By Matt Joass

Selling is a big blind spot for investors. For every thousand articles about when to buy a company, we’re lucky to find one about when to sell. Yet selling has a huge impact on our long-term performance. And the evidence is clear: most people are no good at it. But this weakness also provides the opportunity for a massive competitive advantage.

The Problem

It’s well known that a lot of individual investors suffer from selling biases like loss aversion. Recent research shows that the professionals struggle too. An impressive study found that professional fund managers, although pretty good at buying, are terrible at selling. It was a landmark study, so let’s unpack the findings.

“We document a striking pattern: while the investors display clear skill in buying, their selling decisions under-perform substantially…selling decisions not only fail to beat a no-skill strategy of selling another randomly chosen asset from the portfolio, they consistently under-perform it by substantial amounts.”

The sell decisions of professional investors are so bad that they performed worse than chance. That’s rough. But the buy decisions did add value, so it’s not that fund managers have no idea about investing. Instead the authors found a flawed process where selling doesn’t receive adequate attention:

“We present evidence consistent with the discrepancy in performance between buy and sell decisions being driven by an asymmetric allocation of cognitive resources, particularly attention…We conjecture that PMs [Portfolio Managers] in our sample focus primarily on finding the next great idea to add to their portfolio and view selling largely as a way to raise cash for purchases”

“PMs in our sample have substantially greater propensities to sell positions with extreme returns: both the worst and best performing assets in the portfolio are sold at rates more than 50% percent higher than assets that just under or over performed. Importantly, no such pattern is found on the buying side – unlike with selling, buying behavior correlates little with past returns and other observables”

Most professionals have no good process for selling. They focus on buying, and only think about selling when they are fumbling around to free up cash. When they do sell, it is with little research. So they sell whatever sticks out the most: the biggest gainer or the biggest loser. It’s not logical, and they don’t think about the future prospects. The result is decisions that are so bad, they would have been better off throwing darts at a board to pick a position to sell.

This focus on past returns is also mirrored in much of the folk wisdom that floats around about selling:

- ‘Sell when a stock doubles (or is up 20%, or 30%, or whatever arbitrary number)’

- ‘Never sell at a loss’

- ‘Nobody ever went broke taking a profit’

- ‘Sell anything that falls by 10%’

- ‘Water your flowers and trim your weeds (sell companies whose share price has fallen)

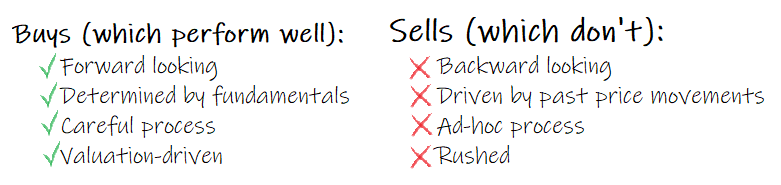

Intelligent investing is supposed to be forward-looking. It’s the future that counts. Yet all these rules of thumb, and the trading of the average fund manager, is based on past price movements.

The core problem is that most people’s sell process abandons all that is good about their buy process:

It’s a big problem. But there is a better way. My style of fundamental growth investing, led me to adopt two core selling principles:

Principle #1: Sell quickly when a thesis is broken

This principle has been a core driver of investment performance for me. Selling quickly when a thesis is broken allows you to ‘lose small’ when you have made a mistake. More importantly, it allows you to quickly re-deploy your precious capital in to a new high-conviction idea.

Like running a marathon, it is simple, but not easy.

There are five steps:

- Identify your thesis (actually write it out)

- In that initial thesis, identify what would cause you to sell

- Continuously monitor the company, its competitors, customers etc.

- Update your valuation estimate and avoid thesis creep

- Sell quickly if the thesis is broken

Let’s work through those steps with a real-world example: Class (ASX:CL1). Class provides a SaaS software product that helps Self-Managed Super Funds (SMSFs) manage their accounts. It’s a sizable industry in Australia, with over 500,000 SMSFs. It’s a growing market: each year more people’s retirement balances hit a size where it becomes worthwhile to consider managing it themselves.

Step 1: Identify your thesis (actually write it out)

Few investors clarify their thinking on why precisely they are buying a company. Even fewer take the time to actually write down that investment thesis. If you do, you will be ahead of the pack.

We must have a clear idea of what our logic is in the first place, so that we can know when that thesis is broken.

We first bought Class shares shortly after the IPO in early 2016. It was a simple thesis. Class was disrupting traditional desktop software – an inevitable shift to the cloud was underway. At the time of purchase, Class was dominating the new cloud-based market, and winning over two thirds of new cloud customers.

Even better, Class’ major competitor, the incumbent BGL Super, had stumbled with their first launch of a cloud product. We initiated a position and over the next two years Class’ share price rose over 80%.

It looked like the ideal investment, a scalable software business that was dominating a sticky niche, while a sluggish incumbent failed to adapt.

But that would change.

Step 2: Identify what new evidence would cause you to sell

The moment before you buy a stock is the last time you will be thinking objectively. It is crucial that you use this moment to write down precisely what new evidence would cause you to sell in future.

