Consensus community valuation

07-March-2024: Cyprium-Metals-Shareholder-Update-and-Presentation.PDF, slide 4:

Source: Money of Mine podcast, 07-March-2024: The boys discuss the CYM update and this slide in particular.

Some Background:

- During 2016, Metals X Limited (MLX.asx) acquired the Nifty copper mine through the acquisition of Aditya Birla Minerals Limited.

- In late 2016, Metals X (MLX) demerged (or "spun out") its gold exploration business from its metals and mining businesses, and issued shareholders with shares in the new entity; Westgold Resources Limited (WGX.asx). Eligible MLX shareholders received 1 WGX share for every 2 MLX shares they owned. (details here).

- In early 2021, MLX sold their Nifty copper mine and two other copper projects for a combined A$60 million, A$24 million of it in cash, to Cyprium Metals (CYM.asx). From commencement of production in 1993 to the placing of the mine into care and maintenance in 2019, Nifty had produced in excess of 700,000 tonnes of copper metal. It was closed down in 2021 when they sold it, and it remains closed down today, although CYM still plan to restart it.

- The sale of Nifty and the other MLX copper assets to CYM was announced on 10-Feb-2021 and completed on 30-Mar-2021. MLX said at the time that the sale of their Copper Assets underpinned the Company’s strategy to focus on the development of their Tin Portfolio. The funds received were put towards MLX's working capital and to reduce their debt at the time.

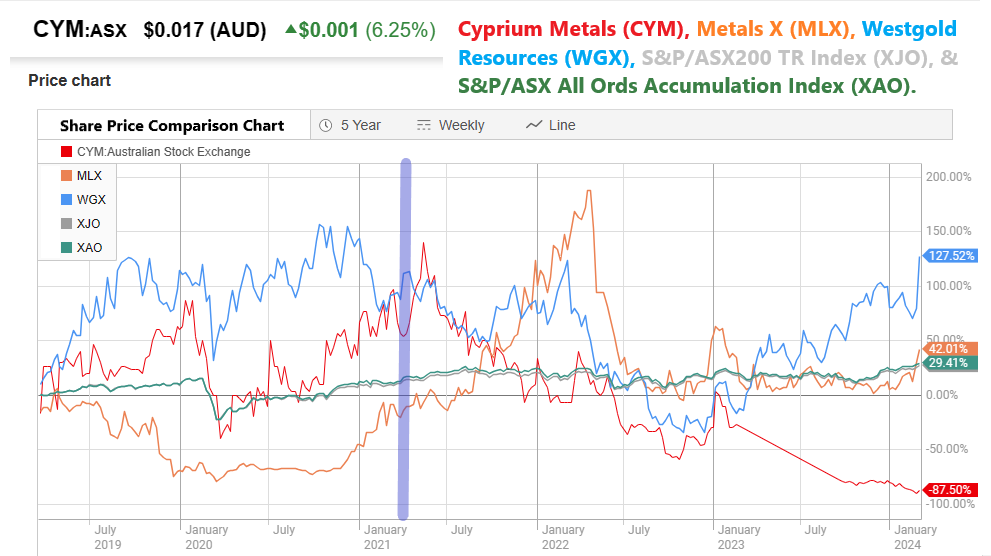

- On the following share price comparison chart, the date of that copper asset divestment - out of MLX - and into CYM - is shown by that vertical purple line in March 2021:

- What we can see from March 2021 onwards is that CYM had an initial pop and then went into a long and sustained downtrend, and they're now trading at less than 2 cents/share (cps) - they were over 20 cps in March 2021 when this deal was announced and spiked up to 32.7 cps on 17-May-2021; MLX had a great run, putting on about +190% by April 2022, but are now just ahead of the All Ords (XAO, +29.41%) and the ASX200 TR Index (XJO, +27.07%) over the full five year period - with MLX doing a little better than those indices since March 2021.

- Westgold is a little ahead now of where they were in March 2021, however they've put on +127.5% over the full five years (since March 2019) vs MLX @ +42% and CYM being down -87.5%.

- It's probably fair then to assume that gold has done reasonably well over the period, and tin hasn't done too badly, although it's been a bit of a boom & bust scenario with MLX, their SP now being back to not too far ahead of where they started both 5 years ago and also 3 years ago when they went 100% into tin, so they haven't lost money - unless you piled in during the "boom" phase in mid-to-late '21 through to April/May '22.

- There are a few more things that happened with Cyprium Metals (CYM) in the past year and a bit; starting with a trading halt on 21-Feb-2023, which rolled into a trading suspension on 23-Feb-2023 with the news that their debt funding package for the Nifty copper mine restart had fallen over: Nifty-Copper-Project-Restart-Financing-Update-23Feb2023.PDF

- That trading suspension lasted for 7 months, until 21-Sep-2023. During that 7 months there were a number of updates, board and management changes and funding attempts, including some successful capital raises, with the following ones probably being the most significant:

- Cyprium-Metals-Update-24Mar2023.PDF

- CYM-$24M-Placement-and-$5-Entitlement-Issue-12July2023.PDF - this one was the one that brought in private equity firm Pacific Road Capital Management (PRCM) who subscribed for $4.05 million in the Placement to hold a 9.9% interest in the Company post Placement; CYM also noted at the time that PRCM would have the right to appoint a nominee to the Company’s board of directors.

