MY LIFE IN MICROCAP LAND—APPROACH WITH WHIP AND CHAIR

As some of you may know, and many of you may not, I spent five years from 2012 to 2017 at Australia’s largest microcap investor. To be clear, I was not the micro fund PM; I ran a few other funds for them. However, I sat in countless investment strategy meetings, company meetings, and contributed many ideas (some good, some not), and witnessed firsthand the experiences of the micro fund. Since many SM investors are interested in this end of the market, I thought it may be useful to compile my observations and learnings from this time. They are my own opinions and, I suspect, may not reflect the opinions of some of my former colleagues……

Definition – What is a microcap

For this fund, and what is/was a generally accepted definition, a microcap stock is one with a market cap between $30 to $300m and covers all sectors. What is below $30m, you ask? Nanocaps! What’s above $300m? Small Caps.

Universe Size and quality

The universe is large, there is no lack of investment candidates, but the overall quality is quite poor. By quality, here I am referring to profitable businesses. Profitable businesses are in the minority. A random selection of microcaps would not produce satisfactory return outcomes; most don’t make successful investments. There is a huge number of speculative companies with ideas, implemented to varying degrees. The “hit rate” (without me doing the quant work) would be very poor due to the poor overall quality of stocks.

As the largest fund, there was rarely a day without a company coming through the door and sometimes up to 8 companies a day, selling their stories. A lot of frogs to kiss. Without some kind of efficient selection criteria, too much of your time is taken up in frog kissing. That was the first lesson, ruthlessly cull the number of stocks to research with an efficient criteria checklist. On what criteria to cull stocks? That depends on your investment philosophy, but I would tend towards profitability or at least cash generative.

Is running a Microcap fund a good business?

Well, there are easier ways to make a living. The problem is that with a $300m limit, you are inherently a seller of your good ideas; they go into the small-cap fund and are forever on the search for an adequate replacement. Therefore, success breeds portfolio instability, and there is a constant search for quality replacements. Imagine finding a company on its way to a multi-billion dollar market cap and selling it out just above $300m, it happens. You need a lot of skill to keep finding great new businesses, with such a poor universe. The losers stay, the winners move on, not good. One reason constantly thrown up as to why micros are a great hunting ground is that there is not much competition at this end of the market, so it is easier to find bargains. Well, there is less competition, but in such a competitive environment as the stock market, the belief that there remains easy profits and that some kind of structural inefficiency exists and you just have to turn up, is just as silly as the pure EMH imo, it’s like the opposite EMH argument (no inefficiencies or inefficiencies everywhere), neither cut mustard IMO. Less competition is countered by more risk and less information (which, of course, is a subset of risk).

Is stock picking harder in microcap land?

I would say for me, with my style and approach, definitely, but it may not be so for all. A full stock analysis for me entails going over a track record of financials for a full economic cycle and examining the impact of various conditions on the business, like competition, fluctuations in demand and supply issues, management track record at capital allocation, etc, etc. In microcap land, you are dealing with a huge lack of information. The process becomes a “peeling of the onion” exercise where, once a layer is removed, something completely different can emerge. That can happen in large-cap land, but to a much lesser extent, in microcap, it is usual practice, and you need a process to manage that. The ability to change your views relatively quickly in the face of new evidence, a very difficult thing for me to do and why I prefer large caps, where you have a bit more leeway and the consequences of inaction are usually not as severe.

Management is always important, but it is critical in micros. The lack of business information means an extra weight falls on the ability of management to manage these unforeseen and unpredictable (due to lack of information) investment risks. These are nascent businesses, often just one poor call can prove critical and puts extra onus on the management team. That means extra due diligence on who is running the company, their track record, do they have a consistent message, are they sellers at every opportunity, the integrity of the board, etc, all count more in micro land. Again, often there is a dearth of information, and it remains a let’s see.

