Consensus community valuation

Discl: Held IRL 1.60%

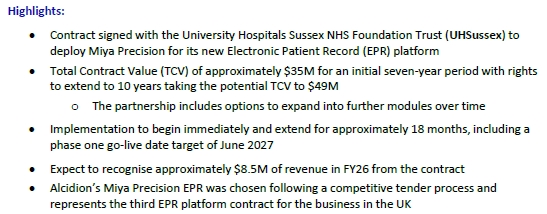

ALC finally signed the UHSussex Electronic Patient Records (EPR) Platform deal, as guided.

Reading a bit more into the announcement, a few observations:

- Coming off the back of a competitive tender process, the overall deal contained no surprises. Kate would have had confidence on her guidance all along.

- Both UHSussex and North Cumbria were via competitive tender

- The scope of modules include Virtual Care, the first time this module will be deployed to a UK customer to support the provision of care and remote patient monitoring for patients that may otherwise need to be treated in hospital - this will be a great UK reference site for the module

- The deal also excludes options to add Miya Emergency and Patient Administration System (PAS), which currently looks to be out of scope of the current deal and will add to the TCV - interesting this is explicitly mentioned in the announcement - could be a hint that ALC is already positioning/pushing this forward to expand scope.

- This UHSussex deal is bigger in value that North Cumbria - UHSussex is A$35m over 7 years vs North Cumbria’s A$37.5m over 10 years, potential TCV for UHSussex could rise to A$49m if it went the full 10 years - the ability to expand the contract size and add new modules a year later from North Cumbria is a positive

The deal announcement does not seem to have moved the share price. Planets have and continue to align for ALC. It is now all about being patient for the rest of the market to pick this up and re-rate at some point.

Discl: Held IRL 1.47% and in SM

Posting this on its own to make it easier to search later!

I took away the following from the Webinar:

1. Customer acqusition - major box tick as it adds 31 totally new customers (there were only 2 customer overlaps with TH) - QLD is key - with this single acquisition, almost all of QLD hospitals open up for ALC - this is very, very nice

2. Elimination of Telstra Health competition on Patient Flow - it is clear that ALC and TH clashed head-to-head on all things Patient Flow in ANZ, with ALC winning most of the recent deals. With this acquisition, the TH competition on Patient Flow is eliminated, paving the way for ALC to march forward with the Miya Platform minus this competition

3. Migrate to Miya and Upsell - Kate made clear, several times, that the end intent is to move Kyra Flow customers to the Miya Precision, both in ANZ and in the UK plus upsell other modules - this is very exciting indeed as 31 customers just opened up, in full, for this to occur

4. It is clear that the Kyra Flow Products are older, from the pre-cloud era, on-prem, and is not cloud enabled.

5. There is virtually no risk arising from the acquisition as Patient Flow is what ALC does best, it has been competing intensely with TH and know their products, and so, there should be little, if any risk of surprises arising from the acquisition.

6. Nice boost to the recurring revenue base - contracts are mostly 10 years duration

7. This appears to be a nice friendly acquisition - TH and ALC jointly agreed that ALC would be the natural home for the Kyra Flow Products

8. Financials look attractive - FY26 3.7m revenue, 90% of which is recurring and in support & maintenance mode, EBITDA $1.0m, positive working capital as billing is all in advance, there should be minimal R&D cost, only care and maintenance cost.

9. The earnout if focused on ensuring the current revenue profile stays, and customers transition to ALC nicely - makes sense.

This acquisition adds to my confidence in terms of Kate and ALC's consistency in strategy and execution against that strategy. That this was ANZ-centric was also nice as it allows for a growth pathway in ANZ to balance the overly-UK-centric growth focus.

@Tom73 , on Telstra Health, I thought it was right for Kate to play a straight bat on all questions relating to TH and their future, but she did make clear that TH is “no longer a competitor in the patient flow space” - she did say that as far as she knew, TH was existing the hospital sector except for billing, and consequently, TH has also exited the PAZ and Clinicians, both of which had a very small number of customers. I think this paves the way for ALC to play with Telstra on infrastructure, hardware perhaps.

Having been in this position as a customer before, I do expect ALC to move forward very quickly with this approach (1) to declare to the 31 new customers that ALC ain’t spending a dime on upgrading Kyra Flow (2) sign here please for Miya Patient Flow, the latest and greatest etc. This should happen throughout FY2027. This will be mostly positive as it adds upside opportunities from the upselling which ALC is now very nicely placed for.

But agree with @Tom73 and @Bushmanpat , this was a low risk, low cost and rather smart acquisition which does not dent the balance sheet or cause operational M&A grief. Very nice indeed!

Valuation (8/3/26) - $0.168

Buying 3 times very small positions from 2019 to 2022, ALC remains below any buy price, including in 30 March 2020! I hope we are through a very frustrating period with this business and a valuation can be done on reasonable expectations as growth and earnings stabilise somewhat in this lumpy business due to improved scale.

An equal weighted Bull, Base and Bear value I land at is $0.168 using a blended DCE and P/FCF (similar in idea to a discounted PE) approach through to FY30 with the general expectations shown below:

Sales growth is the main point of difference between scenarios, margins are the same in each increasing steadily form 82.9% in FY26 to 85.5% in FY30, which based on Kate’s statements should be conservative. For Bear and Base I assume operating costs increase 5% a year from FY27 and 10% for the Bull case. Capex + lease is around $1m +5%/year and I ignored working capital movements.

I see AI as helping via improved development efficiencies as much as it hinders in terms of competition. Seeing the conservative and glacial pace of the adoption of new software and services in hospitals as a moat, as it has been a barrier to growth so far for Alcidion, it will allow plenty of time to adapt to and mitigate competition response.

2026 is a ~$50m sales year in alignment with Kate’s outlook so growth rate is high this year, but the rate growth decay’s is what distinguishes the Bear case which goes into high single digits assuming minimal new customers from the Bull case which assumes solid expansion in the UK or the new Middle East/Canada.

NPAT% expansion due to operating leverage is the most significant value opportunity for Alcidion and what drives share price growth. The slow rate of customer acceptance and onboarding means sales are not going to leap forward at any great rate, but they don’t need to as long as they remain equally defensible as they are difficult to secure in the first place.

Valuation (1/6/21) - $0.30

Alcidion provides IT services and systems for hospitals to help manage patient flows and outcomes, mostly ANZ based but since 2019 also expanding into the UK targeting NHS Trusts. Recurring revenues in the form of long term contracts are forming an increasing proportion of revenue, but dissecting and projecting the types of revenue and margins is very difficult due to the rapid growth and transformation of the business over the last couple of years. The valuation detail and assumptions are in the straw with notes on the company and points of interest below. Due to uncertainty of revenue growth I have done a Bear, Base and Bull sales growth valuations to give a view of sensitivity to different levels of growth, but am working with the Base case rather than a weighting of bull/base/bear so will benchmark future results against the base only. General Impression on the company: • Leadership: With 2 co-founders on the board and the board holding around 30% of the company, there is more than enough skin in the game, experience and knowledge. • Growth & TAM: FY21 should see a return to growth of around 35%, from a slow FY20 of 10% and it is still early days in terms of penetration into the UK NHS Trust market with just 27 of them onboard in some way out of over 200 (FY22 NHS IT market said to be worth 4b pounds). The ANZ market also offers a lot of additional growth, so I don’t see any medium term speed limits on growth due to TAM. • Margins: The reporting of margins has changed in FY21 due to the reclassification of labour costs for service income now mostly being reported in Opex to give H1 FY21 margins of 88% Vs 26% for full year FY20. Messy, but I expect improved margins as recuring income from products (Vs services) increases as a % of income as the business grows. • Competition: The acquisition of ExtraMed has thinned the competitive field, but I expect solid competition from existing and new entrants into the field, however Alcidion has good momentum and traction indicating a solid competitive position and enough market growth that competition is not currently a significant limiter to growth – one to watch. • Industry: Med-Tech is big and growing rapidly, but hospitals are slow moving organisations so it is very challenging to get into hospitals with products but on the flip side, once you are in, it is very sticky. So growth is not likely to be exponential like a SAAS company due to time and resources needed to implement new customers, but revenues would grow with existing customers via cross selling and expanded use. Risks & Opportunities: • The US and European markets are not currently in scope for ALC, they are possibly a great opportunity, but also we may see competitive threats emerge from these markets. • Product failures pose a risk when operating in hospitals where lives are on the line – it hasn’t been a problem and probably wont be, but could be a company killer if a major problem occurs and governments step in. • Future acquisitions – both a risk and opportunity, depending on the quality, price and fit of the target company acquired. ALC is an acquisitive company so expect more. • Other: there is currency risk, legislative risk and key people risks to consider also, but I don’t see these as particularly elevated beyond normal levels of risk, but worth keeping an eye on. Product Notes: • I have not found sales by product, but given the complementary nature of the products (upsell/cross sell opportunities) it may not be possible to carve out specific revenue for these and services. • Services: ALC provides IT systems support for hospitals as a straight service business which is low margin but may be classed as recurring if under contract and also charges for implementation of products which a non-recurring service but leads to recurring and sticky product revenues. • Smartpage is an app based communication system designed to replace pagers, and acquired from Oncall. • Patientrack tracks patients’ needs and status within a ward, and has a considerable installed base in the UK. • Miya Precision allows high level tracking of how a patient is moving through the entire hospital system from admission to discharge. I first started looking at this business when it was 5c, but hesitated, unsure of it’s ability to grow, naturally by the time it showed it could the price was up significantly. Eventually I bought a very small amount of ALC in Sep 2019 then again in Mar 2020 for an average 18c price. I like it’s long term prospects, but will lighten my position if it hits 50c without additional justification, but only half and let the rest ride. That will allow me to ride the volatility I expect and not feel sea sick…

7-March-2026

$0.155 (range $0.06 - $0.28)

Following the 1H FY26 report, SM meeting with CEO Kate Quirk, and various commentary by StrawPeople, I've had a go at valuing $ALC.

