Consensus community valuation

Market Cap is $732.3m at current price $1.06 per share

Board Bio's

Mr Leon Hoare Non-executive Chair

Mr Hoare has served as a PolyNovo Director since 2016, and was appointed Chair in October 2025. Until recently, he was Managing Director of Lohmann & Rauscher (Australia and New Zealand), a privately owned, multinational medical device company. Previously Mr Hoare was Managing Director of Smith & Nephew (Australia/NZ) until the end of 2015, one of Smith & Nephew’s largest global subsidiaries outside the US. He served as President of Smith & Nephew’s Asia-Pacific Advanced Wound Management (AWM) business for five years and was a member of the Global Executive Management for the AWM region. In his 24 years with Smith & Nephew, he also held roles in marketing, divisional and general management. Mr Hoare’s career also includes a senior role at Bristol-Myers Squibb in surgical products, and Vice Chair of Australia’s peak medical device body, Medical Technology Association of Australia. Mr Hoare is currently a Non-Executive Director of Medical Developments International Ltd (ASX: MVP).

Mr Robert Douglas Non-executive Director

Mr Douglas was appointed a Director of PolyNovo on 14 October 2025. He brings over 35 years of expertise in medical device technology with a focus on digital health, alongside 10 years in public company governance. He joined ResMed Inc (NYSE: RMD, ASX: RMD) in 2001 and served in leadership positions including President and COO from 2013 to 2023. He is currently a Board and Audit Committee member at Globus Medical Inc (NYSE: GMED), a global musculoskeletal technology company.

Dr Robyn Elliott Non-executive Director

Dr Elliott was appointed a Director of PolyNovo on 28 October 2019. Until recently, Dr Elliott was – Global Head, Strategic Portfolio Management at CSL Behring, a role that is responsible for governance oversight and business value delivery from a multi-billion-dollar capital expansion portfolio. Dr Elliott previously held Strategic Expansion and Quality Senior Director roles within CSL, was the Managing Director at IDT Australia and commenced her career at DBL Faulding. Dr Elliott has a proven track record in product development, clinical trials, regulatory affairs, audits, quality management, project management and operational strategy. Her worldwide experience in new facility delivery, production scale up, strategy, regulatory affairs and audit will be invaluable to PolyNovo as the company scales its operations globally. Dr Elliott is a member of the Audit and Risk Committee.

Ms Christine Emmanuel-Donnelly Non-executive Director

Ms Emmanuel-Donnelly is an accomplished IP and business development professional with more than 30 years’ local and international experience. Ms Emmanuel-Donnelly has a Bachelor of Science with a major in Economics (Hons: Chem) from Monash University, Certificate in Intellectual Property Law from Queen Mary College, University of London, Masters of Enterprise from Melbourne University. She is a member of the Chartered Institute of Patent Attorneys UK and has been on the Board of the Institute of Patent and Trade Mark Attorneys of Australia for over a decade. Ms Emmanuel-Donnelly is currently on the Board of Medical Developments International Ltd and was previously Executive Manager of Business Development and Commercial at the CSIRO, having founded and grown the central IP management team and led the management of CSIRO’s IP portfolio for over 10 years and managed the growth of the CSIRO equity portfolio for 5 years. Previously she was in-house IP Counsel for Unilever in the UK and practised as a patent and trademark attorney for Wilson Gunn (UK) and Davies Collison Cave and Griffith Hack in Melbourne.

Dr Charmaine Gittleson Non-executive Director

Dr Charmaine Gittleson joined the PolyNovo Board on 1 April 2026, bringing extensive global experience across healthcare, life sciences and governance. She is a former Chief Medical Officer of CSL Limited and currently serves as Chair of Percheron Therapeutics Ltd (ASX: PER) and as Non‑Executive Director of George Medicines Ltd.

Mr Andrew Lumsden Non-executive Director

Mr Lumsden was appointed a Director of PolyNovo on 4 June 2021. He is an accomplished Chartered Accountant and finance executive with more than 20 years’ experience locally and internationally. He holds a Master of Arts in Accountancy and Finance (First Class Hons), is an Associate of The Chartered Governance Institute and a member of the Australian Institute of Company Directors. Mr Lumsden is currently Global Chief Operating Officer of Wellcom Group Pty Ltd (formerly Wellcom Group Limited) having previously held the roles of Chief Financial Officer and Company Secretary. Prior to joining Wellcom, Mr Lumsden was a Senior Manager within the Audit and Assurance practice of PricewaterhouseCoopers.

Feb 2026

$1.05 ($0.77 - $1.60)

Following my Straw last week on the 1H FY26 result for PNV, there is now a protracted difference between the market view of $PNV value (trending down from $1.40 to $0.90 in the last 4 months), and the analysts who remain bullish ($1.78, range $1.00 - $2.65; n=8).

Until this latest update, I have been somewhere in between, but given today’s price ($0.90 at time of writing), I've asked myself, is this business becoming under-valued?

So, I’ve taken some over the last couple of days to have a hard look.

1. Background

$PNV has a strong, established and still growing market presence in the US, dominating annual incremental sales (particular given the rapid fall of RoW from its early hyper-growth).

While the segment of dermal repair across is many and varied indications is competitive, served by many treatment alternatives, BTM is still growing strongly, and MTX is achieving very rapid growth from a low base. The latter is more versatile, without the removable covering, it can be using in cases where layers of product are used to treat the wound.

2. Update on the methodology

With each year, I’ve progressively simplified my DCF model, explicit out to 2034, with historic trends tracked back to 2018.

With investment in facilities that will expand sales growth to the end of my updated explicit valuation period (2034), valuation of $PNV comes down to a simple assessment of i) how quickly revenue grows and matures, and ii) the opex investment to achieve this. I assume – for simplicity – a constant gross margin of 92% can be achieved. Moreover, I assume that D&A is flat at $3m p.a., with minimal finance costs and income.

Previously, I’ve modelled S&M, R&D and G&A expense components separately. But as the business matures, I’ve rolled this into a single annual % Opex growth number starting in 2026 and declining linearly to a stated value in 2034. The assumption is that, within this, G&A and R&D will be minor components of growth, with most of the increase due to continued investment in S&M.

The sales and marketing opportunity remains vast, with the following levers and – more importantly – options for management:

- US intensification in trauma (burns now largely saturated)

- US intensification should the FDA approve the FTB indication (although BTM is already been used off-label for this indication)

- Intensification in mature direct markets: UKI, ANZ

- Moving to a hybrid model to drive greater update in distributor markets, especially across EU

- A steady build in SE Asia and India over the medium and longer term

- Registration and entry in Japan and China in the next 3 years

With over 340 peer reviewed publications, a strong global network of KOLs and innovators, $PNVs success in a competitive, global marketplace depends on sales and marketing excellence, assuming that clinicians continue to apply and innovate with the product.

3. Revisiting Some of the Trends

Old model assumptions have been revisited in the light of several key trends.

Revenue Growth

Despite a sharp slowdown in the last 18 months in percentage revenue growth, BTM/MTX are still growing strongly – significantly more strongly that most competitors.

Importantly, significant incremental commercial sales are being added each period.

I’ve tried to capture this in the chart below, and indicate how its plays into my future projections.

In the chart above, I’ve plotted the incremental commercial sales (i.e. excluding BARDA and grants) achieved in each HY period compared with the PCP. This is plotted in the dark blue bars and the LH scale of the chart.

Then on the RH scale of the chart, I’ve plotted the percentage growth in commercial sales in the half compared with the PCP.

I’ve narrowed the scope to the 3.5 years, as the hypergrowth phase of this business is now ancient history.

For each dataset I’ve plotted a curve to smooth out volatility, and then I’ve projected this forward through 1H26, 1H27 and 2H27.

The reason I’ve done this is to sense check the starting point for my HIGH CASE valuation scenarios.

From this I’ve generated 3 revenue growth scenarios and, within each, 3 opex growth scenarios for a DCF running out to 2034. Revenue growth has an initial annual % rate of growth, declining year on year to a final value in 2034. Values are shown below.

Or graphically:

Opex Growth

Noting that Opex grew 18% FY25 over FY24, and that as the business scales, annual opex growth is also assumed to mature, the following assumptions were used:

· Low Cases: starting at 14.0% to 16.0% p.a. in FY26, falling to 3.0% in 2034

· Base and High Cases: starting at 14.0% to 17,0% in FY26, falling to 4.0% in 2034

Other Assumptions:

- D&A flat at $3,0m p,a,

- Interest 0.5% x revenue

- WACC = 10%

- Share on Issue – growing at 1% p.a.

