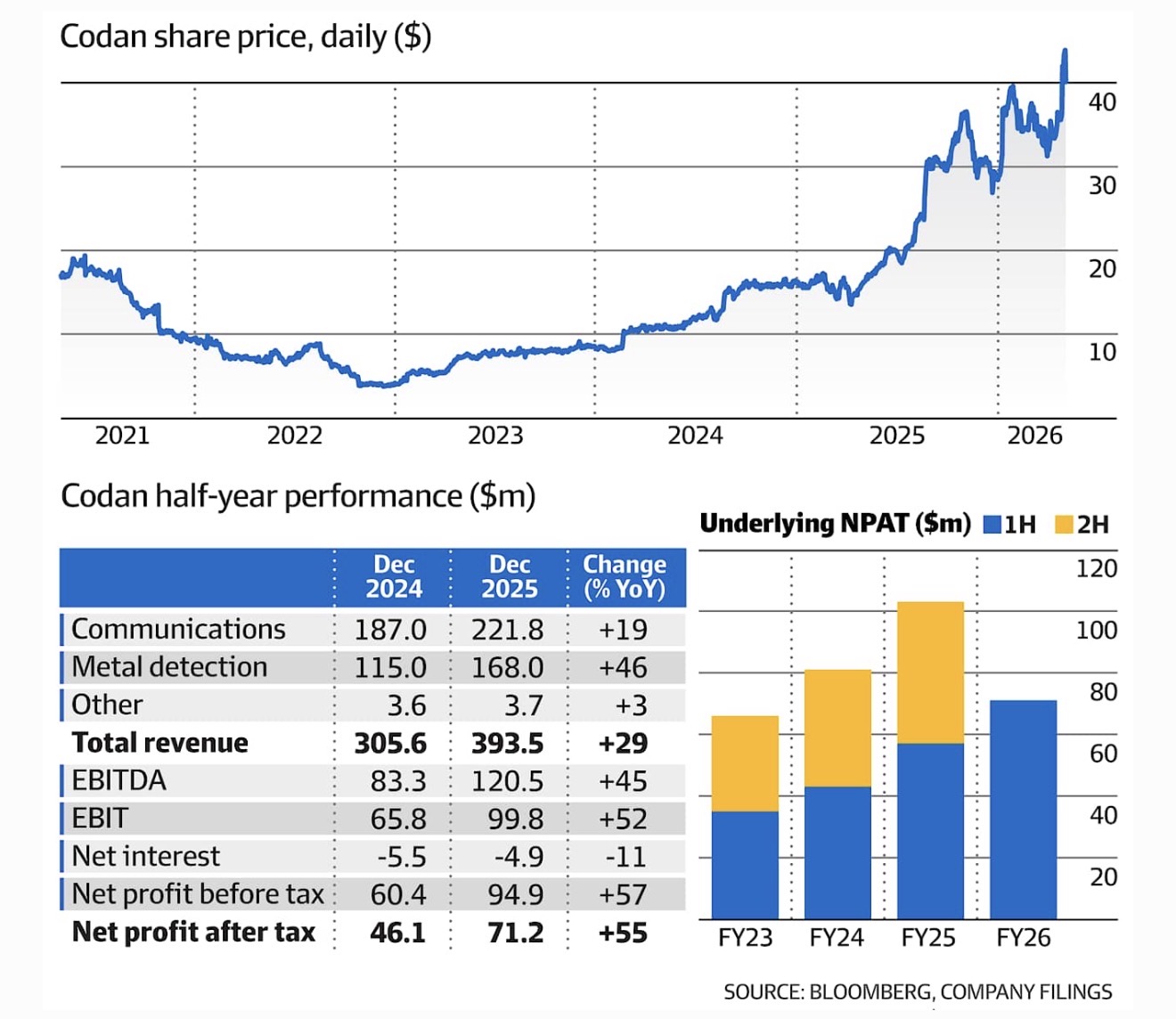

Pamela Wall, the billionaire philanthropist behind $8 billion engineering giant Codan, is taking some money off the table.

Canaccord Genuity was putting together a block trade overnight – valued at around $300 million – on behalf of the family that owns about 18 per cent of Codan, people involved in the transaction said on condition of anonymity given the sensitive nature of the sale.

The stake was owned by co-founder Ian Wall, who set up the company in 1959 with two friends, Jim Bettison and Alastair Wood. It’s now controlled by his 93-year-old widow, Pamela, who will retain around $1.2 billion in Codan shares after the sell-down.

While the numbers were still moving around as of Monday night, it is understood shares were being offered at about $39 apiece, an 11 per cent discount to the last close of $43.92.

It comes a week after Codan handed down a bullish trading update for the 2026 financial year, forecasting $235 million in earnings before interest and tax and $170 million in net profit after tax. Its share price ended the day around 15 per cent higher.

Codan said that its DTC unit was on track to achieve revenue growth at the top end of the 15 per cent to 20 per cent range for the 2026 financial year. Minelab revenue was also tracking ahead thanks to “a favourable gold price and recent successful product releases.”

Held IRL (6.6%) SM (31%)

Codan has just announced an upgrade to guidance. NPAT is now expected to be $170 million, up over 60% on FY25. Analyst consensus for NPAT prior to this announcement was $152.5 million. I calculate EPS of $0.935 per share. At the current share price ($41.50 per share) that’s a PE multiple of 44 times. I think I’d rather be a seller than a buyer at these levels.

(AI summary CommSec)

Full ASX announcement

Held IRL (7.6%) SM (29.5%)

The share price momentum for Codan shares has me gobsmacked! The share price is now 9x its 3 year low back in December 2022. This is when the Minelab sales took a big hit due to the Russian Wagner Group taking over many of the gold mines in Africa, decimating the livelihoods of many of the African artisan gold miners. Back then, Minelab sales in Africa produced most of the earnings for the business. The business has now grown to be much more diversified.

