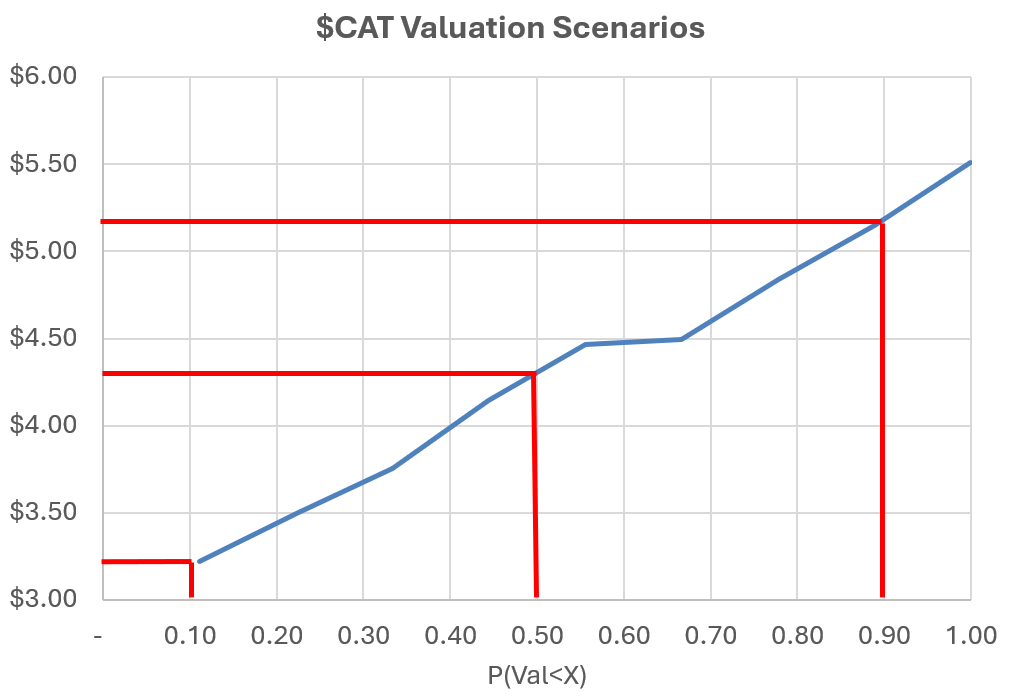

Consensus community valuation

31-May-2026

$4.30 ($3.20 - $5.20)

This is an update to my valuation of one year ago of $5.50 ($4.50 - $6.50)

The major change in my valuation of $CAT reflects more of a change of heart on my part on modelling assumption, than any fundamental change in the performance of the company. While still using a 10-yr DCF method, at a high level the changes in approach are:

i ) Annual revenue growth rate declines progressively and smoothly across the forecast period. Previously, my main assumption was to hold constant at rates of 15%, 17% and 19%. While that seemed defensible at the time (to me at least), given Will's big TAM numbers, it ignores the idea of a "creaming curve" in that $CAT is likely accessing the highest value / highest propensity to buy customers early in the game. While the stated TAM notionally exists, over time it becomes harder for $CAT to access (e.g., rise of competition / new technologies).

ii) Last year, I assumed the "target margins" are achieved by FY29 and then are held throughout to FY36. Now I have allowed a range of scenarios in which the target is achieved, with more opportunity for this to take longer. Equally, I allow some scenarios where modest margin expansion beyond the target as the business continues to scale. Of course, Will could choose to hold the business at the "target margins" and increase resource allocation to drive higher revenue. (I need to look more closely at the differences between the two valuations, as last year's valuations indicates that could be a better strategy than indicated by this update.)

iii) I assumes 100% organic growth, hence moderating dilution assumptions. In reality, M&A may well result in 'stronger for longer' revenue growth, but this won't necessarily drive shareholder value as it will be accompanied by more dilution and also margin compression.

Despite the reduction in valuation, my conviction on this business and the management team are unchanged, and $CAT remains a top-5 RL ASX position for me.

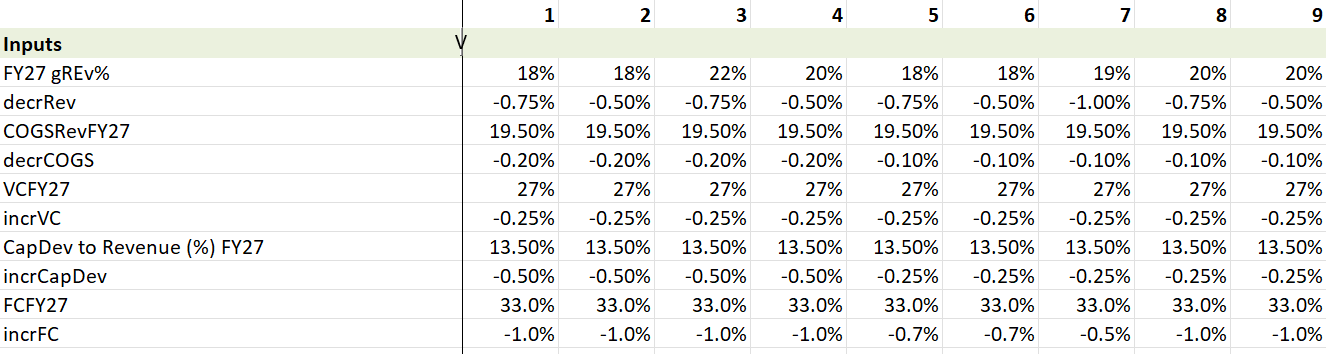

Valuation Scenario Outputs

Input Table

Definition of Inputs in above table (by row):

- FY27 Revenue growth (%)

- Annual decrement in annual revenue growth rate (%)

- COGS/Revenue (%) in FY27

- Annual decrement in COGS as % of revenue

- Variable Cost in FY27 as % of revenue

- Annual decrement in variable cost as % of revenue

- Capitalised Development as a % of revenue in FY27

- Annual decrement in capitalised development as a % of revenue

- Fixed Costs as a % of revenue in FY7

- Annual decrement in fixed costs as a % of revenue

Other Valuation Assumptions:

- Share-based compensation (SBC) as % revene declines from 9.0% in FY27 to 6.0% in FY36

- Annual SBC dilution declines from 1.3% in FY27 to 0.8%

- PP&E as % of Revenue = 1.5%

- D&A as % revenue declines from 25.0% in FY27 to 19.0%

- Working capital increases at 5.0% of incremental revenue

- Effective tax rate ramps up from 5.0% in FY29 to 25%, allowing for accumulated losses

