Discl: Held IRL 13.0% and in SM

The EOS price has gone gangbusters since the announcement of the Placement and Share Purchase Plan!

But more importantly, from a chart perspective, it has been texbook price action:

- From the 10 Feb 26 to 13 Mar 26 move up, it has retraced about 60% twice, almost perfectly to the $7.70 to $7.89 level, prior to this recent take off

- It made a new all-time-high today, peaking at $11.86 - nice bullish continuation

I took the arbitrage opportunity on offer by selling a small parcel today to lock in profit at $11.80 and will almost definitely subscribe to the SPP at $8.00. But am weary of overcooking the selling as it would be reasonable to assume that existing shareholders would be doing the same, the SPP would be oversubscribed and the allocation pared down as a result.

What is even better is this is BEFORE any new deals are announced, either MARRS or base EOS. If there are new deal announcements, the sky is the limit with the price ...

Discl: Held 11.17% IRL and in SM

SUMMARY

As EOS continues to grow into a global defence company, it cannot be constrained by a lack of capital to pursue the big opportunities that are out there - this is the clear management pitch.

Capital raises are never fun, but I can see and accept the rationale for this raise against the oportunities that are out there to win, especially with the Iran war continuing to “battle-prove” EOS’ capabilities and build significant pressure to buy more defence capabilities and have them delivered quickly - these tailwinds are highly positive for EOS.

Have lightened my EOS holdings to much more manageable levels over the past months, so I do have capacity to top up via the SPP, but overwhelmingly, I have not come out on top from SPP participation, so will need to monitor the price movement before deciding what to do.

Otherwise, I remain bullish with EOS - it has the products that governement needs across the spectrum of a layered counter-drone response capability.

THE RAISE

- Fully underwritten $150m Institutional Placement of approximately 18.8m new shares, representing ~9.7% of EOS SOI, falls under available placement capacity

- $8.00 per share, 9.3% discount to last closing price of $8.82 on Fri 15 May 2026

- Share Purchase Plan to raise up to $25m, up to 30,000 shares per eligible shareholder

WHAT HAS CHANGED

MARSS Acquisition

EOS acquired MARSS prior to the Iran war and since then, the Iran war has provided an extremely well timed battle-proven tick of credibility for the MARSS Nidar C2 system, significantly increasing the value of the MARSS business.

MARSS is custom designed for counter-drone warfare and is currently the only specialised C2 counter drone solution for the ME.

The war has provided the opportunity to demonstrate the effectiveness of the C2 system in protecting critical infrastructure in the Middle East from drone attack - most of ~60 installations have been installed and are actively protecting palaces, military installations, Saudi Aramco oil infrastructure among them. It was proven to be effective and consequently, demand for the C2 has surged.

MARSS EUR500m of sales has historically never been achieved but given the strong opportunity pipeline, have moved the stretch target of the earnout to EUR700m of sales to tap on this upside opportunities - the expectation is that the earnout cap will be reached in 6-12 months.

The C2 contracts are not one-off programs but are typically phased.

A$165m deal announced on Fri, 70% Capex, 30% Ongoing Support is a very typical deal size going forward.

Slinger

- Intense negotiations

- Significant opportunities in the ME

Space

- Strong interest from countries - potential European customers are actively engaging

- This was expected to only pick up from 2030 onwards, to drive the 2nd wave of EOS growth, but this has now been accelerated to today

High Energy Laser Weapon

- Netherlands Launch customer project - about 6M ahead of schedule

- Demand is now more intense than expected, negotiations in the ME going well

- Goldrone more likely in 2027 rather than 2026 - as the sale is still conditional, it has not been added to the orderbook backlog and thus has zero impact on any of the financials and orderbook. I have lost interest in this deal - it will happen when it happens,

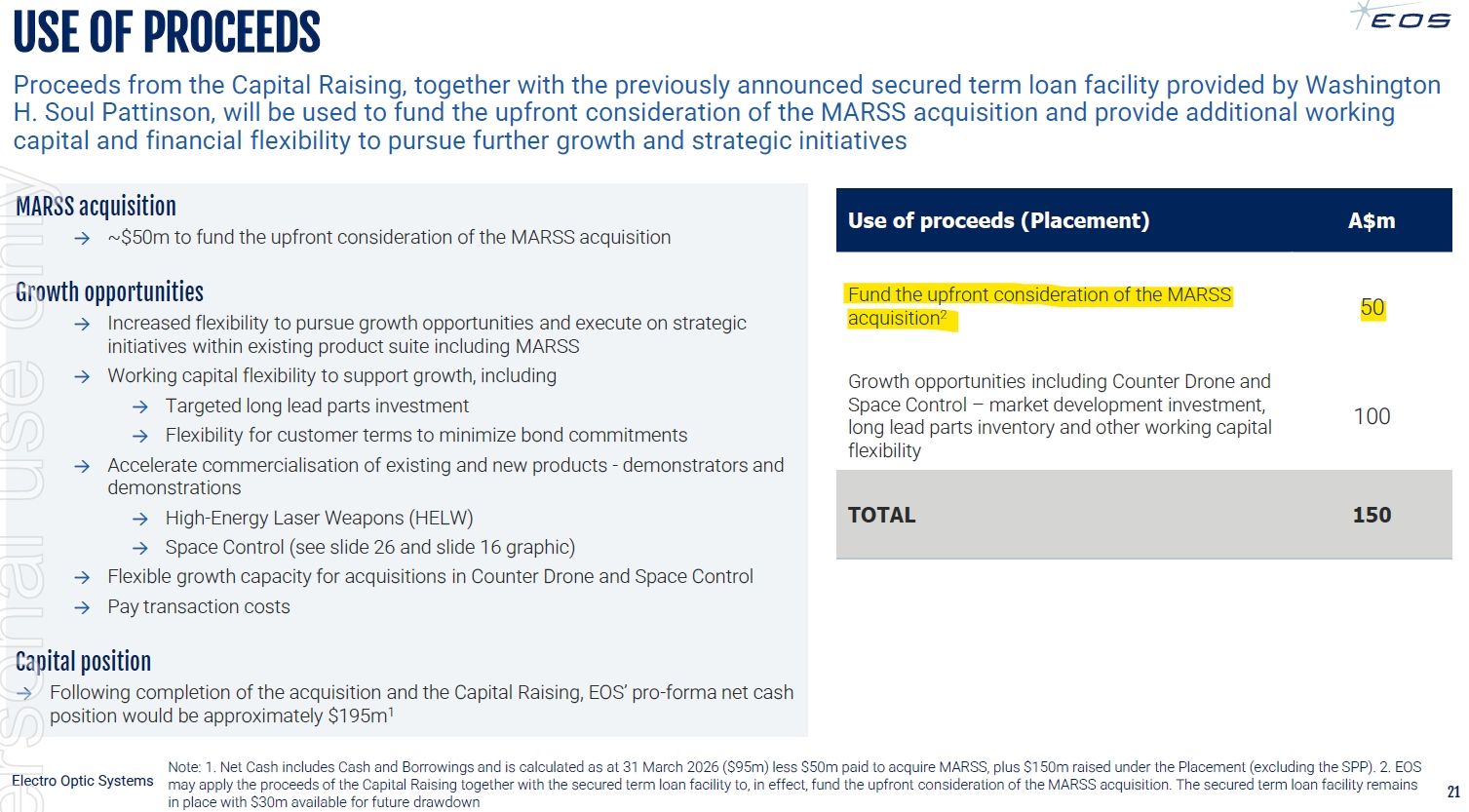

USE OF PROCEEDS

- Primarily to support the growth opportunities in both the MARSS and core EOS businesses

- Working capital and bank guarantee needs

- HELW - Need to invest in a HELW demonstrator, likely in Europe to demonstrate capabilities

- Space - invest in building a mobile anti-satellite system to help capitalise on accelerated market demand in this space

I am somewhat confused with the use of the proceeds to fund the MARSS upfront consideration as on Fri, EOS drew down that amount from the WHSP $100m Term loan to make that payment. I have asked Investor Relations for clarification.

Discl: Held IRL 10.70% and in SM

EOS issued a meaningful update of the MARSS Business and the MARSS Purchase Trasaction. I read everything to be positive as:

- MARSS’ Nidar system is now battle-proven in the ongoing Iran war - a major tick in the credibility of the solution

- Recent EUR102m order this month, customer enquiry and interest from industry participants have noticeably increased - very positive!

- MARSS Order Book of A$217m, which will transfer to EOS upon sale completion in the coming days, expands the EOS order book from $509m to 726m, a 29.8% jump - very nice

- Amended transaction items, most notably the EUR40m increase in earn out is smart and positive as it incentivises MARSS management to take advantage of accelrerating market conditions to secure EUR200m more orders from the baseline EUR500m orders, in the same original earnout period

MARSS BUSINESS UPDATE

With the ongoing Iran war, MARSS NIDAR systems is now battle proven - the NIDRA system has successfully protected critical targets infrastructure. Big tick.

MARSS is seeing accelerated customer enquiry and interest in its integrated and turn-key counter-drone capabilities.