- Terminal Growth Rate: Low 2.5%; Base 3.0%; High 3.5%

- Tax rate = 30%

Outputs

Valuation $1.05 ($0.77 - $1.60)

Input Table

Selected Outputs

Conclusions

At $0.90, $PNV is looking to be lower than my expected value, but it is still not necessarily "cheap". (I benchmarked the revenue mutiples in my Straw last week.)

With the Board and management hopefully now settled, the focus can now be on execution, (without the distractions of "record months" and changing coloured jackets.)

We're still a good 6-12 months until any FDA decision on FTB indication is achieved - a decision which seems likely to push revenue growth towards the higer case scenarios, but also one which would likely rebase the share price.

I'm not investing now. Should the SP fall further to $0.80, then I think I would re-initiate a position, because at that point the risk-reward starts to become compelling again.

For now, $PNV stays on the Watchlist, and we'll see what the FY result brings that might help me narrow my scenarios.

DIsc: Not held

July 2025

$1.75 ($1.27 - $2.20)

A further update to my $PNV valuation, following the trading statement released after the close today.

I've rerun my model, by just putting in a series of more modest revenue growth rates (which appear to have stabilised somewhat H2 over H1).

NOTE: this is not a complete re-rerun of the valuation, but it is a better estimate than my January edition, which was too optimistic on revenu growth and which I therefore want to "correct".

BIG HEALTH WARNING: I need to look at the FY financials when these are available in a few weeks.

That said, DW's forecast for EBITDA of $11.2 - $12.4m is eerily in line with my central case ($11.7m) - but remember, even a broken clock is exactly right twice every day! The cash part of my model for FY25 isn't so good, so something ain't quite right.

Disc: Not held - staying on the sidelines until I can see the full picture.

Disc: Not held - staying on the sidelines until I can see the full picture.

January 2025

$2.20 ($2.00-$2.50)

This is a placeholder following 1H FY25 revenue report, which appears to take higher value scenarios off the table.

This is a rough estimate because cost structure can make all the difference so will update after the full financials are in.

August 2024

$2.60 Range = ($2.30 - $3.50)

Full model rebuild following FY24 results. Results of valuation broadly in-line with previous modelling - just a simpler model, which will be easier to update in future.

In FY24 $PNV passed through the profitability inflection - so you can still get pretty much any valuation you want, depending on what you believe.

Lot's of upside not captured in this range, but the downside is better characterised.

See today's straw "Valuation" for further details, assumptions and outputs (27/8/24).

----------------------------

February 2024

Manual adjustment by +5% to reflect growing evidence of capital discipline, as revenue growth strongly outstripping cost growth.

(January's improvement accounted for revenue numbers).

Full update after FY results in August.

----------------------------

January 2024

Raised from $2.00 to $2.12

Quick valuation update following 1H FY24 Trading Update.

Overall, tracking in line with my expected valuation.

-------------------------------

September 2023

Value $2.00 Range [$1.63 - $3.30]

See Valuation Straw for details

-------------------------------

September 2022

Value $2.46 (Bull $3.28, Bear $1.63)

This updated valuation replaces my earlier valuation from a year ago of $3.62 ($2.50 - $4.25). I make a comparison of the two valuations at the end of this note.

Detailed 10-year DCF developed to understand sensitivities and key value drivers.

MAJOR HEALTH WARNING – you can get pretty much any result you want in DCF modelling. Therefore, in each year key metrics of sales growth, and key metrics (employee expense, R&D, Overhead, investment) and resulting EBITDA, EV, p/e and EV/EBITDA have been extracted and are tabulated below.

The estimate is driven by the following key assumptions, which are constant across BULL and BEAR scenarios.

Key Assumptions - Common to Both Scenarios

1. Sales and Marketing

Modelled sales are driven by growth of the global sales and marketing (S&M) organisation starting in USA, ANZ, UK&I and Canada (“Initial direct markets” or IDMs)

Sales per S&M Employee reach an “Experienced Average” after two years, with ramp up to “Experienced Average” of: 0% in 0-6 months; 25% in 6-12m and 75% over 12-24m. This has been modelled by data on headcount and sales over the last three years and extrapolating various statement from DW and management on investor calls over the last 2 years. The model will continue to be calibrated over time. (Note: Aroa CEO has said that the ramp-up takes 3 years. This is a sensitivity to be tested.)

The current average sales per “Experienced Average” S&M employee is $1.0m p.a. (Note: This doesn’t history match to the data for 2020, 2021 and 2022 because of access issues during COVID19. Results in FY23 will be the first test in a "clean year".)

S&M build-out extends to Europe, China, JKT, India, Middle East in FY23/24/25

Ultimate growth of sales teams by 2032 in IDM markets is tested by an assessment of number of large hospitals and burn units in each market, to ensure number of accounts per territory at maturity does not fall below 6. i.e., the model explicity tests that it does not over-saturate the market with S&M staff.

As indications extend from burns to wound care and onwards to reconstruction, the amount of work per account will increase.

Sales and marketing footprint in 2032 has 53% of sales force in IDMs, 24% in continental Europe and only 14% in JKT and China. Clearly, there is scope for significant upside, particularly towards the end of the decade.

By 2032 the global S&M organisation comprises c. 500FTE, about 55% of the total workforce, which is not very different from the mix today.

2. R&D expense grows y-o-y. However, as a % of revenue, non-employee R&D expense falls as a % of rapidly growing sales from 14% in 2022 to 7.5% in 2026. It is then maintained at a constant 7.5% of revenue. Total R&D expense (including employee costs) is estimated to reach 15% of revenue based on benchmarks, assuming a 50:50 employee:non-employee split.

3. Investment in Facilities: Investment in facilities is assumed to resume at a constant 5% of revenue per annum. In practice, it is likely to be much lower during FY23/FY24, but eventually additional facilities for growing sales and growing product variants will be required.

4. Corporate, Overheads and Other Expenses: Operating leverage means these fall as a % of revenue from 25% in FY22 to 10% in FY32. They are assumed to scale at 60% of the rate of revenue growth each year. (They were lagely flat from FY21 to FY22, but this cannot be sustained, and is considered to be as a result of resource discipline to avoid a capital raising.)

5. Other assumptions

- Effective cash profit tax rate of 25%

- Discount rate 10%

- Inflation 2.5%

- No debt. (Modest gearing will deliver further upside to valuation)

Key Assumptions - Scenarios-specific

Product uptake

A key uncertainty once accounts are established is the organic growth within an account as surgeons use the product across a wider range of indications, and as new products are added to the portfolio in the longer term (Note: this is not "blue sky" as they already exist). Rather than model different indications and applications (e.g., diabetic foot ulcer), a generic factor is applied to the average sales per account to model this growth. Annual in-account growth modelled is:

- +5% p.a. Bull Case (+62% compounded to 2032)

- +3% p.a. Bear Case (+34% compounded to 2032)

These numbers appear conservative given the statement by Max Johnston in the FY22 Results call that accounts existing at the start of the year saw on average of 88% growth. Clearly, this level of growth represents an adoption curve that must flatten off. In any event, the modelled scenarios are likely highly conservative. However, it is equally important not to double-count the two-year learning curve for the sales and marketing team effectiveness.

The combine effects of i) sales and marketing effectiveness and ii) in-account growth (use, indications, products) means that the average annal sales per S&M employee grows from $0.80m in 2024 to $1.34m in 2032, expressed in $2022 for compariso (Bull Case)n. This is reasonable in that the top performers are already achieving $2m p.a. and recognises that within any salesforce there is a wide range of productivities per employee.

Margins

$PNV currently reported continued improvement of gross margins to 95%, assisted by high volumes and increased plant utilisation.

It is hard to make reasonable assumptions for margins into the future, however the following are considered:

- As product development continues, the product portfolio will become increasingly complex lowering GM

- As the sales mix broadens to include more sales outside North America, averaged realised prices will fall

- As synthetic and biologics continue to displace traditional therapies, product-to-product competition will increase

- Attractive margins and expiring patents will lead to entry of alternatives

- Increasing market footprint will require higher inventories

- It may be more challenging to execute a direct sales model and deals via distributors have lower margins.

Over the modelled period margins are assumed to decline by 0.5% p.a. every year in both the Bull and the Bear case, driven by different factors. In the Bull case, cost of complexity and market mix are the dominant factors. In the Bear Case, greater reliance of distributors and competition are the major factor.

Market Penetration – sense-checking model outputs

2032 sales of almost $900m are sense-checked against 2020 figures on TAM and growth provided by $PNV for dermal repair, reconstruction, and hernia markets. Assuming lower market CAGRs of 7.5% than those projected by $PNV to provide a significant margin of safety, the project Bull Case modelled sales represent the following market shares: dermal scaffold 15%, reconstructions 3%, hernia 2%, with correspondingly lower shares in the Bear Case. There is a significant upside if synthetic implants become the standard of care displacing both traditional methods and biologics. Neither are assumed in the Bull Case. Drug elution remains a blue sky upside, as significant sales from this are unlikely to arise during the period modelled given longer regulatory approval timeframes, and are account for in part by the growth rate in the Continuing Value period (See below).

