually 5,000 prescribing dermatologists to begin with.

In short, while 100% penetration is unlikely, there is the potential for the prescriber base to grow over time.

A peak in number of prescribers is assumed to occur in 24 months from launch. The three modelled uptake scenarios are shown below. These scenarios are consistent with the observed fact that in the US dermatology treatments tend to reach plateau sales in the 3rd year.

Exhibit 1: Modelled Prescriber Uptake Scenarios

1.2 Refill volumes

Scenarios are generated for the number of refills issued by month. The assumptions in this model are:

· Existing patients obtain refills, subject to a Monthly Churn Rate (% Churn).

· Active Monthly Prescibers write “n” Scripts per Month

From this simple model, the number of refills in any month is simply:

TRx(n) = Total (Re)fills issued in Month “n” = TRx(n-1) . [1 - % Churn] + NRx(n)

where

NRx(n) = number of new scripts (i.e. new patients, including returning patients) written in the month.

In turn we can find NRx(n) from the Total Number of Prescribers (n) x # Scripts per Subscriber Per month.

So, we have two key variables we now have to understand:

· Number of new Scripts written on average per Prescriber

· % Monthly Churn.

I’ll next look at each of these in turn.

1.3 Average Number of Scripts Per Subscriber Per Month

Here we turn to the data from the first 6 months from The “Webinar”, and perform the analysis shown in Exhibit 2 below:

Exhibit 2: Model Calibration – New Scripts and Churn

Source: The figures in blue are from the “Webinar”.

I’ve estimated the New Scripts in each month (the Churn model is described in the next section). From this, we can calculate how many new scripts were written per Prescriber in each month.

Interestingly, the number started very high, which indicates that early prescribers might have already “warmed up” by having been engaged over the prior 3-6 months as part of the Patient Experience Program. In any event, $BOT presumably had a kernel of super-prescribers and KOLs ready to go at launch.

In previous Straws, we’ve also spoken on this forum about whether a potential “bolus effect” exists. The would be from highly motivated patients aware of the products approval and actively seeking it after launch.

So, the rapid fall-off in the Average Number of Scripts per Prescriber per Month is unsurprising. In fact, we expect it.

A source of error in this analysis is the Churn model leading to an estimate of the number of patient “Lapsing” each month. I’ve played around with different “% Churn" values, and the overall observation is robust.

Scripts per Prescriber per month falls rapidly over the first 6 months, although appear to be levelling off. This is reasonable if the initial population of "super-prescribers" gets diluted by the more general population and/or if the “bolus” effect dissipates rapidly in the early months after launch.

Now, the key question is how this number changes over time.

There is evidence from other drug launched in dermatology, that indicates that the prescribers initially prescribe at a low level, and that this grows by 2-3x over the next 12 months.

Whether this proves to be the case for SOFDRA is one of the big value drivers and uncertainties. At this stage it is unknown.

Note also that I am ignoring the prevalence of the condition at this stage. It doesn’t matter, because the results of the model represent a very low proportion of the prevalent population, so Sofdra will not be limited by the number of patients seeking treatment.

Conservatively, I have generated the following 3 scenarios, which I hold as independent to the number of prescribers:

Exhibit 3: Scenarios for New Scripts Per Subscriber Per Month

I have clearly excluded the scenario that the product “flops”, and clinicians reduce their prescribing over time. This scenario cannot be ruled out, and could occur under two situations.

· Clinical Data doesn’t support continued use (for whatever reason)

· A superior treatment emerges.

I’ve ruled out the first case because of the clinical trial data published by the JAAD, but also the experience in Japan, which showed consistent growth over the first three years in the market. While the product is only partially effective, it appears to be well tolerated and delivers a sufficient benefit to be meaningful to a reasonable proportion of patients who try it.

At this stage, it is unclear whether a superior product will emerge in the near future.

Note: This sensitivity most significantly impacts the valuation.

1.4 % Monthly Churn

The Webinar covered a lot of information about adherence and number of refills. I’ve developed a basic monthly churn model, simply because it is the easiest way to fit the data provided for the first 6 months, and then to project forward.

If 18.5% of patients churn off the drug each month and don’t return, we get the following profile:

· 3.46 total fills from February to June (i.e.2.46 refills)

· Only 11% of patients remain at the end of the first year

· 4.94 fills over the first year

The first point fits the data presented by Howie in the webinar.

On the second point, no-one knows how many patients will come back for another script at the start of the second year. However, 11% seems a conservative approach. Perhaps more will if a significant proportion of reimbursed patients perceive value from the product. So, there is a significant potential upside that I have not considered, as I am choosing a cautious approach in absence of data.

