Consensus community valuation

by Jonathan Shapiro and Peter Ker, Updated Jun 2, 2026 – 2.46pm, first published at 9.00am

Elliott calls for gold giant Northern Star to put itself up for sale

Elliott Management is calling for Northern Star to consider putting itself up for sale after accusing the ASX’s largest gold miner of being mismanaged after a series of downgrades sent the company’s share price sliding.

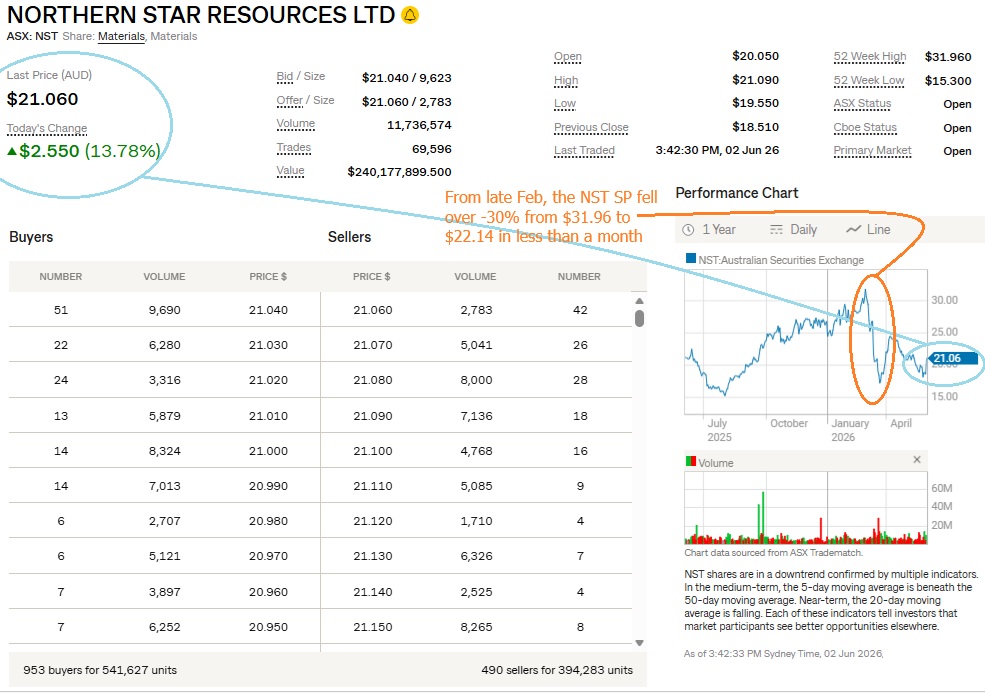

The Florida-based activist fund manages about $US80 billion ($112 billion) and confirmed it had amassed a position “well over $1 billion” in the company. The stake was first reported by The Australian Financial Review and triggered a 13.5 per cent surge in Northern Star shares on Tuesday.

Northern Star chairman Michael Chaney is facing calls from Elliott Management to consider a sale. Trevor Collens

In a presentation titled Northern Star Rising, Elliott called for Northern Star to conduct a strategic review and urgently consider a sale while searching for a new chief executive. Northern Star chief executive Stuart Tonkin announced his resignation in May after the production downgrades.

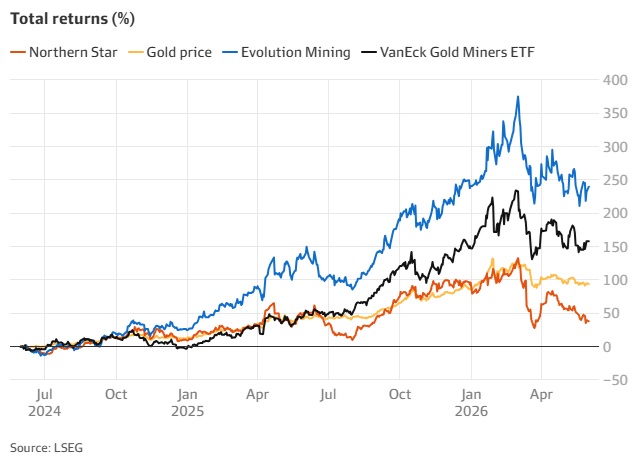

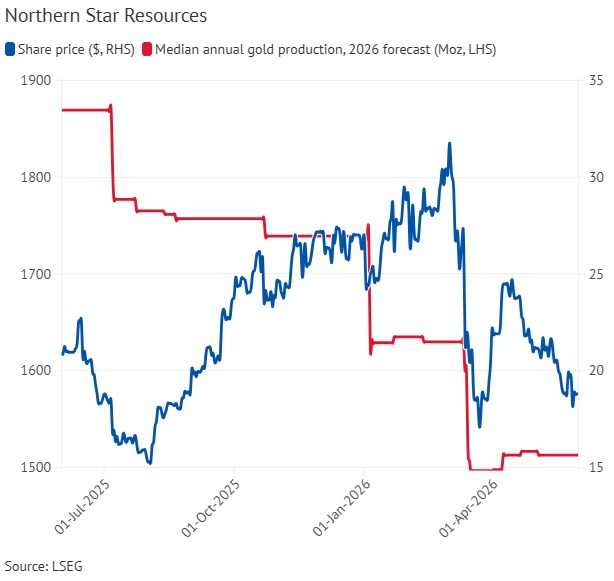

Elliott, which is also calling for the company to hire new directors with “fresh perspectives”, used the 39-page presentation to highlight Northern Star’s 200 per cent underperformance relative to its peers and that it had reduced its production guidance four times in the past three months.

“The market views Northern Star as a poor operator with a pattern of operational missteps and repeated failures to execute capital projects on time and on budget,” Elliott said in the presentation released on Tuesday.

The operational missteps and low valuation had made Northern Star a target for a discounted takeover, analysts warned earlier this year.

“Northern Star owes it to its shareholders to promptly explore all strategic alternatives, including a sale of the company. We believe there would be significant strategic interest in Northern Star,” Elliott said, adding that the company should immediately hire bankers to explore its options.

The presentation said: “Absent a sale, the company should pursue a comprehensive turnaround.

“Northern Star’s assets can be world-class; however, years of mismanagement necessitate an immediate operational review and changes in leadership.”

On Tuesday afternoon, Northern Star told investors that the company “welcome[d] the opportunity for constructive dialogue”, and said the search for Tonkin’s successor was “well under way, with an international search firm appointed and discussions with potential candidates taking place”.

In a statement, Northern Star said it was working with Goldman Sachs, its long-time financial adviser, to review options, which included “managing its existing portfolio of assets and potential broader M&A opportunities”.

Elliott was founded in 1977 by legendary Wall Street hedge fund manager Paul Singer. The Northern Star position is its most prominent position on the ASX in almost a decade. In 2017, it led an ambitious and ultimately successful campaign to force BHP, then BHP Billiton, to collapse its dual-listed structure and divest its energy assets in the United States.

Challenge for chairman Chaney

A campaign for change at Northern Star would pit Elliott against one of the country’s most influential directors, Michael Chaney. The 76-year-old businessman has been on the board since 2021, taking over after the company’s spectacular acquisition-led rise from junior into the top tier.

Chaney is also the chairman of Perth-headquartered conglomerate Wesfarmers, the owner of Kmart, Officeworks and Bunnings, and was previously the chairman of National Australia Bank and Woodside Energy.

Northern Star’s market capitalisation peaked at $44 billion in February, soon after gold hit a record high of $US5597 an ounce as geopolitical tension and central bank buying drove record demand for the metal.

Northern Star’s acquisition of smaller rival De Grey Mining in a $6 billion deal last year also added to investor optimism. That gave the miner control of the Pilbara’s Hemi resource, an asset many in the industry believe is one of the best undeveloped gold prospects in the country.

But Northern Star’s market valuation has since slid to $26 billion, primarily due to production downgrades.

The company’s $1.6 billion expansion of the mill attached to its Kalgoorlie mines has been beset by mechanical problems, delays and cost blowouts. The company also said that the Hemi mine would not produce gold until 2030, three years later than first thought.

Tribeca Investment Management portfolio manager Ben Cleary, who has previously run activist campaigns at BHP, Teck Resources and Glencore, said Elliott had picked the right moment to strike.

“The timing is good from Elliott given the underperformance versus peers and indices, the share register is open and I think most would be sympathetic to running a process,” Cleary said.

“Buy versus build is alive and well in the mining sector and I would expect no shortage of buyers for Northern Star either as a whole or broken into pieces.”

In its presentation, Elliott told investors there was a considerable “valuation gap” between Northern Star and its peers, demonstrated by its price-to-net-asset-value multiple of 0.69 times – which is 55 per cent below the peer average of 1.08 times – and an enterprise-value-to-future-earnings multiple of 3.4 times, compared with the peer average of 5.5 times.