Relying exclusively on publicly available company-released information, imo, still leaves too much undiscovered due to the lack of history with micros. A network of some kind is of real use here, with the reasoning that a source of information outside the company sources can be quite valuable, a small group of like-minded investors with aligned interests is of more importance here, for the reasons stated above. Often, casual comments made by associates of the company were just or even more important than a company presentation, which is usually persuasive.

Living on the edge of the investment universe

Micros are peculiar investments. They are more open to the investment and liquidity cycle than other classes of shares. As liquidity floods across the stock universe, it usually starts at the large caps and then flows down the market cap list. Sometimes, excess liquidity doesn’t make it to micros; they stay flat as if nothing has happened. Then, sometimes, they do get attention as excess liquidity looking for returns, and liquidity flows down the market cap universe. Of course, micros do not have the liquidity to supply this demand, and stock prices spike higher, which attracts more attention, and spike higher again. The upshot of this is you can wait for years for something to happen to the share price, and maybe it doesn’t, and then you can have it all happen very quickly. If you believe, like I do, that in the LT share prices are correlated to cashflows and earnings, this just brings forward demand, and a drought can be expected after the flood. It is a strange world. We saw this as the fund would seem to struggle forever, then double in short order. You had to be still alive when that occurred to get the benefit. These comments refer to the microcaps as an asset class.

More comments about stocks

I cannot recall how many micro stories I heard over the years there, a huge number, from the sublime to the ridiculous, ok, more ridiculous. The interesting thing was that almost every story had a supporter; there was a hook in the story that would snag at least one guy.

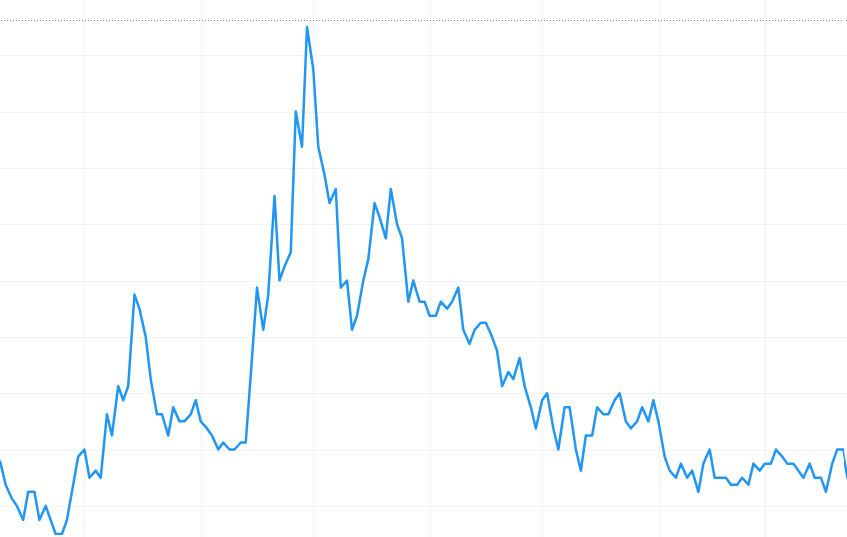

Without naming the stock in the chart below, it shows the base case of a micro’s share price action, imo. We see the emergence of a story, which could be an “exciting” IPO, some theme that has played out in the US, now Australian investors are looking for proxies, and could be some surprising positive announcement, whatever. The peeling of the onion plays out. If you play in this space, it is imperative that your process has signals that handle this share price outcome. That is, when the thesis is broken should be made as plain and clear as possible. There are few safety nets in micros; the end can be harsh. The low hit rate means that the below is the most likely outcome; up and to the right forever is nice, but very rare.

Put another way, lots of things can go wrong, as well as right, and the investment case is often very fluid. Broadly, I call this investment style taking on development risk. You need to have a decision-making structure to identify when the story is off track and the odds of success are now much lower than previously thought. At least as an individual investor, you usually can easily get in and out, unlike the case often for institutional investors. Be prepared for the below if/when it happens.

