Consensus community valuation

The thesis is focuses on the diagnostic 64Cu-SAR-bisPSMA (Cu-64) for prostate cancer with the theragnostic and pan-cancer pipeline as upside opportunities yet to add value. Clarity is seeking an NDA for Cu-64 as a diagnostic tool for application in pre-Radical Prostatectomy and BioChemical Recurrence (BCR) patients via the CLARIFY and AMPLIFY phase 3 studies. Both are key points in the management of prostate cancer that are well suited to the product as Telix has demonstrated with it’s Ga-68 product and provides a credible base line model to use for valuing Cu-64.

Head-to-head studies against Ga-68 via the Co-PSMA study shows significant advantages in terms of efficacy on a 1-hour base line, but the significantly higher half-life allows for 24 hour imaging that has enhanced efficacy further on that base line. The significantly higher half-life and shelf life of Cu-64 Vs Ga-68 (and F-18) are also a critical differentiator for manufacture and clinical application. As such once in market Cu-64 is highly likely to dominate it’s market against existing products capturing a high proportion of the TAM.

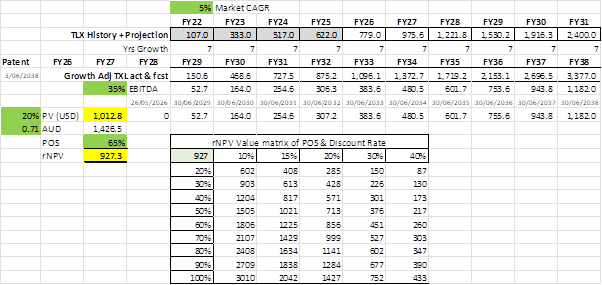

The Clarity CEO has a TAM estimate of $5b based on US$5k treatments and the approximate 1m US diagnosed prostate cancer population that have received and are under serviced with pre-Radical Prostatectomy or BCR related PSMA-PET scans. This is the prevalence (population) and may enhance the initial TAM, however the incidence (annual new cases) is more relevant for forecasting ongoing future sales each year and this is ~330k according to the American Cancer Society, of which around 70% are diagnosed with low risk cancer (Prostate Cancer Incidence) and 60% of those are managed with active surveillance (Low risk active surveillence). So around 58% of new diagnosis go onto have a Radical Prostatectomy which is ~191k a year, giving a ~US$950k TAM for that procedure (at US$5k each).

The incidence of BCR is between 20-40% of those having a Radical Prostatectomy (BCR after RP). The increased use of Robot-assisted radical prostatectomies (RARP) is improving results, so the low end of this range is of most relevance. This increases the Radical Prostatectomy TAM by 20% to ~US$1.15b given it is a related follow up.

This is probably low ball, given there is a case that Clarity with it’s significantly improved efficacy on current options will be used in expanded situation, also I am assuming just 1 scan for each case, but there is likely to be pre and post procedure scan’s plus it may be used in additional follow up testing (testing and treatment paths are doctor and patent dependent). I note TLX has a US$7b TAM for their Precision Medicine PSMA opportunity which seems very large, my understanding is the total prostate cancer diagnosis and treatment market is around US$15b.

A middle ground and factoring market penetration rates for a sales estimate is the Telix forecasting sales of around US$2.4b by FY31 they are currently tracking to around US$800m in FY26, so I will use the combination of Telix’s actual and forecast sales (year adjusted by 5%pa growth) to project Clarity sales from FY29 (my estimate of market entry) to FY38 (patent expiry) as well as take the Telix’s EBITDA of 35% on it’s diagnostic business for a cashflow estimate.

Normally at this stage I would take a statistical average probability of success (POS) for Phase 3 assets of 50% but I value the work @mikebrisy’s has done on Clarity and agree it is much higher. I will take the low end of his 65-75% range to now cast the current value of the company.

Based on this and “now casting” based on the current market price of Clarity I get the below. In short, the current price assumes there is a 65% chance a 20% return is achieved through to FY31. This is just the current PSMA-PET diagnostic, with a net zero value for the theragnostic in Phase 2 and other active programs and pipeline options. A matrix of outcomes is also shown for different POS and discount combinations.

One key thing I am unsure on is the expected time to NDA if successful. As such I have pushed first revenues out to FY29 which I hope will be conservative and will adjust with additional information because even 1 year earlier can make a significant difference to the value of patent protected products.