Continuing Value Growth Assumptions

Both Bull and Bear scenarios assume that $PNV continues to establish itself as a leading, global wound care company, continuing to invest in innovation to drive growth beyond 2032. Continuing period growth assumptions are a significant drivers of valuation. The two modelled assumptions are:

- Bull Case: 7% p.a. growth ahead of growth in global healthcare, given by continuing market penetration outside developed markets, with new products driving penetration of the reconstruction and drug elution markets

- Bear Case: 5% p.a. growth in line with mature, leading healthcare companies. $PNV like remains focused on dermal treatments. (Limited success in reconstructive surgeries and drig elution).

Conclusions

The Bull and Bear cases are both intended to represent reasonably probable cases given everything we know today.

On the downside, major mis-steps such as a botched acquisition, product quality issues or emergence of a new, superior technology are not considered.

Equally, on the upside there is ample room for stronger growth cases. For example, Swami is looking for a bolt-on acquisition that put 100 people on the ground with access to the US podiatric surgery market. If acquired at a reasonable multiple, the revenue synergies could be material over a few years.

Some key indicators to be tracked over the next 2 years, to update the model mechanisms include:

- Gross margin evolution

- Build out of sales and market organisation

- Account growth and $ sales per S&M employee, esp. in USA

- Mix of direct to indirect S&M models (The Canada experience is key)

- Market share (Continue to track Integra and Aroa)

- FDA approvals for new indications; progress of clinical trials; publications

- Evidence of trajectory in most mature markets (ANZ)

Comparison to the last valuation

The major difference between the current valuation and prior model, is that the latest model explicitly recognises the challenges of building out a global S&M organisation. This is now considered the key value driver, particularly given the sluggish growth achieved in Europe via the distributor model. More generally, growth assumptions have been toned down by explicitly considering more of the factors that can slow progress - arguably better representing real life!

Disclaimer:

This is not financial advice. Modelling is for author's personal use only and illustrates hypothetical scenarios. No undertaking is given that model is free of errors. Do not use as the basis for investment decisions.

Why I Think the Market is Struggling with $PNV

Holders might remember I was once a superbull for $PNV and, in truth, it has proven to be a bit of a trading stock for me, which is not my usual style, but sometimes you have to take what you can get.

Today, I attended the 1H FY26 call. Even though I last sold out of $PNV a year ago at around $1.80, I continue to follow it closely and - unsurprisingly perhaps - with the SP now back at sub $1, I have to ask the question "Is this now a buy?". After all, heading in to today's results our "highly esteemed" analyst community had a consensus TP of $1.857 ($1.25 - $2.65, n=8, marketscreener.com). (PS - Thank you for the email DW!)

So you might be forgiven for asking the same question.

I have my hand's too full to write up a complete assessment of the results, so I just wanted to share one killer analysis (below) which perhaps explains why I honestly cannot answer the above question.

First Their Highlights

Commercial highlights: strong growth despite an evolving macro environment

• Group sales A$68.2m up 26.0% on STLY A$54.1m

• U.S. sales A$51.7m up 25.3% on STLY A$41.2m

• NovoSorb® MTX group sales A$6.2m up 195.2% on STLY A$2.1m

• Rest of World sales A$16.5m up 28.3% on STLY A$12.9m

• BARDA revenue of A$2.0m, down (62.5%) on STLY of A$5.4m as expected with the completion of the U.S. Pivotal Trial for full-thickness burns

• Total group revenue including BARDA of A$75.0m, up 25.2% on STLY A$59.9m

• The group recorded Net Profit after Tax of A$0.0m down 99.9% on STLY A$3.3m

• The group recorded EBITDA adjusted for significant items and FX of A$4.7m up 82.0% on STLY A$2.6m

Initiatives throughout the period: key appointments set the stage for the next phase of growth

• Appointed Bruce Peatey as Chief Executive Officer effective from 1 December 2025

• Appointed Amy Demediuk as Company Secretary and General Counsel effective from 16 February 2026

• Completed construction of the additional manufacturing facility in Port Melbourne, meeting all budgetary and operational requirements

My Quick Assessment

With a new Chair and CEO,andt with stalwart, veteran CFO Jan Gielen steadfast with the numbers (and filling all gaps admirably todayin the presentation and Q&A), this was a more staid affair than holders have been accustomed too. Gone is the circus bigtop and red-faced ringmaster, the theatrical flourishes of sheets of BTM, and the long and excited ad lib introductions. No, this was much more like your typical Aussie healthtech small cap preso.

I could easily talk about positive surprises (Australia returns to >50% growth after seemingly, and without explaining being almost flat a year ago) as well as negatives (new R&D facility fire, thankfully insured). There are several others - good and bad.

But below is the one chart I wanted to pull out... my analsysis ... not in the preso pack!

It tracks the incremental commercial sales, half on half, both in $m (LHS) and in % (RHD) terms. And I think it explains why the market is having such a difficult time with this business compared to its cheer leaders (the analysts).

The picture shows just how variable the growth is from one 6-month period to the next. There is no discernible seasonality and, if anything, the volatility of sales growth is increasing.

Overall, there is now doubt in my mind that sales growth is maturing. (The dotted exponential decay fitted to % half-on-half sales growth would be smoother fit across the enture time series, were it not for the bumpy pandemic period of 2H20 to 1H22, when sales rep access to accounts was a challenge. Context matters!)

But at around 25% p.a. annual growth in the US, $PNV is growing faster than competitors and has ahead of it the potential approval for FTB (the fruits of the multi-year BARDA collaboration), possible assignment of CMS codes for use in outpatient settings, and the continued building of evidence in non-burns applications. And that's just talking about the US, and before further trials are conducted into even more indications.

Next there are possible market entries into Japan and China in the medium term, as well as a more proactive short term management of distributor markets. New CEO Bruce Peatey gave some hints of ideas he has, which I would describe as more of a hybrid model - and at another time I will write to explain why this can be very powerful in medical devices for distributor markets.

Now, in terms of financial performance, $PNV just managed to break even in NPAT terms $3,000 (yes, you read that correctly, three thousand dollars!) and so things are set up quitely nicely for a strong second half, financially. On cashflow too, the strong operating cashflows are starting to grow, and with the capex now largely in the rearview mirror, H2 should be significantly free cash flow positive. And from hereon in, $PNV should start to reliably throw off increasing free cash.

Despite the new management, some things never change, and it was slide 18 before we got to see NPAT of $0.0m compared with $3.3m in 1H FY25. (But that's just a perennial bugbear of mine).

But for all the possible market upsides, dermal repair is a contested space. Whereas a couple of years ago I felt that I could generation 3 reasonably tight revenue scenarios with confidence, now, instead of feeling even more of top of things, I find myself with more questions than answers.

So, to the Valuation Question

Assuming $PNV hits FY26 total revenues of $150-$160m - which is a near certainty IMO, then this business at today's SP close of $0.92 is still valued $635m, giving is a market cap / revenue multiple of about 4x.

And that's not cheap when you look at its peer group: $IART=0.6x, $ARX=2.9x, $AVH=1.6x

(I know a revenue multiple is a very poor valuation multiple, but at the different levels of maturity of these businesses as well as the fact that some either still bleeding cash or hovering around breakeven, there isn't another meaningful comparison, so soz.)

I am going to some more work on this business. But I wonder, if the Cheer-leaders start to leave the field, could market gravity bring it further down to earth? Or can the new coach and captain steady the ship, and get everything firing again?

To be clear, I don't think we ever need to return to 30% or 40% revenue growth (as at least one analyst was fishing for today). Those days are behind us. But if the new leadership team can drive a few years of 20-25% revenue growth with good cost control, then this former circus show will start throwing off some serious cash, and then the only clowns will be those that didn't buy today. And that could be a show worth buying a ticket to!

But, honestly, I just don't know.

Disc: Not held (I don't have a current valuation for $PNV)

You would think David would be able to find a more flattering picture.

Maybe not.

