The thesis is focuses on the diagnostic 64Cu-SAR-bisPSMA (Cu-64) for prostate cancer with the theragnostic and pan-cancer pipeline as upside opportunities yet to add value. Clarity is seeking an NDA for Cu-64 as a diagnostic tool for application in pre-Radical Prostatectomy and BioChemical Recurrence (BCR) patients via the CLARIFY and AMPLIFY phase 3 studies. Both are key points in the management of prostate cancer that are well suited to the product as Telix has demonstrated with it’s Ga-68 product and provides a credible base line model to use for valuing Cu-64.

Head-to-head studies against Ga-68 via the Co-PSMA study shows significant advantages in terms of efficacy on a 1-hour base line, but the significantly higher half-life allows for 24 hour imaging that has enhanced efficacy further on that base line. The significantly higher half-life and shelf life of Cu-64 Vs Ga-68 (and F-18) are also a critical differentiator for manufacture and clinical application. As such once in market Cu-64 is highly likely to dominate it’s market against existing products capturing a high proportion of the TAM.

The Clarity CEO has a TAM estimate of $5b based on US$5k treatments and the approximate 1m US diagnosed prostate cancer population that have received and are under serviced with pre-Radical Prostatectomy or BCR related PSMA-PET scans. This is the prevalence (population) and may enhance the initial TAM, however the incidence (annual new cases) is more relevant for forecasting ongoing future sales each year and this is ~330k according to the American Cancer Society, of which around 70% are diagnosed with low risk cancer (Prostate Cancer Incidence) and 60% of those are managed with active surveillance (Low risk active surveillence). So around 58% of new diagnosis go onto have a Radical Prostatectomy which is ~191k a year, giving a ~US$950k TAM for that procedure (at US$5k each).

The incidence of BCR is between 20-40% of those having a Radical Prostatectomy (BCR after RP). The increased use of Robot-assisted radical prostatectomies (RARP) is improving results, so the low end of this range is of most relevance. This increases the Radical Prostatectomy TAM by 20% to ~US$1.15b given it is a related follow up.

This is probably low ball, given there is a case that Clarity with it’s significantly improved efficacy on current options will be used in expanded situation, also I am assuming just 1 scan for each case, but there is likely to be pre and post procedure scan’s plus it may be used in additional follow up testing (testing and treatment paths are doctor and patent dependent). I note TLX has a US$7b TAM for their Precision Medicine PSMA opportunity which seems very large, my understanding is the total prostate cancer diagnosis and treatment market is around US$15b.

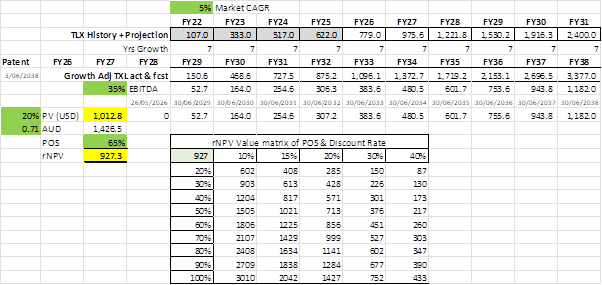

A middle ground and factoring market penetration rates for a sales estimate is the Telix forecasting sales of around US$2.4b by FY31 they are currently tracking to around US$800m in FY26, so I will use the combination of Telix’s actual and forecast sales (year adjusted by 5%pa growth) to project Clarity sales from FY29 (my estimate of market entry) to FY38 (patent expiry) as well as take the Telix’s EBITDA of 35% on it’s diagnostic business for a cashflow estimate.

Normally at this stage I would take a statistical average probability of success (POS) for Phase 3 assets of 50% but I value the work @mikebrisy’s has done on Clarity and agree it is much higher. I will take the low end of his 65-75% range to now cast the current value of the company.

Based on this and “now casting” based on the current market price of Clarity I get the below. In short, the current price assumes there is a 65% chance a 20% return is achieved through to FY31. This is just the current PSMA-PET diagnostic, with a net zero value for the theragnostic in Phase 2 and other active programs and pipeline options. A matrix of outcomes is also shown for different POS and discount combinations.

One key thing I am unsure on is the expected time to NDA if successful. As such I have pushed first revenues out to FY29 which I hope will be conservative and will adjust with additional information because even 1 year earlier can make a significant difference to the value of patent protected products.

Why buy now

Pre commercial Biotech companies on the ASX are for the most part heavily discounted compared to similar US listed companies which is a great edge for Australia investors. However, due to skilled capital management of the CEO, Michael Parker, plus the halo effect of Telix, the discount for Clarity has been much lower or non-existent over recent years. This is exemplified by Telix having a market cap under A$200m at a similar stage of development.

The recent pull back in price provides the margin of safety that was previously missing, I don’t think it was over valued previously but it sure wasn’t undervalued either and I look for investments that are significantly undervalued, which I believe is now the case for Clarity, a price around what it traded at 2 years ago but significantly higher POS.

As such I have a starter position and intend to add on price drops or where clinical progress increasing value is not priced in.

Disc: I own RL