Consensus community valuation

Feb-26

I was going to await the latest DAYBUE results from $ACAD (expected 1-March) before updating, but today's adverse EU news, moves my current view of value even further away from my previous SM valuation. So I will update my valuation as a placeholder to take accout of both 1) last year's data on US sales profile for DAYBUE and 2) today's news from EU, which adds to the Canada "do not reimburse" recommendation last year.

Placeholder: DAYBUE reduce to $10, add 50% to the p50 for NNZ-2591 gives $8 for a sum of parts valuation of $18, but with wide uncertainty.

Uncertainty is very wide. For example, in the downside case DAYBUE could be worth <$10 depending on longer term US persistency and ultimate market penetration. And, in the failure case, NNZ-2591 could be $0.

Feb-25

No change to valuation $24 ($12-$46). "Two-for-the-price-of-one" thesis intact.

Good progress on DAYBUE has probably reduced the likelihood of the downside cases, however, I will wait for clarity on the likely European trajectory before updating from the DAYBUE perspective, assume US hit guidance (so at least 12 months for that).

Aug-2024

See Valuation Straw $12-$46 based on acquisition multiples.

Wide range due to including NNZ-2591, which is still at Phase 2.

Sum of Parts

DAYBUE: $12 - $16 - $20

NNZ-2591: $0 - $16 - $32

SUM: Pick a number! Take p50 DAYBUE + 50% p50 NNZ-2591 ... to more heavily discount the development risk = $16 + $8 = $24.

I know its a bit sloppy, but hey, look at the assumptions I've made!

-----------------------------------------

Dec-2023 $31.00

Today's news on NNZ-2591 materially impacts the value of $NEU.

While I have not modelled NNZ-2591 explicitly, I have tweaked my existing DCF scenarios, which are based on 2 factors: $NEU revenue growth (x4 scenarios) and ultimate penetration of the Rett's market (x2 scenarios) - so 8 scenarios together.

Two sets of scenarios assume NNZ-2591 fails, and that $NEU revenues start to decline from 2029 and 2033. Given the now significantly increased likelyhood of NNZ-2591 leading to a second and even more material revenue stream, I have reduced the probability of these scenarios by half, from 35% to 17.5%.

I have also removed a valuation discount allowing for the emergence of a competitor to DAYBUE. The rationale being that NNZ-2591 success will start to drive revenue from 2026 in the success case, which is earlier than my model (2029).

After these updates, keeping everything else unchanged, the [p10, p50, p90] estimates of value are: [$16, $32, $50], as seen from the plot below.

I will do a more complete model rebuild when we have the Full Year result for DAYBUE and hopefully an update on the NNZ-2591 timeline, in February 2024.

(None of the scenarios consider the extreme upside case that NNZ-2591 ends up being approved for all four conditions. We have to seriously consider that, because the positive animal model effects seen in PMS have carried through to the Phase 2 human trials. There are positive effects in the other animal models - what if these translate? We're then looking at a completely different story. But, too early to evaluate this.)

Basically, with the SP today at around $22, I see a compelling risk-reward upside from here.

Disc: Held in RL (6.2%) and SM

I just listened to the JP Morgan healthcare conference that Acadia presented at and it is pretty positive for Neuren. The surprise was a longer dated sales target of $700m by 2028 for Daybue. This has some pretty significant flow on effects for NEU if it is achieved in terms of milestone payments.

Three scenarios -

1) sales increase in the US and they manage to exceed the $500m threshold for the next $50m payment. I think this is likely as the 2000 patients that have tried Daybue of a total US population estimate of 6000 potentials (up 10% from previous estimate). So probably somewhere around 3-4000 actual patient pool. No mention of Canada approval solutions, so probably not likely to contribute anything by 2028. They mentioned the investment in sales people was having a positive effect. But to me it seems unlikely that they will get to $>750m milestone ($100m payment) from the US alone so I think this will be the final milestone payment from the US for a while and maybe forever. So then they would transition to a steady $60m or so per year of sale royalties

2) A big chunk of these sales come from outside the US, as they expect Europe approval Q1 2026 and an extra phase 3 trial for Japan will be completed in 2026. They were fairly positive on both of these. They will get $35 and $15m milestone payment for first commercial sale, which looks very likely. Then the sales milestone targets are not defined for the ROW, but are up to $170m for Europe and $110m for Japan. I am thinking the initial trigger levels of these payments will be higher than in the USA as they are getting a higher sales royalty - high teens to low twenties vs low teens in US. So I am expecting them to hit some milestone payments but what they are is largely unknown beyond its moving in the right direction.Another unkown is the actual pricing for these jurisdictions haven't been determined as far as I can tell, and this could impacted the sales quantum.

3) Have overpromised, and the new STIX formulation doesn't address the problems that some patients have with the oral liquid, so potential patient pool is still limited to those who tolerate it or perceive it to work. I can't assess this but from what they say about STIX it sounds like a good option, it can be mixed with any liquid (apple juice to gatorade) so should be more palatable, I still shudder at the thought of the unpleasant cherry flavored medicine from when i was a kid. STIX is lower in carbohydrates, which is impoartant as many of the patients follow a KETO diet and limit sugar intake. STIX is also more convenient- doesn't need to be refrigerated, much easier to travel with etc. Overall it does sound like it could be an accelerator but will watch and see. So from what I have seen it looks like a product improvement, they will start selling in Q1 but wont ramp up to full availability til Q2, they also said they will sell each version, but its hard to see why anyone would want the oral solution given the benefits of the STIX formulation.

Its likely to be some combination of these scenarios but I still like NEU, the ability to get a steady income while your developing a pretty exciting drug in NNZ2591. Happy to keep holding this one.

There are a number of positives in this announcement. Firstly, the 700m sales (admittedly in 2028) is higher than expected. Second, the persistency rate increasing is obviously great (and presumably feeds into the higher sales projection). And thirdly, the timeline for results in the Japanese trial is reassuringly early.

SP up over 6% so far today

With the "Canada issue" out of my system in Part 1, here is a summary of last week's $ACAD (Acadial Pharmaceuticals) 3Q Results call.

1. Commercial Performance and Market Dynamics

- Net sales: US $101.1 million in Q3 2025, up 11% year-over-year, marking Acadia’s largest quarterly sales for DAYBUE. This was the highest quarter for net product sales overall

- Market penetration: Approximately 40% overall in the U.S. Rett syndrome market, with 27% penetration in community settings

- Referral growth: Achieved the largest quarter-over-quarter increase in referrals since launch, driven by expansion of the field team and outreach to community prescribers.

- Community prescribers: Now account for 74% of new prescriptions, up from 64% the prior year.

- Persistency: > 50% of patients remain on therapy at 12 months, and > 45% remain on therapy at 18 months, indicating durable adherence.

- Global access: Named-patient supply programs are expanding in Europe, Israel, the Middle East, and Latin America, with 1,006 patients treated worldwide to-date

- Guidance (FY 2025): DAYBUE net sales forecast US$385 – $400 million, with gross-to-net 22.5 – 23.5%, reaffirming momentum

(From Q&A)

- Management reiterated that growth was broad-based across both academic and community prescribers, with community uptake now sustaining most new patient starts. (Note: some 75% of the addressible market is treated by community prescribers, and this segment remains relatively under-penetrated)

- They emphasized that the larger field force deployed earlier in 2025 directly contributed to improved referral rates.

- No change was announced to 2025 guidance, indicating confidence in continued double-digit growth.

2. Regulatory and Geographic Expansion

From presentation

- DAYBUE (trofinetide) is approved only in the U.S. and Canada for treatment of Rett syndrome in adults and pediatric patients ≥ 2 years

- A Phase 3 trial of trofinetide in Japan has been initiated, marking Acadia’s first pivotal trial outside North America

- The company filed a Marketing Authorisation Application (MAA) with the European Medicines Agency (EMA), with an anticipated CHMP opinion in 2026

- Named-patient supply programs already operate in multiple regions (EU, Israel, Middle East, Latin America).

(From Q&A)

- Executives stated that the EMA filing was accepted in Q3, and the CHMP opinion is expected mid-2026.

- They confirmed that Japan’s Phase 3 trial uses the same dosing and endpoints as the U.S. approval study, designed for regulatory alignment.

- Early named-patient use is providing real-world data that will support broader access discussions post-CHMP.

