SaaS SMB accounting and payments platform $XRO reported their 1H FY26 Results today.

I might have said that the SP reaction of -9% on the day surprised me (in truth it did), but as a long term holder of this super highly-rated growth stock, you have to expect that anything much short of perfection gets punished, and the effect was amplified by today's marco data hitting several tech stocks (doubts on further interest rate cuts in light of strong October employment numbers).

However, before diving into the details, there are some contextual issues that set-up an adverse reaction, IMHO:

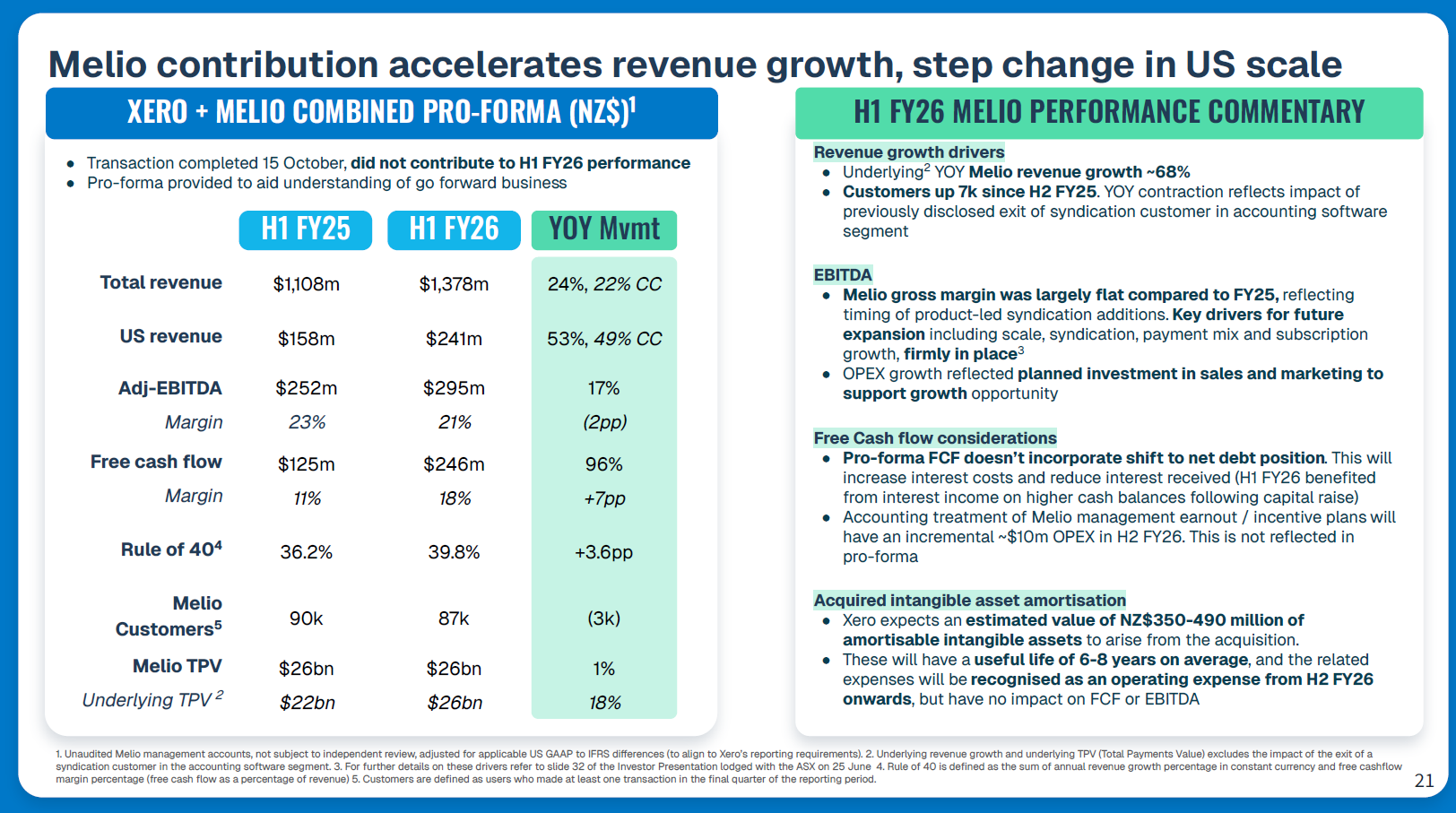

- Acquisition of Melio - many think this is a return to over-paying for material acquisitions that don't deliver the strategic intent. Senitment around this has dragged the SP from a high of $195 in June to a near 18-month low at the close today of $127.

