Consensus community valuation

$TNE announced their 1H FY26 results today.

Their Headlines

- Profit Before Tax of $89.1m, up 9%

- Profit After Tax of $66.8m, up 6%

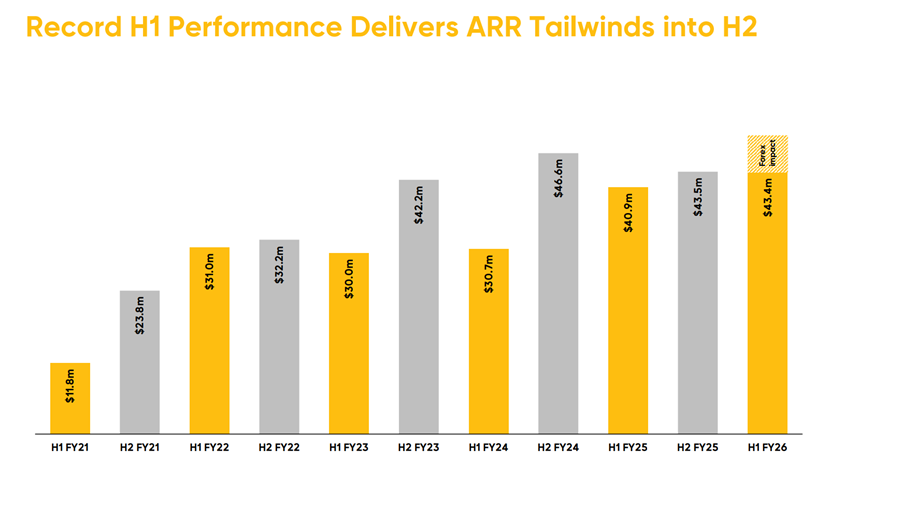

- ARR of $598.0m, up 17%

- Net Revenue Retention (NRR) of 114%

- UK ARR of $53.0m, up 23%

- Rule of 40 result of 55%1

- Record Interim Dividend of 8.0 cps, up 21%

- SaaS and Recurring Revenue of $299.2m, up 13%

- Total Revenue of $322.7m, up 11%

- Total Expenses of $233.6m, up 12%

- Free Cash Flow of $20.3m, down 15%

- Cash and Investments of $245.5m, up 16%

- R&D Investment (before capitalisation) of $84.1m, up 22%, representing 26% of total income

My Analysis

It was a soft result (which explains the weak market response), however, it was well-flagged at the AGM in February, and importantly, management say that the raised guidance for FY26 remains on track.

So, without going into a lot of detail, I’d characterise the presentation and the Q&A as one of reinforcing two sets of key messages. First, management carefully explained the several drivers of the softer 1H result while, secondly, reinforcing their confidence that leads to them holding to the raised FY26 guidance. Because there was a fair bit of repetition of messages from prior updates, I’ll point out a few of the nuggets against each of these two parts of the story.

Drivers of “soft” 1H:

- FX: GBP & NZD both weak vs. AUD, and GBP now a more significant revenue contributor

- Phasing of revenue within the half, weighted to back end

- Showcase costs, absent in the PCP, leading to +$9m costs

- Higher R&D spend in the half, related to launch of new features including SaaS+ (R&D 26% of revenue vs. 20-25% target range; will fall back into target so FY likely to end up back within range)

- As $TNE becomes more profitable, tax rate slowly increasing

Confidence in Retaining FY Guidance

- Historical weighting of revenue is to 2H

- Internally, they are now confident on 2H and balance of the focus within the business for BD is on FY27

- Showcase attendance was +85% on prior Showcase, and has had a “10X impact on the sales pipeline" compared to previous event – some of which is expected to hit FY26

(As an aside on style, in various stories and anecdotes there was a bit too much use of "10X" and "order of magnitude" for my liking. The hyperbole is clearly a smokescreen to not give analyst more visibility into performance drivers than management wants. Which I guess is management's call, and they have earned the right to do this over time. But I find it a bit grating. Rant over.)

Personally, I was surprised when management raised FY guidance at the AGM. Ed reminded shareholders that they’d done that 3 months earlier than usual. Who knows what is going on under the hood, but management have definitely laid their reputation on hitting FY26, and my inclination is to trust them, based on the track record.

The chart below shows that the ebb and flow between 1H and 2H can be very significant, so today’s “soft” result has ample recent historical precedence.

Conclusion

Everything indicates to me that $TNE remains on track.

But the market doesn’t yet buy their story that SaaS+ is lifting the overall trajectory of PBT growth to 18-20% (from 13% to 17%) and establishing the ARR growth target of 16-18%.

That said, compared to other SaaS peers, $TNE is holding up pretty well in terms of market belief as measured by SP.

The FY26 result in November will be an important proof point. But isn’t that always the case!

$TNE remains a solid HOLD for me, squarely within my valuation range: $30 ($24-$36), It remains my largest RL ASX holding.

Disc: Held (RL 13%)

11 April 2026

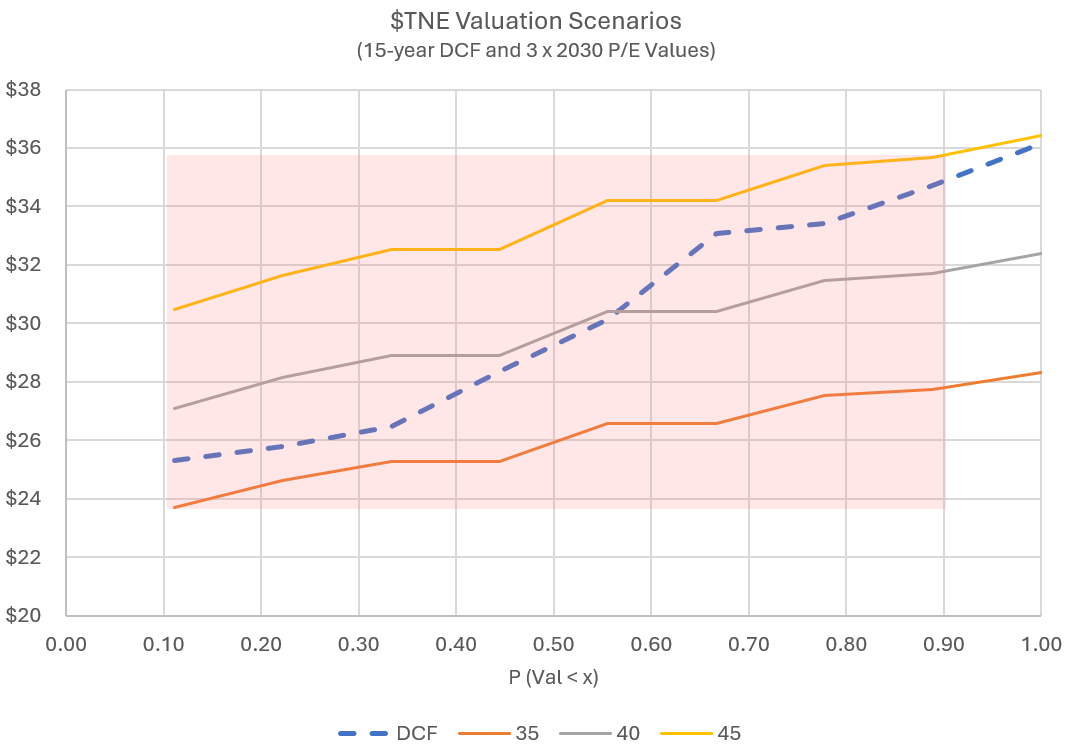

Valuation: $30 (range $24 - $36)

I’ve been overdue in updating my $TNE valuation here. I’ve written several straws here and will keep the descriptive bit here brief. For an excellent summary of why to hold $TNE, refer to the recent valuation by @Karmast, which captures the main points.