- Discount Rate (WACC) = 10.0%

- Terminal growth rate = 3.5%

- Cost of debt 7.0%; Interest in cash 3.0%

- USD:AUD = 0.70

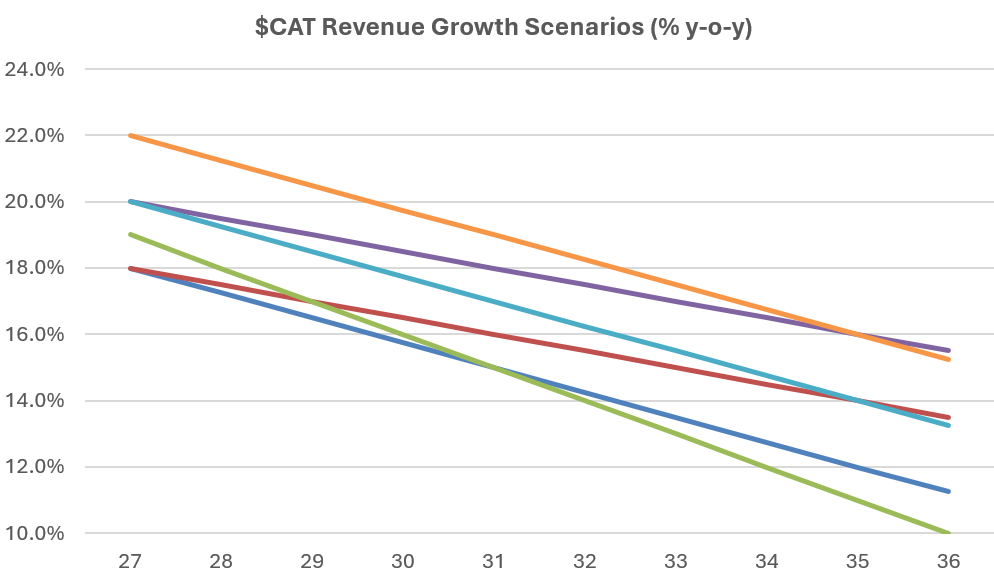

Example of % Revenue Growth Across Scenarios:

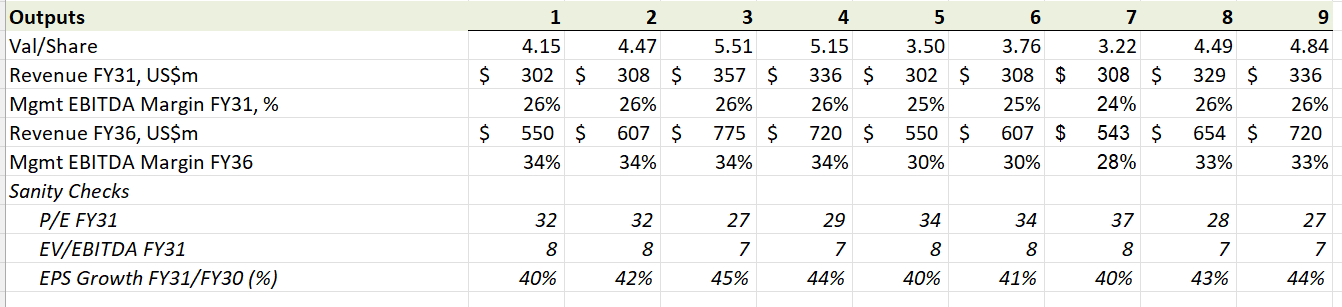

Output Table

Observations on Valuation vs. Market Price

- Given company beta, WACC is arguably more like 11.0% than 10.0%. This alone leads to a p50% valuation of $3.70 - which is pretty much where's today's price is!

- Likely to see higher SBC than modelled, which could lower valuation by c. 5%.

- Not sure on tax assumptions. Might be higher.

- All three points together indicate that the business is likely fairly priced by the market.

Disc: Held (RL 10.5%)

============================================

31- May-2025

$5.50 ($4.50-$6.50)

Details set out in my "Valuation" straw.

Disc: Held in RL and SM

Discl: Held IRL 8.30% and in SM

The CAT price continues to behave really nicely post the results announcement.

- The price has stayed above the $2.91 to $3.35 support area very nicely

- From the short term 19 May 2026 low to the 21 May 2026 short term peak, the price has rectraced a nice 50%, almost on the dot, so it is technically “ready” to move higher from here, it that is the direction it takes

- Immediate resistance is $3.97 to $4.15 - this is a reasonably strong one, given the history, so I do expect it struggle to push past this level - it will be huge if it pushes past $4.15, then $4.51 is the next level of resistance

Given that the results were mostly well received, downside appears limited to $2.91 to $2.35, failing which $2.30 to $2.70 is the next support level.

Discl: Held IRL 7.63% and in SM

The CAT price continues to behave very nicely, technically, since the last post a month ago (time does fly by quickly indeed).

The $2.91 to $3.35 support has held out really nicely for exactly 3 months, lots of accumulation will have been happening at these levels. This sets it up nicely for the results announcement in May.

- If the results are well received, then this would be a very strong base from which the price bounces up through to at least $3.97 to $4.15, and beyond

- If the results are poorly received, then $2.30 to $2.70 would be next down - support at this level, going back to Sep/Oct 2024, should be decent

Discl: Held IRL 8.25% and in SM

The CAT chart continues to “behave”, technically, since I last had a closer look 2-3 weeks back.

- The $3.03 to $3.33 support zone is holding out very nicely, despite rather intense volatility during the time

- Within this zone, the price seems to bounce quite consistently when it touches ~$3.23, since early-Feb 2026 - it has done so 6x in the past 6-ish weeks - there is historical price precedence to this going back to Dec 2024/Jan 2025y

Not topping up as I am already over-allocated, but gee $3.23 would be a very nice entry point to position for ...

Discl: Held IRL 8.74% and in SM

Might be a temporary dent to the very nice price movement these past 3 days.

Very nice to see a long bullish green candle today - haven't seen anything like it for quite some months now. This move stopped at the bottom of the 3.97 to 4.15 resistance zone, which is as textbook a move as can be.

With the news of the Index removal, the big moves these past 2 days, plus historical churn in this resistance zone, a pullback or consolidation at these levels feels more likely before it attempts to move past this resistance zone.

Discl: Held IRL 7.52% and in SM

Northcape Capital updated that is has topped up 1% of CAT. Can't be a bad thing. Prompted a re-look of the chart to see their cost.

Updated CAT Chart

Since the last chart update 2+ weeks ago on 13 Feb 2025, the $3.03 to $3.33 base continues to build out very nicely and selling pressure seems to have abated.

Discl: Held 8.10% IRL and in SM

While clearing emails, realised that I had not gone through the CAT News Email of 12 Feb 2026 in full.

This was a short, easy to watch video interview with CAT's Chief Technical Office, Gareth Griffith. He made 2 points around 7:37 which for me, was a good reminder of how strong CAT's moat is vis-a-vis AI-mageddon

(1) Closed Team Proprietary Data that is generated by and used throughout, the platform; and

"What you can learn what we as a company learn from working with elite teams, we can translate into information for the wider users which they wouldn’t necessarily have access to themselves."

(2) The CAT platform IS the workflow of the teams and is integral to their success ..

"I have never considered us to be a 3rd party company. We are part of the team. And you have to understand how critical we are to their success, and you have to feel part of that success."

