Consensus community valuation

Probiotics brand Biome Australia ($BIO) published their HY report today, with the investor webinar on Wednesday.

I briefly held $BIO from July 2024 until July 2025, until I started to lose conviction in how the business was scaling (including a concern in 4Q25 when some inventory build got classified as an investing cashflow).

So even though I no longer hold, I wanted to take a look at the results and see to what extent my hunch is being borne out.

First, as usual, I'll start with what management are saying.

Biome First Half FY26 Results and Highlights Financial Highlights:

● Biome reports record H1 net profit of $1.18m (1H25: $0.43m), up 172%

● Record H1 EBITDA of $1.47m (excluding share-based payments)

○ Eighth consecutive quarter of positive EBITDA in Q2

● Record half-year sales revenue of $12.40m ○ Up ~40% vs PCP

○ Q2 FY26 revenue of $6.45m

● Annualised revenue run rate of ~$25.8m exiting Q2

● Gross margin of 61.1% achieved (1H25: 61.0%)

● Operating cash inflow of $2.09m, a $3.21m turnaround on PCP

● Cash receipts from customers of $13.35m, up 62% vs PCP

● Borrowings reduced to $1.50m from $2.91m at 30 June 2025

● Basic EPS increased to 0.53 cents (1H25: 0.20 cents)

Business Highlights:

● Fastest growing probiotic brand in Australian community pharmacy, with 100% of the product range in growth

● #2 ranked brand across total vitamins at Terry White Chemmart and the fastest growing in the category

● First major above-the-line winter immunity campaign in development for H2

● Fullscript distribution partnership secured in Canada (announced January 2026)

● Ethics approval granted for first human clinical trial on proprietary BMB18 strain with La Trobe University ● Mecca and Go Vita distribution partnerships commenced in H1

● New CFO Lauren Dwyer commenced February 2026

● New 1,350 sqm warehouse facility secured in Brunswick, VIC, adding 500 pallet positions to support ongoing growth and international scale

My Analysis

At first glance, it is a good result. While 1H tends to be the stronger half, Free Cash Flow generation of $1.9m is a standout, and allowed $1.4m of debt to be paid down, leaving the cash balance up from $2.7m to $3.4m. So, both on a cash and financial basis, $BIO appears to have passed through breakeven.

The HY financial trends are shown below:

And although the half-on-half comparisons are a bit noisey, the overall trends confirm breakeven has been reached and that from hereonin, this should be a profitable business.

So how about about scaling and operating leverage? In the graph below I've plotted COGS and Opex as a percentage of revenue over the last 4.5 years.

For the period FY22 to FY24, the business appeared to be scaling well, driven by 3 consecutive periods of revenue growth in the range 75% to 80% p.a.

However, in FY25 revenue growth slowed to 41.6%, and the lastest report for 1H FY26 shows a growth over the PCP of 39.9%. On its own, that's impressive. But with Opex also up 30.4% on the PCP, and the variations moving around from one period to the next, there remains some doubt in my mind as to how the business will continue to scale from here.

And this matters a lot, as in this capex light business, with %GM expanding modestly over time (from 57.7% in 1H FY22 to 61.1% today), Opex growth relative to Revenue growth is the primary determinant of profit growth. Given the picture of the last four HY periods, it is unclear to me what the future picture looks like.

Another consideration for me, is that it is unclear how quickly the international markets are scaling. $BIO has now had a few years in UKI, and if the product was getting traction there, I'd expect some quantification of progress. Strong international expansion could support overall revenue growth, given an inevitably maturing ANZ position. I'll look out for detail on this at Wednesday's webinar, and, in the unlikey even that I can attend live, I ask the question myself.

Valuation

Depending on how revenue and opex scale into FY27, at P/Es for FY27 of 25 to 35, I can generate value per share of anything from as low as $0.25 to as high as $0.70. Normally, I make investent decisions with a view on how a business scales over many more years; seldom fewer than 5. But I really don't have the conviction to make such a case for $BIO. And my concern is that this is going become a low margin FMCG business with limited brand value/differentiation in a competitive market, notwithstanding a very positive start in getting going in Australia over the last several years.

Conclusion

I will keep on eye on this. If the combination of international growth and continuing ANZ penetration can maintained total revenue growth closer to 40% p.a., and if costs can be controlled to scale at closer to 20% p.a., then of course this still could be a great investment.

But given the trends over the last 3 years, I'm not prepared to make this act of faith and remain on the sidelines for now.

The market has probably got his one right at the moment. In any event, I can't support an alternative view.

Disc: Not held

https://investorpa.com/announcement-pdf/20250828/179668.pdf

This appears to be a great development.

And further solidifies Biomes presence as a premium brand in the premium end of the market

“Shoot First, Ask Questions Later”

Today, probiotic brand $BIO announced its 4C. I took one look at it, and seeing a favourable “buy/sell” queue at the market open, sold my entire RL position, and I’ve just put in the order to sell on SM too.

Why would I do such a thing? I didn’t even have time this morning to attend the Webinar (although I would ideally have preferred to have done so, and I will watch the recording when its available)?

To answer that question, I’m not going to do a complete analysis of the quarter. Most things appear to be going well, with a logical progression of things I’ve written about at great length before. So, to save everyone’s time, I'll get to the point.

Reason 1: Inventory.

Reason 2: Inventory – how it was accounted for in the 4C.

Basically, a “Red Flag” (two actually) for me was raised today, in an area I have covered amply in previous straws. So, I was looking out for it.

Basically, Q4 saw a large build in inventory. Of this, $1.643m was accounted for as Operating Cashflow, and $1.295m as Investing Cashflow.

So, let me plot the 4C in two ways. Figure 1, “as reported”, and Figure 2, “as I read it”.

Figure 1: $BIO Cashflows from 4C (“as reported”)

Source: 4C report

Looking at the fifteen 4C report since IPO, prior to today, all inventory building has been classified as an “Operating Cashflow”, which is pretty normal – particularly in what I consider as a fast moving consumer goods operation.

So, one might think (and I certainly do) that putting a material chunk of inventory into “Investing Cashflow” for the first time ever would warrant an explanation. Well, here’s what was said.