Why buy now

Pre commercial Biotech companies on the ASX are for the most part heavily discounted compared to similar US listed companies which is a great edge for Australia investors. However, due to skilled capital management of the CEO, Michael Parker, plus the halo effect of Telix, the discount for Clarity has been much lower or non-existent over recent years. This is exemplified by Telix having a market cap under A$200m at a similar stage of development.

The recent pull back in price provides the margin of safety that was previously missing, I don’t think it was over valued previously but it sure wasn’t undervalued either and I look for investments that are significantly undervalued, which I believe is now the case for Clarity, a price around what it traded at 2 years ago but significantly higher POS.

As such I have a starter position and intend to add on price drops or where clinical progress increasing value is not priced in.

Disc: I own RL

$CU6 today released the details of the analysis of the Co-PSMA data presented at the EAU Congress 2026. Shareholders and followers of this business might be forgiven for saying "what? again?" as this is the third ASX release in as many months regarding the outcome of this investigator-led trial. Equally, casual watchers might look at today's SP (down 5% at time of writing) and conclude "oh, it's bad news". Wrong. The further detail presented is positive news on all fronts.

There is a lot of devil in the detail of these clinical releases, so in this straw I will summarise:

- (recap) At a high level what we already know from the Dec-25 and Feb-26 releases

- What's news and why it matters

- Overall, so what?

1. What we already know

From the Dec-2025 announcement and the Feb-2026 abstract release, the key efficacy findings of the Co-PSMA trial were already well established. The study met its primary endpoint, demonstrating that 64Cu-SAR-bisPSMA detects significantly more lesions per patient than standard-of-care 68Ga-PSMA-11 in a low-PSA biochemical recurrence setting (PSA 0.2–0.75 ng/mL).

The following quantitative results were fully disclosed in the February abstract: mean lesions per patient (1.26 vs. 0.48, ratio 2.63, p<0.0001); total lesions detected (63 vs. 24); positive scan rate (78% vs. 36%); and management impact (44% of patients). The February release also introduced early diagnostic accuracy data in the form of true positive rates, reported at that time as 75% for 64Cu-SAR-bisPSMA vs. 39% for 68Ga-PSMA-11 (based on 28 evaluable patients with a standard of truth).

In short, prior disclosures had already established a clear efficacy advantage, particularly in low-PSA disease where current PSMA agents are weakest.

2. What's New Today? Why it Matters

Today's release adds several important layers of depth that elevate the dataset toward regulatory and clinical maturity. These additions fall into four categories.

2.1. Peer-review acceptance in European Urology

The Co-PSMA manuscript has been accepted for publication in European Urology, the official journal of the EAU with an impact factor of 25.2. This materially strengthens scientific credibility and external validation beyond the conference abstract, and is a meaningful milestone in the asset’s path toward regulatory submission. I'm not saying it is a part of the regulatory path, but peer-reviewed acceptance in a high quality journal gives an indication that the results stand up to expert, independent scutiny. In that respect, I take it as a leading positive indicator of regulatory success, or at least an improvement in the chance of success.

2.2. Revised and expanded diagnostic accuracy metrics

Today’s release provides a more complete and updated diagnostic accuracy profile. Two important points require careful attention here.

First, the true positive rate figures have changed from the February abstract. The earlier abstract reported 75% (21/28) for 64Cu-SAR-bisPSMA vs. 39% (11/28) for 68Ga-PSMA-11, based on 28 evaluable patients. Today’s release reports 71% (24/34) vs. 29% (10/34), based on a larger evaluable cohort of 34 patients. The expansion of the standard-of-truth denominator from 28 to 34 reflects the final, fully verified dataset and is the more reliable figure.

Second, today’s release introduces explicit false negative rates: 21% for 64Cu-SAR-bisPSMA vs. 65% for 68Ga-PSMA-11. While these figures were arithmetically derivable from the February true positive rates, their explicit disclosure — using the final, larger denominator — is both new and significant. False negative rates directly address the risk of missed disease, which is the key clinical limitation of existing PSMA imaging in the low-PSA setting and is likely to be a focus of regulatory scrutiny.

2.3. Granular lesion location breakdown

For the first time, today’s release provides a detailed anatomical breakdown of where additional lesions are being detected. This data was entirely absent from both the December and February releases and represents one of the most clinically actionable new disclosures.

