Consensus community valuation

Having not been interested when this business came up many years ago, single product (nurse call) and a small player in big space seemed like a long shot. I am taking a second look at what is now a very different business and one I now have an interest in.

Company

Austco has an increasingly established global position in providing nurse call and clinical communication systems into hospitals and aged‑care built through a combination of product development and acquisitions. Its flagship platform is Tacera, an IP‑based nurse call, workflow and communication system with RTLS, mobile apps and integrations; Medicom is its lower‑cost, conventional nurse call line.

Thesis

A decade long management team with reasonable skin in the game (4.9%) have grown the business to this point, having managed that growth and challenges (incl Covid) well, indicating a long-term view to increase value. Share count has grown significantly but so to has EPS and the share price reflecting strong TSR justifying the dilution by adding shareholder value.

Their international footprint provides them a very large market opportunity, but a competitive one, so plenty of growth is available provided they maintain a strong competitive offering to customers, which they have to date. A strong cash position is available to add to their success in acquisitions and augment reasonable ~10% organic growth so there is capacity and capability for continued growth at or above 10%.

Value ($0.48 - $0.65)

Provided these conditions remain in place they warrant a PE of at least 15-20 and so the current PE of 10 on FY26 expected earnings is an opportunity (note valuation model below is bearish on FY26 PE at 13). Sales growth currently convers to NPAT at around 10% about double a few years ago and likely to reach closer to 15% with additional scale, showing further operating leverage on offer. Adding organic and acquired growth to a business that has a good cash position and strong positive operating cash is an attractive combination to the operating leverage with both earnings and multiple rerates on offer.

On what I see as reasonable sales and NPAT% targets for FY30 of $140.6m & 14.2% I get a current value (10% discount) of $0.48 (PE 15) to $0.65 (PE 20) on assumptions of just organic growth. Hence conservative assumptions and good value relative to the current $0.33 price, provided they continue to execute as they have done for the last couple of years.

Market Efficiency

Austco is in it’s third year of ~40% sales growth, profitable, positive cash and cashflow, so why is it on sale? I believe that current market conditions and uncertainty have their part, but also the growth is complex, a mix of acquire and organic but also when looked at by halves or by geographic regions it is very lumpy. FY25 organic growth was mid-single digit so the impressive 40% total sales growth was almost entirely acquired and a large portion of FY26 growth is going to be acquired also, but the company is indicating 10-14% organic growth which I think the market is waiting for proof of.

Margin direction is uncertain they have been flat or trending down slightly due to high margin software is becoming a lower portion of sale and the recent G&S Tech acquisition adds a lower margin business. The movement of NPAT due to tax expense between FY24 and FY25 distorts what is a clear PTB increase year over year, so profit growth doesn’t screen well.

There have also been few recent announcements of large contract wins (or any news out of the company for that matter) and their order back log was last presented at the half year results 3 months ago and was down to $47.2m from at high of $55.8m just after the G&S Tech acquisition. So, I suspect investors see no news as bad news given previous strong news flow on good news…

Conclusion

So maybe the market is right and things have turned/flattened, or it’s just a lumpy sub-scale sales business which will deliver over time but require investor patience at times (18-month sale cycle). I am betting that the market (most investors) doesn’t have patience and so the current price is an opportunity and as always, we will find out in the coming years.

Half weight position, keeping powder dry should current uncertainty and low multi-bag potential change, bought recently.

Disc: I own RL

Healthcare tech provider and Strawman Community favourite $AHC posted their 1H FY26 yesterday. I've been watching this one ever since it was put on my radarscreen by several of the most illustrious StrawPeople, and have in recent weeks opened an initial position following its fall below my "buy" price of $0.35. (RL 4%, although I'm yet to add on SM).

As this is my first coverage of $AHC, my reason for lurking for so long is that I wanted to get a better feeling for how it's M&A strategy is playing out, as I tend to be reluctant when firm's use M&A because i) it muddies the waters of the historical numbers, so I can't see the underlying "economic engine" and ii) well, because I don't like M&A unless I get confident that management know what they are doing. Other than that $AHC is in my sweetspot, combining healthcare and tech, and so I've taken an initial bite.