MARSS secured new orders in May 2026 totalling EUR102m (A$165m) from an existing ME military customer - expands MARSS’ existing installations to deliver a country-wide drone detection and mitigation capability, with NIDAR C2 software at its core, expect to be substantially implemented in 2026/2027, ~70% of revenue and cash to be earned during the period, 30% will be for support services, to be recognised over 3 years thereafter.

MARSS’ order book is EUR135m (A$217m) as of today - a mix of one-off installation revenues typically earned over 1-2 years, and ongoing support revenue recognised over 3-5 year contracts.

In addition to the current order book, MARSS has several potential future opportunities with contract values exceeding $100m.

EOS total order book, including MARSS orders will rise to ~$726m, post completion of the sale transaction, in the coming days.

AMENDED MARSS TRANSACTION TERMS

Due to the current Iran conflict, demonstrable increase in customer enquiry and increased interest from other industry participants, for its systems, increasing the likelihood and size of contracts that could be sigfned during the earnout period and increase the value of MARSS. Key changes:

- Maximum earnout cap increased from EUR100m to EUR140m, a 40%, EUR40m increase

- Conversion ratio remains EUR20m for each EUR100m of order value, prorated for orders smaller than EUR100m

- MARSS needs to generate EUR700m of new orders in the 12 month earn out period from 12 Jan 2026 to earn the revised maximum earnout cap

- There is some change to the method in which the earn out is paid which is in a combination of EOS shares and cash - if the number of shares that can be issued per the original agreement maxes out the previouslyagreed placement capacity gap, then the remainder of the earn out will be paid in cash, so there is no further dilution impact, it appears

- EUR12m to MARSS can be advanced as advance earn-out payments to assist in settling of liabilities of the business not transferring to EOS, repayable to EOS if there is insufficient earn out in the first tranche period. This is no longer an issue as MARSS has already earned the first EUR20m earn out from the new May 2026 contract.

- Offer of a MARSS Director on the EOS Board if MARSS management shareholders collectively hold greater than 15% of EOS issued shares - the Director will fill a casual vacancy and be required to stand for reappointment at the first AGM following appointment and MARSS management shareholders agree that the Director will vote its EOS shares up to a 19.9% cap at EOS Shareholders meetings in accordance with the recommendation of the EOS Board of Directors.

FINANCE FACILITY DRAWDOWN

$70m of the $100m secured term loan facility drawn down to pay for the upfront MARSS acquisition cash consideration of US$36m

Discl: Held IRL 10.94% and in SM

No surprises or concerns from the EOS 1QFY26 Activity Report and Appendix 4C.

From the update on business development activity, the news/videos published on the EOS Investor Hub and the increased Marketing spend, I get the sense that robust business development/demo activity has happened this quarter, which should augur well for future new sales.

Chart Update

While the EOS price appears to be rather volatile day-to-day, the moves have more or less behaved quite nicely and consistently up and down the various support levels, in a still long-term bullish uptrend.

I have been taking profit into the strength regularly to lower my holding allocation, which is now down to more manageable levels.

BUSINES ACTIVITY UPDATE

Focusing only on the new news items from the update:

Manufacturing

- Manufacturing activity during the quarter remained high, in line with 4QFY2025

Contract Backlog

- Unconditional contract backlog at 31 Mar 2026 was $518m, a $59m or 13% increase from 31 Dec 2025

- Excludes any MARSS contract backlog

Market and Business Development Activity

- Goldrone - still ongoing, believes this will convert to unconditional in 2QFY2026

- High Energy Laser Weapon - discussions ongoing with representatives from Germany, France, Italy, Turkey, Saudi Arabia, UAE, India, Korea, Australia and the US

- Some Teaming Agreement/Strategic Partnership Agreements signed which have not been previously announced to the market:

- KNDS, a French-German defence company delivering advanced, interoperable mission solutions for the land domain - a Teaming Agreement to jointly identify business opportunities in new markets and customer segments

- ROKETSAN, Turkey, designs, develops and manufactures rockets, missiles, guided munitions and weapon systems -a Strategic Partnership Agreement on future opportunities involving integrated defence capabilities in selected markets.

- Milrem Robotics to jointly pursue new business opportunities and advance network centric collaborative combat robotics

- Probably no coincidence that these Agreements have been signed - could this be laying the manufacturing foundation for the HELW discussions ongoing with (1) Germany/France/Italy - KDNS? (2) Turkey - ROKETSAN?

CASHFLOW

- Cash Holdings on 31 Mar 2026 was $95.1m, down $11.8m from Dec 2025 cash holdings, no borrowings

- Secured a commitment to a $100m, 2-year secured term loan facility from Soul Patt, not drawn down yet

- Additional $54.3m of cash security deposits held with banks to support bank guarantees and bonds, a $12.7m QoQ increase

OPERATING CASH FLOWS

- Net Cash inflow was $9.5, vs the cash outflow of $19.3m in Q4FY2025

- Cash Receipts this quarter is roughly 3x that of 1QFY25 due to the significant increase in contract backlog - am more focused on the QoQ change as that is a more meaningful comparison against recent higher manufacturing and delivery levels - no concerns on this front

- QoQ, R&D Expenses marginally increased, Staff Costs were flat, Admin & Corporate costs were flat

- Marketing Expenses jumped 65% QoQ - this aligns to an increase in business development activity, both reported as well as news announced on the Investor Hub

- Product Manufacturing and Ops Cost increased 44.5% QoQ in line with high manufacturing activity

- No concern jumps out

Discl: Held IRL 12.75% and in SM

A few updates from EOS, 2 positive, 1 meh.

New US Orders US$17m

- Small US order contract updates of US$17m - feels like follow-up of paid Business Development, rather than a sale sale

- Small dollars but sets things up nicely for much larger orders in the future

Goldrone Korean High Energy Laser Weapon Contract Update

- Not dead, a bit more stuffing around, timeline pushed to Q2 2026, risk it may still not happen

- I am not holding my breadth for this to progress - it is absolutely not thesis busting of this does not progress as none of these is baked into EOS’ FY26 guidance, but am prepared for a sentiment hit to the price

- I was thinking that the HELW could be manufactured in the Middle East, but the Iran war has probably put that option on a back burner in lieu of freeing up manufacturing capacity for regional requirements instead

Director Purchase

Following the drama’s with CEO/Management sales 2-3 weeks back, very nice to see Non-Exec Director Robert Nicholson invest $70k of his own coin to pick up 8,685 shares at $8.06 per share.

While this is a small parcel, what is more interesting is that post this acquisition, Robert owns 146,332 EOS shares, which at $8.30, values his holdings at $1.21m. Nice skin in the game, for sure!

Discl: Held IRL 14.88% and in SM

The EOS price has been very volatile this week following the announcement that CEO Andreas, CFO Clive, and other management team members were selling their recently vested EOS shares. Andreas’ parcel of 1.5m shares was the central focus given the size and fairly quick disposal post the shares vesting.

There was also filings today that:

- Kate Lundy has sold 1/3 of her EOS shares, and has 18,431 left, value at about $182.5k

- Chair Gary Housell has topped up with ~$45k of his own coin,to add to the 517,647 shares he already owns which is worth ~$5.1m at $9.90. So he is still very decently invested.

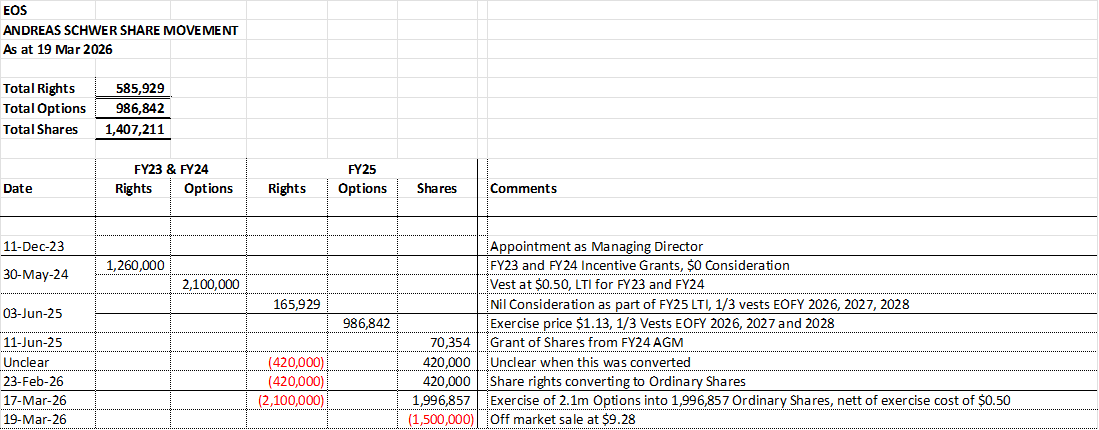

The history of Andreas’ holdings is per below:

The market commentary was interesting - this was likened to the DRO “shock disposal” etc and the EOS price copped a 20% hiding on Wed, about half of it has recovered since.