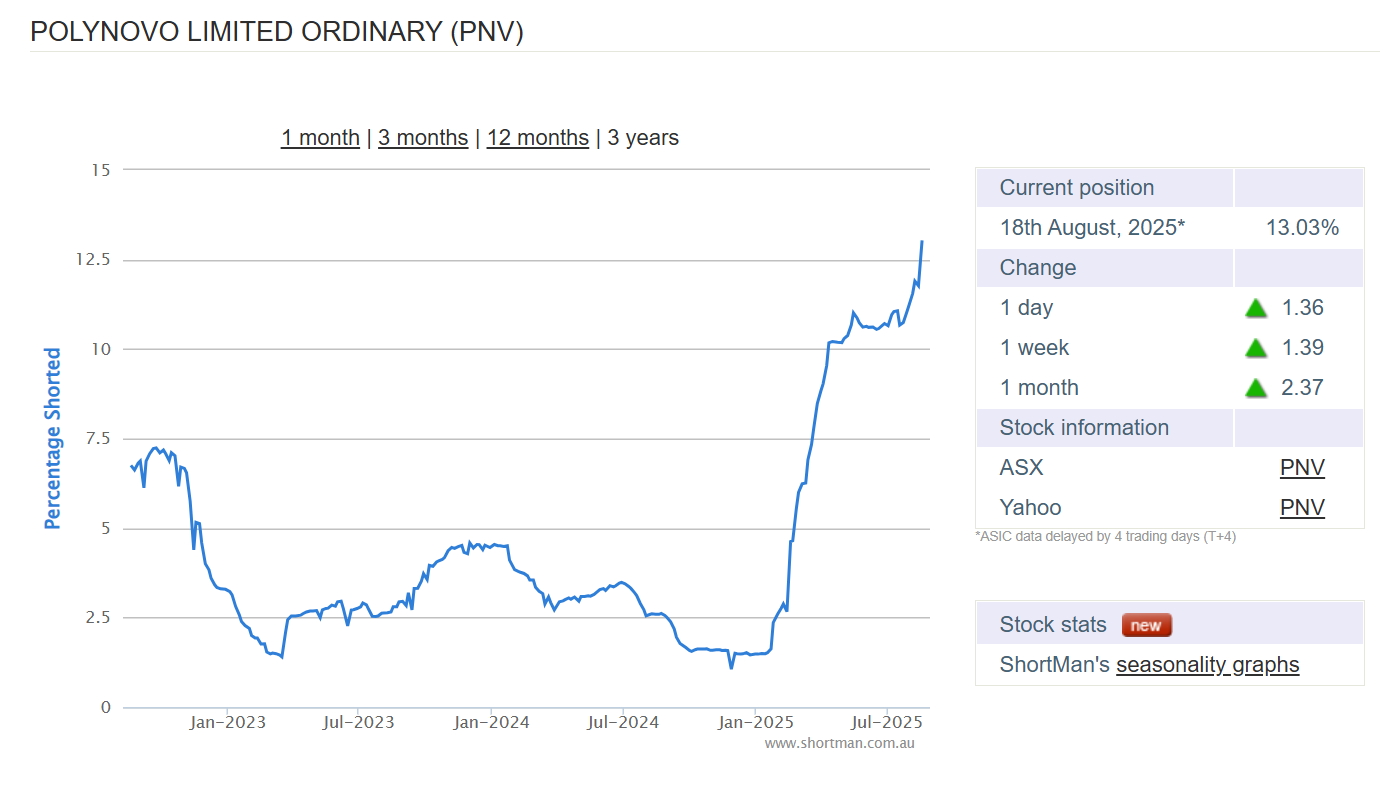

With the FY25 results for $PNV due this afternoon, it is interesting to note the short position (below).

3-year high - while the SP languished at $1.10.

Could be interesting.

Disc: Not held

$PNV's requested a halt as it is about to announce a "significant collaboration" with beta-cell technologies in Europe.

I'm assuming this could be a drug elution product that would use Novosorb as some kind of implant/drug elution carrier to use in concert with one of Betacells drugs? Drug elution technologies were always in prospect at $PNV, but we haven't heard much about it for a while.

Despite the trading haly, I am assuming that this would have to be proven through a full clinical trial program. My assumption is that it is early stage. But I am only guessing here.

There's nothing I can see on their latest pipeline chart (below from Macquarie Conference)

Those who follow me here and also follow $PNV will know that I am NOT a technical investor.

However, I am always eager to learn, and so today plotted the chart below within my CommSec Ap. using the Bollinger band technicals views, which plots the Simple Moving Average (in this case 20-day) with the +/- 2 standard deviations. The basic idea being that when it flies above the upper limit, the stock is overbought and when is flies below, it is oversold. (I have no idea what other technical alogithms say ... @Saiton ... momentum traders are probably offloading?)

So, in this year's version of the $PNV rollercoaster, we've breached the lower Bollinger bound for the first time in over a year.

The other thing I'd note is that the volumes have been modest for a while now, in part because the shorts have quietened down quite a bit on this stock.

Let's overlay newsflow on that:

- 8th May - Record Month

- 23rd July - FY Trading Update (a good news story)

- 16th August - FY Presentation (confirm in the details of the good news story)

- 4th September - Pivotal Trial Complete (quite a good news story)

- 18th Sept and 2 Oct - Director Selling (not good news)

- Number of days since material good news: c. 95

Make no mistake, $PNV is still a highly-valued company, based on the fundamentals, and riding the rollercoaster is a condition of being a shareholder. But I think this is primed well for the next update.

So What?

I don't buy or sell on technicals, I only do that on valuation. And my current valuation is $2.60 ($2.30-$3.50). My problem is, that $PNV is already my largest RL holding. But it has fallen so far below my lower limit of valuation that it sure is tempting to take a small bite, particularly given that I am well within my maximum single stock exposure on a cost-base basis.

Decisions, decisions.

Disc: Held in RL and SM

Following the FY24 results, I have update my valuation for $PNV.

Result: $2.60 Range = ($2.30 - $3.50)

Method: 10 yr DCF

Key Assumptions:

- BTM/MTX only

- Market growing at 8% CAGR

- Assumes market share grows from 2.7% today to 15%/19%/22% by 2034 (Integra estimate of $2.5bn TAM burns & trauma)

- New products beyond BTM/MTX platform treated as a sensitivty to the Continuing Value Growth 5% instead of 4% base.

- %GM declines from 94% (2024) to 88% (2034) due to increasing mix of 1) developing markets, 2) complex product mix, and 3) large increments of capacity that will be under-utilised from time to time

- Capex to deliver just in time capacity: 1st $500m for $27m, 2nd $500m for $40m

- Range of expense/revenue ratios modelled from FY24 to reach reasonable benchmark for global medical device company by 2034.

- WACC 10%; Tax=30%

- Other minor assumptions for interest and working capital scale with revenue

Comments

Compared with my last detailed valuation from Sept-22, I consider the FY24 result puts a much firmer base under the low case.

@Parko5 my top end just hits your $3.50. This is worthy of a comment. There are plausible scenarios where I can get up to $4.00 without stretching my own belief, and so it's worth looking at what's not included (see section below). You'll also see that I contradicted myself a little about revenue growth in FY25. I do indeed model values ranging from 39% to 58%. The reason is a modelling convenience, as the market share increases linearly from today and I didn't break out BARDA. In practice, the "BARDA Effect" that I mentioned in the earlier post is a transient 1-year thing that hits 2025 disporportionately (I'm assuming). It has little consequence in the overall valuation, so I chose to ignore it, as my model is complex enough without adding more complexity!

What's Not Included

Upsides

1. BARDA full thickness burns approval by FDA in 2025, driving "higher for longer" growth rates

2. A strongly favourable IQVIA report in 2025/26 - showing economic and patient outcome advantages of Novosorb, leading to wide adoption by HMOs etc and accerlating market shift away from biologcs More "higher for longer".

3. Award of multiple Federal or State Government Tenders in India, leading to India rapidly taking off

4. Early entry to China beyond Hong Kong (pre-2027)

5. New Products (i.e., beyond BTM and MTX variants) commercialised before 2028 and achieving significant revenues before 2030.

Downsides

6. Emergence of alternative synthetics competitors eroding market share gains in the later years

7. Loss of momentum due to Integra-like product recall (These things happen in medical devices!)

1.& 2. can be argue to be contained within the high revenue growth assumptions. However, the impact could be more material increasing the 2034 market share by accelerating switching from competing treatments. They would also likley accelerate global adoption, particularly in countries without capacity to conduct their own trials.

Model Outputs and Inputs

(I can answer and provide more detail on methods used to get to each of the items below, if anyone wants.)

1. Valuation

2. Model Output Table

2. Model Output Table

3. Input Tables

"i" related to FY24; "f" related to FY34 - model shows linead trend in expense ratios across 2024-2034

Disclaimer: This is intended for my personal use only. It is not advice and must not be used as the basis of an investment decision.

I'm limbering up for the DW Show at 2pm this afternoon with a quick review of the $PNV results. The financials have been well-telegraphed in advance, and I've gone through the Accounts and it's all remarkably close to my forecasts.