Discl: Held IRL 7.20% and in SM

Having established that CAT is definitely a company I want to keep in my post-"AI-mageddon" portfolio (see separate post), the CAT chart looks interesting:

- A short-term base SEEMS to be forming nicely at the $3.03 to $3.33 support area, bouncing around ~$3.30 this past 1-2 weeks - this area goes back to Nov 2024, the longer it stays around here, the stronger this base becomes when the rerating hits. If this breaks,

- The next level looks to be ~$2.30 to $2.70, if this breaks

- Then ~$1.71

After which we are completely in the Back-Up-The-Truck (BUTT) zone when CAT was still a shit company but in full-on turnaround mode.

I also put a note in the chart to remind myself that the last Capital Raise was at $6.68, so all Directors and Fundies are hanging on from those levels and taking the current hit, like those of us who bought in and are still holding.

Discl: Held IRL 6.69% and in SM

Nothing to be concerned about

Post the sale, Will owns 0.80% of CAT, which excludes the 1,444,057 rights he still holds, which vests in stages between now and 30 June 2028.

Timing of the sale is rather unfortunate, given where the CAT price was and is.

CAT announced today that Will Lopes was awarded his FY26 rights, 455,737 rights. Had a quick poke around Will's shareholdings history to see how it has evolved.

In summary, since Will was made Director in Sep 2023, he:

- only has had STI and LTI rights convert into shares

- only disposed shares which was automatically forced to cover taxes and fees on conversion of rights

- holds 1,606,305 shares today, 0.56% of the CAT register

- holds another 2,185,098 TIP Options, which if converted, would take his shareholdings to 1.33% of the CAT register

- will continue to grow his holdings as STI and LTI's convert annually

It looks like decent and continuosly growing skin in the game for Will. And he hasn't yet cashed out any yet - a good sign.

Discl: Held IRL and in SM

In chart review mode tonight. The CAT price action is as textbook classical technical analysis patterns as they come ...

- Sideways consolidation rectangle from Nov 2024 to mid-May 2025

- Then following the results release, breaks out above the rectangle, minor pullback to the rectangle, then off north it goes again

- A textbook 6 day bullish pennant is formed, followed by a nice, decisive breakout

- A descending triangle, consolidating for about 6-7 weeks

- Then off it breaks out again to continue the bullish momentum, where every day in the past 4-5 days, a new 52-week high is made as CAT continues to chart new heights ...

Discl: Held IRL and in SM

As a company moves from micro-cap to small-cap and beyond, a lot of things change but i increasingly think liquidity is a big one. When both price and volume pick up, sustainably, the amount of money changing hands each day really explodes. That’s exactly what we’ve seen with Catapult over the past year.

Using the 60 moving average, daily value traded has gone from $1.7 to $9m in 10 months.

As liquidity grows, the stock becomes easier to buy and sell, which brings in more and bigger investors. Which pushes the market multiple up (in general)

It took me a while to get why bigger companies usually have higher multiples -- i mean, just by virtue of their size you tend to think growth would be more limited. But it’s just that big money values being able to move big chunks without messing with the price. Even us small fry benefit from a liquid and deep market.

For the company, that bigger multiple ultimately means a lower cost of capital. And if they know how to use it, can really help turn a small edge into a solid moat.

All of which is to say, to myself as much as anyone, that across all of the risk/reward spectrum on the ASX, the best options (i reckon) are companies that have a decent shot at graduating from promising, cash-burning hopeful to a viable, credible business with genuinely good prospects. Because as that happens the share price not only gets boosted by the underlying fundamentals, but the liquidity kicker as well. Which can translate into a funding edge. which can help growth, which is a boost to the fundamentals and so on and so forth..

Anyway, have a happy weekend all!

I’m setting out my valuation of $CAT here, which I’ve been working on since the FY results were announced.

I’m not going to go back over the results or over my investment thesis, but definitely read @Strawman s “Bull Case” straw of three weeks ago (for the thesis) and the FY25 Results Forum Topic initiated by @BendigoInvesto, and the forum post by @Valueinvestor0909 (his Arichlife article) for some great analysis of the results.

I also recommend watching last week's video discussion between Claude Walker and @Strawman. Some really great insights here, and I found myself nodding furiously to most of it while cooking dinner last night.

In this valuation, I explore some of the key value drivers and sensitivities. My conclusion is that, despite $CAT’s tremendous SP progression (up around 60% YTD 2025), there remains significant upside potential that is not yet recognised by the market.

My overall view, is that in this particular race, $CAT has a long way to run and that it can comfortably keep delivering 15-20% annual returns from here for the foreseeable future. I would see any significant pullback from today’s price as a buying opportunity.

Valuation

My first detailed view on valuation is A$5.50 (A$4.50 - A$6.50). However, I must stress that this does not recognise the significant upside potential that may exist within the business today, and I point to some of this later in this straw.

The chart below captures my analysis, and I will explain what each of the elements means in the remainder of this straw. I'm sorry it is so complicated, but I will step through it.

The easy bits to see are Friday’s closing price (A$5.85) and the range of analyst views (www.marketscreener.com; n=6) of $5-$6.

An important motivation for me to do this analysis is to properly understand the upside potential in this business. It is clear the market has reacted positively, and the business is gaining increasing analyst coverage. I felt I wanted to have a point of view on risk/reward around the SP, partly to temper any tendency to take some profits if the SP continues to appreciate.

Another prompt is @Strawman's valuation of A$3.51, which is a simple calculation which asks: how long does it take $CAT to get to Will’s US1bn revenue at his target margin structure, and what would such a business be worth today, using an EBITDA multiple? I replicated a similar analysis (getting a similar number). My main concern with that valuation, is that at the terminal point, the business is still growing FCF at 19% annually, so an EV/EBITDA multiple of 12 seems low. Using multiples of 15 and 20 yields SP’s of $4.35 and $5.22, respectively, using similar assumptions to @Strawman .

Conclusion for My Investment Decisions

What emerges from my analysis detailed below is a view that:

- Should the SP fall back towards my lower range of A$4.50, I would be willing to add more to my existing 8% RL ASX holding.

- I won’t countenance selling in the short term at anything less that $7.00.

To unpack the analysis leading to the above chart, I’ve structured this straw as follows:

1. Approach of Valuation

2. Revenue Growth Scenarios

3. Margin Evolution Scenarios

4. Impact of Share Based Compensation

5. Discussion of Valuation Results (Referring to the Graph)

6. Further Upsides Not Quantified

7. Risks and When I’d Sell

8. Other Assumptions Used

1. Approach to Valuation

CEO Will Lopes have given us a nice framework for valuation.

Basically, what he calls “Management EBITDA” is simply Free Cashflow before Interest and Tax.

This has then enabled me to run a simple DCF where I have the starting point of FY25 and simply then have to make four assumptions:

1. By what year are the target margin ratios achieved?

2. How do margins evolve from today until the target ratios are achieved?

3. What is the revenue growth each year?

4. What is the rate of ongoing dilution due to share based compensation?

Of course, there are all the other assumptions that needed for a DCF, which I list at the end of this straw.