- In the headlines … crickets. Oh, but “Net Operating Cash Outflow of $485 in Q4” OK, that’s not a problem because Q4 tends to be the weaker quarter for receipt.

- In the body of the report: “Within the quarter Biome made key strategic investments to support medium to long-term growth in both Australian and international markets. The highlights were the launch of Biome’s new range of products, Activated Therapeutics, an inventory-build to support FY26 growth, an investment in key international markets and the Activated Probiotics Symposium, a once-in-three-year customer education event.” [my emphasis added]

- … and a little later …… “The Company also drew down $1.3m from the NAB trade finance facility for investment in additional inventory to fund future sales growth and to maintain gross margin.” [my emphasis added]

- … and later still … “Payments for inventory and fulfillment was $1.643m, plus an additional $1.3m investment in safety stock. The company will maintain its working stock circa $3m while actively managing its level of safety stock, taking into consideration expected future sales growth, and seasonal, logistic and production factors.”

I don’t like the reporting of inventory build in this way. Building inventory, including safety stock, is completely normal and continuing part of any operation. And generally, as sales grow, the inventory and working capital to support it also grows. Safety stock (certainly as I have taught to over 600 MBA students over a decade) is an important working capital component of an operation. It has to be managed carefully, and it a critical and unavailable part of any operation.

Importantly, inventory also grows as a company expands to more regions (as $BIO has), as you need to hold more pools of inventory close to the market to support sales and customer service.

And inventory also grows the more product lines you have. (Again, as $BIO has, particulary with the whole new Activated Theraputics range.)

Therefore one of the key measures you have to monitor in the growth of any fast moving consumer goods company, is the growth of inventory. Because it consumes more and more cash as sales grow, geographies are expanded, and product variants proliferate. This has been a failure moce for many high growth FMCG businesses in the past, and no doubt it will continue to be in the future.

So, I don’t consider the inventory build as an Investing Cashflow. I see it as an inevitable part of the operation. And so, I have restated the 4C chart “as I read it” below in Figure 2.

Figure 2: $BIO Cashflows (“as I read it”)

This now gives a very different view as to the respective slopes of the “receipts” and “payments” dotted trend lines driving “Operating Cashflow” as I have redefined it. It is a very different picture between Figure 1 and Figure 2.

And for me that’s what today’s report is obfuscating. The operating leverage is not as strong as it has hitherto appeared. But this wasn’t a shock for me, I have been monitoring this factor over several 4Cs, and if you go back and read some of my earlier Straws, you will see I called it out. But I did not expect to see the magnitude of today’s number.

To provide another lens on this, in Figure 3 below I have plotted some other operating ratios.

Figure 3: Key Operating Ratios

Source: 4C reports. Note - all inventory build has been classified as “Operating Cashflow” for the purposes of this report (This differs from the reported basis).

What this picture tells me, is that up until mid-FY24, $BIO’s operations appeared to be scaling quite nicely. However, more recently, the trends have flattened out and – certainly on some metrics – seem to be going backwards.

This is critically important. Because it means that the bigger $BIO is getting, the weaker the cash operating margins are becoming. That’s why it is a thesis breaker for me.

I first invested in $BIO in July 2024, just before the 4Q25 report. My thesis was based on a view that the business would develop more favourable economics as it scaled. Five quarterly reports later, and on each of the three operational ratios plotted above, the opposite has happened.

When I invest, I am investing in an “economic engine” and I want to see – over a series of reports – evidence that the economic engine is building and becoming stronger. I can’t see that here, and therefore I am out.

“Shoot First – Ask Questions Later”

But I didn’t do all this analysis before selling this morning. All I saw was that inventory was up significantly, and that a large chunk of it has been classified as an “Investing Cashflow” with a rationale I found unconvincing and unprecedented.

(As this point, I will recall $FNP or $NOU as it is now called - those who have followed my work over the years might recall it. I have written about this before, because it was an example of a low margin foods business that got into all sorts of trouble with inventory management as it tried to scale. It was my worst $ASX investment ever, and I have written at length about it before. The big lesson I took from that event was how important it is to track inventory metrics in high growth, consumer good manufacturers. I didn’t then, and I paid dearly for it. Now I am not saying $BIO is another $FNP/$NOU. Definitely not. But when I see adverse inventory trends, as well as “reporting oddities”, that’s a double red flag for me.)

So for me it was a case of “shoot first, and ask questions later.” I have exited my full position for more or less what I paid for it. Whew.

Have I over-reacted? Quite possibly. But today’s report adds to a trend that goes against everything I know (and teach) and have experienced to my personal financial detriment.

I hope I am wrong and that over coming reports the business continues to go from strength to strength. If the facts prove me wrong, then I’ll be happy to get back onboard. But I think that, even in the success case, this is going to be a slower burn than I had initially hoped. That, combined with its microcap "fragility", fundamentally changes the risk-reward equation for me.

Finally, I didn't need to do all the analysis that I've presented in this post, because I was looking for the effect. Why? I had three questions on my risk register:

Q1: Is the quality of growth in Australia holding up, as the business matures in this market?

Q2. How dilutive to the operating leverage is getting going in NZ, UKI and Canada all at the same time?

Q3: Is the Activated Therapeutics line (a profileration of SKUs which I view as departing from the core science thesis), actually a good idea? More SKUs, more operational complexity, more inventory etc.

I don't know the answer to these questions. But the summative effect doesn't look good to me....at least in the short term.

Disc: Not held in RL and SM

Probiotics company $BIO published their 4C today.

While the shares have been in doldrums for the last few months, with a fairly ugly short term chart, I'll summarise my analysis which explains why - based on performance - I am not unduly concerned at this stage, and what I am looking forward in the come reports.

Their Highlights

● Biome records $195k EBITDA for Q3

● Biome recorded a net operating cash inflow of $123k

● Biome achieves another high growth quarter in sales revenue, reaching ~$4.51m for Q3, an increase of 41% vs PCP

● Biome achieved a gross margin of 61% for Q3

● Biome had a cash balance of $2.7m as at 31 March 2025

● Biome expects to report its first full year net profit for FY25

● Record cash receipts of $4.91m in Q3, up 61% vs PCP and up 13.% vs Q2

Revenue Growth Chart

(Note: the Q3 dip appears to be seasonal, so expecting a strong final Q)

Analysis of Cashflow Trends

Basically, for the last 6 consecutive quarters, $BIO have been cashflow positive - save for the MD 3yr LTIP payment in 1Q FY25, which more than wipes out the gains!