- CYM-$316M-Equity-Raising-Completed-18Sep2023.PDF - that was the final CR that allowed the reinstatement to official quotation (CYM trading again after 7 months of being in a trading suspension). Details of this CR included a $24M Placement to Sophisticated and Institutional Investors, a $5M Entitlement Offer that closed oversubscribed raising $7.6M from book build and shareholder demand, a $21M (US$14.5M) Bridging Facility Completed in the prior quarter, Clive Donner, an experienced mining industry executive, appointed as Managing Director, private equity firm Pacific Road Capital Management (PRCM) stumped up $8.3M in the Equity Raising to hold a 15.5% interest in the Company, and Matt Fifield, Managing Director of PRCM, was appointed to the CYM Board as their Interim Chairman.

- On Feb 16th this year (around 3 weeks ago), CYM (Cyprium Metals) accepted the immediate resignation of their Managing Director, Clive Donner (see here: CYM-Board-and-Management-Update.PDF), and announced that Matt Fifield, their Non-Executive Chairman, had agreed to assume the role of Executive Chairman, effective immediately, while they searched for an appropriate successor to Clive to take on the MD role. I note that Cyprium do not have a CEO, only a COO, and their CFO is also acting in an interim capacity only - see here: https://cypriummetals.com/about-us/key-management-team/. Their previous CFO, Wayne Apted resigned as their Chief Financial Officer and their Company Secretary, effective immediately, on 12-Oct-2023, having performed those roles since 2019.

- And that brings us up to Thursday's Cyprium-Metals-Shareholder-Update-and-Presentation.PDF and that extraordinary slide 4 - reproduced at the top of this straw.

Looks very much like they are laying the blame on departed management and marking a new starting point in the sand, however I would point out that their lean 3-person Board - which is appropriately small for a tiny $24 million nanocap wanna-be miner, still has Gary Comb in it, who has been a NED of CYM since June 2019, so has been there throughout the Nifty debarkle. All of the other CYM board members and senior management appear to have been purged during the past year.

Also, Matt Fifield, who has only been with CYM since the capital raisings in the latter half of 2023, is now their Executive Chairman, and is also the MD of private equity (PE) firm PRCM (Pacific Road Capital Management) who own or control 17% of CYM's SOI (shares on issue) and are CYM's largest shareholder. PRCM is a PE group who have a few associate companies, including FF Hybrid, L.P and GP Recovery Fund LLC (together referred to as “Flat Footed LLC”) and that 17% of CYM's SOI may be technically held by "Flat Footed" but PRCM has an arrangements that grants them the voting rights over that 17% regardless of beneficial ownership, so PRCM are therefore jointly recorded as having a 17% interest in CYM along with Flat Footed, but it's the same 17%, NOT a different 17%). See here: Change-of-Director's-Interest-Notice-29Dec2023.PDF - and here:

So - while that slide (top of this straw) is refreshingly honest in their acknowledgement of CYM's many failings with regard to ordinary retail shareholders, I'm not sure if they're going for a rallying call or instead trying to bring on a capitulation where ordinary retail shareholders are faced with the shocking facts around what a basket of steaming dogsh!t this company has become and decide to sell out finally. An even lower share price might actually suit a PE company like Pacific Road Capital, who could take this company private and then repackage it, put some lipstick on the pig, and sell it off at a good profit to what they've paid.

If you need any reminders of what private equity is capable of, see here: https://foragerfunds.com/news/dick-smith-is-the-greatest-private-equity-heist-of-all-time/

If you need any reality checks in relation to how large shareholders can bully smaller ones, drive down a share price and then take a company private to benefit themselves - look no further than Advance ZincTek, formerly known as Advance NanoTek, and also formerly known as Advanced Nano Technologies Limited - ANO - ANO - Takeover (strawman.com) and earlier when people were thinking that Lev hoovering up shares could only ever end well: ANO - Advanced Nano Technologies Ltd General Discussion (strawman.com) (last post was over two years ago in that second forum thread at this point in time)

It will not end well for ordinary retail shareholders, IMHO.

Further Reading:

Nifty Copper Mine history:

Copper – Nifty Copper Operation – Metals X Limited

https://cypriummetals.com/wp-content/uploads/SamsoInsightsTheNiftyCopperMineAForgottenGemInThePattersonRange13Mar21.pdf [March 2021] This was a well researched bull-case report, but the assumptions made didn't play out as expected.

Nifty Copper Mine – Cyprium Metals Limited

CYM:

CYM-Quarterly-Activities-and-Appendix-5B-Cash-Flow-Report-Dec-2023-Qtr.PDF $4.79m/qtr cash burn. $22.59m of cash and cash equivalents as at 31-Dec-2023.

ANO:

Intention-to-Make-Takeover-Bid-ANO-October-2023.PDF

ANO-Response-to-ASX-Aware-Letter-02Feb2024.PDF

ANO-Ankla-Takeover-Offer-Closes-07Feb2024.PDF