In line with @Strawman’s valuation, I run the DCF out to 2038, as this is notionally the period over which $CAT can grow strongly to achieve the ballpark $1bn revenue.

2. Revenue Growth

Total revenue growth in the last two years has been 18.5% and 16.5%, however the key value driver has been subscription growth, which has been higher, and there has also been the current headwind of a strengthening US dollar. As @Strawman points out, growing at 20% CAGR means it will take c. 13 years to hit $1bn revenue.

As @jcmleng picked out of the recent Livewire interview, Will has said he aims to get current ACV of $26-$27k per team up to $100-$150k, driven largely off product enhancements currently in development, and continuing to get more teams onto multiple products. In this interview he made clear that this won’t just be the preserve of the top elite pro teams, but that the capabilities in the platform will enable less well-off pro teams to make more productive use of their staff. So $CAT is to the coaching and fitness staff of a pro sports team what Cargowise at $WTC is to workers in a logistics firm, or $XRO to an accountancy practice. The software does more of the repetitive tasks, freeing staff up for higher value staff or allowing an operation to run a leaner crew. This cost saving agenda for clubs is in addition to helping them manage the players better, which is likely a much bigger prize.

This is going to be really important to drive the adoption of $CAT in pro sports teams. For the richest teams with budgets of $100m to $500m p.a., the spend on $CAT is peanuts. Once it is embedded in their workflows, the pricing power will be strong. However, in smaller clubs, with budgets of a few millions, investing in $CAT will be carefully justified. So running with a support staff of 6-8 instead of 8-10 is what will be needed to justify Will's vision of a broad capture of $100-$150k ACV deep into the subscriber base. It seems plausible.

So what's the revenue runway?

There are 3x-4x in the number of teams ahead of it, 4x-5x of multi-vertical conversion ahead, and with further enhancements drived by ongoing R&D spend at a solid 15% of revenue, ongoing, it does not take a leap of faith to believe that $CAT can grow strongly for many years to come. 10x to 15x in revenue seems very plausible.

In fact, in the early years, given the money going into pro sports, the strong growth of video in T&C, and the availability of Vector 8 which offers many improvements, there is every chance we could see revenue growth start to accelerate from the 18%-20% of where we currently are.

So this then leads me to my revenue growth scenarios for the next 14 years:

Within the series of curves on the graphs shown above, in Red Circles 1 and 2, I simply assume constant, annual revenue growth rates of 15%, 17% and 19% from 2026 out to 2038.

But growth won’t be linear, so in the Red Circle 3 lines, I’ve assumed revenue growth starts at today’s c. 19% p.a. and then exponentially decays each year to reach the values on the horizontal axis, i.e., 19% (no change), 17% and 15%. So the Red Circle 3 lines represent the upside to valuation that revenue growth stays "stronger for longer".

3. Margin Evolution

I’m comfortable with Will’s proposed target margin structure shown above, simply because of the track record over the last few years.

But what made me sit up and take notice in the FY results call, was Will’s statement that he believes $CAT can get to this structure by the time revenue hits $200m.

What!? That’s not FY39 but FY29. Wow. Of course we don’t know when that margin structure will be achieved, but it is a very important valuation parameter.

So, in the curves shown by Red Circle 1, I’ve assumed that the target margin structure is achieve in FY38, and that between FY25 and FY38 the gap between the current margin structure and the target closes linearly.

But, Will believes they’ll get there much earlier. And this is consistent with the current trajectory. Therefore the curves shown by Red Circles 2 and 3, assume the gap to the target margin structure is closed progressively between FY25 and FY29. Thereafter I’ve assumed the target margin structure is maintained. (I’ll come back to this later.)

So, now we can see across the three groups of lines how revenue growth and margin evolution drive valuation.

4. Share Based Compensation

I’ve done a deep dive to understand the impact of share-based compensation. It is tedious, but important. In the last three years, SOI have increased by 6.9%(FY23), 6.2%(FY24) and 2.7%(FY25). However, there are some important factors to be considered.

First, in FY23 and FY25 parts of the increase in shares was due to the earnout of the SBG Sports Software acquisition. And in FY24, when the SP was in the toilet, the Board seemed to double-dip, offering a second round of compensation, presumably because retention was at risk as staff shares were worth not very much and options were being cancelled.

So, with this understanding in mind, I’ve run scenarios for ongoing share-based compensation levels of 2.5%, 3.5%, and 4.5%. And that explains why for each set of curves, there are three closely stacked curves. The impact of dilution across this range has a SP impact of around A$0.10 at the lowest valuations up to A$0.15 at the highest.

5. Discussion of the Valuation

The above sections explain all the variables plotted in the chart above.

In choosing my valuation range of A$4.50 - A$6.50 I have been conservative. I believe that the target margin structure will be achieved over the next 4-5 years. And I also believe that revenue growth will be more in the range of 17%-21% p.a. over the next 5 years. Taken together, these will result in upwards revisions to my valuations over time, and the analysis presented gives an indication of the scale of sensitivity.

6. Further Upsides

I am going to explore some further upsides, not included in the model.

6.1 Revenue

Will has established a disciplined resource allocation model that appears to be driving c. 20% annual subscription growth, without pulling the pricing lever. I think that’s the right strategy – driving innovation to maintain the product’s industry leading position, and encouraging more and more of the target market to adopt, all-the-while achieving strong growth in free cash flow.

There are three potential future revenue opportunities:

· Providing more services to broadcasters to enhance viewer experience

· Leveraging the vast database of player data and enhancing predictive analytics

· Connecting third party devices and services into the platform.

And, as I explain at the end, my DCF Continuing Value growth rate in 2039 is 3.0%. Obviously, if $CAT is still growing revenue at 15%, 17% or 19% in 2029, then this is a conservative assumption.

I’ve not modelled any of these revenue upsides.

6.2 Margin

In my modelling I’ve assumed Will can hit the target margin structure and that when he does, the business stays there into the future. So, this is worth a deeper dive.

First Gross Margin. The target %GM of 80% has already been exceeded in the last two years. And with the transition to subscription now complete, and the focus firmly on software rather than hardware development, it seems entirely plausible that as the business scales, higher %GMs will be achieved. It doesn’t seem a leap of faith to consider that a $1bn revenue $CAT could have a %GM of 85%. One to keep an eye on over time.

“Delivery” and “S&M” will probably scale proportionately as the business scales. A target spend of 15% for S&M is comparable with Microsoft (c.12%) and Oracle (16%). Firms in more competitive markets can spend a lot more - Salesforce (33%), Intuit (27%) Adobe (30%). As $CAT scales to $1bn revenue, its reputation in the sector will be well and truly cemented, and so a relatively low 15% S&M spend sounds reasonable.

Equally, spending 15% on R&D is both wise and appropriate. For $CAT to maintain its industry-leading position, it will need to innovate continuously. I see only downside risk to scaling back on innovation.

A final upside is G&A. Here 10% has been assumed. As the business scales, provided it retains a clear focus on pro sports, its should be possible to retain a focused overhead structure. Upsides to 6% to 8% are conceivable.