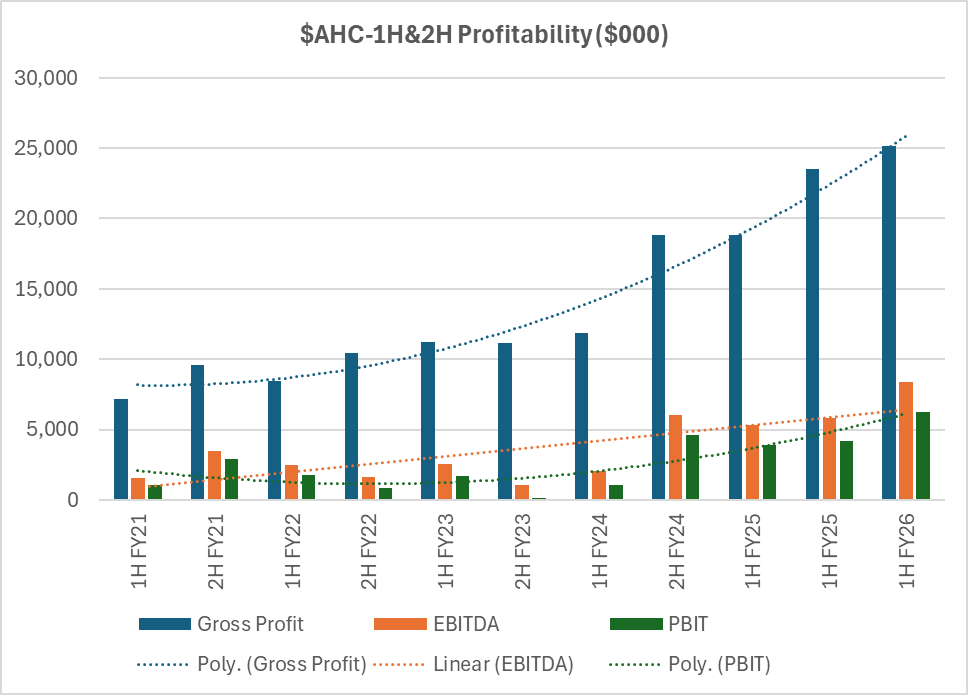

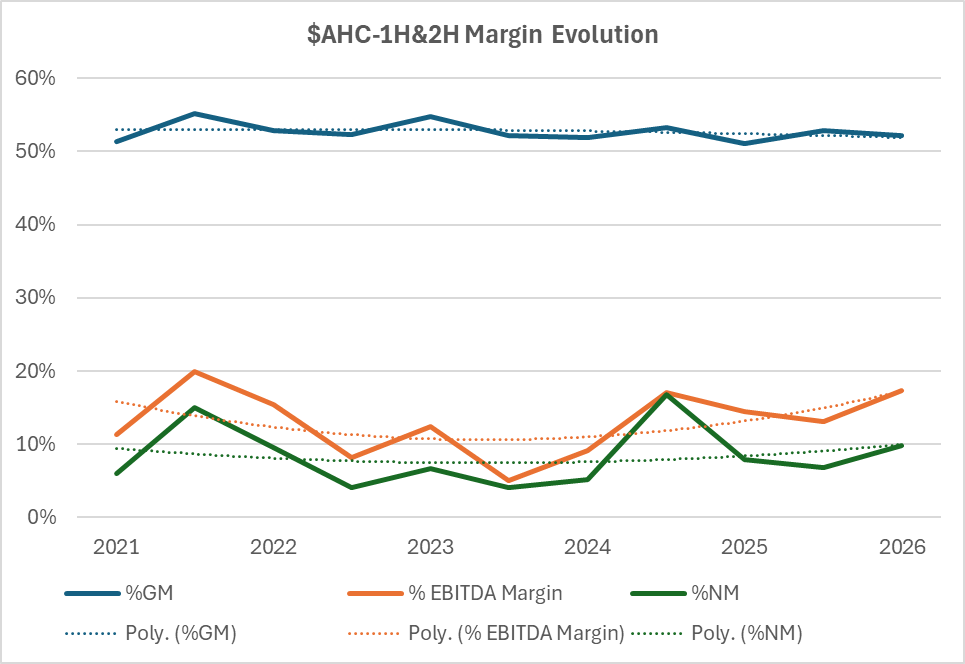

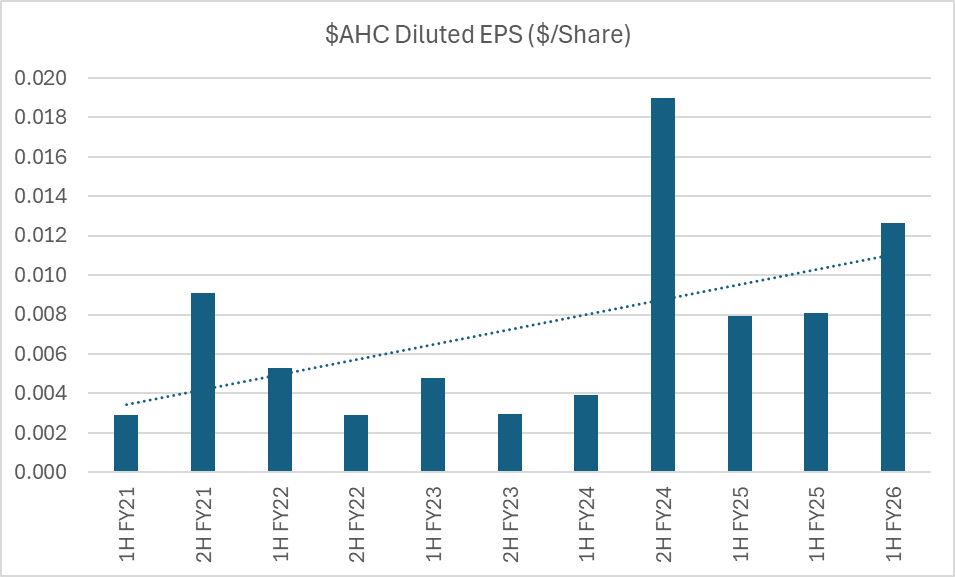

@MangroveJack has already given the headlines, however, because the impressive headline result includes organic and inorganic contributions, I've decided to have a go at pulling things apart in some future detail.

In a break from my usual structure, I drop 3 charts - to give a sense of half-on-half variations and overall trends. Then I'll record my analysis.

My valuation will follow in a few days, however, from my work so far, its looking broadly in line with @Hogajo ($0.45) and @Wini ($0.50) at my p50%, although my range is a bit wider.

As I said, while I have been following this one for a few years, this is my first write up, so I'm very keen for any feedback from those StrawPeople who have a better understanding of this microcap.

Summary

Austco Healthcare delivered a record performance in 1H FY26, combining acquisitions and organic growth to drive revenue up 30.7% to $48.2 million and net profit after tax up 61.7% to $4.7 million.

The company look like it might be demonstrating some operating leverage, expanding EBITDA margins to 17.1% while holding %GM within the range of the last few years.

The result gives an initial positive indication of its strategy to vertically integrate ANZ reseller businesses without diluting profitability.

With a debt-free balance sheet holding $15.2 million in cash and a substantial order backlog of $47.2 million, Austco has solidified its financial position while maintaining strong visibility on future earnings.

As fas as I can discern, acquisitions are currently the primary engine of this growth, and it will be important to see what the organic "engine" looks like from here over the coming periods.

Today's result seems to reduce my view of the risk that low-margin installation revenue would dilute Group quality; instead, Austco seems to be capture more of the value chain margin.

With the UCR flattening, future growth will likely require either new M&A targets in other regions (North America/Europe) or a re-acceleration of pure organic software sales to drive the next leg of expansion. Personally, I hope we get to see some of the latter first, although, the results are encouraging, indicating that management are adept at identifying the right acquisitions, keeping them appropriately sized and then executing well.