Table: Location of recurrence: 64Cu-SAR-bisPSMA (24-hour) vs. 68Ga-PSMA-11

The biggest differential between the two agents is in the prostate fossa (56% vs. 22%) and lymph nodes (20% vs. 8%) — precisely the sites most relevant to salvage radiotherapy planning. This breakdown directly links the improved detection signal to actionable clinical decision-making, and explains the mechanism behind the 44% management change rate. It is also the type of granular, site-specific evidence that regulators and clinical guideline bodies require to support label claims.

2.4. Clearer regulatory pathway articulation

Today’s release provides more explicit positioning of 24-hour imaging as the mechanistic differentiator underpinning the performance advantage, alongside a clearer articulation of how Co-PSMA will be combined with the Phase II COBRA data and the anticipated results from the pivotal Phase III AMPLIFY trial in a future FDA submission package for the BCR indication. Collectively, this framing shifts the dataset from “strong abstract-level results” to a more complete, regulator-ready evidence package with clearer clinical and mechanistic context.

3. Conclusion - So What?

Overall, today’s disclosure does not change the fundamental efficacy story in Co-PSMA — the superiority of 64Cu-SAR-bisPSMA over 68Ga-PSMA-11 was already well established in both the December and February releases. However, the update delivers four meaningful additions: peer-review acceptance in a top-tier journal; a revised and expanded accuracy dataset (including an updated true positive rate from a larger evaluable cohort and explicit false negative data); a detailed anatomical lesion location breakdown that was entirely new and is the most clinically actionable addition; and a clearer regulatory submission roadmap.

Notably, the revision to the true positive rate figures (i.e., from 75% to 71% for 64Cu-SAR-bisPSMA and from 39% to 29% for 68Ga-PSMA-11) reflects a larger and more complete evaluable dataset and should be treated as the definitive accuracy figures going forward. The directional advantage for 64Cu-SAR-bisPSMA is preserved and strengthened on the false negative metric.

In effect, the update represents a de-risking and maturation step rather than a step-change in efficacy, moving the asset incrementally but meaningfully closer to regulatory readiness and real-world adoption, without altering the core investment thesis established by earlier releases.

Overall, pretty good news IMHO.

Disc: Held in RL

Has imaged the first patient in its registrational Phase III 64Cu-SAR-bisPSMA diagnostic trial in participants with biochemical recurrence (BCR) of prostate cancer, AMPLIFY (NCT06970847) 1, at XCancer in Omaha, Nebraska (NE).

Just the CU6 cash position,

- Quarterly Activities/Appendix 4C Cash Flow Report:

https://hotcopper.com.au/threads/ann-quarterly-activities-appendix-4c-cash-flow-report.8561064/

Clarity's cash balance at 31 March 2025 was $95.1 million

Last

$2.16

Change

0.010(0.47%)

Mkt cap !

$694.1M

Clarity how it’s share price compares?

The best crafted model in the world is just that, a model. I find valuing biotech stocks particularly difficult and there is added complexity on the ASX. As one Straw-person put it recently (I will paraphrase), a biotech’s share price is directly proportional to the number of old boys in agreement at your long boozy Friday lunch. Cynical, yes but honestly there are pre-clinical biotech’s that are valued purely on TAM and hope while other revenue generating companies that are making millions and growing at greater than 25% YOY are hammered for missing guidance by a whisker.

I noticed a lot of talk about Clarity on my Strawman feed. I was curious to look at this biotech a little closer. I am absolutely no expert and I have merely taken a cursory glance, so please correct me if I am wrong and critique away.

My first impression is that it seems to be valued very highly for a pre-clinical stage company. While it seems like great tech – potential revenue seems to be years away. It also plays in the difficult space of cancer. I tend to avoid this space as I find that this is well outside my comfort zone.

I am all for investing in early stage biotech companies, if I understand the science and if there is a bargain to be had. The key to success is getting in early before it is priced for success and perfection.

In this straw I have pitted Clarity Pharmaceuticals head to head against 3 other ASX bio-techs that I am more comfortable and familiar with (and invested in). This is a quick and dirty check to see if I am interested in digging further into Clarity.

Clarity’s technology basically injects special molecules (copper based) into patients to bind to specific targets on cancer cells. PET scans then pick up this energy from injected molecules to help locate and target cancer treatment more effectively. Theoretically there is a more targeted treatment and less damage to non-cancerous cells.

