tl;dr -- the first half will deliver essentially flat revenue growth.

Glad i'm out

Ava Risk Group is in the business of protecting critical infrastructure and high-value sites from physical threats. It does this through smart fibre optic sensors, high-security access systems, and intelligent perimeter lighting and detection technologies. Its customers are governments, utilities, and large organisations that need to secure important assets.

The business has evolved a lot in recent years. It divested its logistics-focused services division (at a pretty incredible ROI, although the profits were essentially all paid out to investors rather than retained) and shifted focus to its in-house developed fibre-optic sensing tech.

This technology turns fibre optic cables into smart sensors that detect movement, digging, or climbing along a perimeter. It sends light through the cable and analyses microscopic changes in the reflected signal to classify activity in real time. (For the physics nerds: it uses Rayleigh backscatter and interferometry, with machine learning layered on top to turn raw signal data into actionable insights.)

The result is low power, high durability, and the ability to monitor long distances from a single system. Better yet, it can often be deployed over existing fibre infrastructure, avoiding the cost and disruption of new trenching.

That’s a big advantage over traditional perimeter security methods like fence-mounted vibration sensors, buried coaxial cables, or cameras, which usually require power at the sensing edge, have limited range, and are more prone to false alarms from weather or wildlife.

Alongside its core sensing business (Detect), Ava operates two other divisions: Access and Illuminate.

Access is all about high-security access control. Think biometric readers, encrypted smart locks, and secure systems for things like government buildings and prisons. Ava picked up this capability in 2014 through the acquisition of BQT Solutions. While Detect covers the perimeter, Access handles the internal entry points (doors, gates, restricted areas).

Then in 2022, Ava bought GJD Manufacturing, a UK-based business with expertise in perimeter lighting and detection. GJD makes things like motion sensors, ANPR cameras (for reading number plates), and IR and white-light illuminators -- hardware often used with CCTV to boost visibility and deterrence. Crucially, GJD tech allows you to trigger lighting or alarms in real time based on detection events, which ties in perfectly with Ava’s sensing capability. More recently, GJD released a LoRa-based wireless platform that can connect up to 500 devices without running cables, which is a big plus for complex sites.

Together, Detect, Access, and Illuminate make Ava a multi-layered security solutions provider. Think integrated systems that can detect, verify, and control access across some of the world’s highest-risk environments.

All of this sounds pretty compelling, but for a while Ava was really just a collection of standalone technologies. After the services divestment, it had some great IP but lacked cohesion. The segments operated more like parallel businesses. There wasn’t a unified go-to-market strategy. Internal systems and processes were a mess.

Then came Mal Maginnis. He joined as CEO in January 2023 and brought decades of defence and security experience. His job: get the machine working. That meant aligning products with customer use cases, building the sales and delivery backbone, and putting in place the systems needed to scale. Since then, Ava has become a much more focused business with a clearer strategy.

These changes take time. But it seems to be working. Revenue has grown steadily, hitting $30.2 million in FY24 (up from $28.6m in FY23) with FY25 forecast between $37 and $41 million.

More importantly, the quality of revenue is improving. Annual Recurring Revenue (ARR) hit $2.4 million in H1 FY25, up 20% year-on-year. The company returned to positive EBITDA in the latest half, with a $1.7 million profit (a $2.6 million turnaround). Cash flow has stabilised, and a $4.3 million equity raise has help strengthen up the balance sheet.

A key thing to note is that the internal systems have now been overhauled, commercial reporting sharpened, and the go-to-market model rebuilt. The sales team, especially in North America and EMEA, has been beefed up. The business is now focused on high-value verticals like border security, transportation, telecommunications, and energy infrastructure.

Cross-selling and bundling are now at the core of the strategy. The aim is to combine sensing, locking, and lighting into end-to-end solutions. That makes deployment easier and the value proposition stronger. Existing customers and distribution channels are being used to expand into Europe, North America, and the Middle East. The product set has been mapped to real use cases (eg borders, transport, utilities) allowing Ava to pitch for larger, more complex jobs.

In short, Ava’s shifted from clever tech to real-world commercially viable solutions. The product suite is far more integrated, and we’re beginning to see early signs of faster top line growth and expanding operating margins.

And that's the key part of the thesis -- after two years of investing in internal systems, commercial teams, and product dev (which did weigh on margins), Ava now has the foundations for scale. Management believes the current cost base can support much higher revenue and we’re seeing early signs of operating leverage. H1 FY25 revenue was up 20% year-on-year, margins improved, and the business returned to EBITDA positive. It's a start, but we need to see this continue.

The hope is that earnings growth begins to outpace revenue growth, especially as recurring revenue lifts and more big contracts land. That growth is underpinned by a stronger product offering, growing list of reference sites, and deeper enterprise and government relationships. Larger customers bring longer sales cycles, but once Ava gets in, the revenue is stickier and more repeatable.

Meanwhile, recurring revenue is building. Multi-year support, monitoring, and upgrade contracts are adding predictability and smoothing cash flow.

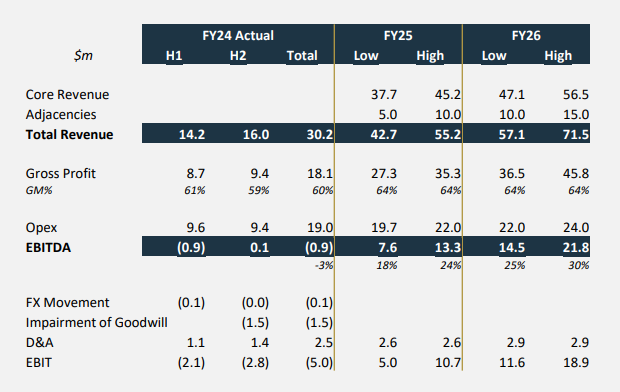

This is the latest management guesstimate from February 2025:

This shows the business moving from modest top-line growth in FY24 toward a more profitable, scalable model over the next 12–24 months.

At 10.5 cents per share, Ava has a diluted market cap of about $30.5 million and an enterprise value of ~$27.9 million. That puts it at around 7× forward EBITDA on the low end of FY25 guidance. But that’s a little misleading because the business is subscale and right on the edge of breakeven. The cost base has been engineered to handle a lot more revenue. If that growth materialises, operating margins should expand meaningfully. If not, well, the economics would remain pretty average..

