Top member reports

Straws

Sort by:

Recent

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

#Quarterly Review

stale

Q2FY25 Update

The Good

- Reiterated H1 revenue guidance of $17m which is right in the middle of the range previously provided along with being EBITDA positive.

The Not So Good

- No update on Telstra deals or products. Previously indicated trials to conclude and others to start within Q2. If the $5 to $10m of adjacencies revenue is to come through, then we will likely need to see some orders coming through in Q3.

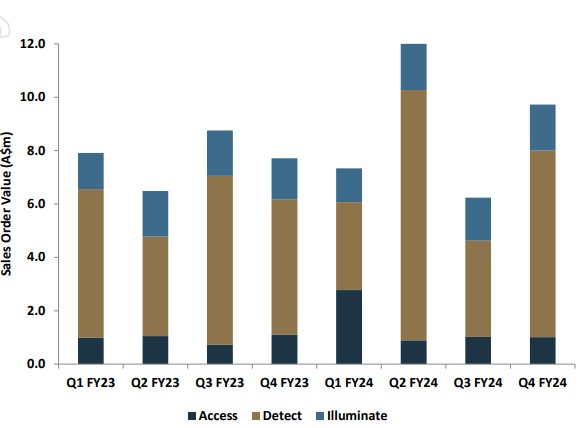

- Although AVA is forecasting an uptick in revenue for H2, sales orders were down to $7.4m in Q2 which is concerning for the work in hand yet to be recognized as revenue which sits at $7.6m. As this is expected to be delivered in H2, a further $12m needs to be won and delivered within the next 6 months to hit the bottom end of the full year guidance range.

Watch Status

- Hold

Valuation Status

- Review at H1FY25

What To Watch

- Progress toward full year guidance

- Telstra Updates

- Detect subsea trial to start in Q2

- Illuminate pit trial to conclude in Q2

- Mobile Tower security

#Quarterly Review

stale

Are there green shoots of growth?

Q1 Update and Presentations

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02874837-3A654561

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02875345-3A654645

The Good

- The business is really building itself around the Aura Ai-X technology with a decent pipeline of potential detect contracts for FY25. (Everyone loves a good pipeline graphic, just ask DRO). What is promising is the range of sectors that the sales are coming from.

- FY25 Guidance of $42.7m to $55.2m provided which is a solid jump on the $30.2m for FY24. What is a bit deceiving is breaking this into core revenue and adjacencies. (Telstra?) Given Telstra is likely a slow moving beast, guidance should be the core revenue range of $37.7m to $45.2m which is still an improvement of 25 to 50%

The Not So Good

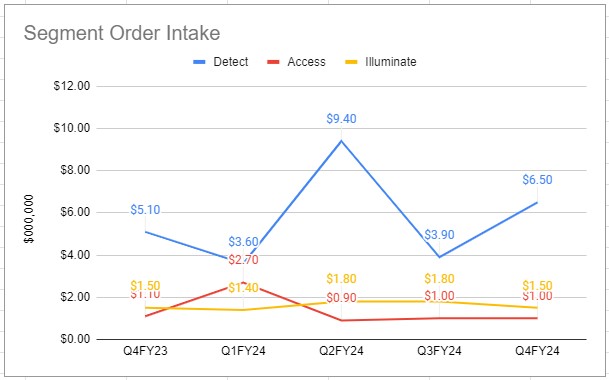

- Ok sales order intake for Q1, with detect doing most of the heavy lifting again. Slight improvement in access with its best quarter since Q1FY24. However sales orders will need to increase to meet the revenue guidance. In previous years sales order intake has been lumpy.

Watch Status

- Slight improvement in sentiment due to guidance range and growth in the detect market.

Valuation Status

- Review at H1FY25

What To Watch

- H1 Revenue Guidance of $16.5m to $17.5m

- Telstra Update

- Detect subsea trial to start in Q2. Events like the recent damage to subsea cables in the Baltic are likely to provide tailwinds in this area.

- Illuminate pit trial to conclude in Q2.

- Mobile Tower security - TBC

- LoRA product line in illuminate launched in the quarter. Expected to contribute to improvement in sales orders for Illuminate.

- Would expect a high likelihood of winning the remaining Sydney Metro contracts given AVA were awarded the first one, unless they have had substantial issues during the commissioning, for this type of project, it is unlikely to have multiple technology providers installed across the same type of scope. SRL is also being delivered by the same groups of contractors.