So Clarity has 3 platforms currently in various trial stages but mostly in the safety trial phases, 1 and 2. These platforms are largely targeting prostate, breast cancer and neuroblastoma. Certainly big areas of need and potential revenue if successful. The other companies in the head to head comparison, unlike Clarity, have FDA approved products or drugs which are already revenue generating. 1).Neuren is collecting royalties and milestone payments from Acadia for its lead FDA approved drug Daybue TM 2). Polynovo is currently selling Novasorb TM world-wide and collecting revenue from BARDA trials and 3). Botanix is collecting very small but growing royalties from its Japanese counterpart for sales in Ecclock TM . Botanix is also about to start selling its first and only FDA approved drug Sofdra TM into the market Q3 this year.

Table 1: Clarity is Pre-Clinical unlike Neuren, Polynovo and Botanix. Neuren has already had 3 successful phase II trials and waiting for Phase III trials. Botanix also is waiting for Phase III trials for Rosacea and Acne and 2b for anti-microbial.

Clarity Pharmaceuticals: A market cap comparison

A quick review of Clarity shows a market cap (at time of writing) of about AU$1.88billion. Remembering this is a pre-clinical company with only products in phase 1 and 2 so far. It is not generating any revenue yet has a similar market cap to Polynovo AU$1.74 billion and Neuren AU$2.07billion.

Table 2. Comparison of Market Cap

Clarity has negative Earnings per Share (EPS) and Return on Equity (ROE). While its compatriots Polynovo and Neuren are selling products/drugs into the market and have positive and growing EPS. While Neuren’s ROE has sky rocketed this FY due to approval of Daybue TM by the FDA. This astronomical rise will not continue but should level out over the next few years and have reasonable increasing % royalty returns.

EPS growth is also estimated to increase for Botanix according to Bell Porter’s latest analyst report. Although this is merely speculation and educated guessing as Sofdra TM is a brand new drug for the US market. However there is a precedent with its lead drug currently being sold in Japan and growing strongly YOY. Hence the 122% EPS growth prediction isn’t outlandish.

So for every dollar I invest I have can choose to buy a company that is generating positive returns or is about to or I can invest in Clarity which is loss making and will be several years away from generating any earnings, if ever.

Table 3. Comparison of Cash on Hand, P/E and Revenue

Clarity Pharmaceuticals: A sales comparison

Comparatively CU6 does have significant cash on hand following $120 million dollar raise in the first half of 2024. However bio-techs are notoriously cash burning with most examples of drugs and products costing between $50-$300 million to bring to market. It is pretty clear with $136 million cash left on hand that Clarity will have to raise again in upcoming years. Raises in bio-techs usually cause significant dilution for long-term holders.

Polynovo with a similar market cap has enough cash on hand to fund revenue growth of near 36% annually. This is now self-funded and the company had its first net profit after tax in the 1H of FY 24. Further dilution and raises are very unlikely unless there is an upcoming acquisition that makes financial sense to bolt on to Polynovo’s portfolio of products.

Neuren has seen large annual growth this FY and royalties and milestones as well as cash on hand of $228 million will be sufficient to self-fund two phase three trials. Whether Neuren does this on their own or is acquired is anyone’s guess but Jon Pilcher has confirmed that the upcoming trials are likely to cost between AU$50 million and $100million and take approximately 3 years to get its second drug NNZ2591 to market. If this occurs Neuren and trials are successful it will keep 100% revenue generated.

Botanix is funded $80 million to take its lead drug Sofdra to market launch. Whether this company becomes self-funded or will need to raise again remains to be seen. Q3 this year will give us insight into the future trajectory of this company. Being on the eve of becoming revenue generating and better yet Botanix will keep approximately 95% of all revenue with only a small royalty going to Bodor the original creater of Sofdra.

So I can invest in Neu and PNV with similar market caps to Clarity and get access to self-funded revenue generating companies that have positive NPATS. Or I can invest in Botanix which has a much lower market cap, admittedly untested and higher risk but also soon to be revenue generating. Whereas Clarity is not revenue generating and yet has a higher market cap than Botanix and is years from making profit.