“Weak execution, continued operational missteps and unclear strategic direction have caused a lack of confidence in leadership that is reflected in deeply discounted multiples using consensus forecasts which themselves embed conservative expectations,” the fund said in its presentation.

- “[Elliott Management’s] track record suggests they will not back down quietly from achieving their desired sale outcome.”

- — Flynn Tyson, Morgans analyst

Elliott also accused the company of being in the midst of a “talent exodus” – presenting a table of 12 executives and managers who have departed the company, including Bill Beament, to take up positions at rival miners.

Morgans analyst Flynn Tyson said Elliott’s campaign was a “strong catalyst” for Northern Star to get a better valuation from investors.

“The fund’s track record suggests they will not back down quietly from achieving their desired sale outcome, and we expect a strategic review to be formalised in the near term,” he said in a note to clients.

“Even absent a sale, the pressure being applied creates a credible path to value recovery. The appointment of a high-calibre CEO and board refresh should materially reset operational expectations over the medium term and restore market confidence in [Super Pit mine] execution.”

Matt Salmon, an executive director at UBS, said Elliott’s arguments were already well known to Australian investors. “The overall tone from Aussies is one of ‘not much new’ and ‘nothing has changed’,” he told clients.

But the market reacted dramatically, pushing Northern Star shares up almost 14 per cent by the afternoon. That made it the second-largest single-day price gain after Elliott revealed an investment in more than 30 campaigns launched by the activist fund manager since 2012.

Northern Star was trading at $21, up $2.49, in the early afternoon.

--- ends ---

NST's Response: NST - Response to Media Commentary.pdf [02/06/2026 1:07 pm]

Click the link to read their response. Nothing earth-shattering in there - see below:

Source: https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-03096306-6A1327955

Disclosure: I hold NST shares both here (SM) and in my real-money ISA (Income Stream Account through CBUS).

After a +30% share price fall in 4 weeks from late Feb, we need a few more days like today to get the NST SP back up to $30 or above - After a circa +14% rise today it's only just above $21. Plenty of headroom left there. Especially as the expanded KCGM mill comes fully online next year and then they turn their attention to developing Hemi.

Note: the market had to not yet closed when I prepared and posted this straw.

Scroll down for the latest update.

Our best ASX-listed gold mining company, and possibly the best run gold miner in the world. A core holding in my SMSF, as well as in most of my other portfolios, including my Strawman.com virtual portfolio.

02-Feb-20: Reviewed my ("stale") valuation for NST. Looks fine to me. I'm maintaining my $14 PT for Northern Star Resources. Still the best run gold miner in Australia and still a core holding in my SMSF.

04-Aug-20: Reviewed my ("stale") valuation again. Need to raise. Going up another 20% from $14 to $16.80. NST are already above $15, so it's not a particularly bold prediction. However, with the gold price still rising, there's every reason to think that Australia's second largest (and best run) gold miner will continue to rise as well.

02-Feb-2021: I still think NST are going back to $16.80 and beyond, and I'm going to leave my valuation at $16.80. In the shorter term, like in the next 12 months, I think they will reach $16, which is what I've based my SAR valuation (of $6.06) on. SAR are about to be absorbed into NST as the two companies merge this month. I've discussed that in much more detail in various straws and in my SAR valuation. My $16.80 valuation for NST is a 24 month price target, so by Feb, 2023. I hold NST and SAR.

28-July-2021: Update: So - here we are, my price target for NST has been $16.80, and their regularly trading at below $10/share nowadays, mostly I suspect due to Bill Beament leaving to head up Venturex Resources (VXR), something that not too many people saw coming. That announcement came shortly after the successful merger of NST and Saracen (SAR) who were the 2nd and 4th largest Australian-HQ'd, ASX-listed, pure-play gold producers. The merged group, which is still called Northern Star Resources (NST) is still our 2nd largest, still behind Newcrest Mining (NCM), but NST have now joined NCM as being one of the 10 largest gold producers globally, both in terms of ounces of gold produced annually, and in terms of market capitalisation.

I believe that NST's new "Global top 10 gold producer" status will cause a positive re-rating at some point in the future when gold is rising again at a good clip, but for now it's all about Bill leaving, which is understandable, because it was his company. He was the visionary leader behind NST without doubt. However, while he had the vision, and the position of executive Chairman, his CEO Stuart Tonkin was executing Bill's vision during those years, and Stuart remains with NST, and has become their Managing Director (MD) now in addition to remaining their CEO. They also have the Saracen guys there who are no dummies; they did an outstanding job building Saracen up to become Australia's 4th largest gold producer prior to the merger. More recently NST have appointed Michael Chaney (Chairman of Wesfarmers and previously the Chairman of Woodside Petroleum) as Northern Star's new Chairman.

I still hold NST in 3 of my 4 real life portfolios and they are also one of my largest positions in my Strawman.com virtual portfolio, a decision that has certainly negatively impacted my performance in recent months, however they are worth a LOT more than $10/share IMHO, and there is a positive re-rating coming once the market realises that the company still has a bright future WITHOUT Bill Beament.

Of course, as with any commodity producer, the price of the commodity that they produce (gold in this case) will be the most important factor in determining their future prospects.

Another thing that is weighing on sentiment with both SBM and NST is their higher costs (AISC) this year. I think that is temporary, and that their costs will reduce over the coming years, however it is also important to remember that despite higher costs at this point in time, due to a variety of factors, these gold producers are still highly profitable; they are still producing gold at a far lower cost than what they are selling it for. The gold price would have to come down a very long way for them to become unprofitable, and in my opinion the gold price is much more likely to rise than to fall over time. I am therefore very comfortable to hold NST and other gold producers during these periods of negative sentiment around the sector, and wait for that tide to turn. However I am lowering my PT (price target) for NST to $14.50 because I believe they deserved to trade at a quality premium due to Bill Beament running the company, and now that he is not there any longer, I'm taking that premium out of my valuation. If the gold price rises substantially from here though, NST will take out my new PT quite quickly I would expect.

27-Jan-2022: Update: This valuation has been marked as stale, so I'm reviewing it and updating it, however I am not changing the price target (PT) (a.k.a. Target Price or TP) which I'm leaving at $14.50, because I still feel that if gold takes off, which it well could, Northern Star will be among the leaders in terms of share price appreciation. They recently released their December 2021 Quarterly Activities Report on 20-Jan-2022 and their SP rose +98 cps (+11.2%) on the day, closing at $9.73. Along with 99% of the market however, probably more, NST has been sold off over the past few trading days and they closed yesterday (25-Jan-2022) at $9.28.

These market moves haven't changed the intrinsic valuation of NST, which as their Dec Qtr Activity Report showed, is greater than what the market has been attributing to the company. Because they are Australia's second largest listed gold mining company, AND because they one of the top 10 global gold miners in terms of production (ounces of gold produced per annum), they are going to be firmly in the frame when gold goes for another positive run.

I won't go on. I've drunk too much alcohol tonight to elaborate too much without going way off topic and probably wouldn't make much sense anyway, but suffice to say that $14.50 looks fine to me for a 25 month PT, i.e. by Feb 2024 (the month I I turn 58). And two years is really just around the corner. And $14.50 is +56% above the current price, so that explains why they are one of my largest positions both in real life and here on Strawman.com.

They are not likely to multibag - they're not one of those types of stocks, but they certainly have the potential to do very well in a sector that may well outperform when most of the rest of the market goes decidedly pear-shaped. That hasn't proved to be the case yet - in this sell-down, but in the past few market crashes gold stocks headed south initially, then gold rose sharply and gold producers did very well.

Call it a hedge. Call it what you like, but I'm holding plenty of NST. They look cheap here to me, and they are run as a business first and as a gold miner second. The way they should be.

Highly profitable. Outstanding total shareholder returns over decent periods of time. Lots to like. I'm a big fan of this company and a happy holder.

Above - Stuart Tonkin, CEO & MD of NST. Below, Stuart with Bill Beament who was NST's founder and Executive Chairman up until when he left in 2021 to head up Venturex, which is now called Develop Global (ASX: DVP). Stuart has been CEO of NST since 2016, so he knows the company VERY well.

07-Sep-2022: This one was marked as stale, so I'm updating it and reducing the price target for NST down to $10.75, something a bit more achievable now that Bill Beament has left the company and nobody seems to like them anymore. They are still my #1 pick in the gold sector, in terms of clear upside, quality, and scale. When the gold price goes for another run, NST won't get left behind. They are one of the globe's largest 10 gold mining companies now, and Australia's second largest, and they will get plenty of investor attention from around the world when gold miners are in demand again. In the meantime, I believe Stuey and his team will keep doing what they do best which is to run the company as a profitable company first, and as a miner second.