FY24 Results and Financial Statements

Their Highlights

- Total revenue including BARDA of A$104.8m, up 57.5% on STLY of A$66.5m

- Strong growth in U.S. achieving record sales of A$68.7m up 49.0% on STLY of A$46.1m.

- ROW sales of A$23.4m up by 73.3% on STLY of A$13.5m.

- Positive cash flow from operations of A$3.7m up 155.7% on STLY (A$6.6m)

- Net profit after tax of A$5.3m (FY23: A$4.9m loss)

- At year end the business had A$45.9m cash and cash equivalents

During the Period, the Company’s other key initiatives and achievements include:

- Record monthly sales in April of A$9.2m (monthly revenue: A$10.5m) and May of A$9.8m (monthly revenue: A$11.3m).

- Initiated a full market launch campaign in the U.S. for NovoSorb MTX in June 2024.

- Strengthened the U.S. team from 93 to 107 (June 2024)

- Increased U.S. customer accounts by 197 from 299 to 496 (June 2024)

- Increased global employee headcount from 218 to 254

- New C-suite roles - Chief Medical Officer, Chief People Officer, General Counsel and President, Asia Pacific.

- Supplied into certain war zones for humanitarian needs.

- Obtained registrations for Bolivia, Ecuador, Thailand, and Sri Lanka.

- Enrolled 120 patients into the U.S. BARDA pivotal trial for full thickness burns.

- Finalised design and selected a builder of the third manufacturing facility to service up to $500m in additional revenue.

- Awarded Victorian Government grant of A$2 million for R&D facilities expansion, subject to customary conditions.

My Analysis

The key for today is that $PNV delivered on their commitment at the capital raise to be profiable in FY24.

EBITDA, EBIT, NPAT, and FCF all positive. The first year we've had this.

Gross Margin % of 94.8%

In the US, with modest sales team growth, new accounts and revenue grew strongly, reflecting the lag effect of 1-2 years between adding headcount and driving revenue per account. A key question is where is the US trajectory from here?

2024 has been a foundational year: 1) broading market approvals across the global where Novosorb can be sold 2) progressing the design of the major manufacturing capacity expansion, 3) re-igniting R&D to build out further products to exploit the platform technology (R&D expense in FY24 up to $11m from $7,4m, but still only a CSL-esque 10% of revenue), and 4) building out the management team. These are all important steps in building a business from this start-up with a genuous product.

In the Chairman and CEO remarks, there were further details on revenue progression in key markets:

- UKI up 81.5%

- EU/Germany distributor markets up 81.2%

- Australia up 38.7%

I take the UKI as a good indicator of what the EU can ultimately do, and it looks like the distributor is kicking into gear. UK/EU growth will be important in maintaining the group trajectory as the US inevitably matures.

The addition of licensing in SUPRATHEL means it looks like $PNV are taking a leaf out of the $AVH book. Once you have the sales foot print, who need to give them more things to help drive contribution margin per account. So, good.

What's not mentioned - India. There is a lack of granularity there. So hopefully the analysts will try to tease out some more on that on the call. After all, we've had 20+ people now working that market for over a year, and there have been some qualitative stories of progress. India does not need to be a "today thing", however, over the longer term the potential for the product to get traction at a reasonable contribution margin in middle income/developing markets helps the long-term growth thesis. (And after all, it's why - or one reason why - Swami joined the company!)

My Key Take Aways

Report entirely as expected. No surprises. So the question is what else can we learn on the call at 2pm.

Lunch now, and then I'll be sure to get my ringside seat for the DW show!

Disc: Held in RL and SM

16-May-2024: Not exactly furious agreement between the brokers on PNV:

Yeah, that's a wide range, Target Prices from $1/share up to $2.75/share and 4 different calls from the 4 brokers - Sell, Hold, Add and Outperform.

Mind you, all four of them wrote those most recent client notes BEFORE this PNV Presentation at the Macquarie Australia Conference last week (on May 8th): PNV-Macquarie-Australia-Conference---Presentation.PDF

This announcement was released on the same day: First-$A9M-sales-month-and-$A10M-revenue-month.PDF

It may not be enough to shift those bearish brokers' views - or their target prices - but it looks positive to me:

I think they've passed an inflection point now, with positive cashflow and positive NPAT for H1, and about to announce results in August for a profitable full financial year (FY2024). The brokers arguments seem to be mostly that people are extrapolating too much sales growth occuring too quickly in the future and that the ramp up is likely to take longer than these bullish investors are expecting - and that PNV don't have the market all to themselves, so there's a competition argument from OM suggesting the R&D spend from PNV will need to remain significant if they are to stay competitive long-term. Well, Duhh! That's what they do.

I added PNV to my SMSF yesterday (Wednesday 15th May 2024) @ $2.17/share, and doubled my PNV position here also. It's not within my cicle of competence, however I'm confident enough that they have a viable product that works and is providing significant benefits, they are now profitable, they're growing at a decent clip, they have a long and wide runway of growth across the entire world and they've only really scratched the surface so far.

I think their results announcement and full year report in August might give the share price a boost, now that they're profitable and the growth across all important metrics is continuing at pace, so I don't claim to know much about the sector, but I reckon this one is de-risked enough for me to hold without a full understanding of every facet of the industry. I also hold CSL and I'm no expert on what they do either, but I don't need to be - coz CSL have their track record of outstanding TSRs over time - mostly through share price appreciation.

I don't mind David Williams - I had a good look into a few of the things he's done in the past last night - and posted a straw here on that - titled #Management - under PNV - and while I generally do not like management to be over-promotional, he's the Chairman, not the CEO or the MD - so he can hype the company up all he wants - and let the management get on with running the company. David is entitled to his opinion - he might not hold 5% of the company, but he holds enough, about $46m dollars worth (21.4m shares).

In terms of valuation, I wouldn't expect a company like this to look cheap, but they do look reasonably priced here considering their exceptional future growth prospects, and that's OK with me.

In terms of the wide range of broker target prices and calls, it suggests to me that either (a) they're not all "experts" in this field, or (b) experts when all given the same data can come to seriously different conclusions about what it is all likely to mean in the future. So what hope do I have? So ignore the valuations and back the management and the product - that's what I've chosen to do now. I haven't thrown the farm at it, but I've got exposure. PNV and CSL. My healthcare sector exposure. Plus some through Wesfarmers' new health division. Plus a little bit of NEU and PME here on SM but none in real life any longer. That'll do. Not in my wheelhouse (circle of competence), but I can live with that exposure to the sector.

15-May-2024: Actually this straw is specifically about the Chairman, rather than about the rest of PNV Management.

Quite a character, our Mr. David John Williams. Chairman of three ASX-listed companies (PNV, IIQ, RMY) and past Chairman of at least three more companies - Medical Developments International (MVP.asx, for 13 years to 28-April-2023), Tassal Group (acquired by Canadian aquaculture company Cooke Inc. in August 2022), and Austin Group (family owned private company); David has also been a director of Select Harvests (SHV, 5 years to 18-Feb-2004) and Amcal which was acquired by Sigma Pharmaceuticals, now Sigma Healthcare, SIG.asx, who entered the ASX200 Index last week (on May 10th) when Boral (BLD) was removed. SIG's m/cap was recently significantly increased by their merger with Chemist Warehouse Group (a.k.a. CW Group).

David is also a lover of either red wine or lots of sunlight, perhaps both, and proficient user of photoshop one suspects.

With a social media presence and a flair for promotion.

David Williams (@DavidJ_Williams) / X

David Williams | Hort Connections

David Williams (businessnews.com.au)

David Williams is also Managing Director of corporate advisory firm Kidder Williams:

David Williams

David has over 30 years’ experience providing mergers and acquisitions, capital raising and strategic advice. Prior to establishing Kidder Williams, David was the Managing Director of Challenger Corporate Finance, Head of the Melbourne corporate finance office of SG Hambros, Head of M&A at ANZ McCaughan, and Head of M&A at Arthur Andersen.

David holds an Honours and Master’s degree in Economics and conducted Ph.D. research on Cooperatives and their capital structures. He is a Fellow of the Australian Institute of Company Directors. David is Chairman of ASX-listed companies; PolyNovo Limited and RMA Group Limited. [Also Chairman of INOVIQ Limited (IIQ).]

Kidder Williams:

Kidder Williams - Kidder Williams

We are a leading adviser to the food, agriculture and beverages industries, and also have extensive experience in medical and digital technologies.

We are globally connected and source international capital for Australian companies.

Kidder Williams Limited provide Corporate Advisory and Investment Banking services to private and ASX-listed companies, including: Corporate Finance Strategy, Mergers & acquisitions, Divestments and demergers, Capital structure, Equity and debt raisings and IPO. We are a leading adviser to the food, agriculture and beverages industries, and have extensive experience in medical and digital technologies. We are globally connected and source international capital for Australian companies. Kidder Williams Limited was originally part of the Mariner Group and set up on its own in 2005.