- G&A lept up a whopping 48% driven by accounting treatment of Sukhinder's large remuneration package, which almost got voted down at the AGM. The official explanation is: "primarily due to higher executive personnel costs associated with the accounting treatment of option and sign on equity grants announced last year. The majority of these noncash costs are not expected to recur in fiscal '27."

- While Subscriber additions in North America were strong (+15% to pcp) , revenue growth was relatively weak at +18% on CC. With a welcome breakout of US data (for future reporting with Melio) we can see that Canada is pretty anaemic - but we know that as the economy is hurting as a result of the Trump tariffs. Quelle surprise.

- There is some ongoing concern about the level of development spend being capitalised, at 47%

- Finally, while there are limited numbers around for the 1H consensus, there are reports that EPS missed consensus by 13%.

I attended the analyst call and have sliced and diced the results in detail. Overall, I'm pretty happy.

So much so, that for the first time in ages, I have acquired more $XRO stock today just before the close, adding to my less-than-well-timed purchase yesterday. (Important context is that going in to today's result, the SP was already 28% below the TP consensus, although I think some of the analysts have lost the plot with their lofy targets, which run as high as $230!)

My Highlights

For me there are several highlights:

- CEO reiterated the target to double revenue from FY25 to FY28

- Revenue was up 20% YoY (+18% CC) driven by Subscribers +10 YoY and ARPU +8% YoY (CC)

- Reiteration of capital discipline, with the FY26 Opex Ratio upgraded from 71.5% to 70.5% (including Melio)

- CEO said Melio acquisition is performing above expectionations, and Xero will launch the US payments in $XRO in December.

- Australia performed strongly, with subs +9% to PCP, and revenue +19% in CC.

- UK performed very strongly (IMO given the macro), with subs +13% and revenue +20% in CC.

- Looking past the "one-off" G&A blowout, both S&M and R&D continued to decline as a % of revenue: -0.3pp and -0.5pp respectively. This should give confidence about continuing the operating leverage recent track record.

- Cash Generation was strong, with FCF up 54% to NZ$321m from NZ$209m in the pcp, alebit flattered by interest earned on cash raised for the Melio acquisition and a weak NZD, but strong nonetheless.

- AMRR was also up strongly +26% yoy (albeit only +19% in CC, again because of the weak NZD)

- While Monthly Churn was up slightly to 1.09%, this remains below the long-term pre-pandemic level of 1.15%

- LTV was up 9% in 6 months from $17.95bn to $19.56bn, albeit only $18.52 (+3%) if we back out the FX benefit.

- LTV/CAC weakened again in ANZ to 10.7 from 11.6 in March, explained as being due to chasing customers via the direct channel, where churn is higher for small customers who try the platform out for a few months and decide not to adopt. International stayed steady at the much lower LTV/CAC of 3.3.

My Assessment

Across the board, the results were strong. Yes, there are pockets of relative strength and weakness, if you dig deeper, but overall there is nothing that gives me concern or is surprising.

One orange flag is the need to keep an eye on the ANZ LTV/CAC trend, but this value has been so high for so long, you can argue on economic grounds that they have been underinvesting in the home markets on customer acquisition. Good to see International is stable at the less healthy 3.3, marking the more competitive international markets.

The long term target of doubling revenue by FY28, restated today confidently by Sukhinder, requires a revenue CAGR of 26% or 21% depending on how you measure it. If measured from $XRO's FY25 results of NZ$2.1bn to NZ4.2bn, a 26% CAGR is required. Alternatively, if you start from the pro forma Melio+$XRO combination of NZ$2.36bn, then the actual required organic CAGR is 21%).

This must be achieved while continuing to drive operating leverage. Both CEO and CFO are clear about that.

Clearly, that means that management are confident that Melio is going to transform and accelerate prospects in the US market.

$XRO has a focused strategy: the 3x3 of Accounting, Payments and Payroll across ANZ, UK and North America. Melio and the inegration of Gusto, gives the US business the full offering, with opportunities to sell Melio into $XRO's existing customers, and $XRO into Melio's customers, with a combined saleforce ready to go.

Sukhinder presented a clear US Pro Forma set of financials, and so the US will now be reported separately, with Canada absorbed into International. Yay! The key slide follows.

And so, we will be able to judge progress over the next couple of reports. And given Sukhinder's eye-watering compensation package, I think there will be little tolerance for mis-steps. I guess she knows that. Melio is quite clearly her "big bet" that she can awaken the US Dog that (so far) Hasn't Barked.

And that really is the big unanswered question and one that is worth a lot more than the upfront US$2,5bn paid for Melio. I say that because while ANZ and the UK are solid (with the latter still containing a long runway ahead), those two markets on their own do not justify $XRO's A$23bn market cap. At some point, there has to be an acceleration in North America. And Sukhinder has clearly rolled the dice with Melio. I'm happy she's done that, and Melio looks like a good pick.