So, someone looking at the trend of the last 6-8Q, rather than the longer trend, could reasonable ask whether the underlying operating economics of this business are strong enough to justify its valuation.

To answer this question, you have to dig a little deeper. And therefore below I have plotted they cash operating ratios, which I think tells the story.

I've been selective here, leaving off R&D and Capex - as they are not material items, exhibiting no major trend.

Overhead (green)

I've combined [Staff Cost + Admin & Corporate Costs] and these are declining nicely as a % receipt from 66% in $Q23 to 33% in 3Q25m down a little from 34% in 2Q25.

So, Blair is maintaining overhead discipline, despite over this time adding a small number of heads for the expansion in UKI and Canada.So far, so good.

Sales & Marketing (Orange)

As a function of receipts, sales, marketing and advertising has fallen from 26% of receipts in 4Q23 to around 9%, up slightly from 7% in the previous Q. That's also pretty good, although I expect the staff costs of the sales and marketng "educators" are accounted for in the "Staff Costs" line.

One thing to watch will be that this might increase in the next few quarters, as $BIO introduces the "Activated Therapeutics" range.

However, overall both as a trend and as an absolutely percentage, there is nothing to be concerned about here.

Inventory and Fulfilment (Blue)

As I indicated in my last major analysis of $BIO, inventory and fulfilment is where we are seeing the drag on overall operating leverage coming through. It reached a lowpoint on a strong downward trend of 40% in 3QFY24, but has been steadily trending up ever since, now standing in the latest period at 53%. It needs to come down again to not be an overall drag on the business economics.

So why is this happening?

As new products are added to the range, expansion occurs internationally, and $BIO steps up the rate of adding new outlets at an accelerated rate, this is clearly adding weight in the supply chain. From my perspective this is the key metric to monitor in the periods ahead.

Inventory and channel management is a big issue in FMCG. It is clear that this is the motivation for BVN to onshore final packaging to Australia, but that in itself can only make a very small difference, as I've shown previously.

My sense is that this is a deliberate strategy from Blair. Having got comfortable that he is there or therabouts on cash flow break-even, he is investing in inventory to supply new outlets and new terriritories, so that product is available in more locations to build the brand and drive sales velocity.

But of course, it is by no means a given that in new outlets sales velocity will continue to grow and so this is the key metric to continue to monitor. It we don't see that turn back down over time, then it becomes a thesis breaker.

My Conclusions

Unlike with many other brands, Blair isn't use big sales, marketing and advertising budgets to drive revenue and brand awareness. He's doing it through the marketing educators with the pratitioner customers, and backing that up with inventory as new outlets come online. Through this strategy, he has got pretty much to a breakeven business, as outlets continue to expand both in Australia and overseas.

So now its game on. There is no possible justification for further territorial expansion until he can show favourable economics across Australia, NZ, UKI and Canada. That is now the point to be proven.

I will now keep alert to two potential future red flags: 1) further territory expansions and 2) inability to get the inventory/fulfillment ratio down - or at least to stablise it. (Of course, adding Activated Therapuetics to the mix might keep some pressure on this metric in the next report or two.)

I'm happy to hold at my current position size and see how this story unfolds over the next year. And with quarterly reporting likely to be retained for a while, I can closely monitor the key operating ratios.

This is by no means a done deal, but the game is now on.

Disc: Held in RL and SM

Probiotics supplement brand company $BIO issued their HY Report today.

Their Financial Highlights

Biome reports its first net profit in H1 FY25

○ +$96,228 (excluding R&D rebate)

○ +$433,395 (including R&D rebate)

Biome achieved positive EBITDA for H1

○ $351,765 (Excl. R&D Rebate and Share Based Payments)

○ $229,917 in Q2 an increase of 89% vs Q1

Biome reports record half year and quarterly sales revenue (H1FY25 $8.86m; Q2FY25 $4.6m)

