Price History

Premium Content

Premium Content

Premium Content

by Jonathan Shapiro and Peter Ker, Updated Jun 2, 2026 – 2.46pm, first published at 9.00am

Elliott calls for gold giant Northern Star to put itself up for sale

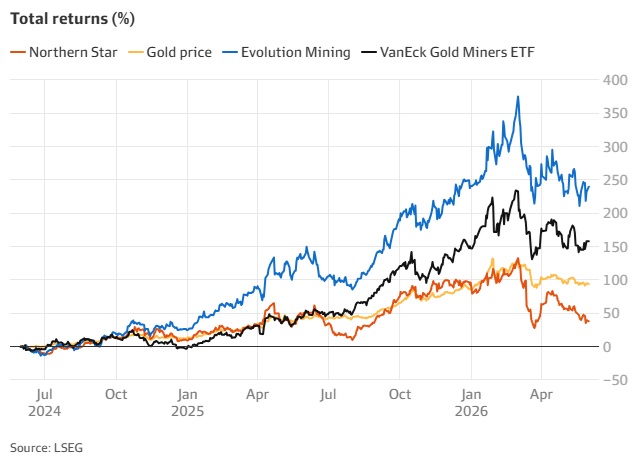

Elliott Management is calling for Northern Star to consider putting itself up for sale after accusing the ASX’s largest gold miner of being mismanaged after a series of downgrades sent the company’s share price sliding.

The Florida-based activist fund manages about $US80 billion ($112 billion) and confirmed it had amassed a position “well over $1 billion” in the company. The stake was first reported by The Australian Financial Review and triggered a 13.5 per cent surge in Northern Star shares on Tuesday.

Northern Star chairman Michael Chaney is facing calls from Elliott Management to consider a sale. Trevor Collens

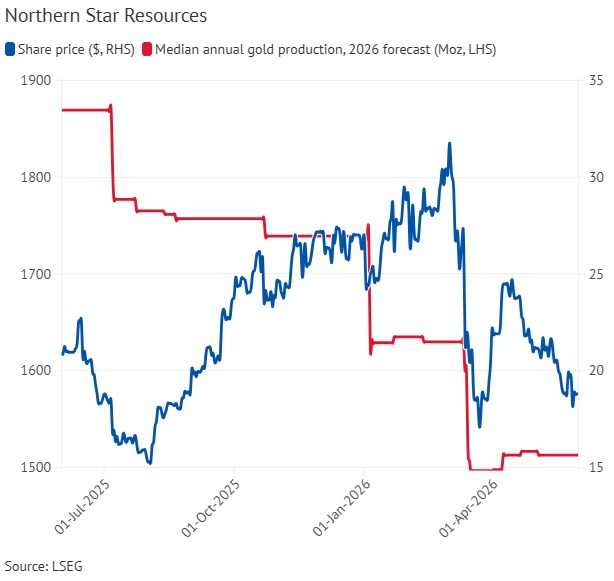

In a presentation titled Northern Star Rising, Elliott called for Northern Star to conduct a strategic review and urgently consider a sale while searching for a new chief executive. Northern Star chief executive Stuart Tonkin announced his resignation in May after the production downgrades.

Elliott, which is also calling for the company to hire new directors with “fresh perspectives”, used the 39-page presentation to highlight Northern Star’s 200 per cent underperformance relative to its peers and that it had reduced its production guidance four times in the past three months.

“The market views Northern Star as a poor operator with a pattern of operational missteps and repeated failures to execute capital projects on time and on budget,” Elliott said in the presentation released on Tuesday.

The operational missteps and low valuation had made Northern Star a target for a discounted takeover, analysts warned earlier this year.

“Northern Star owes it to its shareholders to promptly explore all strategic alternatives, including a sale of the company. We believe there would be significant strategic interest in Northern Star,” Elliott said, adding that the company should immediately hire bankers to explore its options.

The presentation said: “Absent a sale, the company should pursue a comprehensive turnaround.

“Northern Star’s assets can be world-class; however, years of mismanagement necessitate an immediate operational review and changes in leadership.”

On Tuesday afternoon, Northern Star told investors that the company “welcome[d] the opportunity for constructive dialogue”, and said the search for Tonkin’s successor was “well under way, with an international search firm appointed and discussions with potential candidates taking place”.

In a statement, Northern Star said it was working with Goldman Sachs, its long-time financial adviser, to review options, which included “managing its existing portfolio of assets and potential broader M&A opportunities”.

Elliott was founded in 1977 by legendary Wall Street hedge fund manager Paul Singer. The Northern Star position is its most prominent position on the ASX in almost a decade. In 2017, it led an ambitious and ultimately successful campaign to force BHP, then BHP Billiton, to collapse its dual-listed structure and divest its energy assets in the United States.

Challenge for chairman Chaney

A campaign for change at Northern Star would pit Elliott against one of the country’s most influential directors, Michael Chaney. The 76-year-old businessman has been on the board since 2021, taking over after the company’s spectacular acquisition-led rise from junior into the top tier.

Chaney is also the chairman of Perth-headquartered conglomerate Wesfarmers, the owner of Kmart, Officeworks and Bunnings, and was previously the chairman of National Australia Bank and Woodside Energy.

