Consensus community valuation

Discl: Held IRL 4.12% and in SM

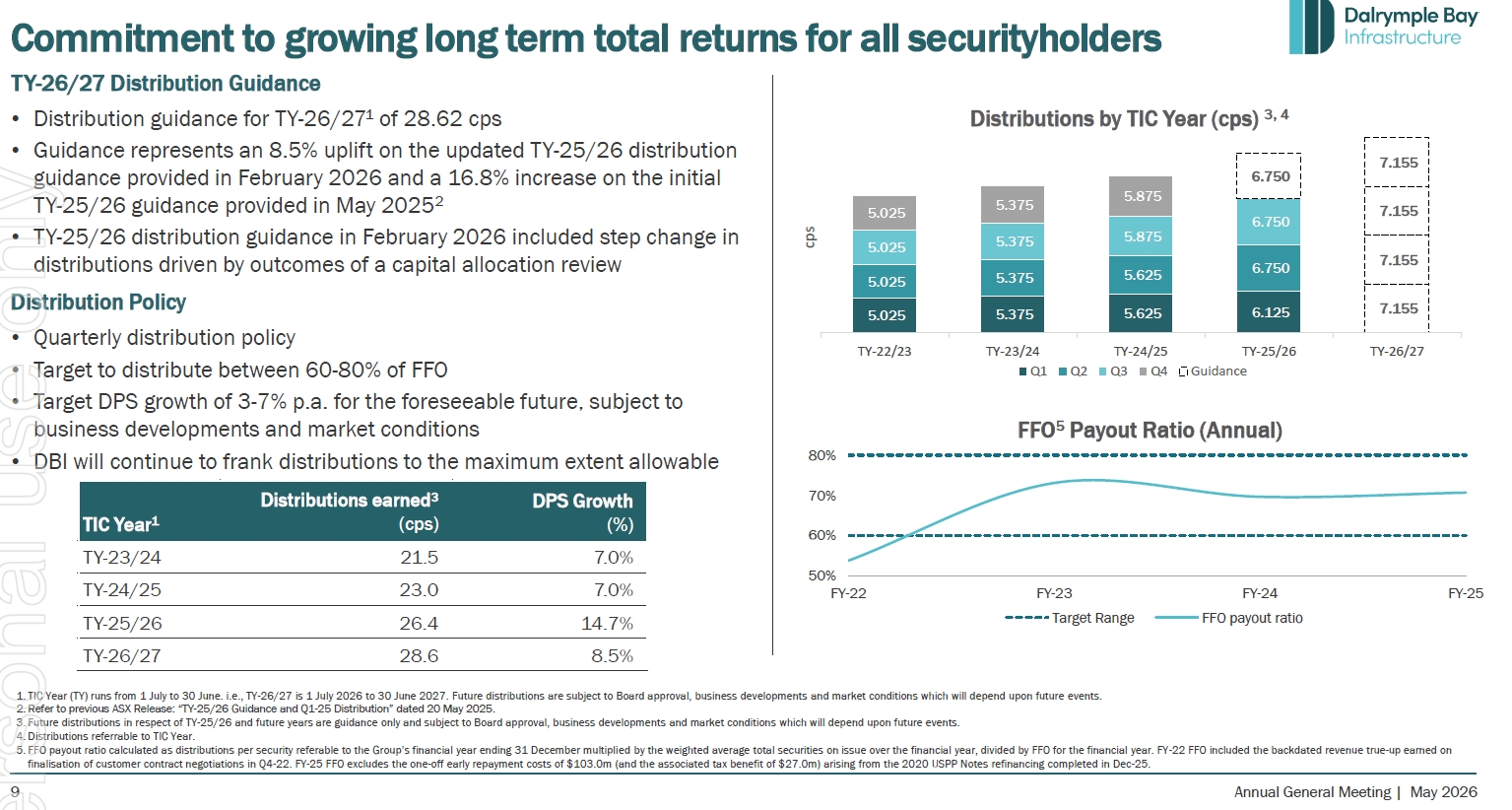

DBI announced its TIC Year Forecast Terminal Infrastructure Charge (TIC) for TIC Year 26/27 and Distribution Guidance for TY26/27, together with its FY25 AGM material.