From my perspective, I believe $TNE has a long runway due to its ability to sustain high NRR from existing customers by continuing to build out functionality, including now with AI. And then the early signs in the UK both with local government and universities are promising, with $TNE still in the early days of a market that is 2x ANZ, offering a couple of decades of further opportunity.

Methodology

I significantly updated my valuation model from the previous, simple FY30 EPS calculation (although, as I show at the end, the current model “history matches” almost perfectly to this simpler model.)

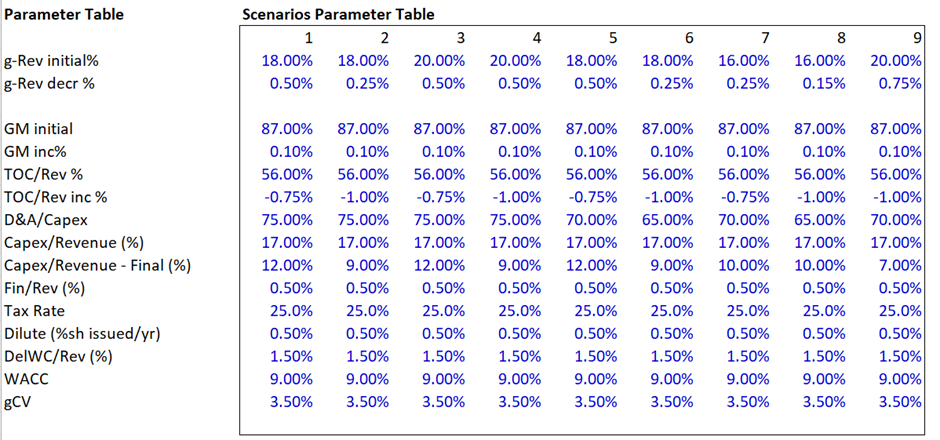

The updated approach is a full 15-year DCF supplemented by calculations of value based on the EPS in FY30, as generated by the DCF model. The model is generated from 9 scenarios considering ranges in revenue growth and expenses/ investment.

Assumptions

Revenue: Growth rates range from 16% - 20% in FY26, with growth progressively declining each year to reach 11% - 14.5% by 2040.

Gross Margin: %GM expands only modestly by 0.10% p.a., as the track record here is patchy, but scale economies should arise over the long term (assuming costs of AI “load” can be passed through to customers). The contribution of %GM assumption to valuation and ranges is small compared with the revenue and opex assumptions, which are the major senstivities.

Total Operating Cost (TOC): Here, $TNE has shown steady operating leverage and with the rollout of SaaS+ and greater deployment of AI. TOC/Revenue (%) is assumed to decline annually from 56% by between 0.75% and 1.00% out to 2035 and remaining constant thereafter, reaching a minimum of 47% to 50%, depending on the scenario. Operating leverage is a key value driver, however, net margins out to 2035 and 2040 remain reasonable for its peer group.

Capex: Capex as a % of Revenue is assumed to gradually decline from 17% in FY26 to between 7% and 12% in FY35 remaining constant thereafter. This represents uncertainty in the level of investment that will be required to ensure that $TNE continues to attract and retain customers with marketing-leading innovation. (To enable the model to produce both Free Cash Flows and full Financials, a ratio of D&A/ Capex is also modelled with scenarios ranging from 65% to 75%).

Other Parameters as follows:

Financing costs: 0.5% of revenue

Share Dilution: 0.5% SOI p.a.

Annual Increase in Working Capital: 1.5% x Revenue ($TNE have actually been able to progressively reduce Working Capital as it scales, but this is not an endlessly sustainable trend.)

Tax Rate: 25%

WACC: 9%

Continuing Value Growth: 3.5%

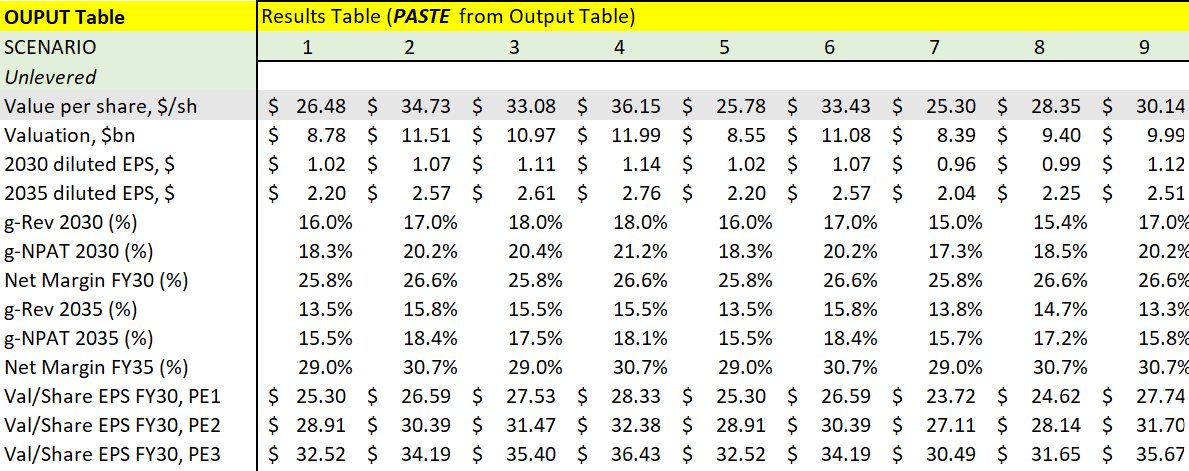

Valuation Results

Model Inputs

Selected Model Outputs

Note: PE1 = 35, PE2 = 40, PE3 = 45 as shown in the graph.

Comparison with Previous Valuation

Rolling forward my previous 2024 valuation of $23.70 by two years at the cost of capital of 9% yields a valuation today of $28.20. Today’s updated valuation of $30 can be explained by the recently upgrade guidance issued by the company.

If we dig into the previous valuation, the modelled EPS (FY30) was $1.045. Today’s DCF update yields results ranging from $0.96 to $1.14, averaging $1.06. This is not a coincidence but rather indicates the stability and predictability of this business.

