Consensus community valuation

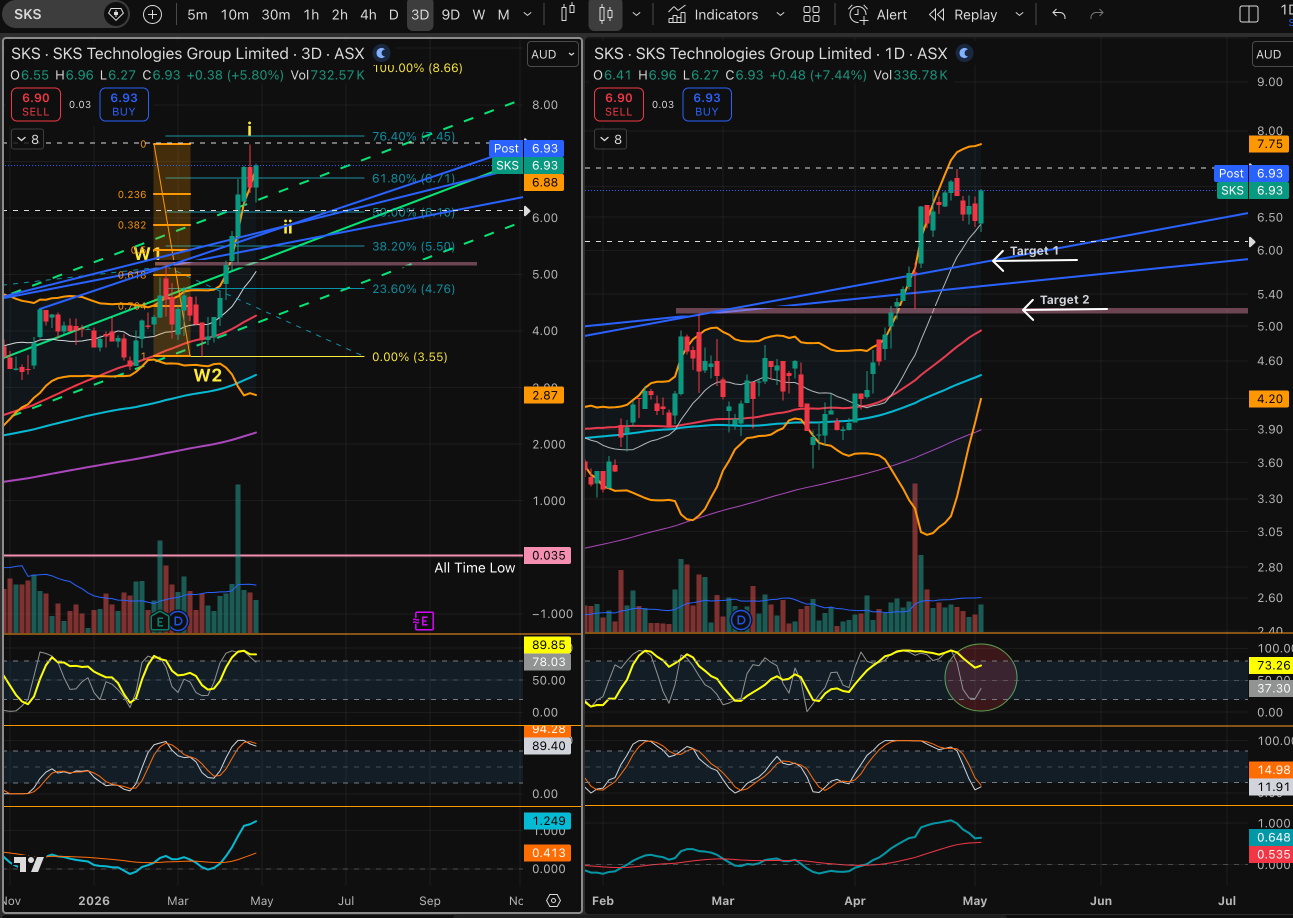

Coming back to @jcmleng question from a charting perpsective with Elliott Wave Theory and Fibonacci levels applied to it from the lows of 0.035 back in July 2020 ish. is looks like the following

Left chart 3d right is 1d

The rising green Lines on the left chart is the LRC (linear regression channel). When it is above and ouside of the top or bottom dashed green lines like this, it usually means it is very extended past the mean ( being the solid green line running up the centre). It works kind of like the Bolinger Bands with a standard deviation of 2.0. As JCM stated, is has retrace to the 23.6%. I make it that it has just completed a W(i) on the 3d. While the compnay has great prospects and has won solid cotract I would like to see it retrace further than what it has so far.