The share price has now passed analyst consensus by $6 per share (12 month consensus of 7 analysts on Simply Wall Street is $28.40 per share).

Codan has definitely been my best ever stock pick, especially when you consider it has also paid fully franked dividends (although the yield has shrunk to less than 1% at these high valuations). Codan still remains my largest holding on SM and our second largest holding IRL despite my attempts to slowly reduce its weighting.

I think it’s very expensive at $34 per share, but in hindsight I shouldn’t have sold a single share! How long do you keep holding a business like Codan when it’s overvalued and on a red hot run like this? Obviously a long time if you are purely a technical investor. There’s a lot to be said for taking notice of the charts in your buy, hold and sell decisions. I’m still learning on this one.

My strategy at the moment is to keep riding with the momentum (while it lasts) while reducing the holding slowly. Codan is definitely riding on the wave of the record gold prices.

Three years ago I started writing about Codan on Strawman. Back then Codan was well and truly in the dog house! I found this old straw I penned at the time, #History repeats. Here is an extract from the straw:

“I’m a newcomer to Codan, having bought my first shares in January this year. However, for those who have held Codan for more than 8 years, you might be feeling an uncanny sense of déjà vu right now. I found this article from June 2014 (copied below). As you read through this article you could be forgiven for thinking you were in an 8 year time warp. The question on my lips now is…will history continue to repeat itself over the years ahead?

Following an 80% fall from its peak share price in April 2014, it took 5 years for Codan to reach its former peak, and then 2 years on from that the share price was more than 5 times higher than it’s former peak. I’d be happy with that!”

Well, guess what…Codan has done even better this time around! This time the share price is 5.5 times higher than its low of $3.72 just 2.5 years ago! Am I happy with that? You bet I am! But what now? Is Codan expensive? I would say yes and I’ve been taking some profits off the table.

Codan is still a high quality business. ROE is still good and improving (forecast 23%), but not as good as it was before the Russian Wagner Group all but destroyed the artisan gold mining industry in Africa. Metal detector sales dropped dramatically because half the metal detectors were being sold to African villagers.

Source: Commsec

Codan management were quick to focus their attention to growing the communications business, which they have. By FY26 Codan should achieve record EPS of approx 65 cps. That puts the current Codan share price ($20.41) on 31 x FY26 earnings. Earnings are forecast to grow at 15.7% and it has a net debt to equity of 25%, which has been increasing with acquisitions over the last 3 years.

So is it expensive? Here is a PE chart of Codan over the last 5 years. I think 31x FY26 earnings is getting up there!

Source: Simply Wall Street

Using McNiven’s formula and assuming forward ROE of 23%, current equity of $2.74 per share, 50% of earnings reinvested, and dividends paid at 1.6% fully franked, I come up with a forecast annual return of 7%. That’s probably OK for a very high quality low-risk business. I’m not sure Codan fits that category.

What do the analysts think? The consensus 1 year target price from 7 analysts on Simply Wall Street is $18.15. So the share price looks expensive here too.

Despite all this I don’t think there is a hurry to sell Codan in a big hurry either. I’m not an expert on technicals, but I think the chart still looks OK, and we all know the chartists rule! Just look at what happened to CBA…until it didn’t!

Of course the fundamentals will override everything when Codan delivers its FY25 financial results in August. Only time will tell.

Held IRL 10%, SM 25.5%. Reducing.

Wow! Codan is up 16.6% today to $9.80. I must admit the market reaction has surprised me a little. When I looked at the results they appeared to be in line with analyst earnings forecasts (3 analysts, Simply Wall Street data) for FY24 of 43cps. Earnings for the half were 20.9cps, so it seems to be on track. Although Revenues look higher than FY25 consensus (Pro rata). Let’s look at the highlights from the Half Year Accounts.

• Group revenue of $265.9 million, up 26% versus prior corresponding period (“pcp”)

• Net profit after tax of $38.1 million, up 24% versus pcp

• Performance by Communications businesses in line with 10 to 15% revenue growth target range:

- Communications revenues of $153.6 million, up 12.5% versus pcp, segment profit $37.8 million, up 9% versus pcp

- Communications orderbook of $183 million, +12% versus 30 June 2023

• Metal detection revenues up 49% versus pcp, with all divisions contributing to this growth

• Net debt of $82.5 million at 31 December 2023, having funded $30.3 million for the Eagle and Wave Central acquisitions in the period

• Earnings per share of 20.9 cents, up 22% versus pcp

• Interim dividend of 10.5 cents, fully franked

Sourced from the Presentation

Perhaps all the excitement is over the strong communications order book of $183 million, and the Outlook statement (see below) where management expect to “continue targeting revenue growth in the 10 to 15% range. With the benefit of acquisitions made in FY24, Communications overall growth is expected to exceed the top end of the targeted range.”

…and the Outlook

“When considering the outlook for the balance of FY24:

• After normalising for the large Communications project delivered in FY23 (approximately $20 million), and excluding the benefit of acquisitions, the Company continues to target revenue growth in the 10 to 15% range. With the benefit of acquisitions made in FY24, Communications overall growth is expected to exceed the top end of the targeted range; and

• Minelab is targeting a second half result similar to the first half of FY24, with FY24 revenue growth of 20% versus FY23

The Company will continue to keep shareholders updated as H2 FY24 progresses.”

My View

I’m a big fan of Codan and I’m pleased to see the bounce in the share price today, but I’m still trying to get my head around such huge positivity. @Bear77 is a big fan of Codan too, and I’m keen to hear what he has say about the results.