#Quarterly Review

stale

Q4 Update

The Good

- Order backlog of $8.5m sets up a good position going into FY25 and an order intake of $9m annualises out to $36m which still sits inline with the bottom end of the FY25 guidance so Ava is roughly tracking in the right direction. Most of this is propped up by the detect business.

The Not So Good

- Ava just scraped into its guidance range with a full year revenue of $30.2m. This means that there is extra work that needs to be done over the next two years to meet previous sales targets.

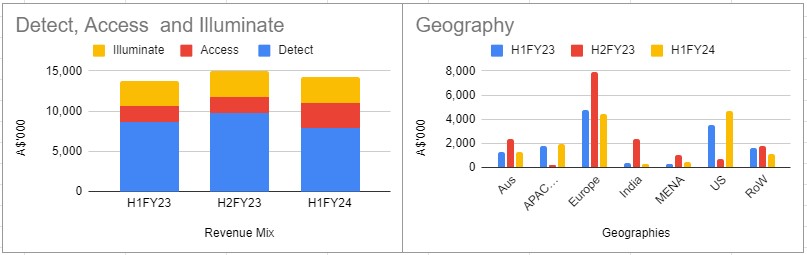

- There were previous indications that the illuminate business unit would start to show signs of growth in H2FY24. So far both the illuminate and access business’s have been fairly stagnant. Changing the sales orders from the stacked column graph highlights this.

Watch Status

- No Change

Valuation Status

- Review at full year results. Current growth rate is below previous forecasts.

What To Watch

- Telstra trials of illuminate and detect products to be completed in H1FY25. Mal hinted in the Strawman meeting in April that the first sales from this agreement will be a surprise, so likely from one of these two business units.

- Impact of US sales on illuminate orders.

#Half Review

stale

The Good

- Sales orders up substantially on prior quarters to $12m. This annualises out to $48m which indicates that if sales can be maintained then revenue forecasts for FY25 are achievable.

- Wide range of projects signed over the quarter which is a positive for the technology base, in particular, Aura Ai-X.

The Not So Good

- Illuminate unit still struggling to show growth, Q2 slightly up which is potentially showing signs of turning.

- H1 revenue of $14.2m is flat over the last several periods, however, it was within the guidance range provided.

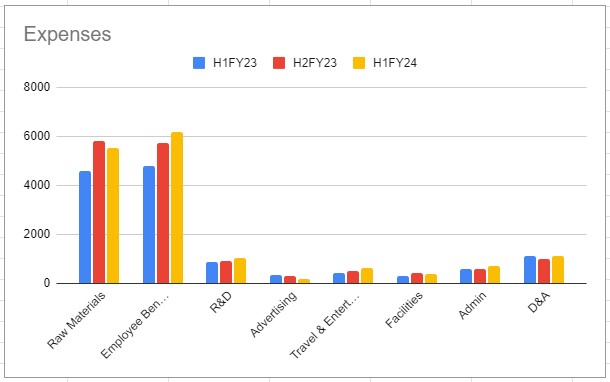

- Costs increased against this, which has resulted in a $2.3m loss for the half.

- The cash position at the end of December was precarious with only $1.78m and a negative free cash flow of $3.5m for the half. Unless there are some payments coming in, money will be running out very quickly.

Watch Status

- Neutral - Negative financial offset by slight improved outlook

Valuation Status

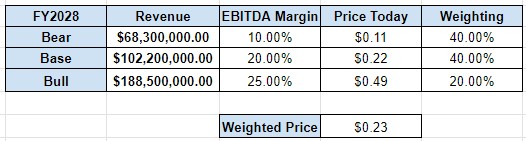

- Increased chance of Bear Case. Need to review forward revenue projections to better align with management forecasts

What To Watch

- Further details on sales commitments from the Telstra Agreement. Telstra has a large network of assets that could be protected by AVA products and this is AVA’s first with a telecommunications provider.

- New LoRa product to be launched in H2FY4 which may provide a boost to sales orders.

- H2 revenue guidance of $16m to $20m. Order backlog of $8.9m with $6.8m set to be delivered over CY24.

- Management is confident of improvement in the Illuminate division in H2FY24. (This has been reported previously)

#Quarterly Review

stale

The Good

- Significant improvement in sales from the access division, which was previously indicated by management on the back of the certification of the cobalt series of locks. These are stocking orders under the framework agreement, so whether or not the level of sales can be maintained is yet to be seen.