At scale, this should be a business delivering 10–15% net margins (at least). And that’s the bet: that Ava can grow into its cost base and scale profitably. If that happens, the upside is big in percentage terms. Even more so from a stock price perspective if success brings multiple expansion.

In that case, the stock is ridiculously cheap.

Of course, the risks are real. If growth stalls or costs creep back in, shares will likely languish under 10cps. But there does seem to be real asymmetry here -- more upside than downside.

The market clearly isn’t pricing in much success. Which, i suppose, is the opportunity.

So why the ‘meh’ valuation by Mr Market? Part of it is liquidity. Ava trades under $100k a day, which limits institutional participation and depresses multiples. But also, there’s a fair bit of market fatigue. Ava’s been talking up its potential for a while, and while revenue has grown, earnings haven’t really followed through..yet. The unexpected capital raise in FY24 probably dented confidence in the company’s ability to fund itself.

That’s why the next 6 to 12 months matter. The hard stuff has largely been done; internal systems, sales capability, product integration. Now Ava needs to execute. That means growing revenue and lifting margins in a visible, sustained way.

If Ava even gets close to its FY26 targets, a 25 cent share price looks entirely reasonable. Maybe more, if there’s real revenue momentum. If it doesn’t deliver, the stock likely goes nowhere.

So why to a lean towards an optimistic stance? Because business transformation takes time, usually longer than markets are willing to wait. Ava’s spent the last two years doing the boring but important work. That phase looks done. Now we’re seeing early signs of execution: revenue is rising, margins are improving, and EBITDA is in the black.

I’m also patient (stubborn? naive?) But what I see is forward momentum. Contracts with Telstra and UGL aren’t speculative pilots, they’re commercial validation. Moreover, the order book is growing and ARR is rising. They seem to reliably convert the sales backlog into cash flows.

I think there’s also a tailwind here. Whether it’s border control, energy infrastructure, or general geopolitical instability, the need for scalable, intelligent perimeter protection is only going up. Ava’s well-positioned to benefit.

So yes, it’s a bit of a turnaround story. And one I was admittedly too early with. But it’s a turnaround that’s showing signs of working.

Strong IP. Streamlined and rebuilt operations. Improving fundamentals. Potential for meaningful operating leverage. And a valuation that barely reflects any of it.

That’s the setup.

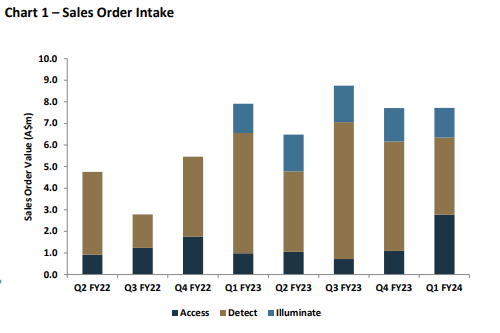

Some strong numbers from AVA, some of which were already revealed in the January trading update.

Still, 20% revenue growth to $17m at an EBITDA margin of 10% ($1.7m compared to a $0.9m loss in the previous first half) was nice to see. Gross margins improved 3% to 64% thanks to a favourable segment mix (Detect has the best margins by far). Contracted annual recurring revenue was up 20%, and represents around a third of all sales orders for the half.

AVA saw a sales intake (signed but not yet delivered) of $16.3m, which is below the $19.7m pace received in H1 FY24 (but part of that was a big order from the Access segment as distributors built inventory). The sales backlog more than doubled to $7.6m and they reckon there is a $100m sales opportunity with close dates in this calendar year. $8.5m of this is seen as high probability and there is $26.6m of sales opportunities in progress.

A big part of the thesis has always been the ability for the business to realise some good operating leverage, and after a lot of restructure after Mal arrived, it was good to see operating expenses dip $0.3m and still see strong revenue growth.

Detect was the star of the show -- and this has always been the most interesting segment -- where revenue rose by 57%, and represented 71% of all first half revenue.

Access segment actually saw a dip, but the comparable period including initial stocking by resellers. So that's not too concerning. Still, will need to see some growth from here. Illuminate was also slightly down, but good to see that there is increasing cross-sell/bundling with Detect sales.

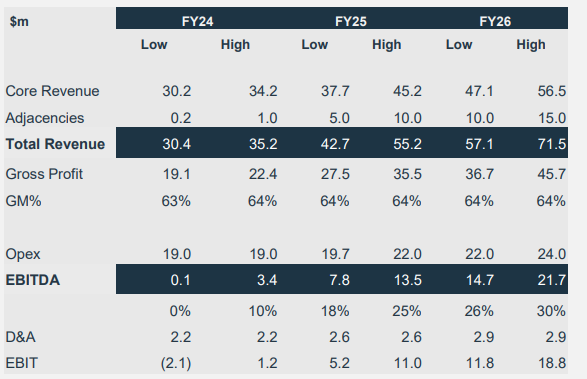

FY guidance is for revenue between $37-41.7m -- which would be ~30% up on last year at the midpoint, and suggests H2 revenue growth of almost 40%. According to their outlook, they expect an 11-15% EBITDA margin on this revenue, which is expected to further improve in FY26

All in all, great to see good sales momentum and expectations for further growth, with a stable cost base and rising gross margins, not to mention being EBITDA positive with $4.7m in cash in the bank. They also broke even on a statutory basis, so hopefully they really are at an inflection point.

The market just cant get excited about AVA, but another half or two of continued progress like this and it will be very hard to ignore, and I suspect a decent re-rate would be likely. I mean, they are on an EV/EBITDA ratio of 5.3x, which strikes me as dirt cheap for a business that is growing the top line at 20-30%, and is breakeven with rapidly expanding operating margins.

Of course, we need a strong second half for this to be true, and maybe that falls short. But if not, you'd have to think AVA could command a share price somewhere in the 20-30c range.

It's certainly been one to test the patience, but I think Mal has done well to reposition the business and it remains somewhat of an asymmetric bet -- much more upside than downside.

[Held]

a

a

I just got off the AVA call.

Key takeaways:

Mal emphasized that FY24 was a transitional year, completing restructuring, launching new tech/products, and setting a firm foundation for FY25. It was a tale of two halves, with things accelerating in the final quarters.

Margin drop was due to a shift in segment mix -- Detect has the best margins, but strong growth in Access was why group margin eased back. Should normalise going forward.