I have a different view:

1. Andreas has done a sterling job taking EOS from the pits to where it is today - for that, he deserves every dollar and share rights/options he has been granted - fair to say shareholders are absolutely reaping the benefit of his expertise

2. He has sold nothing since he was appointed MD in Dec 2023, but like all of us, he has bills to pay - I thus have no issues with him cashing his shares in, he is really entitled to do that with minimal fuss

3. EOS has a minimum shareholding policy in place and Andreas has significantly more shares than is required to comply, plus other options and rights still to vest, so he still has good skin in the game to keep going - quite unlike DRO where the Directors cleared the decks, owning nothing at the end of the process - EOS looks to have learnt from that and instituted the minimum shareholding policy in late CY2025, as Andreas’ plans to sell down would have been raised by then.

4. Thus from a Corporate Governance standpoint, I can’t find fault with how this has been handled - short of asking Andreas not to sell such a large parcel, just as they are vested, I really cannot see how EOS could have improved on this from a Corporate Governance standpoint - this was as orderly as could be is my view

5. I also appreciated the timely communications on the progress of the selldown

6. There was also mention of this sale occurring before potential issues are flagged with the Goldrone contract becoming unconditional, raising again other Corporate Governance issues around the deal diligence, then management selling ahead of any announcements. While Goldrone is absolutely a risk still - the deeper the delay in any positive announcement in March, the higher the likelihood is that the deal could fall through, it also ignore the clear facts that EOS management has repeatedly flagged that the Goldrone deal has not been factored into its outstanding order book or revenue forecasts for FY26, the structure of the contract to ensure that Goldrone is a viable counterparty etc. I still strongly believe that if Goldrone falls over, EOS and the Korean military will find another vehicle to proceed with the deal - they need the High-Energy Laser Weapon - a failed Goldrone is not going to change that defence need at all, I don’t think

The price action was also interesting as despite the sharp falls, the $8.90 to $9.25 support level has held very nicely all this week, suggesting that a decent base could well be forming here.

In short, other than the heightened volatility, which, to be clear, was stomach-churning, nothing has fundamentally changed.

I have continued to take profit at the current lower levels as I was reminded of the the adverse impact of a way-too-high holding on the overall portfolio during the recent drawdown. Will need to lighten another ~2.5%, to bring the allocation closer to ~12% still too high, but more manageable.

Discl: Held IRL 18.78% and in SM

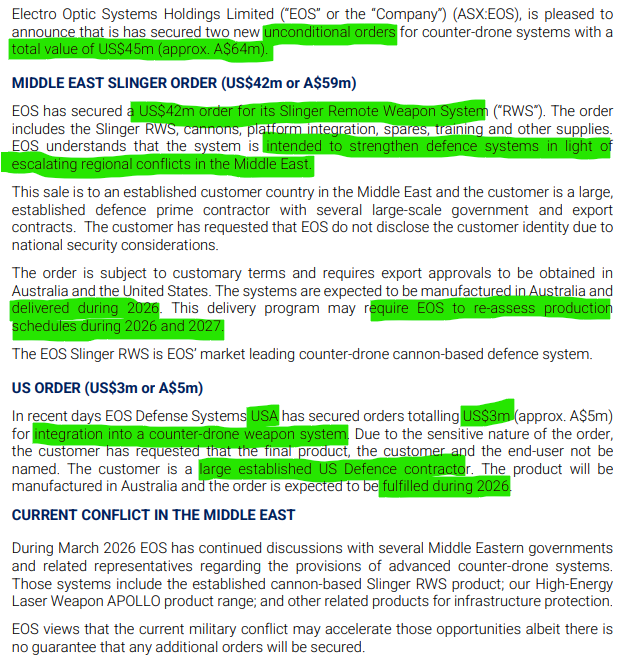

New Orders

I was wondering when new Middle East orders would come in for EOS, given that drone attacks have been front and centre in the Iran conflict, and got the answer today.

The market looks like it was expecting the same ... nice 16%+ pop today thus far, with today’s high, thus far, of $11.62 making a new all-time high.

EOS absolutely has the right counter-drone products for the Iran conflict - the Remote Weapon System, High-Energy Laser Weapon. This might also accelerate the Space products. The challenge will be delivery - these cannot be manufactured quickly. Looks like some re-jigging of the production schedule is already under way.

ASX Rap on Continuous Disclosure Gaps

The language of the announcement has also changed a little around the naming of counterparties.

EOS got rapped on the knuckles yesterday by the ASX on inadequate disclosures around the Goldrone deal. EOS acted promptly by reviewing and updating its Continuous Disclosure policy. I had a read of the updated policy but could not clearly see where changes have been made. Given that the policy update was already published, the rap did not concern me at all as EOS management has demonstrated diligence and focus in cleaning up and maintaining good Corporate Governance.

From today’s announcement, there is now a clear comment on the reason for non-disclosure of the counterparty. The acknowledgement of ASX’s concerns, the quick updating and publishing of the policy and the execution of today’s announcement against that policy is, for me, good evidence that EOS continues to take Corporate Governance matters seriously.

Have been continuing to take profit to lighten my significantly overweighted position, but in very small doses so as not to miss out on more upside from here.

Discl: Held IRL 16.55% and in SM

Latest EOS Chart. When EOS is not in aggro mode up or down, the price generally behaves quite nicely, "respecting" the various support and resistance levels, on the way up and down (more up, really).

It has very nicely respected the 8.90 to 9.25 support level all of this week. Hoping that this becomes the base for a crack at more decisively taking out the 10.80 level, the preious Jan 2020 all-time-high level, then 11.20 the current all-time-high thereafter.

Immediate downside is 7.70 to 7.89.

Discl: Held IRL 16.68% and in SM

A welcome update from EOS today - timing was either immaculate or deliberate, depending on how cynical one wants to be!

1. The R800 RWS Order in India is exciting - small funded business development revenue of $1 to $2m to a prime contractor, nothing to write home about on its own, BUT (1) this is another R800 evaluation and (2) if the prime contractor succeeds, this could lead to 130 units thereafter - that would be huge

2. On the UAE-Korean Defence Industry Partnership, there are potentially 3 wins there (1) any progress in establishing a UAE-based manufacturing base is good news for EOS in the ME and sets it up nicely for an extension into a HELW manufacturing facility in the region as well (2) possibility of more Korean RWS orders and (3) I still think it is setting things up for a Goldrone fail for the HELW - if Goldrone fails, then both EOS and the Korean Govt have a “ready” vehicle and manufacturing hub for the HELW in the UAE, which in turn, will help boost the HELW presence in the ME.

3. There was also a separate announcement that the previously announced $100m Growth Funding Term Loan has been locked in:

- Lender is a subsidiary of Soul Patts, a major long-term shareholder of EOS

- Average interest rate of 14.75% seems high, but (1) there are no financial covenents and (2) the whole facility can be prepaid to Soul Patts and cancelled, within 10 business days without penalty or fee, which would justify the higher cost.

- Provides good incentive for EOS to be judicious in drawing down the loan as well as early repayment.

The EOS price has jumped 9-10% today. I lightened up a bit into the rally as I continue to pare down my too-large EOS position size. Its great on a day like this where EOS is the only green amidst a sea of red, but it can and will reverse equally sharply, so need to create some powder to buy into the dips when it eventually occurs.

Discl: Held IRL 15.57% and in SM

Andreas Schwer, EOS CEO, just about doubled his skin in EOS when 420k rights converted into ordinary shares.

To put this in context:

He has deep incentive to do what is right by EOS as he will directly benefit, big time.

Given that market demand is driven by the complete shaking of the NATO order, EOS has the right products and IP to not only meet demand, but scale capability, my contention is still that Andreas has zero need to do anything funky or stupid to pump the share price.

He just needs to execute steadily and let the actual results speak for itself.

Which in all fairness, is exactly what he is doing.

Discl: Held 14.81% IRL and in SM

It was a good EOS earnings release today. Bit of a roller coaster ride today with the price - down from Friday’s close, then up close to 20% at peak, then settled back at $7.73, up 5.87%, which I thought was a fair outcome.

Remaining very bullish on EOS, but at the same time, deliberately lightening my holdings into price strength, in small doses, as the portfolio holding size has grown a bit too big for comfort.

SUMMARY

FY2025 was never going to about the financials or profitability, it was always going to be about the order book and the growth ahead. And so it was.

Not a squeak about about Grizzly, but if there was one good thing to come out of that attack, it is the added transparency/disclosure and clarity that is now on display - today’s earnings call felt very much like it was the “stuff you Grizzly, here’s the EOS story” session. There was noticeably more counter-party names revealed which is very useful.

Management is targeting to convert 40-50% of the unconditional order book of $459m into revenue of between $180m to $230m at ~50% margin - this is key as ~$200m revenue is when EOS tips into positive NPBT - FY2026 is looking to be the year that this could finally happen

The $459m is also the baseline orderbook - it does not bake in (1) the Korean US$80m deal, which feels touch and go, but the deal is not exclusive and EOS can contract with whoever if Goldrone falls over (2) MARSS order book (3) any new FY2026 orders - given EOS’ FY2025 positioning on several big deals, there looks to be a lot of look forward to in FY2026 in terns of the order book expanding.