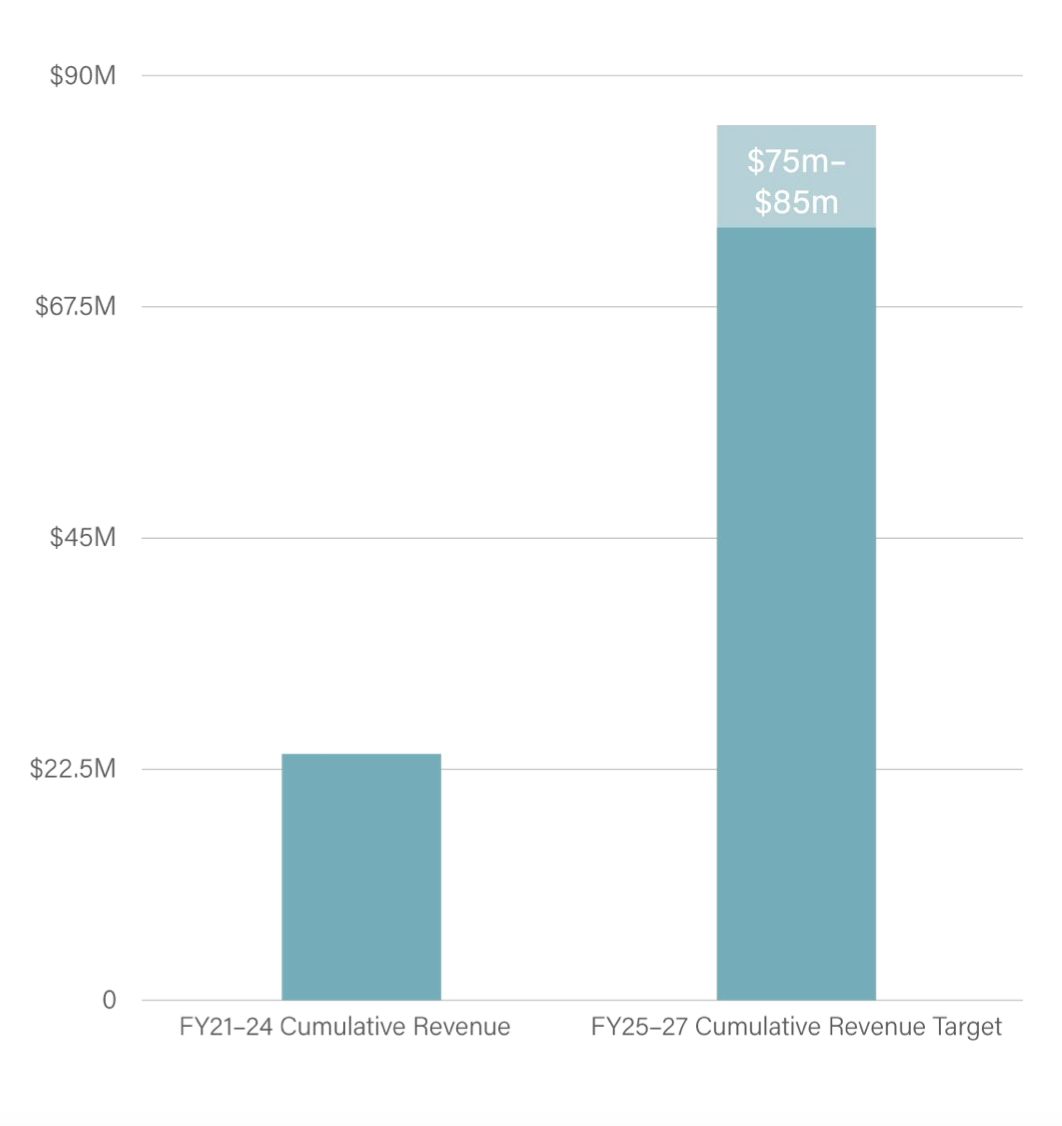

Biome released Vision 27 Strategic plan with three year cumulative revenue guidance of $75-$85m (FY25-27)

Biome reports a gross margin of 61% for the 6 months to 31 December 2024

Their Business Highlights

- Biome increased its Australian distribution footprint in H1 to 6000, an increase of 20% vs H2 FY24

- Biome successfully completed its in-vitro research on its strain BMB18

- Biome entered a partnership with FaBA to gain access to matched research funding to develop BMB18 via a government grant

- Biome launched its new cholesterol-lowering probiotic, Biome Cholesterol™ Probiotic in Q1 FY25

- Biome Successfully launched into Canada with Ecotrend Ecologics in September 2024

Figure: $BIO Quarterly Sales

My Assessment

Pretty much everything in today’s report was either expected or has been reported, such is the fastidiousness with which CEO Blair (BVN) keep us posted on developments. But, it is actually good to see all the achievements of the half pulled together in one place. They’ve been busy and done a lot.

Australia Expanding Outlets

It is good to see a strong focus on expanding Australian distribution. While it is a “soft” metric, getting to the 6000 distribution points target from 5000 6 months early is excellent. After all, it is the Australian sales that will do the heavy lifting of generating cash while the expansions in the UK and Canada find their feet. This kind of trajectory means that the 800o goal in Vision 27 should be easily achieved, well ahead of schedule. Of course, while this is good, BVN has always said that the real potential lies in getting more sales per account.

International - a comprehensive update promised!

BVN has promised a “comprehensive international market update during the year”. This will be welcome. To date we have had some indication of the international sales contribution in FY24, and a little information on the staffing approach. But I’d be keen to see some tangible indications of sales momentum building in the UK, and of course it is very early days in Canada but BVN has spoken positively about product-market fit there, so it would also be good to have some numbers to back that up.

Onshoring Manufacturing - What?

One note in the release caught my attention: “Onshoring finishing manufacturing of Biome’s key product lines.” Without any real explanation. I know BVN has said this is something that might be contemplated in the future, but to see it report as something that is actually done, has caught me by surprise. And I HAVE been paying attention. Just to be clear what this likely means – I would expect that $BIO are finding an Australian onshore contract manufacturer to do the product encapsulation and packaging. I’m not sure what the effect of this will be on %GM, however, with Australia and the major market for the foreseeable future, it will reduce logistics costs, as well as providing some supply chain resilience. So I am all for it, even if I am not sure that $BIO has the scale for this to be a “must do.” I’m keen to learn more about this at future briefings.

Financials

Today’s result is an important milestone. It’s the first half for $BIO achieving positive NPAT, with NPAT up almost $2m compared with the PCP. Just to drive the point home - BVN called out that they achieved this even without the help of the R&D rebate!

This has been driven by strong revenue growth (+47.4%) while Total Operating Expenses actually declined by 3%. The big driver here was a 22% reduction in Corporate Costs to PCP, and sales and marketing growth being kept to only 24.1%.

That financial performance is impressive IMHO. It means the $BIO have been able to moved ahead with Europen commercialisation, run the market test in Canada and then move to commercialisation AND significantly expand the number of Australian outlet by 20% while holding expense essentially flat. Wow! I like it.

Cash - Mind the Inventory

However, digging through the financial accounts there is one thing to keep an eye on, Cash Flow was quite weak, with the business still burning a modest $0.3m of cash during the period. The main driver here is the increase in inventory, which over the 12 months has increased from $2.08m to $3.13m or +50%. Given the expansion of outlets being serviced in Australia, new products, and growth in Europe and North America, this isn’t a concern at this stage. The increase in inventory is broadly in line with revenue growth....just a smidge ahead However, it is a reminder that in FMCG (and I think for these purposes it is instructive to think of $BIO as FMCG rather than healthcare) inventory management is key.

Many a growing FMCG company posts good financials, but can get caught out of cash management given the inventory requirements needed to support market growth (I am triggered by memoroes of $FNP aka $NOU). I think $BIO will be OK, as they have a good %GM and expense control, and they need to invest in inventory to get it to their expanding customer outlets. Of all the places to burn the cash, I am happy that this is the right place for $BIO. BUT, we need to keep an eye on any trends here.

For now, $BIO has bitten off all it can chew, and I expect to now see a period of consolidation around ANZ, UK and Canada. If so, this should enable inventory growth to track more closely in line with revenue growth.

Final Takeaways

This is a good report. No surprises, and overall, it is good to see the financials coming together nicely behind all the recent individual news releases. I’m a happy holder here, and look forward to the update in the international markets.