I think shareholders might be looking back at historical PE ratios and thinking now the company is turning around its now worth a multiple of 23 x FY24 earnings? The last time Codan was trading at a PE of 23x was in 2021 before the Russian Wagner Group all but destroyed artisanal gold mining in Africa. The gold detector business has a higher return on equity than the communications business and we have seen ROE fall from 32% to 17% since 2021 as a result. If someone could get the gold plundering, murderous Russian paramilitary out of Africa then Codan would be back on ROE above 30%. Putin needs the gold to fund the Ukrainian war, so pulling out of Africa is highly unlikely, unless he ends up with some Novichock in his underpants! ( ‘Navalny’ free on SBS is a must watch! A great man murdered by Putin).

Codan is rebuilding and diversifying its business and I expect ROE to improve to low 21% over the next 3 years. I think the current PE multiple is looking a bit high.

Valuation

Once again I’ll use McNiven’s Formua to value Codan assuming ROE 21%, Equity $2.31 per share (1H24 balance sheet), reinvested earnings 50%, and a required return (RR) of 10%, I get a valuation of $8.60. There’s no doubt Codan is a high quality business, but it’s starting to look a bit pricey. It’s one of our largest holdings IRL (9%) and in my top three on SM (14.8%). However, I think it’s HOLD at these prices. I’m certainly not a seller.

Shock 1H23 guidance

AGM Chairman and CEO Addresses, 2022

Codan’s 1H23 shock profit guidance of between $25 - $30 million announced at the AGM not only surprised me, it shocked most of Codan’s investors. It is now feasible that Codan’s FY23 profit result could end up similar to my worst case scenario of $57 million (37 cps).

This could put profits down about 40% on Codan’s record $100 million profit result last year. Codan puts lower profit guidance this half down to the uncertainty relating to the timing of shipments on a large communications project as well as the ‘lack of visibility’ in a number of African markets.

Codan said it recently learned from their people on the ground that there are a number of factors impacting Minelab sales into Africa. The Codan CEO, Alf Lanniello, said “Beyond COVID, geopolitical and macroeconomic challenges remain across Africa, and it is only now clear that there is an overhang of product in the market following the very significant volumes of detectors purchased in FY21 and FY22.”

Codan CEO Alf Lanniello said “Sudan has been materially impacted by the military coup. The previous democratically-elected government actively encouraged artisanal gold mining as a means of driving employment and building wealth within regional communities. Now, under military rule, some gold mining regions are being controlled by military forces and remain off limits to artisanal miners.”

In fact it is worse than this as I uncover further down!

Alf said “This was a key reason for the reduction of our sales in FY22 and this market has further declined in FY23 along with broader weakness seen throughout Africa”.

Alf said “Our planning and budgeting for this year anticipated a gradual improvement in sales into Africa in the first 6 months of this financial year. Following a recent in-depth market by market analysis after our people travelled to all regions, we have now formed the view that sales will remain depressed for FY23.”

Are Codan’s days of consistent growth over, or will this business shine once again?

Codan Blindsided

It concerns me that Codan appears to have been blindsided by what has been happening in Sudan, Codan’s single largest African market. Codan had not picked up on the significance of what was happening in Sudan until just recently when their team was able to “get back into the field after COVID”. At least that is what Codan was telling unhappy investors at the AGM who questioned why profit guidance had not been announced earlier. Until the AGM, Codan had left several analysts forecasting profits similar to last year. So what has gone so wrong so quickly…or perhaps why has it taken so long for Codan to find out what is REALLY happening in Africa?

What’s happened to the African Minelab Profits?

The African gold detecting market has been the largest market for Minelab historically, with sales peaking at $185 million in FY21, before declining to $125 million, or 26% of Codan’s total revenue in FY22. However, due to Minelab’s higher profit margins, this represented about 35% of Codan’s total profits, or $35 million for FY22 (on my calculations).

Now doing some rough maths based on my assumption Codan’s FY23 profit will be c. $57 million, this would mean Codan will be down about $43 million compared to FY22. If we were to write off all the profits Codan made from metal detector sales in Africa last year completely, (c. $35 million), this would put Codan’s FY23 profit at $65 million. Something is not adding up here!

Codan says ROW sales are growing and margins in the Comms business is improving, so how can Codan’s profit fall by more than the profit Codan makes out of Minelab in Africa?

Is it possible that Codan has over-invested in Minelab inventory over the past 12 months in anticipation of increasing sales in Africa and it is now left with warehouses full of metal detectors? This would certainly explain why Codan’s profits and cash flows might be lower this year.

Significance of Artisanal Mining in Africa to Codan

“An artisanal miner or small-scale miner (ASM) is a subsistence miner who is not officially employed by a mining company but works independently, mining minerals using their own resources, usually by hand” (Wikipedia).

“There are four broad types of ASM: permanent artisanal mining, seasonal (annually migrating during idle agriculture periods), rush-type (massive migration, pulled often by commodity price jumps), and shock-push (poverty-drive, following conflict or natural disasters).”

Sudan is Codan’s single largest market in Africa and “artisanal gold mining is widespread across much of Sudan, employing more than two million people and producing about 80 percent of the gold extracted nationwide.” https://phys.org/news/2022-07-sudan-gold-wreaks-havoc-health.am

In 2021 Codan experienced a “COVID Gold Rush” as Africans out of work due to COVID rushed to the gold fields. The growth in Minelab sales during 2021 turned out to be unsustainable.

Russian Interference and Gold Plundering is Affecting Artisanal Mining

“One of the world’s least-developed countries, Sudan is a hotbed of illicit financial activity — Transparency International ranks it among the world’s 20 most corrupt countries. It is estimated that only a fifth of the country’s gold output passed through official channels, with the rest smuggled out of the country. In 2019 more than $4 billion of gold was unaccounted for.

In the new interim government, Hemeti is the second most powerful general after Abdel Fattah al Burhan, the country’s top military leader, who launched a coup to oust the civilian leader Abdalla Hamdok. After the recent coup (October 2021), it has been even easier “to smuggle gold to Dubai.”

https://www.mining.com/web/how-a-sanctioned-russian-company-gained-access-to-sudans-gold/

There are also allegations that Russians are smuggling gold bars from Sudan.