Method: Projection of financials out to FY30 for 3 scenarios, with 3 sub-scenarios each; calculate EPS; value at a selection of PEs; discount back to end of FY26.

Assumptions:

- Annual Revenue growth of 12% (Low), 14% (Base), 16%(High)

- %GM assumed constant at 85% (lower than historical, but assume ongoing bundling with 3rd party products)

- % annual Opex (ex-D&A) growth of 6%-9% (Low), 7%-10% (Base), 8%-11% (High)

- D&A/Revenue = 11%

- Interest/Revenue = 0.3%

- WACC = 10%

- Tax = 30%

- Growth in SOI = 1% p.a.

Model Outputs

Commentary On Valuation

This is a low conviction analysis

Uncertainty on revenue growth is higher than modelled, given spotty history. Arguably, all cases are Bullish given that 5 yrs of organic revenue growth of 12% to 16% is completely unprecedented.

Confidence would be increased if UHSussex contract can be delivered in 2H FY26, and a new Trust added to the EPR "preferred vendor shortlist."

Potential for further upsides if good cost control is maintained, although eventual expansion into new markets may grow uptick in costs.

Model assumes one new NHS EPR system per year plus expansion on existing accounts and zero churn.

Conclusions

Last 9 months trading range of $0.10 - $0.14 indicates market is fairly pricing $ALC.

Market is not recognising the potential upside for $ALC; this seems reasonable given the patchy history.

I will maintain on Watchlist and re-evaluate at FY result. May initiate a small (<0.5%) research position, depending on demand on funds/other positions.

$ALC remains a high risk investment, and unclear that upside justifies the exposure. However, any confirmation that $ALC can maintain a steady tempo of NHS EPR wins while maintaining good cost control would point to this business being undervalued. However, given the coverage $ALC has attracted, the market would likely respond quickly to any such information.

Disc: Not Held

Discl: Held IRL 1.12% and in SM

A lot to like with ALC’s 1HFY26 results. The SM interview with Kate earlier this morning was helpful in providing additional context. Despite a string of good news, the ALC price has barely budged around 10-11c as the market does not appear to have noticed the progress at all. With maiden full-year NPAT appearing very likely in FY2026, think it is time to top up from my current very small allocation to at least 1.5%.

SUMMARY

- Very good 1HFY26 results

- Revenue up sharply, expenses under control, on-trend EBITDA, maiden 1H NPAT which should see ALC achieve maiden full year NPAT in FY2026

- Good sales and revenue momentum with the naterial UHSussex deal to be completed in 4QFY26

- $14.2m cash, no debt - nice, clean balance sheet

- Growth strategy still focused on Canada and Middle East - there is progress made on both fronts

- M&A is in the mix, but will be focused on new customer acquisition, market share expansion or geographic expansion, rather than new products.

OVERALL RESULTS

A good set of results, but not surprising given strong indication from the earlier Appendix 4C release

REVENUE AND GROSS MARGIN

- ALC’s seasonal pattern is such that (1) 1H Maint & Support revenue is stronger than 2H - recognition of Leidos annual licence revenue occurs in 1H (2) Capital Licensing revenue has been stronger in 2H than 1H but (3) 2H Total revenue tends to be higher

- 1HFY26 was a significant 44.4% jump from 1HFY25 and a 10.0% jump from 2H2025, a sharp above-trend outcome

- Driven by (1) full year impact of new customer wins in FY25 (2) expansion of the Leidos (ADF) contract

- The HoH increase over 2HFY25 is actually rather significant given that $8.4m of 2HFY25 revenue was from lumpy Capital Recurring licenses which did not recur in 1HFY26 - the jump in HoH revenue from Maint & Support and Product Impl & Services alone, was a whopping 62.2% - this is shown in the chart below

- Direct Costs were up 96.0% YoY, but moderated to 76.4% HoH

- Total Expenses were 18.1% up YoY, but only 1.3% up HoH

EXPENSES

Employee Benefits (full) has been trending downwards and remained flat HoH - in the SM interview Kate was clear that ALC will not go back to the pre-reorganisation 2024 headcount, AI is allowing ALC to do more with the same, but there has been some hiring of UK sales & marketing and deployment staff that could add ~$1m per annum, so instead of a downward trajectory, there will be an uptick in 2HFY26 and the trend should flatten instead

No concerns with this as the headcount increase in the UK makes sense given where things are at with the NHS

PROFITABILITY

Gross Margin

Gross margin was sharply lower, driven by material 3rd party partnerships signed during 1HFY26, Mizaic (North Cumbria) and Leidos. As this is recurring, gross margins will likely moderate closer to 82.5% moving forward

EBITDA, NPAT

Both EBITDA and NPAT are trending up very nicely indeed

While NPAT was already positive in 2HFY25, 1HFY26 is ALC’s maiden 1H NPAT - assuming nothing adverse occurs, in 2HFY26, ALC should end FY2026 with a maiden full-year NPAT

BALANCE SHEET AND CASH

$14.2m cash, no debt, 2H is historically higher for cash receipts - no concerns

SALES MOMENTUM AND DEPLOYMENTS

This was a good slide summarising the sales momentum

UHSussex - ALC is the preferred supplier, deal should be locked in in 2HFY26, ~$35.0m

GROWTH STRATEGY

Unchanged, but in the SM meeting, Kate has clearly stated that M&A is primarily focused on adding customers, market share or geographic expansion, not to add new products

OUTLOOK

Discl: Held IRL 1.19% and in SM

Can't hurt to boost AI credentials! My first reaction was "good luck to the AI" reading clinicians scrawly handwriting - the AI would have little chance, but then realised these will be typed text notes ...

As this is going to be offered as an optional module, this will be an early ALC-specific attempt at monetising a specific AI-driven capability/module - would be very interesting to see what the uptake is like.

Discl: Held IRL 1.10% and in SM

Noting 2 recent Substantial Holder sales of ALC into relative price strength. Doesn't look worrying given the small % sales but good to keep a close watch over it.

Firstly, a 0.74% sale of ALC from previous Chief Medical Officer and Co-Founder of ALC, Malcolm Pradhan, taking his holdings from 8.67% down to 7.92%.

Secondly, AustralianSuper has reduced its shareholding of ALC by 1.8% from 11.45% to 9.43% after ~3 years of no movement.

Discl: Held IRL 1.27% and in SM

Not a bad 4C from ALC today, mindful that 1H is seasonally flatter than 2H. In reviewing the results, I took the approach of comparing 1H-2H trends in the past 3 years to put this 2QFY26 results in better perspective.