Investment Decision:

I’ve recently been buying in RL between $20 and $23 and now have a full 13% portfolio weighting – my largest ASX holding.

At Friday’s close of $27.69, I consider $TNE a "HOLD" and am pleased to have loaded up with a higher margin of safety. Now that prices have returned closer to "Fair Value" IMO, I am done buying.

I would consider lightening my position above $35 (as I did last time it got up there.)

Disc: Held

===============================================

30 July 2024

Today's material news:

- From ARR = $500m in FY2025, to ARR = $500 by 1H FY25 (recently upgrade from FY26)

- ARR = 1bn by FY30

- NRR to be 115%-120%

- R&D to double their "APAC Whitespace" from $2bn to $4bn (i.e. growing functionality and verticles)

- Profit Margins to expand to 35% by 2030 (23.3% in FY23) "through significant economies of scale"

Valuation

Plugging this info into my quick model, and treating FY30 ARR as revenue in that year (probably an over-estimate, but allowing for them to come in early, so I won't sweat the difference)

- EPS (FY30) = $1.045

- EPS CAGR 2023-2030 = 18.7%

- SOI growth og 0.5% p.a.

- Using a WACC of 10% (which is probably high for $TNE, which is more like 8-9%, but use this as an MoS) discounting back 7 years 2030 to 2024:

- P/E of 35 : Value/Share = $20.70

- P/E of 45: Value/Share= $26.60

Note: Average P/E over last 3 years has been around 47 (currently a bit spicey at 58.)

Taking the midpoint: $23.70

(Assumptions: 2030 ARR and margins achieved per the strategy; FY30 P/E = 40).

As I look at SP movements of my holdings and the watch list, I keep on eye on global comparison.

$TNE has now fallen 53% form its peak SP, and when I compare it to a set of peers/competitors it is evident that global markets are doling out a re-pricing with a fairly even hand. These are all pretty high quality businesses, albeit $SAP the most mature and a legacy defender from the others.

$TNE still looks expensive in its peer group, albeit it is slightly higher quality than the rest.

So my point is that for the highly rated Aussie tech stocks, there is no let-up in the operational and financial performance that is required.

This really is sector-wide and global. Meeting expectations just keeps you in the game.

I have been accumulating $TNE and intend to continue to do so.

I played around with Perplexity today to do a valuation on TNE, below is what it came up with:

Valuation (P/E method): (Current P/E according to CMC is 68.42)

Applying the current EPS ($0.41) across a range of realistic growth multiples:

- Low: 60x = $24.60

- Median: 87x = $35.67

- High: 100x = $41.00

Conservative historic sector range: 40x–60x for Australian SaaS leaders.

EV/EBITDA Multiple Valuation

- FY25 EBITDA: ~$255.7 million.

- Enterprise Value (EV): ~$7.4–7.5 billion.

- Current EV/EBITDA: ~29x (EV $7,430m / EBITDA $255.7m = 29x).

Valuation (EV/EBITDA method):

- Australian tech leaders trade at 20x–35x EV/EBITDA, with TNE at the top end.

- Using FY25 EBITDA and multiples:

- 20x EBITDA = $5.1 billion EV (share price range ~$28–31)

- 29x actual = $7.4 billion EV (share price range ~$41)

- 35x high = $8.95 billion EV (share price range ~$49)

TNE trades in the top range of ASX tech sector multiples due to its exceptional growth, cash generation, and ARR profile. The valuation range by P/E is about $25–$41, while EV/EBITDA is $28–$49. Investors should be aware that this premium is justified by growth and defensiveness, but any reduction in growth rate or SaaS margin expansion could compress the multiples.

I've gone for the average of both methods, which results in a price of $35.65. Given TNE traded at $42.61 as recently as June 25 I reckon that is pretty conservative.

When I see this chart pattern it reminds me of the 'High Tight Flag' = a bullish price action.

Prelim report was: 20/05/2025

Annual Report is expected: 18/11/2025

14-Jan-2021: $9.50 is my 12 months PT for TNE (so by January 2022), however I believe they will double their business again by the end of 2027, being seven years, and they will be trading at over $15/share at that point. Management have restated their belief (in their November 24th results announcement) that they can do it in 5 years once again, but I'm going to give them an extra two, due to COVID.

There are very few companies of higher quality than TNE. They have managed to more than double their revenue and profits every five years for the past 15 years, so they've doubled in size 3 times. Why wouldn't that be reflected in their share price. Well, it has been. Have a look at what their SP has done:

30-Nov-2005: $0.57

30-Nov-2010: $0.96

30-Nov-2015: $4.35

30-Nov-2020: $9.18

Of course, the entire IT sector including all 5 of the WAAAX stocks and the XIJ (the ASX200 IT Index) have all dropped during December and so far this month as well, and TNE has too - closing today down at $7.65, some 16.7% below that $9.18 level at the end of November. APX has dropped the most, due to downgrades, but they've all dropped due to rotation out of growth stocks and growth sectors (like IT) into value stocks and cyclicals (mining, materials, energy, the better quality retailers, etc.). I loaded up on TNE in one of my portfolios today, and I'm planning on doing some more buying (in another portfolio - my super PF) tomorrow.

They weathered a short-seller attack in July that focussed on their accounting and our own @Wini ( https://strawman.com/Wini ) (a.k.a. Luke Winchester) had already posted a great article here on some of the changes they had made - see here: https://strawman.com/blog/beware-false-profits/

I believe that the results they produced in November for their full year (FY20) - which ends on September 30 - have put those concerns well and truly to bed.

Some FY20 highlights:

· ROE = 44.3%;

· ROC = 38% (both from Commsec);

· Their underlying PBT (Profit Before Tax) increased from 27% in FY19 to 29% in FY20;

· They expect their margins to gradually improve to 35%+ in the coming years driven by significant economies of scale;

· They stated that they are on track to double the size of the business once again in the next 5 years;

· They only need to keep growing at 14% p.a. to achieve that, and they managed underlying PBT growth of 13% in FY20 despite COVID-19;

· Cash Flow Generation in FY20 of $66.4m, up +49% on FY19;

· Cash and cash equivalents of $125.2m as at 30-Sep-2020;

· No Debt;

· They've posted record revenue and a record profit every single year for the past 11 consecutive years;

· They've increased their dividend every single year for the past 8 consecutive years, and by +8% in FY20;

· They spend at least 20% of their revenue on R&D each year to stay at #1, and in FY20 it was a $68.1m R&D investment before capitalisation, up 13% on FY19, and that was 22% of their FY20 revenue;

· Their UK business, which they built up from scratch, has just hit breakeven (no more losses), and will be profitable this year;

· Their Australian business has been consistently profitable for over 25 years;

· They've already expensed all of the costs of building up that UK business (from nothing), so it too will be highly profitable in the future;

· They don't grow via acquisition - they grow organically, and it's dependable and sustainable growth, they have the track record to prove that;

