Consensus community valuation

Scroll Down - latest update is at the bottom:

My 21-Jan-2020 12-month PT was $27.72. Old one was 22.77. Data Centres. Cloud Services. Cybersecurity. Customer Service Focus. Very high management ownership. Lots to like!

The MAQ SP is now double my original $22.77 price target, and well above my latest $27.72 PT. I think they are riding the cybersecurity and data centre megatrend wave currently, and there could be a pullback. They may have run too far too fast.

22-July-2020: My new 12-month price target for MAQ is $40, below the $46 level they are at currently, but if they go higher, I'll take it. I do hold MAQ shares. Realistically, they could pull back from here. But I have in the past sold out too early, so I'm just trimming my position up here and letting the rest run. Just because a company looks expensive does not mean they won't get even more expensive when they are in a hot sector.

Update: 17-Dec-2020: And that's exactly what happened. They just kept getting more expensive. There's no denying that MAQ are a great company that is very well run by two brothers with a massive amount of skin in the game (David and Aidan Tudehope own 54.63% of the company), however I don't know if they are worth over $50/share... Anyway, let's call this a momentum trade, and I'll make a not-very-brave forecast of $55 within 4 months, and $60 within 12 months. However, this is definitely a price target, not an intrinsic valuation. Same as my $330 PT for CSL. I think they'll get there, however I'm not sure if they're really worth that much... They'll get there because of the quality premium in the share price, and in MAQ's case, because they're in a hot sector - in fact TWO hot sectors - being (1) data centres (and cloud computing) and (2) cybersecurity. I do hold MAQ shares, however I've been trimming the position as they've been steadily rising, to lock in profits while still maintaining exposure.

18-June-2021: $60 is still OK for a PT (price target) for MAQ. Since I set it 6 months ago MAQ has mostly trades between $50 and $54, and the lowest they dropped to was $44.70 very briefly in March. So $60 isn't too much of a stretch. They are operating in a good space, and they are very good operators within that space, so I'm still a happy MAQ shareholder and I believe there is further upside from here. I would not be buying any more MAQ up here, but I did say that at much lower levels also.

12-Jan-2022: Update: Just got sent home from work as I'm deemed a close contact of someone who has tested positive for Covid-19. My RAT returned a negative result, so I have not got it myself, but I have to isolate at home for 7 days now and get paid for it, and take another RAT on day 6 (next Tuesday). I'll take it!

Perfect! OK, I'm raising my PT (price target) for MAQ, since they've been trading above my old one for the last 6 months. They look like they are struggling to push through $80, and they do look like they've got way too much upside priced in up there to be honest, but I think they can settle a little below $80, such as at $77, once they provide us with their next report, or otherwise announce some new decent data centre contracts.

I feel that MAQ get overlooked most of the time when people are considering DCs, cybersecurity and cloud computer services (web hosting, etc.), but they have a good presence in the space, and are doing very well.

I was originally attracted to the company by the founders (the Tudehope brothers, David and Aidan) still being heavily involved in the management of the company - David Tudehope is an executive director and MAQ's CEO, and Aidan Tudehope is also an executive director and their Managing Director- Hosting Group. They also each speak for just over 11.6 million MAQ shares, which is worth around $787 million at today's closing price of $67.90/share. Part of that 11.6 million shares that each of the Tudehope brothers control is their family company Claiward Pty Ltd, which holds 11m of those shares (just over 51% of the company). Plenty of skin in the game!

Macquarie Telecom also have/had a Danielle Tudehope listed as a Senior Vice President based in the USA, and I think she is their sister, but I'm not 100% on that, could also be a daughter of one of them; She doesn't show up in the Annual Report. She may no longer work for MAQ.

Further Reading:

AFR Story: Rich Lister David Tudehope on the keys to success (afr.com)

How Macquarie Telecom Group creates the world's best customer experience - UNSW BusinessThink

History: Macquarie Telecom Group: Cloud hosting, voice, mobile & data services

(10) David Tudehope | LinkedIn

(10) Aidan Tudehope | LinkedIn

FY21 Annual Report: https://macquarietelecomgroup.com/wp-content/uploads/2021/10/MT_AnnualReportPT_FY2021.pdf

Excerpt from David Tudehope's "Chief Executive’s Message" from the 2021 Annual Report (on page 8):

"Seven consecutive years of profit growth reflects our commitment to our purpose of making a difference in markets that are underserved and overcharged, and our consistent strategy of investing in the growing data centre, cloud and cyber security markets.