Northern Star’s market capitalisation peaked at $44 billion in February, soon after gold hit a record high of $US5597 an ounce as geopolitical tension and central bank buying drove record demand for the metal.

Northern Star’s acquisition of smaller rival De Grey Mining in a $6 billion deal last year also added to investor optimism. That gave the miner control of the Pilbara’s Hemi resource, an asset many in the industry believe is one of the best undeveloped gold prospects in the country.

But Northern Star’s market valuation has since slid to $26 billion, primarily due to production downgrades.

The company’s $1.6 billion expansion of the mill attached to its Kalgoorlie mines has been beset by mechanical problems, delays and cost blowouts. The company also said that the Hemi mine would not produce gold until 2030, three years later than first thought.

Tribeca Investment Management portfolio manager Ben Cleary, who has previously run activist campaigns at BHP, Teck Resources and Glencore, said Elliott had picked the right moment to strike.

“The timing is good from Elliott given the underperformance versus peers and indices, the share register is open and I think most would be sympathetic to running a process,” Cleary said.

“Buy versus build is alive and well in the mining sector and I would expect no shortage of buyers for Northern Star either as a whole or broken into pieces.”

In its presentation, Elliott told investors there was a considerable “valuation gap” between Northern Star and its peers, demonstrated by its price-to-net-asset-value multiple of 0.69 times – which is 55 per cent below the peer average of 1.08 times – and an enterprise-value-to-future-earnings multiple of 3.4 times, compared with the peer average of 5.5 times.

“Weak execution, continued operational missteps and unclear strategic direction have caused a lack of confidence in leadership that is reflected in deeply discounted multiples using consensus forecasts which themselves embed conservative expectations,” the fund said in its presentation.

- “[Elliott Management’s] track record suggests they will not back down quietly from achieving their desired sale outcome.”

- — Flynn Tyson, Morgans analyst

Elliott also accused the company of being in the midst of a “talent exodus” – presenting a table of 12 executives and managers who have departed the company, including Bill Beament, to take up positions at rival miners.

Morgans analyst Flynn Tyson said Elliott’s campaign was a “strong catalyst” for Northern Star to get a better valuation from investors.

“The fund’s track record suggests they will not back down quietly from achieving their desired sale outcome, and we expect a strategic review to be formalised in the near term,” he said in a note to clients.

“Even absent a sale, the pressure being applied creates a credible path to value recovery. The appointment of a high-calibre CEO and board refresh should materially reset operational expectations over the medium term and restore market confidence in [Super Pit mine] execution.”

Matt Salmon, an executive director at UBS, said Elliott’s arguments were already well known to Australian investors. “The overall tone from Aussies is one of ‘not much new’ and ‘nothing has changed’,” he told clients.

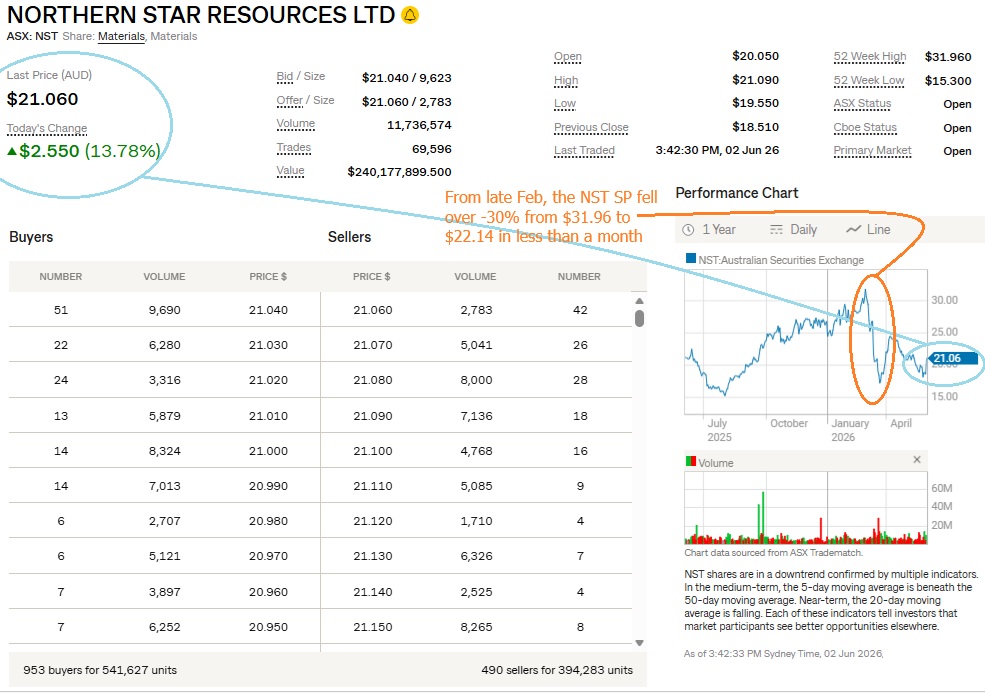

But the market reacted dramatically, pushing Northern Star shares up almost 14 per cent by the afternoon. That made it the second-largest single-day price gain after Elliott revealed an investment in more than 30 campaigns launched by the activist fund manager since 2012.