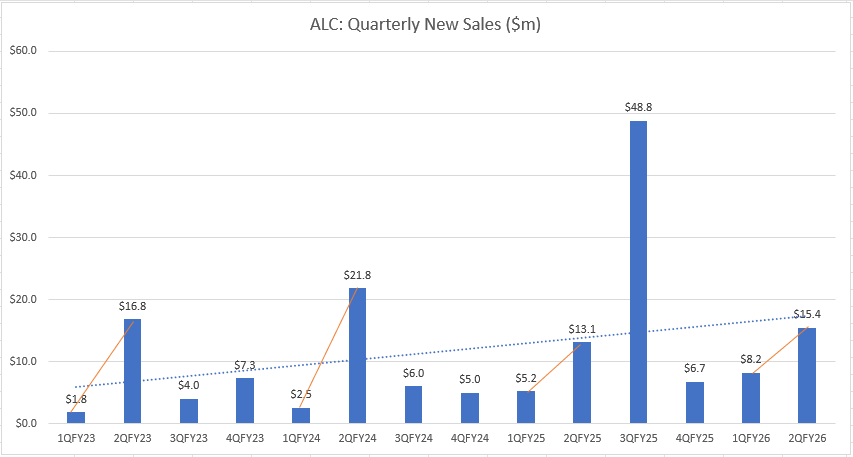

QUARTERLY SALES

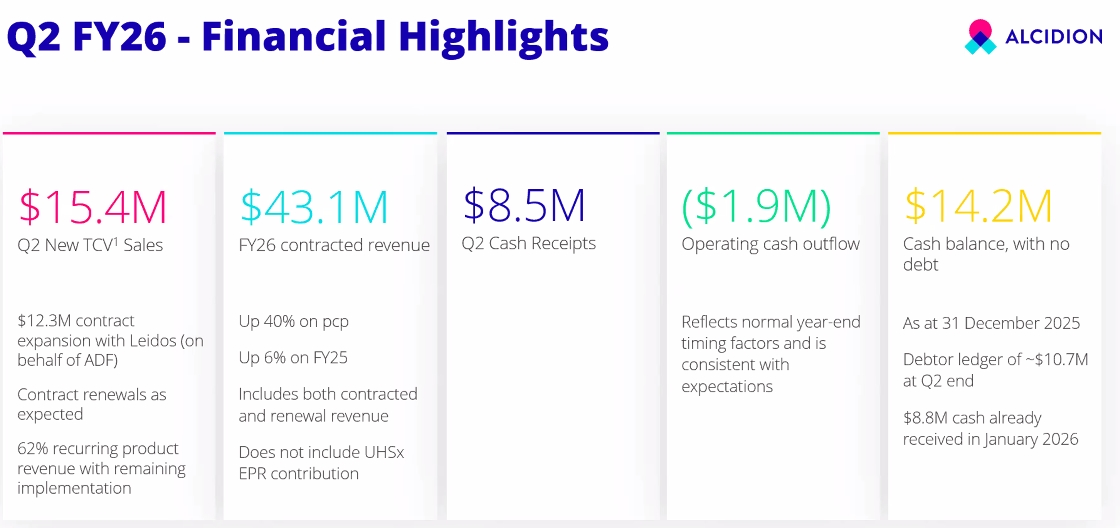

- New TCV sales of $15.4m, $12.3m of which is Leidos JP20260 project related which was previously announced

- Excludes the sales from the whopper UHSussex deal, where the contract is currently being negotiated

- The sharp rise in 2Q Sales vs 1Q in FY26 is consistent with that of the past 3 years, but is that little bit more impressive given the higher 1QFY26 sales vs the past 3 years, so no concerns here

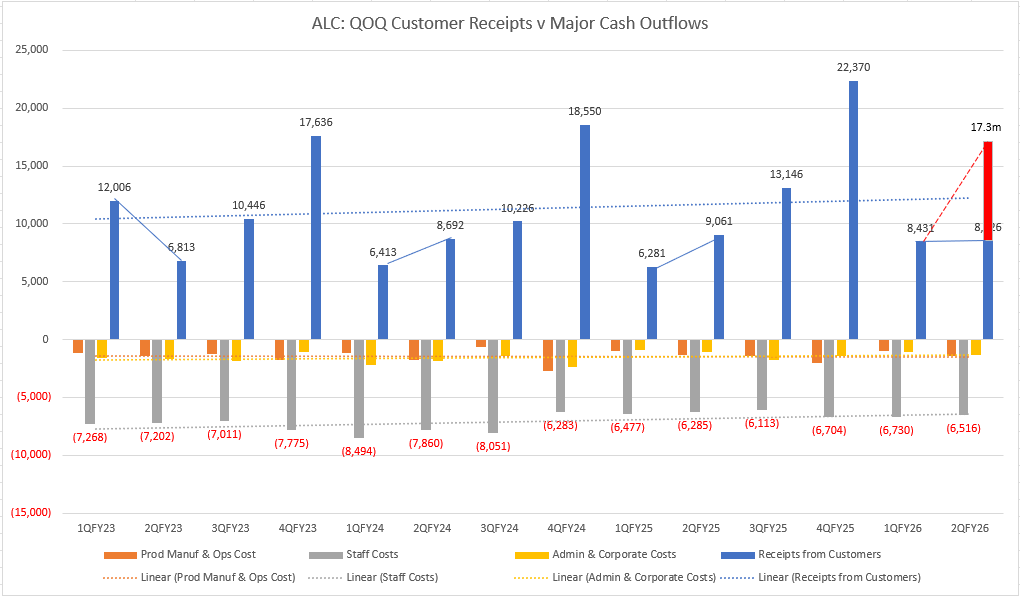

CASH FLOW - No Concerns

- ($1.9m) operating cash flow, $8.5m cash receipts was noticeably flat QoQ vs the past 2 years, but this is purely timing-related

- When adding the $8.8m cash that was collected in early Jan that tipped past 2Q, the cash receipts position (and by extension, the Operating cashflow position) is actually a marked improvement from the past 2 years

- Cash outflows are in line with seasonal 1Q-2Q trends:

- Ops Cost - jump QoQ is consistent with previous 1Q-2Q

- Staff Costs are on trend and generally declining - increased 3.7%, salary increases at ~inflation rate

OTHER KEY FINANCIAL POINTS

FY26 Contracted Revenue is up 40% on pcp but is already up 6% on FY25 at 1H, with a sesonally stronger 2H and the UHSussex deal yet to be accounted for - that is impressive

Cash balance $14.2m, no debt.

NEW SALES

- New sale not previously reported - 3 year Patientrack renewal with NHS Lanarkshire, about ~$1m

- Further info on UHSussex deal:

- 3rd EPR contract for ALC

- UHSussex was a Patientrack customer, with limited existing stakeholders - the EPR deal was won with significantly more stakeholders having to select ALC, reinforcing the significance of ALC winning this deal via a competitive tender in an existing customer

- Kate provided heavily caveated high-level guidance that UHSusex would likely be structured similar to the North Cumbria deal ie (1) ~$2m implementation cost over 24M (2) payment of 7 year licenses upfront (3) the rest being ARR

- The deployment of UHSussex will use existing resources coming off other deployments, may add 1-2 FTE in the UK for deployment, and ~1 FTE for ongoing support, marginal incremental cost is expected

- The UK is now reaching the end of the current 4-year NHS funding cycle, with the new funding cycle kicking in the new UK FY - Trusts are working out the funding possibilities

NEW MARKETS UPDATE

No real updates (1) Middle East - confirmed that there is at least a Patient Flow market, progressing conversation with potential partners (2) Canada - understanding market opportunity and targetting EPR customers

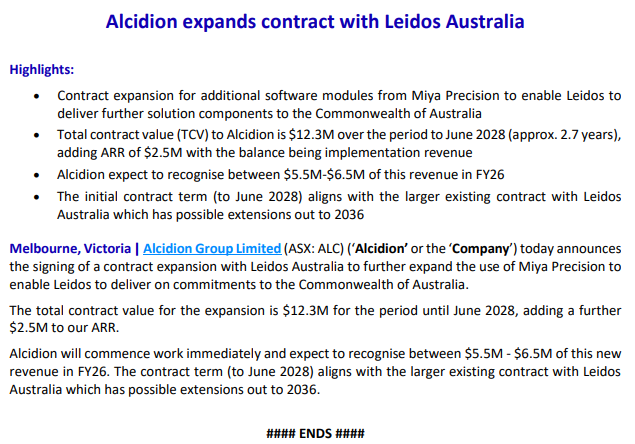

Alcidion out with a short and sweet announcement today (see below).

With the addition of the $5.5 - $6.5m revenue being recognised in FY26 - this should nudge them over the magic number of $40m in revenue which is what they have needed to hit FCF. Still circa 7+ months in the FY, so barring any cancellations they should now be at the FCF inflection point...

Disc: Held IRL and SM.

Discl: Held IRL and in SM

Appears to be a nice win from ALC:

- Very decent 18% TCV uplift from the original NCIC deal of $37.5m in Feb 2025

- Is a great data point that the NCIC deployment should be going OK - companies almost never uplift an IT contract pre-go-live, if the deployment is not going well

- Adds Electronic Document Management System (EDMS) capability into the Miya Precision ecosystem

- Provides another data point on the interoperability of Miya with 3rd party vendors - a good thing

What I am not fully clear with is:

- ALC’s net revenue from the uplift given that Mizaic is a partner with the solution, so a larger chunk of that uplift should logically go to Mizaic

- Margins thereof - should be high as the cost should mostly be around the development work to integrate to/from MediViewer

- Contract upsell opportunities arising - the para below says MediViewer is in 20 trusts today, but it does not say which of the 20 are existing ALC customers - if none are, then MediViewer interoperability could open some new doors or open smaller contract uplifts, if they are existing customers

But any win is a nice win!

Discl: Held IRL and in SM

Had a flick through of the ALC Investor Roadshow Presentation issued by ALC today. I don't normally expect to find anything new but this time, found a few new slides on the Medium Term Growth Strategy and Outlook, slides 27 to slide 32.

It puts a bit more flesh on themes Kate presented at the FY25 results, and looks like the Growth Strategy dry run that is due to be presented at the AGM.

As Phil Collins would sing “I can feel it (M&A) coming in the air tonight, Oh Lord .... "

Finally got a chance to have a closer look at ALC's FY25 results.

Discl: Held IRL and in SM

SUMMARY

There were significant positives in the ALC FY25 results, easily the most positive in quite a few half’s.