"During FY21, we successfully completed development of Intellicentre 3 East and Intellicentre 5 South Bunker on budget.

"In FY22, the Group plans to make significant investments of between $121m and $133m primarily in our Macquarie Park Data Centre Campus, as well as for new cloud and cyber security platforms to enable growth.

"We are investing in Macquarie Data Centres’ staffing and technology to support our leading corporation contract win and continued growth, as well as investing in the fit out of two floors of IC3 East. We expect billing for the leading corporation contract will commence in the second half of FY22. The Australian Government has named Macquarie’s data centres as Certified Strategic, a designation meaning we are able to provide the highest level of security compliance available to support government data. In combination with our 200 Australian Government security-cleared specialists, Macquarie Government is well positioned to meet the cyber security and cloud needs of government agencies.

"We are investing in new staffing to drive growth in cyber security in our Government and Cloud Services businesses.

"Macquarie Cloud Services has shown strong revenue and profit growth through a hybrid offering that allows customers to utilise the cloud that is best fit for their software applications, whether colocation, private or Azure public cloud. We believe that their new cyber security offerings will complement this and drive further growth with corporate customers.

"Macquarie Telecom has seen continued strong demand for SD-WAN and new SD-LAN technologies that allow customers to monitor and optimise their site based network performance and utilisation with AI technology.

"Our outstanding customer experience, which is at the heart of our Company purpose, has been even more important to our customers as they rely to a greater extent on telecom, data centre and cloud services whilst their staff are predominantly working from home.

"In August 2021, we announced plans for Intellicentre 3 Super West, a new data centre which takes the Macquarie Park Data Centre Campus to 50MW IT load over time. This global scale campus will attract investment from multinationals looking to expand into the Asia Pacific region, appealing to both hyperscale and SaaS customers."

--- end of excerpt ---

So I hold MAQ here on SM and in RL - first added (in RL) at $15.20/share in late 2017, then bought more at $15.05 about a fortnight later in early Jan 2018, then bought more in March 2020 at prices ranging from $22.90 to $23.11/share. I've trimmed the position 3 times on the way up. As I said before they've been as high as $82/share on 31-Aug-2021, but I didn't managed to trim any way up there. They were only there for a day. They were a pretty small company when I bought my first MAQ shares, but they're a $1.5 billion company now. $77/share sounds good to me.

05-Mar-2023: Update: I have posted a straw (see below this valuation) regarding MAQ's excellent H1 of FY2023 results. They've been over $80/share, and they're going back there at some point. Meanwhile, happy to stay with my $77/share PT.

27th August 2025: Update post-FY25 Results:

MAQ-Full-Year-Results-Announcement.PDF

Full Year Results - Investor Presentation

Low growth, but still growth, and more profit growth on less revenue growth is good growth. EPS was flat. Nothing too exciting. Hence the market's muted response.

https://www.macquarietechnologygroup.com/investors/

https://www.macquarietechnologygroup.com/about-us/

https://www.macquarietechnologygroup.com/

Disclosure: Holding here on SM, was holding in my SMSF, sold them to buy something else a few weeks ago when they approached $70/share, having previously bought back in at closer to $60/share.

Not shooting the lights out, but good management with plenty of skin in the game - the Tudehope brothers own 41.32% of the company in their private investment vehicle, Claiward Pty Ltd (10,650,990 MAQ shares). David and Aiden Tudehope continue to run this business as owners, which is hardly surprising considering they do own almost half of MAQ.

Cybersecurity. Data Centres. Cloud Hosting Specialists. Heaps of Government clients, particularly in Canberra and Sydney. Lots to like!