Northern Star was trading at $21, up $2.49, in the early afternoon.

--- ends ---

NST's Response: NST - Response to Media Commentary.pdf [02/06/2026 1:07 pm]

Click the link to read their response. Nothing earth-shattering in there - see below:

Source: https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03096306-6A1327955

Disclosure: I hold NST shares both here (SM) and in my real-money ISA (Income Stream Account through CBUS).

After a +30% share price fall in 4 weeks from late Feb, we need a few more days like today to get the NST SP back up to $30 or above - After a circa +14% rise today it's only just above $21. Plenty of headroom left there. Especially as the expanded KCGM mill comes fully online next year and then they turn their attention to developing Hemi.

Note: the market had to not yet closed when I prepared and posted this straw.

4th August 2025: Investor Presentation - KCGM Site Visit [39 pages]

Today's presso is 39 pages long, so below I'm just going to share the 10 most important slides, in my opinion (as an NST shareholder):

Firstly it's important to understand just how big KCGM (Kalgoorlie Consolidated Gold Mines, being the Kalgoorlie Super Pit and the Fimiston Mill and surrounding tenements) is, and why it is NST's key global asset:

Next, here's a breakdown of exactly where NST are in the multi-year upgrade of Fimiston (the KCGM gold mill) which they are expanding from 13 Mtpa to 27 Mtpa, so more than doubling its annual ore processing capacity:

The following slide has to be understood in the following context: Back when Bill Beament was running NST, he developed a really good internal mining services arm that allowed NST to be owner-operators without needing to employ contract miners. Bill came from a mining services background before he took over NST and built it up to be Australia's second largest gold mining company, behind Newcrest which was then acquired by US-based Newmont, so NST is now Australia's largest gold miner.

Not only were NSMS - Northern Star Mining Services - competent, they were actually better, cheaper, and faster than many of their competitors in the Australian gold sector. This slide shows just how much better KCGM underground has been performing since NSMS took over the actual underground mining - it's impressive:

The summary (page 35):

And their FY26 guidance:

Disclosure: Holding.

The market likes it - NST is up +5.88% today to $16.20 (up 90 cents today) - so far - with over 2 hours left in the trading day.

It's is a good day on the Aussie market for the Aussie Gold Sector, with most goldies in the green. In fact there are around 8 companies that are up even more than NST are:

Good to see more green on the screen after a string of red days across the sector recently. Plenty of market/price-sensitive news in the Aussie Gold Sector today, and it's mostly good news.

That's just the top 11 performing Aussie gold companies today, there are around another 50 Aussie gold companies not shown there.

Note: For proper context of the slides in this post, please see the entire presentation:

4th August 2025: Investor Presentation - KCGM Site Visit [39 pages]

Saturday 7th June 2025. A wet and windy day in Adelaide and I'm getting over the flu, so have been sitting in my office with the heater on eating reheated Mexican food, soup and porridge (not in that order) and enjoying MoM's deep dive into the history of Australia's largest gold miner, Northern Star Resources (NST) that MoM released 1 hour ago (earlier this arvo).

How Northern Star Became Australia’s Biggest Gold Miner, Money of Mine, Jun 7, 2025

[Money of Mine Podcast]

[Money of Mine Podcast]Show notes:

How does a shell company turn into Australia’s biggest gold miner, capped at nearly $30 billion?

In this episode, we unpack the fascinating story of Northern Star — from 2c a share to over $20, securing world-class assets across multiple continents, including the Australia’s greatest gold mine, the Super Pit.

We trace the company’s journey, get in the weeds on their M&A approach, and highlight the characters who shaped it — with a focus on the early days at Paulsens, the deal that set Northern Star on its path, and culminating with the coronation of the “King of Kalgoorlie.”

THE DIRECTOR'S SPECIAL

Join 12k+ subscribers to the Director’s Special: one daily email with all the news that matters in mining

https://www.moneyofmine.com/subscribe

-------------------------------------------------------

▶️ CHAPTER TIMESTAMPS

00:00 Introduction

04:05 Paulsens

30:10 Plutonic

34:11 East Kundana & Kanowna Belle

42:57 Jundee

57:18 South Kalgoorlie

58:50 Pogo

1:10:48 Echo

1:13:15 Super-Pit

1:19:18 Saracen

1:25:27 Learnings

1:36:59 Shout out

-------------------------------------------------------

--- end of show notes ---

Here's a small transcript from near the beginning:

"In May 2010, they come out with an announcement that they're going to acquire the Paulsens Gold Mine; The company has a mighty market cap of under $8 million, and the share price is four and a half cents, so... how's that for a starting point?"

--- end of transcript ---

For those who may not be aware, Bill Beament, prior to becoming the MD of NST, which was just a shell at that point (and later becoming it's Executive Chairman when Bill brought Stuey Tonkin across to NST and made him CEO in Nov 2016), held several senior management positions, including General Manager of Operations for Barminco Limited with overall responsibility for 12 mine sites across Western Australia; Bill had also been the General Manager of the Eloise Copper Mine in Queensland.