Detect is really the core business, and Mal described this as a program or project based business, one that can have long lead times (3-12 months)

A $100 million pipeline, particularly strong in the Detect segment, is noteworthy. Mal repeatedly emphasised these leading indicators and you can see from the latest outlook table that they continue to expect high revenue growth against a relatively fixed costs base

At the mid point, you have ~62% revenue growth expected in FY25 and an EBITDA of ~$20m -- a 42% operating margin.

(interesting to hear Mal say "I know you've heard this before")

Aura AI-X has been transformational since its launch, contributing to improved detection and lower false alarms. The strong sales of over 100 units and Cobalt 2’s 48% growth in Access orders demonstrate successful product adoption and integration across segments

There was discussion about H1 traditionally being weaker than H2, with specific references to Q1 (northern summer) and Q3 (holiday season) slowdowns, aligns with their operational cycles.

Illuminate’s expected move to break-even or profitability in FY24

There was a noticeable shift toward emphasizing predictability in revenue, seen in their focus on bookings, pipeline, and backlog as core metrics.

Its a fractured and competitive market, and AVVA is trying to distinguish itself by focusing on the tech and aligning with bigger customers.

Company well funded, no expectations to raise capital. Board happy to commit to paying 30% of EBITDA as a dividend, which they think leaves ample room for growth investment.

Could FY25 finally be the year where things take off? Cost base and operating segments now set, good momentum in orders and sales.. Maybe. If they get anywhere near guidance you'd have to assume something of a rerate.

A do or die year for me.

tl;dr -- It was a good final quarter, but H2 revenue was at the very bottom of guidance issued in April and FY revenue was up only 5.6% for the full year. EBITDA was positive (but unquantified) in H2, compared with -$900k in H1. Positioned well for accelerating growth -- according to the company -- but no guidance given at this stage.

Here's the key figures:

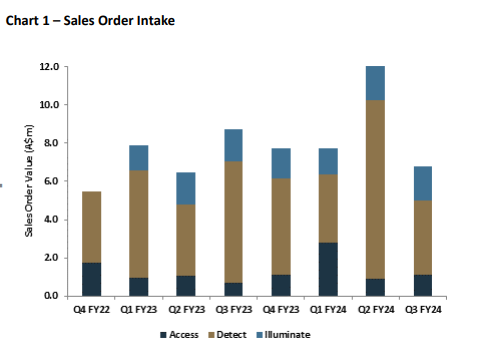

- Q4 sales order intake of $9m, second highest on record (pro forma), 50% above preceding quarter and 17% above previous 4th quarter

- The company brought in $35.3m in sales across the full year -- 14% up on last year

- The sales order backlog of $8.5m compares with $3.5m a year ago.

- FY24 revenue of $30.2m compared to $28.6m in FY23, representing growth of 5.6%

- At the end of Q3 in April, they said they were expecting $16-20m in revenue for the second half. Given they did $14.2m in H1 revenue, the result was at the very bottom of the range

- Telstra supply agreement disrupted a bit by restructuring within Telstra

My view: good to see a decent lift in sales orders and the partnerships with some big clients seem to be progressing well. Nice to see some cross-sell wins, and extensions to previous contracts. But material growth remains elusive.. Still, at 1x revenue (pre market open) it's not exactly priced for much growth. With the *potential* for good operating leverage, and some major trials in the pipeline, FY25 could be the year we finally see some good earnings growth.

If not, I'll concede defeat and move on.

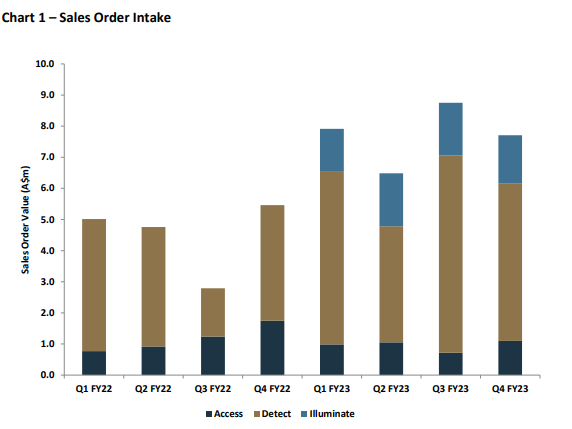

Not a terrible Q3 update from AVA, but not great either.

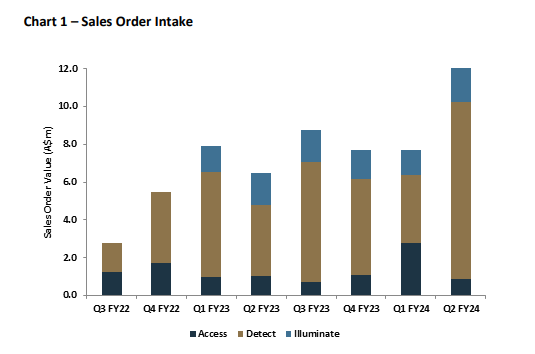

Sales orders are up 15% comparted to the same time a year ago, and they have $8.6m in order backlogs (2/3rds will be converted to revenue this financial year).

The company still reckons it will do $16-20m in H2 revenue (the wide range due to the timing of project delivery). They did $14.2m in the first half of FY24, which means the full year figure will be between $30.2m-$34.2m. That's exactly what their 3 year outlook calls for, and the outlook is unchanged from what they said in March.

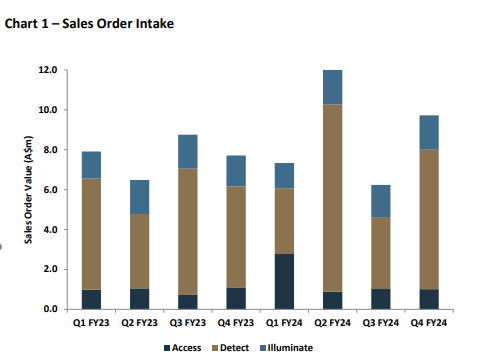

Still, this picture is worth a thousand words:

Growth may be 15% for the FY-to-date in sales orders, but it was Q2 that did all the heavy lifting, and the most recent quarter is down on what they did in the previous corresponding period. Detect was underwhelming due to project timing, and Mal said he expects to finalise various opportunities in the last quarter.

So, it's great to see they are on track to hit their guidance, but what we really need here is an acceleration in sales. You have to give some slack for the variability of revenues, but the market probably wont move much until there is some very clear evidence of growing traction.

[HELD]

Cap raise inbound!

