Price History

Premium Content

Premium Content

Premium Content

Recent Buying

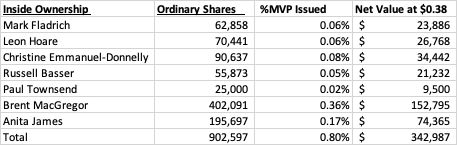

Russell Basser

30 October 2025

Buying On Market 40,000 shares at average price $0.7056 ($28,227)

Mark Fladrich

30 September 2025

Buying on Market 62,858 shares at average price $0.7099 ($44,629)

Paul Townsend

22 September 2025

Buyiing on Market 25,000 shares at average price $0.6714 (16,785.31)

Management Bio’s

Mark Fladrich - Chair

Mark is an experienced leader with over 30 years of experience in the pharmaceutical industry, specialising in commercial, strategic, and operational roles across a broad range of therapeutic areas, including pain management.

Most recently, Mark served as Chief Commercial Officer at Grunenthal, a privately owned German company with a strong presence in Europe and Latin America. During his time at the company, he expanded Grunenthal’s commercial presence into the US in parallel with the relaunch of a non-opioid chronic pain management treatment.

Prior to this, Mark spent 23 years at AstraZeneca, holding various senior roles, including Vice President of Global Strategic Marketing, Country President roles in Germany, Australia and New Zealand and Regional Head of Southern and Western Europe.

Mark has also held leadership roles at Allergan and Faulding Pharmaceuticals in Australia.

Currently, Mark is the Chair of QBiotics, an Australian life sciences company, the Chair of the Strategic Advisory Board for Atacana, a global pharmaceutical and biotech industry consulting firm and serves as a Board Observer and Strategic Advisor at HealthMatch, a Sydney based digital startup who have developed a patient centric platform for clinical trial recruitment.

Leon Hoare - Non-Executive Director

Leon is an accomplished commercial leader with expertise across multiple Life Science sectors. He is currently the Managing Director of Lohmann & Rauscher, Australia & New Zealand (ANZ), a private EU based medical device company.

Previously, Leon was Managing Director of Smith & Nephew (S&N) ANZ, one of S&N’s largest global subsidiaries outside the USA. He served as President of S&N’s Asia Pacific Advanced Wound Management (AWM) business for 5 years and was a member of the Global Executive Management for the AWM Division (as one of three Regional Presidents).

In his 24 years with S&N, he also held roles in marketing, divisional and general management.

Leon’s career has also included a senior role at Bristol-Myers Squibb, and as Vice-Chair of the board of Australia’s peak medical device industry body, Medical Technology Association of Australia. Leon is also the Chair of MDI’s Human Resources Committee.

Public company directorships in the past 3 years:

Polynovo Limited since 27 January 2016

Christine Emmanuel-Donnelly Non-Executive Director

Christine is an experienced IP and business development professional having 35 years’ experience locally and internationally.

Christine is a former Executive Manager of Business Development and Commercial at the CSIRO, where she led the management of CSIRO’s IP team and IP portfolio for 14 years and managed the CSIRO equity portfolio for over 5 years.

Prior to this role, Christine was in-house IP Counsel for Unilever in the UK and practised as a patent and trademark attorney for Wilson Gunn (UK), Davies Collison Cave and Griffith Hack in Melbourne.

Christine is also currently chairwoman of Impedimed Ltd and non-executive director of Polynovo Ltd, Pikcha Holdings Ltd, trading as Seminal. She was previously on the Board of the Institute of Patent & Trademarks Attorneys of Australia for 13 years.

Public company directorships in the past 3 years:

Polynovo Limited since 13 May 2020

Impedimed Limited since 2023

Russell Basser Non-Executive Director

Russell is a qualified physician, with over 30 years of international medical and biopharmaceutical experience. He has worked as a medical oncologist in Melbourne prior to joining CSL in 2001.

During his 21 years at CSL, Russell held multiple global executive roles, including Head of Global Clinical Development, Chief Medical Officer and Senior VP of Research and Development for CSL Seqirus. He has substantial expertise in international drug and vaccine development and spent several years based in the USA.

Russell currently serves as a non-executive director on the Boards of Starpharma Holdings Limited and Doherty Clinical Trials. He has previously served on the Board of the ANZ Breast Cancer Trials Group and the Hadassah Australia Medical Research Collaboration.

Paul Townsend - Non-Executive Director

Paul is an experienced global finance executive with a strong commercial focus and reputation of delivering results across diverse industries, including manufacturing, resources, consumer products and academia.

Paul has substantial ASX CFO experience at organisations including Nufarm, Asaleo Care, and Pacific Hydro, as well as Monash University, bringing a wealth of knowledge to MDI.

His extensive track record includes business turnarounds, new venture start-ups, mergers and acquisitions across local and global markets, navigating equity and debt capital markets and implementing changes necessary to deliver strong earnings growth, robust cash flow, and balance sheet optimisation.

Paul’s strategic mindset and leadership have consistently enabled successful business outcomes and the generation of long-term value. Paul has a Bachelor of Business (Accounting), FCA and GAICD.

Brent MacGregor - Chief Executive Officer

Brent joined MDI as Chief Executive Officer in November 2020.

Previously, Brent was the Senior VP Commercial Operations for Seqirus, from its inception in 2015 until 2020. He has also held roles as Head of North America for Novartis Vaccines and Diagnostics and Managing Director ANZ, Managing Director Japan, VP Global Marketing, and Global Head Strategic Planning for Sanofi Pasteur.

Brent is also a board member of Dynavax, a Hepatitis B vaccine company.

Brent has a BA in Political Science/Economics from Carleton University, Ottawa Canada, MA in Political Economy from Reading University, UK and an MBA from Kellogg – Northwestern University, Evanston IL USA.

Anita James - Chief Financial Officer

Anita joined MDI in May 2022 as Chief Financial Officer, bringing extensive senior finance and commercial experience in ASX listed environments.

Prior to joining MDI Anita worked at Pact Group Holdings Ltd, as General Manager Finance and Investor Relations, and other ASX listed companies in the mining and resources sector, including 12 years with the multi-national mining services Company Orica Ltd.