The Not So Good

- Revenue guidance for H1FY24 of $14.2m to $15.2m which is in line with $15m from H2FY23. This also means that the revenue in H2 needs to be at least $22m to meet management’s previous 3 year targets from the September investor presentation.

- Illuminate division still struggling to show signs of growth. This was put down to macro factors. Management once again reiterated confidence in seeing growth in FY24.

Watch Status:

What To Watch

- Slower sales in detect was put down to sales cycles and likely to see an uptick in Q2.

- Q2 sales orders will need to be significantly higher for revenues to enable time for revenue to land in FY24.

- Potential sales growth in illuminate from growing global footprint.

#Quarterly Update

stale

Ava’s update has been covered by the community so these are just some notes for myself

The Good

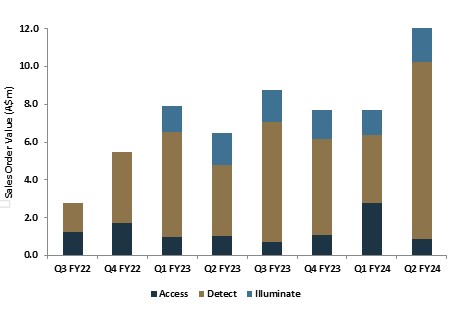

- Sales orders for Q3 up to $8.3m. Growth is largely driven by the Detect business.

- Sales orders YTD up to $23.1m which is 46% organic growth of the Detect and Access divisions

The Not So Good

- Access sales orders continue to decrease / remain flat. So far the agreement announced with Dormakaba in Dec 2021 is failing to produce any impact.

- Illuminate / GJD was reported to have had revenues of $7.95m in FY21. Based off the recorded revenues so far it looks like it would have been short of that number for FY22 and for FY23.

What To Watch

- H2 revenue guidance of $14m to $16m which would be an improvement over the $13.6m in H1. At the upper end of guidance this is on track with the growth rate required for previous three year revenue projections.

- Management have flagged improved sales orders for Access division in Q4 and going forward

- No updates provided on the Anglo American install progress.

- Growth of recurring revenue from Aura Ai-X and Aura IQ platforms and how this is reported in the full year results

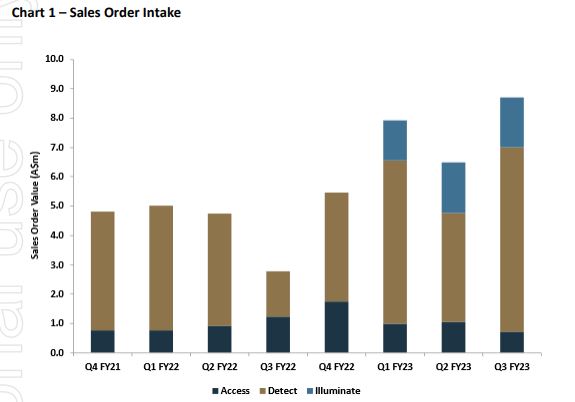

#Quarterly Update

stale

The Good

- H1 Revenue in line with guidance, with H2 expected to exceed H1. If maintaining the same organic growth rate, revenue for FY23 full year could be around the $29m mark.

- Organic growth of 16% over the previous period if GJD is excluded. This is predominantly from the “Detect” side of the business.

- Rearrangement of divisions into the key areas rather than by brand helps send the message of a single source for security rather than an owner of discrete businesses.

- The investor presentation deck provides a good overview on where the AVA product strengths lie in terms of AI & Machine Learning. If the message has improved in the investor deck it is likely the same for the business development teams.

The Not So Good

- Decrease in FFT / Detect orders for Q2 compared to Q1. This typically has been lumpy / cyclical so not a warning sign yet.

- BQT / Access growth still remaining flat

- With both of the above comments it is hard to see a strong signal for maintained growth as management are forecasting, however that may also mean that there is a large potential sales pipeline they are confident about to be able to be making such statements about the long term plans for the business.

What To Watch

- Anglo American AuraIQ to be installed in H1CY23. Watch for execution of order within the nominated timeline and then for timing around “ongoing” revenues.

- To meet the $70m baseline FY26 guidance AVA needs to continue maintaining the current growth rate of around 16% per half. The next several quarters will be a key indicator if this long range target is achievable.

- The other way growth plays out is through a series of acquisitions. What potentially also lends itself to this outcome is the restructuring into Detect / Access / Illuminate business areas.

- Further FFT orders expected from the existing North American energy client in H2.