--- ends ---

OK, so, to recap:

David Williams is:

- the Chairman of PolyNovo Ltd (PNV), and owns 21.4m PNV shares worth around 3% of the company with a current market value of about $46m (@ $2.16/share);

- the Managing Director of corporate advisory firm Kidder Williams;

- the Chairman of INOVIQ Ltd (IIQ), and owns 5.43% of that company, that holding currently being worth around $2.7m;

- the Chairman of RMA Global Ltd (RMY), and owns 184.4m RMY shares, or 33% of the company, that holding currently worth around $12.7m;

- a previous Chairman of Medical Developments International Ltd (MVP), and a current substantial shareholder of MVP with a 13.35% stake worth around $4m (MVP's entire m/cap is now down to only around $36m); and

- a previous Chairman and substantial shareholder of Tassal Group Ltd, buying it out of receivership and arranging the sale of Tassal in August 2022 to Canadian aquaculture company Cooke Aquaculture Inc.

"It isn’t Melbourne investment banker David Williams’ first foray into the salmon game." Photo: Jesse Marlow

Source: Former Tassal Group owner David Williams back for second helping (afr.com) (22-June-2022)

David Williams has also previously been the Chairman of private family-owned company Austin Group and a previous director of Select Harvests (SHV, 5 years to 18-Feb-2004) and also of Amcal (now part of Sigma Healthcare, SIG.asx). Through his work at Kidder Williams, David has worked on numerous mergers and IPOs (SPC & Ardmona, Incitec Pivot), acquisitions (Bega buying back Vegemite), divestments and asset sales (SPC for Coca-Cola Amatil, Tasman Group to JBS S.A. of Brazil, selling Tassal out of receivership to Cooke Aquaculture Inc. of Canada), and other corporate actions, strategic reviews, recapitalisations, etc.

The man has some solid form, and is a rather unique individual.

Further Reading:

Medical Developments International (ASX: MVP) Providing An Alternative To Opioid Addiction - A Rich Life (11-June-2021, by "Downunder Value")

RMA Global Limited (rma-global.com)

Home - Medical Developments International

PolyNovo:

Revolutionary Synthetic Skin Substitutes | PolyNovo

PolyNovo | Healing. Redefined.

Some interesting information in the Macquarie conference presentation.

Two items caught my eye:

- A picture of the capacity resulting from the investment in new facilities. (Not see before although elements of the information have been disclosed before).

I don't recall them before ever having said that existing facilities support a capacity of 180,000 devices (please correct me if I am wrong).

The linkage to revenue is a bit ambiguous, but on one reading it does indicate that in FY25 existing facilities will max out if revenue growth is significantly greater than consensus c. 30% - which I expect it to be. It would have been good to hear the Q&A in the meeting!

2. It's a while since we've seen references to new products - and this time with an indicative timeline. Frankly, I am surprised to see the short term timeframe for SynTrel and Syntrix. But then again, we know surgeons are already using MTX internally, so perhaps its not such a leap.

I wonder if this means they've cracked the polymer property issues which appeared to be holding them back when this was discussed at the AGM. Must be - otherwise the short term timeline is foolhardy, to say the least.

It will be interesting to hear the commenary around this slide at the FY results.

I've already shared some analysis on the $PNV financial results in earlier Straws, which I do not repeat here. However, I commented earlier this week that David, Swami and Jan provided a lot of detail both in their voiceover on the presentation and also in the Q&A.

So, I thought I'd share the key nuggets I extracted from going back over the call and the transcript. In total, I think it provides a much richer picture of the strength of this business, and underscores my bullishness on it as a long term growth stock.

I'll bear all this in mind when I do my major valuation update at FY. There is a lot to consider.

So here goes.

--------------------------

My Overall Key Takeaway: Sustained, capital efficient, long-term growth, driven by existing and new markets, existing and new indications, and potential new platforms. $PNV is now profitable and cash generative.

Key messages

- Strategy and capital allocation - long term growth

- Financials - outperformed their internal budgets and plans

- Capex - material step up in FY25 to build "Mega" for $25m, but fully budgeted in 2022 capital raise

- Markets - now serving 37 markets with increasingly material RoW growing strongly

- Organisation - now built out, so future growth in headcount slowing

- Clinical development - clinicians leading broad expansion of indications; potential for multiple new platforms

1. Strategy and Capital Allocation

DW made clear the strategy is to keep expanding “both in indications and in geographies” wherever they can see the margins. He said this in clarifying feedback he has received on his statement that he doesn’t care about profits. The clarification is that by focusing on growth where he can see margins, then profits will follow. He tweaked his rhetoric by saying, “if you want dividends, you’ll need to sell some shares.”

2. Financials

All details covered in previous straws, but CFO Jan made the comment that they have achieved profitability earlier than budgeted because sales have been above plan

For example, the $8m month in November wasn’t budgeted until April

On cashflow, the business is essentially cashflow breakeven.

DW discussed reporting. He said there has been feedback on their approach of reporting "record sales months". He's discussed it with the Board, and they've decided to continue because they want to keep investors informed as key milestones are achieved.

3. Capex

On the new facilities, the main investment is yet to come

1H24 Capex of $1,1m was design work for facilities plus some R&D equipment

2H Capex “marginal increase in capex as the design process nears completion and we expect to commence construction in 1Q FY25.”

Total planned capex for the third “Mega” production line is $25m over two-year period

Guidance on the spend profile will be given once design is completed (FT24?)

Until new facilities are ready there are no issues with current manufacturing output form the existing two lines, which see continuous improvements in output and efficiency, evidence by the very low % Gross Margin.

Mega will be designed to be modular and scalable, as they plan to have to accommodate many more SKUs than at present.

(My note: Key risk to monitor: will procurement and construction costs increase materially since project first announced in end-22 when the design is complete and contracts let in FY25? A 25-50% cost blowout would not be unprecedented. While that would not be good, it is not really that material, overall.)

4. Revenue & Markets

RoW sales are becoming material "from 16% of total sales to 24%"

Now have sold product into 37 countries

Key market details (not all presented but covered in voice-over):

After not having raised prices in US for several years, there is now an agreed approach for price revisions

In the US, “narrowing the gap” to the market leader in the “difficult burns” category

BARDA trial now 91 patients enrolled; 1st patient enrolled in India (2 centres approved). Looking at options with FDA and BARDA. Base option is to get to 120. Enrolment expected to be complete by May. There will be announcement when it is decided how to close out the trial to a meaningful close. Also working with another FDA agency to see how “real world” data can be sed to give added claims into the trial.

Strong growth in ANZ where already #1 in burns is largely outside of burns

India – “half a dozen tenders” under way. “Getting good soundings.” “Very optimistic that in the very near term we’ll have something to say.”

HK also continues to “trade well”. China – pathway identified, but not yet going beyond HK. Developing plans for extending into Shenzen area (GBA).

Germany: market leader in “Advanced Dermal Substitutes” (4th largest market after US/UK/ANZ – note: Ger. is a distributor market)

Turkey – large initial sales

Middle East – sales driven by a physician who relocated to ME from East Coast US and wanted the product

Japan – have a partner defined and a lead KOL. Working to see if data already submitted to US FDA can be used for submission in Japan with MoH, KOLs and reimbursement agencies.

New demand arising from war zones in Ukraine ($1.2m sale in February - not 1H; “we believe another coming”) and Israel. They believe they are getting some sales orders from other countries that are ending up in these locations, as well as charities.

Several ongoing discussions with charities, UN agencies, Gates Foundation, WHO, MSF, etc. to help get the product to countries that otherwise can’t afford it.

5. Organisation

Headcount +64 on PCP, but only +19 in 1H FY24

Plan for 2H FY24 from 237 to 260 +(23-25)

- US sales: currently 75 (65 reps + 10 managers) going up to 85

- ANZ sales

- R&D and Manufacturing

- Back Office: now have the full teams and scalability

Completing the build-out of the senior management team

- HR lead has started in last few weeks

- Chief Medical Officer joining – leading on FDA and BARDA conversations

- General Counsel about to be appointed

- Close to appointing APAC lead, for entry to China and Japan, and other countries

6. Clinical Developments

My key takeaway: It is clear here is the potential for many years of development leading to new platforms and multiple groups of new indications. Most of this is clinican led.

A key observation is just how important the customer-led (clinicians) work is. (My Note: Just reflect on the following points and consider the tiny R&D budget. I don’t think I’ve ever seen this before in healthcare. There is so much upside to come.)