In conclusion, considering both Gross Margin and G&A opportunities, it is conceivable that $CAT could expand its “Management EBITDA Margin” from 30% to 35%.

Again, I’ve not included this upside in today’s valuation. But it is one to bear in mind over the coming years.

7. Risks and When I’d Sell

Competition & Innovation

The global pro sports industry is vast and is attracting a lot of capital and technological innovation. While $CAT has a clear lead over its much small and less developed rival Statsports, it is worth keeping an eye on the competitive playing field. Of course, the industry is so large that there is room for multiple players. As importantly, is the need for $CAT to innovate, and bring more and more capabilities and features of value to its customers. Maintaining a consistent watch on both its innovation progress and the competition is key.

Management

The more I get to hear Will the more I am impressed with his leadership. Few businesses put out such an explicit, value-based, economic framework against which progress can be tracked. As far as I am concerned, $CAT has no need to offer guidance. They simply have to explain their results in the context of progress against this framework – and this includes periods when progress won’t be linear. I think it is easy to under-estimate the value that Will has personally brought to this business over the last few years. I don’t yet see this as a business that any professional manager can run, and I’d be very concerned if Will were to leave. It would be good to understand more about the bench below him.

Customers

It is important to see $CAT firing on all dimensions of customer value: low churn, increase multi-verticals %, new customer adds, rising ARPU. While growth won’t always be linear, I’d become concerned if during two consecutive years revenue growth fell back to 15%.

8. Other Assumptions Used

All values are $US unless states as $A.

Discount rate: 10%

Tax Rate: 30%

Capital Structure: No LT Debt; net finance cost of 2% of (Variable Costs + Fixed Costs)

AUD:USD: 0.65

CV Growth rate: 3.0%

Disc: Held in RL and SM

Great set of results from Catapult once again. Continues to deliver.

Full results presentation:

https://drive.google.com/open?id=1HMthZNAt7oIM8v_Sra3JkzxLhEljRiMk&usp=drive_fs

I had a closer look at the CAT Investor Day presentation pack. It was a good opportunity to step back from the usual results-announcement pack, look at the bigger picture, and confirm that the overall story and thesis still makes sense. The slides in the pack were useful - have pasted the slides which helped frame the story for me.

SUMMARY - THE STORY REMAINS HIGHLY COMPELLING

- CAT has one hell of a moat in an industry where each of the teams & leagues have every incentive to use technology to create a competitive edge to win

- CAT has many ways to win - Land new logos in an under-penetrated TAM and simultaneously expand/upsell into existing customers, 80%+ of which are single vertical - the business is really CAT’s to lose

- There is a clear strategy on how to win

- Results are showing as the financial metrics not only trend, but are accelerating, in the right direction

- CAT has warmed up nicely and I am eagerly looking forward to the game ahead (pun absolutely intended)

Discl: Held IRL and in SM

THE WHY

- Sports is big business - Large Market > $500b, massive audience, growing value

- Compared to other sectors, tech adoption is still in its early stages

- Teams are transforming everything that creates competitive advantage

And this will set off a Technology Arms Race which CAT is right in the middle of.

COMPETITIVE ADVANTAGE - THE MOAT

3 dimensions to the Moat:

- Vast Global dataset of athletes

- Multi-Sport learnings -> Proprietary Algorithms -> One Stop Multi-Solution Platform

- Specific Team Data used within a team across ALL stakeholders in a one-stop multi-solution platform

THE MARKET

- CAT remains under-penetrated across the globe

- Only 19.1% of CAT’s customer base is multi-vertical - 80.9% of Customer base is single vertical, massive opportunity to upsell

- Both these drive the $1b ACV goal - CAT is thinking big and going for it

PATHWAY TO $1B ACV - THE HOW

- Plan forward is clear - Land, then Expand

- Cross-selling strategy is trending in the right direction

- Clear Mid-Term milestones have been defined - (1) 5,000 Pro Teams (2) 50% Multi Vertical (3) 95% Retention Rate (4) 30% Profit Margin

FINANCIAL METRICS - THE PRIZE

- Significant progress on achieving the Rule of 40

- As revenue grows, costs growth declines - Revenue & Variable Costs, Fixed Cost % of Revenue are all falling and falls are accelerating

- Positive impact on free cash flow - not only turned positive but is increasing at a nice trajectory

This should hopefully at least mean "no negative surprises" ... otherwise, a really saying-nothing-new statement.

Not really that important, but it was fun to see this photo this morning from the back page of The Tiser (which is Adelaide's daily):

To the moon!

(Disc: happy holder)

How huge are these decisions…

CAT has been included in S&Ps ASX 300 and PME included in the ASX50, and (for example) Audinate AD8 has been dropped from the ASX 200…

Think about the weight of the “Passive” ETFs forced buying and selling between now and the 24th… or do they rebalance after the 24th?? ????

Impressive results from whichever angle! I really like the transparency that management have provided in terms of its targets, across the Board. This has really helped in managements narrative as to how improvements in the operational KPI's lead to other good things - the story could not be any clearer for me.

I prefer to compare the results Half-on-Half instead of YoY to gauge ongoing momentum, as there was already a sharp step up from 1HFY24 to 2HFY24. The HoH comparison clearly shows the ongoing momentum across all the key metrics but does temper the achievements a bit. A few things to call out from a HoH perspective:

- Lifetime Duration improved by 0.6 years, a 8.6% improvement

- Multi-Vertical Customers was up a whopping 47.3% - this is good evidence that the Expand Go-to-Market approach and integration with video is really kicking in

- Free Cash Flow was up 50% HoH

- Rule of 40 increased by 5% - this is really good to see following the 6% increase from 1HFY24 to FY24

- Revenue was up 14.6% but expenses only went up 9% - cost control has been sustained - a good sign of things to come

- Tactics & Coaching revenue spiked 31.1% but margins are lower in this segment, hence the 4.1% fall in margin HoH - one to watch out for

- Variable Cost % on Revenue actually went up from 52.2% in 2HFY24 to 52.4% - still bloody good, but it does make the dip in the ratio from the slide pack, which compares YoY, less bullish. The next 7% to get to 45% will be the hardest as the easy steps have already been taken, so I expect this ratio to only marginally drop HoH from here.

CAT Is absolutely firing on all cyclinders but there is still a lot to come. This is my favourite slide that shows the promised land:

It was also good to see the Capex taper off - Will did say a lot of the hard technical platform work was done to enable scale, in the early months of his coming onboard. This is now payback time!

Onward and upward!

Discl: Held IRL and in SM

Sports tech. firm $CAT reported their 1H FY25 results.

My overall assessment - good, steady progress. 1) Good revenue growth 2) Importantly, $CAT achieved incremental profit margin of 75% (which I think is what Will has consistently said the goal is.) and 3) Ongoing innovation, particularly with the sideline video product. Video in T&C is growing very strongly, with strong ACV gains being a leading indicator that this will drive ongoing revenue growth.

