Potential Competitor?

An ad for this product randomly appeared in my google feed (let's not get into why google thought I might be interested in buying fiber optic sensing equipment)

https://www.hawkfiber.com/

This is the main companies website https://www.hawkmeasurement.com/products/fiber-optic-sensing/ - looks like it is a new direction this company is foraying into.

Not sure if anyone else has looked into on this company or its product in comparison to Aura Ai. It is a private company unfortunately...

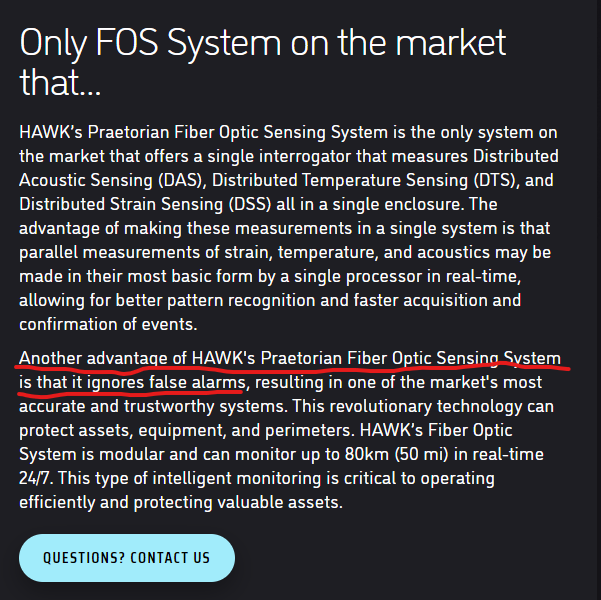

Curiously, they state the following:

I think the underlined has just been poorly worded - all systems will ignore false alarms PROVIDED they know they are false.

Anyway, I think would be good to get Mal's view on this company, and their claims next time we meet him.

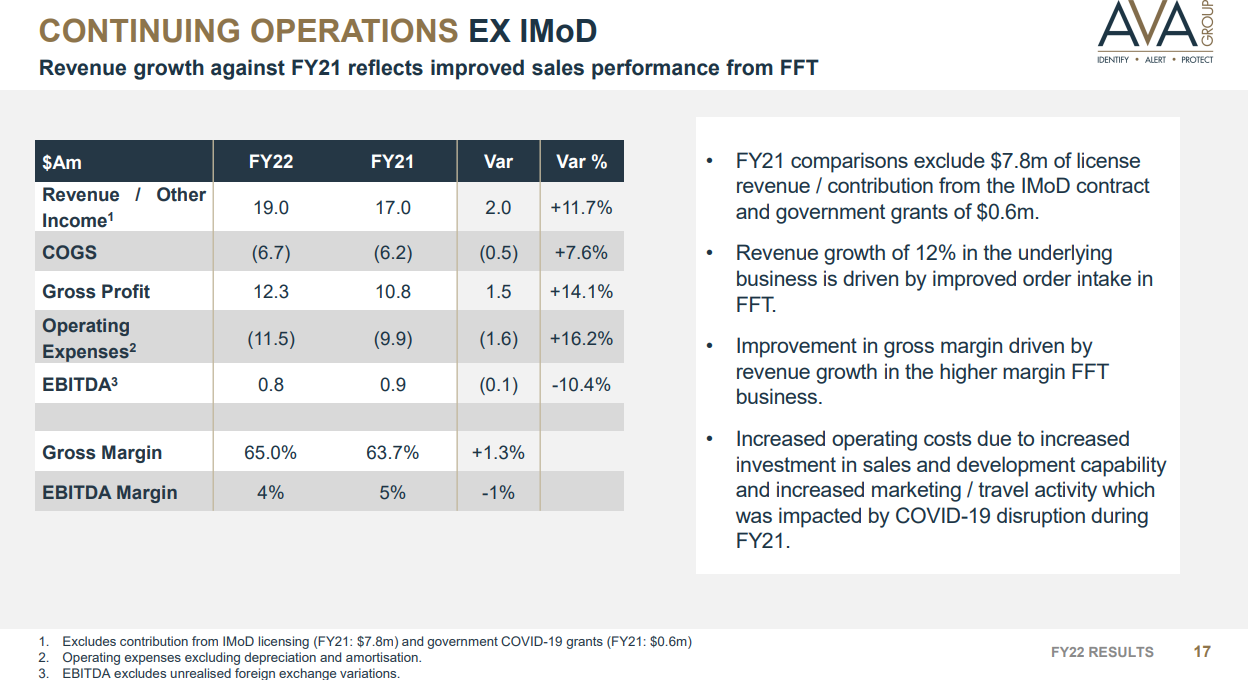

Doing my due diligence on AVA Risk and feel the need to illustrate this from their last investor presentation. Yep, it is old news from the end of August, but as it had not been explicitly mentioned I thought I should add it in.

They are only barely profitable when you factor out the IMoD contract - which makes any valuation based on their current P/E questionable.

Saying that I still chose to add them to my RL portfolio, but I will be keeping an eye on their profitability (with large contracts like IMoD factored out) going forward.

Disc: Held