At Barminco, Bill was responsible for Barminco's mining services (contract mining) contracts at 12 mines, and one of those 12 was Intrepid Mining's Paulsens gold mine, and Bill clearly thought he could run that mine a lot better than Intrepid (the mine owners) were at that time. Intrepid Mines had deprioritised Paulsens in favor of Indonesian projects where they thought they'd get more bang for their bucks. Intrepid were therefore not spending the money at Paulsens to define how far the gold extended or even to run the mine efficiently as it was.

This proved to be a disastrous decision for Intrepid, whose experience with Indonesian mines, specifically the Tujuh Bukit project, was marked by significant disputes and ultimately, a loss of control over the project. While the company initially made promising discoveries and saw potential in the region, it faced challenges with its local partner and legal issues in Indonesia, leading to a major loss of investment, and a protracted legal battle, and accusations of fraud, severely negatively impacting shareholder value and leading to a CEO resignation.

Intrepid Mines Limited ultimately merged with AIC Resources in 2019, becoming AIC Mines. This followed a failed takeover offer by Intrepid for AIC.

Meanwhile, the gold mine that Intrepid Mining were happy to divest back in 2010, Paulsens, did VERY well under NST ownership, and is still being mined today, this time by Black Cat Syndicate (BC8) who bought the mine from NST in 2022 and have extended its mine life through successful regional exploration in the surrounding area within tenements that they (BC8) own.

However, back in the day, from 2010, Paulsens became the foundation of NST's extraordinary success that today sees Northern Star with a share price of circa $21/share, a market capitalisation of $30 Billion, being an ASX50 company, Australia's largest gold miner, and one of the 10 largest gold mining companies in the world, and the only Australian-domiciled gold miner in that list.

And they are certainly still growing - they're in the middle of doubling the mill capacity at Fimiston (the Super Pit, a.k.a. KCGM), and have bought De Grey Mining for $5 Billion recently, so NST now own Hemi, the largest known undeveloped gold deposit in Australia.

It's quite a story and well worth a listen/watch: How Northern Star Became Australia’s Biggest Gold Miner [MoM podcast, Saturday afternoon, 7th June, 2025]

Disc: Yes, of course I hold NST shares! [both here and in my SMSF]

02-Dec-2024: NST’s $5B Deal: Most Expensive Undeveloped Gold Mine Ever (Money of Mine podcast)

"There’s only one thing to talk about today… Northern Star’s big swing for De Grey. This friendly, all-scrip deal which implies a A$5b value for the developer of Hemi is the biggest deal of its kind, so we’ve got plenty to chat about."

CHAPTERS

0:00:00 Introduction

0:01:40 NST make $5b move for DEG

0:08:21 Will Gold Road get in the way

0:13:23 How does Hemi fit into NST

0:22:03 Hemi's met

0:35:12 Thoughts on the deal

DISCLAIMER

All information in this podcast is for education and entertainment purposes only and is of general nature only.

The hosts of Money of Mine (MoM) are not financial professionals. MoM and our Contributors are not aware of your personal financial circumstances. Before making any investment decision, you should consult a licensed financial, legal or tax professional.

MoM doesn’t operate under an Australian financial services licence and relies on the exemption available under the Corporations Act 2001 (Cth) in respect of any information or advice given. MoM strive to ensure the accuracy of the information contained in this podcast but we don’t make any representation or warranty that it’s accurate or up to date. Any views expressed by the hosts of MoM are their opinion only and may contain forward looking statements that may not eventuate.

MoM will not accept any liability whatsoever for any direct or indirect loss arising from any use of information in this podcast.

--- ends ---

[I do currently hold DEG and NST, but not GOR]

02-Dec-2024: Northern Star agrees to acquire De Grey.pdf

And: Presentation - Northern Star agrees to acquire De Grey.pdf

Details of this deal:

- Northern Star agrees to acquire De Grey by way of a recommended scheme of arrangement, with De Grey shareholders to receive 0.119 new Northern Star shares for each De Grey share held; and

- De Grey’s flagship project, Hemi, provides Northern Star with an additional Tier-1 future low-cost production centre, aligning to its strategy to deliver superior shareholder returns.

A Tier-1 gold asset is defined as an operation producing in excess of 500kozpa of gold per annum with a 10+ year mine life.

At 1:42pm Sydney time, DEG is trading up +26.45% (or +40.2 cps) @ $1.922 and NST is trading -7.37% (down -$1.29) @ $16.22.

I have to do some work on whether the price paid is reasonable here, but as an NST shareholder I am encouraged that NST have used their scrip for this deal rather than cash, so this doesn't result in any change to their cash or debt positions.

This deal (0.119 new NST shares for each DEG share) represents an implied offer price of A$2.08 per De Grey share and a total equity value for De Grey of approximately A$5 billion on a fully diluted basis, based on the closing price of Northern Star shares of A$17.51 on Friday (29 November 2024) - obviously a bit less now since NST's share price has dropped today.

The Scheme is unanimously recommended by the Board of Directors of De Grey, and each De Grey Director intends to vote all De Grey shares that they hold or control in favour of the Scheme, in each case, subject to no Superior Proposal (as defined in the SID - Scheme Implementation Deed) emerging and the Independent Expert concluding (and continuing to conclude) in the Independent Expert’s Report that the Scheme is in the best interest of De Grey shareholders.