· They are a $2.6 billion company that is in the ASX200, they are Australia's largest and most successful ERP (Enterprise Resource Planning) SaaS company, and after carving out a niche in Universities, TAFE Colleges and other education facilities plus local governments and councils, they have successfully expanded their offering to other government departments, financial services, health & community services, utilities and managed services, with more to come;

· They were early to move to the cloud and they are now reaping the benefits of that, and so are their customers. Their customers now pay less for the same service but it costs TNE heaps less to deliver that same service, and they are upselling (additional modules to their existing clients) as well;

· Most of their revenue is recurring in nature, from the same clients, so is predictable and dependable;

· They have unbelievably low churn, averaging less than 1% per year and around half of one percent in FY20. What that means is more than 99% of their customers are loyal and stay with them every year, and keep paying them every year;

· Part of that is because of the quality of their software, and the other part is that ERP software is incredibly risky and difficult to change once it's in place;

· They have had a single high profile unhappy client, the Brisbane City Council, who sued them a couple of years ago and that was settled out of court. However, leaving them aside, the vast majority of TNE's clients are happy and loyal; and

· Unlike SAP, one of the World's largest ERP software suite providers to large corporations (I worked for Coca-Cola Amatil when they adopted SAP and I know the problems it caused) who have more of a one size fits all approach, TNE's "single instance multi-tenanted Global Saas ERP Solution" is tailored to suit specific industries and then individual companies and organisations within those industries. And with their high R&D spend, they are staying on top of new developments, improvements and new products.

I could go on. Well, I already have, clearly... Anyway, in case I haven't mentioned it already, I'm a fan of TechnologyOne (TNE). And I hold TNE shares.

30-Mar-2021: In January (14-Jan-2021) I set a 12-month PT for TNE of $9.50. They closed at $7.81 that day. They got there (to $9.50, being a +21.6% rise) in less than 6 weeks. And they got there on 22-Mar-2021 during a period in which the NASDAQ had a technical correction and most "Tech" stocks both in the US and back here on the ASX were being sold off quite aggressively.

They've pulled back a little over the last two trading days (i.e. this week), but they're still within spitting distance of $9.50. They closed at $9.28 today. This could be the start of another leg-down. We shall see. I'm continuing to hold TNE.

They have a financial year the ends on 30-September, so their half year finishes tomorrow (31-Mar-2021) and they are due to release their half year report in mid-May. It's a quality company and I'm going to hold them now, not trade them. For those who are happy to trade them, this could be a good time to lighten the position and then look to load up when they drop below $8 again, assuming they do drop back below $8 again. They might not.

24-Oct-2021: Yeah, Nah, they did NOT drop below $8, far from it, they are now trading at over $12, after announcing in early September the acquisition of Scientia - UK’s Leading Higher Education Software Provider. So it’s not just organic growth now, there is growth via acquisition on top of that. Market like! TNE were trading at $10.13 the day before that announcement and are now trading at $12.35, so they’ve put on +21.9% since the announcement of the Scientia acquisition. Good thing I decided they were a “Hold through the cycles” stock, eh?! My position six months ago was that they MIGHT have another leg down, but that their superior management, track record and industry position would see them continue to rise at a good clip over time, although probably (almost certainly) not in a straight line.

Rudi Filapek-Vandyck, the founder and editor of FNArena.com, penned an excellent article in December (2020) about TNE which can be read here:

https://www.fnarena.com/index.php/2020/12/03/rudis-view-be-respectful-of-the-past/

It is probably the best bull case for TNE that I’ve read actually, and it echoes my own views.

One thing to be aware of is the ongoing wrongful dismissal dispute known as “TechnologyOne vs Roohizadegan” which has been explained well by TNE in various announcements, their latest two can be read here (05-Aug-2021) and here (10-Sep-2021). Essentially, while I know that there are two sides to every story, I think this case has significant similarities to the one that EGL faced after they terminated the employment of their former CEO, Peter Bowd, in 2017 after he made serious allegations against the company regarding money laundering and accounting irregularities (fraud) including payments made for services not provided. As explained in a June 2019 article published in “The Market Herald”, and in the AFR in July – see here: https://www.afr.com/work-and-careers/workplace/whistleblowing-ceo-not-unlawfully-sacked-20190621-p52020

…Bowd had embarked on a dangerous (to the company) path of trying to undermine and oust the Managing Director of EGL at the time, whose family had built up the Baltec I&E business that is now a division of EGL, and there had been a widespread employee revolt and a situation had developed where the people under Bowd were refusing to work for him. He had effectively become ineffective as a CEO, or to put it another way, the EGL Board had no option but to terminate his employment. When what he had been doing (which included trying to get authorities to initiate investigations into the company’s overseas dealings without the knowledge of the Board) and the fact that employees no longer felt they could work with him, and he was putting contracts at risk because of his actions which could see the company go broke, Bowd stormed out and then the following day went to the Police and to ASIC to complain about alleged illegal activity. He was suspended and then dismissed, and he sued for wrongful dismissal. He claimed general workplace protections (“General Protections”) in respect of being terminated for exercising his workplace rights, and one of those rights was taking sick leave. The Federal Court found that he was NOT dismissed for taking sick leave – see here and here. He also claimed whistleblower protection, but the Federal Court found that his allegations were unfounded and malicious with the sole intent of saving his own job (or presumably allowing for a wrongful/unfair dismissal claim – or breach of general protections under employment law claim - to be made if he were to be dismissed), so the whistleblower protections under employment law did not apply in this case.

The AFR article is likely behind a paywall (the one I’ve linked to above), but it’s worth reading for some context, here’s some of it:

'Whistleblowing' CEO not unlawfully sacked

By David Marin-Guzman, Workplace correspondent, AFR, Jul 2, 2019

A chief executive who was fired for alleging his own company was involved in fraud and money laundering has lost his unlawful dismissal case because a court found he made the complaint only to "save his job".

Former CEO of ASX-listed exhaust producer The Environmental Group (EG), Peter Bowd, told the Australian Securities and Investment Commission in 2017 he had uncovered more than $400,000 in irregular transfers between TEG and its Indonesian subsidiary, PT Baltec.

The complaint alleged the money, paid over 12 months, was in the form of loans not repaid, payment of tender expenses and costs of goods sold but without supporting records.

“As CEO I believed there is substantial fraud and laundering of funds from the Australian business into the Indonesian company by the managing director and sales director," Mr Bowd told ASIC.

He told EG's chairman David Cartney the subsidiary might have paid bribes, parties were "skimming monies out of the company", and that managing director, Ellis Richardson, whose family was the former owner of Baltec, might have engaged in insider trading.

Shortly after the complaint, the board suspended and later terminated Mr Bowd for poor performance.

Rejecting Mr Bowd's subsequent $500,000 damages claim against the company, the Federal Court found no evidence to support his allegations.

Justice Simon Steward said the claims were made in the context of a "severe" breakdown in the board's relationship with the CEO.

"Mr Bowd made his complaint to ASIC with the intent of triggering the whistleblower provisions as a means of preventing his dismissal for poor performance as CEO," he said.

"The allegations contained in that complaint were concocted, or at the very least, deliberately exaggerated."