P/E comparisons

Clarity has no P/E ratio as it has no earnings (except R and D tax rebates). Polynovo has a high P/E 127. However paying $2.52 a share allows access to a company growing revenue at 54.9% STLY. Including BARDA this revenue increases to 65.6% growth on STLY. By comparison Polynovo has a very high P/E and shares seem to be fully valued whereas Neuren has a low P/E for a biotech of 13.18.

Polynovo seems reasonably valued compared to other successful pharmaceutical company's such as Pro Medicus, whos P/E sits at 191 with much lower growth rates of 23.8%. This makes sense given Polynovo is such an early stage company and Pro Medicus is much more mature.

While Neuren seems grossly undervalued with such a low P/E to get access to a growing royalty and milestone revenue stream with an impending priority review voucher thrown in. There is also a second future drug potential on the horizon that doesn’t seem to be contributing to valuation currently.

Botanix will be interesting to watch but the wait is not far away and the company is ridiculously cheap with impending US revenue due shortly.

Investing in Polynovo gives you access to this:

Investing in Neuren Pharmaceuticals gives you access to this:

In the last 12 months Neu has grown its EPS from AU$0.0015 to AU$1.23. This was a EPS 12 month trailing growth of 84569.93% due to the FDA catalyst approval of Daybue. The EPS of course will not continue at this rate.

PE ratio for NEU is 13.18% to buy into this growth. The ROE has been 35% in this time. A good company is considered to have an ROE of 15-20%.

Investing in Botanix gives you access to:

Royalties of AU$800 K annually growing at an estimate of 122% according to Bell Porter. Possible projected revenues of US$ 20-$90 million (200,000 units x $490) in FY2025

Management Comparisons

Table 3. CEO compensation and % of tightly held shares

Clarity is certainly a tightly held shares 35.88% being owned by management and the CEO owning 0.75% of the company. Collin Biggin also seems to take a reasonable salary for his position.

There is a lot of speculation about a Neuren buyout. However there is also some protection from hostile takeovers with 13.06% of the company being held by company management. Jon Pilcher takes a very reasonable salary and a majority of his compensation is performance based (59.8%). He also has a 0.3% ownership stake in the company.

Swaomi Raote for all his years of experience is also only drawing an average salary with a 52% performance based compensation. While his % proportion of company ownership is not disclosed when I looked at Simply Wall St.

Howie McKibbon draws an average salary and has the shortest CEO tenure of any of the company's. He was however appointed by Vince Ippolito Executive Director and the two had worked together for many years across different dermatology company's. His compensation is also very heavily performance based. A good sign for shareholders.

Analyst Insights: A comparison

Analysts are in agreement that clarity is a buy and a strong buy according to the 3 analysts covering this stock. Polynovo and Neuren and Botanix are largely also touted as strong buys.

Management teams are largely in agreement with analysts and having been buying stock through 2023. However, Clarity has had lots of stock issued and exercised. PNV has seen Chairman fork out large amounts of his dollars to buy stock in 2023. He did have one sale during this period. Neuren’s former director Dr. Trevor Scott also sold some Neuren shares at retirement. However there has also been plenty of management purchases.

There have been no sales of stock by Botanix management that I am aware of.

Who owns these shares: a comparison

Clarity has yet to have the big end of town hold large % of its shares. One can speculate and argue this is why the price has shot up but I wouldn’t be that cynical. Polynovo and Neuren have a common top 3 investors. We all saw what happened with PNV share price and Neuren’s SP is not fairing so well currently. It will be interesting to keep a watch of substantial holder notices for both company's in the future.

Botanix has largely flown under the radar of these giants and it is a very tightly held company with 17.3% ownership by management. Remembering Botanix and Clarity have both essentially been pre-revenue company's until now so they will not have the same investment appeal for large funds.

SUMMARY

My overall take-away is Clarity is certainly one to watch. I certainly would not have faith investing in the company in the short to medium term. Others clearly disagree and with a price target of $10.00 a share. If you invested 12 months ago you would have achieved a 568% return on your money. So excellent if you were lucky enough to ride this wave. Will it last? Time will tell.

I will watch with interest. I will stick with my measly yearly returns of 34-101% in by current biotechs which are revenue generating and growing at good cadence for now.

So whether there were some long lunches and nods and winks who can say. This is all my opinion, DYOR but a $1.88 billion market cap is certainly interesting. Hopefully the tech eventually helps to improve lives and I would consider buying if the technology passes phase III and if it ever hits a reasonable price.

