Consensus community valuation

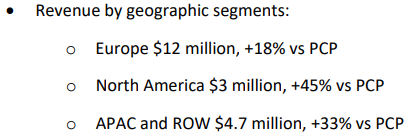

CSX has continued it's strong revenue growth, maintaining the 26% revenue growth from the 1H into the 2H and FY. Growth was strong across all regions:

Off a low base, but 45% in the US is very strong, particularly against the weaker USD this year.

No comment on margins unfortunately, but if they have remained steady I think CSX will achieve it's goal of being EBITDA positive this year.

NB: thank you to @Wini for his work which informed and inspired my interest and analysis.

CSX requires sales growth of 20-30% to pivot into profitability in the next year or two and should see profit grow at around twice (in dollar terms) that of sales if it can maintain this growth rate. This is in contrast with the last 3 years where profitability has improved faster than sales due to significant cost reductions from restructuring the business, which is now mostly complete, hence no longer going to occur.

Take the below projection, assuming 30% sales growth, but expenses also start increasing at 6% in FY25 then by half sales growth and compare to an extrapolation of the FY22-FY25 projection of profit:

With around $7m in net cash and FCF break even due to low capital cost requirements, the business shouldn’t need to raise further capital and may be in a position to pay a dividend in a few years provide growth targets are achieved. Trading at 2x Sales with possible 20%+ net profit margins at scale, the current price is reasonable/cheap, but conditional on aggressive growth assumptions and upside will take several years to translate into PE rations the market will see as appealing and be willing to pay.

Instability of performance over it’s listed history and lack of tangible metrics to value the company as it pivots into profitability provides opportunities for investing at low valuations, but also likely to provide high volatility in price movements over the coming year as sentiment changes.

As such I am open to buying at below $0.40 but I am looking for additional support for the assumption that sales will grow at 30% or there abouts for the next 3-4 years. Good US market execution could do this as well as indication that growth in Europe is likely to continue despite conditions there.

So this is a thesis pending investment if the conditions look right at some time in the future.

Disc: I don’t own, but it’s high up on the watch list.

Slightly edited copy and paste from latest Mere monthly report: https://www.merewethercapital.com.au/wp-content/uploads/2024/12/MC-Nov-24-Report.pdf

CSX is a classic busted IPO, floating in late 2020 on the back of an explosion in revenue to healthcare customers who received Government funding as a response to the Covid pandemic. After doing $11.2m in revenue to industrial customers in 2019, large sales to healthcare customers saw revenue grow to $28.4m in 2020 and $49.9m in 2021.

Unfortunately, healthcare customers panic buying respirators with Government funding sent a false signal to CSX management, who pivoted their business model to try and grow further into hospitals. While the industrial business is entirely sold through distributors who provide sales, training and support to end customers, CSX in-housed these functions for healthcare customers which saw the cost base of the business grow from $8.2m in 2019 to a peak of $24.9m in 2022.

A ballooning cost base combined with collapsing revenues from healthcare customers saw CSX swing from a $16m operating profit in 2021 to a $15.1m operating loss in 2022. The market reaction was savage, with the share price falling from highs above $7 to a low of 20c.

However, of course digging deeper shows a different story. Splitting out segment revenue shows an industrial segment growing at ~37% per year over the last two years while healthcare has fallen to essentially zero:

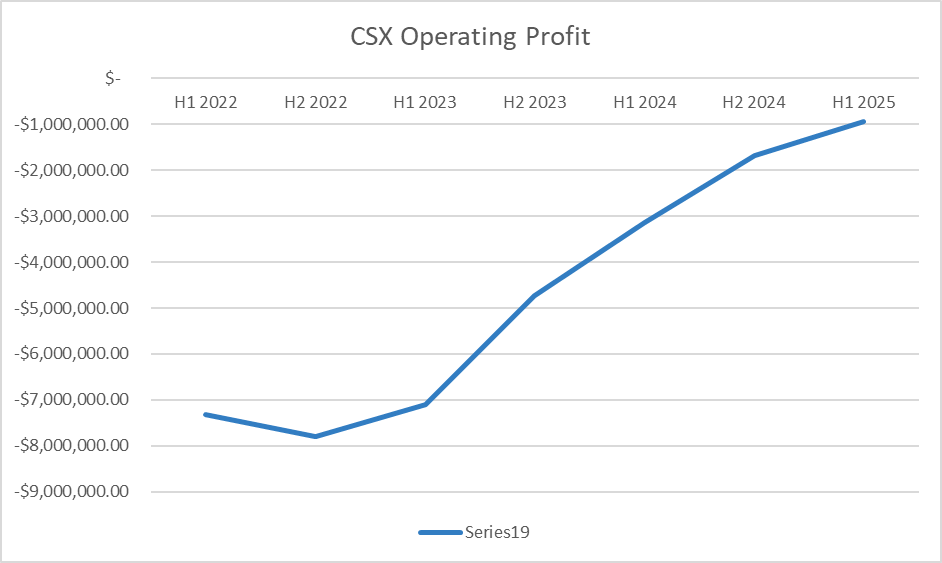

With the business shifting back to its previous operating model of selling industrial units through distributors, the excess cost base has also been removed with the business rapidly moving back towards profitability:

The market is often very poor at recognising business models that will exhibit exceptionally strong operating leverage as they scale. However, once the leverage shows up in the reported numbers, the market tends to get quite excited!