- "Disappointing decision in Canada" (what??! See Part 1 Straw)

3. R&D and Pipeline Integration

From presentation

- DAYBUE remains the core commercial rare-disease asset, while ACP-2591 (cyclo-GPE analogue) is a next-generation follow-up in Rett and Fragile X syndromes

- The company is building a global Rett-syndrome franchise, leveraging DAYBUE’s success to expand to additional indications and geographies.

(Q&A)

- R&D leadership highlighted that DAYBUE’s durable efficacy data continue to inform the design of ACP-2591 Phase 2 planning, with a goal of complementary rather than cannibalistic positioning in Rett syndrome.

- Management also noted interest from academic consortia in exploring DAYBUE in combination therapies, though no new trials have yet been initiated.

4. Other Q&A Comments

- CFO Mark Schneyer confirmed that DAYBUE’s gross-to-net deduction (~23%) is expected to remain stable in 2026 given payer mix and limited rebate pressure.

- Analysts asked about inventory levels; management stated they are “healthy and in line with volume growth,” with no channel stuffing anticipated year-end.

My Assessement (thinking out loud, so apologies for the stream of consciousness format)

DAYBUE sales of US$101.1m for the Q came in below the low case of my model ($102.3 - $104.3 - $106.2). My model had them hitting a FY range of $388.5 - $400.5, and so with the lower number achieved in Q3, I'm expecting they'll be towards the lower end of the narrowed guidance of $385 - $400m.

But this is really splitting hairs, and the key message is that management have confirmed my view form earlier this year that they have a good grip on how the product is performing in the market, and sales force productivity, and so will be making good resource allocation decisions.

What we don't know is how much of the revenues came from outside the US, given that the product is being made available to patients ex-US in an increasing number of markets in early access programs. It's a high-value product, so it doesn't take for many patients accessing the drug from overseas to start to move this dial.

But I am disappointed at the growth rate, because in Jan-25 the company announced a 30% sales force expansion. This was completed in May-25, and while it will have taken some months for new starters to get traction with their accounts, the period Jul-Oct has in my view enjoyed a full quarter with the expanded field force, focused on the community-based prescribers. My range was meant to capture the full ("80%") confidence I perceived at the time.

A year ago, the 3Q-on-2Q growth rate was +7.8%, so even with the +30% expanded sales force in 2025, the sequential q-o-q growth of +5.2% indicates just how much of a headwind patient churn is. That said, Persistency seems to be holding up: c. 50% at 12 months and 45% at 18 months are again reported, and it will probably not be until next year that we get to see what this is becoming out to 24 months.

So, let's have a stab at considering US Revenue Growth from here:

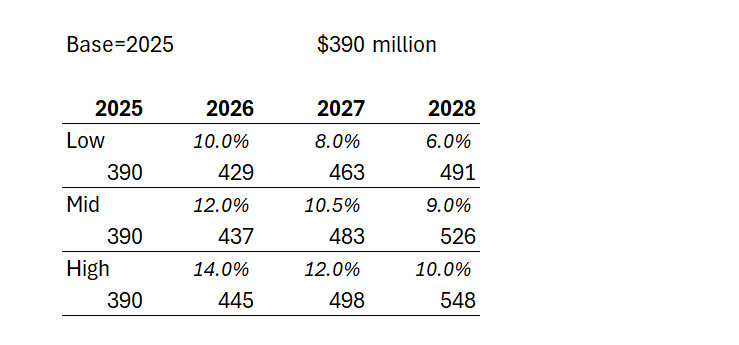

Case 1: Management say they will continue double digit annual revenue growth. So giving them the full benefit of the doubt and assuming they hit 2025 revenue of $390m, at 10% for two years, that gets them to $472m in 2027, and $520m in 2028 - likely the year of plateau sales,... or maybe they'll eek out some further growth in 2029.

Case 2: Being generous, let's assume an upside QoQ growth of 4% or 17% pa for two years. That gets them $533m in 2027, and a likely plateau sales in year 5 of $623m in 2028.

But, then again, I think Case 2 is overly generous. Afterall, the 2025-2024 PCP growth rate was only 11%, and let's trim that to 10% to allow for some overseas patients. The sales force expansion has helped the last quarterly result, and so they will likely struggle to do much better than 10% p.a. over two years, even if the 2026 FY number gives a full year with the expanded salesforce cycling an earlier year before the ramp up, and so exceeding 10% in 2026 should be doable in all scenarios. But it can't be sustained IMHO. The persistency drag is just too high.

Looking at the historical trends, the rate of growth is maturing rapidly. For example, even while benefiting from a full quarter of expanded sales force, 3Q/2Q-2025 was +5.2%, compared with 3Q/2Q-2024 at +7.8%. So there is defintely a sequential decline at play towards a plateau that doesn't look that far off (s-curve).

So, in the table below I've modelled three scenarios for annual US revenue growth over the next 3 years (all in $USm):

Depending on how longer term persistency evolves, we could find either 2028 or 2029 as the plateau year for the US. And in the illustration above, in the low scenario, $NEU doesn't get anymore milestone payments, and on the other two scenarios, will get the US$50m milestone only in 2028. The $750m milestone looks well and truly off the table to me.

I haven't pulled this through my $NEU valuation model yet; however, it is a significant deterioration on my earlier projections.

So, what does this mean for $NEU?

Well, US sales of US$490-$550m in round numbers are $NEU royalties of US$54-$62m or A$83-$95m, and that's much, much lower that the analysts have for $NEU.

Why?

Because I think the analysts are including all of the following things I haven't included:

- Assume continuing growth, and not modelled an s-curve with a continuing persistency driving decline after year-5 plateau

- Added milestone payments

- Added RoW

My model is too complicated to pull through a simple set of number for the value of DAYBUE to $NEU. However, my earlier projections gave me $12 - $20/share (US growth and pro rata RoW offset by 3-4 years)

Today, I believe US DAYBUE will have a plateau in 2028 or 2029 and immediate steady decline, as new patients arrivals fail to keep pace with churn. So, if all we have is the US, then valuing $NEU at 5x peak contining royalties of, let's be generous and say, A$85m to A$120m gives A$425m - $600m, or with SOI of 126.5m shares, that's $3.35 - $4.75 /share.

Yes, that's what $NEU (US-DAYBUE only) could be, if it can't get reimbursement beyond the US and if it can't sustain growth,

Wow.

Of course, I think it will be worth more than that. But hopefully, you can see that at $18/share, NNZ-2591 is now potentially doing a lot of heavy lifting. And it might be worth it. But it also might not.

But that's not what my "2 for the price of 1" investment thesis was all about. So my thesis is well and truly broken.

BIG CAVEAT: I wasn't going to post this, because I was sure I've made an error somewhere. But I have gone through everything a couple of times, and also used a couple of independent methods, and keep getting similar results. And to be clear, I haven't accounted for $NEU's massive cash pile. But I am not doing an enterprise valuation of $NEU, but rather only the value of the royalty stream from US DAYBUE. So, as ever, this is not advice. But it is enough for me to take the decision I have already executed. Oftentimes, more analysis doesn't add more value.

That said, over the coming months, I will properly update my model. And that's because I want to know at what price I am prepared to buy back in for the value of NNZ-2591. But I don't think there is any hurry. The PMS Phase 3 trial has some way to run.

Disc. Not held

I am in the process of writing up my notes from last week's Acadia Pharmaceuticals ($ACAD) earnings call, however, one of the most important insights in the call was a reference by CEO Catherine Owen to a question from Jack Allen (Robert W Bird & Co. Incorporated) about reimbursement in Canada.

TLDR: The Canadian Drug Expert Committee of the CDA in August 2025 filed its decision: "Do Not Reimburse" for trofinetide (DAYBUE)"

I've decided to elevate this to a stand-alone straw for two reasons. First, it is bad news, and in my opinion it could have a significant bearing on the pending EU/UK approval outcome (even though these are completely independent of each other).

Second, I am concerned that it demonstrates a lack of candour by both Acadia and Neuren management, given that I have conducted an extensive search and can find no proactive references to it in investor communications. (And of course, if it is proven I have missed something, then I withdraw this comment unreservedly. This is also why I am flagging the point, in case other eagle-eyed $NEU investors have picked up something I've missed.)

On the call, analyst Allen asked: "I wanted to ask about reimbursement in Europe. I know there were [... inaudible,.. line cut out] ... in Canada over the summer...."