19-Jan-2023: Update: The following is from NST's December-2022-Quarterly-Activities-Report.PDF (released today):

"Our purpose to deliver superior shareholder returns is underpinned by responsibly executing the Company’s profitable growth strategy. Over the past 12 months, Northern Star has been the best-performing senior global gold stock on a total shareholder return (TSR) basis, delivering a TSR of 20% compared with the S&P/TSX Global Gold Sector Index TSR of -1% and VanEck Gold Miners ETF TSR of -7%. Further, Northern Star ranks as the 8th best TSR performer across the ASX 50 Index (Australian 50 Leaders) in calendar 2022."

"Northern Star’s disciplined capital allocation priorities remain returning cash to shareholders, investing in organic profitable growth and maintaining a strong balance sheet. During the quarter, the Company continued its A$300 million buy-back program, which is 42% complete (A$127 million or 15.5 million shares)."

--- end of excerpt ---

I have explained during the past week over in the "Gold as an investment" forum that NST has thrashed the other two ASX-listed large-cap pure-play gold miners over the past six months, 12 months, and 10 years (Northern Star have 10-bagged over 10 years) while NCM actually went backwards. NST is one of the few gold producers that has strong positive returns over all three of those time periods, and they're so far above the other big producers that they're really in a league of their own.

As they point out in today's announcement, they've not only outperformed the global gold sector (so all of the world's larger gold miners) over the last year, they've also provided the 8th best TSR (total shareholder return, which adds capital gains to dividends) of the ASX's largest 50 companies (the ASX50 index) in calendar 2022 (i.e. the twelve months ended 31-Dec-2022). And they're 42% of the way through an active $300 million share buyback, which is yet another way of rewarding their shareholders. Obviously, the more shares they buy back and cancel, the less shares are left outstanding, therefore the value of each remaining share increases.

Up until September last year I had a $14.50 valuation (actually a price target in my case rather than a valuation) on NST, but I lowered that to $10.75 because NST had been trading below $8 and a 80%+ rise to $14.50 seemed a few years away at that point. Well they are now trading back above $12/share and I think $14.75 is quite achievable from here if sentiment remains positive for a year or two.

I maintain my position that NST is the best gold producer (by a country mile) that we have listed on the ASX. They're shareholder focused, they're profitable, they're diversified by number of mines and also by geographical location of those mines (Australia and Alaska), and they are very disciplined when it comes to cost control and with M&A activity.

They remain one of the largest positions in all of my major real life portfolios and the largest position in my SMSF - and also the largest position in my Strawman virtual portfolio.

The S&P/ASX50 Accumulation (Total Return) Index (ASX: XFL) returned +45% over the 10 years. I've left it off that chart above because the result (of XFL inclusion) ended up over the top of the +52% result of the XJO (S&P/ASX200 Total Return Index) and the XJO (largest 200 ASX-listed companies) would be more applicable to most people here than the XFL (largest 50 companies), and the XJO outperformed the XFL anyway.

That chart was created by me this afternoon (using Commsec) after the market had closed, so the prices are current as of today (Wednesday 19th Jan 2023). NST has still 10-bagged (over +1,000% return) while the larger Newcrest Mining (NCM) has lost 5% in share price terms. This chart is only showing the share price performance of NST, EVN & NCM, but is showing the total return (with dividends reinvested) for the XJO (ASX200). Obviously the dividends that have been paid over the past 10 years changes the results of the three gold producers, and would drag NCM into positive territory (but not by much) and increase the positive results of both EVN and NST.

Not only has NST clearly outperformed by a huge margin, it is my firm belief that they are very well positioned to continue to outperform from here.

19-Nov-2023: Update: This one was marked as stale, so I've reviewed it. And raised my price target again. The NST SP came close to my previous $14.75 price target ("valuation") when they closed at $14.40/share on 14th April this year (2023). They've moved around a bit since then, and are currently back below $12, but their SP rose +44 cents (+3.89%) on Friday, so they can move up and down fairly rapidly when sentiment is strong (either way).

They held their AGM on Thursday (16th Nov 2023) and their AGM Presentation was short (6 pages) and to the point. Here's slides 3 to 6:

Source: NST-FY2023-Annual-Report-Chairman's-AGM-Address-and-Managing-Director's-Presentation.PDF

Newcrest Mining has now been acquired by US-based Newmont Gold Corp, so Northern Star Resources (NST) is now Australia's largest ASX-listed and Australian-headquartered Gold Mining Company, and one of the top 10 largest gold miners in the world in terms of both market capitalization and volume of gold produced annually.

They have net cash of A$362 million, they announced a share buy-back of up to A$300 million in August last year and they have bought back A$169 million worth of their own shares so far, as well as increasing their dividends, demonstrating their strong focus on achieving superior shareholder returns.

NST have now achieved investment-grade credit ratings from Moody’s, S&P and Fitch, and in April they issued US$600 million of ten-year senior guaranteed notes at an interest rate of 6.125% pa. Their superior credit ratings allow them to borrow money at very competitive rates, which gives them the flexibility to participate in M&A if they wish to, or to upgrade their existing assets.

NST have now completed the mill expansion at Thunderbox and the plant has commenced ramping up to its full 6Mtpa capacity. In June, the Board approved the final investment decision on the expansion of the Fimiston ("Super Pit") processing plant which will see the milling capacity increase from 13Mtpa to 27Mtpa by FY27, with throughput expected to reach nameplate capacity from FY29. This A$1.5 billion investment will strengthen their portfolio, lower their costs (which are relatively high at this point) and materially increase their free cash flow.

They also now have Marnie Finlayson on their Board. Marnie is the brother of Raleigh Finlayson who built up Saracen Minerals to become Australia's 4th largest gold producer at the time that they merged with (or were acquired by) NST a couple of years ago. Raleigh then left NST to start up Genesis Minerals, which he has already built up to today being one of Australia's ten largest "pure-play" gold producing companies (by "pure-play" I mean NOT including companies like Sandfire or BHP who produce gold as a byproduct of other production).

Marnie is also Managing Director, Battery Minerals, at Rio Tinto (RIO).

Raleigh Finlayson (GMD) with sister Marnie Finlayson (RIO, NST) near the WA School of Mines in Kalgoorlie. Chuck Thomas

Source: Marnie and Raleigh Finlayson: Rio’s lithium star and her Genesis CEO brother (afr.com) [25 Aug 2023]

Excerpt:

Marnie Finlayson is the battery minerals boss leading Rio Tinto into the decarbonisation era. Raleigh Finlayson is a precious metal stayer chasing more success in gold, where his sights are set on a 126-year-old mine.

The sister and brother grew up tormenting one another on a dusty sheep station in Western Australia. They embody the old-meets-new reshaping of WA’s resources industry in their vast childhood backyard, the Goldfields.

Marnie and Raleigh were raised in the Goldfields, a region as rich in the precious metal as anywhere in the world, a major source of nickel for more than 50 years, and now, a lithium hot spot.

Their entrepreneurial uncles – Peter and Chris Lalor – once controlled a string of gold mines and produced tantalum from assets that are now regarded as world-class lithium discoveries.

Those mines – including Greenbushes in WA’s south-west and Wodgina in the Pilbara – are valued at tens of billions of dollars. The Lalor brothers were about 30 years too early to capture any of that value.

There is mutual respect between Marnie and Raleigh, who are graduates of the WA School of Mines in Kalgoorlie. There is also plenty of sledging and stirring. Raleigh, who is younger, took years to grow into his oversized ears and was “spoiled rotten” as the baby of the family.

Marnie hates being reminded that he taught her to drive.

If you believe Raleigh, their jaunts in an old ute sometimes took them onto the highway – aged four and seven. Marnie declares he’s a notorious teller of tall tales.

Marnie, Rio’s managing director of battery minerals, is keeping a close eye on the lithium projects springing up in the wider Goldfields region. Raleigh, as boss of Genesis Minerals, is digging into family history after Genesis’ $628 million acquisition of the Gwalia gold mine once controlled by their maternal uncles.

The familial ties go further: Genesis also has gold projects, including Ulysses, on land once part of their paternal grandfather’s Melita sheep station.

Marnie and Raleigh are both excited by the emergence of lithium in the Goldfields, where Lynas Rare Earths is building a downstream processing plant at Kalgoorlie.

“I think it’s brilliant,” Raleigh says.

“When gold has had its really low days, nickel has supported it and vice versa. All of a sudden we’ve got another commodity [lithium] or commodities when you think about rare earths, that help support the region. You don’t have that sort of feast or famine, and it’s more sustainable.

“I remember not that long ago you couldn’t sell a house in Kalgoorlie and now suddenly, you can’t get one.”

Marnie, Raleigh and their older brother, Daniel, grew up on Jeedamya Station near Leonora.