Their Highlights

• Annualized Contract Value (ACV), Catapult’s leading indicator of future revenue, grew 20% on a constant currency (CC) basis year-on-year (YoY) reaching US$96.8M (A$143M)

• Revenue increased to US$57.8M (A$85M), +19% (CC) YoY

• The profit margin on the incremental revenue generated reached 75% YoY; delivering Free Cash Flow (FCF) of US$4.8M (A$7M)

Catapult delivered another strong performance from its core SaaS verticals, with ACV growth of 20% (CC) YoY. This reflects the addition of US$10M of incremental ACV half-on-half (HoH), the largest incremental dollar ACV increase in any previous half year period. Catapult’s core SaaS metrics continue to demonstrate the embeddedness of Catapult’s product solutions into team workflows, with:

• ACV Retention consistently strong at 96.2%

• Customer Lifetime Duration increasing 7% YoY to 7.6 years

• Pro Team Customers increasing 7.9% YoY to 3,470 Teams

My Quick Assessment on Cashflows

Continuing good progress. 5th consecutive positive operationing cashflow and 3rd consecutive FCF.

Operating leverage showing through in cash flows: Receipts +21.6% to pcp, Payments +17.4% to pcp, leading to OpCF +34% to pcp.

Investment continues to fall as a % of Revenue.

What's good to see in the chart below is that costs continue to be well-managed, while top-line growth continues. (look at the relative slopes of the dotted blue and orange lines)

$CAT took the opportunity in the period to pay down $6m of debt.

Disc: Held in RL and SM

I'm looking forward to reading other SM reports on $CAT today, as I am focused on other things today and won't make the call, but I've just noticed their headlines:

- Annualized Contract Value (ACV), Catapult’s leading indicator of future revenue, grew 20% on a constant currency (CC) basis year on year (YoY)

- The Company hit a milestone revenue mark of US$100.0M (A$152M), up 20% (CC) YoY

- Profit Margin improved +125% YoY resulting in US$4.6M (A$7M) of Free Cash Flow

My quick calculation of FCF is $2.767m (OpCF $31.703 + InvCF -$27.055 + Leases Repaid -$1.972m), however, I've not checked the change in working capital on this.

And of course, this overlooks the hefty non-cash share based compensation element of $9.7m. Which I think means we are being diluted about 4% each year - correct me if I'm wrong.

All that said, the 6-month view below indicates that $CAT has made the transition to a sustainable business. If they can keep on this track. (Note: H2 receipts is seasonally weaker, but look at the cost control. Can they sustain this?)

I recently dipped my toe back in the water with $CAT in RL and SM. I'm still not convinced, so will have to have a harder look at this when I get the time. The slope of my FCF line is promising, however.

MMMM well lately its has been a little difficult to pick the movements and how they will end up panning out. For now Im still seeing a short term down side. Here's what my charts are looking like for now

1 hour chart

So my target is somewhere in the 1.47 to 1.41 range.

That range coincidentally also converges with the 15 sma, & support (the Pink horizontal line and my wave IV zone on my 3day chart. MMM nice set up if it makes it there.

3Day chart

Here's the kicker. You can see the thin blue rising trendline just under todays candle on the 1hr chart. That is forming a consilidattion triangle. If it doesn’t drop below that today ish then it may push higher and not play out my declining wedge pattern shown in Yellow. Again, I will say, Im not sure on direction and will just have to watch and see. Im not putting a larger position on as yet until I have better confirmation of which is going to play out. (also not Jeffries has recently put a price target on for 1.90 which is at the top of my next target box for w3)

Also Im away for anyone who is reading my thoughts so wont post all the time. However I am watching each day and will let you know if I make any decisive moves.

Good luck all

Helllllo Catapult (a nice update)

Well that one dragged on and approx a week ago I wasnt certain if there would be another small leg down to my anticipated box marked (V) on the charts. I have missed out before getting the bottom, hence why I bought in a start position at the green horizontal line. Glad I did after this mornings move.

You will notice the white horizontal dashed line just above the pink horizontal support line. This is where wave ii should have fallen to historically. It never quite got there, again showing a bullish sentiment and boy has it popped. I expect it to climb to the top of the rising Channel into my wave iii target box and also coincidentally Jefferies Brokerage price target however I'm going to build a bigger position on the pull back to wave iv. I will probably skim off the 10% or so profit @ wave iii however I will leave the original position there for the add too at the wave iv for the next big leg to wave v of wave 3.

Good luck all

Im starting to layer in a position, here's why.

1Day chart

30m Chart

Ignor the last green bar up on the 30m chart after I took this screen shot, that was me starting my position. See timiing is impossible really though I do have targets and Im now conflicted if this is the bottom or we still have another small wave 5 down to go. So im staring to build my position. I think the graphs above show everything Im thinking. I do believe it will soon move up with some energy.

The circle on the stochastic indicator on the 1d shows the current (white line) to be above the Yellow (longer term 30m position) which is point pointing down. Thats the only reason I see another drop coming to approx. $1.19 - $1.16. There is a lot of support between 1.13 to 1.19 with moving averages and a historic Support level in there as well.

The market has also been pre empting reporting season lately and building up positions before hand incase of a good report (Drone Sheild, hence why it dropped on a great report, they pumped it up too far).

If this plays out how I expect it to then I will be adding substantially to my position taken today and will be holding much longer term to ride the 3rd, historically the largest, wave up.

Good luck all hope this gives some insight from a technicals perspective.

Update on Cat charts

This is a bullish stock im also hungry to be part of. We can all see by the agressive moves up over the last year and is playing nicely to my targets so far. It has almost satisfied my rules when it finds this next bottom (wave(ii) of the larger wave3) and I will be layering in a sizeable position with a hard stop loss below. My target should be @ the $1.12 SP however when its a bullish stock as this one is, they dont always make it to my targets and proceed to rocket up before reaching them. I will probably take a smallish position before it reaches my target then layer in once I see that its heading up as I predict. Its a fluid choice of course and will take it day by day.

The next wave up (wave3 of 5) is going to be great and is usually the most bullish of any 5 wave structure. As you can see Jeffries (brokerage firm) has a target of $1.50 however I feel it may go even higher (wait and see) See my updated charts below.

Good luck everyone.

Update on CAT. Thought I would update the charts for cat as it drove higher than my last post (should have seen that coming as it was pushing for the top of the incline channel). So looking at it now it seems to be in a side ways consolidating period. Im still waiting for a retrace back for wave (ii) down to aprox 50% of the last wave marking somewhere around 1.14 my new revised target after it pushing higher than i originally thought. I have noted Bell Porter has down graded Cat from BUY to HOLD confirming my thoughts of an impending retrace. So here is what my charts looks like now.