Although I initially took only a very small (c. 1% position), SP volatility has given opportunities to add more at lower prices. But this is still is a risky and unproven business on the international stage. Can they build a multi-national probiotics brand? Early days. So I am going to maintain my current 3+% RL holding and let the company's progress work its magic over time .... or not.

Disc: Held in RL (3.2%) and SM

The post below popped up in my LinkedIn feed this morning, giving an insight into how $BIO is going about establishing the product presence in the UK nutrition and wellness practitioner market. I've added below a brief description of the association, (provided by my BA ChatGPT.)

Industry bodies like this are always on the lookout to drive member engagement and value. So a good reception at, for example, the Berkshire branch, would doubtless lead to invitations over coming weeks and months at other association branches - over time getting the message to a decent share of active portion of the associations 3,500 members, and leading to coverage in association newsletters and social media posts.

These industry bodies appear to be as important in the UK as they are in Australia, and tapping into them in this way, as indicated by the post, is likely a very cost effective way of executing $BIO education-based sales and marketing program.

About The BANT (by ChatGPT)

The British Association for Nutrition and Lifestyle Medicine (BANT) is a non-profit professional body representing approximately 3,500 nutrition practitioners in the UK. Established over 20 years ago, BANT sets standards of excellence in science-based nutrition and lifestyle medicine.

BANT members are trained in nutritional sciences at a minimum of degree level and are equipped to work clinically with individuals. They provide personalized nutrition and lifestyle recommendations, translating complex science into practical advice tailored to individual health goals and dietary preferences.

A key resource offered by BANT is the Nutrition Evidence Database (NED), the UK's first scientific database specializing in nutrition and lifestyle medicine. NED provides evidence-based information to support clinical interventions and inform practitioners' recommendations.

BANT also engages in public education, offering resources to help individuals make informed dietary and lifestyle choices. Their mission is to promote health and well-being through personalized nutrition and lifestyle medicine, contributing to the integration of these practices into mainstream healthcare.

Disc: Held in RL and SM

Q1 Sales revenue represents a ~$17m annualised run rate (ARR)

Get Share price going - Activated Probiotics, Activated Nutrients, and AXP.

ASX ANNOUNCEMENT 1 October 2024 Biome reports record quarterly sales revenue for Q1 FY25

● Biome achieves record quarterly sales revenue of ~$4.25m (unaudited)

● Sales revenue increased ~$1.51m or 55% vs PCP Q1 FY24

● Sales revenue increased ~$450k or 12% vs Q4 FY24

● Q1 Sales revenue represents a ~$17m annualised run rate (ARR) Microbiome health company Biome Australia Limited (ASX: BIO) (‘Biome’ or ‘the company’) is pleased to provide a trading update for Q1 FY25. Biome’s quarterly sales revenue totalled ~$4.25m (unaudited), representing a 55% increase vs the previous corresponding period (Q1 FY24, $2.74m) and 12% above the previous record quarter (Q4 FY24, $3.8m).

This result exceeded the $4m target for the quarter (Ref: ASX announcement dated 3 September 2024) by $250k or 6.3%. Biome’s Q1 sales revenue represents an annualised run rate of $17m, with growth expected to continue through the remainder of FY25.

Biome Australia’s Managing Director and Founder, Blair Vega Norfolk, commented: “I am excited to share this result for Q1 FY25, another record quarter in sales revenue following our recent release of Biome’s Vision 27, which outlined our growth plan and prospects over the next three years.

I look forward to sharing further updates on our growth and performance in the coming periods.” -ENDS

BIO has just released their anticipated plan for the next 3 years "Vision 27" click here

Video presentation click here Once again Blair presents very well. Seems to know his stuff, seems to be across various pharmacy markets worldwide.

At first glance the outlook seems positive, potentially very positive

A few key take aways:

- Increase pharmacy/distribution points in Australia from 5,000 - 8,000 (67% TAM)

- Increase companies global footprint, pushing into Canada and Europe. Funded via existing cash flow.

- New product range to launch in H2 FY25.

- Intellectual Property agreement was completed in FY24 and accompanying project to develop novel biological IP is well underway

Return (inc div) 1yr: 465.38% 3yr: N/A 5yr: N/A

Distributer footprint:

Ecotrend Ecologics | Natural Health Product Distributor

Today we manage over 2500 retail and over 2500 professional accounts, as well as work with over 120 fantastic and unique brands. Ecotrend believes in the human touch. Family and friends play an important role in the almost familial relationships we are proud to maintain with our brands. Treating both people and our planet with dignity, Ecotrend has nurtured a foundation of loyalty and trust. Health is not just supplements and vitamins; it’s a lifestyle. Ecotrend Ecologics is your go-to distributor for high-quality lifestyle products, including top brands of vitamins and supplements.

For what it's worth, Canary Capital brought out the following "Equity research report" last week. Click here

While this may be their effort to pump up the share price, its worth a read.

The report gives some background to the company and the industry. It outlines some key risks the company faces.

Also BIO is compared to Blackmore's, Life-space and Swisse. All of which have been bought out.

Did anyone else notice the coincidental timing of the directors being issued 6.7m shares on December 1, 2023, funded by a loan from the company with a price of 12c/share and then what happened to the share price from the day they were issued ? From what I can see there is no escrow period on those shares.

I checked Biome website:

Activated Probiotics® is a world-first range of live biotherapeutic products clinically proven to help prevent and support the management of various health concerns, including low mood and sleep, bone health, iron malabsorption, mild eczema and IBS, through randomised double-blind placebo-controlled trials. Through practitioner-only distribution, Biome is committed to educating health professionals on the newfound systemic health effects of the gut microbiota and helps them to provide innovative and evidence-based complementary medicines for the management of some of humanity’s most prevalent and chronic health concerns.

Biome also developed and distributes scientifically formulated, organic nutraceutical range Activated Nutrients®.

In my ongoing research, this morning I came across a Bell Potter note - well the front page at least! (Updated June-24, TP=0.73)

Just to compare, their FY25 and FY26 NPAT is $0.3m and $3.2m, respectively. My "scenario" that I showed in yesterday's straw (which I argued supports a TP of $1.10), has values of $1.9m and $7.4m.