Market Cap at $66.11 of $1.7B

Mangement Bios

Peter James, Chairman

Peter has extensive experience as Chair, Non-Executive Director and Chief Executive Officer across a range of publicly listed and private companies particularly in emerging technologies, digital disruption, e-commerce and media. He is an experienced business leader with significant strategic and operational expertise. Peter travels extensively reviewing innovation and consumer trends primarily in the US, Asia and the Middle East. He is a successful investor in several Digital Media and Technology businesses in Australia and the US. Peter holds a BA degree with Majors in Business and Computer Science and is a Fellow of the Australian Institute of Company Directors and a Fellow of the Australian Computer Society. Peter joined the board on 2 April 2012 and was appointed Chairman of Macquarie Technology Group in July 2014. Peter is the chair of the People, Remuneration and Culture Committee and a member of the Audit and Risk Management Committee. Peter is also a non-executive director and Chairman of Nearmap, Droneshield, Halo Food Co and Ansarada.

David Tudehope, Chief Executive

David is Chief Executive and co-founder of Macquarie Technology Group and has been a director since 16 July 1992. He is responsible for overseeing the general management and strategic direction of the Group and is actively involved in the Group’s participation in regulatory issues. He is a member of the Australian School of Business Advisory Council at the University of NSW and was a member of the Australian Government’s B20 Leadership Group. David is a member of the Australian Government’s Cyber Security Industry Advisory Committee. David holds a Bachelor of Commerce degree at the University of NSW. In 2018, David was named Australian Communications Ambassador at the 12th Annual ACOMM Awards. In 2020, David was named CEO of the Year at the World Communications Awards in London. In 2023, David was awarded the Pearcey Medal, the Australian ICT industry’s highest award.

Aidan Tudehope, Managing Director, Hosting

Aidan is co-founder of Macquarie Technology and has been a director since 16 July 1992. He is the Managing Director of the Hosting Group (Cloud Services & Government and Data Centres) with a focus on business growth, operational efficiency, cyber security and customer satisfaction. He leads the Government business unit, encompassing Macquarie’s Secure Government Cloud and Cyber Security offerings. As the former Chief Operating Officer for Macquarie Technology, Aidan played an integral part in the strategy and direction of the Hosting business since its first state-of-the-art data centre, Intellicentre 1 opened in 2001, as well as being instrumental in the development of Macquarie Technologies data networking strategy. He holds a Bachelor of Commerce degree. In 2023, Aidan was awarded the Pearcey Medal, the Australian ICT industry’s highest award.

Lisa Brock, Non-Executive Director

Lisa Brock joined the board on 31 January 2023. She is the chair of the Audit and Risk Management Committee and a member of the People, Remuneration and Culture Committee. Lisa brings more than 20 years’ experience to the Company in business leadership, commercial strategy, corporate finance and infrastructure. She has held a number of senior executive positions at the Qantas Group and is currently a non-executive director at Adelaide Airport. She holds an Honours Degree majoring in Mathematics from the University of Birmingham, UK and a Master of Applied Finance from Macquarie University. She is a Graduate of the Australian Institute of Company Directors and a Member of the Institute of Chartered Accountants in England and Wales.

Adelle Howse, Non-Executive Director

Adelle Howse joined the board on 29 August 2019 and is a member of the Audit and Risk Management Committee and the People, Remuneration and Culture Committee and takes a lead role for Investment reviews. Adelle has extensive executive and non-executive experience in the corporate environment and provides consulting services with a focus on strategy, M&A and governance. She has spent more than 20 years in energy and resources, construction, infrastructure, data centres, telecommunication and property sectors. Adelle is a non-executive director of the Sydney Desalination Plant, an independent non-executive Director of Downer EDI Limited and BAI Communications. She holds an Executive MBA from IMD, a PhD in mathematics from the University of Queensland and a graduate diploma in applied finance and investment. Adelle is a graduate of the AICD.

Macquarie Technology Group (MAQ) reported last week. From their presentation:

Overall a decent result. Somewhat muted increase in revenue and EBITDA as was flagged at the AGM and at the previous full year results.

Data Centre revenue increased which is the highest margin segment of the business. Although this margin was impacted by development activities related to the potential acquisition of a new data centre site in Sydney. Otherwise EBITDA margins would be 50%+.

No change to the outlook provided in terms of the development of IC3 Super West. The 1st part of construction is expected to be completed in Q3 2026 at a cost of $350m with an expected 6MW of IT load available. The total load for IC3 SW has also been increased to 47MW.

MAQ remains fully funded so far with an undrawn debt facility of $450m available and around $91m in cash on the balance sheet.