CEO Catherine Owen replied; "Thanks, Jack. So yes, we are obviously in the middle of discussions and thinking right now around reimbursement in Europe. And you're right, we did have a disappointing decision in Canada. Tom, do you want to share a little bit more about how we're thinking about reimbursement in terms of the sequential approach to that in Europe?"

Tom Garner (VP Commercial) continued ... absolutely no reference to Canada!

Both companies have proactively disclosed and continue to communicate that DAYBUE is approved for use in Canada. And that is true. But after approval (based principally on efficacy and safety), a drug has to gain a reimbursement decision. For countries with a mixed public and private healthcare system, the reimbursement outcome by the responsible public agency, has a significant bearing on prices that will be covered by entities like health insurance payers. So the public reimbursement milestone is critical for determining the revenues that can ultimately be achieved in a market.

And yet, the only reference to the Canadian issue either verbally or in writing that I can find are the following words by Catherine Owen "we did have a disappointing decision in Canada". (Again, other $NEU shareholders, please tell me what I've missed.)

So, I've structured this straw as follows:

1. The Canadian CDA-CDEC Decision

2. How Reimbursement Works in Canada

3. Why I think there is a potential, broad "Read Across" to other Jurisdictions

4. Implications for Valuation

5. Investment Decision

----------------------

1. The CDA-CDEC Decision

I attach the link to the full CDA-CDEC decisions. These are published for transparency in the Canadian Journal Of Health Technologies. It makes for interesting reading.

My BA has summarised the document for you as follows:

Summary of Decision

Agency: Canada’s Drug Agency (CDA-AMC)

Committee: Canadian Drug Expert Committee (CDEC)

Date: August 2025

Decision: DDO NOT REIMBURSE trofinetide (DAYBUE) for the treatment of Rett syndrome in adults and children ≥ 2 years of age and ≥ 9 kg.

Key Reasons for the “Do Not Reimburse” Decision

a. Uncertain Clinical Meaningfulness

- The pivotal LAVENDER trial (N = 187) showed statistically significant improvements in caregiver-reported behaviour (RSBQ –3.1 points, 95% CI –5.7 to –0.6) and clinician-rated global improvement (CGI-I –0.3 points, 95% CI –0.5 to –0.1).

- However, no minimal important differences (MIDs) were established, so the committee could not determine if these changes were clinically meaningful

- The trial had high discontinuation (≈25%), missing data, and relied on outcomes not used in Canadian clinical practice.

b. Lack of Evidence on Quality of Life and Function

- The trial provided no measure of health-related quality of life (HRQoL) for patients or caregivers, and data on communication, motor skills, and caregiver burden were limited and unvalidated.

- CDEC therefore could not determine if trofinetide addresses the unmet needs identified by patients and caregivers.

c. Very Low Certainty of Evidence

- The committee rated the overall certainty of evidence as “very low” due to bias, imprecision, and indirectness between the trial population and the broader Health Canada indication.

- Open-label extension (LILAC/LILAC-2) and supportive studies (DAFFODIL, LOTUS) did not resolve these uncertainties.

d. High Cost

- Annual treatment cost estimated at CA $427,000 – $1.34 million per patient, depending on weight

e. Adverse Effects

- Diarrhea (81%) and vomiting (27%) were common, leading to 17% discontinuations in the treatment arm vs 2% with placebo.

- While manageable, these events raised concerns about unblinding and trial validity.

f. Reconsideration and Patient Input

- Sponsor Request: Acadia requested reconsideration, arguing the RSBQ endpoint was valid and that CDEC had undervalued caregiver-reported benefits.

- Patient & Clinician Feedback: Groups emphasized the severe unmet need and the importance of even small improvements in communication and daily function.

- CDEC Outcome: Acknowledged these perspectives but upheld the original decision, concluding the evidence was too uncertain to demonstrate meaningful benefit or long-term safety

2. How Reimbursement Works in Canada

Now it is important to recognise that the report is a recommendation, and not a binding decision. However, for all practical purposes, I consider reimbursement unlikely, unless $ACAD can submit further evidence that addresses the grounds for denial. Clearly, the company will be working on this, and has in fact already had one shot at it.

Let me explain why I feel this is the case, by explaining how the system works in Canada.

The CDA-AMC conducts independent clinical and economic evaluations of new drugs and medical technologies on behalf of Canada’s publicly funded health systems (federal, provincial, and territorial, except Quebec). It does not set drug prices or directly fund products, but rather provides evidence-based recommendations to help governments decide whether to include drugs on their public formularies (lists of reimbursible medicines).

The Canadian Drug Expert Committee (CDEC) is an independent panel within CDA-AMC composed of physicians, pharmacists, health economists, and patient representatives. It reviews clinical trial data, real-world evidence, cost-effectiveness analyses, and patient submissions. The committee then issues a non-binding recommendation to federal, provincial, and territorial drug plans.

Provincial/Territorial Decision-Making: Each province/territory makes its own final reimbursement decision, typically following the CDEC recommendation. In practice, a “Do Not Reimburse” recommendation from CDA-AMC almost always results in non-listing (no public coverage) across the provincial drug plans.

Private insurers may make separate decisions but usually reference the same HTA findings.

Reconsideration and Transparency: Manufacturers can request reconsideration (as Acadia did for DAYBUE). The CDA-AMC publishes both the original recommendation and any reconsideration outcome on its website and in the Canadian Journal of Health Technologies for public transparency.

3. Why I think there is a potential broad "Read Across" to other Approvals

My reading of this situation starts to answer a question I always had on my "issues" list. DAYBUE is by any measure an expensive drug, and it was a question for me how jurisdictions would deal with it in places where cost-benefit analysis has a stronger bearing on the reimbursement decision. While the US is increasingly alert to healthcare economics, there is no question that it is more permissive of reimbursing high cost drugs where the cost-benefit is open to challenge.

It seems the Canadians have issues with both the strength of the effiicacy data, the side effects, tolerability and low persistance of the drug (all indications impacting Quality of Life) and the high cost.

The EU process will follow a similar path to Canada. The EMA-CHMP will make its decision on scientific grounds, whereupon each countries HTA (Health Technology Assessment) process will kick in, leading to the reimbursement decions. In the EU/UK, public medicine is a much larger share of the drug budget than North America, so the single-buyer country agencies will have a lot of clout in the pricing decision. And European countries have even greater pressures on public health budgets, given weak economies, unfavourable demographics, and a greater taxpayer contribution to the healthcare spend.

All European HTAs consider cost-effectiveness, clinical value, budget impact, and comparative benefit (albeit there is no other treatment for Rett). And so I believe the Canadian decision is a potential canary in the coalmine for Europe. Even though the European process is completely independent, I imagine all the European decision-makers will read the Canadian document. In Europe, there is also greater political pressure than in the US for challenging high cost drugs, and even more so when there are clear question marks on quality of life benefits.

In the best case scenario, I anticipate this will result in European prices heavily discounted to the US price. By heavily discounted, I mean 40%, 50% and even up to 70% or more!

4. Implications for the Valuation of Neuren

The Canadian "canary in the coalmine" puts a questionmark over the remaining value in the right-hand slide above. While RoW paitents may be given access to the drug on special grounds ("early access programs"), these are unlikely to trigger the "commercial sale" milestone payments. Privately-funded patients might also find ways to get access to the drugs.

The Canadian decision also indicates to me that negotiations towards an acceptable reimbursement decision could be protracted. $ACAD needs to hold out for a good enough price that make sense, given that it is on the hook for the initial milestone payments irrespective of the value of the commercial sales. So, in Europe, it will have to see revenues that cover: US$35m royalty + "mid teens to low-20's" tiered royalties + distributors margin (or fixed cost of sales force, if direct).

So with potentially a much lower price, a relatively high fixed royalty, and a lower Gross-To-Net, $ACAD will need to see material revenues, before agreeing to launch.

The reimbursement negotiation is therefore likely to be protracted. $ACAD will marshall all the real world data that they can from the US, as well as the continuing open lable trial data on long term persistency (now down to 45% at 18 months, down from 50% at 12 months) potentially pushing RoW cash flows further into the future.

5. Investment Decision

I haven't crunched this all in my model. However, on a risked view, I am materially marking down my Outside North America DAYBUE revenues (start, ramp, peak), and therefore also the royalties to $NEU (note: the percentage tiered royaties here are significantly higher than the US.)

By eyeballing my current model my "2 for the price of 1 thesis" is blown for $NEU at $18.