- A steady cadence of new contracts were signed in FY25, including the huge North Cumbria 10-year $39m deal - revenue grew 10% to $40.8m, ARR, which excludes capital license revenue, has risen 31% to $28.5m,

- Maiden full-year NPAT 1.65m, maiden full-year EBITDA positive $4.84m, positive EPS of $0.12 - this included a tailwind of $0.9m of forex gains, without which, both NPAT and EBITDA would still have been positive for FY25

- YoY Gross Margin expanded from FY24 86.1% to FY25 88.2% - driven by strong margin of 89.1% in 2HFY25 - given how operating leverage is kicking in, these appear sustainable

- Record year for (1) TCV (2) 2HFY25 highest revenue

- Balance sheet is strong - $17.7m cash, no debt - no concerns other than it might give rise to “M&A ideas”

- Record positive operating cashflow for FY25 of $5.8m, Net positive cashflow for FY25 of $4.9m - driven by record 2HFY25 collection, No capitalisation of R&D spend

- From my own calculations of Rule of 40 - it was big YoY jump of 17.2% from FY24 (6.2%) to FY25 11.0%

- With each new contract win and successful deployments, the Miya Platforms referenceability improves, improving the win probabilities

- Market tailwinds around the increasing urgency for healthcare to move to digitalisation to enhance efficiency remain intact

- Expansion has been flagged (1) Geographically to Canada, Saudi Arabia and the UAE and (2) Adjacent verticals into Aged Care and Community Care

If I had to point out a negative, it would be that the revenue now includes clearer visibility of “lumpy recurring” capital licenses. As these do not recur annually in a linear manner, only when contracts are renewed, and then not for all contracts necessarily, it does add a degree of lumpiness and unpredictability to the revenue stream. This is the same challenge with HSN’s earnings. But all revenue is good, so will just need to adjust expectations to this new reality.

HOWEVER, I have to admit being less excited about ALC turning this corner vs my other holdings. I think this is because ALC growth is now more “steady” than “fast”. It does feel that ALC is now on the cusp of scaling, although it will be more paced/steady and new-contract dependent, rather then rocket-like.

Investment Thesis Is Intact

Having turned the corner and now turning profitability, it does feel like the troubles in the past few years are behind ALC.

Kate summed it up nicely: “ALC has been right-sized and scaled to enable a matured, repeatable model to (1) add new capabilities (2) add new geographies”

This slide is a good summary of why my thesis of ALC is very much intact and I do want to remain invested.

ALC is current a shy of 1% holding in my portfolio, which reflects my excitement and expectations.

Will wait for Kate to reveal the ALC Growth Strategy towards the end of Sept and work out if I should increase exposure thereafter. Am particularly keen to better understand ALC’s expansion plans in term of geographies (Canada, Saudi Arabia & UAE have been flagged) and adjacent verticals (Aged Care, Community Care).

Detail is per below:

------------------------

Revenue and Profitability

The HoH and YoY charts show the following trends:

- Total revenue rose sharply in FY25 with the $8.4m of North Cumbria capital licenses

- Maint & Support revenue was flat HoH and YoY - the contracted revenue from the new sales wins in FY26 have not yet fully kicked in given the timing of when the contracts were executed - only the Hume contract contributed in full in FY25

- ARR has increased 31% to $28.5m - this is before any contribution from FY26 sales - this will underpin the higher proportion of recurring revenue for future periods

- Capital license revenue was broken out for the first time this FY - a good thing from a transparency perspective, but this is “lumpy recurring”, it will recur at contract renewal, rather than annually - this “lumpy recurring” is what the market is still trying to work through with HSN’s results

- The fall in Product Implementation revenue was expected with the winding down of the Leidos Implementation Phase in 1HFY25 - this will pick up in FY26 from the full-year services contributions from the North Cumbria deployment

- Technical Services revenue will remain flat - this is for annual services contracts

- Direct costs have remained very flat

- This has contributed to gross margins increasing to 88.2%

Costs have gone down (1) Fixed costs by 10% (2) Direct costs by 7% as a result of the change in ANZ contracts - this is on a nice flat/downward trajectory

Staffing levels are expected to be similar in FY26, with employee spend mostly focused on Sales & Marketing this year to drive further revenue growth

Which enable ALC to achieve its maiden full-year NPAT and EBITDA.

- 2HFY25 was another half-year record for revenue at $23.1m

- First FY that UK income contribution is higher than ANZ at 63% UK: 37% AU

- Capital Licenses are excluded from Recurring Revenue and Recurring Revenue %

Rule of 40

Used EBITDA and Maintenance & Support, Annual Licenses recurring revenue, in line with how ALC defines recurring revenue, to calculate the Rule of 40

Rule of 40 - big jump of 17.2% from FY24 (6.2%) to FY25 11.0%

Given the current trajectory on Direct Costs, Total Expenses and Total Revenue, expect the Rule of 40 to steadily rise

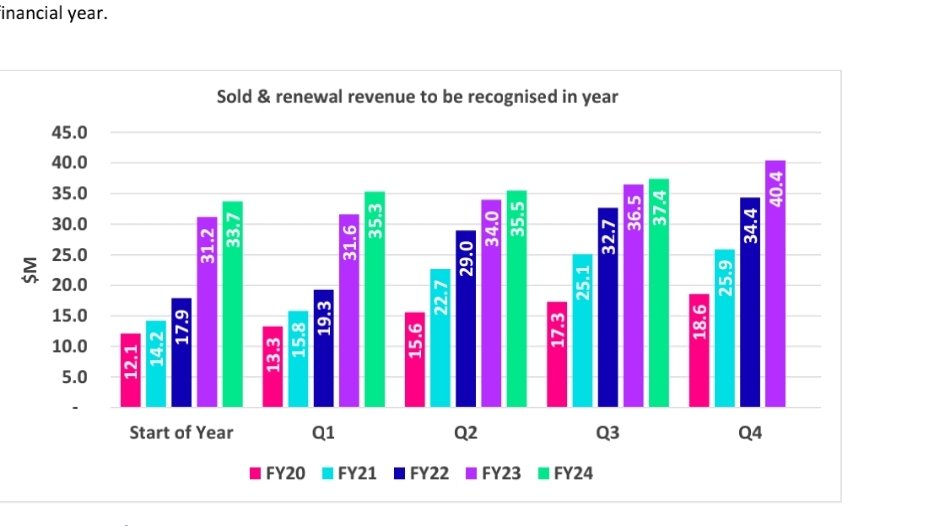

Contracted and renewal revenue to be recognised in FY26 is $34.0m, representing 83.3% of FY25 Total revenue

- Exploring new geographies - Canada (similar maturity to the UK), Saudi Arabia, UAE (similar maturity to ANZ)

- Exploring applicability of Miya platform applicability to adjacent platform verticals - Aged Care, Community Care

- The UK is moving out of an EPR focus - last major tenders expected in the next 1-2 years

- One of the 3 pillars of the NHS 10 year plan is to move from analogue to digital - this is a key tailwind for ALC, hence the investment in the UK leadership to position for this

- Unclear what funding is to be allocated to this pillar and over what timeframe

- Focus is very much on Patient Flow - ALC well placed for this with constantly increasing referencebility

Nice positive 4C update from ALC today. Key takeaways from me:

- Good feeling that ALC is increasingly gaining momentum - steady flow of contract announcements, changing of language to “expansion” is translating to cash flow and should translate to EBITDA

- Really good to see the positive trend and inflection into FY25 positive operating cashflow

- Major expenses appear to remain on-trend, and thus look like they are under good control

Onward and upward, it would seem!

Discl: Held IRL and in SM

Kate provided good context around the Q4 cashflow which included acceleration of (1) payment of 50% of short term incentives for staff and (2) payment of VAT/GST, both typically paid in Q1. Noticeable Q4 spikes in these cash lines vs previous quarters which should start 1QFY26 cashflows in a good position.

One to watch out for is that ~$8m of the cash receipts for the Quarter were for NCIC capital licenses - this will not recur in Q4FY26 for NCIC, will need to factor this when analysing Q4FY26 cashflows. This caused a bit of distortion with HSN’s 1QFY25 results, so am more weary of these 1-off capital licence sugar hits.

Not inconceivable that ALC used the capital license sugar hit to make earlier payments against STI’s and the VAT, so net, net, the Q4 cash flow result is still a pretty good one. All 3 lines should normalise in the coming quarters.

We had chatter on the forums around the impact of forex on ALC’s revised guidance a month or so back - there is a $0.3m positive FX movement this Quarter, not unexpected given the fall in the AUD in recent months.

While high Q4 cash receipts is expected, seasonally, what was nice to see is all of FY25 cash receipts swing upwards from FY24.

A sharp above trend uptick in cash receipts which is very nice

No concerns from the key expense lines (1) Prod Manuf/Ops Cost rose to support increasing revenue/cash receipts (2) Staff costs increased as noted above, but is mostly in line with the decreasing/flat trajectory - this feels under control and (3) Admin & Corporate costs fell QoQ - this has also remained flat, on trend

“Expansion” of contracts - a clear positive change this Quarter, indicating that the upselling strategy is gaining traction.

Good mix of expansion and new contracts across FY25 - modular platform is providing the flexibility to tailor solutions for digital health deployment across different customer budgets, readiness.

In response to a question, Kate confirmed that the materiality threshold for contract announcements is around $4m.

There was some mention of implementation delays in UHS and 2 other contracts, but Kate reported that ALC was ready to go, customer-end readiness/issues mostly - given the magnitude of change the ALC implementations will introduce, it is absolutely better to get it right late, than to get it wrong early, both from ALC and the customer’s perspective. Nothing worse than bad rap from a problematic deployment from both.

