Great writers like Charles Dickens have explored the true meaning of Christmas. I will leave that to them. For my part I always seem to find a way to make Christmas at least a little about myself. And so it was last December when I allowed an eleventh hour Christmas shopping trip to be hijacked at a JB Hifi, as I made extensive inquiries about an Xbox no one else in my life had expressed an interest in.

Actually, this story probably started about a week before that. Or perhaps about a decade before – as being in my mid 30s my computer gaming days are very much consigned to the ghosts of Christmas past. However, that week had seen the zenith of a new golden age of gaming brought about courtesy of an iPhone app. This thing was so addictive. It had dawned on me at breakfast.

My wife had repeated herself for a second time and I was clearly distracted. Although, to put things in context, I was desperately hunting deer to obtain the leather I needed to pay mercenaries to more adequately defend my township of EskyBruhlites from more highly weaponized opponents. Yeah, I deleted that app a few days later, I decided I didn’t need that in my pocket everywhere I go. Really, who needs that level of responsibility, as William Shakespeare wrote, “Uneasy lies the head that wears a crown” [1].

So maybe this Xbox represented a last hope of compartmentalisation. My memory of computer games had always been of something less insidious. And I don’t mean the content itself. I’ve never been too fussed by censorship in that regard. Some of my earliest gaming memories involve breaking out of a Nazi-occupied castle and probably being too young to make the difficult decisions required about what to do with some aggressive German Shepherds. What concerns me more is the nature of modern gameplay and the manner in which computer game companies realise their revenue. For people of my vintage, the start of many new computer games involves some experience like Homer’s at Itchy and Scratchy Land [2]– that is, at least part of your experience is going to depend on how much coin you have on your virtual travel card. Gone are the days of paying just the once for a computer game. An even more sinister aspect to these in-house virtual currencies can be their application in gambling-like scenarios [3].

Even the use of more subtle (as in not specifically gambling related) randomised probabilities is designed to trigger certain behaviour in us. My EskyBruhlites had only a 30% chance at getting their leather from a deer kill. I have since learned why.

So anyway, I asked the electronics store salesman if you could play this new Xbox just using just your TV and a standalone DVD game, the way I remembered. He said “This thing won’t even start unless you are connected to the internet.” In a rare moment of personal insight I just left it there and continued with my overdue shopping for others. I know some of my limits and a gaming device with a live internet connection and knowledge of my credit card details is one of them.