The % Monthly Churn model is flawed. For example, we know a proportion of patients are not going for auto-refills, and are maybe only trying 1 or 2 refills, before abandoning the treatment. However, I am basically comfortable with the model as a rough estimate, given that:

1. It predicts well the average number of refills for the February patients over a 5-month period

2. It aligns with managements enthusiasm that the product is performing well above the norms for dermatological products, which have of an average of 2 fills per patient (i.e., only 1 refill).

I will run two sensitivities on this parameter at % Churn levels of 16% and 20%, noting that at a 20% monthly churn, only 9% of patients are still using the product in the 12th month after first prescription.

This is an area of high uncertainty, and based on performance over the first 6 months and management’s statement about the February Scripts, there is a possible material upside risk to this factor. Rather than introduce further model complexities, this will be something to revisit over time.

1.5 Gross-To-Net (GTN)

$BOT appear to be achieving Gross Sales of AUD1,500 per refill. So with modelling the volume of scripts well-defined, the next big parameter is GTN, in order to achieve net revenue. Management believe they will ultimately achieve a GTN of 30% to 40%.

The exit rate for June was 23%, improving at about 2% per month. Given that Q1 and Q2 are the high deductible season, recovery to the mid-range seems likely.

Secondly, I expect management to tighten the copay policy in Year 2, and also for optimisation of Pre-authorisation of Scripts over time to improve GTN over time.

Analysis from studies of other drugs in sectors like derm. shows that Q1 and Q2 are typically hit by the high-deductible period, with stable revenues in Q3 and Q4,

I have therefore derived the following assumptions based on other studies (note: at this stage $BOT management haven’t said much about this):

· GTN continues to improve at 2% per month, reaching 35% by end of calendar 2025.

· Thereafter, every year, there is a Q1 hit to 72.5% of the Q4 value, and in Q2 88% of the Q4 value, with full recovery by Q3.

We don’t yet know what the Q1 and Q2 annual deductible hits will be. However, the chosen values seem reasonable given experience elsewhere.

The net effect of the 35% assumption, and the annual resets lead to an average annual GTN of 32%. (Note: this is down from my original valuation of 50% - a bit hit to value!)

I have not run any scenarios or sensitivities on GTN. Who knows, perhaps average annual GTN is only 28% or maybe it is 36% - these are now relatively small uncertainties compared with others discussed here! So, I’ll settle with 32% as a reasonably conservative but not unduly pessimistic number. Exhibit 4 shows the GTN over time.

Exhibit 4 GTN over Time

This concludes the revenue model assumptions.

1.6 So What Revenues Do I Expect

According to my model, Sofdra will generate peak revenues of anywhere between $AUD137 and AU$240m by FY28 (or US$90m – US$160m).

That’s very materially down from upside cases I was projecting of anywhere from US$200m to US$600m only a few months ago. (Sad face emoji)

Of course, it is possible that in every assumption I’ve made in this model I’ve suffer from a negative bias induced by the “Nightmare …” and there are certainly upsides I’ve chosen not to consider, particularly around GTN optimisation and, more materially, increasing prescription rates over time.

But rather than “fudge” my model, I’ll run with what it's telling me and – if warranted over time – I'll make adjustments in the light of evidence.

2. THE REST OF THE FINANCIALS

With a high range of uncertainty around the revenue model, I have kept the rest of the financial modelling simple. I’ve also not spent any time trying to get a sensible number for FY25 simply because it is a transition year, with several non-recurring factors:

· Platform build

· Launch preparation

· Onboarding of Sales and Marketing Staff

· Launch inventory build

I want to emphasise this because I will not judge this model by how well it predicts the FY25 Full Year result. I’ve spent zero effort trying to do that because it has no bearing on the company value in the medium term - even though it may well drive the market.

The major uncertainty is the spend on Sales and Marketing. So my approach here, is to take the Expenses from the 1H FY25 Accounts, back out the Sales and Marketing element, and build a simple sales and marketing cost model.

2.1 Sales and Marketing Expense

I will estimate the total Sales and Marketing Expense as follows:

S&M Expense = Sales Force Headcount x Benchmark value

This is a crude but well-established method in pharma to derive total S&M Expense from the size of the field force, with the benchmark picking up all related and overhead costs.

Reasonable benchmarks in Dermatology are anywhere from $USD 300 k per FTE to $500 k per FTE, which turns into AUD 462 k to AUD 770 k.