Let's wait until we see the details, but i suspect the cost of capital could be up there. And if it's just for 'working capital purposes it's more difficult to swallow. Perhaps another situation where a line of credit would be more appropriate? Anyway, getting ahead of myself.

We will see.

A good part of today's results were known, following the company's Q2 update less than a month ago.

The best parts being strong sales order growth of $12m in Q2. (And I guess the company reckons this is a pace they can maintain given they thought to annualise this in today's preso..) This has been underpinned by some large value contract wins, and there's a healthy sales back log to give some confidence in a decent second half.

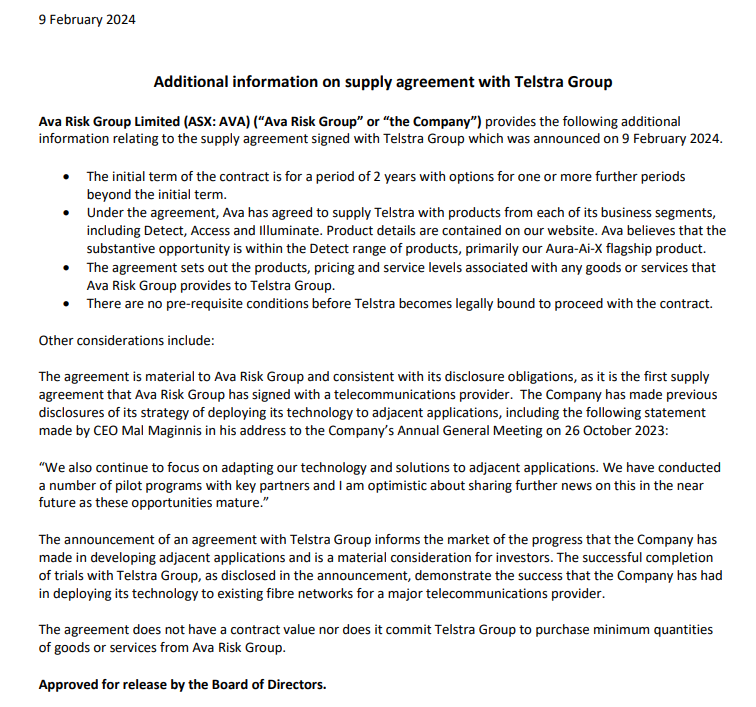

The recent Telstra deal was highlighted, and although it was a botched announcement, it's clearly a deal with some interesting potential (albeit one that the company isn't able to quantify).

Still, the detect segment saw a decline in revenue of 8%, following a weak first quarter. As AVA said at the time, that was mainly due to some timing issues with bigger contracts in Q1, and we did see a very strong Q2 in this segment, but overall it was a weaker half compared to the pcp. AVA reiterated it expects a strong second half here. I hope so.

Part of the issue with AVA in recent periods is that one segment seems to always zig when another zags. And it was the Access segment that did all the heavy lifting this half, and that was largely an stocking event associated with the distribution deal with dormakaba.

But Detect is the biggest segment and that meant total EBITDA dipped back below neutral and continued R&D and inventory expansion saw a $1.8m drop in cash -- there's now only $1.8m in cash left. They said the cost base will stabilise at the current level, but the risks of a capital raise are perhaps higher than I first expected.

The biggest new news for me was a revised 'outlook' scenario, which they have now aligned with financial years.

Before it was this:

Now it is this:

So essentially the same, but clearly the real expansion in operating margins is not expected to start showing up until FY25.

Using the mid-points above, you get only a 5% EBITDA margin for FY24, and basically nothing at the lower end. Yes, things start to look very good after that, but they're basically saying to not expect much this FY. Beyond that, you just need faith these targets are somewhat reasonable.

Maybe they are, and I'm sure they're put forward in good faith, but until we see good evidence in the financials there's a good amount of faith that is required.

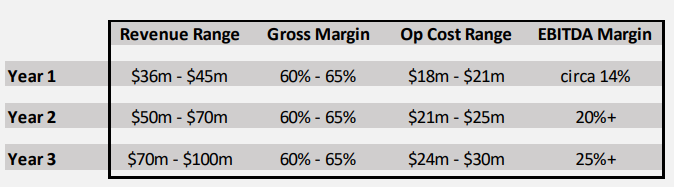

Later in the deck they again reiterate the target for $70-100m in revenue over the next 3 calendar years, with minimal cost increases. And given what they have above for FY26 ($57 -- 71m), and with a good chunk labelled as 'adjacencies' (ie. currently untapped applications of their products), I'm a bit nervous there's a fair amount of "hopium" in managements outlook.

Maybe they're right to be optimistic, and there really is good growth in sales orders, but we're yet to see this translate into anything exciting in the statutory numbers.

There is potential for some acquisitions to help the company reach it's goals, and that can be good cover for a capital raise, but this type of growth isn't always accretive to shareholders and has all kinds of risks. I don't think their GJD purchase is doing much for them yet.

There's clearly some big potential for AVA, and I know that building the foundations for growth always take longer than you think to build, and for that to deliver accelerating sales traction, but this one really is testing my patience. Especially with some recent communication blunders.

Hopefully we can get a better picture of things when we speak with the CEO next month.

Not a lot of extra info here:

All we can surmise is that the contract is "significant". But it seems there is no minimum spend, and AVA are at pains to avoid mentioning any specific financials.

Maybe there are some commercially sensitive aspects to the deal, but this is frustratingly vague...

You beat me to it @Bear77 -- agree the update is generally positive, and while we need a solid second half for the company to land in its targeted revenue range ($36-45m), they seem to be suggesting that is very much in play with a "substantively stronger" second half. In Mal's words:

They'll need second half revenue of $22m to hit the lower end of their target range.

In the first half they have secured just shy of $20m in new sales orders (37% growth), with the second quarter representing 61% of the first half total and representing yoy growth of 39%. There's $8.9m in backlog to be fulfilled this calendar year, most of which is project delivery work -- this compares to a $5.2m backlog at the end of FY23.

This suggests (i think) that most of the sales order intake is converted to revenue relatively quickly (ie they added $19.7m in new sales orders in the 6 months to Dec 31, but the order backlog only increased by $3.7m. (someone please sanity check this assertion!).

Still, the reality is that H1 revenue is only 10% higher than H1 FY23, and is at the very bottom of the guidance they issued in October ($14.2-15.2m). The access segment had a great half but this was helped by stocking orders from their channel partners -- we'll need to see some good end-customer sales before we really know how their new Cobalt locks are being received by the market. And Illuminate was flat, albeit with a good improvement between the first and second quarters.