Planets continue to align for EOS - geo-politics, conflicts both give it the platform to prove its products, strong market demand from the re-arm supercycle, relevant and increasingly capable products, large unconditional order book with a very strong pipeline, coupled with continued strong management and execution discipline.

It crystallised for me that EOS is currently only firing on ONE business pillar, Defence, with very small contribution for Space - it will be very, very happy days when EOS’ Space products eventually take take off and the business is firing on BOTH business pillars.

FINANCIALS

- Revenue came is as guided at $128.5m

- NPAT was $17.5m but included the gain from the sale of EM Solutions, so does not really count

- Balance sheet is very healthy - $106.9m cash, with a further $100m Term Loan undrawn - with disciplined cash management, particularly in contracts, cash/borrowings, once an existential EOS issue pre-Andreas/Clive is no longer an issue and is very well managed

- Revenue trend has been patchy, but the trajectory of Defence Systems is clearly one of growth and FY2026 should be the year that this fully manifests in the financials

This was another positive outcome of the EOS Turnaround, the revenue geographic diversity. Prior to Andreas, EOS was essentially a Middle-East focused company. This has now decisively changed with a much more balanced geographic revenue mix, positioning EOS very nicely in all the global geo-political hotspots.

Ditto with Profitability - patchy, but the trajectory is one of growth

ORDER BOOK

The building of the Unconditional Order Book to $459m was the highlight of FY2025.

- Excludes US$80m Korean HELW deal, which remains Conditional

- Excludes MARSS order book

Given the very strong market and pipeline, it does feel like the only direction from here for the Orderbook is up - there should be lots of upside surprises to look forward to in FY2026

The target is to convert 40-50% of this amount into revenue as orders are delivered in FY2026, with management soft guiding for revenue to come in between $180m to $230m

This is key as EOS is expected to flip to positive NPAT when revenue exceeds ~$200m - given how things are tracking on multiple fronts - facilities, capacity, orders etc, this looks quite achievable, although it will likely be skewed towards 2HFY2026

DEALS TO LOOK FORWARD TO

Andreas said that the BD update was a very conservative one, but it is still one hell of a list

Andreas was bullish on several deals due to land in FY2026, either on the back of initial/prototype deals secured in FY2025 or new deals in the pipeline:

1. Australian Land 146 deal - current contract $ value is not so large, but >A$1b order intake opportunity as EOS is selected by its partners to be the solution provider for the anti-drone solution for Australia

2. General Dynamics deal, while very small, has the potential to be very, very big - selected by the US Army and General Dynamics to be their sole partner to put the EOS R400 Slinger on top of the Abrams tank, allowing this US tank to survive drone attacks in the modern battlefield - the US Army operates thousands of these tanks, including exports, the integration potential over the next 15 years could be up to US$3b, hence the criticality of the initial contract

- Contract was to finalise the integration of a very specific version of the R400 Slinger on the Abrams tank

- Expect to get the next slice of orders in 2026, followed by large orders in 2027 onwards

3. German UTF Tender with Diehl - for about ~3,000 of the R150 RWS, to be produced with Diehl, Total market potential of EUR1b:

- German Govt and Rheinmetall HELW Contract:

- German Govt has supported Rheinmetall on HELW for the last 15 years, EUR150m, subsidised R&D work

- Rheinmetall has reached a 20kW system, agreed with German MoD to develop a 50kW system in the next 5 years for budget of EUR500m

- German parliament became aware of the Dutch HELW contract, reached out to EOS - EOS can deliver 2x the power for half the price in half the time - since then, German Govt and Parliament has decided to stop further procurement in a sole source mode with Rheinmetall, to have a detailed look at the EOS capability, happening right now

4. HELW is scalable to 150kW with no additional spend to make this happen - In negotiation with 2 governments, 1 hopefully to sign this year, to develop a 300kW HELW family, which is also scalable

The one deal that still feels like it is in the air is the US$80m Korean contract with Goldrone

- Deposit and Letter of Credit still not received - this is expected in Mar 2026 - it does not feel like a bullish update

- But key is that the contract is NOT exclusive, EOS is in parallel discussions with the Korean Govt and end users - at any time, can also enter into contracts with the Govt in parallel

SPACE BUSINESS

A lot is happening in the background as EOS focuses on designing, developing and commercialising the Apollo product family, mostly as customer funded initiatives.

Discl: Held IRL 14.95% and in SM

INITIAL REACTION

I am really struggling with EOS’ Announcement this morning, attempting to squash makret speculation of EOS moving both its HQ and listing to Europe. More so after reading the Reuters report: https://www.reuters.com/business/aerospace-defense/australian-laser-maker-eos-heads-europe-defence-demand-soars-2026-01-30/ which formed the basis of the speculation.

Clearly the market does not like it and the price has taken a bit of a beating.

EOS has been super clear that it WILL set up production facilities in countries that insist on that - it is a key EOS competitive advantage. And in the clip on the Reuters site of the interview, this comes out, as it does in the article. There was no video footage of the conversation around the shifting the Headquarters and listing, so I can’t form an opinion on that specific topic.

The comments in green are motherhood, nothing statements really. You would expect the Board to look at everything and anything, which is what this statement is intended to say I suspect. But given the context of the drama, it also keeps the uncertainty very much alive.

It really does not add up. And so, I went on a self emotionally driven rant as the share price takes another beating.

I sent a note to EOS Investor Relations with this request/comment against the announcement:

Hi, are you able to publish a video of the Reuters interview of 30 Jan 2026 where Andreas is said to have made remarks which gave rise to the speculation so that we can form our own opinions on what was said/not said?

I am having great difficulty reconciling between:

(1) EOS/Andreas strong track record of careful public comments, great communication discipline and clarity;

(2) what appears to be uncharacteristically very loose language in reports of the Reuters interview which goes against this tight discipline;

(3) the apparent "clarity" and "defitiveness" of the reported remarks in the Reuters interview;

(4) the announcement commentary of "no plans under consideration in this regard".

Something does not quite add up, unfortunately, and this is of great concern.

A FEW MOMENTS LATER ....

Unless there are absolutely serious discussions occurring for the move and Andreas/the Board is clearly wanting to put it out there to get a reaction and/or is in early-positioning mode.

Rant aside, reflecting a bit more, and putting on a business rationale hat, this is actually starting to feel like this is the right thing for EOS management to not only contemplate, but to actually follow through and execute:

- EOS has already made some moves in this regard by enabling the trading of EOS changes on the Frankfurt Open Market (FOE) in Sep 2025, so the writing has been on the wall

- The Defence action is all mostly about Europe now, and will be, in the forseeable future

- Being physically located in Canberra, must be a physical hindrance to corporate agility - time difference, distance particularly. EOS is in a far corner of the world when the action is happening at the other ends of the world, literally, ie Europe, SIN, Middle East. EOS has perhaps outlived CBR and Australia, generally and being located in the middle of nowhere is starting to contrain the company.

- Physically moving to Europe takes away all these issues and will enable EOS to be that much more agile in responding to fast moving customer demands

- Listing in Europe will upset Aust fundies for sure, but the upside is that it opens up EOS to global and European fundies - not hard to see that any slack created by Aust fundies exiting is likely to be more than taken up by global/European fundies, purely due to easier accessibility to the market, to management, and given the strong market position that EOS is in now

I am now mentally starting to adjust to this new reality. The more I think about it and ignore the share price impact, I am actually changing my thinking that this may actually be a required and smart move.

If I take this view, then Andreas choice of words, unverified as such, is actually entirely consistent with the smart strategic thinking that he and his management team have demonstrated from the time they took over. There was never going to be any easy way to announce this intent and there will be no running away from the price pain that comes with it, however it is announced.

SO WHAT DO I DO

My immediate reaction was to lighten up to take some money off the table.

But an hour later, having got a clearer view on it, I will do nothing.

- The thesis has not changed

- Everything positive about EOS remains positive.

- There are clear and potentially huge business benefits with moving both the listing and HQ to Europe - this may well unconstrain EOS in pursuing the major opportunities globally

- There are really no huge downsides to a move to Europe that I can immediately think of

It may end up being more inconvenient to trade EOS if it was offshore. But that is probably a small price to pay for continued exposure to what is looking like the next logical step of a major global defence company in the making ...

Discl: Held IRL 16.4% and in SM

Given EOS’ continued excellent communication and market transparency, the Appendix 4C & Trading updates is now mostly an exercise to pick out what has not been previously communicated rather than an update of new news. A really good thing!

KEY ACTIVITIES

EOS relocated its business activity in SIN to a new facility, which includes a new Remote Weapon Systems (RWS) service and and High Energy Laser Weapon (HELW) manufacturing facility - this was a condition of the Korean HELW contract signed in mid-Dec 2025. The customer inspection has occurred and no further requirements on the facility were made, ticking off the contract condition. EOS expects the remaining contract conditions to be concluded in Feb or Mar 2026.

CONTRACT BACKLOG

Very nice picture!