We know that $BOT have hired an “A” team of derma industry veterans. And “first product” businesses usually pay over the odds. This will be offset by the fact that some of the expenses covered by the benchmark are already “hidden” in other lines of the Accounts – given the AASB/IRFS model applied in Australia.

Therefore, the approach to be followed is as follows:

· Assume AUD 462 k per FTE

· Run high case sensitivities of AUD$10m, $15m, and $20m (for a 50 strong field force, these sensitivities are equivalent to AUD200k, 300k and 400k per head – so they should cover the potential outcomes).

These sensitivities are also important because we don’t know how much digital marketing spend has been thrown at the business.

Most of the platform build will be included in the 1H FY25 accounts, So we don’t need to worry about that. However, it is clear to me from the Webinar that $BOT are not yet spending big on digital marketing, and as I’ve written previously, that they are seeing the highest ROI on investing in the good old door-knocking salesforce.

Why is this the case? Well, it appears the physicians are easily “activated.” So rational resource allocation is to get your reps in front of all the 4,000-5,000 target derms. asap! Which is what management appear to be doing.

For the model, Sales and marketing is built up as follows:

· FY25: 27 Reps (FY25 is not refined as it's immaterial to valuation)

· FY26: 50 Reps

· FY27: 60 Reps – they go from 90% coverage to expand the base in targeted areas.

And so the Sales & Marketing expense then follows.

2.2 COGS

I’ve assumed a flat 7% of Gross Refill Value is assumed. i.e., 0.07 x AUD1500 = AUD105 per refill

This is on the high side to allow for Tariff impacts (assuming Tarrifs apply to COGS and not Sales!)

An error in the model is that inventory needs to be made 3-6 months ahead of sales, but this is not material given all the other assumptions, so I’ve ignore working capital.

2.3 Total Expenses

Expenses are estimated as follows:

· The expense base at 1H FY25 Accounts (4D) as starting point: AUD 32m x 2 = AUD 64m

· Strip out Sales and Marketing, so it doesn’t get double-counted: -AUD 17.7m

· Expense Base = AUD 47m + Sales and Marketing.

I’ve assumed interest is included in here, and may have under-estimated charges for the expanded debt facility.

2.4 Getting to NPAT and EPS

PBT = Net Revenue – COGS – Expenses

Tax rate assumed at 25%, as there will be benefit from carried forward tax losses.

NPAT = PBT * (1-Tax)

Shares on Issue: Management are using a fair amount of share-based compensation, so I assume 3% dilution p,a,

3. VALUATION

The model generates FY28 NPAT for 12 scenarios, combining the various factors covered.

P/E Ratio – This is the second big driver for the change to my valuation. The change in this valuation over my pervious valuation is that SOFDRA does not appear likely to be a blockbuster. It looks like it will be moderately successful and reaches maturity in FY28, and is not rolled out beyond the US. (The economics are not attractive.)

Growth from FY28 onwards will then depend on whether – over the next three years (not tomorrow!) – management can bring other undervalued dermatology drugs onto the platform.

I’m not sure they’ll succeed and so the P/E ratio scenarios I will apply in FY28 are 20, 25 and 30.

If you think $BOT is “Sofrda and done”, then eventually it will get bought out at some multiple.

So, I’ve taken FY28 EPS and discounted back for 3 years to end of FY25 at10%

Bingo.

This is still betting on management experience and skill in dermatology, and it gives them a reasonable time horizon to either do platform deals or licence in new molecules. If I didn’t believe in management, then P/E scenarios of 15 and 20 would probably be more appropriate. This risk is not explicitly modelled, but that’s because I believe management will find a way to create more value over time.

The detailed inputs and key outputs are listed in Exhibit 5.

Exhibit 5: Model Scenarios and Outputs

The table above shows the outputs from the various scenarios. I’ve not really had the time to think about the scenarios probabilistically, but if I had, the distribution of valuations would be as shown in the Exhibit 6.

Exhibit 6: $BOT Valuation Results

At my refence P/E of 25, I get a valuation range using my usual p50% (p10% - p90%) notation, of $0.35 ($0.22 - $0.90) in roundabout terms.

At my p50% level, the range generated by my P/E values (20, 25, 30) are $0.27 to $0.41

My conclusion is that the market has indeed over-reacted to the “Nightmare on Hyperhidrosis Street”. Even in my lowest case analysis, I can’t get below $0.17. And yet that’s where we are today at $0.16 to $0.18.

