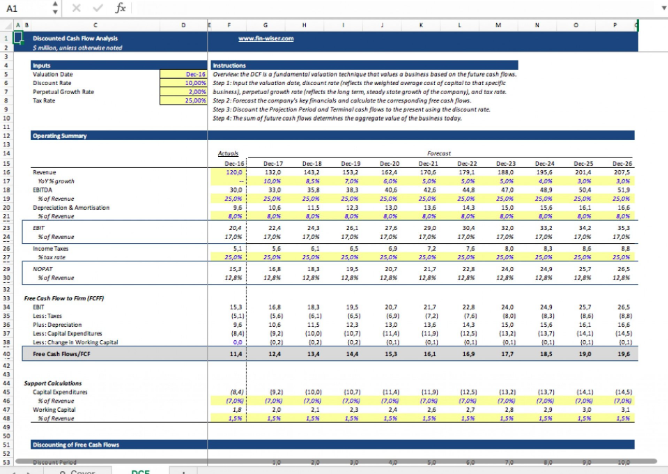

Bigtincan (ASX:BTH) is a developer of sales and service software that helps clients win more deals and improve productivity. Although the name may be unconventional — or not, when you consider other tech monikers — the business model is typical of the new breed of Software-as-a-Service (SaaS) companies, and Bigtincan is a good demonstration of why they can be so attractive.

Focus on a problem in a niche area, solve it better than anyone else using customisable, cloud-based technology that can be easily integrated with existing systems, and charge users an ongoing subscription fee. The best solutions enjoy potent network effects (they are more valuable with more users), become extremely sticky (difficult or inconvenient to move to a competing offering) and are relatively easy to manage and upgrade over a wide array of different customers.

Founded in Sydney in 2011, and listing on the ASX in 2017, Bigtincan has rapidly grown to a $135 million company with international operations and over 150,000 licenced users. With more than $20 million in annual recurring sales, Bigtincan is chasing a $5 billion market opportunity and enjoys strategic partnerships with some silicon valley giants, including Apple and Salesforce.

Like many relatively young tech companies, the business is yet to pass breakeven as it continues to reinvest rising revenues into growth initiatives. Forgo profit potential today, the idea goes, so as to win market share and secure bigger longer-term profits tomorrow. So long as capital is wisely deployed and the competitive positioning further strengthened, it’s a sensible strategy, especially if the business can secure very low cost of capital funding along the way.

If not, it can be a case of good money after bad.

At a point, when sufficient scale is reached, you need a relatively fixed cost base that is capable of underpinning continued growth in high gross margin sales. Unless that happens, the internal rate of return is likely to confound any hopes for decent shareholder returns.

So far, at least, Bigtincan seems to be on the right trajectory. Annual recurring revenue was up 63% at the most recent half, with revenue coming in 56% higher. The statutory loss is rapidly falling away as the company approaches break-even, and Bigtincan has over $12 million of cash on hand to sustain itself in the interim.

Customer retention remains strong at 87% and the average customer lifetime value continues to increase rapidly (up 90% as of Dec 31, 2018). With 91% of revenue derived from North America, Bigtincan has very little exposure to the domestic economy (but plenty of sensitivity to exchange rates).

Given guidance for 40% revenue growth, Bigtincan is trading on a price-to-sales ratio of ~7.3 times. So long as growth remains strong, that’s not especially high. Of course, if the growth outlook deteriorates, the market tends to re-rate such businesses very harshly.

Ranked #25 on Strawman, shares remain a good distance below the community’s estimate of fair value. Click below to learn more:

Strawman is Australia’s premier online investment club. Join for free to access independent & actionable recommendations from proven private investors.

Disclaimer– The author may hold positions in the stocks mentioned in this publication, at the time of writing. The information contained in the publication and the links shared are general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser. For errors that warrant correction please contact the editor at [email protected].

This Service provides general financial advice only, and has not taken your personal circumstances into account. Strawman Pty Ltd operates under AFSL 501223 . For more information please see our Terms of use. Please remember that share market investments can go up and down and that past performance is not necessarily indicative of future returns. Strawman Pty Ltd does not guarantee the performance of, or returns on any investment.

© 2019 Strawman Pty Ltd. All rights reserved.

| Privacy Policy | Terms of Service | Financial Services Guide |

ACN: 610 908 211 | Australian Financial Services Licence (AFSL): 501223