For me, the main game is with Access and Aura Ai-X, which has accounted for roughly 2/3rds of new sales orders. And they really do seem to be seeing some good sales traction there. Group targets aside, even if they 'only' get $18m in H2 revenue, that'll still be annual growth of 15% at the top line. (the previous second half did $15m in revenue, so I dont think that's too much of a stretch target)

Holding gross margins and fixed costs steady -- which is what management have essentially said to expect -- under that scenario you should still get an EBITDA figure that is more than double what we saw in FY23 (from cont. operations) and an operating margin expansion from 7% to ~12%.

The market obviously remains somewhat sceptical (if it wasn't the share price should be easily above 20c imo). But for me I consider the thesis still on track and shares good value. The next 6 months will be telling.

Have been away from me desk all morning, but I got an alert while I was on the go that Ava's first quarter update was out. A quick check of the price (as you do) and saw it was about 5% higher -- "must be good news", I thought!

Anyway, just got back in the saddle to have a look at the update and noticed the price is now down 7%.

Not sure how many times I need to be reminded how irrelevant the market price signal can be for small, illiquid stocks. In this instance (at the time of writing) we're talking about a price move that has been affected by less than $50k worth of trades, and where the high and low of the day ranges from 19c to 21.5c

Anyway, having now read the actual update, and thought for myself (as opposed to letting the market tell me what to think), I think the news is respectable.

I'll let you read the finer details yourself, but the big picture takeaway for me is that although sales order intake was basically flat ($7.7m vs $7.8m in the pcp, and $7.7m in Q4 FY2023), the Access segment (locks) finally saw a good bump as product certification was received for their Cobalt Lock range and Ava's partner Dormakaba stocked up, and the contraction in the Detect segment (fibre optic perimeter detection) was seemingly a timing issue with new orders expected to close in the current quarter.

(The illuminate segment was again disappointing with AVA again citing difficult economic conditions in the UK. The expectation is for FTY growth here -- we'll see i guess)

So adding that all together, the revenue outlook for the first half is for $14.2-$15.2m, an 8% lift on H1FY23 at the midpoint.

What we really need here is for all the segments to fire at the same time -- But it seems one always seems to zig when the others zag. As Mal told us earlier this year, this is a lumpy business.

Nevertheless, Ava seems to be winning new customers in the detect segment, they now have new products and distribution in America and Europe and, for what it's worth, management remain very optimistic for the full year:

"..management expects that second half revenue will substantively exceed the first half."

Take from that what you will, but given the margin assumptions AVA have previously released, it looks very likely that they will at least double FY23's EBITDA. Frankly, with FY revenue of $35m and a 14% operating margin, EBITDA could grow by 150% or so.

Anyway, thesis seems to still be on track.

HELD.

Another contract announcement for Aura Ai-X

Relatively small (A$1m), like the one announced recently, but great to see some traction for the product since its launch 6 months ago.

Held.

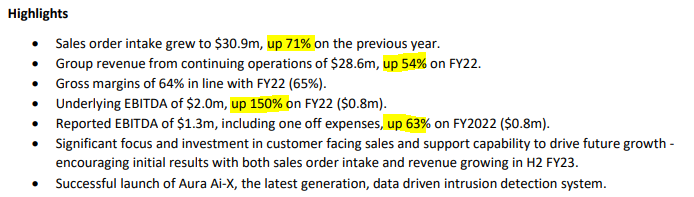

Ava's FY23 results seem good to me. The market disagrees :)

The highlights from their results update:

If you look only at new revenue from the detect segment (an additional $3.8m in revenue), and ignore Illuminate which added $6.8m in revenue following the acquisition of GJD which was acquired in August last year, you still have a 20% lift in revenue. Indeed, around a third of orders for Detect came from North America, which saw a 20% lift in orders received over the year.

In fact, sales orders were up 36% if you ignore the GJD acquisition (up 71% in total). This is a great leading indicator for revenue growth.

Access was disappointing as the company awaits key product certification for the Cobalt 2 locks. Once received, the company expects that to open high quality distribution channels. We'll see.

Gross margins were essentially flat, which ain't bad given the shift in product mix (Illuminate products are lower margin), but the operating margin (ex restructure costs) was up 3% to 7%. A good demonstration of the operating leverage potential. They maintained their slide that highlights ambitions to growth the EBITDA margin to 14% next year, and up to 25% within 3 years. Also had the $100m sales target, which Mal talked about when we chatted with him recently. Very bold aspirations, but not unreasonable in my view.

At the bottom line there was a $1.1m net loss for the year due to higher depreciation and interest charges associated with GJD purchase. (compared to $0.7m in the prior year, ex discontinued operations).

Cash flow was negative for the full year as the business bulked up its inventory in response to supply chain issues. But op Cash flow was positive in the second half of the year. The company has $3m in net cash, but given receivables from recent orders, non-cash depreciation charges and working capital movements, I don't see a big risk of a capital raise.

At a current enterprise value of $46.8m, the EV/EBITDA ratio is 23.4x. That does not strike me as high given the pace of growth in revenue, sales order intake and the demonstrated scalability of the business.

I missed the briefing this morning, but will try and track down a recording and post here.

Full ASX presentation is here.

[HELD]

Some notes from the 4th quarter update today

Looks like AVA will deliver revenue bang in the middle of guidance, somewhere between $28.4 and $28.7m (guidance in April was for $27.6m - $29.6m.)

That means the second half has delivered about $15m in revenue -- 10% up on the first half of FY23 and up 50% on FY22 H2 result.

Sales orders also growing OK -- excluding the GJD which was acquired last August, sales orders increased 13% for the last quarter and were 36% higher over the full year. (up 71% if you include GJD)

Breaking things down across the various segments:

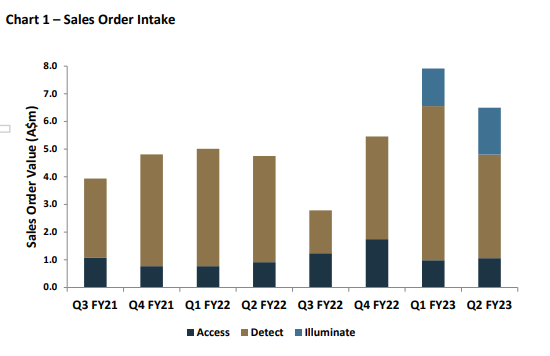

The Detect segment (this is the area that does the fibre optic sensing tech) saw $5.1m in new order intake. For the year, the order intake was $20.7m (an increase of 55%) which was in part driven by the new Aura-AiX product. Still, order intake was $6.4m in Q3, so that's a drop quarter on quarter.