Nothing new with Guidance as this was telegraphed earlier, but always good to see the re-affirmation.

Cash balance of $17.7m with no debt is not shabby at all.

Other Points from Questions

- 27% non-recurring revenue, one-off implementation costs, in the first slide is from Q4 TCV wins only - does not reflect the full-year recurring revenue %

- 15% of the ALC staff base work on delivery projects - a good data point

- Seeing continued NHS commitment to digitalisation - waiting for Phase 2, which focuses on implementation, which is due in Sep 2025

- NCIC upfront license capex $8m, billed in Qtr

- Regional expansion - currently, revenue is roughly half UK, half ANZ - looking at Canada, Middle East as the 2 markets for expansion, South East Asia remains on the radar on a opportunistic basis

- Kate made the point that healthcare organisations are struggling worldwide, ALC is well placed, but they need to manage the balance and focus on upsell opportunities at existing clients, current UK/ANZ focus vs new customers in new regions - makes sense to me, given where things are at presently

Short and sweet guidance upgrade from ALC this morning.

- Fairly decent increase in EBITDA guidance of circa 50%

- Smaller contract upgrades always nice - but will take it with a grain of salt

- Interested to see what costs continue to be cut - there is a happy medium here.

Disc: HELD SM IRL

Decent quarterly update from Alcidion today.

Highlights:

- Upgraded guidance for FY25 EBITDA expected to be >$3m and deliver positive cashflow

- Q3 cash receipts of $13.1M with a positive operating cashflow of $2.5M (compared to a cash outflow of $1.4M in Q3 FY24) and includes no receipts from North Cumbria Integrated Care (NCIC) NHS Trust

- Q3 new TCV sales of $48.8M with $11.5M expected to be recognised in FY25 o Signed new $37.5M, 10-year milestone contract with NCIC NHS Trust to deliver new Electronic Patient Record (EPR) platform o Signed new 5 year, $5.5M contract with Hywel Dda University Health Board, our first customer in Wales o Renewed several PCS (PAS) customers

- FY25 contracted (sold and renewal) revenue stands at $40.2M at end of Q3

- Cash balance of $10.2M and no debt as of 31 March 2025 o Expecting a strong Q4 of receipts with a debtor ledger of $17.7M at the end of Q3

As illustrated by the graph of cash receipts (refer above), Q4 is historically the strongest period for customer receipts, a trend that we expect will continue in Q4 FY25, underpinned by a debtor ledger of $17.7M at the end of Q3.

Overall a pretty rosy update, are they rebuilding our confidence and trust?

Disc: Held IRL and SM.

Kate sold 5.0m shares from her holdings of 43.6m shares at $0.085, about 10% of her holdings. She still holds 3.2% of ALC, so still good skin in the game.

Not ideal but after 6+ years, she is perhaps entitled to reap some reward for the toil ... this (and Trump) could improve my top up price!

Held: IRL and in SM

https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02918351-3A662768

ALC is starting to look better with those new contracts rolling in. I have been underwater in this position for what feels like an eternity, and it's nice to see the SP nudged back from the edge recently (still underwater however).

Hopefully, things will continue to move in a positive direction.

Held in IRL & SM.

Held: IRL and in SM

SUMMARY

With a positive overall quarter, while growth is no longer at eye-watering levels, it does feel like there is steady positive revenue and contract momentum, mostly around Miya Precision/Patient Flow, amidst a relatively stable cost base.

- 2 new 5-year Miya Precision Patient Flow contract wins, 2 renewals, $13.1m sales

- $0.26m net cash outflow from operations, significant $3.0m improvement on cash outflow YoY ($3.37m) and QoQ ($3.86m)

- FY25 contracted revenue $30.8m, exceeding the $28.0m indicated contracted revenue outlined at the FY2024 results announcement - excluding North Cumbria, in final stages of contract

- Confident of a stronger 2HFY25, maintaining FY25 guidance of EBITDA breakeven and cashflow positive

- Cash balance of $7.7m, no debt

OPERATIONS

- $13.1M of new and renewal sales, with the majority being from new customers, with approximately $4.5M expected to be recognised as revenue in FY25.

- Q2 new sales comprised 88% recurring product revenue and 12% non-recurring services (primarily product implementation) revenue

- 2 new 5-Year contracts for Miya Precision via competitive tender:

- Five-year partnership with Northern Adelaide Local Health Network (NALHN) for use of Miya Precision platform to assist with patient flow and clinical operations including messaging, $4.5m TCV over 5 Years

- Peninsula Health in Victoria, which will see our technology help to improve patient flow throughout the hospital whilst assisting clinicians with mobile access to patient records, $3.7m TCV over 5 years

- Won all competitive tenders in Patient Flow in the last 12 months

- These new partnerships continue to validate the strength of our patient flow offering where we now have a material presence across the Australian acute healthcare market.

- 2 renewals:

- Extended ongoing relationship with Sydney LHD, which utilises Alcidion’s Miya Precision virtual care and remote patient monitoring offering

- Signed a two-year renewal for our PCS PAS module with Northumbria NHS Foundation Trust.”

- North Cumbria contract in final stages - this will be a material contract, once signed

FINANCIALS

Modest operating cash outflow of $0.26M, a material improvement on the same quarter last year (outflow of $3.4m), driven by an uplift in cash receipts from new business coupled with continued strong cost management disciplines.

Cash receipts in H1 FY25 were $15.3M with an operating cash outflow of $4.1M, an improvement of $7.3M over the H1 FY24.

Heading into the second half of the financial year, FY25 contracted revenue stands at approximately $30.8M, which does not include any contribution from the North Cumbria contract or other new deals that may occur before the financial year end.

- Exceeds the $28.0m of contracted revenue excl North Cumbria indicated in the FY2024 results announcement

The increased rate of larger contract signings has been the result of the execution of evolving and maturing pipeline opportunities, several of which are still progressing through the tender stage and into the selection stage of the procurement cycle.

We maintain our position of EBITDA breakeven occurring upon achieving revenue of approximately $36.0M and as result of our continued sales progress we expect to be EBITDA and cashflow positive for FY25

Just announced, I'll take this as well!

Would have been better if this was a Trust in the UK, but this looks like a reasonable sized deal to add to the North Adelaide deal last week.

This might warrant taking ALC out of the doghouse, at least for a bit of walkabout ...!

Discl: Held IRL and in SM

I have been a bit annoyed by not having transparent information from Alcidion lately.

Case 1: No explanation of revenue going backward.

So at the end of Q3 FY24 they had sold & renewal revenue to be recognized in year = 37.4m

and then in Q4 they announced, new sales of $5m and 0.9m recognised in FY24 so that brings 37.4+0.9 = $38.3

At the start of FY24 they had $33.7m to be recoginsed and in FY24 they said they added total $6.2m in sales to be recognised in FY24, so technically, revenue should be $39.9m

I can understand if there is some issue and the customer is pulling back or delaying but I couldn't find any explanation in the report - What is the meaning of starting the number of $28m for FY25 that they have given - How can I confidently say that it will be recognised in this year? No idea

So I can only assume that, this reduction in revenue is on top of the things we can see slipped in FY24

On top of all this, the following - They didn't mention during acquisition capital raising - Just cherry-picking information to present to Investors I feel

Bit annoyed.

Chart Update 20th Aug 24

I think we are going to see a drop soon down to between 0.44 - 0.50. While they had some good news recently, it will still take some time before it turns into contracts. They should be releasing their books full year soon and I feel the news of Alcidion being HNS prefered software has already been priced in.

Alcidion released 4th Q update this morning, My initial thoughts

- Staff cost is looking much better now. ( Good for the upcoming period with lower cost base)

- Management reported new sales for FY24 at $35.3m but chose not to highlight them in the graph like in every 4Cs so far doesn't sit well with me. ( It would be better to show the graph as it is rather than hiding it)

Bull case? Well its playing exactly how it should be so far. Im in the whole on this one from way back. To be honest Im pretty disappointed on this stock. So if Im to start working it again it will just be a token stake at the moment. I just dont trust it. Anyway heres the chart.

Chart Update Wed 17th July

Chart Update Mon 1st July

Another words, I dont know. News seems ok however I need to see the market jump on board before I add to my devalued share holding. My Av. holding is way above here as I enetered this stock green (not with envy either) and plan on digging myself out of the hole this position is in. Over all I think the company has a future or a take over (not so good).

Note wave 4 down. It went way lower than my rules allow. This next wave could technically be a wave 5 to finish off however Im also in favour of it starting a wave 1 again after the 5 waves down it just took for my so called w4. This is why I dont enter anything until I see the larger waves 1/2 and how they play out. I usually say "take this with a grain of salt" however this time I'll give it a "bucket of salt".

Daniel Sharp, ALC Director bought 250,000 shares.

Sounds like a lot but outlay was ~$13k, didly squat, similar to Kate's outlay.

On the back of Kate buying, has this been a Board-wide action to shore up confidence by having each director purchase SOME shares, I wonder?

This feels like another half-hearted, no conviction purchase. Better than zero, thats for sure, but doesnt quite move the dial for me.