The end EOFY 25 Contract backlog of $459m is a $323m or 238% increase from Dec 2024

Only includes unconditional contracts:

- Excludes the Korean HELW contract, if included, total backlog is $579m

- Excludes the conditional Ukraine contracts where progress has slowed due to continued funding challenges

SMALL “POSITIONING” CONTRACTS

Nov 2025, EOS Space Systems was part of a Spaceflux-led consortium which was awarded 3 major UK Govt contracts for Space Domain awareness. Modest initial contract sizes (<A$1m), but EOS believes this is a key step into the fast growing UK industry.

Post the end of quarter, one small contract was signed: EOS’ KiwiStar Optics secured a ~A$5m contract to produce critical optical elements for the world’s largest ever optical/infrared telescope: Europe’s Extremely Large Telescope (ELT). Not a big material contract, but very good for EOS to participate in these leading edge space technologies.

CASHFLOW

- Cash Holdings on 31 Dec 2025 was $106.9m, up $15.4m from Sep 2025 cash holdings, no borrowings

- Secured a commitment to a $100m, 2-year secured term loan facility

- Additional $41.6m of cash security deposits held with banks to support bank guarantees and bonds

Operating Cash Flows

Net Cash inflow was $19.3m, reversing the cash outflow of ($34.3m) in Q3FY2025. Noticeable spike in customer receipts as customer completion milestones were achieved.

Other than flat Advert & Marketing costs, costs generally rose in line with higher activity levels to support the increased order book and payments to support future customer deliveries.

Net Cash Inflow from Investing activities of $17.1m was due to (1) the maturity of a $20m term deposit (2) net cash proceeds of $9.8m arising from the reduction of cash security deposits under performance bonds following completion of contract deliverables (3) partly offset by the cash payment of $6.3m as part of the interceptor business acquisition in Nov 2025.

In the past 18 months or so, management have had a clear strategy, executed against that strategy, and the cash management has been proactively managed to support the strategy execution. There is also continued evidence during investor calls of strong project contract discipline to ensure that all projects are cashflow positive from the onset. The cashflow reports confirm the positive impact of this discipline, so have no concerns on cash management.

OTHER UPDATES

There has been some movements/fine-tuning of the various bond facility agreements, covenents and bank guarantees - EOS confirms it has complied with its covenants and other obligations under the various facility agreements

EOS made progress with its obligations to contribute to the economic development in a Middle East country as a contract offset (1) business plan was approved (2) steps are being taken to establish a 49% EOS owned JV with Shielders Advanced Industries to set up local manufacturing and assembly of the R150 RWS in the Middle East. EOS is currently in compliance with its obligations.

TRADING UPDATE

EOS expects full-year FY2025 revenue to be slightly above the previously announced range of $115 to $125m - very positive!

Worth ending this note with the point that FY2026 revenue can only be significantly above the FY2025 revenue as the $579m order book is due to be delivered mostly in in FY2026 and FY2027, spilling into FY2028. Hard to forecast what the revenue profile is, but a simple 50% split of the order book would put the FY2026 revenue at around ~$250-$275m perhaps, a potential doubling of FY2025 revenue, before any FY2026 orders.

A really good place to be.

Discl: Held IRL 17.38% and in SM

The positive news keeps on rolling at EOS, this time, the acquisition of MARSS, a Europe-based defence and technology provider of the NiDAR (Network Integrated Detection and Response) C2 (Command and Control) system.

I appreciate, very much, the detail that EOS management goes into to explain new deals or acquisitions, which has now become standard practice: https://investorhub.eos-aus.com/webinars/NPw9pe-marss-acquisition

SUMMARY

1. Plugs a big capability gap in between the 2 EOS product lines - Sensors (detect drones) and Effector (the kinetic weapons that take out drones) systems - the NiDAR C2 sits squarely in the middle of the sensors and effectors and addresses the human constraint in detecting and understanding aerial movement patterns, make sense of the pattern and then make decision based on the pattern - helps the human operator understand (1) What It Is and (2) What To Do

2. NiDAR C2 is proven technology and battle-tested with 60 installations

3. Transformational as it turns EOS from a company which sells Sensors and Effectors, into a fully integrated end-to-end Counter UAS company which has end-to-end capability to Detect -> Identify -> Decide -> Defeat, with or without a human to make the final decision

4. Very decisively opens up the non-military market - Homeland security and civil installations, and expands EOS global geographic footprint

- Deal is structured with capped earn outs to capitalise on MARSS’ strong ~EUR 500m pipeline in the next 18 months

- MARSS is an established business with revenue ~EUR240m/year over the last 5 years but lumpy, EBITDA positive at various times

- Significant growth opportunity ahead

- Funding is comfortable

MY VIEW

- A very sensible and logical acquisition of proven technology which fills a clearly identified capability gap - this significantly enhances EOS market offerings and which continues management’s very clear and consistent strategy for EOS.

- Ord Minnett said in its note today that “the acquisition represents a sound strategic shift for EOS from being an optical sensor and effector systems provider to becoming a full counter-drone solutions provider” - I disagree with that as I think the strategy was always to be a full end-to-end provider, management cleared the decks to ensure focus and build financial capacity, and the MARSS acquisition is really another step in a logical, well-established strategy

- There is a really good management vibe at play - Andreas is all over the technical details, Clive is all over the commercial/financials - this partnership provides very good technical/capability clarity and financial management discipline - this inspires significant confidence in management.

- This comes on top of an already significantly enhanced order book with the recent wins.

The market seems to have recognised this as EOS made an all-time new high today of $11.20 from the previous Feb 2020 all-time high of $10.80. This decisively ended the almost 6-year period in the wilderness where the price lost 96% of its value when the low of $0.415 was reached in end-Mar 2023.

What is exciting is that this new levels are coming on the back of (1) a significant ~60% de-frothing drop between Oct and Dec 2025 from $10.42 to $4.27 (2) supported by ~$312m of new committed contracts since the Oct 2025 peak AND (3) pre-MARSS revenue impacts.

EOS is now firing on all cylinders - a really, really great place to be as a shareholder!

Discl: Held IRL 15.68% and in SM

A really nice way to end what was a sterling FY25 for EOS with the 30 Dec 2025 announcement of EOS' Minimum Shareholding Policy for Non-Executive Directors, CEO and CFO/COO. It is another good trust-building step in EOS' very good Corporate Governance "rehabilitation" journey.

Discl: Held IRL 14.15% and in SM

A very Merry Christmas it is, indeed, for EOS shareholders with another A$33m RWS contract. I initially thought that this was a mistake as the contract value was the same as the RWS contract announced on Friday ...

The EOS Backlog from FY2025 deals is ~$502m, of which ~$400m is unconditional. The unconditional Contract Backlog at 31 Dec 2024 was $136m. The jump is significant.

The EOS price has climbed rapidly since mid-Dec 2025. To put this in context:

- In the run up to the 1 Oct 2025 price peak of $10.42, A$189m of contracts were locked in

- The EOS price then sank back to $4.27 in early Dec 2025 - a ~60%+ drop

- But since that low on 2 Dec 2025, EOS has signed on a further $312m contracts, 1.65x MORE than the pre-1 Oct 2025 contract total. This should provide very good support for this price move.

There was clearly a lot of defence-sector froth in the run up to 1 Oct 2025, and the de-frothing since was very necessary, but it wasn’t a fun ride at all.

But as the price attempts to break the 1 Oct 2025 peak, all of this recent steep move is back by a solid record of unconditional contracts. This is a really, really good place to be, at the end of FY2025.

Discl: Held 12.29% and in SM

Another EOS order announcement this morning, this time for its R400 Remote Weapon System (RWS), $US21m (A$32m), extending the momentum from the HELW Korean order earlier this week.

The “North America” in the headline was initially interesting as EOS has a stated objective to NOT supply North America, so that it does not get caught up with any US-related restrictions on defence sales. But the RWS is to be supplied to an end-customer in South America, so all good.

No impact on FY26 revenue given that EOS’ FY26 ends on 31 Dec.

Contract Backlog Update

The announcement recapped the FY2025 orders, $458m in total, including today’s new order. What is very nice about this backlog is the good split between HELW and R400 orders which helps spread out delivery as the RWS is manufactured in Australia, the HELW will be manufactured either EOS Singapore or in the home-country of the JV partner

Discl: Held IRL 8.63% and in SM

Very nice announcement from EOS this morning for an order of the 2nd export order for a 100kW class High Energy Laser Weapon.

While conditional, the conditional terms do not look unreasonable.

The deal is exactly the sort of deal EOS has been flagging as its differentiated offering - initial order, then licensing of IP for JV’s to be established in the country so that the country controls the end-to-end manufacture and supply chain for the HELW.

Looking forward to more continued momentum of the 100kW HELW ..

Conditions of the Contract, to be completed by 31 Jan 2026:

- Payment of the initial US$18m deposit

- Customer prcuring the issuance of a Letter of Credit for the remaining contract amount

- Customer inspects and being satisfied with the EOS’ Singapore facility

Other Conditions

- Delivery is by the end of 2027

- Licensing of the IP of the the 100kW HELW and establishment of a Korean JV

Discl: Held IRL 7.51% and in SM

2 announcements from EOS this morning:

Interceptor Acquisition Completed

No excitement around this - it was a simple, small acquisition that nicely fills a gap in EOS’ product portfolio.