In round numbers, my valuation of DAYBUE ($12-$20), has clearly fallen to the lower end, with a significantly lower downside case if DAYBUE cannot achieve significant commercial traction outside the US.

Which means that much more of the current share price rests on the development of NNZ-2591. I had given NNZ-2591 $8 of value at a 50% risking (from $16). Perhaps that is harsh, but until I have a better view, then that is my number.

Which means that at a SP of $18, I need to see $10 of value in DAYBUE, and I don't see that with confidence, as I will make clear in my next write-up on the $ACAD results.

For me, the bottom line here is that more of the value in this business lies in drug development risk, rather than commercial execution. Looking across my entire portfolio, I am carrying quite a bit of this risk, and I am not confident that I have a good grip on the outlook for $NEU. I'd therefore like to take 2-3 quarters to evaluate DAYBUE's progress from the sidelines. And that's because I think there is a reasonable chance that we will soon have visibility of US DAYBUE plateau sales below US$500m (downside) and not much more (upside). I'll sketch this out in more detail in my next note.

Accordingly, I have sold my shares in $NEU.

Disc: Not held

Another step forwards for Neuren on their journey to address new syndromes

US Pharma company (licensee for DAYBUE) announced 2Q results including DAYBE Sales. The key results are shown below:

I'll give a more complete assessment of the data from the call later this morning, but the bottom line is, this is an excellent result.

In the words of CEO Catherine Owen, DAYBUE is moving "through stabilisation and back into growth".

$ACAD are holding to guidance for the year, but according to my analysis they should comfortably now hit the midpoint of guidance and may well get to the upper limit of even exceed it. They were pressed on this in Q&A and said any modification of guidance will come at 3Q. (There is a history with this product of disappointment, so I think they are being cautious. Catherine clearly is in the "under promise and over deliver" camp. Which is fine with me.)

More later. Also, we should expect a related ASX announcement from $NEU before the market opens and likely a conference call to get Jon Pilcher's take. I imagine he'll be delighted and upbeat.

As for SP action, $NEU has run quite hard over recent months. I'm not sure if this is because any of the instos have insights into the sales via channel checks. Persoanlly, I've not read any research on this. If that is the case then today's sales results explain the SP action.

From my perspective, today's result shores up the base of my "two for the price of one" investment thesis (i.e. de-risks the downside) but probably not enough to justify a valuation update. I'll reconsider this after the $NEU results later this month,

I remain a happy hold here. More detail and analysis later.

Disc: Held in RL and SM

The Q1 update from Acadia was very positive. They had previously flagged that Q1 would be a slowdown relative to Q4, based on seasonal effects, so hitting $84.6m revenue from Daybue was pretty positive and sets them up well to hit their annual guidance of between $385-405m. While the revenue chart below looks like an asymptote has been reached, I am expecting this to start increasing again given the commentary around some of the drivers of revenue.

While I consider the numbers to be solid the positive for me were the updates around persistence which is now running at 50% of new starts and has improved considerably since the trials and the commerical launch. It looks like they will have a fairly stable patient population once they get past the 12month mark, with 65% of patients (around 620) have now been on Daybue for >12 months. This is a positive for NEU's continued royalty payments and the likely potential for them to get the $500m sales milestone payment.

The number of patients on the drug has again started to increase after a bit of a softer patch last year. They have 954 active patients up from 870 ending 2024, so they added around 84 in Q1. They still think around 2/3 of the potential patient population haven't tried the drug yet.

They have expanded there on the ground sales team by around 30%, as highlighted last quarter so this should result in higher patient starts now that they move out from the Centre of Excellence Rhett treatment centres. Using the above numbers (84 new starts per qtr and 50% persistence) I can get to the high end of guidance fairly easily without relying accelerating patient growth. Listening to the Acadia call the team seemed fairly comfortable with where they were at and the potential for the next few periods. I think the new CEO has a good sense of the business and has a more polished and focused feel to it than some of the earlier calls i listened too since the launch.

Good news also on the ROW expansion with first non-commercial patient access sales in Germany happening in April and orphan drug designation and a clinical trial in Japan commencing in Q3. So the initial commercial sales milestone ($35m) for Europe are likely in the next financial year and the $15m Japan payment following 1-2 years after.

Overall I'm pretty happy as this had the potential to be a much lower quarter than they achieved. I am not expecting these numbers to move the market but the continued royalty stream really gives NEU the freedom to undeetake the phase 3 trials NNZ 2591 without the potential of a cash crunch

$NEU have issued an ASX announcement this morning reporting on the 1Q 2025 US sales and broader progress of DAYBUE, as reported this morning by $ACAD at the end of the trading day on Wall Street.

I’ll post here $NEU’s overview and then provide my own analysis, having attending the analysts call this morning.

Their Highlights

• Q1 2025 DAYBUE™ (trofinetide) net sales of US$84.6 million, up 11% from Q1 2024

• Record number of unique patients received shipments, up 4% from Q4 2024

• Neuren’s Q1 2025 royalty income was A$13.5 million, up 17% from Q1 2024

• Acadia retained full year 2025 DAYBUE US net sales guidance of US$380 - 405 million, implying full year 2025 US royalty income for Neuren of A$62 - 67 million

• Marketing approval in Europe anticipated in Q1 2026, first shipment of DAYBUE to Europe was made in April 2025 under a Managed Access Program

• Orphan Drug designation granted in Japan

• Distribution agreements now in place to facilitate named patient supply in other regions including Latin America, Middle East and Asia Pacific

• Neuren cash and short-term investments $341 million at 31 March 2025

• Neuren is presenting at Macquarie Australia Conference on 8 May 2025

Further Details from the $ACAD Investor Call

As I will explain in the next section, understanding q-o-q revenue changes is complex. So $ACAD focused on the report that patients treated with DAYBUE in the quarter rose from 920 in Q4 2024 to 954in Q1 2025, i.e., +3.6%.

Last quarter, $ACAD announced they would expand their sales and marketing force by 30%. The reason is that the current salesforce is focused on the high-prescribing Centres of Excellence, with less coverage in the broader community-based physicians who support some two-thirds of the total market. Today, $ACAD reported that the recruitment of these additional sales reps have been completed, and they expect to see the benefit of sale force expansion in the second half of 2025.

At this stage, $ACAD believe that only one-third of the population diagnosed with Retts have tried DAYBUE.

$ACAD also report that now >65% of the 954 patients taking the drug at end of Q1 have been on it for more than 12 months, and that persistency tails off at greater than 50% after 12 months, and thereafter continues to be stable (although I note that no quantification has at this stage been given for what 18 month persistency is looking like. At the next quarterly report, we might reasonably expect to be given a 2-year persistency statistic!)

On tariff impacts, $ACAD report that they “have several years of inventory” in the US, so they are well protected in the short term.

There was some discussion on their exposure to intervention in the US market by the Trump Administration. DAYBUE is a high cost drug and it would exposed if the Administration implements a “most favoured nation” requirement on drug pricing. In essence, such a move would mean that $ACAD would only be able to receive pricing based on prices achieved in overseas markets. The key risk is that if prices in Canada or, say in 2026 / 27 in the EU, are substantially lower than the very high treatment price in the US, then US agreements would be renegotiated. Of course, this is a systemic risk facing the entire pharmaceutical industry, and we are yet to see how this plays out. (Go, the US pharma lobby!!)

Approval in the EU is still expected in 1Q 2026, and $ACAD will soon pass the key 120-day milestone, which is a point in the EMA approval process at which the initial assessment of data is complete. At this point, the EMA can choose to "stop the clock" on its approval process and issue questions to the pharmco. No "Clock Stop" would be a very positive sign for the approval process. So, we should expect a further update on the EU process in the next few weeks. (Remember, any EU approval of DAYBUE in 1Q 2026 then starts the process of country by country negotiation on pricing and reimbursement. Particularly for expensive drugs like DAYBUE, this process itself can take many months and even years!)

My Analysis

The $NEU summary above gives a good overview of what’s going on. Basically, we are seeing steady progress on new patient adds, which remains the key revenue driver.

I want to focus the remainder of this report on the patterns of revenue growth, as there are some important dynamics at play, which are now becoming clearer, and which management have done a reasonable job of explaining.

Patterns in Revenue Growth

Now, the eagle-eyed among us will note that the 1Q-on-4Q revenue decline that was predicted (based on what happened last year, and which took the market by surprise then) has indeed occurred.