Mr Bowd had alleged EG's dismissal breached whistleblower protections in the Corporations Act and was adverse action for exercising his workplace right to make a complaint.

But Justice Steward ruled the ASIC complaint was not a workplace right or covered by whistleblower protections because the allegations were "not made in good faith", which he held was a requirement under the Fair Work Act.

"There was no or no sufficient basis for their making. The complaint was used as a calculated device," he said.

'Extraordinary actions'

Mr Bowd was appointed as CEO in September 2016 and, after some success, turned his focus to Baltec.

His scrutiny led to the sacking of a key employee for serious misconduct, the resignation of another and an aborted push to get BDO accounting to undertake a forensic audit without the board's knowledge or consent.

But Baltec staff started to revolt, accusing Mr Bowd of prosecuting a "personal agenda" and claiming a major client was at risk and the company could fold in three to six months.

When Mr Richardson confronted the board with these concerns including that staff morale was low and EG risked losing $4 million in value, Mr Bowd allegedly "stormed out".

Mr Bowd had assumed the board was going to remove him as CEO, the judge found, and the next day decided to complain to ASIC and the police.

Justice Steward said Mr Bowd had complained without the board's knowledge or consent and without waiting for an external audit into his concerns to finish.

"In my view, such extraordinary actions must have played a significant role in the board’s decision that it could not continue to work with Mr Bowd. In my view, in the circumstances of this case, that is entirely understandable."

The company's auditor ultimately found the "irregularities" Mr Bowd identified were actually supported by documents and that his other claims were incorrect.

Two years later neither ASIC nor police have taken any action against EG.

--- end of article/report ---

Now that concerns EGL, not TNE, and the Roohizadegan case is clearly not the same, but there are similarities in my view. I think Adrian Di Marco, TNE’s founder and Executive Chairman, had no choice but to dismiss their Victorian manager Behnam Roohizadegan, who then sued TechOne for breach of general protections under employment law. He won that case and was awarded a record $5.2m payout by the court. TechOne then successfully appealed that decision and have now been granted a retrial. It’s worth noting that while the original decision has been set aside pending the retrial, TechOne have already sensibly made a provision in their accounts for the $5.2m payout, and that provision remains in place. If the retrial also goes against TNE, they will NOT be in a worse position than they already are, as the money has already been set aside and accounted for. If however TechOne is found to have lawfully terminated Roohizadegan’s employment, they’re going to be able to reverse that provision, so they’ll effectively have another $5.2m cash available.

The Roohizadegan case was explained well in this 11-June-2021 AFR article: https://www.afr.com/technology/no-basis-for-5-2-million-unfair-dismissal-ruling-techone-tells-court-20210611-p5806j

‘No basis’ for $5.2m industrial relations ruling, TechOne tells court

By Hannah Wootton, AFR Reporter, Jun 11, 2021.

Software company TechnologyOne and its vocal founder Adrian Di Marco are calling for a retrial of an employment law case that has them on the hook for $5.2 million in damages, claiming the trial judge “ignored ... a very large amount of evidence” and made legal errors “in every one of his reasons”.

Justice Duncan Kerr of the Federal Court last year ordered the growing company to pay former Victorian manager Behnam Roohizadegan the record payout after finding the company breached general protections he was afforded under employment law by dismissing him in 2016 after he complained about being bullied at work.

A Federal Court judge found that Adrian Di Marco stood with the bullies, not the bullied, in an unfair dismissal case. Tertius Pickard

According to Justice Kerr, Mr Roohizadegan was subjected to abusive language, victimisation, gas-lighting, and “boorish” conduct while at TechOne, with his treatment at the hands of its executives leaving him “incapable of ever working again”.

But in a full Federal Court hearing littered with legal heavyweights on Friday – industrial relations guru Stuart Wood, QC, appeared for TechOne while Mr Roohizadegan retained Bret Walker, SC – Mr Wood said the trial judge failed to consider key evidence that supported his client’s case.

“ ... Everything was put to his honour, and everything was ignored,” the silk said.

“There was a failure to take into account or analyse ... a very large amount of corroborative material, which was put to His Honour for his consideration in the assessment of the statutory task in which he was engaged.

“The reasons that His Honour provided do not reveal, despite referring to in a number of places ‘the whole of the evidence’, the manner in which the corroborative material that we say should have been deployed was deployed.”

This allegedly included evidence that Mr Roohizadegan’s performance was dropping – which TechOne said was the basis for his dismissal – and an email in which TechOne executives discussed terminating Mr Roohizadegan’s employment that pre-dated the bullying complaints.

He added that there “was a legal error in relation to every one of [Justice Kerr’s] reasons, especially around his alleged failure to consider the nature of the complaints made by Mr Roohizadegan.

The barrister alleged that this was “never considered” by Justice Kerr, forming an “obvious error” in the decision which gave grounds to a retrial.

He also hit back at the judge’s characterisation of Mr Di Marco as an “evasive” witness who, as a boss, chose “to stand with the bullies rather than the bullied”.

In the original judgment, Justice Kerr said Mr Di Marco’s own conduct toward Mr Roohizadegan was “deceptive and self-serving if not cruel” and his evidence before the court as “highly unimpressive ... tortured and evasive”.

When awarding the record damages payment, he said that to achieve “effective deterrence”, CEOs needed to know that “there will be a not insubstantial price for failing” to stand with bullies.

Mr Wood dismissed these findings: “There was obviously no basis on the evidence presented to draw that conclusion,” he said, adding that it “was never” the trial judge’s role to consider Mr Di Marco’s behaviour at that time.

Mr Di Marco’s criticism of proxy advisors has come under scrutiny over the past two months as he has publicly advocated for efforts by the federal government to limit the power of proxy advisors, building on his previous complaints about the firms.

His outspokenness follows TechOne shareholders delivering a first strike against the company’s remuneration report at its February AGM after two proxy houses, Ownership Matters and CGI Glass Lewis, recommended voting against it.

--- end of article/report ---

Two sides to every story, but at the very least I don’t think this has any further negative potential to hurt TNE, particularly as they’ve already provided a provision for the full $5.2m payout as well as legal fees. In their recent ASX announcements regarding this matter, TechOne said, “this was a senior executive earning close to $1m per year, who no longer had the confidence of the board and his fellow executives and against whom serious allegations had been raised by staff, and we took action to address in 2016.”

So, sorry to delve into that murky cesspool for a while, but I think that is one of the two skeletons that have been found in TNE’s closet, the other one being the dispute with Brisbane City Council that was settled out of court in the end a couple of years ago. Their one high profile unhappy client. A lot was made of that dispute at the time, but once again there are two sides to that story as well. I won’t waste time talking about TNE’s side of that one. It’s enough to know that their churn rate is less than 1% p.a. and was less than half of one percent in FY20, and there is no evidence that this very low churn rate deteriorated in FY21. Their FY finishes on 30th September, so they will report their FY21 results towards then end of November.

Happy holder of TNE in two of my RL portfolios (including my SMSF) and also here on SM.