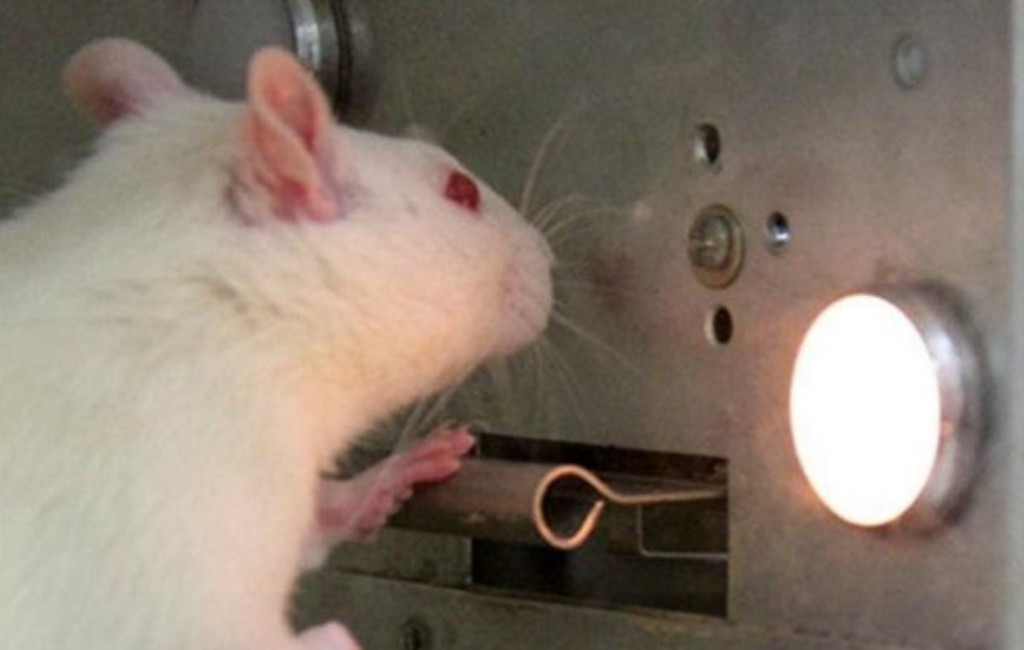

The whole experience piqued my interest in what makes something, anything, addictive. I came across some interesting records of studies commenced by psychologist Burrhus Frederic Skinner from some 80 years ago [4]. By this time he had already conducted extensive experiments on reward and punishment with laboratory rodents. He turned his attention towards the intervals of reward. Imagine a situation where three mice are exposed to three identical looking levers in three separate and otherwise identical chambers. The first lever gives a food pellet on every press. The second lever never gives one. The third gives a food pellet at random. These studies found that the mice with the first lever quickly became comfortable and confident of their food supply and tended to relax and press the lever only when they were hungry. The mice with the second lever gave up after a short time, getting no reward to continue. The third group were the most compulsive with their pressing of the lever.

This is just one of the many weaknesses or biases we have hard-wired in our DNA. And computer game makers aren’t the only people exploiting our propensity to form bad habits. As investors we all have the potential to make ourselves an easy mark.

We can get addicted to the 24 hour news cycle, the constant company announcements, and the daily – or even hourly – whims of the market. If you have ever hit the refresh button on your online brokerage account then you know what I’m talking about – you have done your own little impression of a hopeful lab rodent. It is all designed, of course, for you to take action. To buy something, sell something, incurring brokerage or other transaction costs and expenses. To subscribe to some new service or pay some guy to deal with it all for you instead, so you don’t have to.

It can and should be simpler. There is big money presently being made from our confusion, our anxieties, our hopes. Money made from us as we strive to master better habits. Spend enough of your time thinking, reading and listening about personal finance and you will find the same themes. And they are simple enough to understand – although the more difficult skill to master seems to be that of putting them into practice. From George S Classon [5], to Warren Buffett [6], to Scott Pape [7] the broad principles appear to be unchanging.

I have started to think that in this respect personal finance is a bit like the health and fitness industry. New fads, diets, products, gyms and blenders seem to come and go but most of them are – at their core – new spin or efficiencies of some unchanging fundamental principles: Calories in vs calories out – ‘Eat less, move around more’. However, we are so much more sceptical humans when it comes to fitness products. We know that the fitness model on that 3am infomercial didn’t get to looking like that using that ‘Abs-inator 2000’ product. There is no need, nor will there be one, for a Royal Commission for anyone that didn’t feel they got their money’s worth from the Paleo diet. Maybe it is because since before the dawn of ‘Norm’ we just seem absorb this information by osmosis. I don’t know the answer, but I have decided to translate what little I have learned about personal finance into the language that Australians understand, that of sport and tucker.

Just a brief caveat before you peruse this very experimental Christmas recipe. I am not an expert in either field that I am talking about here. Nor am I necessarily particularly good at putting these things into practice in my own life, but sanctimony is another one of my Christmas indulgences so here it goes. These are just my personal opinions so please take them in the spirit they are intended and always get personal advice to suit your own situation.

Uncle Pablo’s Christmas Cheer – the Personal Finance Diet

Live below your means – control your costs generally. This is the worst part of any diet – the self-control bit – so we will get it out of the way first. On a diet you can’t just eat and drink anything you want. Same goes for money, you have to exercise some degree of control over your daily expenses. Where we can, the experts suggest we should put things on autopilot – taking us and our frail weak wills out of the equation altogether. Set up automated savings, bill payments and investment contributions to take place on the day your pay hits your bank account in the same way that you don’t include that Mars bar on the weekly grocery shopping list. Remove any temptation to sabotage yourself by ensuring both the cupboard and the every day ‘spendings’ account is bare.