We identified multiple risks that could have befallen Class. The government could have changed the rules around SMSFs. A major security breach could have broken client’s trust in Class’ cloud service. Neither of those came to pass.

Another risk was that a competitor could somehow crack the market and start stealing share. Class would not be so lucky on this count.

Step 3: Continuous monitoring

Eternal vigilance is the price of superior returns.

We must continuously monitor for thesis-breaking evidence. That means keeping tabs on the company, its staff morale, its new products, customers, competitors, regulators, suppliers, etc. There are many tools that can help this along: Glassdoor, Google Trends, product forums, Google Alerts, investing forums. But that should be just the beginning. Superior returns require superior portfolio monitoring.

In the example of Class there was one obvious source of intelligence that most of the market somehow missed. Remember that big incumbent BGL? Well BGL would regularly release announcements about how their new cloud based product was progressing.

For a long time these press releases were mostly hot air. Every company claims that their products are market-leading, next-generation, cutting-edge. But in early 2017 it became apparent that BGL’s new cloud products were gaining traction. Talking to BGL’s customers, it seemed that the incumbent may have started to get its act together.

No company goes without serious competition forever though. So we were careful to avoid a knee-jerk response.

That all changed in October 2017.

Step 4: Re-evaluate and avoid thesis creep

Thesis creep is one of the great traps that ensnare investors, particularly value investors. The company reports some bad news, and rather than recognise the mistake and sell, the investor holds on.

The share price has usually fallen by this stage, which can allow the original thesis to sneakily creep its way to something new: “Sure, we originally thought the company would do XYZ, and it clearly hasn’t, but it’s just so darn cheap now, we couldn’t sell at this price”.

There were two new pieces of information that were released on the 5th of October. First, Class’ reported its latest quarterly update. It showed that the company’s net new account additions had fallen, dramatically.

In the comparable quarter a year earlier Class had added 11,880 new SMSF accounts. The same number in 2017 showed just 6,232 new accounts. A fall of 47%. And this was after a soft June quarter, which the company had guided would quickly rebound. To make matters worse, the chart the company usually reported which would have shown this fall clearly was no longer included.

Something had changed.

Later that day it was confirmed. BGL announced that it had now surpassed 100,000 accounts on its own cloud-based product. Worse still (for Class), their biggest competitor had added 23,402 accounts during the latest quarter.

When we first purchased shares, Class was winning approximately 66% of new cloud accounts. Now it appeared to be winning just 20%. That’s a huge swing in competitive position. We updated our intrinsic value estimate with the new information. Lower growth and higher acquisition costs meant the shares were significantly overvalued.

It was time to face a tough truth.

Step 5: Sell quickly when the thesis is broken.

Class had been a star of our portfolio. I had even interviewed the CEO in a fireside chat at a client event. It wasn’t easy to reverse course and admit that we were wrong. But when a thesis is broken, we must be decisive.

We reached our sell decision on the same day the news broke. Although the shares were already down slightly, it would take many months for the market to fully absorb the new competitive paradigm. We were able to exit our position for a 67% gain.

It worked out well. Today, almost 18 months later, the shares are now over -50% below where we sold.

Sell quickly when a thesis is broken.

Principle #2: Sell if you would not be buying today

Holding is an active decision, not a passive one. It just doesn’t feel like it.

Each day the market offers us the opportunity to buy or sell our shares. Every day that we hold a position we are effectively choosing to ‘re-purchase’ it at today’s prices, and in today’s position size. If we don’t think that the current position size is the best possible allocation of our precious capital, we should sell.

This principle – to sell if you would not be buying today – includes those situations mentioned in the first principle. But it also adds the hard edge of a valuation-based sell. If the share price has risen so much that you would not be buying the shares today, it is time to sell. No business is so great that its share price can’t rise high enough to render it an unattractive investment.

It sounds simple, but again the execution takes work. It requires maintaining an accurate estimate of the company’s intrinsic value, and being willing to trim the position, or even sell out entirely, when share prices rises too far above intrinsic value.

My personal approach to investing in high growth businesses is to sell slowly when the motivation is purely based on valuation. This is to reflect the ability of truly superior businesses to consistently outperform even the most optimistic estimates. It is both an art and a science, but ultimately we must be disciplined: sell if you would not be buying today.

Conclusion

Selling is a big blind spot for most investors. But that weakness means we have a huge opportunity to improve. If you adopt a sound selling process, based on the future and not the past, you will gain a massive competitive advantage over other investors.

This article was originally published on mattjoass.com

Return to the Strawman Platform here

Strawman is Australia’s premier online investment club. Join for free to access independent & actionable recommendations from proven private investors.

This Service provides general financial advice only, and has not taken your personal circumstances into account. Strawman Pty Ltd operates under AFSL 501223 . For more information please see our Terms of use. Please remember that share market investments can go up and down and that past performance is not necessarily indicative of future returns. Strawman Pty Ltd does not guarantee the performance of, or returns on any investment.

© 2019 Strawman Pty Ltd. All rights reserved.

| Privacy Policy | Terms of Service |

ACN: 610 908 211 | Australian Financial Services Licence (AFSL): 501223