“Backed by the Kremlin, the shadowy network known as the Wagner Group is getting rich in Sudan while helping the military to crush a democracy movement.

Wagner’s operations in Sudan began in 2017 after a meeting in the Russian coastal resort of Sochi.

After nearly three decades of autocratic rule, President Omar Hassan al-Bashir of Sudan was losing his grip on power. At a meeting with Mr. Putin in Sochi, he sought a new alliance, proposing Sudan as Russia’s “key to Africa” in return for help, according to the Kremlin’s transcript of their remarks.

Over the next 18 months, Meroe Gold imported 131 shipments into Sudan, Russian customs records show — mining and construction equipment, but also military trucks, amphibious vehicles and two transport helicopters. One of the helicopters was photographed a year later in Central African Republic, where Wagner fighters were protecting the country’s president, and where Mr. Prigozhin had acquired lucrative diamond mining concessions.

Gold production in Sudan soared after 2011, when South Sudan seceded and took with it most of its oil wealth, but only a handful of Sudanese have gotten rich. General Hamdan’s family dominates the gold trade, experts and Sudanese officials say, and about 70 percent of Sudan’s production is smuggled out, according to Central Bank of Sudan estimates obtained by The Times.

Most of it passes through the United Arab Emirates, the main hub for undeclared African gold. Western officials say that Russian-produced gold has likely been smuggled out this way, allowing producers to avoid government taxes and possibly even the share of the proceeds that is owed to the Sudanese government.

Several protests against Meroe Gold operations have erupted in mining areas. A Sudanese YouTube personality known only as “the fox” has attracted large audiences with videos that purport to lift the lid on Wagner’s activities. And pro-democracy demonstrators theorize that Moscow was behind last October’s military takeover of the Sudanese government.”

https://www.nytimes.com/2022/06/05/world/africa/wagner-russia-sudan-gold-putin.html

Wagner Group accused of attacks on artisanal mines

Wagner Group CAN massacre YouTube

“Russian mercenaries working for the Wagner Group, a private military company that has been linked to the Kremlin by western officials, have mounted a series of bloody attacks on artisanal mines in the lawless border zones between Sudan and Central African Republic (CAR) in an effort to plunder the region’s valuable gold trade, witnesses and experts have said.

Wagner has been active in a dozen countries across Africa, and has been repeatedly accused of human rights abuses on the continent. Western officials allege the Kremlin is using Wagner to advance Russian economic and political interests across Africa and elsewhere...”

“Unstable regimes in Africa have sought assistance from Wagner to prop up their governments, including in Libya, Mali and Sudan, according to the US.”

Artisanal Gold Miner Describes Attacks

“Artisanal gold miner Alnazir Mohamed said he was digging for gold when an attack helicopter swooped to the ground flanked by tanks. Soldiers who appeared to be foreign streamed into the mining site and opened fire.”

“They killed randomly and looted, taking everything including property, money and gold,” Mohamed, 30, said in an interview last month in Nyala, Sudan.

The mercenaries, working with the domestic army, killed at least 100 artisanal miners between March and June, according to a tally kept by local rebel leaders.

“Their forces scout gold-mining areas using drones,” said Enrica Picco, a senior analyst with the International Crisis Group who was previously a member of the UN panel of experts on the CAR and has been doing field research since Russian fighters arrived in the country. “Then they use helicopters to deploy soldiers who indiscriminately kill miners and rebels in control of the site, loot property and steal gold.” https://www.mining.com/web/russian-mercenaries-seek-gold-sow-chaos-in-car/

“There are regular reports of attackers arriving by helicopter, killing artisanal goldminers and rebels, taking everything they can and then leaving,” she told British newspaper The Guardian. “Sometimes they come back again a month or so later and do the same thing. It is nothing to do with securing a mining site.”

The Wagner Group’s presence in gold-mining areas has increased since governments around the world unleashed massive sanctions against Russia for its war in Ukraine.

https://adf-magazine.com/2022/07/wagner-group-terrorizing-sudanese-gold-miners/

What’s the Future For Codan in Africa?

Alf Lanniello said “While our sales into Africa are currently lower, I want to assure shareholders that management are working hard to rebuild and maximise our sales of gold detectors into this market.”

In reality, given the geopolitical circumstance, the instability of governments and the level of corruption, particularly in Sudan, Codan’s people will have little influence over artisanal gold mining activity.

Alf admitted Codan has “a lack of visibility into a number of the African markets”. I think Codan needs to invest more resources into on-ground intelligence in Africa to better understand what is driving and influencing artisanal gold mining activities across Africa. The level of artisanal gold mining activity directly impacts Minelab sales and profitability.

Rest of World (ROW)

Codan said “Rest of World (RoW) sales for the Minelab and Communications businesses, into markets such as North America, Europe, Lantin America and Asia Pacific represented over 70% of FY22 revenues.”

Metal detection (ROW)

“Encouragingly, Minelab’s rest of world sales – excluding Africa – has been a fantastic growth story, with sales growing at 14% CAGR from FY18 to FY22, despite the cessation of Russian sales. The breadth of products being sold (including gold, coin and treasure and land mine detectors) as well as growth in key geographic markets in North America, Central and Latin America, Australia, Europe and Asia means these sales are generally more predictable and stable compared to our African market.”

“Minelab has a strong track record of successfully entering new geographic markets and we are confident that our ongoing engineering capability and innovation will support the continued release of leading-edge products. Having not released a high-end coin and treasure detector for over 10 years, it is with much excitement that during FY23 Minelab will launch several new coin and treasure detectors.”

“Despite these headwinds our Rest of World metal detection business continues to perform well, maintaining gains made in FY22 and we expect the first half of FY23 to be in line with the prior year after normalising for the ceased Russian market.”