Disc: Held IRL and on Strawman.

Macquarie Technology Group (MAQ) reported last week. I know @raymon68 has already posted the results so this is more for me to journal down my thoughts on the result.

From their presentation:

Overall I thought it was a solid result albeit EBITDA was more on the lower end of guidance.

Not much changed from last report. Data Centre EBITDA percentage slightly down on last half.

Main thesis for MAQ is the continued growth in its data centre segment which is the segment with the highest margins. MAQ currently has around 23MW of data centre load across 3 sites:

- IC1 (Sydney CBD) = 3MW

- IC2, IC3 east and IC3 super west (Macquarie Park) = 10MW (IC2)+ 8MW (IC3 E)

- IC4 and IC5 (Canberra) around 2MW

Future development of IC3 SW is due to start soon and when complete will bring the total capacity to around 68MW.

Outlook was somewhat muted considering IC3 SW has been part of plans for a while now. MAQ expect that the first phase will be online around 3Q 2026 bringing an extra 6MW of capacity. I guess the market probably also didn't like the fact that MAQ expect growth rates in the Cloud and Government segments to slow in the coming FY.

Overall capex is expected to be higher than previous years considering the need to spend to build IC3 SW. Currently MAQ have no debt but there is a loan facility of 190m which I do expect them to tap into otherwise they'll need to do another raise in the next year.

With D&A expected to be slightly lower than FY24, and EBITDA is continue to increase, I expect that NPAT may gain slightly or may be flat based on how much interest costs will be.

Considering we are only just entering the growth phase for MAQ, I will give them some leeway in terms of their financial metrics as I see this being a much bigger business in 5-10 years time once their new data centres are all up and running however it does make this business quite hard to value at the current stage.

A thesis breaker would involve further delays in the development of IC3 SW or a complete blow out in costs involved to build out the centre. So far, apart from delays, it seems that management have fairly good capital management and I trust that this should continue into the future.

Disc: Held IRL and on Strawman.

- Release Date: 28/08/24 19:07

Key Points

• Ten consecutive years of EBITDA growth. • Group Earnings before interest, tax, depreciation, and amortisation (EBITDA) of $109.1 million, an increase of 13.9% over the last 3 years.

• Conversion of EBITDA to operating cash flows generated total operating cash flows of $117.8 million during the year. Strong 103.8% cash conversion of EBITDA into operating cash flows, after excluding tax received and interest.

• Completed acquisition of 17-23 Talavera Rd, Macquarie Park for $174 million plus transaction costs, including a $90 million loan note from the vendor.

• Successful institutional investor capital raising of $100 million to support acquisition of 17-23 Talavera Rd, Macquarie Park.

• Capital expenditure was $51.1 million before acquisition of Macquarie Park driven by Growth Capex of $24.0 million,

Customer Related Capex of $18.5 million and Maintenance Capex of $8.6 million. Chief Executive David Tudehope said, “The acquisition of the Macquarie Park Data Centre Campus land, along with the $100 million equity raise, has positioned us for the growth of our digital infrastructure platform for the years ahead.”

Macquarie Technology Group (MAQ) released results after hours last night. From their presentation:

On the surface seems a pretty good result. Increasing costs have put pressure on margins but they have remained fairly strong.

The Data Centre business once again doing well and this is the growth driver in this business.

Interesting though that most of the EBITDA growth was driven from the telecom business which isn't considered one of the growth segments of the business. The decrease in Cloud Services and Government EBITDA was flagged at the last report due to increased investments and timing of sales.

Outlook was given with particular focus towards the new IC3 Super West Data Centre which has been a long time coming. Works have commenced and expected to be completed in Q3 CY26. This will increase the data centre load from 22MW currently to 60MW with further capacity to increase this to 67MW.

MAQ management have historically been pretty good capital allocators so hopefully this new build can be funded from the profitability of the existing segments of the business without the need for further dilution.

Disc: Held IRL and on Strawman.

Macquarie Technology Group released their results after hours yesterday, from their presentation:

Once again operationally a very solid result with continued growth in all segments of the business.