DBI also announced the TY-26/27 Distribution Guidance of 28.62 cents per stapled security, up 8.5% YoY.

Chart Review

Nice breakout is occurring this morning - the price is now blasting past the previous all-time-high of $5.58.

From the last up move which started on 12 Mar 2026, the price retraced nicely a tad past 38.2%, at prior congestion levels ~$5.17, before taking off again - textbook price movement really.

We have higher lows and now, a higher high, so the bullish trend is very much intact.

This is very much supported by the increased TIC, which translates directly to increased revenue, and by the increased TY 26/27 Distribution, both which keeps shareholders like me very happy indeed!

@Saiton, a good one to add to your watch list from a pattern and fundamentals perspective!

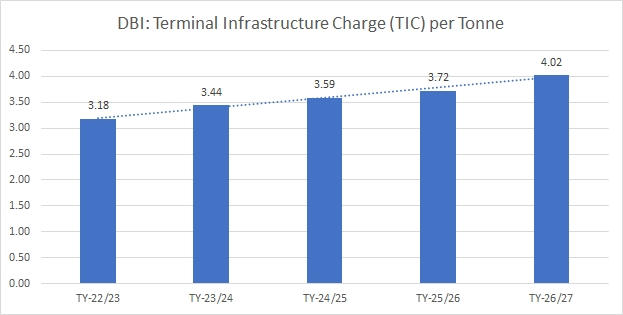

TERMINAL INFRASTRUCTURE CHARGE

The annual TIC Charge growth chart is a nice one as (1) it is indexed to the CPI and (2) the Non-expansion Capital Expenditure (NECAP).

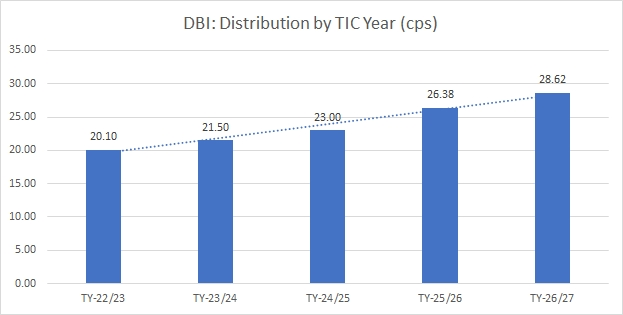

DISTRIBUTIONS

And so is the Distributions chart which runs by TIC year - this continues to grow steadily, supporting the very nice price growth in DBI.

Discl: Held IRL 3.67% and in SM

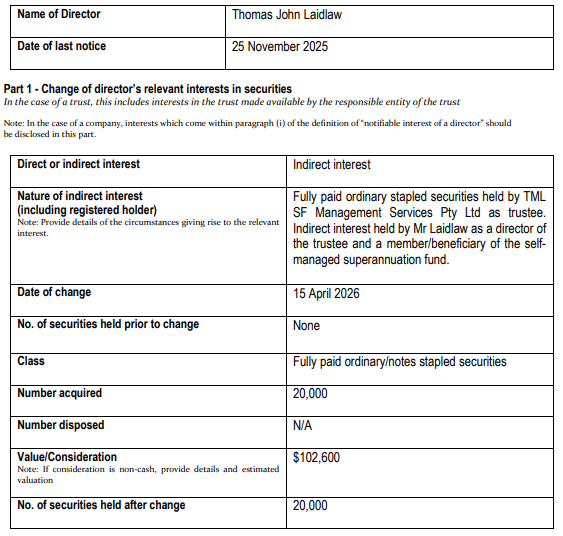

Good to see DBI’s newly appointed Non-Exec Director, John Laidlaw, buy 20,000 shares of DBI, on market, investing $102.6k of presumably his own coin.