Communications

Codan said “there will be a particular focus on increasing the profitability of our Communications business.”

“The acquisitions of DTC and Zetron have diversified Codan’s sales with the Communications division increasing from 23% to 48% of group sales in FY22.”

“However, as the Communications business continues to grow their sales, we would expect segment profit margins achieved in FY22 of 21% to increase, as the business will benefit from operating leverage. Our longer-term objective is for the Communications segment profit margin to reach 30%. This may take some time; however, we are confident in both the near and long-term growth prospects of our Communications division.”

“We believe our Communications businesses represent a significant future growth engine for Codan and expect our results for the first half of FY23 to have sales in the range of $123 to 135 million, which represents a 5 to 15% increase on the prior corresponding period. With respect to the large communications project announced at this time last year, there is currently some uncertainty relating to the timing of shipments. Orders remain in place and we are confident that all product will ship over time.”

“With the growth in sales, we are expecting to lift the segment profit margin for our Communications business from 21% in FY22 to 25% over FY23, as the business will benefit from operating leverage.”

First half FY23 outlook:

• A number of macroeconomic and geopolitical factors have significantly impacted Minelab African sales;

• Minelab’s Rest of the World sales are proving resilient and in line with a normalised FY22; lastly

• Communications will deliver strong growth in both sales and segment profit.

Divisional profit forecasts to December 2022 were considered in detail by the Board late yesterday. We are expecting a first half net profit after tax in the range of $25 to $30 million, given the uncertainty relating to the timing of shipments on our large communications project as well as the lack of visibility in a number of African markets, we believe this is an appropriate range.

The results for the second half of FY22 are expected to be stronger than the first half.

Cash generation in the first half of FY23 has been impacted as our sales into Africa have reduced. Sales into Africa are generally made on a cash before delivery basis. We also have a major $5 million capital expenditure program underway to relocate our Zetron businesses which will minimise future rental costs. We expect to close the first half of FY23 with net debt in the order of $70 million. Over the second half of FY23 we expect to return to the positive cash generation that Codan is known for and therefore drive down our net debt position.

Sum up and valuation

Apart from the African Minelab operations, the rest of Codan’s business is performing well and growing. However, Africa made up about 35% of Codan’s profits during FY22 (on my calculations. I need to confirm this with Codan).

The geopolitical issues in Africa are dire, with alleged Russian interference disrupting governments and artisanal gold mining in a number of already destabilised parts of Africa.

Russia is allegedly plundering gold to fund its war efforts with Ukraine, and with increased global sanctions, this is making the situation even worse for artisanal gold miners across Africa’s gold rich nations. It could take years for the situation to improve.

If we were to write off Codan’s African segment for the medium term, is there enough value left in the rest of Codan’s business to support the share price today and over the next few years. Africa still has plenty of gold and the majority of it will be mined by artisanal gold miners, but it might take years for this to return to the glory days.

Last year (FY22) Codan’s earnings were $100 million. If we were to write off all the African profits, say $35 million, that leaves us with a profit of $65 million. This could be lower this year (say $57 million) due to Codan over spending on inventory for a market that has all but evaporated. This is the pain you get when you “lack visibility” into one of your most important markets.

As a shareholder, and for the sake of knowing what to do with Codan, I’m going to attempt to value the business based on a number of assumptions.

I will assume the African business will cost Codan cash flow and profits this year and consolidated earnings will be c $57 million. FY24 Codan’s earnings will be closer to $65 million assuming there is zero profit from Africa (that’s pretty harsh I know).

I will assume the rest of the business will comtinue to grow from FY23 with a return on shareholder equity of 18% (down from 30% FY22) with 50% of the earnings reinvested into growth. That puts earnings from FY24 growing at 9% per year.

Using McNivan’s formula and a required return of 10% per year, I get a valuation of $5.90 ( without the African gold detector business)

Codan is currently trading around $4.00 and it seems to me the market has already written off the African gold detector business, plus some more.

It looks like the market has overreacted. However, due to the ‘lack of visibility’ shareholders have into the contribution of profits from Codan’s various business segments, it is difficult to make a well informed valuation. For me it’s a hold.

Will Codan shine again? Who knows?

I’m a newcomer to Codan, having bought my first shares in January this year. However, for those who have held Codan for more than 8 years, you might be feeling an uncanny sense of déjà vu right now. I found this article from June 2014 (copied below). As you read through this article you could be forgiven for thinking you were in an 8 year time warp. The question on my lips now is…will history continue to repeat itself over the years ahead?

Following an 80% fall from its peak share price in April 2014, it took 5 years for Codan to reach its former peak, and then 2 years on from that the share price was more than 5 times higher than it’s former peak. I’d be happy with that! :)

Value Stock - Spotlight on Codan (1 June 2014)

“Talk about being in the wrong place at the wrong time. Codan has been smashed as a falling gold price and civil unrest in parts of Africa cut demand for its metal detectors, and as the fading resources investment boom weighed on its mining technology division.

Codan shares more than tripled between mid-2011 and early 2013 as the market latched on to its fast earnings growth and stellar prospects in emerging markets. But after peaking at $3.95 in March last year, the company has slumped to 68 cents in a brutal fall from grace.

Value investors could give up on Codan. Its earnings can be volatile, sales are heavily skewed towards Africa and other frontier economies, and much depends on the hard-to-predict gold price and rate of gold discoveries. Also, it is hard to define Codan’s sustainable competitive advantage.

Clearly, Codan is not for the risk-averse or those with a short investment horizon. No business that earns half its sales from the African mining industry, and operates in political hotspots such as the Sudan, can provide the consistent, recurring revenue that characterises exceptional companies.

Even so, the market habitually gets too bullish on small-cap companies at the top, and too bearish at the bottom. That could be the case with Codan today, making it a stock for portfolio watchlists of speculators, as its share price forms a base.