DFU study: stopped after 25 patients because not getting right wound debridement. Protocol to be re-written and brought back in-hospital (rather than outpatients) to get great consistency needed for a successful trial. Expecting to focus more on to limb salvage – new trial, Announcement on trials coming in a few weeks

Prof Marcus Wagstaff trained 30 surgeons in UK who then took the knowledge onwards to Ukraine

Much clinician-led development taking place into new indications; 230+ publications (214 at FY23), “literally across the entire clinical spectrum”

Customers proposing BTM could be a replacement for allografts (papers on this). Potential to upshift and replace grafts

Several authors proposing that BTM could be a good solution in low and middle income countries where other technologies are constrained

Overall global markets outside US and W. Europe and a few market in APAC “on the fringes” (hey! Swami, that’s no way to talk about ANZ) – we are focused on sustainable, global growth

MTX rolling out in US – demonstrating great outcomes in open abdominal and dehisced wounds. Will start compiling evidence to allow MTX to be rolled out globally. Focus has been using MTX with “expert clinicians” on complex applications, and expecting wider roll-out from July.

Working to be differentiated in connecting KOLs across the world who can teach other surgeons in how to treat acute complex wounds.

$PNV already recognised in burns and trauma, and now looking to go beyond these into:

- Oncological resections of head, neck, scalp, skin and oral cancer

- Potential to use in infections (necrotizing fasciitis and hidradentis) where competitor products cannot deliver

- Getting into complex vascular space to save limbs from being amputated

Developing an implantable platform in hernia and breast. Still not happy to share timelines, but happy with the feedback getting from clinicians. Addressing how to build a “sustainable platform in the implantable space”. (Sounds like still some time off, but I still think this is OK given the growth potential of BTM and MTX)

Working on developing Novosorb Mesh product, currently bench testing, testing with animals, and sharing it with clinicians to establish their expectations on added strength and flexibility. Work is being done to compare with the market leader.

Disc: Held in RL and SM

Three updates this morning - seems about right.

Superbull Macquarie slowly coming into line!

While I am not running my model update until FY, I'll tweak my val. up by 5% just so as not to be too out of whack with the new information.

Disc: Held in RL and SM

October 23

Given Polynovo was a popular topic of conversation yesterday at the Brisbane meetup, I thought I might share my valuation methodology for some feedback after updating for FY23 numbers.

My valuation is based the following assumptions:

- Cost per employee and other expenses as a percentage of revenue are relatively stable.

- Gross margin of 85%. Is this correct/conservative?

- I am conservatively (or maybe not??) assuming the growth isn't going to continue or accelerate from current position.

- R+D of $5-6mil a year.

- Assuming a PE40 in FY28 with 15% discount rate (required return). In all cases this gives a PEG of less than 2.

- Additional 70 employees a year to create the growth.

The two major factors contributing to the profitability of Polynovo and hence my valuation after the above assumptions are:

- The increase in revenue over time

- The extra cost of the additional employees which enables the revenue growth.

I'll start with where I get my numbers from. The table below extracts the % in comparison to revenues from previous years to be able to make the assumptions going forward:

My base, stretch and bear cases are below, orange cells are inputs with the highlighted yellow being the discounted back valuation. My final valuation is the average of the three at $2.19.

Would be extremely interested in any feedback and thoughts on the above! Models are never correct and my model above is somewhat simplistic. When I do the numbers in the way I have Polynovo looks like a potential cash printer but I don't know if my numbers further down the line are a bit too optimistic!

Why I Wish He Wouldn't

I couldn't help myself write this straw on why I wish David Williams would change his investor relations behaviour. The commentators I have seen since yesterday's trading update announcement have made three statements about yesterday's release:

- Why report two months sales data compared to pcp, when the quarter end is a few days away? (There wasn't even an $8m month to at least be consistent with previous patterns of reporting) Particularly when there isn't really anthing to disclose.

- The growth results are strong, fair enough. (Particularly given the languishing SP)

- It doesn't change views on valuation

That's pretty much where I was yesterday in my straw.

But, you say, the market has moved up 14% in the two days. True, but the stock is still down 50% from its current 12m high in February.

So here is why I don't like David's "cherry picking reporting" and it needs a graph to explain. Note that the numbers below are made up, as they seek to illustrate a general point that is applicable to $PNV. The calculated rates of growth are relevant, however.

So here's what it shows. (Don't worry about the absolute numbers, I just picked 100 as an arbitrary starting point!)

Blue Line (acutally a curve), starting at June-22 at 100, this line grows each month at a compound monthly rate of 3.99% or 60% p.a. - which is in the ballpark of $PNVs current annual sales growth.

Orange line: Jul-22 and Aug-22 are depressed below the trend by 20% - indicative of the lumpiness we know exists month to month in $PNV sales. Let's assume we had two bad months at the beginning and two strong months at the end. The "lost" sales from the beginnining are added back in above trend in Jul-23 and Aug-23. So the total sales over the 14 month period is the same for the Blue curve and the Orange curve. It's just that the blue curve is perfectly smooth and on trend while the orange curve is lumpy at each end.

This is my suspicion of what could be going on. Two soft months cherry-picked at the start and cycling two strong months at the end for pcp comparison.

Red Line: So, let's do the maths. What's the ANNUAL SALES GROWTH rate from Aug-22 to Aug-23 (or Jul-22 to Jul-23)?

Blue Line = 60% growth. Red line (for orange curve) = +125%. Over double the underlying growth rate.

That's how misleading annual growth numbers can be if you cherry pick your data-set.

Which is why the high reported numbers in yesterday's ASX release from a management team with a reputation for cherry-picking data shouldn't necessarily result in any change in our view of the underlying value of the business.

Of course, the good news is that, even if the release represents "peak cherry picking", its does mean that underlying revenue growth is still in the region of 50-70%, whereas the market is expecting +42% this year and +34% in FY25.

As a result, no analyst upgrades should be expected, apart from the bears who have a SP <$1.50 or so. (There is one in my dataset with a price target of $1.08. Maybe they'll wake up one day).

Life would be much easier if we got any of the following:

a) Monthly sales, every month or

b) Quarterly sales, every quarter or

c) HY and FY results. Period.

Of course, I could be wrong, and perhaps the underlying trend is stronger. I hope it is. But that's the problem with management who are too promotional and inconsistent in how they report. You just can't tell.

If I wasn't so high conviction on the product and the business, I think I would have given up long ago due to exhaustion.

No doubt, the David Williams Circus will continue to roll on. So,... roll up, roll up.

Disc: Held

I know a few other StrawPeople follow $PNV closely. So this is a question of detail for them.

I've been trying to get my head around the statement: "U.S. NovoSorb sales $46.1m up 44.6% (34.0% in local USD)"

We don't get consistent reporting of numbers, so I have constructured the following table for US Sales in A$ and US$. (Warning - shaded numbers are my calculations and have not been reported by $PNV and may be wrong, particularly given that I am using an annual average FX when volumes vary significantly through the year).

The numbers I am focused on is the constant currency USD sales, %y-o-y difference.

My estimates of the FY-end US Sales Force (FTE) are as follows (note: not reported)

2021 = 36 (reported)

2022 = "54" (At end 2021, DW said Ed would add another 20,... I assume he came up a couple short)

2023 = "75" (And then the same again in FY23)

Note - the last two numbers may be inaccurate, but as far as I can tell, they haven't disclosed US sales force numbers for a bit. DW has thrown some numbers around, and there is as far as I can tell now a sizeable non-Sales US headcount. However, directionally, the numbers make sense given 218 total reported at 30-June-23.

Forget, the fine detail, but doesn't this point to a significantly slowing of US$ sales/ salesperson? We know it takes a year or two for new starters to ramp up their sales volumes. So, given the big increase in numbers over the years, shouldn't there be a sizeable lag effect as productivity of sales staff added 2 years ago continues to grow. So, however you cut it, incremental USD sales of $7-8m FY22 to FY23 appears light.

Maybe something structural is happening. Maybe the initial workforce covered high-use burn clinics, and now incremental workforce are hitting lower returns, with new accounts being less valuable in general hospitals. (By the way, that is an entirely rationale sales and marketing strategy.)

IF (and it is a big if) this is real, its going to masked in FY24 by big numbers coming form emerging markets, and we won't find out until some time down the track that saleforce productivity or market penetration is flattening off.

I feel like I am having to play Hercule Poirot here, and just wish they were more consistent in their reporting. But before I fire off a missive to DW, has anyone else sensed anything?

Has anyone else had a look at this?

$PNV today released 1H FY23 Results ahead of the afternoon's analyst call. Note that top-line revenue numbers have been pre-released. As usual, this straw includes their highlights, my analysis and key takeaways.

Their Highlights

PolyNovo’s ASX release on 16 January 2023 pointed to record sales growth of 67.5%.

