Consensus community valuation

Symbio released its FY23 report

Revenue:

Receipts from Customer

Operating Profit

Singapore Updates

Key Matrics for each division

My View:

- Results aren't as great and as expected from their first half ( where they flagged inventory returns from their mega customers because of the economic conditions).

- That flagged there is pressure in the CPaaS division margin because of cost-cutting from customers and increased competition in the Australian market

- They are more focused on recurring revenue ( and there are certain legacy services that they have discontinued) following graph shows how Recurring Revenue/margin and Variable revenue/margins are tracking

There is a current acquisition discussion going from Superloop to symbio and that exclusivity has been extended for a further 2 weeks - Which is probably what is supporting the share price at the moment. ( I would have thought the market wouldn't like this result)

Symbio received a non-binding indicative proposal from Superloop to acquire all of the shares valuing Symbio at $2.85 per Share + Special Dividend with franking credits of $0.15 per share. i.e. total $3 per Share.

In the same announcement, it announced it's on track to achieve FY23 EBITDA at the upper end of its stated guidance in the range of $27m to $28m.

My View

- At $3, Symbio's market cap is roughly around $260m

- It probably has ~$35m cash so EV = $225m

- Symbio has gone and changed its business significantly in the last 3 years ( it divested all declining businesses and invested heavily in growth businesses and expanded in Singapore and Malaysia) and its almost finished with its investment cycle.

- I think $3 doesn't reflect the potential earning growth Symbio has in front of it

- I don't think this deal will be done at $3 ( There is significant holding from insiders and they will definitely look after the Shareholder's interest in my view). There can be potentially competing proposals from other companies (maybe AussiBroadband locally or Bandwidth (NASDAQ:BAND or similar).

- I would much prefer it not to be acquired and if it has to then it should be acquired by Company focusing on Telco Software rather than pure Telco.

In any case, I am looking forward to 25% paper gain tomorrow. Although $3 barely puts me in the green ( would be very annoyed if this deal gets done - mainly because I invested so much energy/time/effort understanding ins and outs of this business - that all will go to waste.

Symbio announced a very disappointing result for FY22. - Well, if you have read my straw earlier then I have documented that Aussi Broadband (ABB) acquired Over the wire (OTW) and decided to move its business from Symbio to Over the Wire for voice traffic to get synergy from the acquision.

It was well understood that this FY22 result would be affected by ABB and OTW consolidation. However, being upfront about that management just excluded Service In Operation (SIO) for ABB from the chart and gave the impression that growth is normal (shareholders should ignore churn).

- FY21 Presentation TaaS Service in Operation (SIOs) graph ( Check FY20 numbers and FY21 Numbers)

FY22 Presentation TaaS Service in Operation (SIOs) graph ( Check FY20 and FY21 Numbers) - Wha they did is removed the number from lost customer.

Aussie Broadband announced to market following. ABB has moved its voice traffic from Symbio to the Over The Wire voice network.

Its a tailwind for Symbio - However, Symbio confirmed their EBITDA guidance not that long ago so I would suspect it must have got growth to cover for this loss somewhere.

As preparation for reporting season, I just reviewed my thesis and noted down things at a high level I am monitoring for this business going forward. I expect Revenue and EBITDA to decline ( because of divestment of Direct business as well as 11.1m investment Management has flagged for FY22). Should the following things be tracking well in the right direction and because of known expected Revenue and EBITDA decline stock sell-down, I shall be prepared to buy more IR.

- Recurring Revenue and Margin growth

- Three divisions Key performance indicators

- Singapore momentum

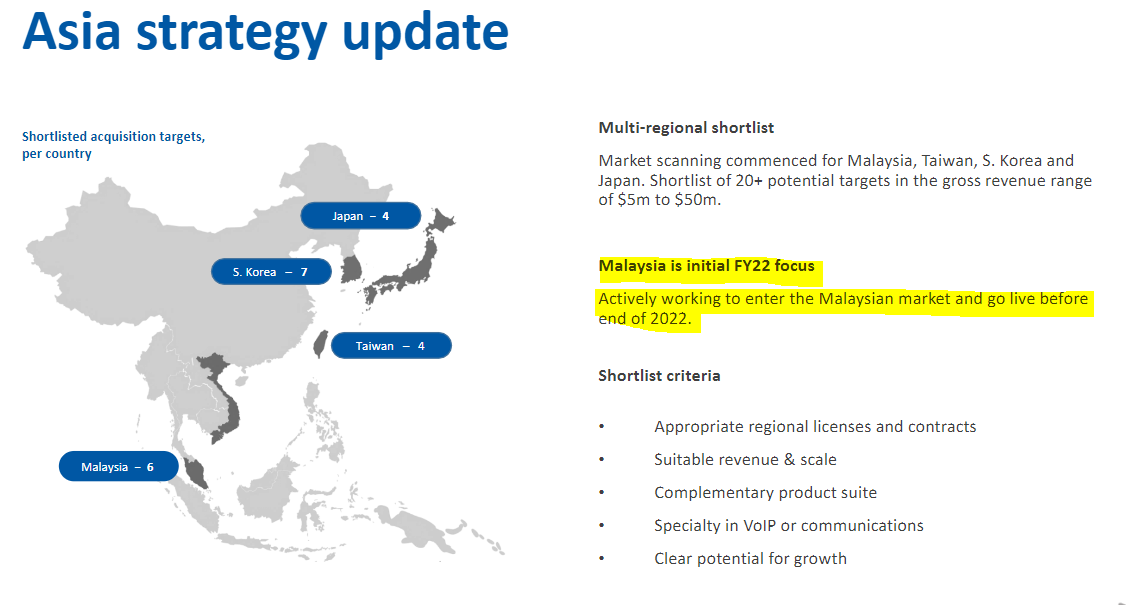

- Malaysia Update

MNF has two types of revenue:

- Variable Revenue

- FY20 - 129.4m with 28% margin (i.e 36.7m)

- FY21 - 105.5m with 32% margin (i.e 34.1m)

- Recurring Revenue

- FY20 - 101.5m with 59% margin (i.e 59.7m)

- FY21 - 113.2m with 60% margin (i.e 68.1m)

If you value business only on Recurring Revenue business -- What multiple would you apply for sticky 60% margin revenue of 113.2m ?

Currently, if you ignore the total variable component (which generates 105m revenue with 34m margin). total business is on multiple of 5.4 X ARR

A major part of revenue drag came from

- Variable revenue from Global Wholesale ( because of lack of international roaming and audio conferencing traffic)

- PArt of this is once-off

- Variable revenue from Direct Segment ( because of declining consumer segment )

- This has been sold now.