To recap, Codan has three core divisions. MineLab is the most important, accounting for 54 per cent of sales in the first half of FY14. It sells metal detectors to small-scale artisanal miners who search for gold as their primary source of income, and to gold hobbyists and prospectors. Governments and non-government organisations also use its detectors to find land mines and other unexploded shells.

The radio communications business contributed 39 per cent of sales for the half. Government and military customers use Codan’s high-frequency radios for long-range communications, and companies and consumers buy land mobile radios for short to medium-range communications.

The Minetec division, which contributed 4 per cent of revenue, provides a range of safety products, asset tracking and communication infrastructure to underground mines. Codan divested its underperforming satellite business in 2012 to focus on these three divisions.

Its strategy, for the most part, had paid off. Codan’s return on equity (ROE) soared from 20 per cent in FY09 to 41 per cent in FY13, thanks to stunning growth in net profit. Net debt had steadily decreased and there was plenty of cash on the balance sheet.

In some ways, Codan was among the more impressive Australian small-cap companies. It had become genuinely global and built a strong on-the-ground presence in difficult frontier markets. Its sales in the developing world have exceeded $100 million in each of the past five years.

Codan still looks well placed to benefit from long-term growth in emerging markets, and as the resource sector eventually recovers. Up to 13 million people worldwide are thought to participate in small-scale gold mining, and many still use traditional methods rather than high-tech metal detectors.

Frontier countries, by their nature, are unpredictable in the short term. Codan’s net profit after tax slumped to $4.8 million for the December 2013 half, from $26.5 million a year earlier. Falling demand for its metal detectors in the latter stages of FY13 spilled over into the first half of FY14.

Civil unrest in the Sudan, extreme weather conditions, counterfeiting of metal detectors, and general political instability in West Africa led to a 64 per cent fall in revenue in the metal-detection division to $32.9 million. Gold-detector sales fell an astonishing 80 per cent on a year earlier.

Lower profit margins compounded the sales woes. A strong second-hand market in metal detectors has emerged in Codan’s key African markets, reducing its ability to sell higher-margin new detectors. And it was caught holding far too much inventory, after not having had enough during its boom years.

Codan’s other divisions also slowed. Revenue in the radio communications business was to $23.6 million in the December half, from $32.3 million a year earlier. Sales of land mobile radio products, predominantly in the United States, were hurt by cuts in US Government spending.

Sales in the MineTec division slumped from $9.4 million to $2.4 million, year on year, as Codan transitioned from supplying traditional mining services to commercialising its own technology. On any measure, Codan’s earnings woes – flagged to the market in December – disappointed.

However investors cut it, the result was a bloodbath.

Codan has responded with $10 million in annual cost cuts, and other volume-related expense reductions. The big question is how much lasting damage has been done, and how quickly it can get its ROE – 7.8 per cent in the first half of FY14 – back to previous levels.

The company’s balance sheet has been weakened: total debt rose from $33.8 million in FY13 to $71 million in the latest half. Excluding cash and short-term investments, the net debt-to-equity ratio is 54 per cent – manageable, although heading towards higher risk.

Codan had $6.4 million in cash at December 31, 2013, from $8.6 million at the end of FY13. Although the $64 million in net borrowings are within its bank facility of $85 million, Codan arguably does not have much scope to withstand continued earnings shocks without additional debt or equity capital raisings. Gearing at 35 per cent in the first half of FY14 is moderate risk.

It is not all bad news. Codan has several new metal detectors due for release in FY14 and FY15, and says its radio communications division entered the second half of FY14 with its strongest order book in several years.

The MineTec business won an important tender to install its mine simulation software, which will provide proof of concept and a platform for further sales. Codan says MineTec is now successfully commercialising its technology in a highly competitive global industry.

Even so, Codan provided muted guidance in the outlook statement in its latest profit report: “Although sales have been softer during the past nine months, our baseline metal-detection business remains strong, and we remain confident of future growth as we continue to develop new market-leading products and extend our global reach, all supplemented by the upside of future gold rushes.”

Prospective investors might have hoped for more specific guidance on how Codan intends to arrest its earnings decline. In fairness, current volatility in the company’s core markets must make it hard to give more precise guidance.

Prospective investors need a high margin of safety to buy Codan, such is the risk of forecasting error (with only three forecasts in the consensus) and the potential for continued earnings volatility. None of its recent problems, notably civil unrest in parts of Africa, look like reversing anytime soon.

Lower expenditure by mining companies and government cutbacks, which affect the radio division, will linger for some time. The surprise could be continued gains in the gold price, which encourages more prospecting and leads to more gold discoveries, which in turn spurs metal-detector demand. But pinning ones hopes to the gold price is risky.

A better strategy is to watch and wait. It is hard to find a re-rating catalyst for Codan between now and the full-year result in August, and the first downgrade is rarely the last for micro-cap companies. A weaker gold price is a threat for its gold-detector sales.

More evidence is needed that Codan is arresting its sales decline, boosting ROE, and restoring market credibility. It said the ‘challenges presented by some of its markets makes it too difficult provide guidance at this time”.

Chartist will keep a close watch on the price action as Codan consolidates between 60-70 cents a share,

– Tony Featherstone is a former managing editor of BRW and Shares magazines. This column does not imply stock recommendations. Readers should do further research of their own or talk to their adviser before acting on themes in this article. All prices and analysis at May 28, 2014.”

…and how did the share price fair over the following 8 years?

I don’t disagree with @Jimmy. I don’t expect to see Codan surprise to the upside in 1H 2023 simply because of the gold price. I don’t think I’m the only one thinking this, however I think much of the short-term outlook is already priced in.