Data centres now comprise 11% of total revenue but amazingly contribute 32% towards total EBITDA. The slide below shows the incredible margins of the data centre business:

Telecom revenue actually declined compared to FY22 however EBITDA increased due to operational efficiencies. Long term I don't see telecom being a major segment of the business but it is profitable at present and does contribute 20% towards overall EBITDA.

Capital expenditure which was forecasted to be $76m-$80m ended up being $65.8m. I suspect this may be due to ongoing delays with their IC3 Super West build which has once again been delayed. IC3 Super West was due to be approved mid 2023 but is now expected late calendar 2023. The build will also now take 30 months, up from 18-24 months from the last report. Total load of IC3 Super West has been upgraded to 38MW with potential to increase to 45MW if needed.

Outlook for FY24 was given:

As expected, Capex will increase in FY24 due to (hopefully) the build of IC3 Super West. On a cash flow level, they shouldn't have any issues given that they raised capital last year and repaid all of their debt. The company also generated free cash flow of around $43m (if you back out the cash they placed into Investment Accounts). There is still the potential to use the debt facility which has a capacity of $190m.

Doing some rough numbers based on their outlook. Say EBITDA grows to around $110m, then assuming around $58m depreciation, there is a potential for MAQ to generate NPAT of between $30-35m.

Disc: Held IRL and on Strawman

Macquarie Technology Group (ASX:MAQ) announced that they will be raising capital to fund further growth in their data centres business.

From their presentation:

Seems to be only an Institutional Placement with nothing for us private investors.

Maybe a little surprising that they are raising capital at this stage given that they still have $80m in undrawn debt facilities and $13m in cash. Although they did say that they will be paying down their debt at the last set of results. Perhaps taking the opportunity to reduce their debt with the cash raised?

FY23 outlook was also given in the presentation:

Total Depreciation and Capex are actually lower than previously forecasted. May be a short term boost to their overall profitability at the next set of results.

Full presentation here

Disc: Held IRL and on Strawman

Note: This is the same post as my $NXT Straw. I just also wanted it to appear on my #MAQ history. So please move along, if you've already seen the $NXT straw, as there is nothing new to see here.

$NXT reported results yesterday that were broadly well-received by the market. Expansions, site acquisitions for new data centres, and expectations of material new contracts supported this long term growth story. Analysts reactions are broadly positive, with no major moves to SP targets based on the updates so far. (Although GS tweaked down their 12m TP from $13.60 to $13.30)

I've had exposure to the data-centre theme IRL for several years ($NXT, $MP1) and continue to see it as a long term growth theme.

However, I have recently switched my RL position from $NXT to $MAQ, and I'll briefly explain here.

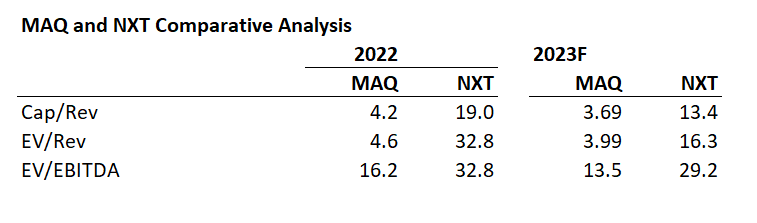

$NXT is a more agressive growth play, with 3-year revenue CAGR to end FY22 of 18% vs. 8% for $MAQ, and a 3-yr EBITDA CAGR of 26% vs, 19% at $MAQ. However, this is at the cost of significant debt, with long-term borrowings now reaching $1.26bn and interest for the last 6 months now up to $62m (annualised).

On a comparative basis $NXT is spending 32% of EBITDA on interest, compared with a more conservative 12% at $MAQ.

Furthermore, $NXT have recently signalled an intention to expand internationally, although we are yet to see what this means in practice. This further increases the risk profile.

Looking at valuation multiples, $MAQ is looking favourable, and I have initiated my RL position recently at $55.50 (2.75%). (I will follow today in SM, because strictly speaking these companies are "yet to prove themselves", which is my criterion for holding in SM.)

Table 1: Comparative Valuation Multiples

Source: www.marketscreener.com; Company Accounts

Overall, with interest rates still rising (and the real chance that peak forecasts will go up further) and with tech companies reducing investment in new storage, this sector may move from a focus on expansion to a greater focus on utilisation and profitability, with consequence implications for pricing.