All three spent school holidays working at the Gwalia gold mine, about 40 kilometres from their home, when their uncles were directors of Sons Of Gwalia. The mine’s long history includes a chapter late in the 19th century when it was run by Herbert Hoover, later the 31st president of the United States.

The 46th president, Joe Biden, has fired up lithium interest in the wider Goldfields region through his Inflation Reduction Act.

Marnie was hooked on mining from the start. Raleigh grew to love it. Daniel has his own successful business on the WA coast making cray pots, the traps used to catch lobster that fetched huge prices on the Chinese market before Beijing’s trade war in 2020.

No childhood on the Goldfields where sheep eventually gave way to cattle can be described as idyllic.

“We grew up in quite a difficult environment. We loved it and hated it at the same time, growing up on the station and working hard,” Marnie says.

Raleigh says: “It was tough just about every year, but a drought would make it even harder. But every year was a good year as far as how tight the family was and continues to be. So for us, there was no better childhood to be blunt, as hard as it was.”

Pocket money

Even shovelling rocks at Gwalia for $5 an hour could not dissuade Marnie from mining.

“I shovelled rock for 12 hours a day. It was my first experience in the industry and I absolutely loved it. From the first moment I started, I knew that the mining industry was absolutely the one for me,” she says.

Marnie presented a battery minerals strategy she developed to the Rio board at the end of 2021. She has lived in Serbia, where she was in charge of Rio’s Jadar lithium project and also ran Rio’s borates operations in California.

The Rio board was sufficiently impressed to back it and make her head of battery minerals.

Why a passion for battery minerals for someone who grew up in the Goldfields, and agreed to join the board of another gold miner, Northern Star, last year?

“I’m passionate about ensuring that mining delivers the materials that are required for the energy transition because I believe that’s critical for ensuring there’s a good future for my children and their children,” she says.

“I see myself in a perfect position to be able to mobilise that, not just through the materials that are produced through the battery materials strategy, but more importantly – and this is Rio’s objective – how they are produced. We’ve got an overall societal challenge about ensuring that mining is done in a sustainable manner.”

Marnie joined Northern Star’s board after Raleigh’s departure as its managing director.

Will they ever work together? “You never say never,” Marnie says. Chuck Thomas

Superpit

It was around August 2021 when Raleigh started to think about his next big challenge after deals that included Saracen’s $1.1 billion acquisition of a half share in the Superpit mine on Kalgoorlie’s doorstep, and a $16 billion merger with Northern Star. His gold industry contemporaries Bill Beament and Jake Klein were lamenting the investor focus on decarbonisation and related minerals.

Asked by The Australian Financial Review in March last year about why he stuck with gold and set about consolidating Leonora, Raleigh replied: “It would have been the easy and obvious option to flip out of gold and into the new fancy metals.”

Today, his response is more even-handed.

“It’s what I know,” he says.

“I could very comfortably go to those [Genesis] shareholders and articulate the strategy and articulate that we’ve got good knowledge of the area and that we have operated lots of mines to be able to get that type of equity over the line at zero premium or zero discount.

“If it had been a green metal and I’m sitting there trying to convince myself – let alone my shareholders – that I’ve got experience and knowledge in that space, it is probably a different conversation.”

Raleigh acknowledges that lithium has “gone beautifully” since he opted to stick with gold. He also points out the gold price is hovering at about $3000 an ounce compared to about $900 an ounce when he started out at Saracen.

Peter and Chris Lalor founded the third and final iteration of Sons of Gwalia in the early 1980s, and turned the listed company into one of Australia’s biggest gold producers at its peak. Things went badly in the mid-2000s.

Early bets

In its heyday, Sons of Gwalia was the world’s biggest supplier of tantalum to the electronics industry. Most of it came from Greenbushes, whose abundant lithium was largely ignored.

Greenbushes is now considered the world’s best hard rock lithium mine and is owned by New York-listed battery chemical giant Albemarle, China’s Tianqi and its partner, IGO Limited.

In 2002, the late Peter Lalor said there was no magic in “new metals” after having his fingers burnt on a mistimed lithium venture once.

Hype around lithium and its use in ceramics, glass, speciality steels and even treating bipolar disorder in the 1990s had compelled Sons of Gwalia to build a lithium plant next to the Greenbushes tantalum plant.

Lalor described how a rival producer out of Chile ruined his plans to dominate what was then a small global market in lithium.

“They had a much lower cost of production and, basically, we were not competitive,” he recalled. “It was essentially a better ore body in the form of a brine deposit, which meant the lithium was recovered in an evaporative process. A hard-rock ore body can never compete with that.”

The brine versus hard rock debate rages today, but these days the big players Albemarle, SQM, and future partners Livent and Allkem, keep a foot in both camps.

Rio too; it acquired the Rincon brine project in Argentina for $US825 million last year and hasn’t given up hope on the Jadar lithium-borates project despite Serbia revoking its licences and approvals in January last year.

Living in Serbia opened Marnie’s eyes to the pace of electrification in Europe. “I really got to understand the importance of batteries for the energy transition and became very passionate about it,” she says.

“We as an industry have a role to play to show how mining can be done well, and how we minimise the impacts and how important it is to the future.”

Small world

Raleigh bumped into old mate and Northern Star chief executive Stuart Tonkin, another WA School of Mines alum, on the streets of Kalgoorlie.

“Stu goes, ‘I always suspected Marnie was better and smarter than you, and now it’s been confirmed’,” he recalls. “I said, ‘Mate, I didn’t have to suspect it. I’ve always known it’.”

Raleigh, who turns 45 in November, says their professional paths are likely to cross in either an executive or non-executive capacity somewhere down the track after the near-miss at Northern Star.

“We do talk a lot about what she is seeing and thinking and ditto for me. We sort of mentor each other in lots of ways, provide support and spitball different ideas,” he says.

Marnie says Raleigh didn’t apply himself in the classroom but had a lot of fun. His boarding school encouraged him to get an apprenticeship, and their father suggested the army.

His second job, after Gwalia, was working part-time at the Superpit.

“One thing Ral and I absolutely share is a passion for people, and we’ve got very similar leadership styles. We just apply them in different types of companies,” Marnie says. “We do talk a lot about leadership.”

Will they ever work together? “You never say never,” Marnie says. “If you’d told me five years ago, ‘You’ll be managing director of battery minerals for Rio Tinto and sitting on the Northern Star board’, I would have laughed.”

--- end of excerpt ---

See Also: Appointment-of-Non-Executive-Director-Marnie-Finlayson-to-NST-Board-13-09-2022.pdf

In summary: NST has very good and highly-competent Management and a very experienced Board, Chaired by ex-Wesfarmers' Michael Chaney, who are focussed on superior shareholder returns and have a superb capital allocation record compared to most of their peers in the industry.

To quote Chaney in his Chairman's address at their AGM last week: "The company has many attractive features: high quality assets which generate strong cash flows, with realistic growth opportunities and long mine lives; a strong balance sheet; skilled operational and entrepreneurial management and a highly skilled workforce."

I agree with that assesment by Michael.

Disclosure: I hold NST and GMD shares. (Not RIO, sorry Marnie!).

Stuart Tonkin, NST's MD & CEO with Michael Chaney, their Board Chairman.

Directors & KMP | Northern Star (nsrltd.com)

10-June-2024: Update:

Marked as stale again - raising the TP by 50 cps to $15.75. They recently tagged my previous target price of $15.25 and then dropped back a little. NST are now Australia's largest listed pure-play (so NOT producing gold only as a byproduct of other production) gold producer that is HQ'd here in Australia.

Newmont GoldCorp (NYSE: NEM and NEM.asx CDI) is the largest constituent of the Australian Gold index, but it shouldn't be, as it's a US company, not an Australian company, but it still has a fair whack of Aussie holders because they received NEM shares in exchange for their Newcrest Mining (was NCM.asx) shares last year when Newmont acquired Newcrest last year.

So NST is the second largest constituent of the Aussie gold index, the largest Australian gold producer, and is one of the top 10 gold producers in the world now, and they expect to be in the top 5 once the KCGM (super pit) expansion is complete in a couple of years.

The next largest Australian gold producer is Evolution Mining (EVN) who also produce a lot of copper now, so they are really a gold/copper producer particularly as two of their mines produce far more copper than gold. If you're bullish on copper AND gold, then EVN could be a good way to play that, but I'm cautious on copper in the near term and bullish on copper longer term, so I'm not in EVN now, but likely will be when I get more bullish on copper - I'm always bullish on gold.