There is an enormous skew of returns in micros, as can be expected given the huge range of likely outcomes from a low market cap. Often, then, the strategy suggested is a venture capital style one. That is, you have a bucket of, say, 12 stocks. The investor is, of course, bullish on all, but it is unclear which stock will be the winner. Given the low hit rates, it takes one big winner to cover the disappointments of the rest. I couldn’t live with that risk given my investment objectives (retirement income and where my equity investments make up, by far, the bulk of my wealth), but it may have a place in a satellite strategy, but that’s not for me. I also point out that there is not much margin for error between getting one big winner and getting none, an outcome I am not willing to contemplate.

Many times, analysts would hold a valuation way too long, ok, that’s a problem with all share investing, the difference here with micros is that the ending can be terminal. Micros are much more fragile businesses than established large caps, and your investing strategy must adjust to this fact.

As an overarching comment, I do find it interesting that the most difficult area of investing (IMO) attracts the most inexperienced investors. In a universe full of no revenue or no profit from ideas that may or may not be, it tests the best investors. To me, that’s what Buffett says when he states Berkshire jumps one-foot hurdles, not eight-foot ones, plus other countless similar comments, even micro investors like Ian Cassel rule out companies with no profits. It should be noted that micro investing in the US has a much larger quality pool than Australia, and is, in Cassel’s words, mainly small profitable niche companies that dominate their space. Remember that when looking in Australia for micro treasures. I have also heard the story that if Buffett were starting again, he would be a micro investor. The 1950s were very different to today, and I suspect Buffett would be following an approach similar to Cassels, not investing in maybes, imo.

CONCLUSION/SUMMARY

For me, the experience of seeing micro investing in real life, even with the huge resources and the ability to access information unavailable to many, left me thinking it is a hard game to play, given my execution abilities and style that are not quite suited to this space.

How do I (that may not be you, given different objectives and skills) look at micros given the above?

1. Be very selective on coverage, very few would warrant the effort

2. Valuation is much more fluid in micros; a quality business is so rare, once found, bias action to hold it, look at the quality of the business, give valuation some leeway in the early stages.

3. Have a thesis and follow it; you can get back in (much easier than institutional investors) if the story changes. Keep a list of critical criteria. There is little in the way of a safety net here.

4. Any chance to access reliable intelligence outside the normal reporting avenues is worth more here than higher up the capitalisation range. I admit hard to construct.

5. Remember there is no free lunch in micros, luck and risk play a larger part in outcomes in this end of the market, don’t allow that to lead you to the wrong conclusions, “resulting” in Annie Duke’s parlance.

6. Even though the larger part that luck and risk play in micros may be driving share price outcomes at times, maybe dramatically so, the investment “physics” of profitability, growth and duration still applies to businesses here.

7. Personally, in investing I am about repeatable processes to generate alpha, that do not relying on luck or risk, in that regard, perhaps the most unsettling thing about micros I found it very difficult to differentiate between winning calls and poor calls, ex ante, eliminating luck and risk is just harder at this end and that unsettles me as an investor. That is, I require a few more pieces of the jigsaw puzzle before I gain conviction. That is me.

8. Playing close to your pads is the best way to generate repeatable returns in micros. Imho. Otherwise, it also acts as a reconnaissance action; the earlier you find something, no matter how hard, the better off you are.

Strawman is Australia’s premier online investment club.

Members share research & recommendations on ASX-listed stocks by managing Virtual Portfolios and building Company Reports. By ranking content according to performance and community endorsement, Strawman provides accountable and peer-reviewed investment insights.

Disclaimer– Strawman is not a broker and you cannot purchase shares through the platform. All trades on Strawman use play money and are intended only as a tool to gain experience and have fun. No content on Strawman should be considered an inducement to buy or sell real world financial securities, and you should seek professional advice before making any investment decisions.

© 2025 Strawman Pty Ltd. All rights reserved.