Consensus community valuation

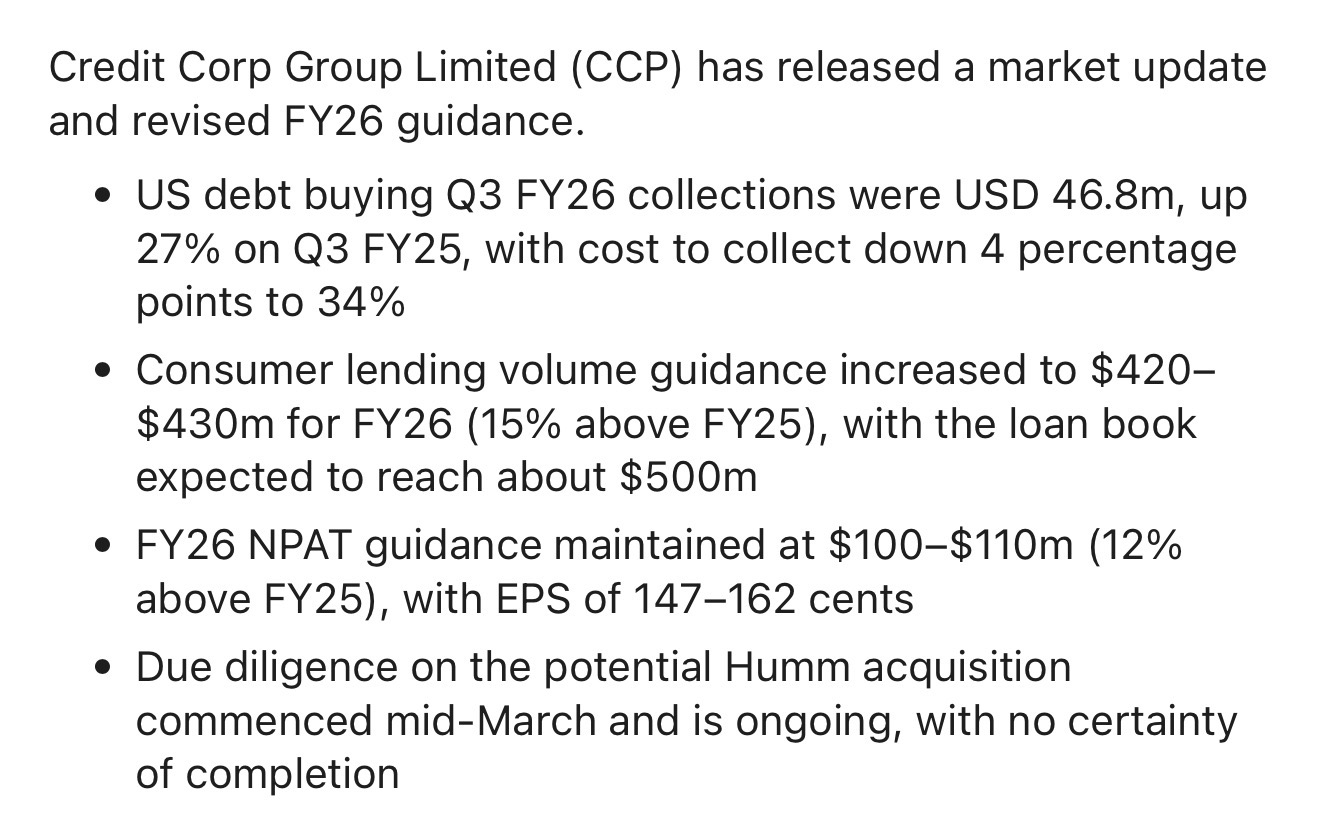

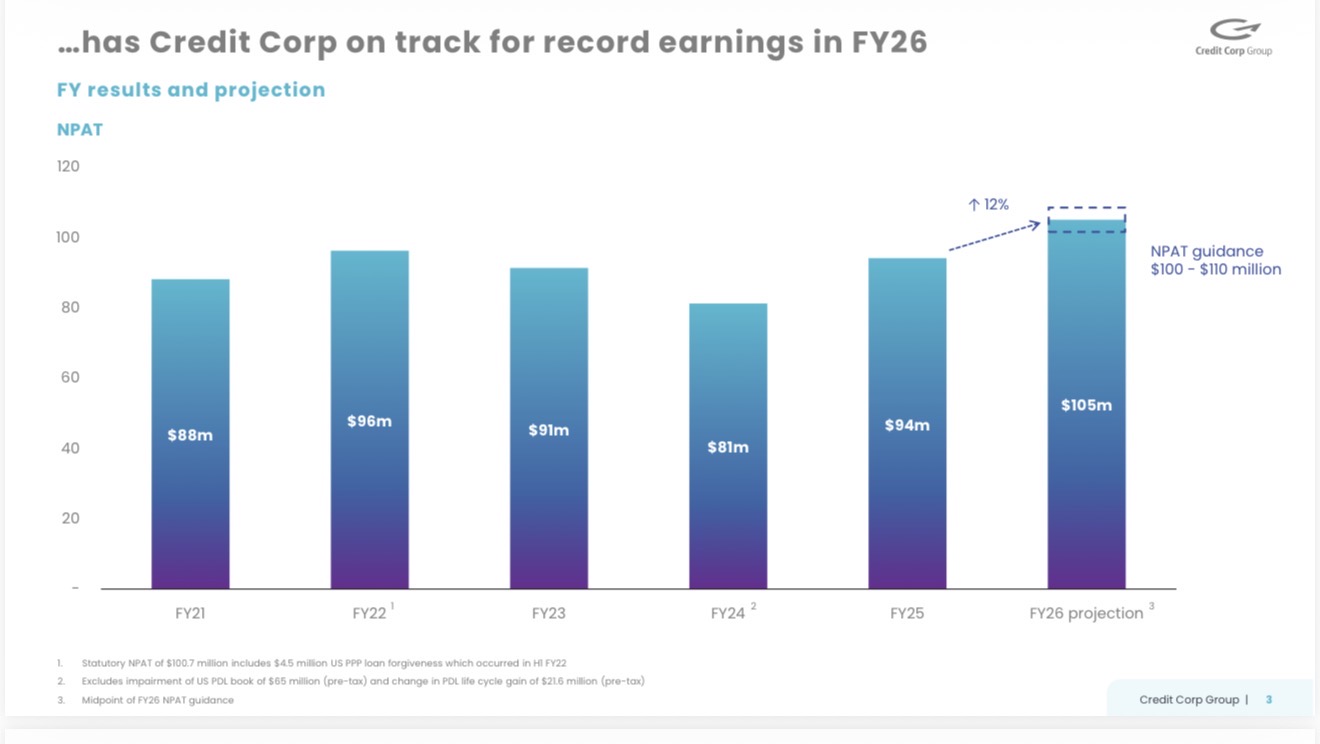

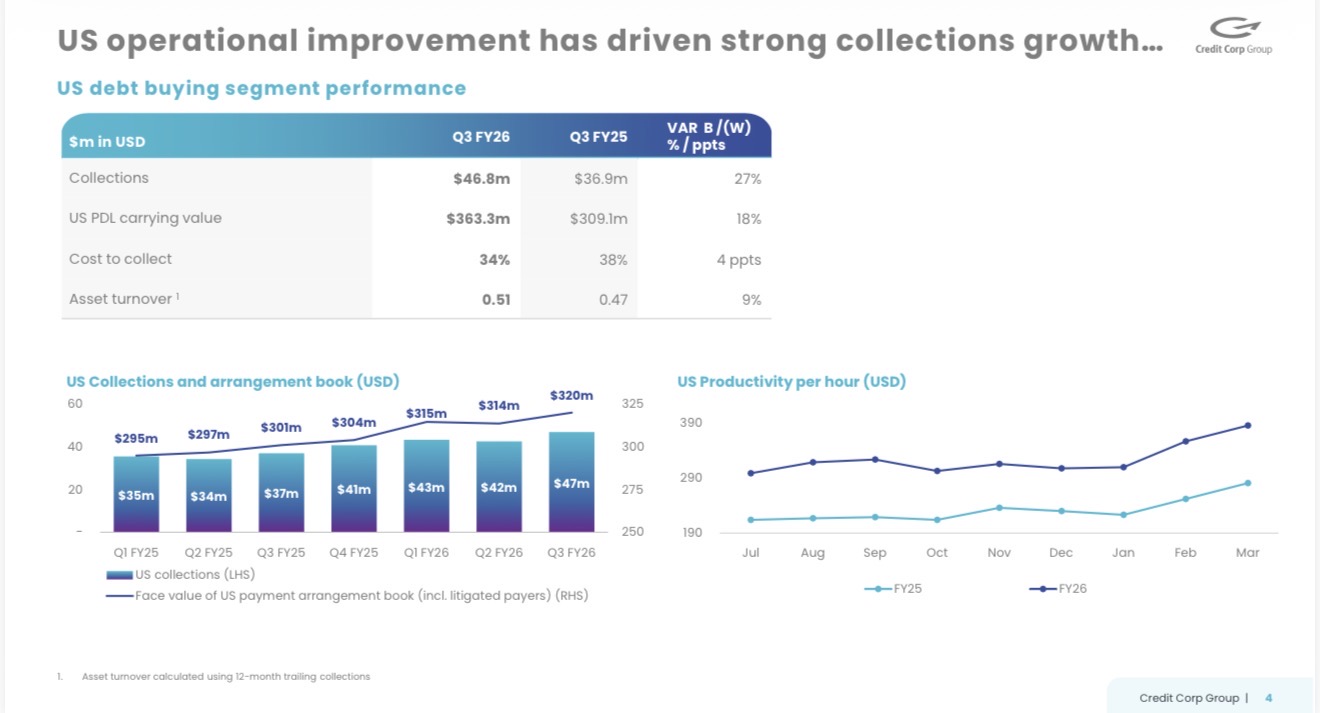

A positive update from Credit Corp today. Management have confirmed FY26 NPAT guidance, US debt buying collections up 27% in Q3 FY26 on pcp, and the cost of debt collections down 4 percentage points to 34%. Consumer lending book up 15% on FY25.

I think it’s good timing for Credit Corp as interest rates rise and things start to get a little tougher.

I think Credit Corp is mispriced as it enters a sweet spot…but I could be wrong!

I have Credit Corp returning 16% per year to investors based on McNiven's Valuation formula (growth + dividends’+ franking credits).

I’m looking forward to the nice dividend this year, likely to be over 7% fully franked (10% gross yield).

Held IRL (4%)