The Scheme Consideration represents a significant and attractive premium of:

- +37.1% to De Grey’s last closing share price of A$1.52 per share on 29 November 2024; and

- +43.9% to De Grey’s 30-day volume-weighted average price of A$1.45 per share up to and including 29 November 2024.

Upon implementation of the Scheme, Northern Star shareholders will own approximately 80.1% of the combined Group and De Grey shareholders will own approximately 19.9%.

Here's the 5 year SP graphs of both companies up until today:

Here's the important stuff (IMO):

So NST's Ore Reserves increase by +29% to 26.9 million ounces, and their Mineral Resources increase by +22% to 74.9 million ounces.

Low cost - Hemi should be in the lowest quartile of the AISC (cost) curve.

Consistent with NST's purpose of generating superior returns for shareholders.

So, I'll have a think about the price, but at this stage, I'm happy enough with this as an NST shareholder.

Thursday 22-August-2024: FY24 Financial Results

Results Presentation for Year Ended 30 June 2024

Also: Northern Star - delivering on our commitments - Diggers & Dealers Presentation, August 2024

https://www.nsrltd.com/investors/presentations/#type=Presentation

https://www.nsrltd.com/investors/asx-announcements/

https://www.nsrltd.com/investors/

Disclosure: Yes, I hold NST shares.

And so does Marcus Padley's "Growth Portfolio" (managed fund) as from today (Monday 26th August). Here's his commentary on Friday:

- Northern Star Resources (NST) – One of our favourite gold plays along with EVN (NST is less volatile than EVN, daily ATR of 2.3% vs 3%). NST reported yesterday, rising 3.2% before losing morning gains to finish up 1.7%. The results either meeting or beating broker expectations. Record cash earnings of A$1.8bn, 1,621koz of gold was sold at AISC of A$1,853/oz, meeting its FY24 guidance. The outlook included gold sales of 1,650-1,800koz at an AISC of A$1,850-2,100/oz. Solid numbers but results for commodity stocks are less important compared to companies like WTC or BXB (covered yesterday). The biggest share price driver by far is the gold price which has been hitting one record high after another this year. Our gold price outlook is that despite being at record highs if bond yields continue to fall the gold price will continue to rise, supported by ongoing central bank buying around the world. Commodity stocks can be risky, there is every possibility of a 10-15% dip along the way but for a long-term holding it’s a buy. Will add to the Growth Portfolio with a 5% weighting on Monday provided Powell doesn’t do anything to scare the market tonight.

Source: https://marcustoday.com.au/

So he's adding it based on technicals and momentum. I hold it because it's Australia's largest gold producer and a very well run company. Here's some excerpts from their FY24 results summary announcement.

Under Bill Beament as Executive Chairman back when he was still at NST, he always said they ran the company as a business first and a miner second, so profitability and shareholder returns were what their decisions were based on.

Stuey Tonkin was their CEO under Bill and he's now their MD as well, and he's carrying on that same tradition.

In Summary: Why I hold NST:

- Australia's largest and best gold exposure (Aussie HQ'd and their primary listing on the ASX);

- Profitable, with plenty of growth, particularly the KCGM (a.k.a. the Super Pit/Fimiston Mill) mill expansion, underway right now;

- A$2.7 Billion of liquidity including 30 June cash and bullion of A$1,248 million with net cash of A$358 million, plus during the year, they refinanced their corporate bank facilities with maturity dates of December 2027 and December 2028 across two equal tranches totaling A$1.5 billion, which remains undrawn at year end, and which along with their cash and bullion, provides liquidity of A$2.7 billion leaving the Company very well-funded;

- Zero net debt;

- On top of what they already own and operate, which is very substantial, NST have guided for $180 million just for Exploration expenditure in FY25, so there's certainly plenty of further potential upside from that as well;

- Despite higher costs at Yandal (which is still profitable), NST's group AISC remains competitive, particularly considering their size and the fact that they aren't relying on hundreds of millions of dollars worth of copper by-product credits to reduce their AISC (yes, I'm looking at you EVN !) - so NST will remain profitable at substantially lower gold prices, and they are controlling their costs reasonably well (considering the inflationary environment they've been exposed to in terms of mining and engineering sector costs); and

- I like Stuey's management style - low profile, but gets the job done.

02-May-2024: Annual Resources, Reserves and Exploration Update [489 pages]

Market Like.

NST closed at $15.10 on Friday and have been down every day this week (Mon, Tues & Wed) prior to today (Thurs 2nd May), with the worst day being yesterday when NST's SP dropped -51 cents (-3.41%), so good to see some claw-back today on the back of this annual Reserves, Resources and Exploration update.

Since that low point in early October (@ around $10/share), NST have been in a decent uptrend, which is not surprising given what the gold price has done and that NST is Australia's largest gold mining company.

Some people may think gold has peaked for now based on yesterday's sector sell down...

Source: MarcusToday daily EOD newsletter yesterday, Wednesday 1st May 2024.

But today Gold and Financials are the best sectors - leading the market back up.

Source: MarcusToday, mid-day email, Thursday 2nd May 2024 [so middle of the trading day snapshot]

Consumer Staples are the worst sector today mostly due to the market selling Woolies (WOW) down by around -4% on the back of their Third-Quarter-Sales-Results.PDF.