The 2 year gold chart looks awful, similar to Codan’s share price. This will be weighing heavily on Minelab sales this half.

https://goldprice.org/gold-price-history.html

To be buying Codan now, you have to believe that the gold price will turn around over the next 6 months. I believe it will, and I am still slowly adding Codan shares with a view to hold for the long-term, for at least 2-3 years.

For the gold price to improve the US dollar will need to come off it’s highs as there is an inverse relationship between the two. A US recession might do this? So is it possible Codan could be a hedge against a US recession?

In the mean time, I think the communications business will continue to grow and the dividends will be enough to pay its way until the gold price cycle improves. Unless of course, gold as an appreciating asset becomes a thing of the past? Anything is possible.

Consolidated Return on Equity

Up until FY21 Codan steadily improved ROE, reaching a peak of 32.4% in FY21. For FY21 Commsec data shows Codan’s ROE as 27.4%. In the FY22 Presentation Codan reported ROE as 30%. Why are the reported ROE values different?

The difference comes down to how the ROE values were calculated. Codan has calculated ROE as the NPAT/Average Shareholder Equity (FY22). Average Shareholder Equity is the average of the equity at the beginning and the end of the financial year.

Commsec calculate ROE as NPAT/Ending Shareholder Equity (FY22). I note this is also how ROE is calculated on Simply Wall Street data. This method of calculating ROE generally results in a lower value (unless equity actually declines). Which method is correct?

I don’t know if there is an accounting standard for calculating ROE, but in my opinion if ROE is being used for valuation purposes it should be calculated as NPAT/ Equity at beginning of the financial year. This would be inline with how you would calculate the yield on a term deposit.

This is not the point of this straw. I thought it was worth mentioning given the discrepancy in reported ROE values.

Source: Commsec, 27 September 2022

Codan’s Segment Performance

Codan business consists of two key segments, Metal Detection and Communications. Codan’s overall performance over the past 5 years has been very strong. Codan has grown earnings by over 22% per year, Gross Margins are over 50%, Net Profit Margins are c. 20%, ROE has been around 30% and net debt on equity has been less than 8%.

Over the past 5 years the revenue contribution by the communications segment has grown substantially, from 26% to 48% (See chart below).

Source: Codan’s FY22 Presentation

Codan management sees increasing revenue from the communications segment as a good thing as it helps to diversify the business and increases resilience. However, what impact is the communications segment having on the overall performance of the business?

Segment Net Profit Margins

The chart below shows that the communications segment is contributing 29% of the net profit while the metal detection segment is contributing 71% of the net profit. Therefore net profit margins for the two segments are, Metal Detection 27% and Communications 12% (See the table below for segment revenues). Unless communication margins improve there will be some dilution of net Profit margins as the communications segment grows.

Segment Return on Assets

Referring to the table above, the communications segment generated $29.2M of profit from $351.4M in assets (ROA 8.3%), while the metal detection segment generated $70.9M of profit from $199.6M in assets (ROA 35.5%). The communication segment is significantly more asset heavy generating 29% of the net profits from 64% of the total assets. Metal Detection is generating 71% of the net profits from 35% of the total assets. As the communications segment grows Codan will become more asset heavy.

Segment Return on Equity

I found segment ROE much more difficult to estimate. I couldn’t find equity values for each segment in the FY22 reports so I have assumed that the equity for each segment was proportionate to the assets (this assumption might be flawed).

If this assumption is correct the Communications Segment has a ROE of 13.3%, while the Metal Detection has a ROE of 60% (See markups on the table above). I have a hunch the Metal Detection ROE has been overstated here.

The impact of the growing communications segment on consolidated ROE will become evident over the next few years. It will be important to keep an eye on the ROE trend from here.

Performance Dilution

It would appear that while the communications segment is helping to diversify the business, it is also having the effect of diluting the high performance metrics typical of the metal detection segment. As the communications segment grows to become a larger part of the consolidated revenue, Codan’s ROE is likely to decline. Unfortunately this will also have an impact the valuation.

Revised Valuation

I have reworked my valuation of Codan based on a lower ROE of 23% and earnings growth of 6.5% per year over the next 3 years. Using McNiven’s StockVal formula and my required return of 10%, my current valuation for Codan is $8.70.

Disc: Held IRL (10%) and SM (12%).

Concerned about the possibility of Minelab losing its moat as a world leader in gold detectors, I decided to do some extensive research! Since I don’t have a talking mirror like the Wicked Witch in the fairy tale ‘Snow White’, I decided to ask Google.

‘Hey Google, Google, who makes the best gold detector in the world?’

Google replied ‘I found five on the website popsci.com. The best overall was Minelab Equinox…blah blah.’ (Try this yourself, it’s fun!).

That was enough for me. Who could argue against the wisdom of Google!

And like the Wicked Witch, I might just keep asking Google this same question each year until I find out that Minelab no longer makes the best gold detector in the world, at which point I will become absolutely furious and sell all my shares! :)

Seriously though, most of the reviews I found on the internet came up with Minelab detectors as #1

To put McNivens StockVal formula to the test, I thought it would be interesting to do a case study on one company using the formula to work out valuations over the past 8 years and compare these valuations with what actually happened to the share price. This should be a good evaluation of StockVal…right?

As you can imagine, this took a little while to do, but the task was made a lot easier by using a spreadsheet @PortfolioPlus prompted me to build recently.

Below is the comparison of the StockVal valuation for Codan (Orange) compared to the actual share price at the end of June each FY (blue line). The valuations were based on the ROE and Equity value for each FY, and using a Required Return (RR) of 10% and also factoring in the value of franking credits with the dividends. Interesting…Right?

As you can see, if you bought Codan after 2015 based on Codan trading at a discount to valuation for over 5 years, you would have done quite well. It’s worth noting that Codan is now trading at the biggest discount since 2017 based on the StockVal formula. Mind you, I have also pulled back the 2022 ROE of 30% to 26% for the current valuation of Codan. This is the only year I have changed the ROE used in the formula to that actually reported in the FY results. I find this a comparison very interesting and informative and gives me more confidence in using StockVal as a one of the tools for valuation of profitable businesses.