Overall, while I like both $NXT and $MAQ, I consider that $MAQ is more defensively positioned given these risks. I have been watching it for several years, and with the SP below $60 I feel now is the time to switch horses.

$MAQ brings some other differences to $NXT as follows:

- It is founder-led, managed and majority owned

- The limited free-float means that it is not as easily accessible to institutions; however, liquidity is fine for a retail investor

- Its capital structure is different with a higher proportion of capital leases vs. owning real estate.

I don't often switch horses within a sector and, while I think BOTH companies will generate long-term shareholder value, I now prefer the risk-reward profile of $MAQ. So, out with $NXT and in with $MAQ.

Disc: $NXT - not held; $MAQ - held IRL (and later today on SM)

P.S. For those who follow Gaurav Sodhi, you'll recognise I have adopted his rationale. I have been aware of his perspective for well over a year, and on this occasion my analysis aligns with that story. You can look it up by watching back issues on "The Call" - just search for $NXT and $MAQ and pick the days when he the "talking head".

21-Feb-2023: MAQ released their results after the market closed (as they have done for a couple of years now). It's funny. If they were disappointing results, I'd probably be annoyed that they released them after the market had closed, but they're not, and I'm not, and they have form for doing this; their last full year results (for FY2022) and their last two half year results were all released after the market had closed.

Here's the first page of today's half year results announcement:

You can read the full announcement here: Half-Yearly-Report-and-Accounts.PDF (there is a second page, but I've also included that below if you keep reading.)

No dividend declared yet again, but as Buffet says, (and I'm definitely paraphrasing here) better for companies that need cash for growth capex to reinvest their profits at decent rates of return than to give it to their shareholders as dividends and then borrow money and pay interest on it. MAQ do both, reinvest their profits and borrow money for growth, but they've said today that in FY23 their debt will reduce. They give a fair bit of capex guidance on the second page and it looks like their spending is slowing down at last. Not that I've minded - they've spent well! Seventeen consecutive halves of profitable growth isn't something that most companies that not many people have heard of can claim. And, let's face it, Macquarie Telecom is not exactly a household name. Known mostly for data centres, cloud computing, cybersecurity and as a reliable business telco, they have a lot of government clients, including the ATO, and they tend to sail under the radar of most investors, even investors who are generally interested in those very areas.

MAQ has been trading at or just above $50/share of late, which is around their 12-month lows, so it will be interesting to see how the market reacts to this report in the morning.

MAQ-Half-Yearly-Report-and-Accounts-Presentation.PDF

Those returns shown on the right are capital gains (or a capital loss in TNT's case) over 5 years, and those numbers don't include dividends. If you add in Telstra's dividends it ain't going to get you up to MAQ's +255% return from TLS's +21% return. That's not annualised. That's your return at the end of 5 years if you placed the same amount of capital into those 4 companies. You'd get Telco exposure with TLS, you'd get cybersecurity with TNT, you'd get cloud storage (data centres) exposure with NXT, but you'd get all of that exposure with MAQ and heaps more capital growth as well.

MAQ has been damn impressive over the past 5 years that I've held them, and even since I added them here to my Strawman portfolio more recently (in 2019 and 2020, as shown below). I obviously hold more in real life than I do here on SM (the limitations of a $100K portfolio here mean my dollar weightings tend to look pretty small; a lot smaller than my real life positions). IRL my average buy price for MAQ was $17.38/share. Here it's $21.33/share. They've been as high as $80/share (in August 2021) and they're back down to $54 now. I think they go higher tomorrow on the back of this evening's report, all other things being equal.

Like I said, I can forgive them for not paying dividends for this sort of capital growth.

That 37.15% for my MAQ here actually IS annualised, so that's the money weighted annual return - +37.15% p.a. for the past three years.

I've done straws on the company before, so I won't go on, but they're a nice little growth story. Although their current market cap is $1.14 billion, so perhaps not so little any more.

Here's the second page of today's MAQ FY23 first half results announcement this evening:

Noice!

MAQ reported last month however I'm just coming around to reading through the results. And realised no one had posted a straw yet about their results. From their announcement:

- Eight consecutive years of EBITDA growth.

- Full year revenue of $309.3 million, an increase of 8.5% compared to $285.1 million for FY21.