I'm always in NST however, in my SMSF, in my largest real life portfolio and of course here on SM as well. The management premium came out of the NST share price when Bill Beament left to head up Venturex, now called Develop Global, however Stuey Tonkin was there as CEO for years when Bill was the Executive Chairman and Stuey is running NST now pretty much as it was run under Bill Beament, so there hasn't been a noticable change in management style, to me at least. And they've got a steady hand as Board Chairman in Michael Chaney.

The bull case for NST is that they are still the best run gold producer in the world, they have some of the best longer term TSRs of ANY company listed on the ASX, they now have scale (being a global top 10 player and getting bigger), the management have skin in the game and run NST as a business first, and a miner second, so they look after their shareholders, and they have the tailwind of a rising gold price as well.

That's the US$ gold price on the left, and the A$ gold price on the right, obviously the changes in the exchange rate between the U$ and A$ makes a difference, but not a huge difference over the long term, the overall trajectory is north east for both. Not in a straight line, but north east nonetheless.

Gold isn't for everyone, and even if you want some gold exposure in your investment portfolios, you can always go with physical gold either through actual gold bullion, or a gold bullion backed ETF (I recommend PMGOLD, backed by gold bullion at the Perth Mint) - although those are really ETPs - exchange traded products - rather than pure ETFs - exchange traded funds. Or you can go for leverage through a higher quality gold producer. It doesn't always work this way, but the idea is that because the gold producers own SO much gold - the majority of it still being underground and unmined - their share price CAN rise more in percentage terms than the gold price when the gold price rises, and they can certainly fall more in percentage terms than the gold price when the gold price falls. The share prices of Australian gold producers HAS been rising along with the gold price, but in percentage terms they have mostly underperformed, so more than a few commentators are now saying that the gold producers' share prices still have some catching up to do.

One of the reasons I've heard lately why the gold producers are not trading higher than where they are is that rising interest rates are generally expected to present a headwind for the gold price so people were sceptical that the gold price rise was sustainable in a rising interest rate environment. However, most commentators also now agree that we are closer to the end of the rising rates cycle than the beginning, so falling interest rates are not too far away, and falling interest rates SHOULD present a TAILWIND for an already very high gold price - i.e. it should actually go higher still.

Of course there are plenty of other factors that play into the gold price and as we have mentioned here recently, trying to predict gold price movements is generally a waste of time because it's almost a coin flip in terms of whether you will be right or wrong, so in that light I suggest just backing the best management teams in the space, because really good management plays a VERY important role in the performance of all mining companies, particularly gold mining companies. And that's because gold mining is really a series of capital allocation decisions, and as a management team, if you get those right, you'll probably do well, but if you get those wrong, you'll lose money, and so will your shareholders if they stick with you.

Of course grades, location, infrastructure, regulatory environments, macro factors, ore consistency, geology, plant chemistry, plant reliability, breakdowns, weather events, natural disasters, consumables and employee availability, contractor performance and reliability, the gold price, etc. all play their part as well, but do NOT underestimate the importance of management.

The thing is, we can't accurately predict most of the other stuff, but we can get a fair idea of management competency based on past performance. And while past performance may not be an accurate indicator of future performance, it's absolutely worth considering, in my opinion.

And NST has good management. They had great management when Bill B was there, but they still have good management. Possibly great, but good at the very least. In terms of Australia's larger gold miners, NST is right at the top in terms of quality and performance, and that's why I hold them.

27-Oct-2024: Update:

Nothing has changed with NST except the gold price, which has just broken through A$4,000/ounce (last week) with continued momentum. I am therefore raising my price target for NST to just under $20, because they are worth more with a higher gold price, and especially when their KCGM (Super Pit) expansion is complete because it's their biggest mine and mill (processing plant) and they are doubling its annual production capacity, which they believe will propel them from their current status as a top 10 global gold producer to being a top 5 global gold producer.

That means top 5 in terms of both market cap and annual gold production. Now the gold production part is on-track - that relies simply on their succesful completion of the Super Pit / Fimiston Mill upgrade and then succesful ramp-up to its new nameplate capacity, which is due in CY 2026.

The other part is of course the market cap, and that doesn't depend on a multiple expansion so much as the market recognising that a company that produces more gold, profitably, is worth more, so the significantly higher gold production that NST is going to achieve within 2 years from now most likely - is going to mean they are going to produce significantly higher cashflow and profits, so they will get priced accordingly - and we're seeing that start to happen now.

On Friday (25-Oct-2024) NST made a new all-time high of $18.32 before closing at $18.29, the highest closing share price in their history. And that SP rise is due to three main factors:

- The gold price making new record all-time highs;

- NST being Australia's largest gold producing company; and

- NST being in the middle of a significant growth project, being the doubling of annual production capacity at their largest gold mill, which they believe will see them land within the top 5 largest gold producers on the planet when it is completed and the mill is running at nameplate capacity, being top 5 in terms of gold produced p.a. AND in terms of market capitalisation.

So, yeah, I hold NST shares, both here and in my SMSF.

27th April 2025: Update:

NST closed this past week @ $20.84, after hitting an all-time high of $23.30 intraday on Tuesday (22nd April 2025; they closed a little lower at $23.01 that day).

They've blown through $20/share on the back of the sharply rising gold price and Trump's tariffs and other policies causing multiple negative sentiment shifts, including declining sentiment around the stability of the US$ as the world's reserve currency in future years, declining sentiment around US and global growth in the near to mid term, and declining sentiment around how dependable US Treasuries are likely to be under Trump 2.0.

US Treasuries are government debt securities issued by the US Department of the Treasury to finance government spending, so they represent loans from investors to the US government, and come in different forms like Treasury bills, notes, and bonds, each with varying maturities. Treasuries have generally been considered a safe investment due to the US government's ability to tax and raise money by other means, making them popular among investors.

What's changed is that while Trump's Rebublican party, a.k.a. the Grand Old Party (or GOP) clearly want to reduce the enormous US deficit, they are mostly trying to do that by spending less rather than raising more money, in particular they do not want to raise taxes, particularly for the richest people in America; in fact they are still intending to pass tax cuts that include cutting tax for those on the highest incomes. Additionally, Trump and a couple of his advisers seemed hell bent on getting other countries to pay more to America through tariffs, despite the obvious fact that those very tariffs are paid by those who import goods, within America, and are usually passed through to the consumers who buy those products - the end users - they are not paid by the exporters. The people selling goods into America from overseas don't pay these tariffs, they just lose sales because the tariffs that are added to the goods and services as they enter America simply make those goods and service more expensive so arguably less competitive with alternatives.

That's a long paragraph. Not trying to get political here, but the reality is that even if the whole tariff saga was really about trying to strengthen the US position in relation to trade negotiations with other countries, i.e. to force countries to agree to more of what Trump wants from them in exchange for reduced tariffs or no tariffs, the fallout from this so far has been serious loss of faith in the USA as a reliable trading partner with almost everybody else, serious erosion of faith and trust in global trade agreements and norms that had previously been accepted and relied upon, and nothing short of a changing world order where old alliances have fallen apart and new ones either have been or are being formed.

The loss of trust and faith goes beyond Trump, and the USA, and global trade; it extends to global markets, global financial systems, and changing expectations around who and what is going to influence the world order in future years.

If it's all been about negotiating tactics, it's backfired spectacularly and the damage done will either taken many years to repair, where repair is a possibility, and some of it clearly now being permanent.

In terms of what Trump and Musk have achieved in their first 100 days, this MSNBC report sums it up very well: Musk demoted again! Elon retreats as he loses $1 billion PER DAY under Trump [yesterday, 26th April 2025].

So central banks have been buying a lot of gold over recent months, particularly China. I won't get into exactly what the Chinese motivations are likely to be behind significantly increasing their physical gold bullion holdings, but the fact that they have been buying is just that, a fact, and that's been a major driver of the gold price, which has been on a tear. It's down -6% from it's recent peak, but that's likely a small pause in a longer uptrend:

The gold price in both A$ (left side) and US$ (right side, above) is down over the past day and the past week, it's still up for the past 30 days, and all timeframes beyond that. It hasn't broken that uptrend yet.

And despite NST's SP being up +38% over the past 12 months, thrashing the All Ords Accumulation Index (XAO, up by just under 5%) and the ASX200 Total Return (TR) Index (XJO, up just over 5%), NST has only been the 6th best performer out of Australia's 7 largest gold companies (the seven largest constituents of the Aussie Gold Index), as shown below:

Even after the pullpack we've seen in all of the larger gold companies' share price over the past week, the 12 month performance number for the share prices of those 7 goldies are impressive:

- Genesis Minerals (GMD), up +121.65%

- Evolution Mining (EVN, gold/copper miner), up +97.28%

- De Grey Mining (DEG, has just been acquired by NST), up +92.03%

- Capricorn Metals (CMM), up +85.98%

- Perseus Mining (PRU, best of the West African focused gold miners), up +43.10%

- Northern Star Resources (NST), up +38.01%

- Newmont (NEM, CDIs here for US shares; they are listed on the NYSE and are the world's largest gold mining company), up +29.68%.