John was appointed on 25 Nov 2025 and looks highly credentialled

The share price has continued to run up beautifully, behaving like the highly defensive growth stock that it is!

Discl: Held 2.56% and in SM

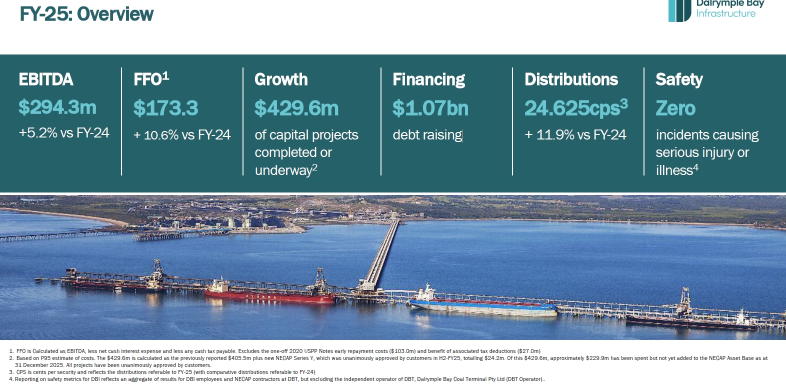

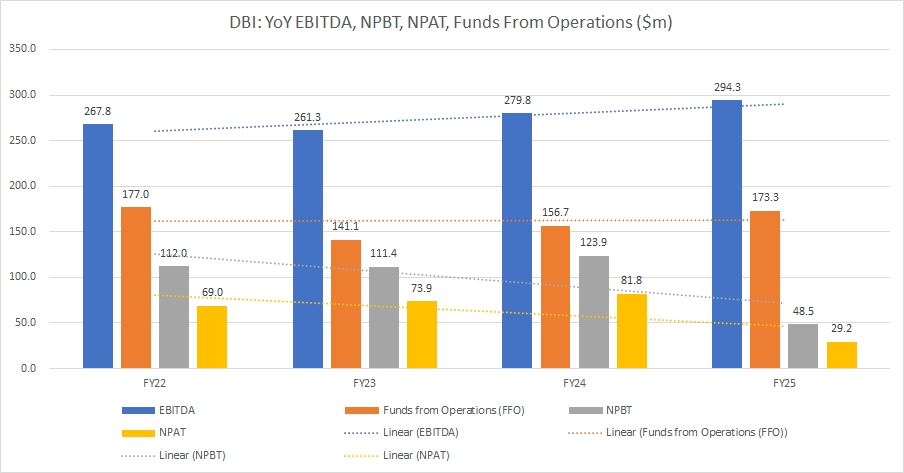

Struggled a bit to summarise the key points of the very good DBI FY25 result, this being my first half year since opening a position on DBI towards the back of CY25. I think this is because there really is no “operations” to focus on, such is the nature of DBI, so the usual things to look out for/graph are not quite relevant to DBI.

DBI made another all-time high yesterday, but fell back to more realistic levels today. This is one hell of a chart - nothing defensive about it at all!

I topped up a bit today and will top up further around ~$4.90 and ~$4.73. Given how DBI is uniquely structured, this is one company where I don't think too hard about averaging up ...