Valuation

As I have put more of my RL portfolio into SM, I realise I've never posted my own valuation here for $XRO. And I haven't updated the model for the Melio pro forma FY25 starting point as yet.

So, as a starting point, I am putting in numbers for $XRO pre-acquisition, with simple assumption of organic annual revenue growth of 21% p,a to FY28, Opex Expense Ratio declining to 69% in FY28, $GM to 90% by FY28. (Discount Rate 10%; Tax 30%; SOI gwor at 1.1%)

While the low %GM Melio business messes this up, I am assuming that the Melio acquisition is value neutral, save for the fact that it enables $XRO to sustain revenue growth of 21% pa, with improving operating leverage out for 3 years.

The following table shows the results for this valuation (A$ shown):

I've chosen P/E's of 50, 60 and 70 because in FY28, the growth in EPS is still 26% so, the business will still likely be highly rated at that point, albeit it will have fallen significantly from recent highs!

I've chosen P/E's of 50, 60 and 70 because in FY28, the growth in EPS is still 26% so, the business will still likely be highly rated at that point, albeit it will have fallen significantly from recent highs!

I note that my FY28 EPS is significantly higher than this morning's analyst consensus of $3.26, so that's something to look at again once I have rebuit my valuation for the $XRO + Melio combination.

This gives my valuation for $XRO of $146 ($122 - $170) at YE FY26,

So how does this compare to the analysts? Looking to MarketScreener.com and converting NZD to AUD at 1.16, the analysts price targets have an average of $192 with a range of $96 to $231. Go figure.

Invesment Decision

Even though my valuation hasn't properly modelled the impact of Melio, I am a great believer that M&A rarely adds value on its own. The long term value comes fom how it transforms the organic economic engine. The above valuation is an upgrade to my numbers from the FY25 results, driven by my belief that Melio will transform $XRO's underweight US offering,

With the SP today falling to $127, $XRO has fallen to the lower end of my range, and therefore I am happy to top up, given that the midpoint of my range would deliver a 15% return in 6 months.

So, if Sukhinder is right, and Melio transfroms progress in the US, and ANZ and UK keep doing their thing, then today the market has offered me a chance to top up on one of my longest held ASX stocks (first held in 9-Sept-16).

I've been happy to take that opportunity, increasing my RL holding today and yesterday from 5.5% to 7.8%.

$XRO have just released their FY25 results.

Summary

My Quick Take

Quick thoughts ahead of the conference call at 10:30:

- Revenue in line with expectations

- EBITDA - broadly in line/slight miss

- Expense ratio at 71.8% comes in below guidance of 73%, same as 1H

- NPAT - a miss NZ$228m vs. NZ$245m consensus

- FCF - a strong beat: NZ$507m vs NZ$424m

- Subscribers - all over the place because of the 1H cleanup of "dormant accounts" as predicted, Overall, % subscriber additions rate broadly in line with 1H, with slight upticks in US and UK and downticks Aus and RoW compared with rate of additions in 1H.

- ARPU increase of +15% doing most of the heavy lifting for revenue +23%

- Churn appears under control at 1.03% (underlying) in H2, up from 1.00% (underlying) in H1. Continuing a gentle upwards trends, but still below pre-pandemic levels.

- "Rule of 40" continues to advance higher, with FCF Margin now does most of the work.

Overall, there's a lot to like (not sure how the market will view the NPAT miss), but in the current environment of challenged business confidence, I'm pretty happy with this result. The operational metrics look good, and I love the strong FCF growth of +48%, so that's a big tick for me.

That's just a quick take before I get my morning run in, before the results call.

Disc: Held in RL only

I'm looking forward to $XRO’s FY results tomorrow (investor call at 10:30am). With fewer companies reporting (given the April–March cycle), it’s been a quieter week—so I’ve taken the chance today to prepare and record a few thoughts ahead of the results.

Key question: What are the respective contributions to FCF and NPAT growth from price, subscriber numbers, and operating leverage? And what are the implications for my long-term thesis? How much of a drag has weak business confidence been?

The signals are mixed, but overall, the result should be solid. Business formation has remained sluggish across all major markets (ANZ, UK, US), but $XRO continues to push through price increases, supported by feature upgrades—and frankly, customer stickiness.

MRR churn has remained below pre-pandemic levels, although it has trended upward slightly over the past three years. It'll be interesting to see whether the most recent price increases have had any lagged impact on churn, especially when combined with discounted introductory offers from rivals (which $XRO also deploys).