Newmont is the largest of those, but they are a US-listed and US-HQ'd company with only CDIs here on the ASX for their US shares, despite being one of the largest 3 constituents of the Australian Gold Index.

Northern Star (NST, $24B m/cap) is the largest Aussie Gold company, with Evolution (EVN, $16B m/cap) second and the others a fair way behind in terms of market cap (m/cap).

De Grey (DEG) is the closest at just under $6B, however the federal court last week approved the scheme of arrangement under which NST will acquire all of the issued shares in DEG, so DEG will be absorbed into NST and the DEG ticker code and De Grey as a company will be removed from the ASX list on Tuesday May 6th, in just over one week's time.

The NST offer for DEG back on 2nd December valued DEG at $5 Billion, which seemed like a lot at the time, but De Grey's Hemi is the largest gold development project in Australia (i.e. a project that is not already a producing mine). It's now closer to $6 Billion because it's an all-scrip takeover, meaning De Grey shareholders will receive NST shares in exchange for their DEG shares, and NST shares have gone up +25.6% (over $4 per share) since 2nd December when that offer was made.

Good outcome for DEG shareholders, but arguably also a good outcome for NST shareholders as long as NST don't stumble while taking Hemi through to a producing gold mine.

Raising my PT for NST to $27.30 based on recent upward momentum and the higher gold price.

Disclosure: Of those gold companies discussed above in this update, I hold NST, EVN, GMD, and I did hold CMM but sold all of my CMM last week when they announced their CEO was taking leave after being charged with assault.

I am most bullish on NST and GMD out of those, with EVN in third place.

28th January 2026: Update:

Nothing much to add here really, just chasing the share price up in terms of raising my price targets every 5 or 6 months.

As I explained here today (in a forum post), I can't pick a price target that I have a great deal of conviction on, mostly because I don't know how far and how fast the gold price will rise from here; And there are also company specific factors relating to NST such as how their Super Pit (KCGM) expansion goes, including the integration and ramp up (it's a BIG upgrade), and how fast and how well they can develop Hemi and the other De Grey Mining assets that they acquired last year - which they intend to get stuck into once the KCGM expansion is complete, so Hemi is going to take some years from here. Plenty of growth to come - it's just the execution that is the main unknown relating to that growth, and what the gold price does during that period of course.

They do have good management! I'm backing Stuey Tonkin and his crew at NST.

I'm still a happy holder. They're going higher, I just don't know how high. Or how fast.

The following chart is the MAIN reason why NST has done so well over the past year, so where the gold price goes from here matters a lot to NST's future share price trajectory:

Charts/Tables Source: GoldPrice.org on Sunday evening (25th Jan 2026).

4th August 2025: Investor Presentation - KCGM Site Visit [39 pages]

Today's presso is 39 pages long, so below I'm just going to share the 10 most important slides, in my opinion (as an NST shareholder):

Firstly it's important to understand just how big KCGM (Kalgoorlie Consolidated Gold Mines, being the Kalgoorlie Super Pit and the Fimiston Mill and surrounding tenements) is, and why it is NST's key global asset:

Next, here's a breakdown of exactly where NST are in the multi-year upgrade of Fimiston (the KCGM gold mill) which they are expanding from 13 Mtpa to 27 Mtpa, so more than doubling its annual ore processing capacity:

The following slide has to be understood in the following context: Back when Bill Beament was running NST, he developed a really good internal mining services arm that allowed NST to be owner-operators without needing to employ contract miners. Bill came from a mining services background before he took over NST and built it up to be Australia's second largest gold mining company, behind Newcrest which was then acquired by US-based Newmont, so NST is now Australia's largest gold miner.

Not only were NSMS - Northern Star Mining Services - competent, they were actually better, cheaper, and faster than many of their competitors in the Australian gold sector. This slide shows just how much better KCGM underground has been performing since NSMS took over the actual underground mining - it's impressive:

The summary (page 35):

And their FY26 guidance:

Disclosure: Holding.

The market likes it - NST is up +5.88% today to $16.20 (up 90 cents today) - so far - with over 2 hours left in the trading day.

It's is a good day on the Aussie market for the Aussie Gold Sector, with most goldies in the green. In fact there are around 8 companies that are up even more than NST are:

Good to see more green on the screen after a string of red days across the sector recently. Plenty of market/price-sensitive news in the Aussie Gold Sector today, and it's mostly good news.

That's just the top 11 performing Aussie gold companies today, there are around another 50 Aussie gold companies not shown there.

Note: For proper context of the slides in this post, please see the entire presentation:

4th August 2025: Investor Presentation - KCGM Site Visit [39 pages]

Saturday 7th June 2025. A wet and windy day in Adelaide and I'm getting over the flu, so have been sitting in my office with the heater on eating reheated Mexican food, soup and porridge (not in that order) and enjoying MoM's deep dive into the history of Australia's largest gold miner, Northern Star Resources (NST) that MoM released 1 hour ago (earlier this arvo).

How Northern Star Became Australia’s Biggest Gold Miner, Money of Mine, Jun 7, 2025

[Money of Mine Podcast]

[Money of Mine Podcast]Show notes:

How does a shell company turn into Australia’s biggest gold miner, capped at nearly $30 billion?

In this episode, we unpack the fascinating story of Northern Star — from 2c a share to over $20, securing world-class assets across multiple continents, including the Australia’s greatest gold mine, the Super Pit.

We trace the company’s journey, get in the weeds on their M&A approach, and highlight the characters who shaped it — with a focus on the early days at Paulsens, the deal that set Northern Star on its path, and culminating with the coronation of the “King of Kalgoorlie.”

THE DIRECTOR'S SPECIAL

Join 12k+ subscribers to the Director’s Special: one daily email with all the news that matters in mining

https://www.moneyofmine.com/subscribe

-------------------------------------------------------

▶️ CHAPTER TIMESTAMPS

00:00 Introduction

04:05 Paulsens

30:10 Plutonic

34:11 East Kundana & Kanowna Belle

42:57 Jundee

57:18 South Kalgoorlie

58:50 Pogo

1:10:48 Echo

1:13:15 Super-Pit

1:19:18 Saracen

1:25:27 Learnings

1:36:59 Shout out

-------------------------------------------------------

--- end of show notes ---

Here's a small transcript from near the beginning:

"In May 2010, they come out with an announcement that they're going to acquire the Paulsens Gold Mine; The company has a mighty market cap of under $8 million, and the share price is four and a half cents, so... how's that for a starting point?"

--- end of transcript ---

For those who may not be aware, Bill Beament, prior to becoming the MD of NST, which was just a shell at that point (and later becoming it's Executive Chairman when Bill brought Stuey Tonkin across to NST and made him CEO in Nov 2016), held several senior management positions, including General Manager of Operations for Barminco Limited with overall responsibility for 12 mine sites across Western Australia; Bill had also been the General Manager of the Eloise Copper Mine in Queensland.

At Barminco, Bill was responsible for Barminco's mining services (contract mining) contracts at 12 mines, and one of those 12 was Intrepid Mining's Paulsens gold mine, and Bill clearly thought he could run that mine a lot better than Intrepid (the mine owners) were at that time. Intrepid Mines had deprioritised Paulsens in favor of Indonesian projects where they thought they'd get more bang for their bucks. Intrepid were therefore not spending the money at Paulsens to define how far the gold extended or even to run the mine efficiently as it was.

This proved to be a disastrous decision for Intrepid, whose experience with Indonesian mines, specifically the Tujuh Bukit project, was marked by significant disputes and ultimately, a loss of control over the project. While the company initially made promising discoveries and saw potential in the region, it faced challenges with its local partner and legal issues in Indonesia, leading to a major loss of investment, and a protracted legal battle, and accusations of fraud, severely negatively impacting shareholder value and leading to a CEO resignation.

Intrepid Mines Limited ultimately merged with AIC Resources in 2019, becoming AIC Mines. This followed a failed takeover offer by Intrepid for AIC.

Meanwhile, the gold mine that Intrepid Mining were happy to divest back in 2010, Paulsens, did VERY well under NST ownership, and is still being mined today, this time by Black Cat Syndicate (BC8) who bought the mine from NST in 2022 and have extended its mine life through successful regional exploration in the surrounding area within tenements that they (BC8) own.

However, back in the day, from 2010, Paulsens became the foundation of NST's extraordinary success that today sees Northern Star with a share price of circa $21/share, a market capitalisation of $30 Billion, being an ASX50 company, Australia's largest gold miner, and one of the 10 largest gold mining companies in the world, and the only Australian-domiciled gold miner in that list.