The 1Q 2025 sales of US$84.6m were down 13% on 4Q 2024. Interestingly, last year the decline was also around 13%.To provide an overall picture, I’ve plotted the quarterly revenues as well as the percentage changes Q-o-Q (orange bars) and % to PCP (green bars) in the chart below. Early values of the % growth figures are omitted, as they are not meaningful, coming off a small base.

I’d like to dig into this in some detail, as it was discussed on the $ACAD call this morning.

Three things seem to be happening consistently between 4Q and 1Q, as follows:

- Patients pull forward their refills in 4Q from 1Q – potentially ahead of holidays. Management explained that this “pull forward” effect accounted for US$3.5m of revenue being pulled from Q1 into Q4.

- Consequently, scripts and refills are down in 1Q, and there may also be a seasonal effect with fewer patient presentations to clinicians in the winter months

- Net revenue per script falls in 1Q, and this recovers in later Qs due to seasonal patterns in reimbursement, particularly for patients on hybrid Medicare-Private cover.

The first two points are simple to understand. The third requires some explanation. Here goes.

Pharmaceutical companies often see lower net revenue per patient in the first quarter of the year due to how U.S. insurance plans—including Medicare Part D—are structured. At the beginning of the year, many patients haven’t met their deductibles, which means they face higher out-of-pocket costs. This can delay prescription fills or reduce adherence, especially for expensive drugs. In response, companies may provide increased copay assistance, which reduces the revenue they recognize per patient.

Under the 2025 Medicare Part D redesign, the financial burden on drugmakers has also shifted. Manufacturers must now cover a portion of drug costs earlier in the year under the new benefit structure, even before patients reach coverage. This increases rebate obligations in Q1, further lowering net revenue per prescription.

As the year progresses, more patients move past their deductibles and into more stable coverage phases, leading to steadier prescription volumes and fewer financial concessions from manufacturers. As a result, pharmaceutical firms typically see higher net revenue per patient in the later quarters of the year.

So, this 1Q reduction in revenue is a regular feature of both prescribing/refill seasonality and reimbursement/copay dynamics, and little conclusion can be drawn from the revenue number. We’ll need to wait for the 2Q number to better assess whether $ACAD remain on track to hit the annual guidance number. This next result will provide an important baseline against which to assess the impact of the expansion of the sales and marketing force which is expected to start contributing in H2.

My Takeaways

Overall, this is a reasonable result from $ACAD on DAYBUE sales.

The 1Q number is difficult to interpret. It was a bit softer than I hoped for, however, if the expanded sales force has the intended impact, I consider it reasonable that $ACAD have left guidance unchanged. Having said that, I don't have a good quantitative understanding of the reimbursement/copay/Part D dynamics - so I am somewhat blind on that, and have to go with what management are saying. That said, under the new CEO Catherine Owen Adams, communications have been clearer and more consistent from one presentation to the next.

The 2Q number will be more telling, as the bounceback after 1Q will set the stage for the second half of the year, and we have last years number to compare with.

The market has therefore responded reasonably in my view, with SP off 3% at the time of writing. There was little news to react to, one way or the other, after all.

We may see some further reaction based on Jon’s delivery at the Macquarie Conference later today. As each quarter advances, $NEU gets closer to its next milestone payments which would come from any EU approval – or rather first commercial sales in any EU territory which could following during 2026. And, of course, the royalty rate for RoW sales are more attractive than the US.

Overall, $NEU remains on track with my “two for the price of one” thesis.

I was considering topping up after today's result, as I still have only a modest 4.7% allocation. However, even though I have some understanding of the 1Q dynamic, I can't tell to what extent it is masking a weaker overall sales growth. So, I'm going to have to wait another Q.

Disc: Held in RL and SM

15-Jan-2025: 1:30pm: NEU down as much as -9.17% today (closed @ $12 yesterday and down to an intraday low of $10.90 so far today) with a couple of hours to go. So much for being close to the bottom of their downtrend.

I'm not seeing negatives in today's announcement - Trofinetide-marketing-application-submitted-in-Europe.PDF - but clearly it's below some market participants' expectations. Perhaps it's the pace of the DAYBUE™ (trofinetide) roll-out globally that has some punters thinking that while the growth is there it might take longer to play out than previously expected.

I guess that's the trick. How do you accurately manage market expectations when the market is often irrational and many people are simply following trends or charts without too much understanding of what the business does and the environment in which the business operates?

Pharma is well outside of my wheelhouse, but I know enough to know that trofinetide has been derisked and is going to be rolled out globally, and it's already selling in the US and Canada, and the FDA in the US is regarded by most people to be one of the hardest nuts to crack for pharmaceuticals. And the global roll-out will take time, i.e. years - it won't happen overnight.

I'm bemused, but otherwise unphased. I was obviously back in too early with NEU (in December) and I guess that tends to happen to me more often with companies that operate within sectors that I have less overall knowledge about and experience in (outside my sphere of competency), however when I bought back into NEU in December, it was in my SMSF only, and I'm back to being comfortable with 5 year plus timeframes there now - after my TPD claim got approved and paid in October so my prior need to make shorter term profits is no longer there. I'm back to being a medium-term value investor - mostly - who also likes to make a buck here and there on shorter term opportunities. All good.

Today's Announcement:

Disclosure: I hold NEU both here and in my SMSF.

This is not a full valuation or a bear case, it’s a base case on the currently commercial part of the business to get a feel for what it is worth. On this basis I now have a full position in NEU, with a simple thesis that the current prices is reasonable for just the royalty income from Daybue (as @mikebrisy concluded with much better analysis) and I expect milestone payments to cover the cost of any further research in NNZ-2591 and assume that research fails to generate any commercial value.

Assumptions:

· Duybue sales in NA of US$400m growing at the cost of capital, generate US$43m (A$64.2m) in Royalties, which I view as conservative.

· ROW sales are worth around the same value, so A$64.2m in Royalty revenue.

· The cost to operate the business and for further NNZ-2591 research is covered by Milestone payments on Duybue (ie they net out) including the US$50 for the current milestone and US$50m for the PPV sale.

· PE of 12 and Cash as at 30 Sep of $210m.

· Base Value per share of A$10 per share

Given how rough this is I have bought in at under $13, seeing the downside as minimal. The upside however is significant and I am yet to put any figures on it but each of the following could be worth at least the current value of the company:

· Daybue commercial success above current expectations.

· Fragile X royalties and milestones from Acadia.

· NNZ-2591: multiple opportunities but current Phase 2 candidates for Phelan-McDermid, Pitt Hopkins and Angelman are worth ascribing value too.

I have a lot more work to do on NEU which will take a long time and I had thought I had missed the opportunity when the price spiked, but thanks to RFK’s appointment and the market I am taking this second chance on the basis that this is a very asymmetrical investment in my view.

Disc: I own RL

Summary

Following $ACAD 2Q Results in Aug and recent conference presentations in September also by $ACAD, I have firmed up on my recent valuation ($24, $12-$46), and am getting more comfortable with the future US sales trajectory for DAYBUE.

As a result, I've added back most of the shares I sold in May at yesterday's price, which I consider a bargain.

I consider that today the market is offering $NEU on a "two for the price of one" basis, ... or thereabouts.

Context

With all the focus on ASX reporting over recent weeks, I’m only now catching up with some of the wider research opportunities in my portfolio. One area I am giving some focus is $NEU. I’ll not repeat information here from earlier straws and posts, but in summary, this business has two important things going on:

1) DAYBUE being sold under licence by $ACAD in the US, with work underway to gain approval in Canada (likely end-24/early-25) and EU & Japan (approvals likely only in 2026+)

2) NNZ-2591 has completed Phase 2 studies in three neurological conditions, with an end of Phase 2 meeting with the FDA for Phelan-McDermid syndrome due this month. (This is likely the first indication to advance to Phase 3, given the US market potential of 17,000-32,000 patients. While there's still clincal development risk, it's potentially much bigger than DAYBUE)

We’ve covered NNZ-2591 in other recent straws/posts. My focus here is to consider my view on DAYBUE in the light of recent communications from $ACAD, including over the Summer Conference season in the US.

I’ve given a rough valuation of $NEU as $24.00. Being $16.00 due to DAYBUE and $16.00 due to NNZ-2591, risked at 50%. In my normal way of presenting valuations, I have this down as $24 ($12-$46).

This compares with analyst views of $26.56 ($22.90 - $29.90, n=6).