Settlement of ASIC Investigation

- $4m settlement of an ASIC investigation around “continuous disclosure obligations in the period 25 July 2022 to 31 October 2022”

- This was all pre-Andreas and the current management team, who joined back end of CY2022

This is good news as (1) it removes a management distraction and should clear the closet of pre-Andreas shennanigans (2) it removes the overhang of litigation costs, greater penalties and (3) locks in a small penalty.

I topped up IRL last week at $4.56 as I think the hot air around the defence thematic has mostly be taken out.

It will now be down to converting the strong sales pipeline, with all the tailwinds of defence spending and urgent need for the EU to be self-sustaining in protecting itself, anchored by baseline growing revenue that has been locked in for the next 2 years.

Discl: Held IRL 7.90%

EOS just released news of its acquisition of a UK-based “Interceptor” business from MARSS Group.

This acquisition makes good sense.

- A$10m - no stress to the cashed-up EOS balance sheet

- Expects 12-24M of further development before full commercial launch - faster and lower risk than in-house development

- Further investment of up to A$10m over the next 3 years, with potential for customer development funding - this is nothing BAU money, really

- The Strategic Rationale is very much aligned to EOS’ overall strategy which Andreas has been very clear and consistent about

Discl: Held IRL 7.55%

Nice new $20m order for EOS for its Slinger Counter Drone Remote Weapon Systems from a “Western European NATO country”.

To put this in context, EOS' revenue:

- FY24 for Continuing Operations (post the sale of EM Solutions) was $176m

- Full-year FY25 revenue is expected to between $115-$125m.

This sold and unconditional backlog means that revenue growth is pretty much locked in for FY26 and FY27 as the current baseline scenario, with all the upside still to come from increased global spending on counter-drone defence.

It is never easy to watch the share price halve as it has with EOS, but I would hope that all the froth has been shaken out and we are now down to pure fundamentals of EOS as a company. And gee, I absolutely like what I am seeing.

Discl: Held IRL 8.99%

Had a read of the much anticipated European Commission’s “Preserving Peace - Defence Readiness Roadmap 2030” which was released on 16 Oct 2025 and which defence industry companies have been waiting for. Not a difficult read.

A summary of the key points of the roadmap

From an EOS standpoint, this was really exciting to see as:

1. The horizon is a very short 5 years

2. The milestones against each of the 4 Defence Flagships looks mighty aggressive for any nation, never mind the EU as a whole, but it reflects the huge sense of urgency that the EU feels to get their defences ready, both country and as a region, against primarily Russian aggression

3. The plan calls for projects to all be launched by 1HCY2026

4. This will not be a one-size fits all scenario - the phrase “multi-layered” pops up everywhere

5. It almost feels like EOS not only saw all this coming, but actually cleared the EOS decks by selling EM Solutions to enable the organisation to fully focus on riding this Roadmap - both EOS Divisions, Defence Systems and Space Systems look to have offerings that could play a part in each of the 4 Defence Flagships

6. There is a big focus on in-country/in-region production - this augurs well for EOS as one of the major advantages of the High Energy Laser Weapon offering is that EOS owns the IP and has made “in-country production” one of the key selling points of the HELW

7. One of the best moves that EOS did during the turnaround was hiring Andres Schwer as CEO - he has brought deep industry and engineering knowledge and experience and the European network and connections to enable EOS to be in the heart of this wave.

Lots to look forward to in the coming 1-2 years, I think.

Discl: Held IRL 9.38%

Not too much new in EOS’ Trading Update today. EOS has been very transparent about where things are, so most of the new deals have been previously announced.

CONTRACT BACKLOG

This was a good perspective of the changing EOS order book, which currently stands at $415m, a $279m or 206% increase from 31 Dec 2024. This will underpin revenue for the next 2+ years.

NEW DEVELOPMENTS

A few new developments not previously announced:

1. EOS USA is developing enhanced capabilities for the Slinger Counter-Drone RWS, incorporating capabilities to meet the growing challenge of drone attack, such as aided target recognition and selectable autonomy. Customer funded, and is linked to the US8.5m order for Slinger counter-drone development work and an inaugural order for 1 x R800 heavy-calibre RWS - EOS is optimistic that this could lead to increased order intake in the future

2. Several Ukranian donation opportunities continue to mature

3. Demonstrable increase in enquiry from new potential customers interested in the 100kW High Energy Laser Weapon

4. EOS and Diehl Defence (Germany) signed an additional Teaming Agreement for a new opportunity an jointly submit a bid in response to a German request for approximately 3,000 light RWS. Next stage of proposal down-selection is expected to occur in late 2025 or early 2026

5. In mid-Oct, the European Commission released its “Preserving Peace Defence Readiness Roadmap 2030” - need to peel this to understand the potential impacts to EOS and the broader Defence industry

CASHFLOW

- Cash holdings was $71.5m, down $38.8m from 30 June 25, no debt - there is a further $20m of Term Deposits, and $52.0m of Security Deposits for Performance Bonds, Guarantees

- Net Operating cash outflow was $34.3m - timing differences from customer receipts vs cash payments of $50.8m

- No concerns given order book and full-on manufacturing that is ongoing to fulfill order deliveries

TRADING UPDATE

No change to FY2025 guidance - full year revenue expected to be $115-125m, with the potential to add $25m if new orders can be signed before 31 Dec 2025.

Disc: Held IRL

EOS announced the signing of a A$108m Remote Weapon System for the ADF’s LAND 400-3 project today.

This is the 2nd and final of the 2 x $100m+ contracts it announced in July 2025.

This should now increase the contract backlog from $299m, announced on 30 Sep 2025, to ~$407m, very healthy indeed.

With both these $100m contracts now locked in, any new contracts from hereon through to the end of CY2025 should be new wins. These wins will not move the dial on the FY2025 revenue as there will be no time to deliver and recognise the revenue, but will add to the significant growing backlog.

Market response was muted, given the size of the contract, Quite possibly, news of the win could have prematurely leaked out last week, which caused the pop past $10. This announcement is perhaps reality catching up.

Discl: Held IRL

Scratching my head at the catalyst for today’s EOS 13+% pop with fairly decent volume. Can’t say I was overly enthused in reading the Announcement this morning on the FY2025 revenue outlook and Contract Backlog. I was actually concerned that the market might actually be disappointed with (1) where FY25 revenue would land and (2) the nothing terribly new contract backlog numbers.

What might have prompted excitement is the drone attack on Ukraine overnight as well as the recent drone attacks in Copenhagen and Aalborg, Denmark, which again highlights the increasingly brazen-in-your-face drone attacks and the criticality of anti-drone capabilities in warding off these attacks.

Full Year 2025 Outlook

This was new news. Revenue in recent years has been lumpy, but the current FY2025 guidance does not quite stack up with revenue in recent years, even if the stretch $25m revenue, is achieved.

Contract Backlog

The contract backlog seems to have generated some market excitement, although I am struggling to see the fuss. EOS has announce $189m of additional contracts per below, and the $136m contract backlog at 31 Dec 2024 is public news.

That the contract backlog now is ~$299m should not be new news either as EOS has been very transparent with new contract announcements.

Chart Review

Price-wise, EOS is not too far away from its all-time high of $10.80 of January 2020. With strong market momentum clearly behind it, and the ongoing drone-drive wars fuelling demand for anti-drone products, it does feel like the all-time-high could be taken out soon.

Will continue to let EOS run ...

Very nice EOS move, which probably explains the sharp pop these past 2 days. Another smart-no risk-no-big-change-high-impact move from management which enhances the EOS flywheel currently in play.

Discl: Held IRL and in SM

Reading the horribly depressing news lately, this WSJ article and diagram of the drone which Russia flew into Poland caught my eye.

This really looks like a larger and souped up Remote Control (RC) plane, the ones that would grab attention in a RC weekend flying event at the local RC airstrip due its larger than normal size.

But the NATO response to shooting down 19 of these was interesting:

- Dutch F35's

- Polish F-16's

- Black Hawk helicopters (no mention how many of each, but it was plural, not singular)

- 1 x Italian AWACS plane.

And the latest is that the following hardware will now be deployed to Poland's eastern flank:

- 3 x Czech Mi-171Sh helicopters

- 3 x French Rafale jet fighters

- 2 x German Euro fighters

This puts in perspective the EOS 100kw HELW system recently sold.

- The drone looks to be of the type that the HELW was intended for

- It can take out 20 drones per minute

- No need for ammunitions - all they need is power

- $1-$10 per shot

- But the 100kw Range is 1 to 8km only ... and the EOS 100kw is the first of its kind for 100kW

- The higher the power, the longer the range - EOS looks to have the ability to scale to 150kW

- Each country will need a heck of lot of these systems if it to make any dent in the counter-drone capability, not just 1 or 2 units ...