Discl: Held IRL and in SM

Ok, so there's some cause for optimism in these results.

You can read the ASX announcement here, but the key points are:

- ALC has $37.4 in contracted and scheduled renewal revenue for the first 9 months of the year -- up 2% on pcp. And there's almost $3m in additional revenue to be recognised this year from new sales made during the quarter. Ok, so the revenue growth will look tame compared to previous years, but it should be positive and it should also deliver improved margins now they've reduced expenses by about $6.4m annually (hopefully not at the expense of future growth).

- Q4 (historically the best quarter, which is a pattern ALC expects to continue) will enjoy the full benefits of cost cuts, and the business is expecting to be cf +'ve in the second half.

- They have $6.5m in cash and said they have "adequate funds"

- Cash receipts down a little on pcp, but up 17% on the preceding quarter and there's $12.9m due from debtors (last year it was $7.3m)

- Basically cash flow b/e on an underlying basis, when you remove redundancy costs.

- Continued to sign up new trusts, which as Kate says help build their "referencability"

Despite the drop in the pace of growth -- which seems more to do with the industry environment, rather than the business itself -- the company is still moving forward. Maybe they lose some marks for ramping costs up too fast (although that's always easier to know in hindsight), and maybe they'll handicap themselves with less resources going forward, but the bigger picture thesis doesn't seem broken to me. Although i'd rethink that if they couldn't get back to higher rates of growth, or they lag on a relative basis next to other players in the NHS.

Last year shares were on ~4x sales, now they're on 1.5x. So i'm happy to keep my holding for now (about a 1.7% weighting).

Following @mikebrisy 's notes, I did a bit of googling to try to get my head around ALC's NHS opportunity. Some notes to add to the pot which was interesting for me, but may be old news for others:

- There are currently 215 NHS Trusts (googled "number of nhs trusts in england")

- A total of 189 trusts have now introduced new EPR systems, meeting the UK Govt's 90% target by end 2023 (189/215 = 87.9% but lets ignore the % for a moment!)

- Therefore 26 Trusts have yet to introduce new EPR systems

- The next target is for 95% of trusts to have an EPR in place by March 2025. The remaining hospitals are expected to go live the following year. https://www.ukauthority.com/articles/nhs-england-hits-national-target-for-epr-roll-out/ (there are many articles, carrying plus minus the same story, stats etc)

- "NHS England is investing £1.9 billion to support hospital trusts to either adopt a new or improve their existing systems. Last year it spent over £400 million to support 150 NHS trusts, and a further £500 million is due to reach trusts this year" (which @mikebrisy has pointed out, there HAS BEEN spend activity)

- To hit the 95% March 2025 target, 204 of the 215 Trusts must have an EPR in place by Mar 2025, so 15 more to go-live in the next 12 months, then 11 Trusts from Mar 2025/2026

- Because the budget is both for new and improvement of existing systems, that STG500m must fund 15 new Trust implementations and presumably, improvements to EPR systems in some portion of the189 trusts that already have EPR's

- There was a STG700m budget cut in 2023 which is presumably the driver to push out the end date to 2026 (and possibly beyond) . HSJ had the following article July 2023 which I could not access, other than the headline:https://www.hsj.co.uk/technology-and-innovation/digitising-all-trusts-by-2025-unachievable-after-700m-cut-government-admits/7035234.article

May 2022 Article below - behind a paywall, managed to dump this out before the super-quick free trial cut me out. While dated, of interest is the list of 27 Trusts, who at May 2022 do not have an EPR. This number coincidentally lines up with the 26 Trusts which need to implement an EPR in 2024-2026 from above, which we can infer from the Nov 2023 announcement.

Essentially, the list of 27 Trusts below, plus minus, is the remaining universe for ALC to implement an EPR in the next 1-2 years. We do not know which of these Trusts ALC are bidding for/chasing and we do not know the contract size of each Trust.

I think I am going to use the list of Trusts below and work out where each Trust is in the procurement process. Kate mentioned that there is quite a lot of transparency in the NHS Procurement process, so theoretically, we should be able to find out the procurement status of each trust that has at least started the procurement process. Each of the 27 Trust which awards to someone other than ALC in the coming months means there is one less Trust for ALC to win. This then puts a bit of a boundary around trying to define the NHS universe that ALC is chasing and how big the remaining opportunity is likely to be.

Would be good if everyone could post any EPR-related updates to the 27 Trusts below as the list must narrow in the coming months.

For me, this extra bit of information more or less lines up with what Kate has been saying, but I previously had no numbers against which to evaluate the extent of the opportunity/ies, the procurement and budget issues and ALC traction.

In summary:

- There has been budget cuts which has impacted the procurement processes and pushed out the overall Govt EPR timeline to 2026

- 26-27 Trusts need new EPRs, 15 by Mar 2025, 11 by "sometime 2026" - this is ALC's maximum possible uiverse

- Each award of these remaining 26-27 Trusts to anyone other than ALC, reduces ALC's maximum universe - this gives us a reasonably finite boundary against which to monitor ALC's contract success and momentum over the next 12-18M

- If 15 Trusts need to go-live by Mar 2025, the fastest EPR implementation that I can google was 5-6 months and the STG500M budget unlocks soon, ALC contract wins need to be rolling in by 4QFY24/1QFY25 and implementation must start 1QFY25, 2QFY25 at the very latest

- If ALC's contract traction remains muted in the next 3-4 or so months, it would mean that ALC's opportunity shrinks to the last remaining 11, by which time, the show could well be over ...

-----------

Almost 30 NHS trusts do not have comprehensive electronic patient records amid a renewed push by government to get electronic systems into all NHS hospitals, according to HSJ research. A total of 27 trusts - across 20 integrated care systems - reported not having EPRs in place when asked by HSJ (see box below). While some of these may use smaller-scale electronic systems in individual departments, several trusts continue to rely on largely paper-based patient records.

NHS England is also pushing for ICSs to reduce the number of EPRs within an ICS to help data flow more freely between organisations when needed and saving time for clinicians who do not need to learn how to use different EPR systems.

Miriam Deakin, director of policy and strategy at NHS Providers, said getting EPRs into trusts was a “significant task” and added it will be “challenging” for the NHS to meet the government’s target.

HSJ asked every NHS trust in England if they have an EPR, and – if not – whether it was currently procuring an EPR.

Although 28 trusts told HSJ they did not have an EPR — representing around 14 per cent of all trusts (excluding ambulance trusts) — HSJ understands that NHSE believes the number of trusts without adequate EPRs is between 35-40.

The regulator is thought to be aiming for trusts to be using EPRs which would achieve a level 5 HIMSS rating, which is an international standard for hospital IT. It is not known how many trusts’ EPRs would achieve a level 5 rating currently.

Several major teaching hospitals are among the 28 trusts which told HSJ they do not yet have an EPR.

This includes Liverpool University Hospitals Foundation Trust, Nottingham University Hospitals Trust, and Norfolk and Norwich University Hospitals FT.

LUHFT said it was currently procuring an EPR as part of a national programme launched last year to improve EPR procurement. In 2019-20, the trust pulled out of its EPR procurement after naming Intersystems as preferred provider.

NUHT said it was using “elements” of one EPR and had “plans to purchase the remaining elements in the next two years”, while NNUH is working on an joint EPR procurement with Queen Elizabeth Hospitals

All the trusts are outside London except Barking, Havering and Redbridge University Hospitals Trust and the Royal National Orthopaedic Hospital Trust.

Rory Deighton, acute lead at NHS Confederation, said trusts’ efforts to roll out EPRs quickly and effectively have often been “hampered by inadequate levels of available capital funding”.

He said the upcoming NHS digital health plan should “commit to providing leaders with the necessary support to roll out comprehensive EPR systems”.

Every trust which responded to HSJ’s questions said they were either in the process of procuring one, or developing a business case to secure funding in order to launch a procurement.

Several trusts indicated plans to run joint procurements for EPRs or align themselves with other trusts in their ICSs.

For example, University Hospitals Plymouth Trust said it was “working with our ICS colleagues, and under the leadership of the ICS, to set out our case for a future EPR for UHP and the wider system”.

Another trust, Stockport FT, said it had “started activities to progress with this key digital ambition for the organisation, working with our ICS, regional and national colleagues”.

Two trusts in Cheshire, Mid Cheshire Hospitals FT and East Cheshire Trust, said they had run a joint electronic patient record procurement and had chosen Meditech as their preferred provider.

The government has sought to get trusts to use electronic patient records since the early noughties, but its flagship programme to deliver this in the 2000s — the National Programme for IT — failed to incentivise trusts to adopt EPRs amid questions over their quality.

Ms Deakin, NHS Providers’ policy director, said procuring and implementing an EPR is “expensive and time consuming, but trusts know it carried real potential benefits for patient care and safety”.

She added: “Trust leaders know that it’s vital to get EPRs right but they are delivering this while overstretched staff are working flat out to tackle backlogs and deliver care to patients as quickly as they can.”

An NHSE spokesman said: “The NHS is focused on supporting local care systems so that 90 per cent of trusts have an EPR in place by December 2023 in line with the long-term plan ambition.”

Earlier this week staff raised patient safety concerns after four hospitals in Manchester suffered a “total IT failure”.