This picture below shows the SP progression relative to the consensus view, which suffered a modest downgrade in August, due to $ACAD downgrading guidance for 2024 DAYBUE sales.

So, we all know that momentum players in the market hate downgrade cycles, and so a very large gap has opened up between valuations of the business and the SP.

Hence the title of this straw: I view that with $NEU you are essentially getting a DAYBUE business (which I see as worth $16) and a success case for NNZ-2591 (which I see as worth $16 unrisked) for $13.59 at the time of writing. The analysts agree – two for the price of one!

The reason I sold down 1/3rd of my RL holding in $NEU on 15-May was that I was concerned about the 1Q report from $ACAD. According to my model, $ACAD were never going to hit 2024 guidance for DAYBUE, and I didn’t buy the offered story about a harsh winter causing clinics to shut down. But as importantly, I became suspicious of management – having prematurely offered annual guidance, and then spinning a 1Q story and acting as though things were on track for the year.

Roll forward to the 2Q report in August. While sales began to recover, guidance was indeed finally lowered, and that pushed many ASX shareholders into a funk with shares sliding from c. $18 to $13-$14.

To put this in context, you can buy $NEU today for less that you could at the launch of DAYBUE, which pre-dated the stream of positive newsflow on NNZ-2591.

So, What Can We Say About DAYBUE?

Having gone back over the $ACAD 2Q Results call (8-Aug), the Morgan Stanley Healthcare Conference (4-Sept) and the Baird Conference (11-Sept), I have firmed up my view on what is happening with DAYBUE. (BTW, recordings of both conferences are accessible on the $ACAD website.)

It is now clear to me that what happened following the launch of DAYBUE: $ACAD were completely surprised by the demand in the first 5-6 months. In retrospect, this should not have been surprising. Rett Syndrome is a very challenging condition, and there is a strong global Rett community. With no pre-existing treatments on the market, there is a well-established specialist support network via Rett Centres of Excellence that support about 25% of US Rett patients. Highly motivated patients, including the parents of sufferers who carry the burden of care, quickly accessed their HCPs requesting the product as soon as it was launched.

This drove strong initial sales in Q3 and Q4 2023, and it led $ACAD to prematurely issue what now turns out to be overly-optimistic guidance (… which was clear to me as early as May).

But as we know, DAYBUE is not well tolerated by many patients. So Q1 and Q2 2024 saw two things happen. 1) The initial “surge” from "c. 25%" of the potential market subsided and 2) discontinuations from this initial “bolus” swamped new patient adds. Aaaaah! DAYBUE has stopped growing! Sell!

This complex dynamic made the interpretation of data from Q2 very challenging. But as a new normal in net patient adds began to establish itself, $ACAD were able to reset 2024 guidance to a more realistic level.

Why Am I So Interested in What $ACAD have been saying in September?

With the “panic spin” of the 2023/24 winter behind us, I have been forensically examining $ACAD's statements throughout September, to test them against what was said in August. I can bring myself to overlook what I consider as “Winter Spin” because, indeed, the dynamic – while easy to model after the fact – must have been very disorientating at the time. And who knows, maybe winter clinic closures and delays in reimbursement renewals for refills created a genuine “winter fog”. Management word salad didn't help, but perhaps I was too quick to judge.

What matters is the future and whether $ACAD are properly characterising the current performance, and the path ahead.

So Where Are we Now?

Throughout the last three public disclosures, a consistent picture is emerging. Here are the key points.

Persistency in the real world remains about 10% ahead of clinical trials. This has been a consistent story for 2024. The best estimate of long-term persistency remains around 50%

Patient adds are net positive, and they are coming into line with the patterns $ACAD say they more typically expect to see in rare disease treatments

A consistent picture is emerging for each of the HCP segments:

1. COEs (25% patients) – 50% penetrated, 1/3rd of prescriptions to date. Major area of focus, as these continue to attract new patients. (My thesis is that the availbility of a treatment might increase diagnoses, expanding the market from 5,000 current to the 6,000-9,000 estimated prevalence. CoEs will likely attract an outsized share of new diagnoses.)

2. High volume non-COEs (60% patients) – “good penetration” and the current area of focus

3. Low volume HCPs (25%) – many treating only 1 or 2 Rett patients – large number of HCPs.

Overall, c. 30% of the total diagnosed Rett populated has started treatment on DAYBUE and, by my calculations, Q2 revenue represents an annual revenue run-rate of c. US$340m.

Against the updated (downgraded) guidance for 2024 Revenue ($340-$370m), $ACAD have said at the September conferences that they are tracking to “just below the midpoint of guidance” which I interpret as being c.$350m.

They’ve also said that they see “more upside than downside” from here, which says to me that they are seeing the guidance offered in early August as still appropriate, and we are now getting to the closing phase of the year.

My Analysis

The message consistency across three presentations spanning 5 weeks, indicates to me that $ACAD have got to grips with DAYBUE sales performance. Things seem stable.

I see the journey of the 16 months since launch in three clear phases:

Phase 1: The Pent-up Demand “Bolus Surprise" - April-October 2023

Phase 2: “Winter of Discontent”: Early Patient Discontinuations swamp new scripts - Nov 2023 – March 2024

Phase 3: “Stabilisation” – Normal Market Penetration and Steady Growth - April 2024 onwards

Looking further ahead, while, based on my model, $NEU are unlikely to get their 2025 $500m US milestone, this is likely to come in during 1H 2026. Canada might give 2025 royalties a bit of a push, as it experiences its own “mini-bolus”, and then hopefully Japan and EU will add new impetus to revenue with milestones and royalties in FY26 and FY27.

So, overall, I’m increasingly comfortable about the downside floor to the SP being in the $low-teens. Which is where we are today!

So, my original investment thesis is intact. Today, I can buy $NEU for less than the fair value of DAYBUE, with the free option of the upside of NNZ-2591.

Investment Decision

My valuation remains as published previously. However, yesterday in RL I have added some $NEU to my portfolio, getting back to 94% of my original position. I’ll potentially add some more, but at just over 5% in RL, I’d also be happy to settle here.

Near term upcoming news flow is:

- Readout from September FDA meeting on NNZ-2591

- $ACAD Q3 results in mid-October

Disc: Held in RL and SM

I've now gone back over the recording of the $ACAD announcement with a fine tooth comb.

Contrary to my initial impression, listening a little (i.e. A LOT) more carefully, I felt there was less evasion and more just some incompleteness and relatively minor inconsistencies. More a "misty day" than a heavy fog or smoke screen. So, I do need to row back a little on some of my less generous remarks about the management team.

I still believe there wasn't a straight answer on the active patients as at 30-June. However, I can understand from my own experience why a management team would agree not to put out such data for 30-June and 1-August, which covers the Summer month of July, to mitigate the risk that some idiot analyst would multiply the difference x 12 to get a misleading annual growth number. I.e., discontinuations don't slow down, but new scripts do over the summer month. Fair dues, I have also been guilty of managing similar messages when on their side of the table. And we all have our our experience here in Australia of the "Dance of the Seven Veils" with DW at $PNV.

OK, now I've got that off my chest, on with my analysis and key takeaways.

We've had a lot of posts on $NEU from several members with a lot of data and sound bites, so I'll not repeat any of it. Rather, I will lay out some calculations, based on the US alone, and then use that as a basis for further discussion of value and risk.

Methodology

I have decided to use a range of M&A mutliples of forecast peak sales to set out a range of scenarios for the value of DAYBUE in the US to $NEU.

Method is as follows:

- Market size (A): base 5,000. Range 6,000-9,000,... so conservatively I am taking scenarios of 6,000 and 7,500

- Long Run Persistency (B): 50% - there is upside and downside, but I'm keeping that simple

- Peak Market Penetration (C): scenarios of 40%, 45% and 50% (we're already at 30%-33%)

Revenue Per Patient (D) : As a shortcut, I used an RBC Capital Note from June 2024. They set out their calculations using dosing assumptions and cost per patient per annum of $585k and a gross-to-net leading to $536k per patient per annum.

The reason I chose RBC Capital, is that they appear to be a House Broker, who undertook or commission some detailed market research to support the valuation. I'm therefore not accepting their market assumptions, as I think they might be biased, but there dosing and revenue per customer assumptions appear to be OK.