Updating an old straw from one year ago. This is to keep track of Rhodotron numbers which is crucial in the production of Cu67 - not that anyone here is keeping track. But it is important visual to see Clarity's target geographies for therapy. Note that Cu67 has a half life of 2.5 days so just maybe Oz may be included???

This is the current number of Rhodotron deployments which hasn't grown in over a year (April 2024). Can't really say for sure if this really is a true picture or IBA has been too lazy to update their website.

Of course Australia is still behind the eight ball behind other developed nations such as Japan, Korea, Phillipines (??) and even China

Original content below for comparison

Clarity Pharmaceuticals Webinar Nov 22

https://www.youtube.com/watch?v=_9G8Gyjx-TI

At the 9 minute mark there is a discussion about using Cyclotrons to produce Cu-64 and Rhodotrons for Cu-67

All in all, not the disaster that Telix and myself made it out to be in the previous straw that copper isotopes are hard to find. And If they were hard to find, then FDA trials would be much harder to proceed.

ANSTO does have a cyclotron and a synchrotron. However, it looks most of the Rhodotrons installed are based outside Australia, the closest being in Singapore/Malaysia. Could see some share price upside if ANSTO decides to purchase a Rhodotron for local use.

Source: IBA industrial

Also have to note the IPO price was $1.40 so in the meantime the price could drag along the current range (0.8-1.00) for longer.

[held]

Doesn't look like Dr Alan Taylor is participating in the latest placement.

And non exec director Dr Christopher Roberts also did not take any recent placement

Also long termer TM ventures not taking any of the insto placement.

Maybe a clue that I should not take the retail placement?

Maybe the bears will be proved right and this is overvalued

[held]

David Williams who is chairman of PolyNovo pens a few thoughts on Clarity Pharma

Full version from the AFR behind the paywall:

I'm still considering whether to take the entitlement.

[held]

Why picking ASX biotechs is mostly for the crazy brave

Tom Richardson

3 April 2024

The Australian Financial Review

Sharemarket It's a space with a reputation for rollercoaster returns, but some investors get really lucky, writes Tom Richardson.

The Australian biotechnology sector has produced massive winners such as the $140 billion blood products giant, CSL, but is also notorious for its unnerving volatility and costly clinical trials.

The ASX has 171 companies in the healthcare sub-sector, 85 in the pharmaceuticals sub-sector and 39 in a biotech sub-sector. Aside from gems like CSL, it is a space with a reputation for rollercoaster returns and outlandish claims about "breakthroughs" that never materialise.

Hugh Dive, the chief investment officer at Atlas Funds Management, says picking biotech winners is tricky because each company is underpinned by inherently complex science. "So much rests on understanding the science, so you get a very binary outcome - either it works fabulously, or it goes to zero," he says.

"Unless you have extreme specialisation in an area, it's hard."

Dive points to CSL's recent setback with a drug known as CSL112 to treat heart attacks, as an example of how failure can occur despite positive market expectations and a $1 billion investment by an already wildly successful company.

On the other hand, one of the sector's biggest recent winners is $4.1 billion cancer diagnostic radiotherapy group Telix Pharmaceuticals. The stock is up 1453 per cent over the past five years and has added 1880 per cent since its November 2017 float price of 65¢. It was trading around $12 yesterday.

Biotech investor David Williams, who runs corporate advisory firm Kidder Williams, says Telix's success shows Australia's radio pharmaceuticals sector is "hot as Hades" in producing huge winners like Telix and Sirtex. Sirtex, which is best known for its technology to fight last-stage colorectal liver cancer, soared on the ASX before snaring a $1.9 billion takeover bid in 2018.

"I got China Grande [China Grand Pharmaceutica] to take 8 per cent of Telix about a year-and-a-half ago when it was worth $300 million, and now it's worth more than $3.5 billion," he says.

"Now I'm an investor in [ASX-listed] Clarity Pharma. It has a radiotherapy product for pancreatic and prostate cancer. The testing in humans is unbelievable, so it's gone from almost nothing to $800 million and [I think it] will be $5 billion someday soon."

Since listing on the ASX in August 2021 at $1.40 a share, Clarity's value has climbed 96.4 per cent to $2.75 a share, with backers including Mr Williams, former Cochlear chief executive and Clarity director Chris Roberts, fund manager Firetrail Investments and KKR-backed cancer care provider GenesisCare.

