I have been a bit annoyed by not having transparent information from Alcidion lately.

Case 1: No explanation of revenue going backward.

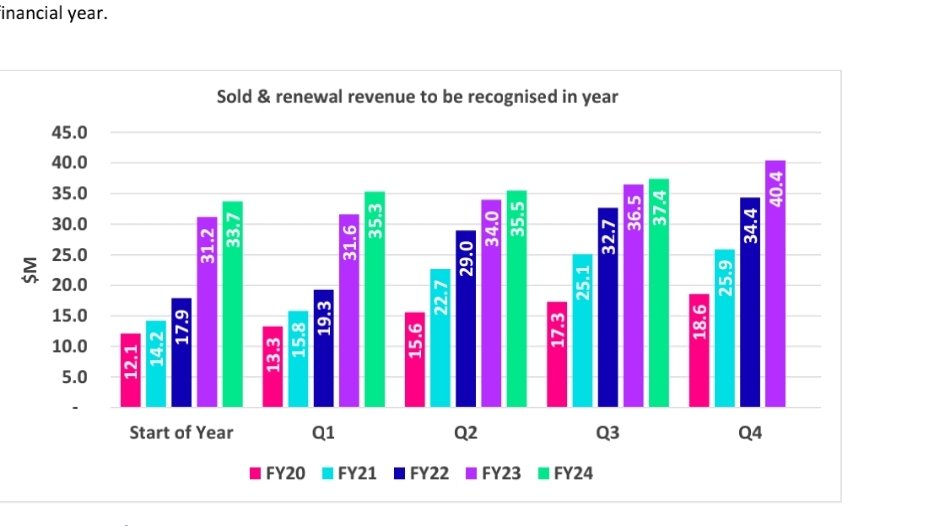

So at the end of Q3 FY24 they had sold & renewal revenue to be recognized in year = 37.4m

and then in Q4 they announced, new sales of $5m and 0.9m recognised in FY24 so that brings 37.4+0.9 = $38.3

At the start of FY24 they had $33.7m to be recoginsed and in FY24 they said they added total $6.2m in sales to be recognised in FY24, so technically, revenue should be $39.9m

I can understand if there is some issue and the customer is pulling back or delaying but I couldn't find any explanation in the report - What is the meaning of starting the number of $28m for FY25 that they have given - How can I confidently say that it will be recognised in this year? No idea

So I can only assume that, this reduction in revenue is on top of the things we can see slipped in FY24

On top of all this, the following - They didn't mention during acquisition capital raising - Just cherry-picking information to present to Investors I feel

Bit annoyed.

Alcidion released 4th Q update this morning, My initial thoughts

- Staff cost is looking much better now. ( Good for the upcoming period with lower cost base)

- Management reported new sales for FY24 at $35.3m but chose not to highlight them in the graph like in every 4Cs so far doesn't sit well with me. ( It would be better to show the graph as it is rather than hiding it)

Alcidion reported its FY23 report

Revenue:

Receipt from Customers

Expense

Operating Cash

No. of Shares

My view:

In the absence of an NHS contract, Alcidion currently looks like a slow growth company. However, I get a sense that Alcidion has significantly hired in anticipation of NHS contracts and because of those contract delays, expense has grown fast compared to revenue.

In one of the calls, Kate mentioned that it would be very shortsighted of her if she started cutting costs and suddenly had NHS contracts and struggled to find the resources to fulfill them.

Although Alcidion hasn't performed that poorly in the absence of NHS contacts - However, I anticipate there will be significant pressure on Alcidion's share price for some time because one of the co-founders ( Ray Blight) seems to be selling his portion after his resignation. He resigned on 30 June 2021 and also Alcidion's previous CFO Collin MacKinnon who retired last year is selling down his portion. ( Highlighted yellow in the screenshot below).

So If Alcidion wins large NHS contact sometime in the next 6 months, that will provide significant liquidity for them to get out ( if they completely want to) and then there will be more buyers than sellers hopefully.

Alcidion announced today that it had signed two Silverlink PCS contract renewals.

Along with this signing, these two contracts also trigger the earnout payment of A$2.8m agreed upon during the acquisition.

An interesting new update is that their current cash on hand is $15.6m Which is $4.5m more than the last disclosed figure as of 31 March 2023 in their 3Q 4C.

So two months of 4th Q have passed and their general expense of Q is ~11.5m so I think it indicates to me that 4th Q receipt will be in the vicinity of ~$15m.

So if we exclude this $2.8m payout, their FY23 operating cash outflow will be roughly 2m or thereabout.

Essentially, if it manages to sign a few big NHS contracts by the end of FY24, the Probability of them being cash flow positive in FY24 is very high.

sentiment currently for this business is very low.

Seems like the perfect setup for better performance compared to the index in my opinion for the next 2 years.

Alcidion released Q3 cash flow and commentary.

I was looking for Cumulative new sales graph which is obviously missing. ( Edit : I will take this as missed by mistake rather than intention as I could see this graph in presentation that was delivered in zoom meeting)

From Q3 FY22

From Q2 FY23

Another issue I find that, It advised the market in Q2 following,

I would expect Q3 to be huge if $5.2m of Q2 is delayed and landed in Q3.

FY23 EBITDA positive will not be achieved.

The only shining light is :

EDIT:

Kate seems a very open and transparent CEO and knows what she is doing. This is more of a confidence in management to deliver what they say. When Kate says that they is delay in NHS contracts - I am more inclined to believe her rather than be cynical.

I will hold my position because of strong and capable management

Just going through Annual report and few things stands out