SUMMARY

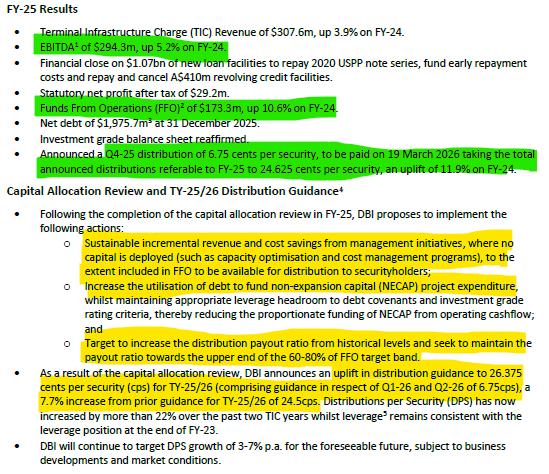

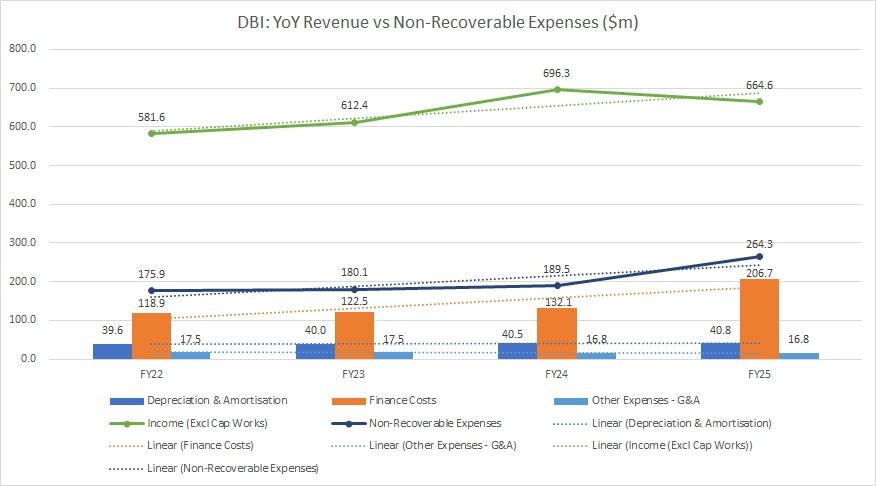

G&A costs flat YoY, expected to remain flat in FY2026

Net Finance costs spiked up $89.6m due to the early repayment costs associated with the repayment of the 2020 USPP notes - this would otherwise have been flat YoY

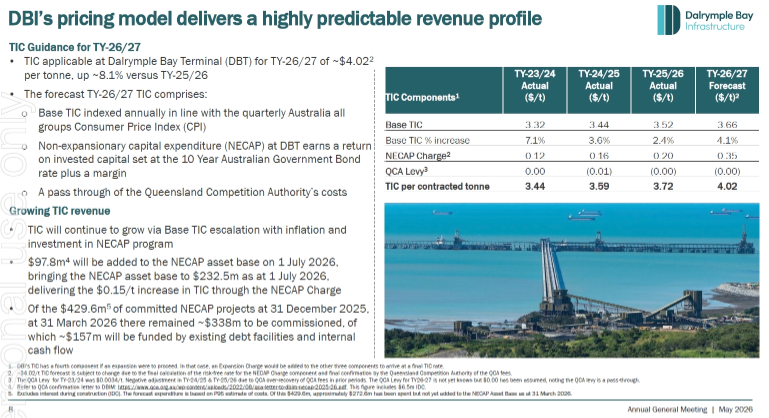

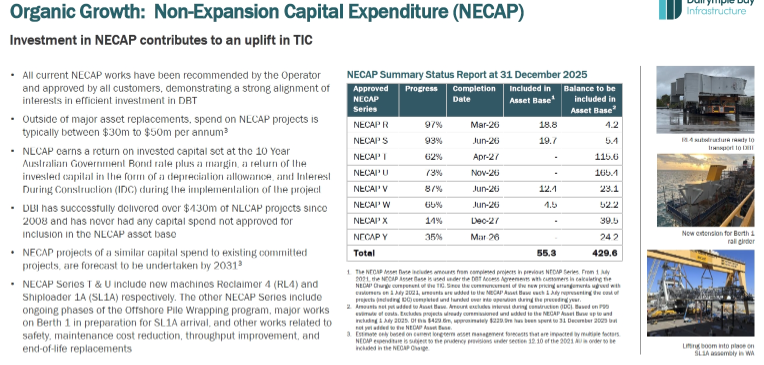

NECAP

- NECAP in the last 12 months is added to the asset base for the calculation of TIC on 1 July each year, so this is a source of future organic revenue growth of the TIC revenue