"It may sound funny, but third-party endorsement adds to a biotech's credibility," says Dive. "The presence of large corporates or well-known fund managers on a company's share register is one form of endorsement we look for, especially the multinational fund managers with vast teams of analysts."

Williams says he targets biotechs with a disruptive product that could work as a platform technology across multiple applications. He says burns treatment specialist PolyNovo, a company in which he is both investor and chairman, is an example of a rare platform technology success as the product is now used by surgeons for applications other than treating burns.

"In Australia, there's about 150 pure biotech companies listed, but 95 per cent of them have never done anything, I guess 20 per cent will fail before June," he warns. "Lots have just spent 10 years testing on mice, recycling themselves, and paying themselves.

"So you better make damn sure a company has a viable product, you've also got to raise money, there's plenty about, but you need someone who knows what they're doing, and you need great executives to run it."

He says some biotechs may get lucky if they invent a product that becomes popular for an off-label purpose. "Take botox," he says, "people take that now and go, holy shit, this is great, and Ozempic was supposed to treat diabetes but is taken for weight loss."

The S&P/ASX 200 Health Care Index, which comprises leading medical and biotechnology businesses, has gained 1 per cent over the past 12 months, versus a return of 9.3 per cent for Australia's flagship S&P/ASX 200 Index over the same period.

However, one speculative biotech that has thumped its peers and the broader market is Opthea. The biotech is running two large clinical trials in patients to develop a therapy to treat common eye diseases.

The stock has swung wildly over the past five years, with the company boasting around $150 million cash on hand as at December 31.

Gerard Satur, chief executive of MST Financial, says Opthea is among his top picks for success, alongside neuroscience success story Neuren and neurodegenerative researcher Alterity Therapeutics. "You have to be very selective to invest in biotech stocks on the ASX, there are too many stocks we believe do not offer attractive risk-return as an investment," says Satur.

"We have the largest healthcare research team in the market, we do thorough due diligence on companies like Opthea, which we like because it has the potential to be the first drug for wet AMD [age-related macular degeneration disease] in more than 15 years.

"The divergence between good and bad is massive in biotech. We turn away a lot more companies than we cover for research as we just don't feel like they should take investors, and we hate it when companies spruik too much."

Satur says the returns are lucrative if an investor manages to unearth a winner and a successful company can raise a lot of capital if necessary in Australia. "Regularly there can be five or 10-baggers," he says. "And there needs to be, as there's risk with biotech." A 10-bagger is an investment that appreciates in value 10 times its initial purchase price.

Ultimately, the speculative nature of the sector means it is an "avoid" for Dive as the risk of permanent capital loss is too great. The stock picker says he prefers to focus on established, profitable players such as CSL or Sonic Healthcare, but that should not preclude others prepared to take more risk.

"Often with small biotechs you hope they get taken out by big pharma companies that write a cheque if the tech is good, so sometimes you get takeovers and the rewards," says Dive.

"But it takes vast amounts of time and money to get a biotech through the hoops. And probably the most crucial thing is how much cash runway a company has, so if it's burning tonnes of cash and doesn't have much in the bank, you're probably facing a highly dilutive capital raising or worse.

"If the capital markets are unfriendly, the company may run out of cash prior to their therapies being approved, or may be unable to fund the next stage in the testing process."

Always get the feeling that retail is last in the queue

Retail gets one share for every 33 held at around $2.50

First it was Dimerix and now Clarity. Wonder if this is always like this in biotech land?

Not known how much the proportion of the 20.6m going to costs of the offer (ie: Bell Potter)

Not known how much the proportion of the 20.6m going to costs of the offer (ie: Bell Potter)

The raise was always going to happen soon, given only 40m left from the last report which is a few quarters of cash.

Given the breakdown above and the lofty market cap compared to the small recruitment target in the SECuRE trial (see my previous straw) will give this a pass for now and see if the shares I don't take up get sold at a lower price.

I also need to spend time going through some of the recent takeovers by Big Pharma but I believe most of those (Fustion, Point, RayzeBio) were more advanced in their trials and thus more attractive acquisition targets.

A takeover could be a long wait for Clarity.

[held]

You heard it first from me 2 weeks ago :)

https://strawman.com/member/forums/topic/8550

https://www.afr.com/street-talk/clarity-pharmaceuticals-preps-110m-raise-wilsons-on-the-tools-20240325-p5fex4

Street talk thinks the raise will be around $2.60 which was around the time those options were excised @ $2.50.