The trusts which told HSJ they lacked an EPR

- Doncaster and Bassetlaw Teaching Hospitals FT

- Worcestershire Acute Hospitals Trust

- Mid and South Essex FT

- Royal Orthopaedic Hospital FT

- Northumbria Healthcare FT

- South Tees Hospitals FT

- Torbay and South Devon FT

- University Hospitals Plymouth Trust

- United Lincolnshire Hospitals Trust

- Dartford and Gravesham Trust

- Barking Havering and Redbridge University Hospitals Trust

- Royal National Orthopaedic Hospital Trust

- Queen Elizabeth Hospital King’s Lynn FT

- James Paget University Hospitals FT

- Norfolk and Norwich University Hospitals FT

- Queen Victoria Hospital FT

- Robert Jones and Agnes Hunt Orthopaedic Hospital FT

- Stockport FT

- Northampton General Hospital Trust

- Sherwood Forest Hospitals FT

- Nottingham University Hospitals Trust

- Royal Cornwall Hospitals Trust

- North West Anglia FT

- Airedale FT

- Mid Cheshire Hospitals FT

- Liverpool University Hospitals FT

- East Cheshire Trust

Source: Information obtained by HSJ

Source Date: April and May 2022

From <https://www.hsj.co.uk/technology-and-innovation/revealed-the-27-trusts-still-without-an-electronic-patient-record/7032511.article>

Beleaguered $ALC reported their 4C this morning, with the investor call later this morning (I won't be able to attend so will have to catch up with the recording)

Their Highlights

- Q2 new TCV sales of $21.8M; $0.7M expected to be recognised in FY24

- Signed $23.3M South Tees contract extension for an additional 8 years (to 2033 with 2 years remaining on current contract) for Miya Precision Electronic Patient Record (EPR). Further options to extend out to 2038 and add further Alcidion modules which if taken would result in a total TCV of up to $54M over the next 15 years

- FY24 contracted revenue at end of Q2 of $35.5M, up 4% on pcp

- Sold & renewal revenue over the next 5 years (excluding FY24) of $126M

- Q2 cash receipts of $8.7M; up 28% on pcp, resulting in an operating cash outflow of $3.4M. Debtor balance at end of Q2 of $7.3M (PCP: $5.6M) which included $3.9M from a major customer which was collected in the first week of January 2024

- During Q2, raised $5.4M via Placement and SPP to ensure maximum flexibility and maintain a strong balance sheet to execute on market opportunities and drive revenue growth

- Cash balance of $7.9M and no debt at 31 December 2023, strengthened further following receipt of $3.9m in early January 2024

My Analysis

2023 was a horrible year for the company, and investors voted with their feet with the SP down almost 2/3rds and the SPP component of the capital raising towards the end of the year essentially shunned by investors.

My usual 4C Cashflow picture below tells the story - no discernible growth trends, a growth stock currently becalmed with the sails flapping in the breeze. I've added the TTM picture for operating CF over a longer timeframe, so you can more clearly see the adverse inflection over the last 12-18 months.

Within all the bad news there is the good news of the South Tees renewal - previosuly announced. We don't know the full terms of the deal in terms of margin; however, this is a high gross margin business, and such a long term contract with the potential to deliver average annual revenue of $3.6m over 15 years and act as a flagship reference case. The South Tees procurement team will have struck a good deal, you can be sure.

The blame on slow procurement is placed squarely on the customers, which I am not sure is totally justified. I have previously published a sample list of recent NHS deal announcements. Product and Sales Capability are two other factors in the mix, and there has to be question-marks on both.

Kate is turning her attention to managing costs, which she has to do. Taking direct control of the UK team by not replacing the MD is a significant step, and she'll have a tough year directly running a microcap operating on two sides of the globe. But that is the work to do, as it is a fight for survival now.

My thesis is broken, and I should exit. However, with the SP on about 1.2x expected FY24 sales there is every chance that some wind might be blown back into the sales. One or more material sales deals, which are as ever said to be in prospect, even a decent upsell to an existing customer would be positive catalysts. There is also the prospect of M&A - not a reason to hold on its own - but $ALC has to be on someone's shopping list at this level.

So, I am not going to shoot myself in the foot by exiting today. My position is small (RL now only 0.5%) and the damage is done. I'm a grumpy HOLD.

Alcidion reported its FY23 report

Revenue:

Receipt from Customers

Expense

Operating Cash

No. of Shares

My view:

In the absence of an NHS contract, Alcidion currently looks like a slow growth company. However, I get a sense that Alcidion has significantly hired in anticipation of NHS contracts and because of those contract delays, expense has grown fast compared to revenue.

In one of the calls, Kate mentioned that it would be very shortsighted of her if she started cutting costs and suddenly had NHS contracts and struggled to find the resources to fulfill them.

Although Alcidion hasn't performed that poorly in the absence of NHS contacts - However, I anticipate there will be significant pressure on Alcidion's share price for some time because one of the co-founders ( Ray Blight) seems to be selling his portion after his resignation. He resigned on 30 June 2021 and also Alcidion's previous CFO Collin MacKinnon who retired last year is selling down his portion. ( Highlighted yellow in the screenshot below).

So If Alcidion wins large NHS contact sometime in the next 6 months, that will provide significant liquidity for them to get out ( if they completely want to) and then there will be more buyers than sellers hopefully.

Given the interest in Alcidion recently there seems to be a lack of update on competitors.

Oracle has rebranded their Cerner Acquisition.and put NHS on the front page

https://www.oracle.com/healthcare/

I think Oracle will be very hard to dislodge. My logical thinking therefore is Alcidion could be an acquistion target.

But it won't be Oracle as they have already found their "dance partner" with Cerner.

In the meantime for many of you it would be good idea to go through the Oracle website. Maybe go through all the other competitors too which there are probably many.

On the flipside, I don't think Oracle has managed to dislodge the dominance of Xero with their Netsuite offering. So maybe there is still some hope. However Xero had a big headstart over Netsuite. Oracle also likes a "big bang" approach on deployments compared to ALC's future strategy.

ALC is on the watchlist but I think I need to see a bit more consistency on some metrics and get them to highlight more on the advantages over the incumbents. Maybe someone with more background and time here should do a SWOT analysis on their products versus competitors and do a kind of Gartner "Magic Quadrant". Also at this market cap with so many competitors I'm seeing better value elsewhere with better competitive advantage.

I agree with @NewbieHK and @Remorhaz that the $ALC result today was a postive.

I'll skip the usual summary of results and analysis and focus instead on an assessment of my usual CF trend analysis and take a look at contracted revenues. The common thought process I am bringing to all of my small caps that are approaching inflection is: "now that costs are under control and also now that we are seeing the organic growth engine exposed, is the revenue growth and operating leverage strong enough to make this an interesting investment?"

First some general observations:

- The selling of incremental modules approach appears to be working.

- The mix of renewals and new contracts is good.

- NZ appears to have reached a possible turning point. No point writing too much, as it is the size of an Aussie State, but worth a mention. Kate has commented before on the slow progress in NZ, because they have been impacted by the consolidation of District Health Boards into a consolidated structure. This kind of reorganisation plays havoc with IT procurement decisions because of all the energy that is consumed in the internal reorganisation. So I am sure they will be focused on trying to get a roll out of the module that is in place in one of the former DHBs. And after that more modules? Eventually, the new organisation will kick into action and start making decisions. (I have three members of my extended family working in the NZ health service, and the staffing pressures are as real there as in Aus and UK.)

- The key message of "we're saving clinicians time", be it doctors, nurses, or orderlies will resonate strongly with decision-makers, given the perennial staffing pressures in all markets.

- They are building strong "reference cases". This is important because public health services are not in competition with each other and openly share good practices, and coalesce around common solutuions. $ALC are doing a good job on social media with this, as others here have observed.

- Costs appear to be reasonably under control, with Kate setting clear expectations for FY24.

Now to the analyses.

1. CF Trend Analysis

Above is the usual CF analysis. I usually prefer to focus on FCF, but because of the acquisitions within the 8Q window I am going to focus on OpCF. (Although, you can see that absent the Silverlink earnout, $ALC is solidly in the exploitation phase with minimal capex.)

Previously, I have shown the trend lines over the entire dataset, but I am increasingly using the last 8Q, as above, because I think that is a better reflection of the impact of management efforts in the more recent capital constrained environment.

If you compare the above chart, with earlier editions, the good news is that the slope of the OpCF line is increasing significantly. Obviously, the very strong most recent Q helps a lot.

Given the high Q-on-Q volatility it would be wrong to say that the last 3Qs shows a positive trend. So, I won't say that! But the longer term trend is there. Again, I'm not going to show the FCF trend line, as the one-off Silverlink impact renders this meaningless.

2. Analysis of Contracted Sales and Revenue

In lieu of an explicit outlook, I've noticed that in each Q4 report, Kate gives a statement of how much of the contracted revenue is expected to be realised as revenue in the following FY.

So, in the graph below I compare that component of the CR (denoted as "CR(Q4-1)FY") with the revenue or the forecasted revenue from the FY (denoted as "Rev FY").

Above each blue bar (the CR), I plot the % of how much of the next year's revenue is already contracted.