The gold price has certainly dropped back from its recent all-time highs, but I doubt that the rally is done yet, I would expect this is more a pause in a continuing uptrend. But you never know.

11-Apr-2024: NST-Operational-Update.PDF

Source: Commsec.

Nice Update (below, link above), nice chart, onward and upward.

Cost guidance (AISC) up, but gold production guidance of 1.60-1.75Moz maintained, despite the bad weather around Kal in April and March affecting production. They produced 1.18Moz in the first 9 months of this FY (to March 31st), so they only need to produce 402koz in the final quarter to hit the bottom end of that full year production guidance. And they produced 401koz in the March quarter despite the weather. Additionally they expect a strong June quarter, with increased grade and improved mill utilisation rates.

Northern Star Resources (NST) is Australia's largest listed gold miner headquartered in Australia, and Australia's best gold miner by a country mile. The market weren't too interested in them after Bill Beament left to head up Venturex (now Develop - DVP), but the market is coming around now - because with the gold price hitting new all time highs now on a regular basis, and NST being so big and dominant in the sector, and performing well too - producing so much gold at reasonable costs (remembering that costs have increased for every gold miner), NST is hard to ignore. They will also be an obvious play for international money looking to find some exposure to the sector, because NST is now one of the top 10 gold mining companies in the world (see here: Largest gold mining companies by Market Cap (companiesmarketcap.com)) and the 34th largest mining company (across ALL commodities) in the world (see here: The top 50 biggest mining companies in the world - MINING.COM 05-April-2024).

NST also operate one of the 10 largest gold mines in the world (the Super Pit, next to Kalgoorlie) - see here: Here are the top 10 largest gold mines in the world (miningreview.com) - and one of the two largest gold mines in Australia - the Boddington Gold Mine (owned by Newmont GoldCorp) is the other one.

The "Super Pit".

NST have stated (see here: Northern Star Resources approves $1.5 billion upgrade to KCGM's Super Pit Fimiston processing plant - ABC News 22-June-2023) that they believe that with the increased capacity, the Super Pit is primed to supersede Boddington Gold Mine as Australia's largest gold operation and join it as one of the top five gold producers (mines) in the world by 2029. And that will propel NST further up the world rankings in terms of top 10 global gold miners. Depending on what sources you use and the recency of the reporting, NST sits somewhere between 7 and 11 currently, however I believe they will be at #6 by 2030, and possibly higher if there is further M&A within the current top 6.

So the target is that NST will be a top 7 gold miner (likely #6 IMO) and be operating one of the world's largest 5 gold mines by 2030. Could be sooner than that depending on progress with the Super Pit expansion. It is already underway and due for completion in 2029, with full ramp-up being completed in 2030.

In June last year (see here) they said they had 120 million tonnes of pre-mined ore, estimated to hold about 3 million ounces of gold, at the Fimiston Mill (a.k.a. the Super Pit mill), and their chief technical officer (CTO) Steven McClare said that stockpile would be a "key feed source" for the new mill and provide certainty for the miner. Steve said, "If we stopped mining today, we could process that material and it would take more than nine years to actually get through that stockpile."

And they didn't stop mining obviously, so the stockpile continues to grow due to the current capacity constraints of the existing mill, however they are spending $1.5 Billion to upgrade that mill from 13 million tonnes a year to 27 million, so more than doubling annual ore processing capacity. And that is just ONE of their gold mines.

Disclosure: I hold NST shares, both here and in my largest two real money portfolios.

06-May-2022: (Friday): Interesting ABC News article on Wednesday (04-May-2022): Miner Northern Star Resources strikes gold beneath Kalgoorlie's Super Pit - ABC News

Plain Text: https://www.abc.net.au/news/2022-05-04/gold-miner-drills-beneath-kalgoorlie-super-pit/101035098

Miner Northern Star Resources strikes gold beneath Kalgoorlie's Super Pit

ABC Goldfields / By Jarrod Lucas

Posted Wed 4 May 2022 at 3:05pm, updated Wed 4 May 2022 at 3:23pm

Underground access was restored from within the Super Pit last year through a portal on the western wall. (ABC Goldfields: Jarrod Lucas)

It has been described as the "first glimpse" of a new world-class gold system beneath Kalgoorlie's famous Super Pit.

Despite more than a century of mining on the historic Golden Mile, there has been limited exploration outside of the rich deposits which have yielded more than 21 million ounces since the Super Pit began production in 1989.

Underground access portals on the western wall were developed last year to provide new drilling platforms for testing north-west of the existing pit.

The work represented the first significant underground mining activity on the Golden Mile in more than 30 years.

The investment by Perth-based gold miner Northern Star Resources is starting to pay off after it said it hit pay dirt.

In the company's annual reserves and resources statement to the ASX this week, Northern Star said drilling had increased the underground resources 20 per cent to 5 million ounces.

Northern Star Resources chief operating officer Simon Jessop inspects the entrance to the new underground portal inside the Super Pit in May last year. (ABC Goldfields: Jarrod Lucas)

Northern Star managing director Stuart Tonkin said the portals had been developed 1.5km in length and drilling only began last November.

"It's really not been a lot of time drilling and we're obviously continuing to drill now," he said.