Raising my TNE PT (price target) to $13.70, and that’s a 2 year PT, so by late October 2023.

Further Reading:

Annual Reports - TechnologyOne (technologyonecorp.com)

Life@TechOne: Company Values - TechnologyOne (technologyonecorp.com)

TechnologyOne - Global SaaS ERP Solution (technologyonecorp.com)

19-Nov-2024: Update:

Well, they just keep performing - FY24 full year results announced today. Here's their ASX announcement: FY24-ASX-Results-Release-TNE.pdf.

Unfortunately I'm no longer holding this one as they looked fully priced to overbought. I was wrong about that it seems.

They just keep releasing record results every single year:

Ah well, you can't pat all the fluffy dogs, eh Claude?!?

BRISBANE, 19 November 2024 – TechnologyOne (ASX: TNE), Australia’s largest ERP SaaS company and the world’s first SaaS+ company, today announced its financial results for the year ended 30 September 2024.

It's their 15th consecutive year of record profit, record revenues, and record SaaS fees.

FY24-ASX-Results-Release-TNE.pdf

2024 Full Year Results Presentation.pdf

Other highlights that caught my eye:

Source: https://www.technology1.com/resources/media-releases/full-year-results-2024

TNE's share price closed up +10% @ $29.45/share but did get up as high as $30.34/share during the day.

This is one I wish I had not sold out of in June. Like @mikebrisy - who cut TNE loose this month - I thought they were overbought - with some upside already priced in - and that the share price could be smashed if they didn't live up to the market's lofty expectation with their results.

Well, they certainly did live up to the market's lofty expectations.

Very high quality company this one.

Disclosure: Not held currently - unfortunately.

I have this morning exited my entire RL $TNE position at $26.591.

It's a great company, but the decision was based on valuation. For me its $23.70 ($20.70 - $26.60).

Getting to my upper valuation limit of $26.60 requires strong sustained growth for 6 years, with an exit P/E of 45 in 2030 - which is high by any measure.

SP has run up over 67% since the stellar 1H result, and I fear expectations have started to run ahead of reality. For such a steady perfomer, a forward P/E of 72x and trailing of 79x just seems excessive. A result next week that does anything other than blow well-guided consensus out of the park could see a significant pull-back. The outperformance required to drive yet another leg up seems to be a stretch. (Let's see how well that prediction ages!)

Of course, whenever I hop off the bus like this, I know I risk missing the chance to get back on. But can I see it doing +15% from here over the next 12 months? Frankly, no.

I'm reasonably confident that this one will come back, and would be happy to get back on more around $21-$22. (Just wait for the next round of US inflation concerns to raise their heads!)

Disc: Not held

$TNE announced their FY23 results today. It is my largest RL holding, so I attended the call, and here will bring out a few points.

Their Highlights

• Profit Before Tax of $129.9m, up 16%, beating guidance of 10%-15% growth

• Profit After Tax of $102.9m, up 16%, beating guidance of 10%-15% growth

• Total Annual Recurring Revenue (ARR) of $392.9m, up 23%

• On track to surpass $500m ARR by FY25

• Net Revenue Retention (NRR) of 119%. Above our long-term target of 115%

• Total Revenue of $441.4m, up 19%

• Revenue from our SaaS and Recurring Business of $390.7m, up 22%

• Expenses of $311.5m, up 21%

• Cash Flow Generation of $104.6m, up 36%

• Cash and Investments of $223.3m, up 27%

• Total Dividend of 19.52 cps, including a special dividend of 3.0 cps, up 15%

• R&D investment of $112.0m before capitalisation, up 21%, which is 26% of revenue

My Analysis

The results are impressive, and the highlights above speak for themselves.

Yet the market had run up in anticipation of the results - both expecting a good result given the strong 1H and as part of the wider macro pick-up in recent weeks. So, $TNE closed the day down 2%, as those who play with a shorter-term horizon took some profits. This is often the pattern with this stock.

The presentation held some interesting insights, which continue to support my thesis to continue to hold $TNE long term.

Cash generation was particularly strong, reportedly due to good performance by the collections team, with Cash Flow Generation (a number they use which is close to FCF) was 102% of NPAT – something CEO Edward Chung claimed was a year earlier than expected.

$TNE upgraded their target to hit $500m ARR by 2026 pulling it forward to 2025 – again, this was widely expected.

Net Revenue Retention was a very strong 119%, aided by pricing increases in an inflationary environment. However, even excluding the inflation effect, Edward said the result was very close to their ongoing goal of having NRR of 115%. This "target" allows the company to double revenue every 5 years, from existing customers.

Churn remains low at 1%, which was also positive. As $TNE gets to the end of the transition to a 100% cloud SaaS company, this was expected to lead to the loss of some customers on legacy platforms.

Although profit growth beat consensus, it was weaker than indicated by the strong ARR growth because costs have increased, driven by increased spending in R&D to drive development of the SaaS+ platform, and building out their full One Education offering.

Two case studies presented on Slide 25 showed where they are winning full government department ERP and whole of university ERP deals (student management, finance, HR and payroll). So, it has taken a lot of development investment to get to this point.

Consequently, PBT margins have fallen back to 30% from FY21’s high of 31%, however, Edward said that this will now gradually ramp up towards 35% over the coming years. Given the prospect of strong, ongoing revenue growth, this should turbocharge earnings growth over the next 3-5 years.

Long Term Prospects

My thesis for long-term sustained growth rests on two pillars: 1) continued strong growth from existing customers and 2) UK as a material future growth horizon. I’ll update briefly on both.

1) Growing Existing Customer with SaaS+ the next phase

A lot of rubbish gets written about $TNE by analysts who talk about the company’s growth slowing as they run out of room in ANZ, and today’s presentation addressed this head on.

Without going through the detail of the product suit that makes this possible(but they now have 16 products and over 400 modules), I include on chart from the presentation below that shows how $TNE’s innovation allows it to grow revenue strongly from existing customers.

Presentation Slide 29: Case Study of Existing Customer Growth

The slide shows selected case studies indicating how the transition to SaaS from the on-premises legacy drove the initial step-up in ARR, to which over time they have added new modules. Nothing new here, it’s the classic SaaS modular land and expand model.

What’s exciting is the new SaaS+ model, which is an enhanced SaaS ERP service including support for implementation and training and other services bundled around it. The offering has been developed to enable customer to adopt the service without having to use system integrators to manage the implementation. Slide 30 shows how this added value creates a new horizon of growth – one that is not yet material at the portfolio level, but which drive growth over the coming years.

Slide 30: Impact of SaaS+ (Case Example)

Edward was at pains to point out that while their competition in education and local government (including SAP) have now moved their offerings to the cloud, unlike $TNE these systems have not been designed as SaaS, cloud native products. Edward stated that $TNE have rebuilt their entire tech stack 4 times over 36 years. He claimed that no other ERP player has even ever done it once. So, they have a massive advantage against competitors in having very low technical debt. Importantly, the architecture is design for ease of implementation, as well as modular expansion.