- Earnings before interest, tax, depreciation, and amortisation (EBITDA) of $88.4 million, an increase of 19.8% from prior year, at the top end of June’s guidance.

- Conversion of EBITDA to operating cash flows generated total operating cash flows of $98.0 million during the year. There is a closing cash balance of $3.0 million and undrawn debt facilities of $64.0 million having drawn down $126.0 million.

- The Company has completed work on the fit-out of Intellicentre 3 East data centre development (“IC3”) and has commenced billing of its hyperscale customer.

- Net profit after tax (NPAT) of $8.5 million, reflecting the increase in depreciation & amortisation flowing from the significantly higher levels of capital expenditure since FY20.

- Capital expenditure for FY22 was $98.5 million (FY21: $139.1 million) driven by Growth Capex of $64.5 million primarily relating to fit out of IC3 East in Macquarie Park. Customer related Capex was $24.5 million. Maintenance Capex was $9.5 million.

On first glance the results are pretty impressive on an EBITDA level. Revenue increased by 8.5% but EBITDA increased almost 20% showing some operating leverage and scale. The breakdown of each segment and its contribution was also interesting. Data centres only comprised 8% of total revenue but contributed 31% of total EBITDA. Although capex (and future depreciation and amortisation) will also be high as they increase capacity.

Outlook:

- The Company’s EBITDA will continue to grow in FY23. Due to investments being made in Data Centres and Cloud Services & Government in the 1H FY23, EBITDA will grow in 2H FY23.

- Expected EBITDA for the Data Centres business in FY23 is between $31 to $33 million.

- Inflation impacts on cost base are being materially passed through to our customers.

- We continue to see a strong demand for cyber security and hybrid IT in our Government and Cloud Services businesses.

- Telecom is focusing on new initiatives to improve operational efficiencies and continued growth of our successful SDWAN business.

- Pleasingly we are able to increase the total IT Load capacity of IC3E by approximately 1MW independent of the IC3 Super West build. We will invest in this opportunity by 2H FY23. This leverages our existing investment in IC3E.

- State Significant Development Application submitted for IC3 Super West. We expect to receive DA approval in late calendar year 2022 to mid-calendar year 2023 and construction to be completed 18 to 24 months later.

- Depreciation and amortisation for FY23 is expected to be $70 to $74 million, driven by full year impact of IC3 in FY22. Cloud Services & Government and Telecom depreciation to remain broadly flat at $27 to $28 million and $19 to $20 million respectively in FY22.

- We are focused on maintaining industry leading Net Promoter Score greater than +70 across all business segments.

- The Company plans to make further investment in growth and customer growth capex during FY23. Total capex is expected to be between $76 to $80 million consisting of:

- Growth Capex - $37 to $39 million

- Customer Growth - $23 to $24 million

- Maintenance Capex - $16 to $18 million

- Telecom capex will remain broadly flat at $11 to $12 million in FY23 with Hosting capex at $65m to $68m.

Nothing too surprising in the outlook for FY23. Capex is expected to be lower than in FY22 but I expect this to accelerate again into FY24 and FY25 due to continued build out of their data centres.

Overall I think this was a decent result for MAQ. They are slowly building out a very strong cloud and data business and doing it whilst maintaining profitability. On a cash flow level they were also FCF positive for this year and although the cash balance appears low at $3m, there is plenty of loan facility available to utilise.

Disc: Held IRL and on Strawman

14-July-2021: IC3 Super West and Confirmation of Guidance

Plus: IC3 Super West Investor Presentation

Macquarie Data Centres: IC3 Super West - 50MW Campus

Macquarie Telecom Group Limited (ASX: MAQ) provides the following update to the market:

IC3 Super West

Macquarie Data Centres has today lodged a State Significant Development Application to build a new data centre at the Macquarie Park Data Centre Campus, within the Sydney North Zone. The new data centre will be called “IC3 Super West” and will be the largest data centre on the campus, adding 32MW of IT Load to bring the total campus IT Load to 50MW over time. IC3 Super West is designed to seamlessly interconnect with IC3 East.

Macquarie Data Centres is aiming to complete construction of Phase 1 of IC3 Super West in the second half of calendar year 2023. IC3 Super West has been designed to meet the needs of the corporate, government and wholesale markets and will enhance the state’s cybersecurity infrastructure and capabilities.