- NECAP will be debt funded from hereon, not from operating cash per previously

- Same amount of committed capital for NECAP projects in the next 5 years

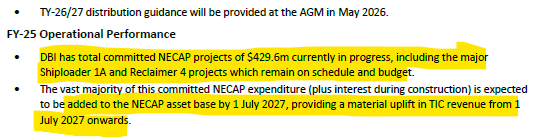

- Expect NECAP to be slightly more than $55.3m by 1 July 2026 - expecting $60-70m of commissioned projects, excl interest cost, ~$340m likely to be added to the Asset Base on 1 July 2027

- NECAP Projects - SL1A - on track and on budget

OTHER NOTES

- No FX risk for interest or principal repayments

- Ave 6.5% interest rate from mid-2026 onwards is lower than the 8.0% interest rate guidance at HY2025

- 83% of drawn debt is fixed, 17% floating

20-Nov-2025: https://investors.dbinfrastructure.com.au/DownloadFile.axd?file=/Report/ComNews/20251120/03025613.pdf

That link above may download a .PDF file to your device rather than open the file in your browser, but if you have any issues with that link, you can use the one below and click on "ASX Announcements" and then "Investor Presentation - Dalrymple Bay Terminal Site Visit"

Source: https://investors.dbinfrastructure.com.au/investor-centre/

Nine Sample Slides:

I hold DBI in my SMSF and I topped up the position today. I originally added DBI to my Super after watching the second (and most recent) meeting here between Andrew and DBI's CEO Michael Riches.

On September 30th DBI announced that their Board had appointed Michael Riches as DBI's MD, in addition to his role as CEO, so his title is now ‘Managing Director and Chief Executive Officer’.

DBI has a compelling business case, even though they are not a growth story that is going to shoot the lights out. With their quarterly partially franked dividends DBI is a dependable income provider with some growth as well, that is a solid inclusion for an income portfolio or just as a place to park cash while waiting for better opportunity to deploy that cash, IMO.

I have trimmed some of my gold producer positions today (NST, CMM, EVN) and fully exited CSC (Capstone Copper) and have re-initiated positions in ARB and TNE - both of whom have fallen enough recently to provide some double digit percentage gains if they trade back up to where they were trading just 5 to 6 weeks ago. I don't believe they are worth less today than they were 5 to 6 weeks ago, and while I do understand that they both had quality / management premiums in their share prices then, so would have looked expensive to many, I believe those premiums were well-deserved.

I view TNE and ARB as two of the highest quality companies on the ASX, and ARB in particular as having one of the best management teams, and I'm always happy to add them back into my SMSF when they have share price falls like they have had in recent weeks. Both are up today, so I'm hoping the selling is over with both of them, but even if it's not, happy with these prices I paid today. I looked at MAQ as well, but the near-to-mid-term upside looks greater with ARB and TNE.

DBI is not in the same league as ARB and TNE (or MAQ), not by a long shot, but DBI do provide me with some diversification which I reckon I need when my SMSF is so heavily weighted to gold companies.

DBI is a solid defensive position in my view, as evidenced by the fact that their SP either didn't drop at all, or dropped less when it did drop, during the market's recent "down" days. DBI is actually a very well structured infrastructure play with very little downside over the next few years because of their structure and the fact that they are fully contracted via take or pay contracts and they have a waiting list for any spare capacity they may have in the future, so I rate them as a great place to park cash.

Discl: Held IRL and Pending in SM

Following the very good SM meeting with the DBI CEO Michael Riches and my notes last night, I opened a 0.65% position on DBI this morning at $4.34. my immediate buy level. Have also opened a position on SM which is pending.

This was another holding where I gained strong conviction as soon as I wrapped up listening to the SM meeting, and decisively pulled the trigger early this morning. The following is my thesis.