My Detailed Assessment

1. Revenue Growth: Inorganic Drivers dominate

Revenue rose 30.7% to $48.2 million.

This follows a 40% jump in FY25 full-year revenue. The growth trajectory remains steep, but the composition has shifted.

Organic vs. Inorganic: While the company cites "continued organic growth," particularly in North America, the primary driver appears to be the full-period contribution of recent acquisitions (Teknocorp, Amentco, and G&S Technologies).

- ANZ Revenue: Surged 57% to $26.9 million. This disproportionate growth in a mature market confirms the impact of rolling up resellers (G&S, Teknocorp).

- North America: Grew 38% to $15.4 million, which is likely the strongest source of pure organic growth, given fewer recent acquisitions in that specific region compared to ANZ. (I see this as a big positive)

- Asia: Revenue declined to $3.9 million, highlighting project lumpiness in organic markets without M&A support.

2. Margins and Operating Leverage: The Key Success Story

The most critical positive in this result is the expansion of margins despite the integration of typically lower-margin reseller businesses.

- Gross Margin: Improved to 52.2% (up from 51.1% in 1H25). This defies the historical expectation that acquiring hardware resellers (who earn lower margins than the OEM) would dilute Group margins. It suggests Austco is successfully capturing the full vertical margin (manufacturing + reseller markup) or realizing manufacturing efficiencies.

- EBITDA Margin: Expanded significantly to 17.1% (up 310bps from 14.0% in 1H25).

- Leverage: Overhead expenses grew 23.6%, lagging well behind the 30.7% revenue growth. This confirms that the fixed cost base (R&D, corporate) is being efficiently spread over a larger revenue base, a classic indicator of successful scaling.

3. Earnings Quality and Cash Flow

- NPAT: Up 61.7% to $4.7 million. The effective tax rate has normalized to ~24.5%, making this a "clean" profit number compared to FY24 which was boosted by one-off tax assets.

- Cash Flow: Operating cash flow of $9.2million was strong, effectively matching EBITDA ($8.3m). This indicates high earnings quality; profits are converting to cash rather than getting stuck in working capital (receivables/inventory).

- Capital Allocation: The company remains debt-free with $15.2 million in cash. However, organic investment is relatively modest (Capex $0.5m), with the bulk of free cashflow ($6.0m) directed toward acquisition payments (earn-outs).

4. Forward Visibility

Unfilled Contracted Revenue (UCR): Stood at $47.2million. While substantial, this has essentially plateaued since August 2024 ($50.3 million) and June 2025 ($53.8 million). A flat or slightly declining UCR in a high-growth environment suggests that while the company is executing delivery (converting order book to revenue) efficiently, the rate of new organic wins may be stabilizing rather than accelerating. The order book is being consumed as fast as it is being replenished. This is something that will be important to monitor over the next coupld of 6-month periods.

Overall, a nice result. And although the market agreed with the SP up 18+% today, this movement has to be considered in the context of the pullback over the last 3-4 months.

Disc: Held (RL 4%)

Austco released a trading update today to coincide with their AGM later this morning. Overall impression is it was what you would want to see, which is to say, solid. They didn't break down the organic/inorganic split, which would have been nice, but did reconfirm targeted 10-14% organic growth for FY26. Highlights included:

• Revenue of $23.2 million, up 51% on the pcp, which includes both organic and inorganic growth.

• EBITDA of $4.2 million, representing 18.1% EBITDA margin, up from 16.0% at FY25 year-end.

• Order book of $54.6 million at 23 October 2025.

Here's how the order book has tracked over the past six years:

Overall it continues to deliver at or above what I need it to in order to justify continuing to hold. I've been lightening some positions that have gotten a bit frothy in recent months but Austco is not one of them.

[Held]

Good to see some actual Performance Rights with Hurdles. Not common in the shares I hold down in this part of the market cap world.