There’s been commendable cost discipline—overheads, development spend, and CAC are all under control. Thankfully, large M&A has been shelved under Sukhinder Cassidy, now into her third year as CEO.

Analysts using app download and search trend data suggest that $XRO’s growth in 2H FY25 has outpaced international competitors QuickBooks ($INTU) and Sage ($SGE). Will that be borne out in the results?

Of course, we need to be cautious interpreting subscriber metrics. Recall the "inactive subscription" cleanout reported in 1H FY25, which muddied the waters across subscriber-linked KPIs. Hopefully, they've resolved this and now report only active subs. There’s really no excuse now.

Because that subscriber reset was disclosed in 1H, it will distort FY-on-FY comparisons. So I’ll be reviewing the FY numbers in light of the “cleaned” 1H base.

By region:

UK:

The March Budget renewed the push on Making Tax Digital (MTD) for sole traders, with phased implementation over the next three years. While this won’t impact FY25 meaningfully, I’ll be looking for FY26 commentary. MTD should drive new subs at the entry level (Xero Simple and Xero Go), which aren’t big value drivers initially—but some of these businesses will grow and eventually upgrade. With UK business confidence still weak, it’ll be interesting to see how $XRO tracks relative to the 11% subscriber growth posted in 1H. Cloud accounting adoption in the UK still lags ANZ, and with $XRO the market leader, there’s further upside. (# of UK subscribers are ~60% of Australia’s, in a market at least twice as large—though with competition for SaaS accounting customer now more well-established than when ANZ was at a similar stage of penetration.)

North America:

This remains a key long-term interest, with QuickBooks the dominant player. Sukhinder has now had two years at the helm and has put $XRO on firmer footing—focused on the core business, abandoned speculative M&A, and improved cash generation. Now is the time to start assessing whether the team has a strategy to become a credible #2 in the U.S. That was a core objective when she joined. I’ll be watching closely for signs of traction and what the key initiatives are—i.e., new features for US customers, accountant engagement, marketing investments etc. For example, US online bill payments went "live" at the end of April. In 1H, North America posted “underlying” sub growth of 10%—a bit “meh”—so let’s see how FY measures up.

ANZ:

I expect subdued subscriber growth, with most revenue expansion coming via ARPU gains. It’ll be worth comparing full-year subscriber growth to the 11% underlying figure reported for 1H FY25. Given that business confidence will be a driver here, the question is, how much has it come off?

Valuation:

I have $XRO roughly at fair value. The analyst 12-month price targets average $188.70 (range: $155–$206, n=13 via TradingView), against today’s close of $173.86.

RBC recently benchmarked $XRO against other SaaS peers using the Rule of 40 (on an FCF margin basis). Here’s one of their charts. At a forward P/E of 121x, $XRO clearly carries downside risk if it missteps—but relative to SaaS peers, its valuation isn’t outlandish. (I’ve highlighted $INTU, $SGE, and $XRO for reference - if my marking isn't clear, the red marks indicate left ro right $SGE, $INTU, then $XRO.)

Disc: Held in RL ASX portfolio only (6.5%) , not on SM

$XRO announced their 1H FY24 results this morning. These are the first results where we can see the full impact of CEO Sukhinder Cassidy's refocusing the business towards a strategy of profitable growth.

Their Highlights

Xero delivered strong operating results with operating revenue up 21% (20% in constant currency (CC)) to $799.5 million. This, along with disciplined cost management and restructuring outcomes, supported a 90% increase in EBITDA compared to H1 FY23, to $206.1 million. This reflected Xero’s ongoing focus on balancing growth and profitability, and resulted in free cash flow increasing to $106.7 million, representing a free cash flow margin of 13.3% compared to 2.4% in the prior period. This focus was also reflected in Xero’s net profit, which increased to $54.1 million compared to a net loss of $16.1 million in H1 FY23.

CEO Sukhinder Singh Cassidy said: “We’ve demonstrated good momentum this half. As we look forward, we’re sharpening our focus on Xero’s key levers of growth as we aspire to become a higher performing SaaS company. We will continue to balance growth and profitability, while delivering more value to our customers.”

My Analysis

The bottom line improvements (EBITDA +90%, Operating Income +225% and an NPAT result of $54m) are impressive, and they follow logically from the refocusing on to profit.

Interestingly, if I look across the consensus results (as reported a few days ago by GS):

- Revenue growth $800m (+21%) vs consensus of $814m

- Gross Profit $700m vs consensus of $710m

- EBITDA $206m (+90%)vs consensus of $211m

- EBIT of $79.5 vs consensus of $94m

- Subscribers 3.945m vs consensus of 3.964m

So on all metrics, expectations were high, and the result - while impressive, came in a little short.