Today has a nice poisitive green bar which is in golf the past three days of trade, so obviously the market is keen to push ahead. Also, stochastic shown below with the circle around it in the indicators also leads you to believe it's making another push. Currently, I believe it's quite exhausted to be that far above the three day LRC line. The three day stochastic is very high, & so too is the weekly and one month stochastics. The question is, will this push up over the next week end up being a double top, then seeing it fall to the levels I'm after or will it continue to push on (it's been known to happen just think of DRO).

For myself, I would not be comfortable in taking a position at the moment with the indicators looking like they are. I will wait and see

Discl: Not Held

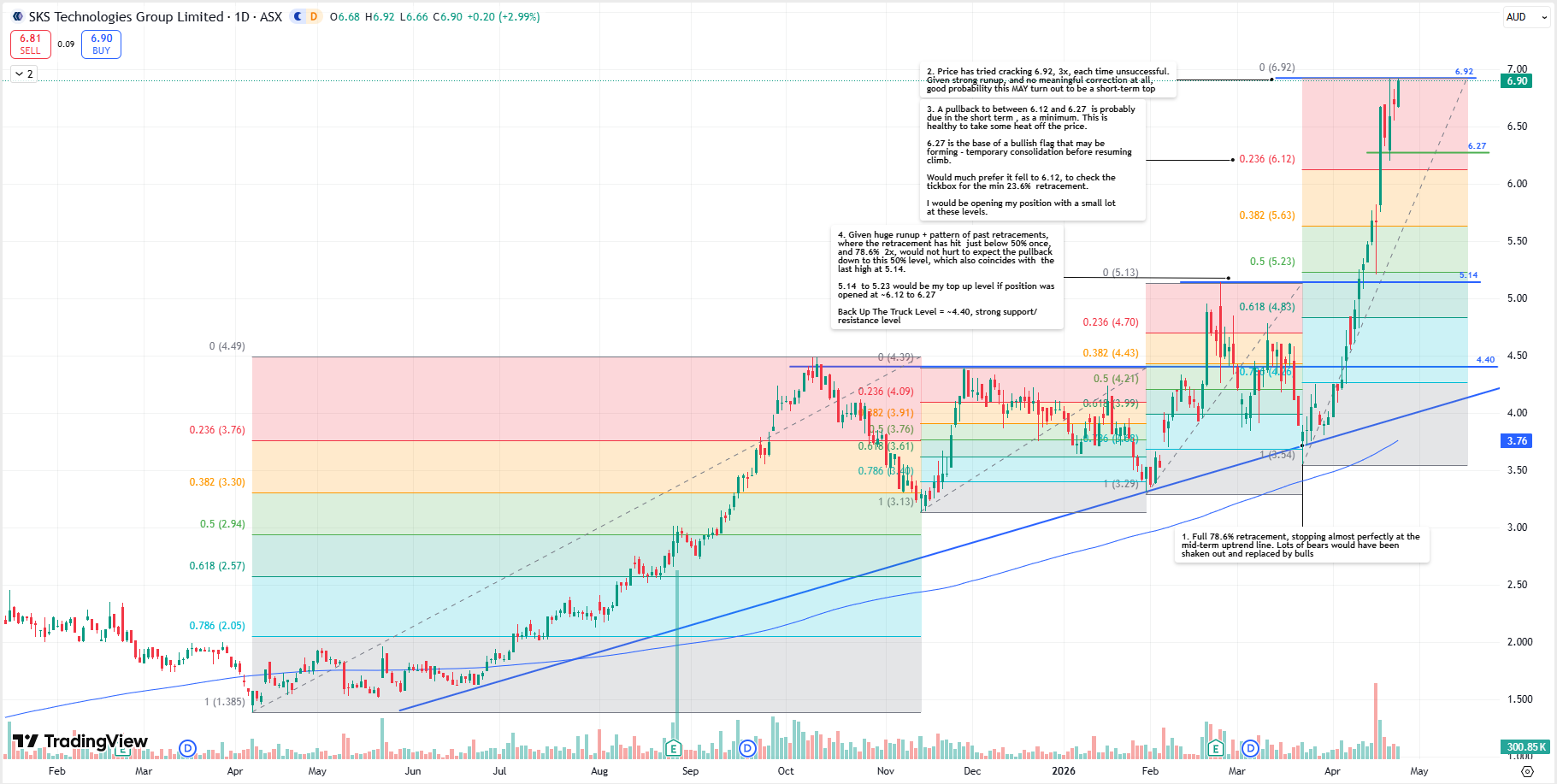

Updating the SKS Chart and comments from a week ago. A top WAS made at $7.31 and the price retraced ~23%+ since.

