Price History

Premium Content

Premium Content

Premium Content

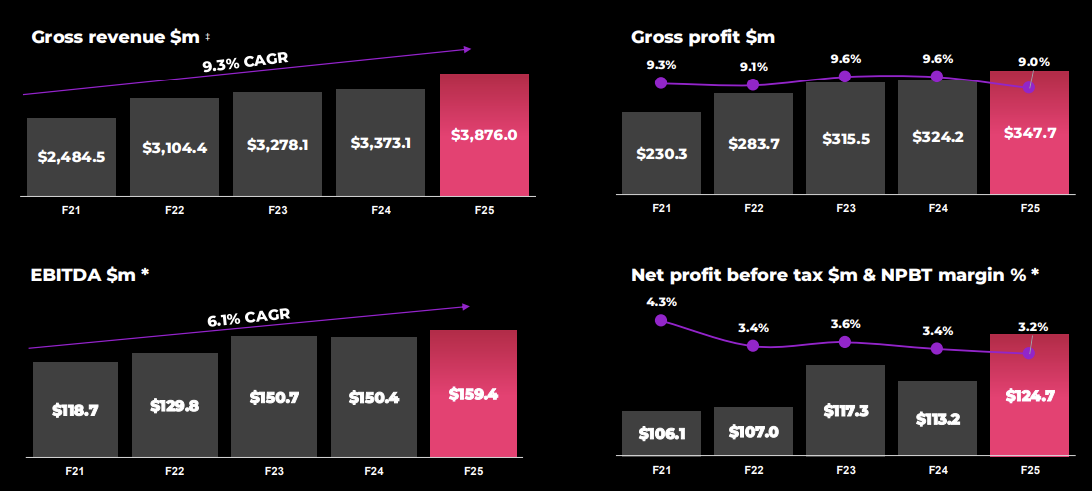

Dicker Data (DDR.ASX) reported their FY25 results this morning. From their presentation:

Overall a very good result for the year with record gross and statutory revenue, gross profit, NPBT and NPAT numbers. Margins were a little compressed due to a shift in customer mix with more higher volume, lower margin enterprise and AI infrastructure deals.

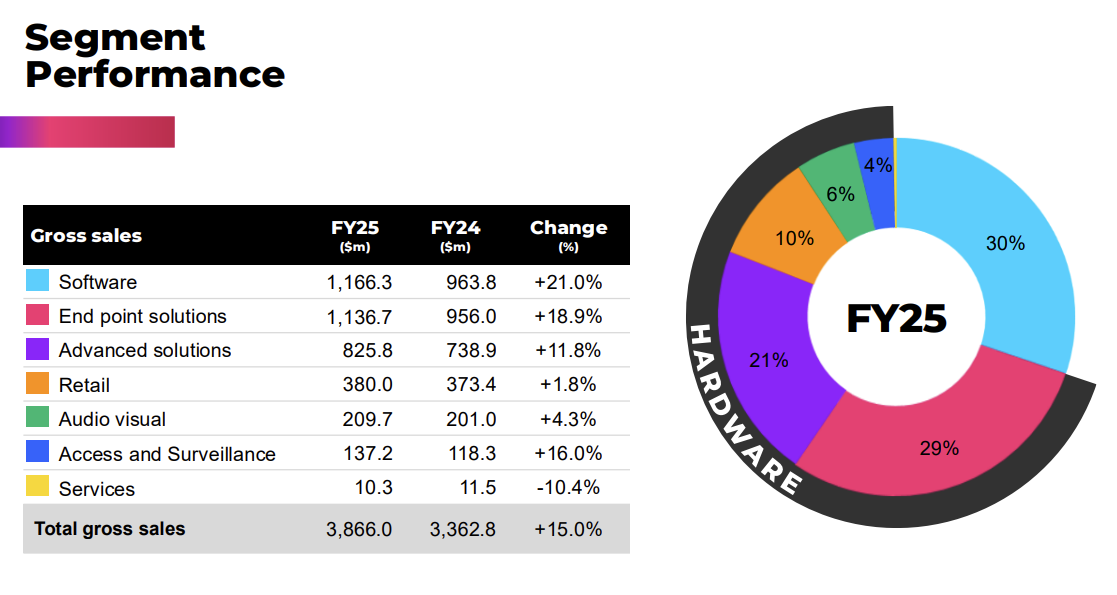

On a segment basis, software continues to be the main growth driver with $1.1b worth of sales being recurring. End point solutions also had a strong year due to the Windows 10 PC refresh cycle. COO Vlad Mitnovestski said that whilst FY25 was a big year for Enterprise customers, the SMB market was somewhat subdued. But he believes this will be a tailwind for FY26 as SMB will also need to upgrade their PCs from Windows 10.