$XRO has been pulling the pricing lever this year, adding $1.8bn on LTV by growing ARPU from $34.61 to $37.38 with additional assistance from FX and product mix.

Despite the price increases, churn has stayed comfortably low with monthly churn only nudging up from 0.90% to 0.94%.

Rather than go into lots of detail, I want to focus on a few important points.

Subscriber growth is moderating. In the graph below I have compared the 1H %y-o-y additions by region (blue and orange) and I've also added the 1HFY24 h-o-h comparison to FY23 (grey bar).

Its an interesting story.

Figure 1: % Subscriber Growth (1H y-o-y for FY24 and FY23 and 1H h-o-h for FY24)

Looking first at the Y-o-Y comparisons

The powerhouses in ANZ are holding up well, although growth is moderating.

The UK is maintaining solid subscriber growth, despite the depressed economic environment in that country.

North America is also slowing - with the growth rate trending down to the ANZ average, however, $XRO has only achieved a subscriber base in this market of 396k (vs. 584k in NZ!), and while 42k were added for the year, only 12k were added in the last half (NZ added 17k in the last half!).

International, once a hypergrowth segment as $XRO entered markets such as South Africa and Singapore, is cooling significantly.

Now look at H-o-H comparison (1H24/ FY23)

The grey bar shows a very mixed story.

Australia is holding up well. 8% h-o-h is actually 17% annualised!

However, NZ, UK and North America have slowed significantly, with international holding steady at 5%, which is 10% annualised.

The slowdown should not be suprising for three reasons:

- The macro-environment has continued to cool, with businesses tighening their belts and tighter credit conditions likely a brake on new SME starts

- Price increases over the last year have been significant. Although we are not seeing churn for existing customers, perhaps there is some price elasticity for new customers?

- Competition: $INTU has declared Australia, Canada and UK as its priorty markets for international expansion. But there are multiple competing offerings, all on SaaS, in all markets.

This story is supported by the chart below from $XRO's presentation. On the key SaaS value metrics, the international business is of much lower quality with a LTV/CAC of 3.0 compared with the stunning 14.6 in Australia and NZ.

$XRO has clearly broken through into positve earnings territory - a major milestone. The focus on profitable growth and control of costs is turning this into a cash gusher, with $107m FCF and a FCF of 13%....there'll be more to come.

With guidance on operating expenses, $XRO should continue to grow strongly both with cash generation and earnings growth as all three levers contribute: price, subscriber growth and cost control.

Valuation

However, $XRO is still priced as a high growth stock, with a forecast P/E going into this mornings result of 124x and EV/Revenue of 11x.

My Key Takeaways

Directionally, today's result was always going to happen given the strategy shift. We are staring to see the economic power in this business and that is going to drive earnings and cash for some time to come. But in the details, it is a softer result. How the market responds to a soft result and slowing subscriber growth remains to be seen.

Embedded in the presentation are further details of Sukhinder's strategic review of North America. Its simply about focus and discipline in execution. We were given a heads-up at the AGM, which triggered my exist from $XRO in RL and SM. While it makes perfect sense, its not enough. $INTU has a strong incumber position, and there are other alternatives.

$XRO is a quality business, with a great product. Its leadership in ANZ appears unstoppable.

But that's not enough to justify the valuation. The fact is that there are other offerings for SaaS accounting in the material target markets of UK and USA. While the UK is still progressing well, it is apparent that success in the US will be a long haul.

$XRO has started pulling the pricing lever to drive revenues earlier and harder than my thesis to account for moderating subscriber growth. That could have a negative feedback loop on growth and create further opportunity for competition.

So farewell from me for now, and thank you for being one of my best investments ever on the ASX in the last 7years. But investing for me is about numbers and not sentiment. For me, the numbers don't stack up.

Disc: No longer held in RL and SM

I attended the investor call for the $XRO FY23 results. In my earlier straw today, I summarised the key metrics, which I’ll not repeat here. As a replay of the call is available on the IR website, I’ll just focus here on some of the key takeaways important to my investment thesis, rather than giving a summary of the entire results. I very much recommend all holders listen to the replay.

Overall, strong growth was driven by mid-teens subscriber growth (Australia 15%; NZ 11%, UK 14%, NA 13% and Int. 12%) and ARPU by 10% from $31.36 to $34.61 primarily due to price increases.

Australian growth was impressive, given the maturity in this market.

Growth in the UK has ticked up again, so the work to fine tune the model appears to be bearing fruit. Sukhinder believes that HMRC relaxing the framework for full MTD for small businesses is not essential, as small business are increasingly understanding the benefits (including business resilience) of cloud accounting. If this is true then, with a larger potential market size and much smaller penetration than ANZ, there could be a lot of running room ahead in the UK.