Continuing the Method:

- Calulate Peak US Revenue: (PRev) = (A) x (B) x (C) x (D)

- Calculate $NEU Royalty Payments from tiered US Royalty Schedule (Roy)

- Apply Peak Revenue Multiple: (M)x(Roy)

- Add Sum of Milestone Payments (SMP)

- Convert to $A

- Value of US DAYBUE to $NEU = (M)x(Roy) + (SMP)

- Divide by Shares of Issue

- Result is an estimate of the $/Share of $NEU attributable to the Payments from $ACAD due to US Sales of DAYBUE

Acquisition Revenue MultipleBenchmarks

For the acquision revenue multiples, I have considered a wide range.

I've rejected more spicey multiples of forecast peak revenues in biotech, which can get up to 12x to 20x and more, and this is perhaps an area requiring further consideration.

Having examined some benchmarks, the reasonable range for a pharmaceutical company with a fully commercialised product in the market is an EV/Forecast Peak Revenue multiple ranging from 5 to 10.

In any event, it is simple enough for you to form your own view.

Here are the calculations:

So What? (Part 1)

If I assume that DAYBUE gets to a peak 45% market penetration within the next 2-3 years, so as to attract an acquisition multiple of 7.5 x Revenue, then the revenue stream to $NEU could be valued in the ballpark of $7 - $12.

Now I have to allow for Canada, Japan, EU and RoW - should these eventuate. These have a more attractive royalty structure, however, they are likley not to be as material in aggregate as the US. Let's assume that the better royalty structure is balanced by the small underlying aggregate revenue, so that Peak RoW equals Peak USA.

Assuming Peak ROW occurs 4 years after Peak USA, then by the same method, its worth $5 - $8 /share

This means the value of DAYBUE to $NEU is $12 - $20 - or $16 at midpoint.

But What About NNZ-2591

NNZ-2591 could be worth $0. But it could be worth 3 x DAYBUE, but another 5 years into the future, so let's say it could be worth 2x DAYBUE today.

My Decision

Who knows what the market will do tomorrow. But now, I just don't care.

My investment thesis is that $NEU is worth the value of DAYBUE, giving me a free option to the Upside of NNZ-2591.

If tomorrow, $NEU tanks 20% to below $14, then my thesis is completely intact, because I believe even given the less-than-stellar performance of DAYBUE, $NEU is worth anywhere from $12 - $46.

There is still uncertainty around DAYBUE, but it is rapidly becoming de-risked with now 9-months of Real World persistency data, and the growing evidence of open label clinical extension data spanning 3 years.

This is precisely the kind of risk I still want in my portfolio. I'm so grateful for the Angelman Trading Halt, because it has given me the time to do a proper analysis.

In fact, if the market throws a tantrum tomorow, I will buy back the one-third I offloaded on the back of the 1Q result.

I'm laying this all out in detail, as I value the views of the other StrawPeople who are following this one closely. (I won't hold my breath while you find the obvious errors!!)

Disc: Held in RL and SM

P.S. I have referred to the work of $ACAD House Broker RBC Capital. While they have a bias that is plain for all to see, they are one of the few houses I have seen that has done a detailed market analysis, based on primary research. Their reaction to the $ACAD result was to mark it down from $29 to $26 vs. closing SP of $15.17. The bias is evident in their elevated valuation; however, the fact thay they only marked $ACAD down by $3 or 11% from their elevant elevated valuation is telling - it is in line with my own view based on entirely indpedendent analysis - apart from the $/patient assumption.

Note: Don’t hold sold out a few months back. I am interested in getting back in.

Are the risks that Phase 3 results are not as good as people are expecting? Digging into the Phase 2 results showed (see below).

I don’t know it’s not exactly what I would say shooting the lights out. Just trying to get a sense if it’s worth getting back in.

I just had a feeling the report (Phase 2 trial shows significant improvements in Pitt Hopkins) released 27/5 wasn’t as up beat as previous.

$NEU announced the initial read-out of it Phase 2 Clinical Trial of NNZ-2591 for Pitt Hopkins syndrome.

Their Highlights:

- Statistically significant improvement from baseline assessed by both clinicians and caregivers in all four efficacy measures specifically designed for Pitt Hopkins syndrome (Wilcoxon signed rank test p<0.05)

- Clinician and caregiver global efficacy measures showed a level of improvement considered clinically meaningful:

- Clinical Global Impression of Improvement (CGI-I) - mean score of 2.6, with 9 out of 11 children showing improvement assessed by clinicians

- Caregiver Overall Impression of Change (CIC) – mean score of 3.0, with 8 out of 11 children showing improvement assessed by caregivers

- Improvements were seen in clinically important aspects of Pitt Hopkins syndrome, including communication, social interaction, cognition and motor abilities

- NNZ-2591 was safe and well tolerated, with no serious or severe adverse events and no meaningful trends in laboratory values or other safety parameters during treatment

- Second positive Phase 2 trial result further strengthens confidence in NNZ-2591's potential relevance for multiple neurodevelopmental disorders

The webinar is at 11:00 today, but in advance of that, these look like very strong results to me – even given the small sample size.

My Assessment

The CGI-I mean score of 2.6 compares with the score of 2.4 in the PM trial, so only slightly less strong, and the difference between the two is not statistically significant.

Equally, the CIC mean score of 3.0 compares with a score of 2,7 in the PM trial. Again, slightly less strong, but again the difference is likely statistically insignificant.

From a physician's perspective 9/11 children showed improvement and from a caregiver prespective, it was 8/11. That's very positive.

See graphical analysis from the presentation below:

So that’s two-from-two at this stage.

We have to recognise that it is still early days for NNZ-2591, with years until we have a commercial drug in the market. But this is very good news, from my reading of it.

NNZ-2591 is currently undergoing clinical development for four rare neurological conditions at Phase 2 clinical trial level. All programs have been granted Orpha Drug designation by the FDA. The results of the trial for Phelan-McDermid were reported in December, showing significant improvements in that condition. The next cab off the ranks is Angelman syndrome, for which the company announced completion of enrolment of subjects in December 2023. This trial is expected to report in Q3 2024. The final of the four, Prader Willi, opened its first site in June 2023, but I don’t recall having heard further information on progress.

Implication for Valuation

Clearly positive.

With potentially 10,000 patients in the US, NNZ-2591 for PW alone could be another DAYBUE, albeit discounted off into the future by 3 years, and perhaps discounted by 50% as the CoS from here. Still, if you value DAYBUE around $20, and you assigned no value to PW, then today you might add anywhere from $5-$7 of SP value. Let's say NNZ-2591 has already recognised half this value for PW, then you'd see the SP rationally increased by $2.50 - $3.50 off today's news. We'll see.

In any event, the market will clearly respond positively to this news.

I recently reduced my exposure to $NEU by one-third, given that I have marked down the valuation of trofinetide based on the latest DAYBUE sales. Clearly, with four potential conditions to treat, the ultimate value of NNZ-2591 may dwarf trofinetide, and today’s result makes me feel more bullish about the prospects for $NEU.

I need to mull this one over. Such it the rollercoaster of drug development, that there is time for a considered response after the heat of the day has passed. $NEU remains by 7th largest RL holding, although after today I imagine it will pop up to 6th or maybe even 5th.

Disc: Held in RL and SM

As the $NEU SP enjoys another SP pop on the back of no new information at a conference this morning, I thought I'd air something that has been bothering me since I analysed the results of DAYBUE in detail over the weekend.

HEALTH WARNING: the charts I have posted below are the just the results of modelling. Even historical data are not disclosed results and there are discrepancies with disclosed facts. So the analysis should not be understood to be my forecast.

With the disclaimer out of the way, I realised I cou;=ldn't fully reconcile the DAYBUE Q1 sales results with some of the statements made on previous calls. Understandably, with the product in the market for only one year, $ACAD are being careful.

Top Level Question: Can DAYBUE sale reach 2024 Guidance (The market seems to think it can with only modest downgrades to TP's for $ACAD and $NEU)

Facts: What do we know?

Sales Revenue ($US m):

Q223 $23.2

Q323 $66.9

Q423 $87,1

Q124 $75.9

Patients Taking the Drug

Q223: not disclosed; 400 prescribers had written scripts, with 7/10 so far converted to paid prescriptions

Q323: about 800 patients taking the drug

Q423: almost 900 patient taking the drug (ok, I assume 890)

End-Feb: 860 patients taking the drug

End-Mar: 862 taking the drug of 1300 who have initiated.

Other Key Facts

Over the winter holidays there were payer delays with getting refills.