CSX has a business model that inherently has very strong operating leverage. It begins with 70-75% gross margins, world class levels for a manufacturer driven by CSX selling their PAPR’s with high-margin recurring consumables (masks and filters).

As already detailed, the use of distributors around the globe to reach industrial end customers greatly reduces the sales and support footprint required. As an example, speaking recently with the CEO he outlined how the US sales team was being restructured with the previous healthcare focused team let go with the current plan to have four industrial focused sales representatives for the entire country.

The manufacturing itself is also very capital light, with less than $1m in plant and equipment on the balance sheet as manufacturing is simple manual assembly.

Interestingly, the volatile history of CSX means we don’t have to guess what we think operating leverage may look like in the future, because the spike of Covid healthcare sales gave us a very brief glimpse of the business’s economics at scale. In the calendar year 2020, CSX did $60.8m revenue which resulted in $26m operating profit. Again, the potential for 40% operating profit margins is world class for a manufacturer.

So, all of that is to say I am confident that if CSX continues to grow it will soon become profitable and beyond that become exceptionally profitable. The key question is how confident can we be of future growth?

Answering that question begins with the product itself and how it compares to peers in the industrial PAPR segment.

CSX was founded by Dan Kao in 2009 after spending the previous 8 years at Resmed as a Senior Design Engineer. Dan saw the potential to take Resmed’s sleep apnoea respirator technology and apply it to the industrial market.

Generally speaking, competitors in the industrial PAPR segment are quite low tech, using fans to blow a constant stream of air through a tube connected to a face mask. With a constant stream, those PAPR machines will filter roughly 180L of air per minute, however by using a patented technology CSX products sense the changes in air pressure as a user breathes and only blows in filtered air as they inhale.

With that technology, CSX respirators process less than 50L of air per minute (assuming the user is breathing normally) meaning they can drastically reduce the footprint of the respirator unit. All other competitors use a backpack or belt mounted system to carry a unit that weighs 3-4kgs, but with a smaller battery and fans CSX respirators weigh less than 500gms and can rest on the back of the neck making mobility for users much easier:

Cleanspace Ultra compared to 3M Versaflo

Together with Bluetooth reporting technology to both end users and an enterprise level for work health and safety auditing, CSX has a best-in-class product that is priced roughly 10-20% cheaper than peers. While a product edge is no guarantee of success against large incumbent competitors, it provides the opportunity for CSX to continue to grow their business into the future.

However, it won’t be smooth sailing. The drawback to the low operating cost model of selling through distributors is CSX will be a victim to the re-stocking/de-stocking of inventory through its customers supply chains. Both end customers and distributors tend to order CSX’s products in bulk meaning period to period they can be victim to lumpy sales depending on ordering patterns.

Which brings us to the recent purchase of our position following a nearly 30% fall in the share price following a weaker than expected trading update at the AGM.

At their AGM during the month, CSX management updated the market disclosing that sales through the first four months of the financial year were flat on last year, below the 30% growth target they had previously set.

A few reasons were provided such as a disruption from the Olympics in their largest market of France and the transition to the new industrial focused sales team in the US slowing sales to new customers. However, I suspect the largest impact was the simple lumpiness that exists in the business that is exacerbated on the current low revenue base.

The start to this financial year was cycling a period of over 50% growth last year, benefiting from the roll-out of new products and partnerships with new distributors. While below budget/trend, management guided to 15% revenue growth for the first half of this financial year and maintained their 30% target for the full year. Speaking to the CEO after the AGM, they have seen normal ordering patterns returning from distributors and seeing very good signs from early US sales discussions.

At the current share price of 35c, CSX is capitalised at roughly $28m with a clean balance sheet with no corporate debt and $8.5m in cash. Management have guided to being at least EBITDA and cashflow breakeven for this financial year despite the weaker than expected first quarter.

However, given the operating leverage inherent to the business model, it is the 2026 financial year I expect to be the breakout. On the 2024 financial results call management stated that the cost base is now largely right sized, and moving forward they expect that to achieve their targeted 30% growth it may require costs increasing 5-10%.

Even taking a conservative view of 20% revenue growth and 10% cost growth, I expect the business can do $2m EBITDA which would look very reasonable against the current market capitalisation. However, like any business around the profitability inflection point, it is the incremental dollars hitting the bottom line that matter and in CSX’s case it should be quite exceptional.

Nonetheless, it is a new position in the Fund and not without risks so for now it is a medium weight in the portfolio. As I’ve said before, it usually takes the market a while to wake up to businesses inflecting strongly into profitability, so I suspect we will get a chance to add to our position if the thesis is playing out.