The presentation includes all the standard slides with some new ones added providing further transparency into the business performance, so that you get a good understanding of what is underlying and what is one-off. With the various write-downs and Waddle exit, the finances are messy, so this increased transparency is helpful.

Our first in-depth view of new CEO Sukhinder Singh Cassidy

Two words characterised the call and were repeated throughout the presentation and again in the Q&A more times than I can remember: “focus” and “discipline” as $XRO pivots from a seemingly unconstrained drive for revenue growth, to one of “profitable growth”. In a word, Sukhinder gave an impressive performance. Moreover, her presentation was well-structured and clear. In the Q&A where she had an answer to give, it was clear. Where she didn’t, she was candid and explained why.

Sukhinder has been in the CEO chair a little over 100 days, and has acted swiftly in reducing organisation costs, with a $35m restructuring charge in the P&L and the majority of cash costs to come in FY24. The benefits of these are yet to show through. I don’t think this is a slash and burn exercise, because I believe the $XRO cost base had gotten bloated as it tried to pursue too many initiatives as once.

The most important content of the presentation – for me – was Sukhinder sharing her key observations on: 1. North America, 2. Planday, and 3. Modernisation.

Observation 1. North America

We’ve all watched over the years as $XRO has made grinding progress in North America, where it remains unprofitable and a distant fourth to Australia, UK and NZ.

Sukhinder has met with customers and accountants and said she has continued confidence that North America is a critical market and that customers value Xero. $XRO estimate their global TAM is 45m customers (English-speaking markets), of which 34.5m are in North America. Today, NA only has 384k customers - a penetration of 1%, compared with ANZ where 2.14m customers represent 57% of the TAM of 3.7m customers. Even in the UK, $XRO has 970k customers of a TAM of 5.5m, so 18%.

If its early days in the UK, then North America hasn't even really begun.

She was candid in saying that she doesn’t know what the right strategy for North America is, but she committed to focusing on this over the next 6 months and reporting back to investors in November. On the Q&A a couple of the analysts tried to push for more on North America, but with only 100 days under her belt, the internal restructuring and resetting of the cost base has been the right initial focus. So, Sukhinder would not be drawn further on what she believes the answer for North America is. She is clearly keeping all options on the table.

My reflection is that we have to recognise that $XRO was first with a cloud offering in ANZ and early in the UK. By the time it had got going in North America, Intuit (QuickBooks) had launched its cloud offering, and it is the 800lb gorilla in that market. (Just doa Google trends for Quickbooks vs. Xero in the USA and you'll see what I mean!)

However, Sukhinder reiterated the view of previous management, that NA is way behind ANZ on adoption of cloud accounting, and she considers the market opportunity is sufficient for several winners. So let's see what she concludes after her deep dive!

Observation 2. Planday

$XRO took a write-down of $77.9m on Planday, reflecting a “reduction in valuation multiples along with an element of operational performance.” With the acquired Planday CEO leaving and a new CEO in place, Sukhinder noted that it had taken longer than planned to get Planday launched in Australia.

Planday (workforce management software) was acquired in March 2021 for up to Euro 183.5m, however, the upfront payment was only Euro 155.7m, and given performance to date I’m not sure how much of the performance payments were made, if any. However, as the table below shows, there is still $139m of goodwill on the books for Planday, so we might not have seen the end of this part of the story.

Waddle is now completely exited. In the Q&A, Sukhinder made clear that there are plenty of other aps available for lending against invoices, and that $XRO’s focus will be to connect to the aps customers use rather than to build an entire eco-system – an example of clear strategic focus.

Table 1: Goodwill

Source: $XRO FY23 Annual Report

In looking at the above numbers, we have to remember that these are sunk costs and while Planday may continue to muddy the financials, I am not concerned now that it is being managed within a disciplined resource allocation framework.

So where does this leave Planday? From my perspective, the original problem with the acquisition has not gone away. Most of its business is in countries where $XRO is not focused on, i.e., continental Europe. In Q&A as well as in the presentation, Sukhinder made clear that she sees a lot of opportunity in the existing (English-speaking) markets. She wants to focus on these first and importantly to find a way to crack North America. She is not looking to move into other markets in the short-to-medium term. Under Q&A she was asked about India and answered it is a “future option” that they will not be pursuing at this stage.

So $XRO will focus on seeing what Planday can achieve in Australia and in the UK, and presumably preserving the value of what it has elsewhere. There are many other workforce management platforms out there for the SMB sector, and so I expect the Planday CEO will be given a year or two (at most) to see what can be delivered and whether there is an offering that customers really value.