"But we've already added a million ounces of inferred material."

He said there was 5 million ounces of Fimiston underground resource.

"So again it shows us the thin end of the wedge," he said.

"That investment is starting to show great signs of where the future can be underground there."

Deepest workings 1.4km underground

More than 3,500km of tunnels and shafts have been created underneath the Super Pit — equivalent to driving from Perth to Sydney- in a century of mining the area.

The deepest historical workings extend about 1400m below the surface.

But drilling has hit gold mineralisation as deep as 2km below the surface.

Northern Star has made no secret of its ambitions to eventually restart underground mining and is taking delivery of 39 new haul trucks as part of a $250 million fleet overhaul.

Northern Star Resources chief executive Stuart Tonkin inspects the Fimiston Mill.(ABC Goldfields: Jarrod Lucas)

"We're really only looking at the one quadrant at the moment," Mr Tonkin said.

He said the company would put more drill drives to the south as well as onto the eastern side beneath the plant.

"At the moment it's like trying to eat an elephant, you've got to pick off bits and really focus in on it, and this drill drive is the first part of that," Mr Tonkin said.

Mine life beyond 2035

The current reserves at the Super Pit and neighbouring Mt Charlotte mine stand at 11.9 million ounces.

There are 27 million ounces of resources which require further geological work to prove up as reserves under the JORC Code.

The significance of the latest underground drilling results is the fact they are outside the current mine plan, which will result in further cutbacks of the Super Pit until at least 2035.

Drilling from the underground portal has already defined one million ounces of new gold resources. (ABC Goldfields: Jarrod Lucas)

"This is currently not in the plan, so it's important we get in and do this work over the next couple of years to define it and start to work out the scale and magnitude and how it can come into the mine plan," Mr Tonkin said.

"This is on top of the confidence we already have for the future of the Super Pit."

He said he was not surprised by the latest find.

"We're really confident we have multiple decades ahead of us," Mr Tonkin said.

"There is no geological reason why this terminates at depth."

The drilling results were released as Northern Star prepared to announce the results of a feasibility study into a potential expansion of the Fimiston Mill in coming months.

The Fimiston processing plant is one of the biggest in Australia and was commissioned in 1989.

It has since undergone two expansions and treats more than 13 million tonnes of ore a year from the Super Pit and Mt Charlotte.

Mr Tonkin said expanding to 23 million tonnes a year was among the options being considered.

Key points:

- Northern Star Resources is Australia's second-biggest gold producer behind Newcrest Mining

- The company paid $1.1 billion for a 50 per cent stake in Kalgoorlie's Super Pit in 2019

- Northern Star Resources and Super Pit co-owner Saracen Mineral Holdings completed a $16 billion merger last year (meaning that Northern Star now own 100% of the Super Pit).

--- ends ---

The Kalgoorlie Super Pit is just one of NST's mines of course, but there wouldn't have been too many people who viewed it as a future growth option for NST, but it has just become exactly that with the gold they are discovering under the existing pit.

Disclosure: I hold NST in all of my main RL portfolios and NST is also the largest position in my Strawman.com virtual portfolio.

14-April-2022 - Just to add to the straw by @edgescape on NST's announcement yesterday that they have agreed to sell their Paulsens Gold Operation (Paulsens) and Western Tanami Gold Project (Western Tanami) to Black Cat Syndicate Ltd (ASX: BC8) for $44.5m. This deal is subject to BC8 achieving finacing and if that occurs, NST will receive $14.5m plus 8,340,000 (i.e. 8.34m) fully paid ordinary shares in Black Cat (BC8) at a deemed issue price of $0.60 per share which is worth an additional $5m (or $5,004,000 to be exact). BC8 closed at 68c/share today. The other $25m is made up of $10m worth of milestone payments (details below) which are dependent on future gold production from both mines and $15m "deferred consideration" to be paid on 30 June 2023, so NST are really selling Western Tanami and Paulsens (which was their original company-making foundation asset) for just $14.5 million, plus around $5m worth of BC8 shares, plus another $15m to be paid in the middle of next year (total value: $34.5m). If BC8 produce gold from both mines in the future then NST can be paid up to an additional $10m in milestone payments as those milestones occur, as follows:

- $2.5 million cash on production of 5,000 ounces of refined gold from Paulsens;

- $2.5 million cash on production of 5,000 ounces of refined gold from Western Tanami;

- $2.5 million cash on production of 50,000 ounces of refined gold from Paulsens; and

- $2.5 million cash on production of 50,000 ounces of refined gold from Western Tanami.

Don't know about you, but I don't reckon I'd ever heard of Black Cat Syndicate before yesterday...

It should be noted that Paulsens and Western Tanami have both been on C&M ("care and maintenance", i.e. mothballed) as the AISC was too high for the gold that remained there in each case. A smaller company could perhaps give those assets the love and attention they need to become money makers once again - which is clearly what BC8 intend to do - however for NST, Australia's second largest gold mining company (behind NCM) and now one of the top 10 largest gold producers in the world (in terms of both market cap and ounces of gold produced per annum), they have bigger fish to fry now.

Source: https://www2.asx.com.au/markets/company/nst [14-Apr-2022]

Still look like good value here to me!