I have put alerts on it for the bottom pink support line (and coincidently the 50% mark of the last big wave) and also on the 50sma on the 1 day chart to alert me its heading in my target direction. FYI im looking to enter on the next major pull back. Ill let you know when it gets down there as to my udated plans

I have been watching CAT for a while now and is finally getting close to my buy set up so thought I would up date you all. So far it has performed perfectly to my target zones and is behaving to my Fib levels spot on. Today it should reach the upper end of wave (i) on the chart @ $1.25 and the retrace to approximately the 1.03 - 1.07 zone for wave (ii) before starting the next large wave (iii) taking us up to the 1.50 - 1.64 zone of wave (iii). Ill update you all when it reachs the wave (ii) zone on my thoughts then although I will be looking to enter around there with a hard stop just below.

Catapult has today given a trading update following the end of their first quarter (their financial year ends in March)

It looks like the company is (finally!) on the cusp of being free cash flow positive. And top line growth remains strong.

They don't usually do quarterly updates, and there's not a lot of detail, but you can read the full announcement here

Very short 14 minute call as the detail of the preso is contained in a pre-recorded video that accompanied the results announcement.

Will reiterated the highlights of the FY23 performance

Then took 3 questions, as that was all that was forthcoming, responses to those questions:

- Wearables growth came from expansion in underperfoming regions - EMEA, US Collegiate, Latin America/APAC

- Confident of sustaining the 25% growth in wearables as (1) only ~2,400 professional teams are customers vs 20,000 professional teams (2) good greenfield growth in FY23, expect to maintain this pace of growth in the next 2-3 years (3) launching of 2 new products in FY23 which opens up new markets

- Vector T7 - opens up basketball which is under penetrated

- Vector Core - lighter version of Elite Wearables designed to help very large organisations support lower tier teams

- Video growth came from 2 areas:

- Legacy Video solution, 7% growth targeted at American Football and Ice Hockey, mostly from upsell and price increase

- SBG Video solution 27% growth, targeted at Soccer, Motosports etc - this is almost Wearable-like growth

- There is a transition plan for NFL from Legacy to SBG Video starting this season, fully transition in the next 1-2 seasons

- Strategy of “Land with Wearables, Upsell with Video” is working very well - there was a 9% growth for customers with 2 products - expecting this to rise to 30-50% (if I heard correctly) as they focus on upselling more video

- FY23 was the year that saw the operating leverage from the SAAS model kick in

- Focus in FY24 is to return to FCF positive - very confident of this occurring as EBITDA has been a good proxy for FCF

Will need to view the management pre-recording to further digest the results, but am liking what I am seeing thus far.

My view remains that the turnaround has already occurred since Will/Hayden rocked up. The FY23 results is the evidence of that turnaround working and in play - game on!

Have been busy for most of the day, but when I skimmed Catapult's results this morning my first instinct was "the market should like this".

But, with shares ending down 10%, it seems I was way off base!

So let's dig in and see why that might be.

Of course, the company was keen to put its best foot forward. And it did have some genuine positives to report.

- The transition to a subscription model is largely complete, with subscriptions now 92% of total revenues (and 98% for the Professional Performance & Health segment)

- ACV grew 32% (double FY20) and was 51% higher in the all important Americas market.

- Average Annualised Contract Value (ACV) per customer was up 4.2%

- Customers that contribute to ACV were up 16.3%

- P&H churn remained low at 3.5%

- MatchTracker and Vector integration ahead of schedule, with Tactics and Coaching growth of 29.7% in APC during the key selling season.

- Customers with more than one solution grew 27%, showing good success with cross selling, and they expect this to accelerate with the integration of MatchTracker and Vector

- Positive operating cash flow (just, and with some caveats)

- US$26m in cash on balance sheet and growth spend fully funded.

- Strong prosumer ACV growth (but off a very small base)

Aside: The transition to SaaS always has a bit of a drag on revenue, as revenue that was previous booked upfront is now recognised over a much longer period. The advantage is that it provides for smoother and more consistent cash flow and revenue, and (ideally) makes for an easier purchase decision by the customer as it's a smaller ongoing cost, rather than a large one off cost. It transitions expenditure from Capex to Opex. Now that this transition is behind them, growth in revenue should more closely match growth in ACV.

The best part of Catapult has (to my mind) always been the Pro P&H segment, and here we saw 32% ACV growth and they have still only captured <10% of the available market opportunity. I've said it before, but i wish they had remained focused purely on this instead of trying to expand into too many other areas, too quickly.

At any rate, they did what they did, and while that has seen higher costs and investment spend, they do have (finally, i hope) a market ready product in Tactics & Coaching (T&C) and a solid P&H customer base from which to cross-sell from.

Indeed, the T&C segment has a large addressable market for which they have only captured less than 2.5%. The customer spend here is higher than for P&H and enjoys 90% gross margins and even lower churn (1.5%). The APAC region was the only market in which the newly integrated product was able to be sold (due to the different sales cycles in different geographies), and here T&C ACV was almost 30% higher, compared to just 7.2% and 3% in the Americas and EMEA, respectively. It bodes well for future growth when they start to present this to the northern hemisphere markets.

The company is targeting long-term ACV of >US$400m, compared to US$63.9 at present.

If we just take expanded penetration of P&H, T&C and increased customer spend, that takes us to just shy of US$300m. The rest is inorganic (acquisitions) and prosumer -- and i'm not really keen to put much weight on that. Still, it's a decent uplift if it can be achieved.

Ok, so all of that seems pretty good. Catapult is now a more pure play subscription business with a fully fledged market ready product set and very strong ACV growth with a very large market opportunity still ahead -- and they remain the largest player in this space.

And you get exposure to all of this for 2.6x ACV or 2.2x revenue. That just doesn't seem demanding at all -- especially with the company guiding for FY23 ACV growth of 20-25%. AND, management said they were fully funded to achieve growth ambitions (ie. no more capital raises)

So, what's the market worried about?

Well, mainly, the company is still not profitable. When they hell are we going to see some scale advantages start to emerge? Surely not for a while if they keep increasing the expenses -- in fact, we saw cost increases across sales, product and operations. I'm all for spending money with a good ROI, but c'mon guys! I think we've been patient, but when are we going to see the results? Show me the money!!

The NPAT was negative US$32m

EBITDA negative US$5.8m, even on an underlying basis

Positive operating cash seems largely a result of shifting a lot of expense to the investing section (capitalised development COGS costs). Free Cash Flow was negative US$17.9m

I do think the new CEO is far more targeted in the investment spend, but I was hoping to see even more restraint. Especially in this new market environment which is far less tolerant of cash burning operations.

So i do get the market's reaction now that I've had a chance to dig into the details. But, call me an optimists, the potential here remains very attractive:

Catapult is a market leader in a large and resilient industry undergoing structural change (digitisation). There is genuine sales traction, and that's growing at very strong rates. The revenue is very sticky and with attractive gross margins. It is also, apparently, well funded and on track to achieve its ambitions without the further help of shareholders.

Sadly, until they achieve sustainable free cash flow, while still maintaining growth, the market is likely to remain sceptical. And fair enough.

If it wasn't for the very solid ACV growth, and expectations for that to continue, I'd be out of here. But, for better or worse, i'm prepared to stay put for now. I think it's called the endowment effect...