So my "scenario" is quite a bit more bullish than BP, but in the grand scheme of things, it is in the ballpark.

If I am critical of this note, it appears that they talk about a "gap in the market". This may be true about the Australian market (which is also supported by @Rick's anecdote, yesterday). However, I am less clear the extent to which the same can be said in other markets.

Without making a negative remark about Bell Potter, I do make the general comment that some analysts tend just to repackage what management has told them, without doing independent, fact-based research. So, in sharing this research, I am not endorsing the statements, but just sharing the views of others.

I remain in an information gathering and analysis mode, and I am not yet taking a view on the stock (for avoidance of doubt). But it is interesting.

Disc: Held in RL (0.25%) and SM

In this straw I set out an interesting journey I have been on this week, following an exchange with @Tezzdog last weekend, that put $BIO on my radar screen. I posted an initial - and somewhat bearish - response to @Tezzdog's question.

@Strawman promptly came to the party and, by midday Monday, had lined up a SM Meeting with MD and Founder Blair Vega Norfolk (BVN) for Monday coming. (Well done, sir! Where else can you get that kind of access to a CEO – I ask you.)

For those who are interested, this straw contains some further resources that can help prepare for Monday. (If you are anything like me, I like to go into Strawman meetings with a lot of research under my belt, as I find I "hear" so much more. I agree with @Wini from the recent SM Meeting that its important to have an informed point of view, before you listen to management.)

Alternatively, you can skip all this and I’ll see you on Monday, leaving you with the thought that, yesterday, I picked up a tiny starter stake in $BIO - even though there's every chance I have royally overpaid. However, if it meets my expectations, I have a lot in the tank I'd be prepared to allocate over the next year or two. So, I'm not too fussed.

Summarising my Bearish Views

My governing thoughts (based on an hour's research on Sunday) was that I considered 1) the global competitive landscape and 2) the strength of board and management as significant barriers to achieving the global success to which $BIO aspires. I also highlighted why, at 11x revenue - whatever the outlook - it ain't cheap. That was then.

Meetings with BVN which Helped Me Form a More Bullish View

The following two videos are worth viewing:

There's quite a bit of overlap between the two videos, with more insights in the second. So, I got my assistant Claude.AI to summarise the transcripts under key headings. I've reviewed it, it seems pretty accurate, and I’ve dumped it at the end of this Straw for those who are interested, but haven't got 30 minutes to watch the video. (Scroll down to the dotted line, if you want to skip straight to that bit.)

My Take-Aways - what I've learned over the last 5 days

I structured my takeaways from this material and other research under some key headings, including what I learned in doing the next level of research, and how it challenged some of my initial bearish views. I was not starting from scratch, as I did some work on the probiotics market several years ago when I was looking at Blackmores, but never progressed further. It is a market that has long been of interest to me, partly because it combines healthcare and retail – two areas in which I am very happy investing and have enjoyed some success over the years.

1. Research-supported Condition-specific Activated Probiotics

In my bearish response at the weekend, I focused on just how large and well-established the global probiotics market is, and how established the international competition $BIO will faceas it ventures beyond Australia.

BVN made a remark in both videos (which no doubt we'll hear on Monday) that $BIO are first movers in "clinically supported, condition-specific, probiotics". Having cursorily examined some of the global competitors, I am not sure I agree with this statement, and I believe I can show that it is incorrect. However, it is true that the vast majority of the current global probiotics market has quite general label claims (e.g., “promoting gut health”), without specific clinical trials support or defined, specific indications.

Another advantage is that the formulation/encapsulation technology $BIO uses allows more of the live probiotics to survive passing through the stomach to reach the gut (small and large intestines). Again, while I am sure this isn't unique, it is a differentiator from the vast majority of probiotic pills, powders, yoghurts, and drinks out there, which churn around in the stomach acid for 30 minutes or so. (I happen to have 5 years’ experience working in pharmaceutical formulation technology and manufacturing, so am not an entirely novice in this area. In fact, part of my post-doctoral research involved a collaboration looking at sustained-release formulations, albeit I was not a principal investigator for this work!)

The standard behind $BIOs claims is that each formulation is supported by double-blind, randomised, controlled, clinical trials measured against specific end points. Again, I want to emphasise that I don't believe they are unique in this respect. However, it does differentiate them from most of the current market. Learning this, made me sit up and take more notice.

2. A Differentiated Go To Market (GTM) Approach

This is where BVN's marketing background shines through - and I think it really does differentiate them. Listening to him speak convinces me that this guy really does have deep marketing expertise.

Most probiotics are essentially a fast-moving consumer good (FMCG). Develop the brand, do the distribution deals, and get as much shelf acreage for each SKU. Support sales through brand-building, advertising and marketing spend. This is what Blackmores does with Bioceuticals. If necessary, discount the hell out of it to land the mega distribution deals, e.g., Chemist Warehouse.

$BIO is different. They sell "behind the counter". They aim to provide products to the community pharmacist, the nutritionist, the dentist, etc. where they can add value to their customers. They are giving these customers something you can't get at the "pile 'em high and sell 'em cheap" outlets.

This means the professional is incentivised to recommend $BIO's product. Because they generate more margin per sq metre of shop space than the competing mass market offerings, where margins are thin. While $BIO does distribution deals, they won't compromise on price. BVN quantifies these metrics in the videos, and I’m sure we’ll hear more about that next week.

To test this, I've done some online trawling, and indeed, each product appears to have a consistent price floor. Maintaining pricing discipline appears to be a core value – it maintains margins and supports the delivery of value to the healthcare-professional-retailers.

3. A Global Rollout that Follows the Australian GTM Approach

$BIO are not in a hurry in their global rollout. While they have plans for UK, EU, Canada and soon we'll hear about the USA, they are following a strategically slow approach.

The UK and Ireland is an example. They've been working there already with key professionals and opinion leaders to market test the product fit and build the support of the healthcare professional community.

This approach is consistent with what they've delivered in Australia since 2018. It not a boots-on-the-ground and roll it out classic FMCG sales and marketing strategy. They want to work with the targeted healthcare professionals to build product support and market fit.

(I think BVN started out in luxury goods marketing, so he understands brand value and pricing!)