Sukhinder described her resource allocation strategy of a disciplined approach to “core”, “growth” and “emerging” parts of the business. I see Planday very much as in the “emerging” bucket, and it will need to prove whether it moves into the growth stage.

Observation 3. Modernisation

Sukhinder spoke at some length about the multi-year journey to modernise the software stack – its been around a while. This will be key to achieving driving greater productivity and efficiency, as well as bring greater value to customers. It sounds like this will be a core and significant ongoing part of the development spend.

Controlling Costs

Efficiency is a key new focus, measured by operating expenses as a % of operating revenue. This was 84% in FY22 and has been driven down to 80.7% for FY23, excluding the restructuring costs. The target for FY24 is “around 75%”.

If you assume revenue growth of 25% in FY24 (my target, not theirs), then for a FY24 revenue of $1.75bn, moving the cost base from 84% to 75% represents an incremental operating cash flow contribution on $158m before tax. If we use $XRO’s definition of $102m FCF this year, then that would indicate the potential for very strong FCF growth over the year ahead.

Of course, this requires efficiencies to be extracted without impacting revenue growth or investment in the platform. The good news is that Sukhinder has put a marker in the ground and I think this is what the market has reacted to positively today.

Sukhinder’s Growth Framework – Rule of 40

Sukhinder thinks about growth using the “Rule of 40”.Here the goal is to achieve annual revenue growth percentage + annual free cash flow margin percentage (FCF as a % of revenue) totalling 40%.

Under this model, the FY23 result was revenue growth 28% + 7% FCF margin (102/1400) = 35% (- even though I don’t agree with $XRO’s calculation of FCF, and I get a number more like $69m, incl lease payments or $85m if acquisitions are excluded).

If mid-20’s % revenue growth is achieved, this implies FCF getting to 15% of Revenue ... or $260m to hit Suhinders "target" (which she made clear is not a target for next year). But I think this could be do-able given what I've written in the costs section above.

Valuation

With the SP breaking back above $100 for the first time since over a year ago, $XRO is not cheap at an EV/Revenue multiple of 12x or a whopping 55x $XRO’s "adjusted" EBITDA.

Prior to analyst revisions, target prices average $100 (n=16, min=$61 to max=$128; www.marketscreener.com ). It will be interesting to see what the revisions bring. It comes down to whether the analysts see more value in a more focused, higher margin set of markets vs. previous assumptions. What they assume about NA is anyone's guess, and this will likely explain a continuing wide divergence in views on value.

My own DCF – which requires significant updating – has a central value of $113.

For now, I am happy to have bought back into $XRO, and I am happy to hold and see what the team can deliver over the next year.

Finally, a Note on my journey with $XRO

I was a long-term holder (first purchase 9-Sept-2016) and $XRO has been my most successful ASX investment in absolute terms. However, I lost patience with the approach of previous management to fail to follow a more balanced approach to growth, bailing out of my last holding in June 2021 (RL only).

When the new CEO was announced I re-initiated a position in November 2022 (RL and SM). What had separated this business from my thesis was a management that didn’t appear to prioitise cashflow generation, and were following what was in my opinion a dilutive and unfocused strategy without addressing the key question of whether the core offering could succeed in North America. I felt $XRO needed a fresh set of eyes from someone not wedded to the decisions and statements of the past.

Sukhinder’s approach is exactly what I think is needed, and so my conviction for this business has increased today, and the thesis is restored. Let’s see if the team can deliver, and let’s tune in in November to hear what Sukhinder has decided about North America!

$XRO is unproven in terms of its ability to deliver shareholder value through sustainably growing Free Cash Flows. Therefore it qualifies for inclusion in my SM portfolio, which is why I added it in November 2022.

Disc: Held RL (5%) and SM (9%)

$XRO reported their FY23 results this morning. The table below from the release show their highlights.

The financials are messy, due to yet more write-downs of acquisition goodwill (Waddle and ... wait for it ... PlanDay). However, looking past the profligacy of the past, on an operating basis the result is strong, with 28% revenue growth, Operating Cash Flow of $390m (up 65%) and FCF of over $100m.

Costs have been well-managed, and we are yet to see the full benefit of the cost reduction effort initiated late in the financial year. The restructuring costs of $35m are also a drag on the financials.

As highlighted above, the operating leverage is now showing through strongly and with disciplined management, we will now start to see $XRO becoming a strong cash generator.

Growth was driven both by new subcribers, price increases and usage, and monthly churn stayed low at 0.9%. Importantly, as the major price rise was in September, with a small one in mid March, there is a strong revnue exit run rate for the year, which sets up FY24 with a good start.