David Tudehope, the Chief Executive of Macquarie Telecom Group said: “IC3 Super West will expand our Macquarie Park Data Centre Campus to 50 MW of IT Load. This global scale data centre campus will attract new investment into Australia from multinationals looking to expand in the Asia Pacific region. The Macquarie Park Data Centre Campus will also be the home to our new Sovereign Cyber Security Centre of Excellence which is being launched today with the support of Investment NSW.”

Macquarie Data Centres is currently obtaining the necessary planning consents, which are expected to be received in early 2022. Construction and funding of IC3 Super West will then follow and remains subject to final Board approvals.

Sovereign Cyber Security Centre of Excellence

The Sovereign Cyber Security Centre of Excellence is an integrated mix of leading edge physical and virtual infrastructure designed to monitor and manage cybersecurity events. It will be monitored 24/7 by trained engineers equipped with the latest tools. The infrastructure and personnel will be housed in IC3 Super West offering a truly Australian sovereign solution to the growing cyber security threats.

David Tudehope, the Chief Executive of Macquarie Telecom Group said:

“NSW’s digital economy is rapidly growing, and this project will create world class infrastructure and valuable long-term jobs in the digital and cyber security sector.”

Confirmation of Guidance

The Company today confirmed that its FY21 EBITDA will be within the previously announced guidance of $72 to $75 million.

--- ends ---

[Disclosure: I hold MAQ shares.]

24-Feb-2021: 1H FY21 Results Announcement plus 1H FY21 Results Presentation and Half Yearly Report and Accounts

Macquarie Telecom delivers thirteen consecutive halves of revenue and EBITDA growth

Macquarie Telecom Group Ltd (ASX: MAQ) today announced its strong performance for the half-year ended 31 December 2020, in line with guidance.

Chairman Peter James said, “Our strategy of investing in Data Centres, Cloud and Cyber Security continues to drive further shareholder value and ongoing returns and has resulted in thirteen halves of profitable growth”.

“Macquarie’s focus on customer experience was recognised by the “Best customer experience in the World” award by 60 international judges. Macquarie is the first Australian company to win this award in 22 years of the World Communications Awards in London”.

KEY POINTS

- Revenue of $143.6 million, an increase of 9% on 1H FY20 ($131.9 million).

- Earnings before interest, tax, depreciation, and amortisation (EBITDA) of $36.4 million, an increase of 15% on 1H FY20 ($31.6 million).

- Conversion of EBITDA to operating cash flows generated total operating cash flows of $13.6 million during the half-year.

- Net profit after tax of $7.0 million, an increase of 5% on 1H FY20 ($6.7 million).

- Capital expenditure for 1H FY21 was $32.9 million (1H FY20: $23.1 million) excluding Intellicentre 3 East.

- Customer Growth Capex was $13.9 million, 20% more than 1H FY20 $11.6 million, reflective of our continued data centre sales success and product mix.

- The company has drawn down $93.5 million to support data centre developments in Intellicentre 3 East and Intellicentre 5 South Bunker.

Chief Executive David Tudehope commented, “Macquarie’s 20-year strategy of investing in world-class data centres is based on strong demand for data centre capacity as customers migrate to cloud and colocation services. The win, of the 10MW of IT Load sold to a Leading Corporation, recognises the world class investment we have made in the Macquarie Park Data Centres Campus in Sydney’s North Zone.”

OUTLOOK

- FY21 EBITDA is expected to be approximately $72 to $75 million.

- Telecom continues to win customers from legacy data and IP carriers with our nbn and SD WAN solution.

- FY21 Total Capex is expected to be between $57 - 66m, excluding IC3, consisting of:

- Customer Growth - $25 to $28 million.

- Growth Capex - $17 to $20 million.

- Maintenance Capex - $15 to $18 million.

- IC3 Expenditure - $123 to $126 million.

- FY21 Depreciation is expected to be between $50 and $53 million.

--ends--

--- click on the links at the top for more ---

[I hold MAQ shares. They don't shoot the lights out, although their share price has over the past couple of years. Their results however are just steady growth, and they are still building the company, particularly the data centres and the hosting (cloud services). Great company with strong tailwinds.]