You can see that over the last 3 years, it has been 69% (2021), 58% (2022) and 71% (2023), yielding and an average of 66%.

For FY24, I have used these %'s from the previous years with $33.7m of CR to be recognised as revenue in FY24 to project a range of forecast revenue outcomes for the FY24.

These revenue projections equate to FY23-FY24 revenue growth rates ranging from 19% in the low case to 45% in the high case, with a mean of 28% revenue growth.

This is where I have to write "past performance is no guarantee of future performance" and indeed, with a constant sales force going in to FY24, you might expect being at the lower end of the range to be more likely. It might even be lower (all things being equal) because a constant level of incremental sales represents a progressively declining % increase of each year's base.

However, if $ALC lies anywhere on that range, and provided costs can controlled as Kate has indicated, then we should expect FY24 to be both significantly cash generative at the OpCF and FCF levels.

(OK. I'll stop there and put my inner analyst back in the box).

My Key Takeaways

Overall, the $ALC analysis indicates that the company is passing through the CF inflection point. Given the very large Q-on-Q variations, it is important to take today's positive result in its wider context, and I think Kate's measured and qualified delivery did justice to that.

However, in the UK (and to a lesser extent in NZ), the health systems face particular head winds. In the UK the NHS is widely perceived to be in crisis. I have lived in the UK for 20 years and much of my business network and extended family live there today. At a personal level, I am aware of stories that show the system to be under stress, subject to industrial unrest and suffering from political interference. Kate made reference to these headwinds, and again to her great credit was very balanced in how she tells the story.

$ALC's continued progress despite these headwinds is encouraging. My only issue, is in the case of the UK, there is no end in sight.

I am considering increasing my position in $ALC. With the SP at 25 x EV/EBITDA(FY25), it is sitting between $M7T (12) and $VHT (38), and my current position size indicates a higher risk rating than it deserves. One to mull over, and I will likely wait until Monday, when $M7T reports. There's enough data now that it might even be time to build a DCF. Now there's a cheery thought.

Disc: Held in RL (0.9%)

Straw significantly edited as there were some errors in the earlier cash flow figures, now corrected.

Text also updated following the presentation Q&A and some observations added. Apologies for what is now a very messy straw ... but accuracy is important!

Figure 3 added to show the quarterly new sales from the presentation.

@Valueinvestor0909 has picked out the key issues.

Based on Q2 FY23 report we were all expecting at least $2m (edited from $3m) of the cash receipts (** see below comment) to be due to the late payments in the previous quarter. So the reported receipts of $10.446m are really only c. $8.5m (edited from $7m) from the quarter, so meh.

Also, Q3 Sales are unimpressive, - the graph wasn't in the 4C release, but is included in the presentation. (Edited out my earlier comment, throwing shade at Kate for not reporting this metric!) I've included it in Figure 3, below.

Taking a step back, I've updated my usual 4C Cashflow plot (Figure 1). And because $ALC is lumpy from Q to Q, I have plotted the same data in a trailing 12 months (TTM) format.

Basically, $ALC is running hard to stand still - there being no significant trend now in OpCF since the Silverlink acquisition.

I'm hanging on because Kate appears to be controlling costs well, and the UK implementations are providing reference sites. It should be expected for these implementations to take time, given the long sales cycle. So I am holding for now, but I think another year or so, and the strategy needs to start delivering operating cash flow growth.

** Comment:

During the Q&A today, one investor asked about the "late $5.6m receipt", to which the CFO (correctly) replied that the questionner was mistaken. He then clarified that there was a late payment of $2m in Q2 and, because some payments in Q3 were also received late, that Q3 receipts could be considered "normal" (swings and roundabouts argument). This confused me, because if this is true, why did they make a song and dance about it in Q2. Doesn't it just mean that a portion of payments falling due towards the end of the Q will always risk falling into the next Q?

CFO was adamant that Q4 will be the strongest receipts of the year. This is also in the release, so that indicates to me that >$13m Q4 receipt is in the bag. Given that the cost base is stable and investments are dialed right back, this means they will likely have a final Q that is OpCF and FCF positive.... provided they get paid ;-)

Key Takeaway

Management are trying very hard to get the most out of each quarterly report, for example, to achieve the (now abandoned) promise of being EBITDA positive this year. Personally, I think they are trying too hard to put a positive gloss on their communications. Now I don't believe Kate and her team would mis-state the facts, but they need to be careful with the spin, as it is easy to trip yourself up over time. For example, it is fine to talk about NHS staff shortages and strikes. But we all watch the news, and that is a characteristic of the market they are playing in. It is a fair headwind countering the tailwind of the drive to digitally emable the NHS.

I am observing a pattern in several tech holdings that, when sales and receipts in the quarter fall off the growth trend, there is a tendancy to talk about timing of payments, slow sales cycles, delays in renewals, and the strength/growth/record nature of the pipeline. (Examples from $3DP, $EVS and $ALC). As investors, we only have to wait 13 weeks to see if the story plays out so, thank goodness for the 4C and quarterly reporting! Equally, it is important to recognise that 13 weeks is a short period of time and the lumpiness from quarter to quarter can be very significant, as Figure 1 shows. It is as important not to over-react to one bad quarter as it is to over-react to one good quarter. Whatever the fair value of $ALC, I don't believe that today's result warrants a 10% markdown. Of course, using a cricket analogy, for every over that you don't hit the target run rate, it means more boundaries are needed in subsequent overs to stay on target overall.

Figure 1

Figure 2

Figure 3

Disc: Held IRL and SM

Alcidion released Q3 cash flow and commentary.

I was looking for Cumulative new sales graph which is obviously missing. ( Edit : I will take this as missed by mistake rather than intention as I could see this graph in presentation that was delivered in zoom meeting)

From Q3 FY22

From Q2 FY23

Another issue I find that, It advised the market in Q2 following,

I would expect Q3 to be huge if $5.2m of Q2 is delayed and landed in Q3.

FY23 EBITDA positive will not be achieved.

The only shining light is :

EDIT:

Kate seems a very open and transparent CEO and knows what she is doing. This is more of a confidence in management to deliver what they say. When Kate says that they is delay in NHS contracts - I am more inclined to believe her rather than be cynical.

I will hold my position because of strong and capable management

Just going through Annual report and few things stands out

Just had a chat with Kate from Alcidion who is at the ASA conference in Melbourne.

A couple things of interest:

She reiterated that their customers are hyper defensive. In fact, any funding squeeze tends to be good as they force hospitals to increase efficiency.

Cash flow positive and very comfortable with the balance sheet.

She's quite excited about recent wins and how they should be able to increase penetration with these clients.

Good momentum with sales.

Alcidion reported a net cash outflow for the 3rd quarter of $0.4m, although this was impacted by the settlement of M&A costs from the Silverlink acquisition. Excluding that, Alcidion saw a net inflow of $1.6m. Full results here.

In terms of customer cash receipts, the picture is pretty pleasing on a year to date basis:

But, of course, expenses have also increased. Here's a chart from Claude Walker to give you a better picture of the cash flow history (this includes the Silverlink M&A costs). Note that cash receipts for the 3rd quarter are below where they were in the previous corresponding period.

For the quarter, the company reported $12.5m in new sales TCV (total contract value). $4.3m of this will be recognised in this financial year. So far in FY22 (ie. the first 9 months) Alcidion has generated $42.9m in new TCV, of which $12.9m will be recognised this year. That's a 93% lift on the same period last year, and over 4x where it was in FY20

All told, it's a decent result, with a lot of new sales won so far this year. A slowdown in quarter cash receipts, when compared to the previous corresponding period, isn't great but may just be timing issues (hard to tell).

The balance sheet is in good shape, and with around -$0.5m in free cash flow, and over $17m in the bank, there's no urgent funding requirements. Indeed, barring a major acquisition you'd have to expect the business should be self-sustaining going forward.

No guidance was given, but I'm thumb sucking around $33m in FY revenue -- that's a 27% lift on FY21. Based on that figure, shares are on a forward P/S of 7.5x. That bakes in a decent amount of growth.

Alcidion's results were ok, with record cash receipts and cash flow positive for the qtr. $15.9m in cash at the bank.

FY revenue is expected to come in between $18.4-18.7m (up ~10% from FY19), and with $12.8m of contracted revenue already locked in for FY21. There's roughly another $4.5m locked in each year through to 2025.

For a business on >8x sales, it's really not enough.

$3.7m in contracted revenue was added over the quarter, double the same time last year. Over the past 12 months they've added around $14m -- but this is over multi-year contract periods.

It's great to be start starting FY21 with $12.8m already locked in, but remember that they started FY20 with $11.7m. Not all sales are recurring (~75% are), so there's still a lot of work to be won.

Still, i think that's possible.

With an expanded presence and resources, they should hopefully be able to build on the sales won last year -- especially given the covid tailwind. $6.8m in sales were added to FY20's starting position. If we assume $10m in new sales added for FY21, we'd get full year revenue of $22.8m in FY21 -- about 20% top line growth.

$50m in sales by 2025 would require this growth to be sustained over that period.

Definitely achievable, but I wouldn't want to bank on more than that for valuation purposes.

ASX release here