Sure, it's a growth-by-acquisition story, but at least they are acquiring into an industry with structural growth tailwinds.

Net Profit After Tax lower: $5,933Mill (16.2%)

Net Debt/ Equity is ok so has liquidity here .. We looking for the these acquisitions to be integrated, sustainable.

https://hotcopper.com.au/threads/ann-appendix-4e-fy25-financial-statements.8731195/

Unfilled Contracted Revenue Recent large contract wins in North America and growth in most other regions across the group have contributed to the continued growth of Austco’s Unfilled Contracted Revenue (UCR). Our UCR book now stands at $53.8 million at 13 August 2025. This includes a net $6.3 million from the recently acquired G&S, being their UCR less orders they had open with Austco NZ.

Cash and Working Capital Position Cash on hand was $14.5m at 30 June 2025, up from $13.6 million at June 2024. Cash generated from operating activities of $13.48 million reflected underlying profitability and allowed for the investment into further businesses (G&S acquired in May 2025) without the need for debt or raising capital. Despite working capital increasing as a result of acquiring G&S, the Group is well placed to fund future contingent consideration obligations without the need for liquidity events, if it chooses to do so.

AHC closed lower while the XJO 8,395 -0.40% also lower

Return (inc div) 1yr: 71.43% 3yr: 50.53% pa 5yr: 38.36% pa

Updated calculation 12th Aug. 2025

My valuation Calculation from 3 weeks ago Just to clarify the projected Share Price $0.504 ( say an eps growth 12% pa)

The Intrinsic Value shown in your Google Sheet ($0.38) is the estimated true worth of AHC’s shares based on your forecasted financials and valuation assumptions.

https://hotcopper.com.au/threads/ann-austco-healthcare-trading-update-and-guidance-upgrade.8677109/

think, AHC should be able to scale up the model: support for over 5,000 healthcare facilities worldwide.

Unfilled Contracted Revenue Unfilled contracted revenue currently stands at $55.8 million, up from $50.2 million reported in February 2025. The increase reflects the addition of G&S Technologies to the Group since the last update, as well as continued strong operational performance, including a record revenue delivery of $13.2 million (unaudited) in June 2025. Amentco Earn-Out Adjustment The earn-out period for the acquisition of Amentco concluded on 30 June 2025.

Based on the strong performance of Amentco, Austco now expects a final earn-out payment of approximately $8.4 million, exceeding the previously accrued amount of $5.9 million. Under accounting standards, the incremental $2.5 million must be expensed through the income statement rather than adjusted through goodwill. While this will reduce statutory net profit as at 30 June 2025, it has no impact on EBITDA.

Austco retains the option to settle up to 50% of the $8.4 million earn-out in Austco shares, with the balance in cash. A decision on the option to settle is expected following on or around the release of the audited Full Year Results.

CEO Commentary Commenting on the performance, Clayton Astles, CEO of Austco, said: “FY25 was a transformative year for Austco. We delivered strong double-digit growth, successfully integrated acquisitions, and executed our strategy with discipline. Our ability to fund acquisitions through operating cashflow while maintaining a strong balance sheet reflects the resilience and scalability of our business model. With robust contracted revenue and momentum across key markets, we enter FY26 with confidence.”

The Company expects to release its audited Full Year Results and Appendix 4E on 26 August 2025. Authorised for release by the Board of Austco Healthcare Limited.

Austco Healthcare Limited (AHC) is an international provider of healthcare communication solutions, including nurse call systems, mobile communications, and clinical workflow management. Founded in Australia, the company has expanded its presence globally, with subsidiaries in six countries and support for over 5,000 healthcare facilities worldwide. Austco's competitive advantage lies in its advanced IP-based nurse call systems,

Chart shows a great trend here:

Return (inc div) 1yr: 81.40% 3yr: 54.60% pa 5yr: 40.97% pa

Can AHC announcements be found at https://hotcopper.com.au/asx/ahc/?keywords=AHC ? 1/ For example 14th May 2025 - Toronto Western Hostpital

Yes — HotCopper does list AHC’s ASX announcements, including the one from 14 May 2025 regarding the Toronto Western Hospital contract.