Save. Just as you assign time in your life to diet and exercise a portion of your income should be set aside each payday. The money gurus all put this no-brainer as another first step before investing.

Let compounding work for you: Get out of debt and reinvest your returns. If you have changed your habits merely to build a buffer for a Christmas blowout you will soon be back at square one. Re-investing your returns is essential for you long-term financial well-being. The notion of virtuous circles will be familiar to anyone who has made lifestyle changes to diet and exercise. Just as higher muscle mass increases your ability to burn more calories stacking on the mass of your money pile increases your returns. Ditto for debt which is just compounding in the wrong direction – we all know from our own lives that poor decisions in diet and lack of exercise have a multiplier effect.

Control your investment costs. This is now a mainstay for modern personal finance. And yes, it is really a correlative or sub-section of number 1 of controlling your costs generally. Consider this to be like the ‘sensible choices’ part of the diet. Have you done the math on how far and long you have to run to burn off that 350 calorie piece of New York-based Cheesecake? It is natural to ask yourself if it is worth eating in the first place. If you decide it is not then low-cost indexing may be an option for you. You will save time, effort and almost by definition get market returns.

Unless of course you just love running. If you have found yourself on Strawman you love the financial equivalent of running and you want to have your cake and eat it too. There is always the potential for extra rewards for the active investor. However, be honest with yourself about the time and the difficulty involved in chasing these down.

There is an in between of course, the power-walking like a Prime Minister in a Wallabies tracksuit option. That is basically investing in anything in the top end of the ASX 200 that consistently pays a dividend. Each to their own.

Avoid debt leverage – or at least acknowledges its risks. Financing your investing with debt is like taking steroids: there may be some more immediate gains but it is almost always more dangerous than you think; there are regulatory issues that you need to be aware of; and you are almost certainly risking your long-term wellbeing. You don’t need to use it, and if you do you should acknowledge the degree to which you may be dealing with the unknown and the damage it could do.

Invest in your human capital. You study your sport to get better and your diet to see what low-calorie sweetener can make that kale smoothie more palatable, same goes with money. Basically, get smarter about money, working and investing…all whilst remembering that when it comes to shares a working knowledge of ‘Technical Analysis’ is about as useful as having a Masters degree in Phrenology. If you want to learn more about investing in companies then, in my opinion, you should focus your education on fundamental analysis.

Manage risks, and adequately insure against your downside. Hmm, I’m going to say stretching…much like I’m stretching this analogy at this point. Just as in sport your body or your equipment can fail you at times so too can your financial world be thrown into disarray by certain mishaps. You need insurance for what can derail you – such as your house, your car, or your ability to work.

Own a house – even if you were born after the 1960s have a crack at this. Given our national real estate obsession this one is well and truly in the common sense lexicon within Australia. Really this also properly comes under number 1 of controlling costs. Oh the sport thing? That concept was a couple of rumballs ago now…Maybe it’s like when you get good enough at your sport and you want to stop borrowing equipment and buy your own top notch stuff…Terrible link I know. I’m surprised I made it this far to be honest, which is incidentally my motto when it comes to both finance and any sporting endeavour.

Have a plan for your retirement. Finally, don’t let your twilight years become the first time you start to see your physical and financial health as being related. Most retirement calculators assume both your home ownership and your good health. The advice seems to be to squirrel away extra if you see trouble down the track and do what you can about preventable illnesses.

Merry Christmas and a Happy New Year to the growing Strawman.com community. May 2020 bring you good health and many happy returns!

Strawman is Australia’s premier online investment club. Join for free to access independent & actionable recommendations from proven private investors.

Disclaimer– The author may hold positions in the stocks mentioned in this publication, at the time of writing. The information contained in the publication and the links shared are general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser. For errors that warrant correction please contact the editor at [email protected].

© 2019 Strawman Pty Ltd. All rights reserved.

| Privacy Policy | Terms of Service | Financial Services Guide |

ACN: 610 908 211