Credit Corp has been sold off following the 1H 2026 results announced on 3/02/26. Profits came in 10% below expectations. Revenue was up 4% on pcp, but NPAT, EPS and the dividend were flat on 1H2025.

There were a few encouraging signs, including:

- US collections +23% versus prior corresponding period (pcp)

- Record lending volume and +7% loan book growth over the half year

- Strong growth in the AU/NZ debt ledger investment pipeline to $120 million

Net Profit after Tax (NPAT) of $44.1 million was in line with the prior year. This reflected reduced earnings in H1 arising from strong loan book growth and disruptions to AU/NZ purchased debt ledger (PDL) purchasing only remedied late in the first half.

Guidance

Both these factors will produce higher H2 earnings, and the Company reaffirms its full year NPAT growth of 6 to 17%, in accordance with previous guidance.

Credit Corp has two main growth engines:

- Debt buying & collections (core driver of value)

- Consumer lending (Wallet Wizard etc.)

Performance depends on three variables

- Supply of bad debts (to buy cheaply)

- Pricing of those debts

- Ability of customers to repay (collections)

In the US consumer stress is rising, credit card delinquencies are increasing and Subprime auto loan stress is increasing. The labour market has also softened. If this trend continues Credit Corp’s outlook will improve further.

Strong Dividends

Credit Corp declared a 32 cps fully franked dividend (goes ex-div on 17/03/26). I am expecting total FY26 dividends of 68 cps fully franked, the same as FY25. That’s a gross yield of 8% including the franking credits. Over the coming 13 months I am expecting 3 dividends totalling $1.00 per share fully franked. That’s a grossed up yield of 12.3% including the franking credits. The dividend should be sustainable with a 50% earnings payout ratio.