Catapult has announced its entry into the eSports market with a partnership with NASDAQ listed Motorsports games (NASDAQ:MSGM). (see here)

There's no doubt that eSports is an exciting space, and Catapult was keen to emphasise the size and growth of the sector. And given the data they collect, it makes perfect sense for them to move into this domain.

But..

There were no details on the nature of the multi-year subscription agreement (although we can assume it's not material in and of itself, as it wasn't marked as a market sensitive announcement).

Moreover, I'm not sure Motorsports Games is that impressive a customer. Their latest instalment of their Nascar series looks to have bombed:

Reading through the reviews, it's pretty brutal stuff.

That being said, NASCAR 4 & 5 have much better reviews, and it's also probably fair to say that these titles are more aimed at the very serious end of the market, and not casual gamers (you need a steering controller to play these games).

Looking at MSGM's track record, shares are down ~70% since listing and the latest quarterly result isn't great (although they claim this is due to the timing for some of their releases). In the last 9 months, they made US$120k from eSports segment, down from US$290 in the previous corresponding 9 month period. Again, there are timing factors at play in relation to when events were held, but they are clearly a very small player in this space.

I'll be keen to ask management more about this at our upcoming December meeting.

Anyway, like I said, this is a logical area to move into and a great way to gain extra value from the data they collect. I'd just like to better understand the nature of these deals, what development and operational costs are needed to support this foray, and whether or not they are partnering with organisations that have any strong presence in the eSports market.

Catapult has signed a multi-year deal with Roush Fenway Racing to use its recently acquired Racewatch solution.

No financials given, and in and of itself the deal is likely not likely material in the overall scheme of things -- but it's an encourage first step into a large and (hopefully lucrative) new vertical.

Roush Fenway Racing is a major player in NASCAR and should serve as a potent reference client for future sales.

Doesn't change the thesis for me, but good to see some movements on this front after their acquisition of SBG Sports a few months back.

Shake 'n Bake ;)

The announcement of a new independent director isn't usually a factor for me, but Catapult's latest appointment seems noteworthy.

Tom Bogan (linkedIn profile here) will join Catapult's board from tomorrow. He's got an impressive CV, acting as the current vice-Chairman of Workday, former CEO of Adaptive Insights and former partner at Greylock. All of these are huge success stories in the US.

Given Catapult's North American focus and opportunity, it's great to be able to tap into that experience and no doubt a valuable network. In fact, he's heading up a new SaaS Scaling Committee specifically created for this purpose.

I don't want to oversell it -- i'm not changing my valuation or anything -- but I do think this is quite encouraging. Someone like that virtually has their pick of board spots, so to pick a relatively tiny Aussie company suggests he sees big potential (Workday does 40x CAT's revenues).

If Catapult can continue to show cost restraint and a rebound from the covid-induced slump, I suspect it will be due for a re-rate by the market.

FY21 will be a rather ordinary year given the weak first half and the lingering covid situation in the US, but i'll be pleased so long as there's some good indications the sales trajectory is returning to a 15-20% range. If not, it'll prompt a rethink.

ASX announcement here

This was a really good result for Catapult. It gives me further encouragement that the business has indeed (finally) turned a corner, and that the new CEO is on the right path.

- Subscription revenue up 21%

- EBITDA up 225% (from $4.1m to $13.3m, and ahead of expectations for $11.5-12.5m)

- Free cash flow positive, $9 million

- 39% growth in multi-solution customer numbers

- Cash on hand of $39.8m (as of 14 August)

Capital sales were down 27% as the peak US sales season was impacted by covid, and as the grouop continues to shift customers to a subscription model. As a result, Revenue was only 6% higher. The company expects a good deal of sales that were deferred in Q4 to be recorded in the current first quarter.

Also, applying D&A, the company still reported a statutory loss of $7.7m.

Looking ahead, the company expects to increase R&D and also some cost reductions acheived in response to COVID will be wound back. The business still expects to generate free cash flow in the current year.

(note, they are moving to a March year end and will report future results in USD to reflect their geographic exposure and better align with sales cycles).

There's a bit of detail to explore, read the results presentation here.

Catapult is expecting the following for FY2020:

Total revenue between $100-$101 million, up 5.3% from $95.4m in FY19.

EBITDA of $11.5-12.5m, up 192% from $4.1m last year.

$9m in free cash for FY2020; a big turnaround from the $24m loss last year and achieving a positive result a year earlier than expected.

Cash balance is $27.5m.

CEO Will Lopez said the professional sports landscape had improved since the last update on March 27, and that the business had continued to win new deals and retain customers during the lockdowns. However, this disruption has delayed things and many of the sales that would have been made in the last quarter are now expected to be delivered in the FY21 year.

With cost reductions already in focus, it seems covid allowed the business to cut costs faster and deeper than originally planned. There was always a nicely profitable business inside of catapult, so it's great to see that being unearthed (seemingly) without much of an impact on sales growth.

Speaking of which, 5%-odd top line growth would normally be a very disappointing result, but in the context of a raging pandemic -- one that had a direct and significant financial impact on its customers -- it could have been a lot worse.

As you can see in the chart below, sales are always much stronger on the second half (with sales typically dropping a bit from one year's second half, to the following year's first half). In this instance H2, sales were the same as H1 and down 5% from H2 2019. Normalising FY20 second half result using the H2 19's growth, sales would have come in 12% higher at $112m.

Given things will be tough for the foreseeable future, I'd be happy enough if they could score 10% sales growth for FY21, before returning to 15-20% odd growth (on average) over the coming 5-6 years.

Based on last close of $1.27, shares are trading at an EV/EBITDA ratio of 18. Assuming they can recover to near pre-covid sales growth in the coming years, and maintain cost discipline, that seems very undemanding.

Full results will be out late August.

Read ful announcement here

A good result for the 6 months ending Dec 31, 2019.

Revenue grew 18% to 50.7m, while the net loss essentially halved to -$4.8m.

Catapult recorded a positive EBITDA of $5.7m compared to a loss of -$1.4m in the prior first half. (They did get a bit of a boost from the adoption of AASB16. On a like for like basis, EBITDA came in at $4.7m)

Importantly, Catapult saw positive free cash flow of $13.6m, which has boosted cash to $24.7m. There's some seasonality here, but the company reaffirmed its expectations to sustainably generate positive FCF by FY21, and it seems unlikely it will need to raise cash again.

Cross-sell initiatives seem to be doing well, with the number of customers with more than one Catapult product rising 66%. Overall customer numbers grew 19%.

The major North American segment saw growth of 21% in revenue -- it now represents 70% of the total. EMEA grew 15.5% and APAC grew 10%.

ARR grew 20% to $68.8m.

Perhaps best of all, operating costs declined by 4%. (poor cost discipline in prior periods under previous mamangement was always a big concern).

Churn decreased from 5.2% in FY19 to 4.8% at the half.

Also encouraging to see the previously striggling Prosumer segment improve its loss from -$3.6m to just -$0.4m. Revenue growth was 9%, with reduced costs and marketing spend driving the bottom line improvement.

Results presentation can be viewed here