Example: AHC — Toronto Western Hospital (14 May 2025)

- On HotCopper, the thread titled “AHC Ann: Secures $2.1M contract at Toronto Western Hospital” reflects the official ASX announcement posted on that date HotCopper.

- In addition, the Announcements page under AHC on HotCopper compiles the company’s recent ASX disclosures, including that same contract announcement, along with many others like acquisitions, results, and trading updates HotCopper+1.

Summary

Yes, you can find AHC company announcements on the HotCopper site — including the 14 May 2025 announcement about the Toronto Western Hospital contract. It’s a convenient repository that mirrors, in near real-time, the ASX releases.

The CHAT GPT missed - the announcements so I conclude Chat GPT is has limited asx knowledge here:

at 23rd July 2025 good results.

todays Price Share Price $0.38 + 14.9%

Noted; Net Profit is double digits and growing positively.

*1 year Valuation Intrinsic $0.31 you pay w' average $0.37

Valuation before the 23rd July announcement:

Valuation after the 23rd July 2025 announcement:

If the EPS grows at 12%pa ( as per previous year)

Then 3 years: EPS growth 12%pa guess 2028 Intrinsic value ~ $0.38

The AHC share could be North of this at $0.48

Holder: RL

Austco today announcing the acquisition of NZ-based call system solutions provider and Austco reseller, G&S Technologies. I don't know about others but I find it very difficult to play armchair quarterback on acquisitions. There are just too many factors, like working capital pegs and balance sheet health, that are completely unknown unless you're in the tent. However, what we can say based on what's available to us:

- 3.5 times EBITDA - tick. It's in line with other acquisitions they've done, which have so far proven successful. They're maintaining price discipline.

- The EBITDA conversion % is roughly in line with the existing Austco business - tick. On that measure at least seems to be of reasonable quality.

- Strengthens direct sales capacity - tick. They've been doing this across multiple regions and it's been working so far.

- Up to 75% funded by scrip, at Austco's discretion - tick. Give them skin in the game and preserve cash. Yes, it's somewhat dilutive but there's always going to be a trade off.

- It's a meaningful addition - tick. It roughly represents half of Austco's business from 12 months ago. They've grown considerably since so probably represents about a quarter of FY25 business but still significant.

Only slight quibble is that they didn't take the opportunity to update on the order book but I'm nit picking.

[Held]

Austco puts out out their hand for a capital raise

Bell Potter are the underwriters.

Bell Potter also did the raise for Clarity Pharmaceuticals and only 33% took the offer.

I think this could head the same way. Extra 15m shares for retail OR Bell Potter has to buy up to 10m shares (going by the 33% using Clarity and an example) if retail do not take the offer.

I know comparing Clarity Pharmaceuticals and Austco is not an apples to apples comparison but I'm making the point that that retail right now doesn't have the stomach to tip money into the begging bowl unless there is very clear upside and synergies.

Sold on the pop on the morning

[not held].

@LifeCapital and @BendigoInvesto covered this, so I won't back over what they've written. Except to say that I was scratching my head at this result. The numbers just looked too good, and I couldn't get them anywhere near to adding up until I re-read almost to the bottom of their trading update:

Talk about burying the lead - a 5.6% increase in GM is huge! Much higher than anything they've done for at least 10 years. What is that? Is that Technocorp? I'd thought of Technocorp as strategically important, but of lower quality than the existing business. That isn't borne out by the numbers though:

So Teknocorp appears to be holding its own and then some. But the underlying business appears to have had a standout quarter as well. While I thought the 1H numbers were fair-to-good, I had expected a lot more given the growth in order book and commentary around impacts of COVID impacts easing. Q3 appears to have made up for that.

It's just as dangerous to extrapolate a good quarter as it is a bad one, but I'll do it anyway cause I'm a slow learner. Although they disclose NPAT, I'll focus on EBITDA because their tax is all over the shop. They are run-rating at almost $10 million EBITDA, which is an EV/EBITDA ratio under 6. Add a record order book and I'm a happy holder.