CURRENT PORTFOLIO CONTEXT

- 18 companies + 2 ETF’s vs portfolio limit of 20 companies + 2 ETF’s

- Significantly fast growth, technology skewed

- Dividends is not a current explicit focus or investment objective, although 6 of 18 companies plus both ETF’s are active dividend/distribution payers - 40% of the portfolio companies are dividend/distribution. This is not expected to change despite not being too far from entering SMSF pension phase

- Hold no commodity miners, only critical/essential pick and shovel services to the mining industry

DBI INVESTMENT THESIS

- Very significant and tight investment moat in the Dalrymple Bay Terminal (DBT) as it relates to the Bowen Basin met coal miners - the alternative ports of Gladstone and Port of Abbot Point are much further and add significant cost

- The miners have direct skin in the game in the running and financials of the DBT, and are locked in as customers for a very long time given mine life spans, further entrenching the moat

- High revenue and cost certainty - pricing, capacity, cost pass thru’s are all locked in through to 2031, any risk of non-recontracting of capacity is mitigated by the cost being spread to remaining contracted customers - this is ALMOST risk-free, given how the arrangements are contracted

- High dividend yield certainty and growth - fixed deposit-like as capex requirements are well understood, well managed, cost is hedged, all capex is essentially cost recovered from customers. There is very little to no-risk that there will be sufficient funds to sustain the growing dividends in the foreseeable future. Dividends are likely to grow every 1-2 years given historical trajectory - nothing to suggest this trajectory will remain as the base case, with all the upside of higher dividends as revenue improves

- Good upside opportunities in the share price from any small incremental improvements that are made to the facilities when they directly impact revenue as any capex improvements come with virtually no cost uplift to DBI given the cost recovery arrangements. The revenue profile will also likely see a step up once the 8x Project is delivered to add further capacity to the Port. This is reflected in the long term up trend of the share price.

- Good and likely to be strong price downside support as falls in the share price increases the dividend yield, assuming no change in the business fundamentals

- Risks of global decarbonisation are noted, but this still feels like a long way away - mitigated by the increased demand expected from newer steel making countries India, Vietnam etc.

DBI is thus a truly investment-grade, high certainty holding, that will add significant ballast and good diversification to the current high fast-growth Technology centric portfolio skew.

POSITION SIZE

Expect to build this out to a 2.0 to 2.5% holding over time.

APPROACH TO BUILDING POSITION

Because of the yield implications, the DBI position needs to be built more carefully than previous holdings - over paying will reduce the dividend yield and thus, the attractiveness of the DBI investment.

- Opened a 0.65% in DBI today at $4.34 as the price briefly fell to this level, which locks in a 5.64% yield on FY26 distributions - this is a higher than my usual opening position size

- Next attractive top up levels will be ~$4.21 (5.82% Yield), then $3.99 (6.14% Yield)

- Will need to be decisive in topping up if price falls below $4.34 on no negative change to the business fundamentals

The recording for today's chat is now live on the Meetings page and you can interrogate the transcript here:

DBI Transcript October 2025.pdf

As mentioned, DBI strikes me as a low risk affair -- Provided, that is, they retain balance sheet and CAPEX discipline.

Here's a condensed summary of the risks from AI, which I asked to review the transcript:

Coal is undoubtedly a sunset industry, but it’s a very long sunset. The transition will take decades to play out, and metallurgical coal is likely to be the last segment to decline. Electric arc furnaces are part of that shift, but smelters typically don’t upgrade until their existing blast furnaces reach the end of their useful lives (often 30-40 years). In the meantime, countries like India are expected to prioritise the lower-cost, traditional (and dirtier) blast furnace route to support their rapid steelmaking expansion.

A 5.6% yield, (roughly 60% franked), with the dividend expected to grow between 3-7%pa sums to a very tidy return (*if* that's what they are able to deliver). Plus, if you like your divvies, they pay distributions quarterly.