The half year audited results attached to this release show:

• Record 1H FY23 sales of A$27.3m up 67.5% on STLY of A$16.3m

• Total revenue including BARDA of A$29.5m up 62.2% on STLY of A$18.2m

• Strong growth in U.S. achieving 1H FY23 record sales of A$22.8m up 61.0% vs. STLY of A$14.1m

• ROW sales of A$4.5m up by 110.1% vs. STLY A$2.1m including new sales in Hong Kong and Canada.

• The Group recorded a net loss after tax of A$3.8m (1H FY22: A$1.6m profit). The profit in 1H FY22 included the reversal of A$4.7m in share awards and share options expense forfeited by the previous CEO and COO on their resignations and an unrealised forex gain of A$0.4m. Excluding these items results in an underlying loss of A$2.5m for the prior period.

During the Period, the Company’s other key initiatives and achievements include:

• A $53,000,000 capital raising

• First $5 million BTM sales month in September (Sep 2022: $5,402,454) recurring in October ($5,263,100) and December ($5,306,540)

• Appointment of CEO Swami Raote

• Received FDA 510(k) clearance for NovoSorb MTX

• Entered Hong Kong, India, and Canada markets in December

• Leased the adjacent property in Port Melbourne to significantly increase manufacturing capacity

• Commenced SynPath Diabetic Foot Ulcer Clinical Trial

• Awarded Victorian Government grant for manufacturing Diabetic Foot Ulcer product (SynPath)

• Increasing sales teams and customer base globally

• Produced for 1H FY23 the equivalent of 74% of the total devices produced in FY22

Analysis

Revenue

On revenue, these were pre-released, so there was no material new information. A breakdown of the monthly sales following the first $5m month in September, shows that both October and December exceeded $5m.

In terms of revenue drivers, Figure 1 (Slide 5) gives a good overview. Growth in Customers (Hospitals) and Employees (a large portion being sales and marketing) are leading indicators of future revenue growth, as it takes time for the sales to grow once both a new account opens and a new salesperson is in place. This should give confidence of a strong trajectory through H2. The slide makes the point that a return to >60% revenue growth marks the return to better customer access post-COVID.

Figure 1 (Slide 5)

Figure 2 (Slide 6)

On Figure 2 (above), I see that ANZ and RoW are now starting to become significant. At $4.6m in aggregate, they are about the same as the USA was in 1H FY19. While ANZ is relatively mature, it is still growing at >60% and we are yet to see meaningful contributions from Canada, Hong Kong and India. Interestingly, there is no mention of Europe beyond UK. So RoW should be expected to maintain strong growth as we start to get early traction in new territories. BARDA is also growing, so I wonder how far off we are from seeing a strategic stocking decision?

Costs

Today is all about understanding how expensive the cost of accelerated expansion is going to be.

Comparing 1H23 to 1H22, the incremental revenue was $11.2m, while incremental costs added are $16.9m. That sounds pretty bad on the face of it. However, the previous period included a credit of $4.7m reversing lapsed options of departing executives, so the underlying incremental cost is only $12.2m, by my calculation. While I am not a fan of underyling corrections - particularly when they happen every period - in this case, I hope we will see some management stability and so I'll let that adjustment pass. Overall, cost increases will always run ahead of revenue growth. So, the real test of this strategy is going to be in the FY23 and 1H FY24 reports.

Of course, it is important to remember that we haven’t seen the full effect of the step-up in cost base as the changes in increased staffing occurred through the half. We’ll see the full effect in the H2 numbers at FY. I expect to hear some questions on this from the analysts on this afternoon’s call about a forward view on cost evolution.

Profit and Cash Flow

Unexpectedly, therefore, we’ve seen a small increase in losses to $(2.2)m.

FCF was $(3.1)m compared with $(3.7)m in the PCP (note: I'm deducting lease costs from the FinCF line from OpCF), so in the context of now having $50m in cash available, the cash burn is sustainable. Of course, in FY24 and FY25 we are going to see a step-up in capex, as new facilities are built. However, if revenue continues to grow at current rates, the cash generation should mean that cash reserves are not eaten into that much.

My Takeaways

With revenue numbers pre-released, and the capital raise clearly indicating that SR had moved DW on from the “boot-strapping” strategy (no doubt a condition of SR’s joining), today was always going to be about how much costs are stepping up to drive expansion. Because of timing, we are only getting a first view of that.

Overall, it’s a bare-bones, no-nonsense presentation, which I personally find refreshing. It will be interesting to see how it is received. The analysts have been used to getting more granular detail, so I expect there will be more digging in the Q&A, as analysts try to get their FY numbers right. (I’m looking forward to the tussle!)

I am happy with the progress shown in this report. Nothing has a material bearing on my valuation, which sits at $2.46 (being the average of distinct bull and bear case DCF scenarios.) I will wait to do an industry read across including Aroa, Integra and Avita reports to see if this offer any insights on competitive positioning over the coming weeks.

Disc: Held IRL ( 6.8%) and SM (22.9%)

New release from biotech daily sent through from David Williams this morning. Does help to put some context to the Aus Biotech space. 2 of my biggest biotech holdings did very well in 2022 PNV and NEU and I anticipate an even better 2023.

BOT even got an honourable mention although I don’t agree with the lumping together with the CBD space. This is a biotech using synthetic CBD for dermatology and anti-biotic clinical trials plus it has a new non-CBD lead drug that is due for FDA approval in Q3 2023. I feel this lumping has meant BOT is one of the most overlooked and poorly understood biotech companies on the ASX.

An interesting summary below in BIOTECH DAILY

Edit: corrected monthly growth in sales past 8 months to 4%, not 4.9% as previously stated.

A very pleasing Q1 FY23 sales result, September quarterly global sales up 73.3% on the same time last year.

The monthly sales graph provided in the announcement was a bit weird, if I have interpreted it correctly! The ‘x’ axis does not show consistent time periods between the monthly sales bars. This skews the graph to make monthly sales growth look linear, which it is not!

Polynovo have done themselves a disservice here. What this graph fails to show is the accelerated monthly sales growth over the past 8 months up to September 2022 compared to the previous 3 periods.

On the graph below I have indicated the time gap in months between each of the monthly sales bars, and calculated the monthly growth in sales for each period (ie. simple monthly growth for the period, not compounded month on month growth).

In the first 8 month period on the graph (Apr 2019 to Dec 2019) the growth in monthly sales was 7.7% per month.

Then for the next 18 months (Dec 2019 to June 2021) the growth in monthly sales was much slower at about 2.1% per month.

Between June 2021 and Jan 2022 (7 months) monthly sales growth increased to 3.4% per month.

The good news is that over the past 8 months the growth in monthly sales has increased by 4% per month. This acceleration in monthly sales growth is very significant for Polynovo, especially if it continues at this rate for the remainder of FY23 and beyond.

Disc: Held IRL (3%), Strawman (12.6%)

ASX Announcement: First Ever A$5m sales month and Record First Quarter Sales A$5 million Sales Month

• The Company is buoyed by its first ever $5m sales month and by the growth trajectory outlined below

• The graph highlights the first achievement of each AUD 1m incremental monthly sales milestone

First Quarter Financial Highlights

• The Company had record (unaudited) September quarter sales of AUD 12.5m up 73.3% on STLY of AUD 7.2m. This includes a record month in September of AUD 5.4m.

• Growth accelerated in U.S, achieving a record quarter sales result of AUD 10.4m up 71.3% vs. STLY (in USD $7.3m up by 61.3% vs. STLY), whereas sales ROW at AUD $2.1m grew by 84.0%

Chairman, David Williams said “By focusing on hiring the right talent and expanding our commercial footprint, we are confident of building a Global leader in Soft Tissue Regeneration based in Australia. However, while the growth trajectory is clear and exciting, month to month sales are still lumpy.”

Chief Executive Officer, Swami Raote said “Our results are a vindication of surgeon recognition of consistent outcomes, better patient experience along with hospital systems acknowledgement of lower complexity and cost associated with NovoSorb BTM. I am pleased with how our teams are now beginning to translate our burn heritage and supremacy into trauma and other acute surgical soft tissue reconstruction opportunities. PolyNovo has always been focused, responsible and capital efficient in delivering results and I look forward to accelerating our global impact.”

This announcement has been authorised by PolyNovo Company Secretary Jan-Marcel Gielen.

About PolyNovo®

PolyNovo is a disruptive medical device company, focused on Advanced Wound Care. PolyNovo is an Australian based medical device company that designs, develops, and manufactures dermal regeneration solutions (NovoSorb BTM) using its patented NovoSorb biodegradable polymer technology. Our development program covers Breast Sling, Hernia, and Orthopedic applications. For further information and market presentations see www.polynovo.com

About NovoSorb®