Customers of competitors, on the other hand, generally continue to face the historical implementation challenges, including hefty consulting bills. As evidence, Edwards showed that $TNE consulting revenues actually fell 11%, which was celebrated as a good thing, demonstrating the ease clients face in implementation.

SaaS+ is proving an early hit with clients. 2023 was the first year of implementation, and they had targeted 10 deals. They delivered 34.

To show the enduring nature of the growth from existing customers, they included a cohort chart (which looks very much like what you see from $ALU and $WTC).

Slide 28 – Cohort Analysis

2) UK is making progress

The UK is the second part of my long term growth thesis.

$TNE started operations in the UK just before the pandemic, turning a profit in the first year, 2020. (Just think about that in the context of some of our other SaaS favourites here on SM that have spent 2-3 years around the inflection point!)

In FY23, ARR was $26.5m (up 52%) and profit of $3.7m was up 54%. It is still not a material part of the business, but it is intereesting nonetheless.

See the following two charts for an overview. (They have been just a bit naughty, in that the first chart is not to a consistent scale!)

One question mark in my thesis is whether $TNE can replicate their ANZ success in the UK. Or, are they late to the party in the UK, and up against established competitors who are all now also in the cloud. (Perhaps like we’ve seen with $XRO in its international expansion, where the international business is facing slowing growth, and represents objectively a lower quality business.)

While it is still early days, the signs are promising, and the management team expressed confidence that they are going to continue the trajectory established.

The reason for the confidence is the innovation their have built into their products which beats the competitor ERP offerings in the core verticals of education and local government. In fact, examples were presented where clients using competitor on-premises products, rather than risk a painful transition to the cloud used that transition decision as the opportunity to switch to $TNE. If $TNE develops an industry reputation as offering the best customer experience for on-prem to cloud transition, then perhaps they are just in the right place at the right time.

Progress in the UK is one I am watching closely. It’s not material at the moment, but looking out over 5-10 years, it could be a very important part of the long term growth story.

Valuation

$TNE is not cheap (understatement). Based on today’s result and closing price, the p/e is 51. That’s well into the upper half of its p/e range over the last 5 years (p/e range c. 35-60).

In my basic DCF models, I get valuations ranging from $13.50 – $22.00. With a stable margin structure, it really comes down to how long and how hard you believe it can continue to grow.

I’ve plotted the last 10 years SP below, with an exponential best-fit curve overlaid. If that curve is a good approximation to fair value, then pretty much every year you can get an opportunity to buy $TNE at a 10-20% discount to fair value. That is in fact when I last topped up in early 2022. But today, I’m not a buyer.

I’m certainly also not a seller, as I have a high conviction that with continued good management, this journey can carry on for the next 5-10 years. $TNE is my largest ASX holding in RL, and second only in conviction to $WTC.

My Key Takeaways

The FY23 was good on all fronts. There is really nothing to be critical about.

This is a high-quality business, and it appears to have a good runway ahead. In truth, it is hard to know just how good the market runway ahead of it is in ANZ. They claim to be no more than 15% penetrated in any of their verticals. I am happy to judge them year-by-year on delivery. The interest for me is the early progress in the UK – a market 2-3x ANZ. They’ve started well, and if the trajectory can be sustained, then even buying at today’s price will look like a great decision in 5 years’ time.

Disc: Held in RL (7.5%) not held on SM

Upfront about the Back Office incident.

to Add: TechnologyOne will update the market on its performance and outlook with the release of its 1H 2023 financial results on 23 May 2023.

Threatened - internal Microsoft 365 back-office system.

Trading Halt:

Technology One (TNE) released FY22 results (Sept year end). From their release:

- Profit After Tax of $88.8m, up 22%

- Profit Before Tax of $112.3m, up 15%, at the top end of guidance

- SaaS Annual Recurring Revenue (ARR) of $274.2m, up 43%

- Total Annual Recurring Revenue (ARR) of $320.7m, up 25%

- Total Revenue of $369.4m, up 18%

- Revenue from our SaaS and Continuing Business of $358.7m, up 22%

- Expenses of $257.1m, up 20%

- Cash Flow Generation of $77.2m, up 21%,

- Cash and Cash Equivalents of $175.9m, up 22%

- Total Dividend of 17.02cps, including a special dividend of 2.0 cps, up 22%

- R&D investment of $92.2m before capitalisation, up 19.6%, which is 25% of revenue

Another fantastic year for TNE with NPAT growth of 22%. Management have had long term targets of $500m+ in ARR by 2026 and also to double the business every 5 years (implying 15% CAGR).

I have updated my valuation on Strawman to reflect these results. I still think the current share price is a bit expensive and have sold my shares in my real life portfolio but continue to hold on Strawman. However TNE is definitely one of the highest quality business' on the ASX and a company I will look to re-enter at the right price.

Full Announcement Here

Full Presentation Here

Full Report Here

Disc: Held on Strawman. Not held IRL.

29-Nov-2021: Technology One (TechOne, ASX:TNE) released their FY21 full year results on Tuesday morning last week, and their SP dropped -2.86% (or -37 cps) on the day, then their SP dropped another -8.61% on Wednesday (24 Nov) as two brokers downgraded their calls on TNE. Macquarie dowgraded TNE from "Neutral" to "Underperform" with a new $11 TP (target price) and UBS dowgraded TNE from "Neutral" to "Sell" with an $11.90 TP. It didn't seem to help that Morgans maintained their "Add" call on TNE with a $13.73 TP (raised from their previous $10 PT). The other broker covered by fnarena.com who covers TNE is Credit Suisse who maintained their "Neutral" rating with a $12 PT. See below:

I note that as of right now (around 3pm on 29-Nov-2021), fnarena.com have not yet added TNE's FY21 numbers to those graphs in the top half of that screenshot. The broker updates at the bottom ARE up to date however. (As of today at least)

Here's some more detail:

Macquarie - 24/11/2021, Downgrade to Underperform from Neutral, Target: $11.00, Loss to target $-0.47

Following FY21 results for TechnologyOne, Macquarie raises its FY22-24 EPS forecasts by 10%, 15% and15%, respectively, due primarily to lower opex. The broker lifts its target to $11 from $9.20 and notes solid momentum in the SaaS transition.

However, Macquarie reduces its rating to Underperform from Neutral after comparing multiples for domestic and overseas peers. Management's lower revenue growth forecast was also taken into account.

Target price : $11.00 Price : $11.47 (24/11/2021) Loss to target $-0.47 -4.10%

(excluding dividends, fees and charges - negative figures indicate an expected loss).

UBS - 24/11/2021, Downgrade to Sell from Neutral, Target: $11.90, Gain to target $0.43

UBS assesses a solid FY21 result for TechologyOne though downgrades its rating to Sell from Neutral after a 30% share rally in the last three months. The profit result was a 1% beat versus the broker and towards the top end of guidance, primarily due to cost efficiencies.