The Access Segment saw a 50% lift in new orders from Q3 to $1.1m, but was down 17% for the full year. Not great, but apparently things have been held up by attaining product certifications in various channels.

The Illuminate segment was very "meh", generating just $1.5m in new sales orders in the last quarter and $6.3m for the full year. The company blamed challenging conditions in the UK.

Sales orders tend to be pretty lumpy, as can be seen above, but I am encouraged to see the Detect segment -- by far the largest -- making some progress. There's been a real dearth of announcements, so it seems this is a story of a lot of small wins, rather than any single large contracts.

If AVA are to hit the lower end of their 3 year aspirational target ($70-100m), they'll need to do at least 35%pa top line growth from here. We need to see increased momentum on an organic basis if they have any hope of doing this. We're speaking with the new CEO tomorrow, so it'll be good to get some more detail. And the full year results will be out in another month, and I'm pretty keen to get a sense of what margins look like.

Disc: held.

Pleased with the latest from AVA.

The number of new sales orders was 47% higher, thanks in large part to the acquisition of GJD. However removing this still shows a 15% jump in the sales intake for continuing operations.

Statutory revenue was up 50% to $13.6m (looks like about 16% higher without GJD). And EBITDA margins rose to 9% to $1.2m (the pcp was messy due to divestment of Services division and IMoD contract, but excluding these the EBITDA margin was 2.5% for continuing operations last year).

All segments delivered growth. And the business seems to be scaling well.

Operating cash flow was -$2.2m due mainly to changes in working capital (increased receivables and inventory due to increased orders and recently completed projects), and also added R&D. There's still a bit of padding on the balance sheet with net cash balance of $4.4m, after subtracting $2.7m in borrowings.

AVA reiterated that over the next 3 years they expect $70-100m in revenue at 25% EBITDA margins. Even at the lower end of that range, and assuming 20% EBITDA margins, that's $14m in EBITDA, or 6x higher than the current annualised level.

If they do that, you'd get a 10% average annual capital gain so long as AVA trades at a EBITDA multiple of 6x or above at that point. At the upper end of guidance, EBITDA comes in at $25m.

Anyway, aspirations are one thing, delivery is another. As of this point, shares are trading at roughly 26x annualised EBITDA.

But i see a business that is growing well, with improving operating margins (and stable gross margins), industry tailwinds, and that is likely to be self-funded (in the absence of an acquisition).

Held.

Decent result from AVA it seems.

Revenue from continuing operations expected to be up 50% to $13.6m (guidance was for $13-15m)

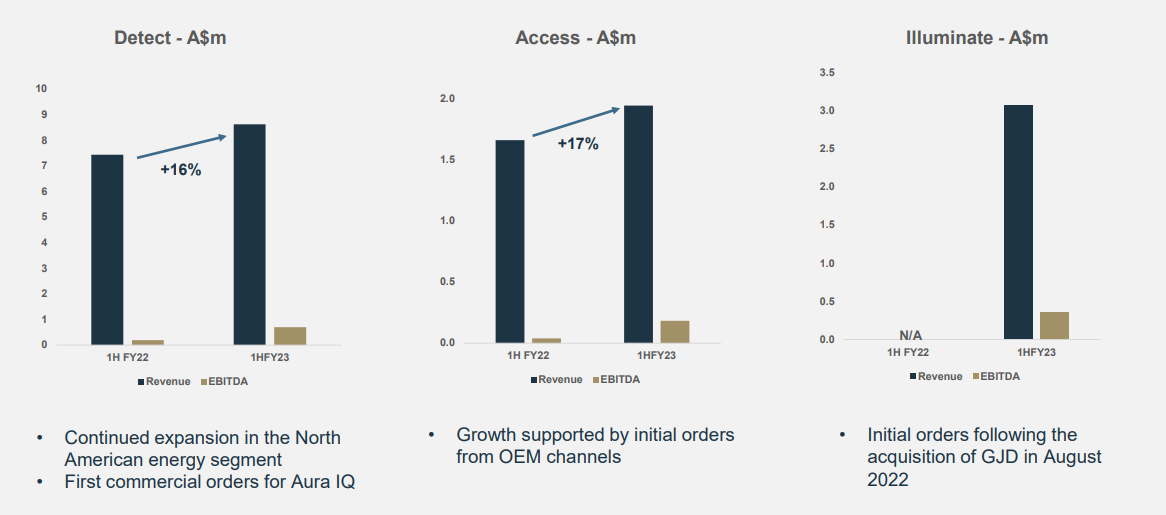

Sales order intake up 16% if you exclude orders from GJD acquired in August 22, but 47% if you include. Existing FibreOptic and access control businesses saw sales grow 15% and 21%, respectively. Good momentum into north American energy sector with more sales expected. New CEO says they expect continued growth and operating leverage in second half. Received "strategically" important orders for AuraIQ.

Next half we'll get a full 6 month contribution from GJD, but on a pro-rata basis AVA is on 2x sales.

Growth continuing, strong balance sheet, CF positive, undemanding valuation and doesn't seem to be facing any real headwinds. Valuation, undemanding.

Held.

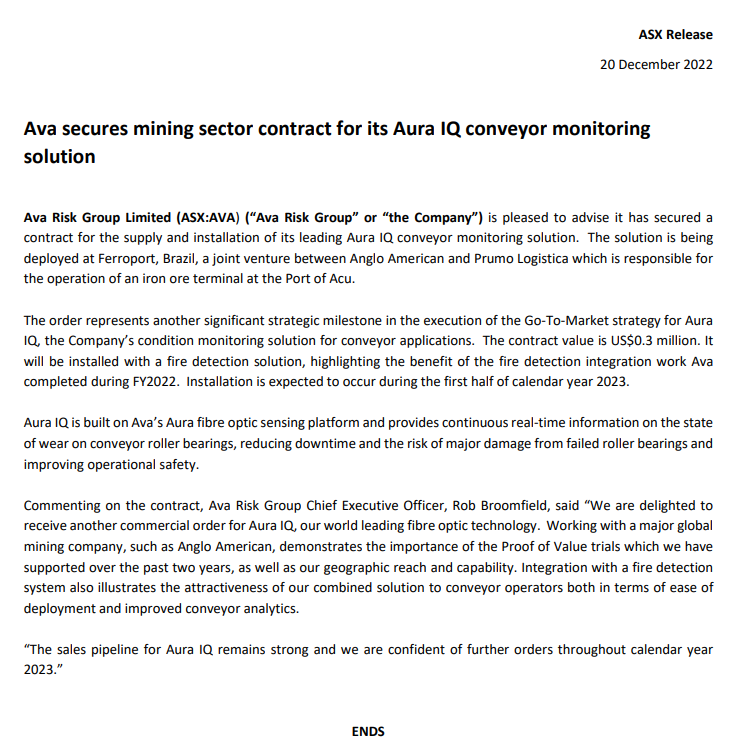

$300k to install Aura IQ in combination with a fire detection system at a iron ore terminal in Brazil. Due to occur first half of calendar 2023.