Question for next week is whether it takes off again, as the minimum technical retracement of 23.6% was met,

OR

it pulls back further to either 38.6% or 50%.

See chart for comments.

Discl: Not Held, Not Intending to Open Position

https://strawman.com/forums/topic/13043#post-43163

@Noddy74, posting the response to your request for comments on the SKS Chart here, from the post above in the SXE folder.

Full disclosure, I don't follow SKS, and have only now looked at the SKS chart for the very first time, please treat this as crystal ball gazing entertainment, with a crystal ball of unknown capability, at best!

It is a really interesting chart from a few perspectives:

1. It is very much "similar" to the SXE chart - nice uptrend, then it went sideways-with-an-upwards-bias for a period, then it launched to the moon. This is likely driven by the DC boom showing up in the books & orders. Similar to SXE, the SKS price is at stratospheric, all-time-high levels, so we have no more historical technical markers from here.

2. $6.92-ish seems to be shaping up to be some sort of a "temporary peak". It has tried to crack this level 3 times, including today, and failed. Given the huge runup + no meaninful correction on the way, the probability is perhaps skewed toward this level-ish being a short-term top, followed by a correction. These sorts of runups are not sustainable indefinitely without some heat being taken away from it. Given today's close at 6.90, a rather strong day, will be interesting to see if the price pushes past 6.92 on Mon, and if so, how far more will it go ...

3. But the longer term trend is up and bullish, no question.

4. The 3 rounds of consolidation prior to the current run up would have shaken out a lot of the bears, leaving remaining/new bulls with the capacity to push the price as aggressively as they have. SXE has not had that 3 rounds of correction, only 1 round really, which may explain why the SXE run up is nowhere as aggressive as SKS.

5. Have marked on the chart where I myself would consider opening a position and then topping up on a pullback - (1) ~$6.12 to ~$6.27 initially (2) then ~$5.14 to ~$5.23 then (3) my BUTT (Back-Up-The-Truck) level ~$4.40.

@Saiton, one for your watch list? SKS has some really nice and "clear" waves, with good fundamentals and Data Centre tailwinds!

Hope this makes sense and helps!

20/03/2026 - SKS is my over-achiever carrying the load for the rest of my poor performers.

It's actually sitting right at the top of my base-case and heading into best-case scenario valuation territory, so while I'm loving the price I'm also a little cautious not to get to carried away.

Valuation estimations:

Worst Case:

- Data centre capex slows sharply

- Global tech slowdown reducing investment (unlikely, but you never know)

- Project delays + cost overruns compress margins

Result: $1.20 – $1.90

Base case:

- Continued data centre expansion in Australia

- SKS successfully executes its data centre pipeline, growing revenue to ~500m by FY28-29.

- compounded annual revenue growth +/- 15%

Result $2.50-$3.80

Best case: with my super optimistic rose coloured glasses on:

SKS becomes a leading specialist in data centre infrastructure, capturing outsized share of a booming AI-driven build cycle. Revenue exceeds $600m with strong margin expansion from operating leverage and repeat work.

- Continued high repeat business from tendering and direct awards

- Strong execution without margin leakage

- Expansion into adjacent high-margin services (maintenance, upgrades)

Result $4.00-$7.00

Summary:

For a high-growth, small-cap, SKS is all the things I dream about. Albeit maybe I was just fortunate to invest early enough to be seeing meaningful gains personally. They have strong operating leverage and provide a nice dividend, whilst simultaneously still growing at pace.

~85% of their work is related to data centres so there's some potential risk here from macro impacts on the segment, but they've got a really strong balance sheet to ride any cyclical waves.

Disc: Held IRL.

This slide from the 1h26 report puts the scale of the datacentre sector in perspective. This is SKS summary of their open tender responses.

I hold IRL, but not on Strawman.

another revenue and NPBT upgrade from SKS- i suspect it wont be the final upgrade for FY26 also. Kicking goals- not cheap per se but fantastic execution from management!

held in RL 9%

SKS has gone back-to-back with a couple of welcome announcements in the last couple of days.