Management reiterated the FY26 $500m annual reccuring revenue (ARR) target, after progress on SaaS transitions during 2H21, points out the analyst. The broker lifts its target price to $11.90 from $11.70.

Target price : $11.90 Price : $11.47 (24/11/2021) Gain to target $0.43 3.75%

(excluding dividends, fees and charges - negative figures indicate an expected loss).

Morgans - 24/11/2021, Add, Target: $13.73, Gain to target $2.26

TechnologyOne's profit result was in line with Morgans' forecast and towards the top end of the guiidance range. Both revenues and expenses were lower than forecast but tight cost controls supported earnings.

The transition of customers to SaaS continues with SaaS annual recurring revenue up an "impressive" 43% year on year. The legacy on-premise business will be disconinued in 2024 and management remains comfortable with its $500m SaaS ARR target for 2026.

Add retained, target rises to $13.73 from $10.00.

Target price : $13.73 Price : $11.47 (24/11/2021) Gain to target $2.26 19.70%

(excluding dividends, fees and charges - negative figures indicate an expected loss).

Credit Suisse - 24/11/2021, Neutral, Target: $12.00, Gain to target $0.53

Credit Suisse increases its target price for Technology One to $12 from $9.50, following FY21 results that came in at the high-end of guidance. Despite a lack of near-term catalysts, the analyst now expects sustainable double-digit profit growth.

By FY24, the broker forecasts a 35% profit (PBT) margin. End of on-premise support is planned for October 2024, which should accelerate the completion of the shift to SaaS.

In the longer term, the broker weighs positive drivers (product and geographic penetration) versus increased competition. Neutral rating maintained.

Target price : $12.00 Price : $11.47 (24/11/2021) Gain to target $0.53 4.62%

(excluding dividends, fees and charges - negative figures indicate an expected loss).

--- end --- Source: fnarena.com

The TNE share price was then up +4.27% (or +49 cps) on Thursday, then down -3.34% (or -40 cps) on Friday, and now today they are up +44 cps (or +3.81%) so far, so trading at exactly $12/share as I type this, and they have been as high as $12.19 earlier today. I couldn't really understand the market's negative reaction to the TNE results last week, however it is good to see TNE rising today in a falling market. The cream rises to the top when all is said and done. And TNE is the cream of the ASX IMHO. Disclosure: I hold TNE in multiple RL portfolios as well as here on SM.

As I have stated before, including in my valuation for TNE, they have managed to double their revenue and profits (+100% as a minimum) in a five year period three times already:

Their share price (SP) has reflected that:

30-Nov-2005: $0.57

30-Nov-2010: $0.96

30-Nov-2015: $4.35

30-Nov-2020: $9.18

Today (29-Nov-2021): $12.

As they explained on Tuesday last week:

$500m+ ARR by FY26 - With our fast-growing SaaS business and the announcement of the end of our On-Premise business, we are on track to hit our target of $500m+ ARR by FY26. Given the current ARR is $257.5m, this is an additional $242.5m of Annual Recurring Revenue in the next 5 years.

Revenue from SaaS & Continuing Business was up 9% [in FY21]. This is our future state business. By FY24 we expect our total business to be growing by 15%+ per annum.

Some people might call this optimistic, but TNE have a track record of achieving their own ambitious targets.

Rudi put it best: https://www.fnarena.com/index.php/2020/12/03/rudis-view-be-respectful-of-the-past/

I agree with Rudi that TNE is one of the best quality companies available to invest in on the ASX, and has been for a number of years. If you are after good growth year after year and a company that sets ambitious targets and then hits those targets, then TNE fits the bill perfectly.

That said, I'm possibly not going to be topping up here at these levels because I last bought TNE shares in January 2021 (this year) at $7.74, and they had significantly more shorter and mid-term upside from those sub-$8 levels than do up here at around $12/share, plus I have a large enough weighting to the company already, particularly considering the capital growth I've enjoyed. If I was underweight TNE shares however, these levels would look pretty good if you take a medium to longer term view, say 3 to 5 years.

Sample photo from their media kit - see here: Media Kit - TechnologyOne (technologyonecorp.com)

Edward Chung (CEO & MD) and Adrian Di Marco (Company Founder, Executive Director and Executive Chairman).

Yet another strong year for Technology One.

Annual Recurring revenue (ARR) up 43% to $192.3m following an 18% lift in SaaS customers.

NPAT came in at $72.7m, a gain of 15%.

The dividend increased by 8% (for the 7th year in a row), with 62% of NPAT returned to shareholders. This is a business that can grow really well with minimal capital reinvestment.

Like many software businesses, they are transitioning away from a license model to a recurring revenue model -- something that is a great long term move, even if it drags on revenue during the transition.

The company reckons it can roughly double its ARR over the next 5 years, achieving a ~14% compound annual growth rate. And that it can also increase its pre-tax net margin to 35%.

Taking these numbers together, and assuming around 330m shares on issue, that gives an EPS of roughly 40cps (compared to 22.6cps in FY21).

Over the last 5 years, the average annual PE ratio has been between 30-40. So if we assume a PE of 35 for FY26, that gives a target price of $14, which is $8.69 if you discount back by 10%pa.

Even a more bullish assumption of a PE of 40 and a target EPS of 45cps, you get a target price of $11.18.

To come at it another way, let's assume the dividend continues to grow at 8%pa and that the company trades at a yield of 1.5% in FY26. That also gives a target price of $14 or $8.69 when discounted back.

TNE is a very high quality company. High margin, high retention, high growth, rock-solid balance sheet. But I think a lot depends on the market maintaining high multiples for shareholders to achieve attractive returns. My concern is that even if the company does indeed double sales every 5 years (as they claim), any multiple contraction -- which would be likely under a higher rate environment -- would add some significant downward pressure on the share price.

I have a small holding which i'm happy to keep, but not tempted to add more at these prices.

25-May-2021: TechnologyOne SaaS up 41% & H1 FY21 Profit After Tax up 48%

plus: TNE H1 FY21 Half Year Results Presentation

and: Half Year Report 2021 - Amended

Key results were as follows:

- Profit After Tax of $28.2m, up 48%

- Profit Before Tax of $37.3m, up 44%

- SaaS Annual Recurring Revenue (ARR)* of $155.8m, up 41%

- Revenue from our SaaS and Continuing Business of $140.6m, up 7%

- Total Revenue of $144.3m, up 5%

- Expenses of $107.4m, down 5%

- Cash and Cash Equivalents of $100.1m, up 20% from 31 March 2020

- Cash Flow Generation** of ($2.9m) as expected, and will be strong over the full year

- Dividend of 3.82cps, up 10%

- R&D expenditure (before capitalisation) of $34.6m, up 14%, which is 24% of revenue

Notes:

- (*) ARR represents future contracted annual recurring revenue at period end. This is a non-IFRS financial measure and is unaudited.

- (**) Cash Flow Generation is Cash flow from operating activities less capitalised development costs, capitalised commission costs and lease payments. This is a non-IFRS financial measure and is unaudited.

[I hold TNE shares.]