Client is a joint venture between Anglo American and Prumo Logistica.

Again, not overly material, but good to see some orders coming through and that the sales pipeline remains strong.

This isn't overly material in it's own right (in dollar terms), although new deals are always welcome.

Where it's noteworthy is that this is the third implementation for this facility, and is replacing another system. That is, the customer gave it a go, found it superior and is extending its use -- all after only a few months since the first system was installed.

And, as the statement says, more sales are expected down the track.

We know from speaking with Ian Olson from Pointerra that the energy sector is very cooperative in the US (they don't directly compete and there is a large sharing of ideas and solutions). I can imagine this will become an important reference site for AVA in the US utility sector.

Disc. Held.

Looks like Rob Broomfield is retiring.

I'm not sure of his exact age, but he started his degree in 1978 so i'm guessing he'd be around 65. He's staying on for a further 3 months, will be doing consulting for a further 12m and the Chairman had a lot of nice things to say about Rob in the announcement -- so it all seems very amicable. He also said he remains a "committed shareholder"

Given they already had a replacement lined up, I'm assuming the board knew this was coming.

Rob will be replaced by Mal Maginnis, formerly the president of Rapiscan Systems, an airport security firm which did close to A$1b in revenues in FY22. Mal has 35 years experience in the security sector.

It seems the team at AVA have some history with Mal, having known him for some time. I've also heard from a broker that Mal was the person who recommended the recently appointed global head of sales Jim Viscardi -- whom he worked with at Rapiscan. So the chemistry between sales and Chief Executive is well established

The remuneration package seem appropriate for the role and size of the company. $330k pa fixed (Singapore dollars, which is about $360k AUD). Plus he gets 1,000,000 shares vesting annually in 3 tranches over 3 years -- about $185k at today's share price.

He'll get another 500,000 shares per year for 3 years, if the share price is 20%, 40%, and 60% higher from his start date.

ASX announcement here

Let's see if he can kick some goals.

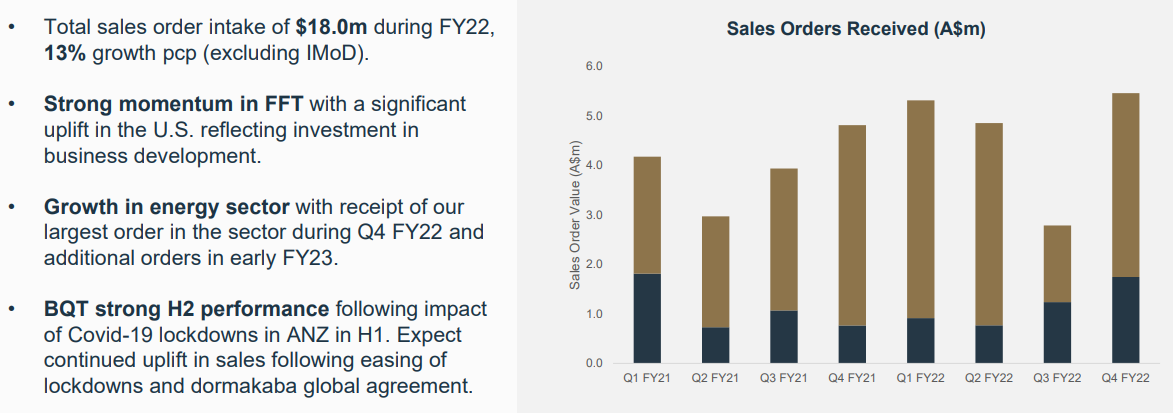

AVA reported revenue of $19m, in line with what they suggested at the last quarterly update. That's a 25% drop from last year, even when you exclude the now sold services division, but it's a 12% improvement when you take out the license fee revenue for the Indian Ministry of Defence (IMoD) and covid grants.

nb: We shouldn't easily dismiss the IMoD revenue from previous years, but this type of (extremely high margin) license revenue is always going to be lumpy. So stripping them off does offer some insight into 'core' operations, which pretty much seem to be chugging ahead nicely. Hopefully we see a few more significant license fee deals -- and in fact there's one due to start in Latin America this year -- but we shouldn't extrapolate too much from them.

It was also good to see the gross margin lift to 65%, especially in light of the current macro backdrop. This was a feature of more sales from the higher margin FFT segment. So overall, again focusing on core, continuing operations, gross profit was 14.1% higher.

Moving further down the income statement, added expenses saw EBITDA drop 10.4%, with the operating margin moving from 5% to 4%.

This was because R&D, sales and marketing, office and travel costs were all higher -- about 63% higher to almost $3m for the full year. That feels like a lot, but all told it's an extra $1.2m and this expense is to help penetrate into new markets and underpin future growth.

Indeed, revenue for North America, which is the stated priority region, saw revenue double for the year.

Operationally, the business is investing further in machine learning processes to help improve the efficacy of detection systems, and increase the attractiveness of long-term support contracts. Indeed, AVA has 52 support contracts signed -- up from just 4 last year. This will hopefully become a good source of recurring revenue and improve client retention by ensuring they are getting the most out of installed systems. In fact, they have 2,500 customers in their existing install base, so there should be a good deal of low hanging fruit here.

There wasn't much on the new Dormakaba agreement, other than there was "significant momentum" in performance as of the end of FY22.

Management did warn that although they had navigated global supply chain issues successfully, they expected the situation to remain challenging in FY23.

Although the company distributed $38.8m back to shareholders during the year (due to the sale of the services division), the balance sheet remains in excellent shape with $15.2m in cash and no debt.