Nice, company continues to deliver.

Further acquistion should add to bottom line if costs can remain low.

What do they do?

Ausco develop software and hardware relating to healthcare communications systems, primarily nurse call and real time patient tracking systems, as well as re-sell and market complimentary systems.

They are also Systems integrators (nurse call and PTS installation contractors), through acquisitions, giving them sales channels into various geographic markets. It has achieved this primarily through acquisition, and is part of a strategy to enhance their direct sales channels in Australia, where systems integrators tend to have the customer relationships.

Financials

The business experienced significant disruption throughout FY 2021 due to COVID-19. Since then, revenue CAGR is 18%

Gross margins have remained relatively flat over the past 3 years at around 52%.

Profit margins have been in the range of 2-7%, noting the business has been profitable over the past 3 years.

Since H1 2022, software and software services revenue CAGR is 28% over the past 2 years, and is now 21% of total revenue. AHC has been developing its Nurse call and clinical comms platform Tacera,

Sales Pipeline: Sales pipeline has more than doubled to $44.4 million over the past 12 months, leading into H2. AHC revenue streams are seasonal, with H2 traditionally being the stronger half. The sales pipeline has benefited from the following recent acquisitions:

- Acquired Amentco (Integrator) for $10.6M (3.5 x 2023 EBITDA) - Feb. 2024

- Acquired Tecknocorp acquisition for $2.6M plus earnout (3.5 x EBITDA) - Sep. 2023.

- Present revenue value is annualising H1 revenue.

Share Price Performance

Share price has been in an upward trend since early 2019.

Valuation

Austco Healthcare Ltd is trading on a trailing PER of 24.5. However, given the strong pipeline into a seasonally stronger H2, I would estimate the forward PER is around 20, which appears to be reasonable value, assuming it can continue to grow at around 10-15% pa.

Ownership

The largest owners are:

- Former CEO / Founder: Robert Grey (19.2%)

- Aust. Ethical Investments (17.8%)

- Asia Pacific Holdings (18.1%)

The board is a lean one, with just 4 members

MD, Clayton Astles owns 1.1% of the company, and Brendan Maher (CFO) 0.85% . Other directors holdings of around $100-200k each.

AHC has some solid institutional investors, with reasonable inside ownership

Management Incentives

Short term incentives are based on pre-defined profitability, gross margins, and revenue financial targets. Non-financial are product development, process improvements, and Leadership and team contribution.

Summary

AHC strategy of rolling up integrators and re-sellers in Australia at about 3.5x EBITDA will juice revenue and hopefully profits over the next few years. The call option is it the re-sellers / integrators enable AHC to get their sticky Tacera platform on sites around the country. Once these systems are in, they are difficult to replace.

Presently, sales orders are exceeding the H1 2024 revenue run rate, indicating a strong H2 is ahead of us.

DISC - HELD

Austco has announced a $3.8 million contract win across two hospitals in Singapore.

They have also announced this has taken their order book to $40.7 million, up from the $38.7 million announced at the AGM last month. They've been on a bit of tear this year having more than doubled the order book since February this year.

Zooming out a bit the order book has been steadily rising since late 2019, apart from some COVID and supply chain impacts through 2022 and early 2023.

Nice to see at least one of my holdings kicking ass and taking names. I still think it flies under the radar a bit considering its history of profitable, non-dilutive growth. @Strawman have we spoken with Clayton?

Austco has come out with a roadshow presentation today, with lots of funky graphs and "buy me" arguments. Not a lot new, although they did disclose sales orders were up again from last month's record high to $37.2m - so they're filling the funnel faster than they can drain it. (Ignore the 'Revenue from customers' tag - revenue it ain't).

Austco is one of my more comfortable holdings. They disclose often enough to make you feel wanted, without getting all over-promotional. When they make investments in product or people they set realistic expectations about how long it will take to get a payback from the investment. They certainly appear to be in that zone of getting a return of previous investment right now though.