A lot to look forward to with EOS in terms of (1) increasing HELW demand (2) increasing pressure to deploy the HELW faster - the countries needed it yesterday, literally (3) increased pressure to scale to 150kW and beyond to get longer range, and (4) a ready real-life battlefield when the system will actually be needed, to prove its capability ...

Discl: Held IRL and in SM

Discl: Held IRL

More information on the Land 156 bid.

- This is an Integrated approach vs a technology-based piecemeal approach, which makes intuitive sense, given how counter drone technology is now significantly more technology systems-centric - the integration between different pieces of technology is more key than ever

- It feels like this is in EOS' sweet spot for both its kinetic counter drone (Slinger) and High Energy Laser Weapon (HELW) offerings

- By the time this project takes off in earnest in CY2026/2027, there will have been progress on the HELW project, which the ADF will no doubt be keeping a really close watch on

- Small dollars for what sounds like a "what does minimum counter-drone capability look like" focus through to Dec 2025.

- The possibilities thereafter when capabilities are proven to work in an intergrated-systems envionrment is what is more exciting to look forward to.

You have to be in it, to win it, so big tick to the first step of "granted entry to the tent to play the game" ...

Price reaction to the announcement today is muted thus far, following the massive over reaction to the initial announcement (OMG Major deal, whoo hoo!) , then yesterday's retracement (Ah ... so ....) to today's (Ah OK ,,, chill, only an initial demo deal). A much more sensible reaction to a very-positive-but-very-early-days deal ...

What is more interesting for me is to see the price "behave" within the support/resistance and retracement areas that I have been watching, in these wild swings ...

Discl: Held IRL

While not a done deal and deal size is small, at least at this stage, this can’t possibly hurt ....

This opportunity was flagged in EOS’ list of Notable Opportunities.

Discl: Held IRL

SUMMARY

- As EOS has communicated extensively in the past 2-3 months, nothing terribly new

- 1HFY25 results unimpressive but not the focus - FY25 revenue heavily weighted to 2HFY25, as previously guided

- Building the Contract Order book was the 1HFY25 focus - contract backlog is now $307m, up from $136m in Dec 2024

- Planets are aligning for high-volume HELW orders - the urgency in getting the HELW to counter drone swarms is driving this dynamic, the hard work and long contracting period to lay the contractual ground with the HELW launch customer will likely pay off

- It really is all about the big orders coming through - each order won will turbo charge the contract backlog and revenue in a stepped manner ...

KEY TAKEAWAYS FROM EARNINGS CALL

Financials

- EOS 1HFY25 Financials - unimpressive in absolute YoY terms - Revenue $44.1m (down 61.4%), Underlying EBITDA ($13.3m) (down12.3%), NPAT ($44.8m) (down 34.0%) after large contract completions - but this was flagged including the outlook that “2025 revenue is heavily biased to 2H”, so no cause for any concern

- Very clean balance sheet - $130.3m cash, $51.9 security deposits, zero debt

Order Book

- EOS is really a Contract Order Book story - this was the focus in 1HFY25

- The market was again reminded of the significant opportunities ahead, especially for 100kw High Energy Laser Weapons, but all of the information has already been announced in recent weeks. The reminder was nevertheless, good to hear still ...

- Contract backlog on 20 Aug 2025 is $307m, up from $136m in Dec 2024 - this is the key parameter to focus on

Updates on Key Contracts

A. Middle East UAE Slinger R500 - successor to R400 product contract to UAE, $500m+

- Customer has participated in demonstrations

- Within the UAE, have different client groups - each have different requirements causing contract complexity

- May take longer to close, but good confidence this will close in CY2026

B. High Energy Laser Weapon 100kw

- Build will take ~2.5 years, plans are in place to accelerate this delivery period

- Customer is a very established customer, sole sourced as there are no other competitors, well known for its highly stringent procurement process and financial audits - other countries are likely to rely on this customer’s due process and ride on this initial contract rather than negotiate a contract from zero

- This initial contract allows other NATO countries to easily ride on the contract, paving the way for shorter contract processes in 2026

- EOS has an internal lower powered demonstrator to showcase the HELW - no need for clients to see the 100kW system as they can extrapolate what the 100kW system will do from the lower powered demonstrator

- The criticality of the HELW to country defence strategies to counter the latest drone threats means that there is no time for the typical elongated 5-7 year procurement process ie, buy 1-2 units to prove effectiveness, before placing larger orders - there is significant urgency for countries to rely on the live demonstrations and the initial contract to expedite the delivery large quantities of the HELW - “we want it now”

- EOS is well placed with no competitors in this 100kW space, is the only “Golden Dome” player outside of the US - expecting that contracts with large quantities of the HELW should come through

Improvement of Product Software and AI Capabilities

A current battlefield problem is manned battle stations are intended to defend against single drones, not drone swarms and drones controlled by AI

Need a “robotic” solution, to build intelligence into the battle stations to counter drone swarms - this is all software-driven, but there is currently no software capability - need to focus on building this capability into EOS products

Manufacturing Capacity for HELW

HELW production in Singapore is about to be moved to new facilities which can handle 5 contracts simultaneously

Production capacity is not a concern as most countries are insisting on localised production facilities to retain self-control and eliminate supply chain issues - likely to have local manufacturing partners who will provide the required manufacturing facilities, capex etc

Management thus expect capex requirements to scale HELW production to be small, with no impact expected to the SIN facilities

EOS got belted today, together with DRO and other Defence companies. A possible "explanation" is that Mr Market somehow believes that the war will end soon, time to exit defence.

Can't understand that logic, if that was the rationale - this WSJ article helps crystallise how the path ahead is fraught with so many challenges. Much as I hate Trump, I have to concede that he is at least giving it a crack. He will need to keep smoking the fine stuff he must be smoking if he believes he can actually make this happen.

I hate war, so am wanting the Ukraine war to end as soon as possible.

My EOS thesis is not based on an indefinite Ukraine war at all. So while there will be a short term price impact if the war actually stops, the longer term thesis of mandatory EU defence spending, the need to protect countries against drone swarm attacked, then protecting civil installations from drone attacks, then space control, will still be very much intact for many more years to come.

The EOS chart looks quite good and healthy actually. The current insane leg up was way too steep and way too hot - a correction was not only imminent, but necessary, if it is going to sustain the good momentum. Todays belting takes the retracement past 23.6%, thats a good technical tick in terms of satisfying the Fibonacci retracement minimum.

$4.59 to $4.76 could provide the next level of support, failing which, the next retracement level of 38.2% beckons at $4.35, then likely to be stronger support around $3.70 which not only a decent support area from the late July rally, it is also the 50% Fibonacci retracement.

Discl: Held IRL at overweight allocation

Nice to see another new fundie appear in the EOS Register, FMR LLC.

Per the announcement today, purchases were made on the market between 14 July and 8 Aug 2025, between $3.05 and $5.00, so rough average cost around ~$4.00 perhaps, probably contributing a bit to the pop in the price in early August.

Discl: Held IRL

A really eye-opening presentation by EOS this morning as it updated Investors on High Energy Laser Weapons (HELW), on the back of the $125m HELW deal EOS announced 2 days back. Link is below, and my notes from the call follows.

SUMMARY

- This was a ground-breaking, world-first deal in the 100kW HELW space which addresses many challenges in anti-Drone warfare and is shaping up to be a significant milestone deal for EOS.

- EOS has between 3-5 years headstart over its nearest competitor, owns the full IP of the HELW - a key differentiator, as it allows EOS to work with customers to customise the installation in-country, giving the customer full control over the system, free of dependence on supply chains, US export restrictions etc - these form a significant technological and capability moat.

- Demand is strong - not only for military battlefield purposes, but also for Homeland security to protect critical infrastructure, public venues/installations, from remote drone attacks - Homeland Security is a bigger TAM than military uses.

- Will wake up the market that a 100kW system is now commercially available - this could well spark an “HELW arms race” as other countries now fall behind in having this capability and are thus vulnerable to ongoing drone attack.

- EOS is now in a position of significant strength and leverage as it holds the technology IP keys to strong anti-drone defence in a countries layered-defence strategy which is what is needed in today’s battlefield - this leverage will significantly reduce the risk of commercial stupidity of the past, demonstrated by the diligence in the economics of the deal.

My ESG and patriotic conscience is very clear - war is inevitable and unavoidable as long as mad persons are allowed to roam the world. EOS capabilities are for DEFENCE AGAINST attack, not offence to attack. This is good and necessary for the prevention of loss of human life and destruction of property, with an Aussie company at the world forefront of this.

Fair to say, EOS is firmly out of my portfolio doghouse and in my “likely to continue rocketing” bucket. The market seems to have now taken notice, given the very sharp price pop since the deal was announced.