While my previous very bullish view on $BOT has been materially deflated (sigh), I think the market has got this one wrong. Standing here today, you’d probably need to give me $0.60-$0.70 to get me to part with my shares.

4. Discussion of Valuation and Model Outcomes

4.1 Discussion

Depending on how you compose your scenarios, you can generate either more valuation results at the low end or more at the high end of Exhibit 6.

So, picking a number is indeed a fools game. I’m not sure of the value of doing more analysis on this, simply because the spread of valuations starts squarely at today’s market price and are solidly risked to the upside. IF YOU BELIEVE MY ASSUMPTIONS.

It is true that I could easily generate valuations down to $0.10 or lower, but equally, I can easily still get valuations north of $1.00 – in both cases using reasonable assumptions.

But based on what I believe to be reasonable assumptions, I am a solid HOLD on $BOT given by 4% RL position.

4.2 M&A Valuation

If we assume that by FY27 it becomes clear that $BOT is nothing other than “US Sofdra and Done”, then it won’t make sense as an ongoing entity and will get acquired.

To test the valuation, I’ll apply a modest 5 x FY28 revenues, and discount back.

Doing this I get a range of valuations of $0.24 to $0.42. Funnily enought, the midpoint of $0.33 is eerily close to my bottom-up $0.35 p50% at P/E = 25. (Honest, I haven't had time to fudge the models!)

5. “A Nightmare on Hyperhidrosis Street 2 – The Revenge of the Applicator”

So, why another “comprehensive” webinar on Monday?

I think management HAVE to do this because the 4C is doing to drop on Monday. Revenue and Cash will be bugger all, and cash burn will be scarey. And so management has to help the market make sense of the cost base. If they don’t do that, half the analysts will predict that $BOT runs out of money pretty soon.

And I don’t think they will run out of cash. For example, I’ve plotted the financials below for one of my more central case scenarios in Exhibit 7. $BOT can get close to breakeven in FY26 and is strongly cash generative in FY27.

Exhibit 7: Modelled $BOT Financials (Scenario 6)

Even in the case where I’ve layered on $20m of excess sales and marketing costs, with the lowest monthly prescription case (Scenario 12), there’s probably enough liquidity to get through to positive cash flow in FY27, just.

Exhibit 8: Modelled $BOT Financials inHigh Cash Burn / Lower Revenue Case (Scenario 12)

Of course, I’m also hoping for some more insights about rollout. After all, there’s been another 4 weeks of data, so hopefully there’ll be an update on scripts and prescribers.

6. So. What about My Thesis?

The whole point of doing all this work was find out if my investment thesis is intact or not. And?

My investment in $BOT was initially predicated on the view that the market was seriously mis-pricing development and execution risk. Development risk mispriced, because we knew the product works based on experience in Japan and the promising US clinical trial data (now published in JAAD). Execution risk overblown because 1) there is huge unmet need in the market, 2) the management team have a strong track record in dermatology launches and 3) the existing anticholinergic product in the market has well-defined deficiencies, and is being managed by a lightweight company trying to juggle multiple products.

I bought $BOT between $0.325 and $0.47 in the belief that this business was worth anywhere from $1.00 to $2.00.

Wind forward to today, and while physicians are getting onboard, prescription rates are underwhelming, and conversion to net revenue is less than (I) expected. Added to that, the company is rapidly scaling up sales and marketing spending.

So, the market is in the doldrums, seeing this business as worth $0.16 - $0.18. But I think it would be worth anywhere from $0.20 to $0.90. That’s a serious haircut to what I thought, but still an interesting investment. And it is early days.

So, my thesis while seriously diminished, is not broken. I’m happy to see how this story continues to unfold.

At this stage, I’m not sweating.

Disc: Held in RL(4%) and SM

As @Strawman made special efforts to feed the "spreadsheet jockeys" on the call this morning, I thought it only fair to respond in kind.

Matt referred to the potential that Sofdra really takes off, being a case not at all considered in the E&P and EH valuations of $0.47 and $0.55. So I thought I'd have a go a putting some dimensions around that.

Assumptions (details shown in the spreadsheet below)

- Assume sales build to peak over 5 years according to the profile given

- 5% of diagnosed market captured in yr 5

- 2.5% of undiagnosed market capture in yr 5

- 12 scripts per year at 50% persistency (absolute, not progressive/cumulative)

- %GM 76%; SG&A grows at 20%; R&D at 10% of revenue; nominal DD&A (capital light)

- No debt

- SOI grow at 2.5% per annum

- P/E in 2029 of 50 (which is modest if this baby takes off)

Crank the handled and discount back at WACC of 10% and you get a valuation of $12bn, today.