This is very important to me, because it means that with the next 1-2 years of getting going in the UK, we'll have an opportunity to see to what extent they can scale in another market. And from UKI, then the EU is next.

4. Capital Raise - What Capital Raise?

In my bearish response over the weekend to @Tezzdog, I "confidently" predicted that with the recent, massive uptick in SP, and the impending global rollout, that $BIO will be raising capital, and soon.

But will they? Watch the video and see what you think. BVN clearly takes some pride in that they haven’t done a major raising since IPO and that they are now cashflow positive. Their GTM approach is entirely consistent with boot-strapped growth (think $PME).

Furthermore, with 60% gross margins (which I think must include elements of embedded "R&D" and "manufacuting capex" in the cost of goods given their business model), excellent expense control, and a capital-light model, maybe they can do it.

That said, the SP has gone crazy over the last year, so perhaps there is something to be said for building a strong balance sheet. Defintitely one for @Strawman to question on Monday.

5. Market Position

This is really all about Australia. $BIO has established 5,000 “distribution points” across Australia, roughly split 50:50 between community pharmacies and practitioners. They have deals with Terry White Chemmart (600 pharmacies) and Priceline, and supply 1500+ independent pharmacies, giving them a product line that the big discounters can’t access -well they can if they are prepared to pay the full price.

So, what does $13m of sales look like in an Australian market context?

Well, according to Research and Market (2023), the overall market size is around $350m. But of course much that includes the animal segment and probiotic foods. Based on an older source (2016), only about 8-10% of the headline market relates to “Dietary Supplements”. If that’s true, then $BIO have achieved a significant Australian market share in 5-6 years. (I need to do more work on this.)

BVN believes the runway ahead in Australia is 8x current sales, driven by doubling the number of outlets and then growing the sales per outlet. I’m less sure about this, and hopefully we can discuss further on Monday. (To what extent does the “creaming curve” and “diminishing return” come in to play?)

In any event, it looks like there is a good runway ahead in Australia, where they appear to have established a financially sustainable model at $13m revenue, growing at c. 70-80% p.a..

6. Economics and Scaling - Looks Good So Far

6.1 Quarterly Cash Flow Trends

(edited straw now includes legend in graph below)

The chart above shows my usual trend analysis from the 4C Cashflow statements. While there is some seasonality through the year (which BVN comments on), the trend is clear.

This business appears to have clearly headed to the inflection point, while yet to achieve $15m in annual revenue. This has been possible because of disciplined expense control and the capital light model (R&D partnerships, and outsourced manufacturing – active agents and formulation.)

6.2 Balance Sheet

With only $2m in cash at the last 4C, $BIO is running close to having to raise capital.

However, rather than do this (beyond exercise of options), BVN has been drawing down some debt. At the last 4C they had drawn $1m of a $1.2m facility.

Although $BIO now appears to be cashflow positive, a question for the SM meeting is whether it would be prudent to leverage the current high SP and raise some capital to buttress the balance sheet for the next phase of growth. (To my mind, $20 million wouldn't be too dilutive, and would give some head room on staffing, and licencing in new molecules.)

6.3 Financials and a What-If Scenario

I’ve done a little “spreadsheet jockeying” this week (of course, as I’ve had two weeks of cold turkey!), and from the 2021-2024F actuals, and a modelled scenario for FY25 and FY26 I have developed the picture below.

The above picture is a scenario – its not a forecast!

What it shows is the impact of strong revenue growth, 78%, 76% and 80% (FC) for the last 3 years, including the current.

Expense control has been exemplary, with +3.4% (FY22) and +6.7% (FY23), and I’ve thrown in a +20% assumption for each of FY24, FY25 and FY26.

With minimal D&A (capital light), if revenue growth in FY25 and FY26 are 75% and 70%, this baby is soon generating a meaningful NPAT!

Why did I choose these revenue growth numbers for this scenario – see my comments in 5. Market Position, above. And BVN says in the video that current rates of growth can be sustained in the short to medium term.

7. Ownership

According to Simply Wall Street, individual insiders own 34.5% of $BIO, with BVN’s shareholding at 8.5%, and BVN’s long-term partner in science Dr JB (who I referred to last weekend as the part-time chief scientific officer) has 1.72%,

So, there is reasonable alignment and, in one year, BVN has become a wealthy man!

8. Valuation

In my experience, it is notoriously difficult to value a company that’s coming up to the inflection point.

In terms of valuation multiples, you might take one look at 11x Revenue and move on.

But if $BIO can deliver the financial performance in the scenario I’ve shown above, then at a SP of $0.63, its P/E in 2026 falls to 19.

If its P/E in 2026 is 40 (which would be very modest given my forecast revenue and earning growth), then the valuation discounted back to today would be $1.10.

So that’s not a valuation, but as a result I felt quite comfortable taking a RL position of 0.25% because I want to follow this business very carefully as I do further research.

4Q is typically a high payments period, so if there is a bit of a "SP panic" at the next 4C, I’ll up my position. Whatever happens, our shared experiences here in microcap land is that you can take your time building a position. FOMO is for Dumbos!

9. BVN – A Founder with a Vision

BVN tells his personal story in the longer video – and it is quite interesting. I’m quite impressed by him. We’ll all get a chance to form our own views next week, so I’ll keep this brief.

One point from his CV is that he is a Non-Exec Board Member of the International Probiotics Association. I think this is interesting because it means he is linked into the global industry players, and this role will help him incubate the partnerships that are key to $BIO’s business model. And it also gives him an international industry perspective, which is so important to $BIO’s long-term success. (You can see some of his posts showing his attendance at industry events on LinkedIn.)

CONCLUSIONS

I find $BIO and BVN interesting. It was easy to be dismissive with 1 hour’s research on Sunday. But with now 30 hours of more in-depth work under my belt, including updating my view on the sector globally, I find $BIO to be very interesting and am really looking forward to next week’s meeting.

I still have concerns about the Board and Management bench strength, given the company’s ambition. But I find BVN to be impressive. He is the founder and has a vision for this firm. He appears to be strongly values-driven, and clearly articulates his strategic thinking. (And remember, Sam Huppert and Richard White grew with their businesses over the years!)