Yesterday it was my lone soldier in green, among a sea of red, after announcing an intent to proceed with a modest acquisition. On paper it looks like a good solid line and length acquisition, smack bang in their existing data centre (DC) fitout vertical, but giving them extra exposure in the state that dominates the DC space. Presumably it was this and the modest multiple they have agreed that the market applauded. The $13.75-15 million, depending on earnout, price represents 5 times earnings averaged over the past 3-years. That would be a reasonable EBITDA multiple, but they're one of the rare companies that have calculated the multiple on earnings, so it actually looks relatively cheap. Whilst not yet binding and non-conditional, it has been agreed so would seem highly likely to proceed. The consideration is a mix of cash and scrip, with the scrip locked up in two tranches, at 12- and 24-months respectively.

Today they've followed that up with a new $130 million DC project in the great state of Victoria, their largest single win to date. This project is expected to deliver them revenues all the way through to FY27 and has led them to upgrade FY26 guidance to $320 million, which would represent well over 20% YoY growth. The win has increased their order book to a new all-time high of $304 million.

SKS has been my biggest winner by far in the last few years. I started buying in December 2023 at 24 cents and have watched it travel all the way up to $4.48 recently. I've bought some and sold more along the way (including 3 tranches in the last 2 months), but it's one that always seems to punish me for not just leaving it alone. Still, it is or is close to, my biggest position so I'm not lamenting too much. It has had a big run up in recent months though, so does the air need to come out of it a bit? If they achieve revenue guidance and get a similar PBT margin to last year, they'll deliver PBT north of $25 million. Based on the significant cash balance they disclosed yesterday, that represents a PBT/EV multiple just over 13. They do need to keep filling up the funnel, but so far they clearly are and have been a big beneficiary of the cloud migration. I dunno, I'm tempted to take at least some of the proceeds of recent sales and top up again at a significantly lower price today.

[Held]

August, FY25 update:

So 92% revenue growth yoy with guidance of more than 15% for FY26. Given 72% work on hand is datacentres you would think some reversion is inevitable (work on hand reduced from 220m in May to 200m in June), but there still 358m in open datacentre tenders. Check out their customers, impressive list (microsoft, amazon, defence, alibaba, etc).

Sure price has 10x since start of 2024 (and up lots since I looked at it), but revenue has grown with that and these guys have executed wonderfully,

NPAT Margin only slightly improved to 5.3% from 4.9% yoy but they did pay themselves an extra 3m (not complaining and there hasn't been much dilution) and they say their cost base can support 350m of revenue. Overall, base case seems relatively conservative for FY26. It's still a cyclical business, H1FY26 may present as high margin and good exit point.

Note, I really should look into working capital and inventory - it's important for this kind of business.

bear case, 10% revenue growth, 5% NPAT margin, pe of 12 => $1.58

base case, 15% revenue growth, 5.5% NPAT margin, pe of 20 => $2.78

bull case, 20% revenue growth, 6% NPAT margin, pe of 30 => $5.63

weighing equally gives $3.22.

Feb, H1FY25 update:

This is a tough one, >100% revenue growth from H1FY24 to H1FY25 - this can't continue, but what could it be? Highly uncertain, but there lies the opportunity!

Assuming 20% revenue growth to FY29, 7% PBT margin, PE 15x gives EPS of 15 cps and $3.66, discounting back 5% gives 3.01.

Forward PE if 260m FY25 achieves @ 2.09 is 18, assume you would get multiple expansion if achieved but shouldn't rely on this. cf. IPG @ PE ~17 which has stagnant growth, similar revenue but higher margins.

Downside risk, I worry margins won't be stable, e.g. 5% PBT gives $2.10 ~ pretty much current price.

SKS had a welcome boost today after securing another $100M data centre contract, this time in western Melbourne. The award sent orders on hand to a record $220M. With the build expected to complete in September 2026, it sets the company up for a healthy FY26, after reiterating guidance for FY25. The project is for fitout of building C and follows SKS's successful completion of buildings A and B on the same site.

Up until today it had been a quiet few months for SKS and the SP had drifted, as it is prone to do. Today's announcement has put some attention back on them and we'll see how it lasts, although it does seem to be a stock that overextends at both the bullish and bearish ends of the barbell so here's hoping it goes on to test new highs.

Interestingly the order book is now exactly twice what it was 12 months ago when it was about to start a tear from circa 70 cents to a 12-month high of $2.45. Apart from the order book, the number of open tenders is also at a new high and the value of those tenders is similarly elevated (although not a record after the awarding of todays $100M contract).

[Held]

Anyone want to guess the time in SKS's results call that the CEO mooted a capital raise because "various organisations are encouraging us to do so"?

[Held]