In this scenario, they are writing 2m scripts p.a. in 2029. That's just double the rate in Japan after 3 years. With excellent marketing and execution, that's not inconceivable.

To be clear, this IS NOT my valuation. I am happy to leave my valuation at a "modest" $1.20.

The point is that if we see a strong revenue trajectory in 2Q25, 3Q25 and 4Q25, then this indicates the order of maghnitude change that could possible emerge - which is probably more in line with where Howie and Vince are thinking.

For sure, there is a lot amount of execution risk. But this kind of upside potential means that this morning I've added a further 20% to my RL holding at $0.335, and will align SM accordingly. I want to place a bigger bet here.

I wasn't around to get on the $PNV bus pre-revenue, but I'm damned sure that I'm on this one with a solid position.

I'll write a separate straw with some reflections on the SM meeting later today.

Disc: Held in RL (7%) and SM

Just over a month ago Euroz Hartley published a short term price target for $BOT of $0.33, predicated on their assessment of the typical run-up in SP ahead of an FDA decision. Sure enough, with days to go, SP has passed this target standing today at $0.345.

I have absolutely no interest in short-term trading, as I am placing a 90% risked bet that this will be a much more valuable proposition. Much more over time. That said, it is interesting to watch the volumes and prices.

Last week's "non-announcement" appears to have given the market a little nudge, reminding the hot money out there about the impending FDA decision.

In the success case, on fundamental grounds, I expect the SP to go a lot higher. However, if there is a negative decision, this baby has pumped up enough that any correction will likely be hard indeed.

At time or writing there are still slightly higher volumes in the "BUY" queue (9m) than the "SELL" queue (7m), but things have evened up a little from this morning. But today marks the 3rd conseuctive day of higher than normal volumes.

tick-tick-tick

Disc: Held in RL and SM

$BOT have sent existing shareholders and everyone on their mailing list the updated Euroz Hartley report following last weeks Commercial. It is a thorough and well-written report, so I have put screenshot below in this straw.

Its gives a valuation of $0.33, and clearly seems to encourage the pre-FDA SP uplift short term trade. (Not for me)

I prefer to focus on the long term investment proposition in the success case.

Before reading, be aware the EH supported $BOT in the recent capital raise. It is also likely based on my reading of the disclaimer they have been engaged by $BOT as their defence adviser. EH have been paid by $BOT in shares for the advisory services they've provided. So although EH have certified that this is their own opionion, it is clear that it has been prepared benefiting from the EH collaboration with $BOT management and board.

So when I read it, I read it more as the view of $BOT management than of an independent analyst. So, I wanted to make that clear up front.

You can read the report yourself, but I wanted to highlight a few points.

FDA Approval

The imply a CoS of FDA approval in June as 90%

Benchmarking ASX FDA Knockbacks Leading to CLRs

They compare recent ASX companies that received a knockback at FDA approval (listed in Fig 3. on page 4). Of the 7, 5 were finally approved, one withdrawn, and one under review.

However, what is important, is that none of the sample group received knock-backs purely for label/patient information data. All were some combination of safety, efficacy of manufacutring, with one (later approved) not providing details.

%BOT's CRL was was labelling and patient information. The corrected labelling led to 100% compliance in the human factors study.

Therefore I think 90% is a reasonable CoS, and perhaps given $BOT reports of having high confidence of approval following engagement with the FDA in recent weeks, it is hard to understand the basis for a rejection. Should a rejection occur it would be a shock.

Revenue Profile

Figure 8 on Page 7 provide revenue projections. The growth curve looks reasonable. However, to my eye it looks conservative give the gap in the market that SOFDRA addresses. The projection is to only penetrate 1.0% of the market by 2033 - 9 years after launch.

As ever, the drug will only suit some sufferers, and not everyone will respond. In any event there is certainly upside to this if the drug is well-received by the market.

Cautioning my own enthusiasm, I note that the analysis has considered the progress of the drug in Japan in developing their projections. $BOT reported that Kaken have sold 350,000 units in the last 12 months in Japan. The valuation forecast projects the US taking 5 years to get to this. So following launch (assuming approval) it will be instructive to follow the early US profile compared with the experience in Japan. There has to be a bull case to do much better than the EH profile.

Valuation

Of EH's valuation of $0.33, $0.26 comes from SOFDRA and $0.06 from the development portfolio.