Disclosure: I hold NST in my 3 largest RL portfolios as well as in my Strawman.com portfolio. They are still my number one gold producer pick, even with Bill Beament gone.

Northern Star CEO Stuart Tonkin, executive chairman Bill Beament and former chairman Chris Rowe in 2016 posing for a Mining Journal article titled, "Beament not going anywhere" They were right for the next 4 years at least, but Bill did leave in 2021 to head up Venturex, now called Develop Global (DVP), and Stuey took over as MD (retaining his CEO position also). Bill B was replaced by Michael Chaney AO, who is also the Chairman of Wesfarmers and had been Wesfarmers' MD for 13 years (from 1992 to 2005). Chaney (pictured below) was also previously the Chairman of NAB and Woodside (WPL) and was a former director of BHP. He started his career originally as a petroleum geologist.

That's all folks... For now...

Except: Paulsens the DNA of Northern Star - MiningNews.net

And: Northern Star hits gold at Paulsens (businessnews.com.au)

Those articles are from circa 2015/2016. Bill Beament bought Paulsens off Intrepid Mines for $40m in 2010 and built Northern Star up from that one foundation asset. NST's market cap today is $12.8 billion.

Intrepid to sell Paulsens mine for A$40M - The Northern Miner

Intrepid to sell Paulsens mine for A$40M - The Northern Miner

Paulsens

Paulsens

Paulsens

Paulsens

Pogo Mine reaches 4 million ounce

Pogo Mine reaches 4 million ounce

26-May-2021: Investor Presentation - KCGM Site Visit

Also - two days ago (24-May-2021): Northern Star appoints Michael Chaney as Non-Executive Chair

In their KCGM (Kalgoorlie Consolidated Gold Mines, i.e. the Kalgoorlie Super Pit) Site Visit Presso, NST took the opportunity to reconfirm their FY21 guidance, saying KCGM was...

- On track to achieve FY21 production guidance; 440-480koz at AISC A$1,470-A$1,570/oz

- Operation being de-risked and productivities are increasing with multiple production sources; Production to rise to +675kozpa by FY28

- KCGM leads Reserve and Resource growth:

- 11.6Moz Reserves (up 20% over 9 months)

- 26.3Moz Resources (up 38% over 9 months)

- Underpins ~13 year mine life

- Further growth via Resource conversion (KCGM Inferred Resources 8.6Moz), host of strong intersections outside Resources and Reserves, backlog of assays pending due to congested assay labs…

- ...and focused exploration across a >90Moz gold camp.

And KCGM is just ONE of their assets.

[I hold NST shares, and I like their choice of Michael Chaney - who used to head up Wesfarmers {WES} - as NST's new non-executive Chairman, now that Bill Beament is moving to head up Venturex {VXR}.]

[P.S. I wonder whether the "backlog of assays pending due to congested assay labs" is positive for XRF Scientific {XRF} or ALS Limited {ALQ}...]

By the way, at the bottom of the below image (the KCGM asset overview; click on the image for a larger version) - you can see the northern end of the town of Kalgoorlie - the streets and houses - which puts the Super Pit into some perspective. It is BIG!

30 August 2018: Northern Star is the best managed gold miner listed on the ASX. I have presented a pretty good bull case for NST over in an "Industry/Competitors" straw for Evolution Mining (EVN).

EVN is the second largest (after Newcrest - NCM) and EVN are also the lowest cost producer of the top 3. NST are the second lowest cost producer, and the third largest, but they are the best run.

I hold both NST and EVN in my super, and also in my main trading / income portfolio. They do both pay dividends, but they're not income stocks. I like to hold some gold for insurance. Or a hedge if you prefer. If we get a crash, there's a better than even chance that gold goes up while share markets are falling fast, and Australia's biggest three gold producers will do well in that scenario. Meanwhile, both EVN and NST have exhibited excellent growth over multiple time frames. Here are the latest TSR numbers for NST, based on today's share price of $6.96 (on August 30th 2018):

- 34.5% over 1 year (these numbers include dividends plus capital growth);

- 54.2% per year over 3 years;

- 51.1% per year over 5 years; and

- 63.3% per year over 10 years.

[From Commsec]

It's hard to find another ASX100 company that has provided those sort of returns consistently over the last 10 years.

They announced an aquisition this morning - of the Pogo gold mine in Alaska:

NST announcement 30 August 2018 of acquisition of Pogo Gold Mine in Alaska

Investor Presentation - Pogo Acquisition

I haven't looked at this in detail yet, but Bill Beament is a very smart operator, and I think he's probably found something pretty good to buy here - at a good price. He has a track record of seeing value in run-down gold operations and then turning them around. One thing is for sure - this announcement will put NST firmly back in the spotlight again.

![]()

{kind=link}

Disclosure: I hold NST shares.

14-Oct-2018: Update: Since the Pogo acquisition announcement, Northern Star has had a higher share price which has raised their market capitalisation, making them the second largest ASX-listed pure-play gold producer, behind Newcrest Mining (NCM). Evolution Mining (EVN) has been bumped down to the #3 position now. Bill Beament (the top man at NST) has been itching to regain this #2 position ever since EVN took it off them a couple of years ago, and Bill's achieved that now. Pogo looks like a good fit for NST and the market likes this move.