Valuation

Credit Corp is currently trading at 7.7 times FY26 EPS guidance ($1.54 mid-range), and 7 times FY27 earnings consensus (EPS $1.66 per share). Over the last 5 years PE has ranged from 9 to 22 times.

If Credit Corp achieves FY26 EPS guidance of $1.54 per share (mid-range), and the outlook continues to improve, the shares could realistically rerate to a 10 times multiple, or $15 per share.

Using McNiven’s Valuation formula assuming current equity of $13.13 per share, ROE of 11.7% (based on FY26 EPS guidance of $1.54 per share), 50% of earnings reinvested, and a required ROI of 12%, I get a valuation of $15.33 per share.

Rounding off to a current valuation of $15 per share.

Broker Price Targets

Morgans analysts have retained a buy rating on Credit Corp with a reduced price target of $19.35. This follows the release of Credit Corp's first-half results, which revealed profits that were 10% short of expectations. While disappointing, Morgans feels the selloff that followed, which dragged its shares 17% lower, was overdone and has created a buying opportunity for investors. The broker highlights that at just 7x estimated FY 2027 earnings, Credit Corp's valuation is undemanding. This is especially the case given that management has reiterated its guidance for FY 2026. https://www.fool.com.au/2026/02/08/top-brokers-name-3-asx-shares-to-buy-next-week-8-february-2026/

The consensus price target from 6 analysts on Simply Wall Street is $18 per share.

Held IRL (2%) and SM. Accumulating on weakness.

Another year on from the Including staff acquired as part of the acquisition of Collection House during H1 FY23

Noted: Net Profit Margin 1 Year is down from: 19% to 9.37%

But

ROE: is rising

CCP share price and company information for ASX:CCP

About CCP

The Company operates within the Australian debt collection and consumer lending industry.

Events

Directors / Senior management

- Mr Eric Dodd

- Chair, Non Exec. Director

- Mr Thomas Beregi

- Managing Director, CEO

- Mr Phillip Aris

- Non Exec. Director

- Mr Bradley John Cooper

- Non Exec. Director

- Ms Lyn McGrath

- Non Exec. Director

- Mr James Morrison Millar

- Non Exec. Director

- Ms Trudy Vonhoff

- Non Exec. Director

- Mr Matthew Angell

- Chief Op. Officer

- Mr Michael Eadie

- CFO

Secretaries

- Mr Michael Eadie

- Company Secretary

- Mr Thomas Beregi

- Company Secretary

CCP head office

Head office contact information

address

Level 15, 201 Kent Street, SYDNEY, NSW, AUSTRALIA, 2000

Telephone(02) 8651 5000

Fax1300 483 012

Web site

Share registry

Share registry contact information

share registry name

BOARDROOM PTY LIMITED

address

LEVEL 8, 210 GEORGE STREET, SYDNEY, NSW, AUSTRALIA, 2000

Telephone(02) 9290 9600

Sold my holdings on the day of the results. Like @lankypom, I’ve held for an extended period of time since Nov 2010. I also held it in a previous stint from Sep 2004 to Nov 2007.

Consumer Lending did a lot of heavily lifting in the result. The EBITDA return on the carry value of the three main segments - Consumer lending, ANZ PDLs, and US PDLs were 33%, 15.7% and 8.8%. Who would have thought 10 years ago that Consumer Lending would be the division that would be wildly more profitable than the core PDL businesses.

My main concern is the ballooning carry value of the PDL assets on the balance sheet.

Collections have been declining in the past 3 halves, yet the PDL carry value has been increasing. If one thinks that an asset is increasing in value, should it be yielding less? This doesn’t make a whole lot of sense, and shows that management have had a shift away from their ultra conservative accounting practices.

The ANZ PDL business is currently in run off as its not able to get the supply necessary to grow collections. The business collected $141m in 2H. Just for comparison, this is very similar to the collection level the group had in FY15 which was $288m for the full year. To highlight the shift in the company’s conservativeness, the carry values for FY15 vs Today is $164m vs $297m.

I’m harping on about PDL carry values because the amortisation of it affects every number from the revenue down. Revenue is in fact Collections minus PDL amortisation. And the shift to a less conservative stance has benefited the bottom line over the past couple of years.