And they are certainly still growing - they're in the middle of doubling the mill capacity at Fimiston (the Super Pit, a.k.a. KCGM), and have bought De Grey Mining for $5 Billion recently, so NST now own Hemi, the largest known undeveloped gold deposit in Australia.

It's quite a story and well worth a listen/watch: How Northern Star Became Australia’s Biggest Gold Miner [MoM podcast, Saturday afternoon, 7th June, 2025]

Disc: Yes, of course I hold NST shares! [both here and in my SMSF]

02-Dec-2024: NST’s $5B Deal: Most Expensive Undeveloped Gold Mine Ever (Money of Mine podcast)

"There’s only one thing to talk about today… Northern Star’s big swing for De Grey. This friendly, all-scrip deal which implies a A$5b value for the developer of Hemi is the biggest deal of its kind, so we’ve got plenty to chat about."

CHAPTERS

0:00:00 Introduction

0:01:40 NST make $5b move for DEG

0:08:21 Will Gold Road get in the way

0:13:23 How does Hemi fit into NST

0:22:03 Hemi's met

0:35:12 Thoughts on the deal

DISCLAIMER

All information in this podcast is for education and entertainment purposes only and is of general nature only.

The hosts of Money of Mine (MoM) are not financial professionals. MoM and our Contributors are not aware of your personal financial circumstances. Before making any investment decision, you should consult a licensed financial, legal or tax professional.

MoM doesn’t operate under an Australian financial services licence and relies on the exemption available under the Corporations Act 2001 (Cth) in respect of any information or advice given. MoM strive to ensure the accuracy of the information contained in this podcast but we don’t make any representation or warranty that it’s accurate or up to date. Any views expressed by the hosts of MoM are their opinion only and may contain forward looking statements that may not eventuate.

MoM will not accept any liability whatsoever for any direct or indirect loss arising from any use of information in this podcast.

--- ends ---

[I do currently hold DEG and NST, but not GOR]

02-Dec-2024: Northern Star agrees to acquire De Grey.pdf

And: Presentation - Northern Star agrees to acquire De Grey.pdf

Details of this deal:

- Northern Star agrees to acquire De Grey by way of a recommended scheme of arrangement, with De Grey shareholders to receive 0.119 new Northern Star shares for each De Grey share held; and

- De Grey’s flagship project, Hemi, provides Northern Star with an additional Tier-1 future low-cost production centre, aligning to its strategy to deliver superior shareholder returns.

A Tier-1 gold asset is defined as an operation producing in excess of 500kozpa of gold per annum with a 10+ year mine life.

At 1:42pm Sydney time, DEG is trading up +26.45% (or +40.2 cps) @ $1.922 and NST is trading -7.37% (down -$1.29) @ $16.22.

I have to do some work on whether the price paid is reasonable here, but as an NST shareholder I am encouraged that NST have used their scrip for this deal rather than cash, so this doesn't result in any change to their cash or debt positions.

This deal (0.119 new NST shares for each DEG share) represents an implied offer price of A$2.08 per De Grey share and a total equity value for De Grey of approximately A$5 billion on a fully diluted basis, based on the closing price of Northern Star shares of A$17.51 on Friday (29 November 2024) - obviously a bit less now since NST's share price has dropped today.

The Scheme is unanimously recommended by the Board of Directors of De Grey, and each De Grey Director intends to vote all De Grey shares that they hold or control in favour of the Scheme, in each case, subject to no Superior Proposal (as defined in the SID - Scheme Implementation Deed) emerging and the Independent Expert concluding (and continuing to conclude) in the Independent Expert’s Report that the Scheme is in the best interest of De Grey shareholders.

The Scheme Consideration represents a significant and attractive premium of:

- +37.1% to De Grey’s last closing share price of A$1.52 per share on 29 November 2024; and

- +43.9% to De Grey’s 30-day volume-weighted average price of A$1.45 per share up to and including 29 November 2024.

Upon implementation of the Scheme, Northern Star shareholders will own approximately 80.1% of the combined Group and De Grey shareholders will own approximately 19.9%.

Here's the 5 year SP graphs of both companies up until today:

Here's the important stuff (IMO):

So NST's Ore Reserves increase by +29% to 26.9 million ounces, and their Mineral Resources increase by +22% to 74.9 million ounces.

Low cost - Hemi should be in the lowest quartile of the AISC (cost) curve.

Consistent with NST's purpose of generating superior returns for shareholders.

So, I'll have a think about the price, but at this stage, I'm happy enough with this as an NST shareholder.

Thursday 22-August-2024: FY24 Financial Results

Results Presentation for Year Ended 30 June 2024

Also: Northern Star - delivering on our commitments - Diggers & Dealers Presentation, August 2024

https://www.nsrltd.com/investors/presentations/#type=Presentation

https://www.nsrltd.com/investors/asx-announcements/

https://www.nsrltd.com/investors/

Disclosure: Yes, I hold NST shares.

And so does Marcus Padley's "Growth Portfolio" (managed fund) as from today (Monday 26th August). Here's his commentary on Friday:

- Northern Star Resources (NST) – One of our favourite gold plays along with EVN (NST is less volatile than EVN, daily ATR of 2.3% vs 3%). NST reported yesterday, rising 3.2% before losing morning gains to finish up 1.7%. The results either meeting or beating broker expectations. Record cash earnings of A$1.8bn, 1,621koz of gold was sold at AISC of A$1,853/oz, meeting its FY24 guidance. The outlook included gold sales of 1,650-1,800koz at an AISC of A$1,850-2,100/oz. Solid numbers but results for commodity stocks are less important compared to companies like WTC or BXB (covered yesterday). The biggest share price driver by far is the gold price which has been hitting one record high after another this year. Our gold price outlook is that despite being at record highs if bond yields continue to fall the gold price will continue to rise, supported by ongoing central bank buying around the world. Commodity stocks can be risky, there is every possibility of a 10-15% dip along the way but for a long-term holding it’s a buy. Will add to the Growth Portfolio with a 5% weighting on Monday provided Powell doesn’t do anything to scare the market tonight.

Source: https://marcustoday.com.au/

So he's adding it based on technicals and momentum. I hold it because it's Australia's largest gold producer and a very well run company. Here's some excerpts from their FY24 results summary announcement.

Under Bill Beament as Executive Chairman back when he was still at NST, he always said they ran the company as a business first and a miner second, so profitability and shareholder returns were what their decisions were based on.

Stuey Tonkin was their CEO under Bill and he's now their MD as well, and he's carrying on that same tradition.

In Summary: Why I hold NST:

- Australia's largest and best gold exposure (Aussie HQ'd and their primary listing on the ASX);

- Profitable, with plenty of growth, particularly the KCGM (a.k.a. the Super Pit/Fimiston Mill) mill expansion, underway right now;

- A$2.7 Billion of liquidity including 30 June cash and bullion of A$1,248 million with net cash of A$358 million, plus during the year, they refinanced their corporate bank facilities with maturity dates of December 2027 and December 2028 across two equal tranches totaling A$1.5 billion, which remains undrawn at year end, and which along with their cash and bullion, provides liquidity of A$2.7 billion leaving the Company very well-funded;

- Zero net debt;

- On top of what they already own and operate, which is very substantial, NST have guided for $180 million just for Exploration expenditure in FY25, so there's certainly plenty of further potential upside from that as well;

- Despite higher costs at Yandal (which is still profitable), NST's group AISC remains competitive, particularly considering their size and the fact that they aren't relying on hundreds of millions of dollars worth of copper by-product credits to reduce their AISC (yes, I'm looking at you EVN !) - so NST will remain profitable at substantially lower gold prices, and they are controlling their costs reasonably well (considering the inflationary environment they've been exposed to in terms of mining and engineering sector costs); and

- I like Stuey's management style - low profile, but gets the job done.

02-May-2024: Annual Resources, Reserves and Exploration Update [489 pages]

Market Like.

NST closed at $15.10 on Friday and have been down every day this week (Mon, Tues & Wed) prior to today (Thurs 2nd May), with the worst day being yesterday when NST's SP dropped -51 cents (-3.41%), so good to see some claw-back today on the back of this annual Reserves, Resources and Exploration update.

Since that low point in early October (@ around $10/share), NST have been in a decent uptrend, which is not surprising given what the gold price has done and that NST is Australia's largest gold mining company.

Some people may think gold has peaked for now based on yesterday's sector sell down...

Source: MarcusToday daily EOD newsletter yesterday, Wednesday 1st May 2024.

But today Gold and Financials are the best sectors - leading the market back up.

Source: MarcusToday, mid-day email, Thursday 2nd May 2024 [so middle of the trading day snapshot]

Consumer Staples are the worst sector today mostly due to the market selling Woolies (WOW) down by around -4% on the back of their Third-Quarter-Sales-Results.PDF.