While I don’t completely buy everything he has said (when viewed from the perspective of some of the larger probiotic-specialist competitors overseas), $BIO is definitely a unique play in this part of the world. The big question is – how do they scale and compete internationally? UKI will give us the first insights, and we will see this over the next 1-2 years. Yay!

My final word – thank you @Tezzdog for asking the question! If nothing else, you have helped me have a very interesting first week back from holiday.

--------------------------------------------------------------------------------------------------------------------------

Claude.AIs Summary of the "Shares In Value" Interview with BVN (5th July 2024)

--------------------------------------------------------------------------------------------------------------------------

Company Background and History

Biome Australia (ASX: BIO) is a company focused on developing and commercializing live biotherapeutics and complementary medicines. Founded by Blair Vega Norfolk in 2018, the company's journey began much earlier:

- In 2012, Norfolk completed his MBA and was working in California advising nutraceutical companies on customer understanding.

- After developing his second autoimmune disease, Norfolk partnered with Dr. JB, an Australian PhD in medicine with 20-30 years in drug research, to formulate nutraceutical products in 2013.

- They initially planned to test market in Australia before launching in North America, but realized Australia was a significant market for complementary medicines and probiotics.

- From 2013-2018, they used their initial company as a vehicle for R&D, market understanding, and building relationships with distributors, pharmacy groups, and suppliers.

- In 2016, they moved into R&D and research in the microbiome space.

- Biome Australia was founded in 2018 to focus on condition-specific probiotic products.

Product Range and Unique Selling Proposition

Biome Australia launched its Activated Probiotics brand in November 2019 with nine products. Key aspects include:

- First-mover in condition-specific probiotic products globally

- Unique IP and products put through randomized, placebo-controlled, double-blind clinical trials

Product highlights:

- Biome Lift: Clinically validated probiotic for mental health

- Biome Fem: Probiotic for female vaginal health conditions

The company's point of difference in the market includes:

- First-mover advantage in condition-specific probiotics

- World-first clinical trials

- No direct competition on their products

- Premium, affordable pricing strategy without discounts

- Strong margin (60%+) compared to industry standards

Growth and Distribution

Biome Australia has experienced rapid growth since its launch:

- FY20: 100 stores, $800,000 revenue

- FY21: 1000+ stores, $2.1 million revenue

- FY22: $4.1 million revenue

- FY23: $7.2 million revenue

- FY24: $13 million revenue (beating upgraded forecast of $12.5 million)

Current distribution:

- Approximately 5,000 distribution points in Australia

- Roughly 50/50 split between community pharmacies and practitioner market

- Major customers include Terry White Chemmart (600 pharmacies) and Priceline Pharmacy

- 1500+ independent pharmacies

Future growth strategy:

- Currently at 40% of addressable market in terms of distribution points

- Only 25% developed within existing distribution footprint

- Potential to quadruple current revenue with existing distribution

- Opportunity to double distribution

- Conservative approach to expansion, focusing on optimizing existing accounts before adding new ones

Financial Performance and Outlook

Key financial highlights:

- Achieved first quarter of positive cash flow in December quarter (FY24 Q2)

- Positive cash flow in March and June quarters (FY24 Q3 and Q4)

- Positive EBITDA for the first two quarters in a row

- Cash flow positive and expected to remain so

- No capital raising since IPO ($8 million raised)

- Grew from $2 million to $13 million in sales and became profitable with initial capital

Future financial outlook:

- Continuing to reinvest for growth

- Aiming to become a significant dividend-paying business in the long term

- Planning to release "Vision 27" - a three-year strategic plan

- Likely to provide revenue forecasts for upcoming quarters and financial years

Clinical Research Pipeline

Biome Australia differentiates itself through clinical trials on finished products:

- Leveraged 30 years of partner IP and research to develop their product range

- Own 40-50% of their product formulations and research

- For licensed products, conduct clinical trials to own hybrid IP

Current clinical trials:

1. Biome Lift (mental health probiotic):

o Study with La Trobe University on sub-threshold depression

o Product on long-term exclusive license, but clinical trial gives Biome IP ownership

2. Biome Daily Kids:

o Study at Federation University on children in daycare settings

o Focus on upper respiratory tract infections, colds, flu, and stomach bugs

o Biome owns the IP, formulation, and concept

3. Additional studies in late-stage development (yet to be announced)

Research strategy:

- Lean R&D budget

- Develop relationships with universities and IP companies

- Negotiate partnerships where Biome provides advice and product, while partners fund the studies

Product Efficacy and Impact

Biome Australia focuses on demonstrating product efficacy through:

- Clinical trials

- Real patient feedback and testimonials

- Visual evidence for dermatological products (e.g., eczema and acne treatments)

The company emphasizes its social and ethical impact:

- Registered as a B Corp company

- Reports on social, environmental, and sustainability standards

- Focuses on patient impact and improving quality of life

International Expansion

Biome Australia has a conservative but strategic approach to international expansion:

- Entered UK and Irish markets 2.5 years ago

- Initial soft launch focused on educating health professionals

- Launched into health retail in UK and Ireland in January 2024

- Recently received Health Canada approvals

- Considering North American market entry via Canada in the near future

Leadership and Vision

Blair Vega Norfolk's background and vision:

- Over 13 years of experience in the global nutraceutical and probiotic industry

- Passionate health advocate

- Speaks to medical professionals about probiotics

- Board member of the International Probiotic Association

- Goal to solve health problems not addressed by current medical interventions

- Aims to position Activated Probiotics products alongside pharmaceutical drugs

- Long-term vision to grow Biome Australia to rival major players like Blackmores

Investment Potential

Key points for potential investors:

- Microbiome space is leading drug discovery and development in the pharmaceutical industry

- Probiotic businesses globally are performing well due to product efficacy

- Biome Australia has potential to capture significant market share

- Company has internal expertise to potentially develop probiotic drugs in the future

- Considering pursuing TGA or FDA-approved probiotic drugs to gain trust from health professionals

Closing Remarks

- Investors can find more information on the Biome Australia website's Investor Hub

- The company is open to answering further queries from potential investors

- Biome Australia represents an opportunity in the growing microbiome and probiotic market, with a focus on clinically-proven, condition-specific products and a strong growth trajectory.