In absolute terms, Credit Corp’s PDL carry value is still conservative vs its competitors. But that’s not saying much in an industry littered with blowups.

The US PDL carry value is the one I’m most concerned about. They’re carrying A$465m on the books, and collecting about $200m a year. Having seen repayment plan delinquencies creep up in Q4, collections have started to flatten after heavy investments PDL and big headcount increases. The carry value seems bloated and the Amortisation vs Carry Value ratio for the US business is at PNC’s levels of 0.21, having consistently trended down over the past few years.

I’m concerned about write downs. If not write downs, then the headwind the relaxation of the amortisation policy will have on the profits in future years.

NPAT fell by 5 per cent over the prior year to $91.3 million. While lending segment earnings grew strongly, the impact was offset by continued run-off in the core AU/NZ debt buying business and costs arising from increased US resourcing.

Conclusion:

FY23 earnings were 5% lower on FY22, as rising wage costs and lower labour productivity more than offset a 15% growth in revenue. Nonetheless, the results were in line with consensus expectations. However, management's FY24 earnings guidance is ~10% below consensus expectation.

Share price reaction down ~ 11% ...Good for ones looking to purchase some more.

Reducing Exposure: Voting power back to 7.60%

6 signs you should sell | Wilson Asset Management

- Large investors exit

A shareholder owning more than 5% of a company must notify the market if they cease being a substantial shareholder.* We closely watch substantial shareholder notices announced on the ASX to identify if large investors are entering or exiting a company. When one of these large investors announces it is no longer a substantial shareholder, it may indicate they are planning to completely exit their holding. As large positions can take many weeks (or even months) to unwind, this may put downward pressure on the company’s share price in the short-term.

While we can only make inferences from substantial shareholder announcements, they can provide valuable insights which may feed into our investment decisions. Investors should note that when large shareholders announce they are no longer a substantial shareholder, they may only be temporarily exiting, or modestly reducing, their holding in the company.

For example, fund managers of open-ended investment vehicles may be forced to sell some of their shares in order to fund redemptions.

Credit Corp (CCP) released their first half results for FY23 this morning. From their release:

CCP attributed the decrease in NPAT (compared to CCP) to:

- up-front loss provisioning and marketing expense from rapid loan book growth;

- costs arising from increased US resourcing; and

- run-off in the core AU/NZ debt buying segment.

I think overall it was a poor half on the surface for CCP but this could be laying the foundation for future growth especially in the US. Just on the lending side, they are expecting 2HFY23 NPAT to be $25-30m (up from $4.3m in 1HFY23).

Guidance remains unchanged:

Will continue to hold but will need to see their investments pay off especially in the second half of this year.

Full presentation here

Disc: Held IRL. Not held on Strawman.

As previously advised, the DOCA includes the transfer of all shares of CLH to Credit Corp (or its nominee), subject to the Deed Administrators obtaining an order from the Court pursuant to section 444GA of the Corporations Act 2001 (Cth) (“444GA Order

Credit Corp Group (CCP) today announced its FY22 results. From their release:

- 9% increase in net profit after tax (NPAT) to $96.2 million

- Record annual investment:

- US purchased debt ledger (PDL) outlay 80% above previous peak (FY2020)

- Gross lending volume 24% above prior record (FY2019)

- 16% increase in US segment NPAT

- Recovery in lending segment earnings and loan book

Management also provided guidance for FY23:

Overall a fairly good result for CCP. I see this business as counter-cyclical given their business of debt collections. Management did flag that overall AU/NZ debt purchasing has not recovered to pre-covid levels and thus most of the growth in the business has been through the increase in US debt purchasing. This has also run into issues in regards to staffing in a tight labour market although management have made the move to use offshore (Philippines) staff to make up the numbers.

Free cash flow was negative as a result of acquisitions (Radio Rentals in particular) although management do expect FCF next year to exceed $100m providing them with sufficient cash for potential acquisitions.

Outlook implies not a lot of growth for the coming year although I feel management are always quite conservative in their guidance.

Disc: Held IRL, not held on Strawman.