[held]

Table to visualise current progress of the SECuRE PSMA therapy trial

Cohort trial design and dosage below

Alternative table from the Wilsons Broker note

Data from the announcement "Clarity’s theranostic prostate cancer trial advances to multi-dose phase"

Cohort 1 result can be found in "Ann: Theranostic prostate cancer trial advances to cohort 2" 24th May 2023

So in summary 12GBq is most effective.

[held]

Received this note from Frazis Capital Partners for anyone not yet subscribed to his email updates

Clarity Pharmaceuticals

This is the most exciting company I’ve come across in Australia lately. Clarity has been steadily releasing data from patients treated with their copper therapies with late stage prostate cancer.

Clarity has been on a bit of a tear lately. If their data continues to hold, this is still early days, and it remains a fraction of the value of recent acquisitions in the space with early stage data.

I will send out a note on the space shortly.

Current players include Novartis, which entered the space through their US$2 billion acquisition of Endocyte, Lantheus, which offers a radiodiagnostic, and Telix which is rapidly gaining diagnostic share from Lantheus. The whole space itself is growing fast and expanding into new areas.

M&A activity has been intense.

Two days ago Bristol Myers Squibb bought RayzeBio for US$4.1 billion, with early stage data for their alpha-particle emitting Actinium-based radiotherapy targeting gastroenteropancreatic neuroendocrine tumors. The company is enrolling patients in a Phase III trial.

And Novartis paid $2 billion for Endocyte in late 2018 with only Phase II data. This has proved a big winner, with first year revenues for their first product Pluvicto forecast at over US$1 billion.

Point Biopharma, in partnership with Lantheus, was itself bid for by Eli Lilly for US$1.4 billion - again with only Phase II data. Last week Point’s data came in a little soft, leaving open space for new entrants like Clarity.

This is going to be a large market. In prostate cancer, the trend is towards increased monitoring and (where possible) fewer surgeries and hormone therapy, which involves the unwelcome side effects of incontinence, impotence, low testosterone and depression.

These companies are focused on heavily pre-treated patients. But the hope is that these targeted treatments, with their milder side effects, will move further up the treatment timeline, which could double or even triple industry revenues.

This will take time, given the high hurdle for changing standard-of-care, but is looking more likely than ever today.

In the meantime, a steady rise in the incidence of prostate cancer, combined with an increase in monitoring, suggests the market will expand significantly regardless.

In a space where companies with promising data are being acquired for billions of dollars, and Clarity’s early indications look best-in-class, the company’s post-runup US$340 million valuation looks cheap.

And just today (28 Dec 23) the share price reached an all time high of $2 before settling back down to $1.89

I presume the rally was on the back of coverage from this email update.

Michael Frazis of Frazis Capital Partners is known for ignoring financial metrics in favour of more unconventional measures of customer satisfaction, loyalty, addressable markets and ideas that involve cutting edge technology and science. His style is more inline with ARK invests Cathie Wood

For the record, I'm not as enthusiastic as Frazis on the growth of the PSMA market, I think the rise of drugs such as Ozempic could slow the rate of growth in Prostate Cancer and the underperformance from Lantheus and Telix is evidence of this. Frazis could be just a victim of wanting to catch the CU6 uptrend late in the cycle while ignoring his bad call on Paul Hopper's Radiopharm Theranostics.

[held]

CU6 has really been on a tear recently

Apart from the latest report from Wilsons shared by @Bear77, there was also an earlier update on the SeCURE Therapy trial for Cohort 2. Although there were only results from 3 patients, the update on page 1 looked promising but as usual I brushed it off

The more significant part is on page 2 where I have highlighted the update where patients has had radiogland therapy with not much success but has showed progress in the SeCURE trial

While the radiogland therapy is not named, we can probably guess that the one they could be referring to is either Novartis (Pluvicto) or maybe others from Lantheus (can't think of the name) or Telix (TLX591)

In either case, the news seems significant enough to justify the current rise.

However this is still early stage with only 3 patients tested (cohort 2). And still a "science experiment" with no revenue till 2026 and why I've held back on putting any more in CU6. Seems fairly priced now.

[held]

Interesting to see Clarity getting bid today.

There was a Bell Potter conference a few days ago

Milestones to look out for

[held]