If I were being hyper-critical I'd say the CEO is very well compensated for a company of this size. However, Clayton appears to be getting the job done so I'll not quibble while that remains the case. It's arguably not a screaming bargain but if they keep growing at the rate they are it will look cheap soon enough. Happy to hold.

Pop in share price after AGM update

Would have been good if they had a slide that tracks their progress against competitors. Otherwise lots of content to take away and digest.

Still have watch position

[held]

Austco snuck in a price sensitive investor presentation this morning, which was an interesting decision given they released results less than two weeks ago (sans presentation). It came two days after a competitor, Hills Limited (HIL.ASX) announced they had been successful in bidding for the New Footscray Hospital tender in Melbourne. I'm not saying it was because of that. I'll leave that to others.

Largely it replicated what they they had already released with some swanky graphics added. It did give a little more detail about the growth investment being made in each region. One nice little new tidbit it shared was an increase in the order book to a record $24.7m. That's $2m higher than they had disclosed at the end of August and is probably what justified it being price sensitive.

[Held]

Essentially what you have here is a profitable, dividend-paying, growing, tech company in the Healthcare sector - they just need lithium and they've won Buzzword Bingo. All of that comes for bargain basement price of just $33m market cap.

Revenues are growing in the mid-teens but their margins have been under pressure - like every one else - from higher product costs and supply availability issues. However, they have largely offset the impact with more software revenue (higher margin) and sale of higher margin products.

It will be interesting what FY23 will bring with several offsetting impacts to weigh up. The company has flagged an investment in sales in FY22, but call out long sales cycles means the benefit of this won't be realized until FY24 onwards. Additionally we'll need to back out COVID assistance grants over the past two years.

Offsetting this is a strong order book and improved hospital access post normalization of COVID (get well soon Chagsy), which is being reflected in growing revenues. Normally we'd like to see order books growing over time but I think at this stage of COVID recovery it's a bullish signal that the order book appears to have peaked as it suggests normalization of access is real. This, plus the fact their revenue is growing much faster than the run off of the book, means it doesn't unduly concern me the order book may now be reverting to a more normal setting before it starts to grow again (it has grown to $22.7m since year end).

One thing I like about this company is they seem pretty straight forward and conservative. They call out issues they're seeing even if they may not be apparent from the numbers as there are offsetting 'good guys' or are yet to be reflected in the financials. They keep adjustments to a minimum and where they do use them it's to back out the impact of one-off grants and gains, rather than back out costs.

They raised capital in 2019 to invest in sales capacity and growth. What was pleasing is when COVID hit they didn't deploy it for this use or any other. They just sat on it. Now they're coming out the other side they can invest for growth at a time when a lot of other companies are bunkering down and trying to strip costs out.

Their future opportunity is to move into patient monitoring, including post-discharge, and patient engagement, including entertainment and food. This may require acquisitions with competition already heavily invested in this tech.

The declaration of a dividend is a moderately bullish signal for me. I'm not sure the last time they paid one but I don't think they have for at least 6-7 years.

Overall, I expect them to continue to steadily grow the top line with this accelerating in FY24 and beyond as growth initiatives being spent today bear fruit. It may be difficult to grow the bottom line at the same rate in the short term with ongoing margin pressures and investment in sales capacity. However, that operating leverage will come in time.

Based off a fairly conservative DCF.

[Held here and IRL - both underwater, which puts them in plenty of good company]

The latest investor preso (see here) warns shareholders of supply chain issues -- increased raw materials and transport costs, semiconductor shortages -- and says that management expect these pressure to last for the remainder of FY22, and possibly beyond.

This will impact margins, and has prompted the company to build up inventory. The business will also be investing in added sales resources. With $7m in cash, they are also on the lookout for acquisitions, particularly in Europe and the US.

Will be interesting to see how sustained these supply chain issues are, and whether there is much capacity to increases prices (i suspect not)

I think there's good scope for sales growth as they prosecute their record order book, but with ongoing investment and added costs it'll make profit growth more difficult.