My Quick Valuation - Bull Case - SOFDRA is approved in June with minor risk adjustment

I think the EH sales profile is a prudent forecast, and I base my valuation solely on SOFDRA.

On the basis that $BOT achieve an EBIT in 2029 of US$104m, carrying no debt, and applying tax at 30% and USD:AUD 0.67 give 2029 NPAT of A$109m.

With 1,575m SOI, although $BOT will be highly cash generative quite soon, I'll allow some dilution due to share based compensation, so assume SOI of 1,800 in 2029.

That gives a 2029 EPS of $0.061.

I'll deal with the uncertainty via the P/E ratio, ranging from 25 to 45 - probably very conservative for a high growth pharma company.

I'll add a risk premium to the WACC, and discount at 12%.

My unrisked valuation range is: $0.88 to $0.1.56 (but including a margin of safety in the risk premium)

So, now I am going to apply my 90% CoS, and assume that in the 10% failure case

- There is a net 5% chance that there is a subsequence approval on what ever the residual issues are, and that the profile gets pushed out by another year, leading to a further discount and a further dilution of 10%.

- There is a net 5% chance that the drug is withdrawn amd the value of the business is $0.06 of the development portfolio.

Boiling all this up together, and I get a risked valuation of: $1.13

What do I have to believe: 1) SOFDRA gets approved some time in the next year, 2) the telemarketing strategy is successful, 3) the product gets some traction over 9 years with 1% of the potential market.

Not a long bow to draw for a Bull Case.

Now at the start of this straw, I speculated that EH are $BOT's defence advisor. If their valuation is truly $0.33 that clearly cannot be true, because as my analysis shows, if you believe the forecast, and had deep pockets, you'd happily put in a takeover offer today of $0.50 to $0.60. The board should send any acquirer away for anything south of $0.60 or even $1.00 IMHO, given the upside which I haven't even attempted to assess.

So there is a lot of risking being applied to the EH analysis, unless I am missing something!

(I note that my fellow $BOT bull @Nnyck777 is at $1.92 ... I'm slowly getting there :-)

Disc: Held in RL and SM

$BOT have issued their 4C.

Highlights

Cash holdings actually increased, thanks to exercise of options.

We're now two months away from the expected FDA decision on Sofdra - one way or another that will be a major SP catalyst, with anything but an approval a major surprise.

Accordingly, $BOT are making good progress in preparations for launch. They've focused activities on the US payers (insurers) and report"

"The Company has now engaged players that account for 80% of covered lives in the US and is pleased with the feedback regarding pricing and the relative absence of obstacles for patients to access Sofdra following planned approval."

So, if the approval is straighforward and goes as expected, then FY25 is going to be an important year!

Disc: Held in RL and SM

I wanted to better understand the precedence around the FDA letter holding up approval of sofpironium bromide gel based on labelling and patient information deficiencies.

I found an interesting reference on the subject in JAMA (Sacks et al. (2014) JAMA 311(4) 378-384). The article is a little too dated for my liking, but the information in Table 5 is interesting. (below)

Of 151 drugs not approved in their first cycle, 71 were subsequently approved following resubmission, with 80 not approved during the lifetime of the study.

What is more interesting is that only 4 drugs (2.6%) were not approved first time for labelling alone, and all 4 of these were subsequently approved.

Although the median delay in the study was 435 days this includes the entire population which is dominated by drugs with safey, efficiacy, chemistry, manufacturing and controls issues, many of which would have required further clinical trials. There's no data on the delay for labelling ony.

So this provides some independent support for the CEO's confidence that the drug will be approved when the labelling feedback is addressed.

It is many years since I was a practitioner in the industry, so it is good to know that the 2.6% of labelling rejections aligns with my own intuition that, while not un precedented, a labelling-only knockback is unusual.

In his interview on Ausbiz yesterday Howie McKibbon said "It's something that we anticipated. If we were going to get any feedback from the agency, we would have that much earlier in the cycle. So we were quite surprised that this occurred," which reinforced my own expectation that label feedback is usually addressed in earlier communication between the FDA and applicant, prior to the final decision.

Thinking about this overnight, I think the reason that this didn't happen in this case, is that the instructions relate to the use of the gel applicator, that requires validation in a controlled environment. So, its not just a change to the label (as you might easily do for a pill or capsule) but a patient instruction that has to be validated by observation and requires a supplemental submission reporting the results. I think that is why a resubmission is required and makes me think that maybe Howie shouldn't be so surprised. (It also weakens any argument about conspiracies!)

Source: Sacks et al. (2014)