January: significantly reduced Rett Clinic days in over 50% of COEs

January-February: discontinuations peaked (due to massive uptake in Q4) exceeding new starters, hence net patient declines.

For the 6 weeks up to 3-May, net patient adds positive again for each week (which means net declines continued to late March!)

We know the Persistency of the drug over time. Below is my modelled curve which interpolates gaps in published data.For the purposes of this analysis we can treat this as a fact (even though there is long term uncertainty).

Modelling Method

With all the above information, I have built a simple model as follows.

Patients (month m) = Patient (month m-1) x Persistency Function + New patients (m)

Guess and iterate patients in months 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 to fit reported numbers

Ramp down new patients in month Dec, Jan, Feb and March to hit reported numbers

Ramp back new patients from May 24 and hold new adds constant to match company statement that we are entering a more linear phase (this was the report at Q4 results and essentially repeated most recently).

So what will the rate of new patient adds be? That's the billion dollar question.

In the scenario below, I've modelled 88 per month. That would take them from 1300 patients having started the drug by end April 2024 (26% of the US diagnosed population) to 2000 (or 40%) by end 2024.

Note: you can't do the maths without the model because you need to apply the perisistency function to each cohort.

Here's what it looks like.

Revenue Calculation

This is the hairy bit. I do a prop rata calculation on the quarterly revenue based on the average modelled number of patients taking the drug in the quarter and BINGO. (I could have been more sophisticared and taken the unit price x n x 75-80% average rate, but I am nore sure that this leads to a better answer. Add to the "to do list".)

For the scenario shown above, my modelled 2024 DAYBUE revenue is: $US346m (versus guidance of $370m to $420m)

So, if I believe the model, the question is what level of monthly new patient adds do I need to hit the bottom of guidance.

Answer: 116

This gives end 2024 patients of 1428 with 2225 having initiated, which is 44.5% of the diagnosed population.

If they can sustain that rate of patient adds, they'll get to 2313 patients by end 2025, with 3613 patients having initiated or 72.3% of the diagnosed population.

I won't model higher rates because I don't think its credible. Here's why. Reaching the entire population will be a challenge. My scenario above assumes linear growth is sustained, which is very unlikely into 2025 as you start to penetrate the second half of the population. (New adds will follow some kind of exponential decay function).

One reason uptake will fall off, is that a significant proportion of the population will likley elect not to try the drug. Side effects and limited efficacy will put some off. Furthermore, there will be accessibility issues.

Implications

First, maybe my modelling is wrong. But do far I haven't found the bug.

Second, maybe my revenue calculation introduces signfiicant error. After all, the model predicts that Q124 revenue should have been $88m, whereas is was $76m, but maybe they really got hit bad by reimbursement delays over the winder holidays?

But if the model is right, why didn't $ACAD update guidance? Who knows. Maybe they want a clear quarter, so they can update when they report in August. But by then if my model is right it will be very, very clear. So continuous disclosure obligations would push them to announce an earlier update.

$ACAD have better data than me, and would be able to build a much better model. (Mine only took an hour's work!)

The Bear Thesis

DAYBUE sales were blamed on seasonal effects impacting: 1) reimbursement and 2) new patient adds.

The model, which is pinned to reported data, help visualise how significant this must have been. It is interesting to re-read the transcripts with this picture in mind.

$ACAD might just hit bottom end of guidance. Too early to tell. But likely guidance will be revised downwards, once they have a better handle on monthly new patient adds. They only have 6 weeks of stabilisation at the last call, so maybe fair enought.

Implications for $NUE

2024 - the US$50m milestone is safe, so that's great news.

2025 - the next US$50m milestone will just be hit in 2025, if $ACAD hit 88 new patient adds per month and sustain this into 2025. If new patient adds fall in 2025, then it will miss.

Canada will help royalties for 2025.

My rough forecasts for $NEU as follows (consensus in brackets):

88 monthly patient add:

2024 $130m ($152m); 2025 $163m ($172m)

116 monthly patient adds (to be clear, I consider this scenario unlikely, based on the modelling)

2024 - $134m and 2025 - $185m

Implications for the Investment Thesis

The modelling confirms my hunch that the $ACAD results point to more than a seasonal blip.

That said, with Canada, Japan and EU in the pipeline, DAYBUE could still become a $bn+ drug by 2027 / 2028.

However, the weight of my thesis has shifted squarely over to NNZ-2591.

The result on the Phase 2 trials due in Q2 and Q3 this year will guide my portfolio weighting.

In the interim, I am bracing myself for an $ACAD downgrade - which would knock the SP.

On balance, my sense of risk-reward has shifted, and I have taken the opportunity today to trim my position size by one-third.

Investment Strategy

I now have a model to which I can history match the Q2 result. This will add a lot to my insights and projections.

If NNZ-2591 continues positive results in future indications - will add back to my full position as SP allows.

Likely catalyst to add back will be the $ACAD guidance downgrade, which I am pretty confident is only a matter of time. Based on commentary so far, the downgrade will be a surprise and so $NEU will take a hit.

If NNZ-2591 results are not positive AND DAYBUE disappoints, I'd potentially exit quite quickly.

Looking to $NEU Strawman Bulls to challenge this ... after all its a strawman!

Disc: Held in RL and SM

As @Nnyck777 has highlighted, $ACAD announced their Q1 results including sales for DAYBUE.

I attended the call early this morning, and wanted to drill into the results in a little more detail. (all numbers USD)

While sales of $75.9m represented a decline of 13% over Q4, this had been signalled at the FY23 results presentation in February.

$ACAD has retained 2024 Guidance of $370-420m.

Decline, what are you talking about?

So, why the decline, if such strong growth is expected for the FY? Three reasons have been cited:

- Many patients who started in Q3 and Q4 faced admin delays with payers over the holiday season

- The initial surge of new patients in Q4 also saw a high level of discontinuation, as not everyone can tolerate the drug well vs. the benefits they see

- Severe weather during the East Coast winter saw access to prescribing physicans, especially, the important Centres of Excellence fall, due to a reduced number of "Rett Clinic Days"

$ACAD reported that prescribing has now picked back up, with the last 6 weeks showing postive net patient additions. Because of this they are holding to their guidance for the full year. The high level of discontinuations in the early part of the year as a result of the surge in prescriptions in Q4 has now levelled off.

My Revenue Analysis

The table below indicates the kind of quarterly revenues that will be required to hit the revenue guidance range of $370-$420 (midpoint $395)

Table 1: Daybue Sales Scenarios Required to Hit 2024 Guidance

So how reasonable is this?

Well, at the FY call, $ACAD disclosed the following information, in terms of number of patients taking the drug:

- End Q3: about 800

- End Q4 about 900

- 27th Feb: 860

- 8th May; [862]

Today, I think I heard them say there are 862 patients on the drug (I'll have to check the transcript when it comes out as I am not sure I heard this correctly).

If that's true, and if 862 represents 6 weeks of net additions, then its likley that Q2 Revenue could reasonably get back to the low point or the mid-point of guidance. What we don't know if what the trough was and what the rate of recovery has been.

If they could get back to 900 patients by end of Q2, that would require net weekly addition of 5-6 patients. At that level, average patients for the Q would be about 870-880, compared with c. 850 in Q4. So, in broad terms, you'd expect Q2 revenue to be north of $87.

Importantly, with all this information and the "noise" of Jan and Feb out of the way, the Q2 result is going to be a key predictor of longer term growth. This is for three reasons: 1) the intial surge of highly motivated patients has passed, 2) we will be clear of the seasonal noise and 3) the product is now moving into a more steady state / linear growth phase.

Other Key Insights

To date, 1300 of a prescribed population of 5000 have started taking the drug.

Although it is believed that 6000-9000 people have the condition in the US, and it is expected that there will be increased diagnoses, we haven't heard any evidence of that, as yet.

9-month persistency is 58% (versus 47% on the Lavender trial), so the real world setting outperformance on persistency above the clinical trial appears to be holding up.

Importantly, $ACAD have reported that of the patients who took the drug during the Phase 3 trial, more than 50% are continuing to take the drug after 2 years. They further said that discontinuations are at a maximum over the first two refills, and decline significantly after refills 4 and 5.

On discontinuations, they have observed the following:

- Some patient discontinue before they have titrated to the effective dose and therefore may not be seeing the benefits

- Some patients prescribed outside of COEs, may be starting on the label dose, and then discontinuing due to GI side effects