Perhaps the most interesting part of the earnings calls was the change in Dividend Policy which used to be a payout of 100% of NPAT. This was most likely due to founder David Dicker not taking a salary and only being paid in Dividends. However with him now fully exited from the business, the Dividend Policy has now shifted to a payout of between 80% - 100% based on cash and capital requirements. Management expect to be able to use this extra cash to fund more internal investment as well as to pay down debt. In my opinion this is a good change as it allows the company to be more flexible with how it uses its cash.

Outlook for the business was strong with IT spending in Australia and NZ expected to grow in the high single digits / lower double digits. Vlad mentioned that a major part of spending growth will occur in the Data Centre space with them having to update their equipment. Vlad also talked about how at current they are holding onto more inventory as they believe some supply constraints especially in RAM is causing some pricing volatility and thus may actually increase the value of their inventory in the coming months.

Finally, the team mentioned about upcoming potential ASEAN expansion looking into Singapore and Philippines. At current there is no confirmed timeline but there are some internal targets for launch. Hopefully this can further grow the company although I am always weary of Australian companies trying to expand overseas (at least this is not to the US which seems to be a graveyard for Aus companies).

Disc: Held IRL and on Strawman.

Dicker Data released their FY23 results a few days ago. From their presentation:

I thought the result was pretty good considering FY22 was a disappointing year. Overall gross margins finished at 9.7% which is the highest in 5 years.

Revenue reporting will change from this report onwards due to a difference in revenue recognition. Above shows how revenue would have been reported in FY22 under the new reporting standard.

Overall a good result in a sector with some good tailwinds. The increase in computing needed to drive the AI sector will benefit DDR going forward. Also the windows refresh cycle will begin soon with Windows 10 losing support later this year.

Disc: Held IRL and on Strawman.

Dicker Data announced a final dividend for FY23 of 15c per share for the December quarter. Total dividends for FY23 came in at 45c per share.

Given that DDR have a 100% NPAT payout policy, we can assume that EPS will be around 45c per share or around $81m NPAT (compared to FY22 NPAT of $73.4m).

Disc: Held IRL and on Strawman.

Dicker Data released an update for their Q3 performance yesterday (Note they report on a calendar year basis).

I thought this was a pretty good result considering the issues they have been having in the past few years with supply chain and also the decreasing gross margin.

The newest segment DAS has been a good contributor to the growth in Revenue and Profit.

They mentioned that YTD gross margin has come in around 9.6% which is a good turnaround from it being sub 9% in FY22. This has been a result of increased gross margins in their NZ segment of the business.

The next few years will be interesting as they have mentioned that there will be a new refresh cycle for Microsoft devices with Microsoft stopping support for Windows 10 devices in October 2025. Management predict that there the current downturn in PC demand will bottom out in the current half and accelerate towards the end of next year.

Full Announcement Here

Disc: Held IRL and on Strawman.

Dicker Data released some unaudited results today:

Company said that the increase in revenue was partly due to an increased demand for networking and storage products, software and the new DAS business (access and surveillance) which offset a decrease in demand for personal computing devices. The decrease was attributed to an increase in hybrid working environments.

Pleasingly, gross margins improved back to above 9%, finishing at 9.4% which was up from 8.8% from pcp.

DDR also mentioned that there were signs that the supply chain was normalising which had impacted them with large amounts of backorders in previous periods having been completed this half.

Audited results will be out Aug 30.

Full announcement here

Disc: Held IRL and on Strawman.

Dicker Data released a market update this morning. From their release:

Overall a good improvement compared to info they released towards the end of last FY. Gross margins improving back to above 9% having dropped below for the previous few quarters.

Dividend is expected to be 10c per share (down from 13c PCP). Most likely the decrease is related to an increase in share count given they did a raise last year. Dividend policy unchanged at paying out 100% of NPAT.

Will maintain my valuation for now until we get some more information but seems like the business is stabilising after a disappointing FY22.

Full Announcement here

I do also note that CEO Vlad Mitnovetski purchased 20000 shares last week.

Disc: Held IRL and on Strawman

Dicker Data released their FY21 results today (they report on a yearly basis). From their release:

- Total revenue of $2.48b for the year, representing an increase of 24.2%, or $484.3m

- Australian revenue grew by $300.3m, representing an increase of 16.3%

- New Zealand revenue grew by $184.1m, representing an increase of 128.7%

- Nine new vendors were added in FY21 (excluding Exeed) which contributed an incremental $54.7m

- Software recurring revenues increased by 19.7% to $520m

- Statutory net profit before tax increased to $105.1m, representing an increase of 28.4%

- Earnings per share increased to 42.63 cents per share, an increase of 25.6%

Another solid year of business for a DDR. I think this slide in particular outlines what a high quality company this is:

At the current share price ($14.15) they are on a PE of around 33x. Historically shares have traded at a PE of between 10 and 20 however since 2020 there has been some multiple expansion and shares have traded between 20x and 40x.

I have updated my valuation based on their latest results. If the PE got down to 20x ($8.50) I would likely back up the truck.

Disc: Held IRL and on Strawman