All told, we have a business that looks to be at a decent inflection point. With the company now firmly in the commercialisation phase, and with some encouraging momentum, there's good potential to scale from here -- something that should multiply any top line growth. And, importantly, this is cash flow positive, with a strong balance sheet.

$66m market value (at time of writing) gives a 3.5x sales multiple, or EV/EBITDA of 64.

I'll dial into the results call and update on any insights.

disc: held here and in real life

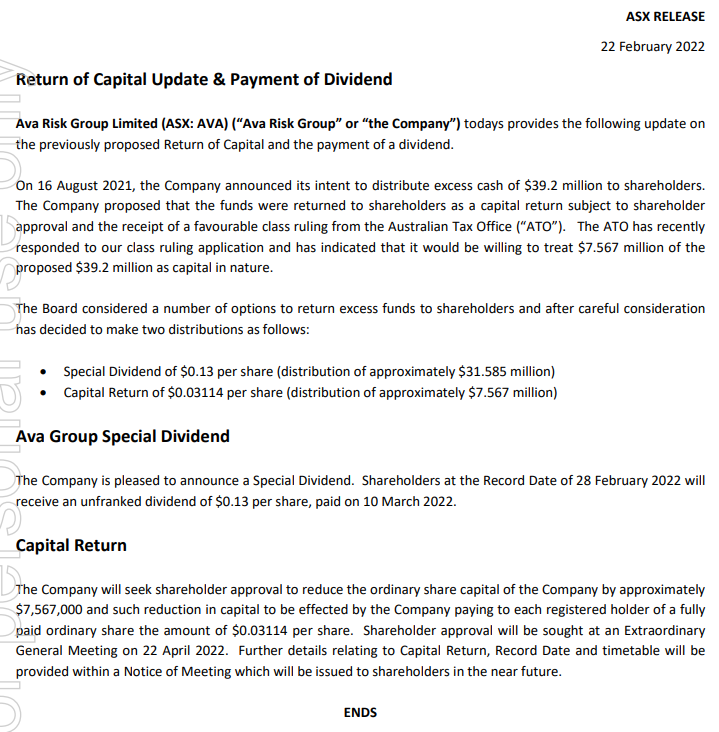

Finally an update from the ATO on AVA's proposal to return $39.2m back to shareholders.

Unfortunately, the ATO was only prepared to treat $7.567m of this as a capital return (a mechanism that would allow shareholders to defer any tax). That's equivalent to $0.03114 per share. They will seek shareholder approval for this at a special meeting on the 22nd April.

As such, AVA will distribute the rest of the money as a special dividend of 13c per share. Sadly, this will be unfranked (they simply don't have any franking credits to distribute given they have barely had to pay any tax due to the use of carried forward losses).

The record date for the dividend payment is 28th of February, which means anyone on the share register at that stage is eligible. Given the settlement period, that means you need to buy shares no later than the 26th to be eligible.

Obviously, a full capital return would have been the most tax effective method of returning excess money given AVA's situation, but there's little they can do if the ATO isn't going to play ball. Still, the fact they are returning this capital, and are not tempted to invest it on an acquisition or new capex shows a good bit of discipline to my mind.

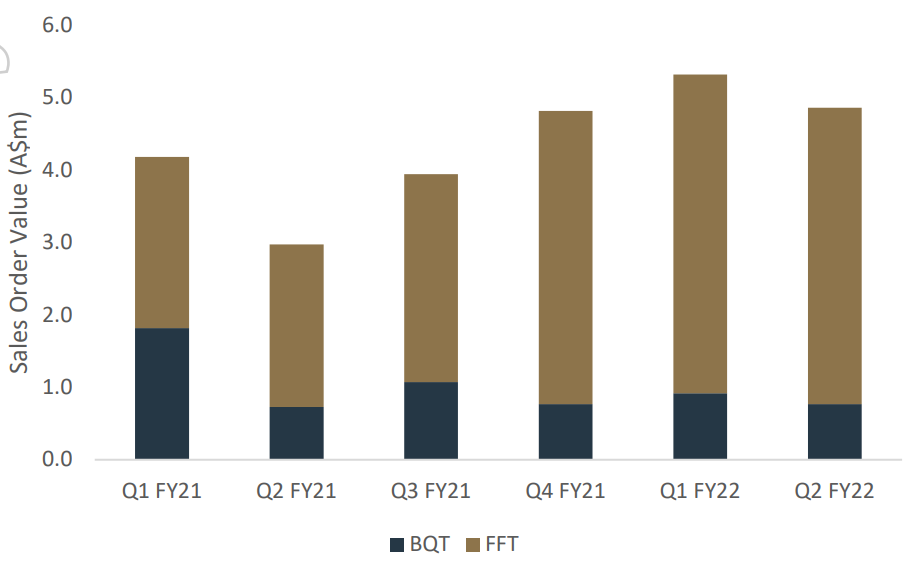

This was a solid result from Ava (see here)

The group's technology division -- now the core focus after the divestment of the Services business -- received confirmed sales orders of $4.9m, a 63% improvement on the previous second quarter despite some covid related impacts. Year to date, Ava's tech division has generated $10.2m in the first 6 months of the year, a 42% improvement.

The FFT segment was the key driver of the improved result, with significant growth in the US market, up 150% year to date. Military installations and solar farms were called out as especially strong.

The company also has a confirmed order backlog (awaiting fulfilment) of $4.2m -- the majority of which is expected to be realised in FY22. Note that this excludes the Indian Ministry of Defence (IMOD) contract, which the company doesn't expect any material contribution from for the remainder of the year.

The new Dormakaba agreement came into effect at the start of 2022, and an initial order is expected before the end of January. I expect the blue part of the chart above to become more meaningful as this starts to ramp up.

The balance sheet remains insanely strong with $55m in cash and no debt, although $39.2m of this will be returned to shareholders (about 16c per share) as soon as they (hopefully) get a favourable ruling from the ATO. As a business delivering free cash flow, even after the return of capital, the balance sheet will be in very good shape.

The company also reaffirmed guidance of $20.2-21.2m in H1 revenue and EBITDA of $2.2-2.5m. This will include 3.5 months contribution from the divested Services segment. Still, removing this and accounting for the 16c cash return, you have a high margin, fast growing, profitable, well funded technology business, with an attractive market opportunity, that's probably on a Price to Sales of roughly 3x.

Will be good to get a "clean" set of results, but the business just seems good value to me.