The gold price has certainly dropped back from its recent all-time highs, but I doubt that the rally is done yet, I would expect this is more a pause in a continuing uptrend. But you never know.

11-Apr-2024: NST-Operational-Update.PDF

Source: Commsec.

Nice Update (below, link above), nice chart, onward and upward.

Cost guidance (AISC) up, but gold production guidance of 1.60-1.75Moz maintained, despite the bad weather around Kal in April and March affecting production. They produced 1.18Moz in the first 9 months of this FY (to March 31st), so they only need to produce 402koz in the final quarter to hit the bottom end of that full year production guidance. And they produced 401koz in the March quarter despite the weather. Additionally they expect a strong June quarter, with increased grade and improved mill utilisation rates.

Northern Star Resources (NST) is Australia's largest listed gold miner headquartered in Australia, and Australia's best gold miner by a country mile. The market weren't too interested in them after Bill Beament left to head up Venturex (now Develop - DVP), but the market is coming around now - because with the gold price hitting new all time highs now on a regular basis, and NST being so big and dominant in the sector, and performing well too - producing so much gold at reasonable costs (remembering that costs have increased for every gold miner), NST is hard to ignore. They will also be an obvious play for international money looking to find some exposure to the sector, because NST is now one of the top 10 gold mining companies in the world (see here: Largest gold mining companies by Market Cap (companiesmarketcap.com)) and the 34th largest mining company (across ALL commodities) in the world (see here: The top 50 biggest mining companies in the world - MINING.COM 05-April-2024).

NST also operate one of the 10 largest gold mines in the world (the Super Pit, next to Kalgoorlie) - see here: Here are the top 10 largest gold mines in the world (miningreview.com) - and one of the two largest gold mines in Australia - the Boddington Gold Mine (owned by Newmont GoldCorp) is the other one.

The "Super Pit".

NST have stated (see here: Northern Star Resources approves $1.5 billion upgrade to KCGM's Super Pit Fimiston processing plant - ABC News 22-June-2023) that they believe that with the increased capacity, the Super Pit is primed to supersede Boddington Gold Mine as Australia's largest gold operation and join it as one of the top five gold producers (mines) in the world by 2029. And that will propel NST further up the world rankings in terms of top 10 global gold miners. Depending on what sources you use and the recency of the reporting, NST sits somewhere between 7 and 11 currently, however I believe they will be at #6 by 2030, and possibly higher if there is further M&A within the current top 6.

So the target is that NST will be a top 7 gold miner (likely #6 IMO) and be operating one of the world's largest 5 gold mines by 2030. Could be sooner than that depending on progress with the Super Pit expansion. It is already underway and due for completion in 2029, with full ramp-up being completed in 2030.

In June last year (see here) they said they had 120 million tonnes of pre-mined ore, estimated to hold about 3 million ounces of gold, at the Fimiston Mill (a.k.a. the Super Pit mill), and their chief technical officer (CTO) Steven McClare said that stockpile would be a "key feed source" for the new mill and provide certainty for the miner. Steve said, "If we stopped mining today, we could process that material and it would take more than nine years to actually get through that stockpile."

And they didn't stop mining obviously, so the stockpile continues to grow due to the current capacity constraints of the existing mill, however they are spending $1.5 Billion to upgrade that mill from 13 million tonnes a year to 27 million, so more than doubling annual ore processing capacity. And that is just ONE of their gold mines.

Disclosure: I hold NST shares, both here and in my largest two real money portfolios.

The announcement looks innocent enough but it has wider implications for the valuation of NST

Anyone who studied finance probably would have come across the concept of WACC or Weighted Average Cost of Capital.

This is basically the weighted sum of the cost of debt and cost of equity before tax as proportion of market value of debt and equity. You can look up the formula on the internet.

But in simple terms and from my basic understanding of debt and assuming NST had a higher cost of debt of more than 6.5%, locking in these senior notes in a period of rising interest rates would have the affect of lowering their cost of debt and therefore WACC and it would explain why the share price has rallied in the last week. Since lowering the cost of debt would decrease WACC and in effect increase the NPV of NST. This is not even accounting for what they plan to use the debt to increase shareholder value.

Probably the slight negative on this is that this will also increase the enterprise value.

I was a bit slow to act on this announcement and already had my NST proceeds deployed elsewhere.

For those who want to see the numbers, here is my rough sensitivity analysis of NST NPV/sh versus Gold Price (AUD)

Applying discount of 8% (ie: Disc factor 1.08). I should try and work out the correct WACC for the discount but takes more time to calculate and probably the only flaw in the below model. So I may have overstated the discount value - who knows.

We've only had a spike over 2780 for about a few weeks before the gold price crashed back down to the current level of 2703 AUD

In addition to @Bear77 updates. Going to put this here so it is easier to read and discuss

Pogo: Jury is still out on AISC and production guidance, but heading in the right direction. AISC guidance US$1,300 - 1,400 US/oz (1,857 - 2,000 AUD/oz). FY23 Prod guidance 240-260koz

Yandal: AISC slightly up. Guidance 1,525 - 1,625 AUD/oz. FY23 Prod guidance 480 - 520

Kalgoorlie: AISC pretty much flat. Guidance 1,560 - 1,660 AUD/oz. FY23 Prod guidance 820 – 870

Kalgoorlie: AISC pretty much flat. Guidance 1,560 - 1,660 AUD/oz. FY23 Prod guidance 820 – 870

Overall performing as expected. Only shining light is KCGM (Kalgoorlie). Pogo still a bit of a concern. Yandal might just scrape through for FY23.

Enough of a hold for me. I did contemplate selling out at one stage for maybe one of the Strawman "favourites" (ie: AD8, CGS etc...) but seems gold has been trending up. Will ride out for now until I find something else.

Will be interesting to do a DCF valuation in the same way I do Capricorn Metals. I also noticed NST trades at a higher multiple than Capricorn (CMM) although Karlawinda reserves are 13 years.

[held]

Looks like the buyback is just a drop in the ocean for now. Still 1.16b shares outstanding. Halfway through the buyback

15m out of 39m bought back so far.

Question is whether NST will continue or pause the buyback.

KCGM Mill Expansion PFS Update

Going briefly through the slide deck and the announcement, it is not clear why they looked at full rebuild option (22mtpa) as CAPEX is more and IRR is less. Will hazard a guess the rebuild would be the less complex option.

Also there is no figure for the NPV.

Looks good on paper. But the study looks very generic and not much detail. I suppose we may get another update soon. I'm yet to listen to the recording or see the transcript.

06-May-2022: (Friday): Interesting ABC News article on Wednesday (04-May-2022): Miner Northern Star Resources strikes gold beneath Kalgoorlie's Super Pit - ABC News

Plain Text: https://www.abc.net.au/news/2022-05-04/gold-miner-drills-beneath-kalgoorlie-super-pit/101035098

Miner Northern Star Resources strikes gold beneath Kalgoorlie's Super Pit

ABC Goldfields / By Jarrod Lucas

Posted Wed 4 May 2022 at 3:05pm, updated Wed 4 May 2022 at 3:23pm

Underground access was restored from within the Super Pit last year through a portal on the western wall. (ABC Goldfields: Jarrod Lucas)

It has been described as the "first glimpse" of a new world-class gold system beneath Kalgoorlie's famous Super Pit.

Despite more than a century of mining on the historic Golden Mile, there has been limited exploration outside of the rich deposits which have yielded more than 21 million ounces since the Super Pit began production in 1989.

Underground access portals on the western wall were developed last year to provide new drilling platforms for testing north-west of the existing pit.

The work represented the first significant underground mining activity on the Golden Mile in more than 30 years.

The investment by Perth-based gold miner Northern Star Resources is starting to pay off after it said it hit pay dirt.

In the company's annual reserves and resources statement to the ASX this week, Northern Star said drilling had increased the underground resources 20 per cent to 5 million ounces.

Northern Star Resources chief operating officer Simon Jessop inspects the entrance to the new underground portal inside the Super Pit in May last year. (ABC Goldfields: Jarrod Lucas)

Northern Star managing director Stuart Tonkin said the portals had been developed 1.5km in length and drilling only began last November.

"It's really not been a lot of time drilling and we're obviously continuing to drill now," he said.

"But we've already added a million ounces of inferred material."

He said there was 5 million ounces of Fimiston underground resource.

"So again it shows us the thin end of the wedge," he said.

"That investment is starting to show great signs of where the future can be underground there."

Deepest workings 1.4km underground

More than 3,500km of tunnels and shafts have been created underneath the Super Pit — equivalent to driving from Perth to Sydney- in a century of mining the area.

The deepest historical workings extend about 1400m below the surface.

But drilling has hit gold mineralisation as deep as 2km below the surface.