This chart is interesting also. The variables considered in the StockVal formula:

What a difference a conference call can make!

I chased the buy button up from $8.00 up and got left behind!

I haven’t revalued Codan yet but I think the long term outlook for the business is strong and if we ignore the exceptional result from metal detector sales achieved in FY21, the trend in the metal detector sales should continue into the future.

It’s also worth noting that there is strong growth in the communications business which now makes up 30% of the profits.

My gut feeling without looking at the details in the financial statement is that the business is still cheap!

In an article published last week ‘Top brokers name 3 ASX shares to buy next week’, James Mickleboro from The Motley Fool shared a note out of Macquarie.

“Macquarie analysts have retained their outperform rating and $11.60 price target on Codan. This follows the release of a trading update which revealed that it expects to report a record profit of $100 million in FY 2022. This was in line with the broker’s forecasts. Outside this, Macquarie feels that solid results from recently acquired businesses could boost confidence in future M&A optionality.”

My view

Generally I don’t take much notice of broker targets, but I am interested in their opinions.

I always worry about acquisitions especially when the only insight you get sometimes is, “the acquisition will be immediately earnings accretive”. Isn’t that what they all say?

Increasing earnings from a new business means very little unless it is put in context with the ROE for the new business. Adding a business with lower ROE can dilute the overall performance of the combined business.

In Codan’s case there is already evidence their acquisitions have at least maintained the ROE in the combined business. Using Codan’s FY22 earnings guidance of $100 million, and shareholder’s equity of $304 million, ROE of 33% is a slight improvement on last year’s 32.4%. What is more important is the trend! While ROE continues to improve at already high levels, I’m sticking around for the future growth Codan has in the pipeline.

Source: Commsec, 30/05/2022

My previous valuation on 29 March was $10.00. This was based on McNiven’s StockVal formula and is lower than most other valuations I have seen. This is because it is not a target value for Codan. This is the price you can pay for Codan now and expect a 10% return going forward (and this does not include franking credits on the 3.8% dividend). I used an ROE of 30% in my valuation. Given the FY22 guidance and ROE of 33% this looks reasonably conservative.

Disc: Held IRL and SM.

This morning Codan released its half year report, ASX 1H22 Announcement

At first the market seemed excited by the news with the share price opening up at $8.95 before reaching $9.05, then as investors digested the news the share price fell as low as $8.21 mid-morning. At time of writing the share price was $8.61.

I thought the result was good overall, particularly in respect to the company’s Highlights:

• Highest half-year profit in the company’s history

• More balanced, diversified and stable revenues across the Codan group

• DTC secured the largest contract award in the company’s history

• Recent acquisitions, DTC and Zetron both tracking ahead of first year profit targets

• Communications orderbook of $163 million, $71 million expected to ship H2 FY22

• Excellent results from Minelab given geo-political disruptions and a return to more normal levels of demand after the Covid impacted FY21

• The conscious decision to invest in increased levels of inventory across all business units places the group in a strong position as we enter the second half of FY22

• Net profit after tax of $50.1 million, a 21% increase

• Group sales of $257 million, a 32% increase against FY21 record first half

• Interim dividend of 13.0 cents, fully franked, a 24% increase

• Earnings per share of 27.6 cents, up 21%

I think there are a number of things the market didn’t like about the news, including:

- increased Inventory

- Cashflow negative

- Detector sales declined compared to 2H21

- Debt increased

- No guidance

Inventory

Codan said that ‘In early calendar 2021, we took the conscious decision to invest in production capacity and inventory across all business units. This has enabled us to maintain supply to our customers and position ourselves to satisfy future demand. In the case of Minelab, our investment in additional inventory has had two key benefits. We reduced freight costs (as we were able to freight a proportion of our products by sea rather than air) and most importantly, the additional inventory has mitigated the supply chain risks from the current global shortage of electronic components.

This build-up of inventory over the first half has impacted cash generation. As supply chains normalise and component availability improves, we will manage our inventory levels down. We believe the investment in inventory places the group in a strong position as we enter the second half of FY22.’

Cash Flow

Codan said they had made a conscious decision to increase inventory levels across the business. This had an impact on cash flows. In addition, they entered FY22 with negative working capital due to prepayments from a number of large customers last year to secure supply. These factors, coupled with a near record sales month in December 2021 and positioning DTC and Zetron for growth, meant that Codan invested an additional $65 million in working capital in the first half. This will gradually normalise over the next 6 months and positive cash flows will follow. Net debt dropped from $48 million to $38 million in January 2022.

Detector Sales

First half metal detection sales over the last 3 years have been FY20 $100 million, FY21 $155 million (+55%) and FY22 $138 million.

Debt on Equity

Total debt at 31 December 2021 more than doubled from $24 million to $58.4 million. However equity also increased from $303.6 million to $331 million. Debt on equity has increased from 7.9% to approx 17.6%.

Guidance

Codan did not provide guidance due to a number of positive and negative factors that are relevant when considering the outlook for FY22:

• The successful uptake of GPX6000® gold detectors into the developing world

• Resolution of the on-going civil unrest in Sudan

• The extent to which DTC and Zetron will exceed their initial full year profit targets

• The challenges that Covid and variants continue to pose

The Board is not in a position to provide full year profit guidance at this point however, we will continue to keep shareholders updated as the year progresses.

My Take

It is not good news that Codan had negative cashflow for the half, detector sales fell compared to last half, debt increased and there was no guidance for FY22. However, I think FY22 earnings will exceed FY21 and Codan will be back to positive cash flows next half.

I am retaining my valuation of $10.70 for Codan and have been adding to my IRL portfolio today ahead of the 13c per share fully franked dividend.