Discl: Held IRL

PRELIMINARIES

As I joined the call just before the start, there were already 57 participants - a good sign of investor interest in the EOS story

DRONE WARFARE ISSUES

- Drones are now built in backyards for <$1k, some 200k used per year, deployed in swarms - larger and more autonomous

- Can be hardened to resist anti-spoofing/anti-jamming capabilities using simplistic measures eg. Faraday cage shields, fibre optic gyro’s - jamming, spoofing now ineffective

- Use of fibre optics which cannot be defeated by jamming - 50km range

- ~70% of all armoured vehicles in recent times have been taken out by drones

- There is currently no appropriate counter-measure response to these drone threats

SIGNIFICANCE OF THE HELW DEAL

- Historical deal from an industry, military operations,battlefield and EOS perspective - 1st of its kind for a 100kW high power/high energy laser system

- Game changer in anti-drone warfare as it can detect and shoot down class 1 to 3 drones

- Addresses key battlefield issues:

- High economical operational cost - $1 to $10 per shot vs ammunitions and missiles

- High speed, highly agile - 20 drones per minute capability, 5-10x more effective than kinetic counter-drone measures

- Has range between 1-8km, 2-3 seconds engagement time over 2km

- Can scale from 100kW to 150kw - important as the higher the power, the lower the engagement time and the longer the range

- 150kW takes the capability into the air and missile defence space to provide anti-rocket and anti-missiles

- The “ammunition” is electricity, not munitions that require ongoing cost - battery rack can do 300 kills without a power connection, once connected to power, there is no limit to the shots, thus no supply chain and run cost issues

COMPETITIVE MOAT

Slide 11

- EOS is approximately 5 years ahead of its rivals, technologically, in the 100kW space

- Israel’s Rafel/Elbit collaboration is the closest and only real competitor in the 100kW HELW space, but the key issue is that they don’t own the IP across the solution and Israeli technology has limited access to some markets

- UK’s Dragonfire system is only 50kW and will only be ready by 2028, EOS is at least 3 years ahead

- US - focused in same space but will not be able to export the technology and will be US focused - EOS sees itself playing in the “Rest of the World” market with the US focusing on the US

- France - 2-5kW systems only

- Chinese - 50kW systems but inherent security concerns will prevent any expansion into Western/NATO nations

- Germany - 20-30kW focus, no commercial products

IP

Slide 14

- Excluding Power and Amplifiers, which are commercial off-the-shelve components, EOS owns and controls ALL THE IP of the laser system

- IP is based in Singapore

- This is a very crucial asset as it allows EOS to customise the installation for each customer for them to be (1) self sufficient/self managing of the system (2) free of US Content ie. ITAR free, and hence, be the masters of their own defence destiny, free of dependence of any country or any supply chain

MARKET DEMAND

- Demand is strong - not only for military battlefield purposes, but also for Homeland security to protect critical infrastructure, public venues/installations, from remote drone attacks

- Homeland Security is a bigger TAM than military uses

FINANCIAL DETAILS OF THE DEAL

- Contract is for ONE unit of the HELW system + lots of customisation to incorporate the system into a multi-layer air defence battlefield system - this will be the first 100kW battlefield operational system, once deployed

- Deal is profitable and cashflow positive

- Revenue Recognition - (1) FY2025: $5 to $10m, so not an uplift to guided revenue (2) Bulk of revenue will be recognised in FY2026 and FY2027, and a bit in FY2028

- EOS target gross margin on projects is typically between 40-50% and EBITDA project margin is typically ~20% - the expected Gross Margin on materials of this deal is expected to be around 50%, with incremental EBITDA margin expected to be 20% “or higher”

- Expect expenses to rise by $5 to $6m, mostly people cost

- No additional capital required as EOS SIN facility has capacity for 4-5 projects simultaneously

- Expect neutral cash flow in the first half of the project, then profit thereafter

- Singapore will be the hub for laser innovation, with Canberra having a greater space control focus - wide footprint of laser experts within EOS

- Clarification on “Customary Cancellation” contract clause - contract is (1) unconditional (2) allows client to cancel the contract for significant events eg. Change in government, political eruptions (3) Client still has to pay for all expenses incurred. Very rarely occurred and is not a threat to EOS

FOLLOW-ON OPPORTUNITIES

- EOS has the opportunity to be a very embedded supplier if it gets this right

- Have been in advanced negotiations with another client - likely to be signed in 2026 than in 2025

- Following the deal announcement, the market will wake up that 100kW is now available commercially for distribution

- First clients typically order lower quantities, then once proven, mostly procure larger quantities

- Expect future projects to be built in-country, fully funded by customers - this ability to customise and localise is a game changer for the industry given the highly strategic nature of the capability

- SIN facility has capacity for 4-5 projects at a time, which can be expended if required

Very nice Yeah Baby! moment with EOS announcing this EUR71.4m.AUD125m order for a High Energy Laser Weapon (HELW) for drone defence capability.

While this was pre-telegraphed as being "imminent in 2HCY20205" in the Appendix C last week, it is always good to see the deal actually being done!

This deal is significant from several perspectives: (1) revenue boost (2) technologically - a world first for a 100kw laser defence system, converts a R&D development capability to reality (3) clear evidence that the strategic management pivot to focus on HELW as 1 of 2 EOS pillars, was absolutely the right and smart move.

It also puts more distance and separation between EOS and the like of DRO in terms of anti-drone capabilities, such that I do not think they now compete directly as they offer different capabilities for different use cases.

Nice pop in the price today with good volume. The pop is especially nice from a technical chart perspective, as it comes after the ~25% price retracement in the past week.

Discl: Held IRL

Discl: Held IRL

SUMMARY

- A lot of activity - small customer orders that look like paid BD, a strong focus on manufacturing to fulfill sold orders and a good geographic spread of BD activity

- There appears to be solid progress on 2 large deals that could deliver between $180-$200m revenue in 2H2025, one of which is for a High Energy Laser Weapon - management decision to pivot and focus on HELW’s looks to be bearing fruit

- Balance sheet is now extremely clean and rock solid - $130.3m cash, zero debt, Asset Contract Value now down to $5.1m following cash collection of $60m from its Middle East customer - this was problematic for many years.

- Following the full repayment of WHSP debt and the final collection and closure of the ME contract, it does feel like a line in the sand has now been drawn on the EOS of old

- EOS is now significantly stronger, focused and well positioned to capitalise on the imminent upswing in global defence spending in anti-drone capability

Having stomached the very painful turnaround, patience is now needed to let the business do its thing - have very high confidence in Andreas and his management team as they have done an outstanding job cleaning up EOS.

Am now a very happy EOS shareholder!

Some interesting pieces of news in EOS’ June 2025 Appendix 4C.

CUSTOMER ORDER ACTIVITY

There are new small orders which look more like paid Business Development - augurs well for future orders

MANUFACTURING AND DELIVERY ACTIVITY

Focus in the Quarter has been on manufacturing:

ORDER BOOK DEVELOPMENT ACTIVITY

Contract backlog at 30 June 2025 was $170m, a $34m or 25% increase from 31 Dec 2024

These 2 deals look very promising - $80-$100m and $100m, respectively, due to be signed in CY2025

The High Energy Laser Weapon is also exciting as that would be the first big sized deal in that space since EOS started to laser focus (pun absolutely intended!) on it in the past year.

Lots of ongoing Market Development activity - the key takeaway is the geographic spread of the activities which is nice to see - UK, India, US, Japan, Indonesia, Belgium, Greece - a good expansion and pivot away from the heavy Middle-East focus in the past years.

FINANCIALS

Total Cash 30 June 2025 was $130.3m, a $27.2m increase from Mar 2025 - very healthy

Over and above this, $51.9m is held as cash security deposits with banks to support bank guarantees and bonds

Solid $78.1m cash receipts, driven by the finalisation of a Middle East contract where $60.0m was collected - this drove a huge drop in Contract Asset Working Capital Balance to $5.1m. Have been tracking this FY2023 where the Asset Contract Value was $139.0m .... very good to see this brought down and cash collected.

Nothing concerning with operating cash flow burn of $47.8m in 2Q - reflects the focus on manufacturing

Cashflow and Investing Cash flows have normalised following debt repayment and receipt of EM Solutions proceeds in 1QFY25

Following the full repayment of debt to WH Soul Patt, EOS has one heck of a solid balance sheet - strong cash balance, zero debt, minimal working capital after collecting final cash from the problematic Middle East contracts - it is a really, really good place to be

TRADING UPDATE

No change to previous trading update:

- 1HFY25 revenue to be between $40-$45m

- Full year FY25 revenue to be heavily biased to 2HFY25

The updates around the 2 big deals highlighted above and the strong focus on manufacturing provide confidence of the 2HFY25 jump in revenue per the guidance.

The EOS chart is also looking very interesting.

- The very nice and strong bullish run stalled at about $3.72, which is the top of the support resistance zone that goes back to Jul 2019 and Oct 2021.

- Price has since retraced 23.8% to $3.10, to ~$3.02 which looks to be a resistance/support areas, and looks to be consolidating around these levels - this came with low-ish volume, which indicates a nice healthy pullback

- While I would hate for the price to fall back further, a drop to ~$2.75-ish would not only not be bad, it could be healthier for the price in the long run, as it would have retraced 38.2%, with profits been taken and new holders coming into the picture

Will be very interesting to see where the price goes once results are announced.

Discl: Held IRL