Customer additions were strong in Australia (+15% yoy) and UK (+14% yoy), and were double digits across the board. North America still making steady but slower progress at +13% (competition from Intuit is just too strong).

Jumping on the Investor Call at 10:30 and will report any significant insights over the next day or so.

HIGHLIGHTS FROM RELEASE

CASH FLOW TRENDS

(Note my numbers for FCF are different from their reports, as it looks like we include/exclude different items in getting to FCF.)

Disc: Held IRL (4.8%) and SM (8.3%)

@TycoonTerry interesting perspectives. I am also a long term holder (9-Sept-16; $19.36; courtesy of Matt Joass, MF Pro)

I think it is important to understand how $XRO got to where they are and the strategy that drove the acquisitions - which I am sure you know.

$XRO started as an NZ small business accounting software provider that was the first to disrupt traditional accounting by providing a cloud solution that removed a bunch of on-prem hassles from business users, and more importantly transformed the way businesses could manage their book keeping and their relationship with their accountants. Both business owners and accountants appear to love it.

Starting in NZ, which has an entrepreneurial culture and is adept at rapid adoption of innovative home-grown solutions, over time it grew to dominate the market - achieving c. %60 market share in cloud accounting in NZ by 2021.

This provided the spingboard to enter Australia, where the incubment - MYOB - was not yet cloud-based. Rapid growth in Australia turbocharged an already profitable and focused NZ business, and delivered the operating cash surplus for reinvestment in the platform and international expansion.

The various acquisitions were part of building an overall integrated SME finance "ecosystem". At one stage around 2018-19, some pundits were saying the blue sky valuation was $100bn! I think we all got wrapped up in that story - I certainly did.

In truth, the various acquisitions to broaden the scope of the $XRO platform are essentially unproven in large part and international expansion faced inevitable competition, nothwithstanding the relative immaturity of cloud-accounting. As international expansion was taking off, everyone else (Intuit, Sage, etc.) also moved to the Cloud. So the initial point of difference in ANZ was lost.

Furthermore, each local jurisdiction requires a tailored implementation and, the relationship between businesses, book-keeping, accountants and tax professionals are different, requiring both localised code and local go-to-market strategies.

A further complication is that UK, where $XRO had a good initial run at a market that could be 2-3x ANZ, got bogged down in BREXIT and COVID blues. HMRC relaxed some of the MTD deadlines that provided initial impetus for small business and sole traders to go online, so growth there has slowed and they face more competition than in ANZ. However, they still have a strong position and are in the early days compared with ANZ. (See Figure 1)

See Figure 1 (UK), Figure 2 (USA) and Figure 3 (Canada). Competitive position looks strong in UK, very weak in USA and moderately weak in Canada. However, together USA and Canada are much larger markets than ANZ and UK combined, so even a small business here - if it is focused - might ultimately be profitable. Also, cloud accounting adoption has been relatively quick in ANZ, with other countries several years behind ... especially USA!

Figure 1: Google Trends Analysis for UK (Xero, Quickbooks, Sage; last 5 years)

Figure 2: Google Trends Analysis for USA (Xero, Quickbooks, Sage; last 5 years)

Figure 3: Google Trends Analysis for Canada (Xero, Quickbooks, Sage; last 5 years)

My concern, is that with Waddle, I wonder if we are seeing a foretaste of a future larger writedown of the more material PlanDay acquisition? There hasn't been much newsflow of $XRO kicking goals with PlanDay, and despite it being available in Australiasince 2021, Google Trends almost shows a flatline, when compared with Deputy and ELMO - other SME solutions in HR and workforce management. I also haven't met any Xero users who use it.

So why do I still hold $XRO? (albeit regretting not offloading at $150!)

At its core, is a set of functions valued by customers. Clearly the cloud accounting is core, and only $XRO management truly understand the respective value of each of the other functions in the platform. I believe that the expansionist mindset of previous management meant that they were not examining this core.

The new CEO appears to have got this. I believe there is headroom to grow the core adoption and value in the established markets: NZ, Aus, UK, USA, Canada, South Africa, Singapore, and the operating cashflow is strong enough for $XRO to continue to innovate and build its core offering, while also generating free cashflow.

I had been waiting for and hoping for this change of direction. I almost sold out last year despairing that we would ever see it under Thodey / Vamos, but I decided to hold on when the new CEO was announced.

In truth, I now have a much lower conviction on $XRO. I am going to give the new CEO 12-24 months to see whether she can move the dial. I will not hold any future write-downs of past acquisitions (e.g. PlanDay) against her, as that would be consistent with my overall thesis and in any event these costs are sunk.

Disc. Held